01 January 2021

By Maynard Paton

Happy New Year!

I trust you enjoyed the festive break and are now ready to battle the market for another twelve months!

This 4,631-word post provides a ‘year in review’ of my current portfolio holdings. I recap how each business performed during 2020 as well as provide a few remarks about valuation.

These reviews are very useful to write — not least because they help ensure I am still invested for the right reasons! Any upsets I will suffer during 2021 will most likely be caused by the shares I already own rather than any new shares I will buy.

I undertook the same annual review at the start of 2015, 2016, 2017, 2018 and 2019.

My portfolio gained 16.9% during 2020. This blog post explains that performance in more detail and clarifies how my portfolio starts 2021.

I have covered each of my holdings below in order of size within my portfolio.

I have accompanied each review with a SharePad chart to show how each company has progressed over the longer term. The charts display the share price, earnings per share (or in one case, net asset value per share) and dividend per share.

Of course my calculations, logic, assumptions and charts may have little bearing on the future… so please do your own research!

Contents

- Tristel

- Bioventix

- Mountview Estates

- System1

- S & U

- FW Thorpe

- City of London Investment

- M Winkworth

- Mincon

- Andrews Sykes

- Tasty

- Daejan

- Summary

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, Tasty, FW Thorpe, Tristel and M Winkworth. This blog post contains SharePad affiliate links.

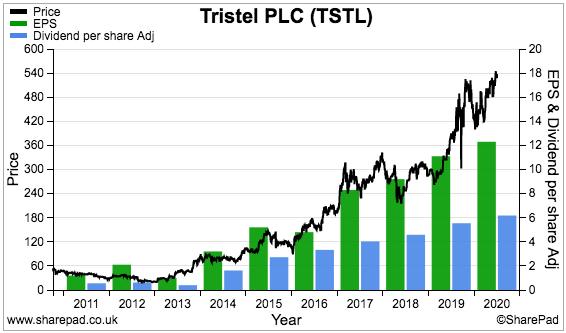

1) Tristel (TSTL), price: 524p, market cap: £244m

TSTL reached a milestone for my portfolio during 2020 — the share became my first 10-bagger after 25-plus years of investing.

I bought TSTL at an average of 46p during 2013 and 2014, and last year the shares gained a useful 38% to trade beyond my 460p landmark.

I must confess I sold 75% of this holding at various occasions (and for various reasons) during 2014, 2015, 2016 and 2017 at 79p, 100p, 123p and 289p. But I have kept the faith during the last three years, and I am likely to refrain from top-slicing during 2021 as well.

TSTL was a pandemic beneficiary last year. Extra orders for the group’s hospital disinfectants were even disclosed before the lockdown began within February’s half-year results.

October’s preliminary statement confirmed annual revenue and profit had climbed 21% and 26% respectively. Progress was perhaps not as spectacular as some had expected, but the figures set new records for the seventh consecutive year.

The results unveiled a 22% operating margin and a 20% return on equity — attractive ratios underpinned by a ‘moat’ based upon extensive patents, scientific testimonies and manufacturer approvals. The balance sheet has commendably remained cash rich and debt free.

Overseas income currently represents 60% of sales, with 35% H2 international growth buoyed in part by new disinfection rules in France. The product-approval process within the United States continues to be protracted, but advances could be forthcoming after last month’s AGM referred to “very encouraging progress”.

My October sums suggested the shares were priced at an elevated 39x earnings, which seems understandable given Covid-19 may have created an irreversible trend of hospitals enhancing their disinfection regimes.

TSTL’s directors do like their options, which agitates some shareholders but does not bother me so much (as long as the option plans and trading updates are disclosed properly). Corporate-governance detectives may have already spotted the (very) small print within the 2019 annual report that revealed the chief executive and finance director are now married (point 4).

My TSTL buy report | All my TSTL posts

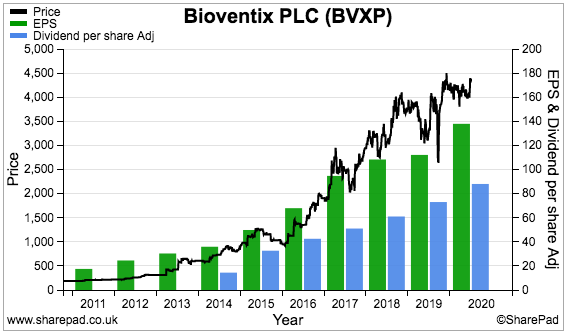

2) Bioventix (BVXP), £43.20, £225m

BVXP remained my second largest holding last year following a welcome 32% share-price gain. I bought BVXP during 2016 at £11 and the price has since almost quadrupled. I have never top-sliced this position and I don’t expect to top-slice during 2021.

I had believed BVXP would be ‘pandemic proof’ when the antibody specialist said first-half profit had jumped 26% and the second half ought to witness “further progress”.

But the subsequent annual figures implied routine blood-testing numbers had fallen 15-20% during April, May and June, which led to lower antibody royalties and underlying H2 profit gaining only 4%.

Mind you, the 2020 figures were BVXP’s best ever, and extended the group’s run of substantial yearly growth to ten years. The accounts continue to be among the classiest in the market, not least because of their terrific 79% operating margin and wonderful 62% return on equity.

The cash continues to mount up, and shareholders were rewarded during 2020 with a 21% dividend lift and a 53p per share special payout. A one-off dividend has now been declared for each of the last five years.

Pandemic blood-test numbers aside, 2021 attention will be directed towards the company’s troponin and vitamin D antibodies. Management has implied troponin sales might quadruple during the next two years to become 12% of group revenue, and replace the income that will be lost from an expiring product.

Vitamin D meanwhile supports 47% of revenue, and growth last year reduced from 20% to 10%. After years of management false alarms, demand for vitamin D might actually now be “plateauing”.

The 32x near-term P/E reflects the group’s exceptional economics and the general predictability of antibody usage for blood tests. Once in general use, diagnostic antibodies tend not to face much competition or disruption.

I have my fingers crossed that 2021 sees troponin sales take off, vitamin D income not stagnate and another special dividend declared.

My BVXP buy report | All my BVXP posts

3) Mountview Estates (MTVW), £124, £483m

I have mixed feelings about MTVW.

True, the regulated-tenancy landlord has coped well with the pandemic. Despite “procedural delays” putting property sales on hold for up to six weeks, net asset value (NAV) continued to inch higher while the dividend was again maintained. Management even implied the (virtual) auction rooms could now provide “exceptional opportunities” within the housing market.

Yet MTVW could do so much more to explain its attractions to investors.

In particular, the directors refuse to undertake another formal valuation of the group’s property estate. An initial valuation was conducted during 2014 and calculated the estate’s market value to be more than twice its reported book value. Other quoted companies with similar properties undertake such valuations every year.

Ongoing family disputes do not help either. The chief executive and various relations continue to control 51% of this business, while the chief exec’s sister and various other relations own 24%. Communication between both factions seemed to break down completely last year, with significant protest votes recorded for the fourth consecutive AGM.

MTVW therefore offers a degree of ‘fiefdom’ risk, but the financial history is actually quite reliable. Since the current chief exec took charge during 1990, NAV has rallied 17-fold (+10% per annum average) while the dividend has jumped 35-fold (13% per annum average).

I am hopeful for a favourable 2021. November’s interims intriguingly disclosed lofty margins from property sales, which may be just a one-off or maybe the start of permanently higher profits. MTVW’s tight-lipped board naturally did not explain what had happened.

Any lifting of previous Brexit “uncertainties” may help this year, too.

The higher margins suggest MTVW’s NAV could be up to £225 per share should all of the group’s properties lose their regulated-tenancy status and are then sold. That estimate compares to a £124 share price.

I first bought MTVW shares during 2011 at £42. I then topped-up at £98 during 2018 and 2019, and have yet to top-slice. I do not expect to be selling this year.

My MTVW buy report | All my MTVW posts

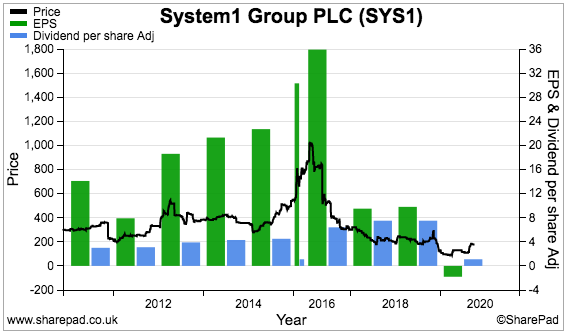

4) System1 (SYS1), 170p, £22m

SYS1 was my big investment idea of 2020 — I increased my holding by 75% at 251p during Q1 and then by a further 225% at 173p during Q4. This time last year SYS1 was my second smallest position and today it is my fourth largest.

My purchases were prompted by SYS1’s service agreement with ITV, which I am convinced is a landmark event for shareholders. The arrangement validates SYS1’s advert-testing work, which for the last few years has struggled as the business transitions from offering advert consultancy to supplying advert data.

To emphasise the hole SYS1 had dug itself into, the 2020 results admitted £5m had been spent on a new ad-testing website that had earned total revenue of only £56k.

November’s interims revealed a remarkable performance — with a pandemic-blighted Q1 loss suddenly transforming into a worthwhile Q2 profit. UK revenue actually improved during the half, an achievement I am sure relates to the ITV arrangement given the general Covid hit to advertising.

True, November’s interims kept formal guidance suspended and the dividend at zero. They also disclosed the receipt of US government Covid subsidies. But the books carried net cash, the Q2 margin looked useful at 16% while the presentation PDF boasted of adidas becoming a client. SYS1’s evangelical boss/23% shareholder is probably keen to see his business recover, too.

Wishful thinking perhaps, but SYS1 offers vague similarities with TSTL back in 2013 — a company with a leading niche product, but has suffered a rough time and the market cap has been left unloved at a possible 8x multiple. I reckon of all the shares I own, SYS1 has the greatest chance of significant returns during the years ahead.

I should add that I bought SYS1 at 325p during 2016 and at 238p during 2018 — just before the company went all in on that aforementioned £5m ad-test website. This year’s purchases take my average entry price to 200p and I have never sold.

My SYS1 buy report | All my SYS1 posts

Enjoy my blog posts through an occasional email newsletter. Click here for details.

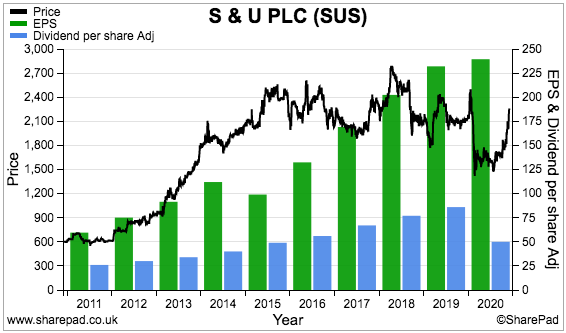

5) S & U (SUS), £22.80, £277m

SUS is a fine example of how owner-friendly businesses can survive trouble when the unexpected arrives.

The pandemic could have landed this motor-finance lender into all sorts of difficulties, and I was rather worried when the March lockdown commenced. Would the group’s ‘non-prime’ customers ever repay their loans?

Amazingly enough, collections have continued and were last running at 87% of due versus a comparable 94% for 2019. Not a bad achievement, especially after the FCA allowed six-month repayment holidays. SUS claimed these holidays were enjoyed by many customers that were not financially affected by the pandemic.

September’s interims disclosed a £14m one-off Covid write-off, which represented a very acceptable 5% of all outstanding car loans pre-pandemic. The statement also conveyed a 35% dividend reduction. Not great, but not as terrible as I had once feared.

Making the difference has been SUS’s veteran family directors and their “steady, sustainable” approach to long-term growth. With a £100m-plus shareholding at stake, the board has consistently mitigated the downside by keeping loan quality high and balance-sheet gearing under control.

Assuming one day the pandemic recedes, I am hopeful of a full earnings recovery. S&U prospered after the banking crash as competitors failed and customer quality improved, and recent board comments again point to struggling rivals and higher credit standards among new borrowers. Upcoming affinity partnerships with ‘prime’ lenders seem promising, too.

Near-term profit forecasts for SUS remain complete guesswork, but a return one day to 2019 earnings and the previous £26 share price provides a good baseline to work from.

Last year I felt £17 offered the prospect of double-digit annual returns and I increased my holding by 20%. I may buy more during 2021 should the share price weaken on further Covid worries.

I first bought SUS during 2017 at £21 and doubled up during 2019 at £19. I have yet to sell.

My SUS buy report | All my SUS posts

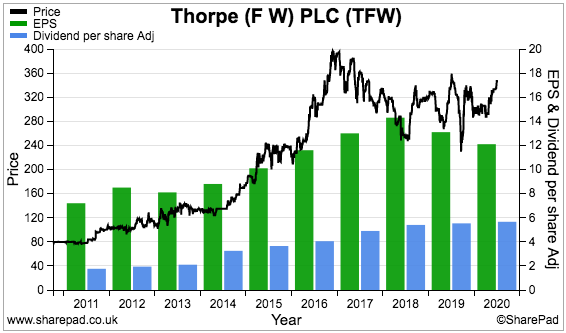

6) FW Thorpe (TFW), 341p, £397m

TFW is another pandemic survivor that owes its resilient 2020 to conservative management decisions.

For years this lighting business has carried significant cash balances, with the pre-lockdown position showing cash at a mighty £52m and debt at zero. The executives never really explained why such a huge bank balance was required… but now we all know.

Despite the Covid disruption and H2 profit sliding 17%, TFW’s cash reserves allowed a 2% dividend lift to extend the run of consecutive annual advances to 18. TFW commendably did not rely on government handouts, but instead self-funded its staff furlough payments.

Similar to SUS, resilient results during times of worry are very possible when the board has £100m-plus riding on the share price.

While coping well with the 2020 lockdown, TFW could find this year a different story. Director remarks concerning a “global recession” and a “downturn in orders” seem likely to herald a difficult 2021. The slowing rate of LED adoption is another drawback raised by management.

TFW’s headline numbers obscured two encouraging developments.

First, TFW’s Dutch divisions — which represent about a quarter of the group — enjoyed much better lockdowns than their UK equivalents and could shore up near-term progress.

Second, longer-term excitement is emerging through SmartScan — a lighting-control system that has witnessed sales surge from zero to 23% of total group revenue within just four years.

SmartScan was enhanced recently to include vehicle-activity and electricity-usage monitoring, which leads to imaginative scenarios of TFW becoming more of an IT/data/analytics business than a lighting manufacturer.

Maybe SmartScan explains why TFW’s shares trade at up to 25x earnings when profits next year are likely to be stagnant at best. Maybe the multiple also reflects the all-round dependability that the aforementioned cash hoard provides.

TFW is my longest-held share after I first bought during 2010 at 69p. I bought more during 2011 at 80p and during 2012 at 89p, but sold 25% of my holding at 234p during 2016 on (unfounded) valuation worries.

My TFW buy report | All my TFW posts

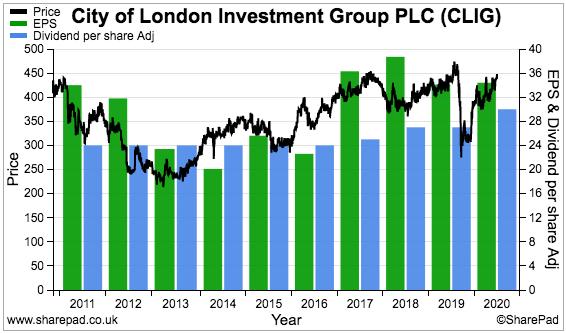

7) City of London Investment (CLIG), 431p, £218m

This time last year I remarked “new clients remain frustratingly elusive” at CLIG.

Well, this fund manager has done what many quoted companies do when new customers are hard to attract — acquire another business.

The £78m all-share merger with Karpus Management doubled CLIG’s size and brought with it new customers and an entry into managing fixed-income investments.

While significant mergers are always unnerving, the Karpus deal did not seem too awful. Both parties had similar investing approaches (through closed-end funds), the merger had been in the works for two years while the founder of Karpus (George Karpus) would end up with 31% of the larger group.

Providing some reassurance of a smooth integration, clients at Karpus first had to approve the deal and George Karpus even produced a thank-you video.

But will new clients remain frustratingly elusive now the merger has completed? Quite possibly. An October update projected funds under management advancing only 4% by June 2022.

Throw in five-year investment returns that averaged 4% per annum — versus 3% for the FTSE 100 — and CLIG’s shares trading at c10x earnings is quite understandable. Until the investment performance picks up and new clients climb aboard, the rating is likely to remain modest. The shares have traded at 10-12x earnings for the majority of the last ten years.

Patient shareholders are nevertheless rewarded with generous dividends. The October update implied a 30p per share payout from earnings of 45p per share that supports a possible 7% income. Even after this year’s market upheaval — with funds under management at one point down 27% — the payout was lifted a commendable 11%.

The dividend’s foundations lay within some robust accounts, with margins at a super 35%, return on equity at a splendid 40% and net cash/investments standing at a chunky £19m.

I look forward to collecting the 7% income during 2021. I invested at a 281p average between 2011 and 2013, and sold 42% of my holding during 2015 at 335p.

My CLIG buy report | All my CLIG posts

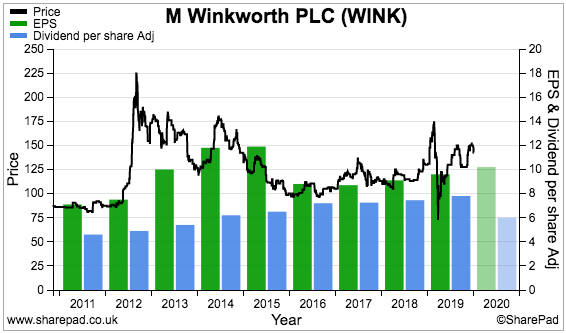

8) M Winkworth (WINK), 135p, £17m

Headlines such as A Quarter Of Agency Branches May Be Closed Forever reflected my worries of WINK becoming a “heavy casualty” of the lockdown.

But the estate-agency franchisor proved surprisingly resilient, and my gratitude once again goes to conservative family management that likes to operate with surplus cash and no debt.

Declaring a Q1 dividend down 12% — rather than down 100% as I had feared — was the critical announcement that brought relief to shareholders. September’s first-half results then showed a 20% profit drop, but the second-half omens were positive.

In particular, WINK referred to a “significant uplift in activity in the sales market” following temporary stamp-duty reductions and changing commuting patterns. And October’s Q3 dividend was cut by only 5%, which lent further credence to a recovery.

WINK’s performance versus Foxtons (FOXT), which claims to be “London’s leading agent”, has been super impressive. WINK has gained market share against FOXT every year since 2016, and my analysis suggests WINK’s self-employed franchisees handled the capital’s 2020 property market far better than FOXT’s conventional employees.

In fact, FOXT reported a loss for H1 2020 and had to raise emergency money from shareholders. In contrast, WINK reported an H1 profit through a robust 18% margin while a £4m cash/investment position prevented a rights issue.

WINK’s earnings have stalled during the last few years as its franchisees battled a London housing market subdued by Brexit. But I am hopeful WINK can gain further market share against FOXT (and others) to one day support a profit ‘breakout’ when the pandemic retreats.

These shares have been mostly range-bound between 100p and 140p since 2016. I bought initially at 90p during 2011 and then sold 70% of my holding during 2013 and 2014 at 173p. I then rebuilt my stake at an average 116p during 2016 and 2017. I could buy more during 2021 if the valuation makes sense.

In the meantime I will collect the quarterly dividends alongside the family management, which still owns a fraction above 50% of the business.

My WINK buy report | All my WINK posts

Reader offer: Claim one month of free SharePad data. Learn more. #ad

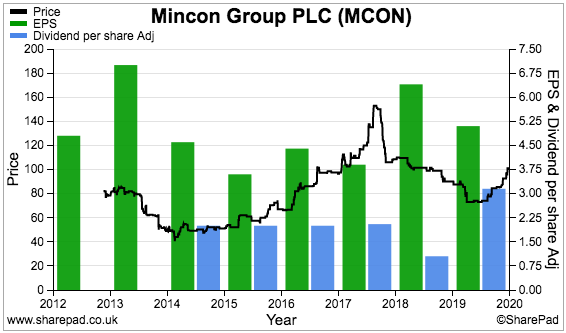

9) Mincon (MCON), 96p, £203m

MCON’s dividend appeared, disappeared and then re-appeared last year.

Annual results released in March were very muddled, with profit down 28% and all sorts of adjustments included. But the statement barely mentioned Covid-19, and the maintained payout implied the industrial drill manufacturer could resist the pandemic.

Then August’s first-half figures showed underlying profit rebounding 25%… but this time the dividend was suspended as management “adopted a prudent approach”.

Two months later, a Q3 update disclosed the dividend would return — with the suspended interim payout set to accompany the upcoming final payout. The dividend reinstatement was prompted by sales gaining 12% after “strong prices in precious metals and iron ore” prompted greater activity among the group’s mining customers.

MCON’s dividend disappearance is evidence of the company not yet exhibiting true ‘quality’ characteristics. MCON reckons its drills are top notch — the annual report refers to “engineering excellence” numerous times — but the accounts are not quite at the same standard.

The 2019 operating margin and return on equity were both lacklustre at below 10% following MCON’s efforts to broaden its customer base, develop “disruptive” new drills and sell direct rather than through distributors.

Huge investment in working capital — stock levels represent an enormous 41% of revenue — remains a significant accounting drawback and has left the balance sheet carrying net debt. Earn-out obligations following various bolt-on acquisitions can’t be ignored either.

If MCON’s drills and services really are as good as the company claims, the accounts should eventually improve. Until then MCON is stuck in a ‘moat-building’ phase that has persisted since I paid 45p for the shares during 2015.

As with many of my holdings, I am relying on veteran family management — which in MCON’s case controls 57% of the business — to eventually deliver lucrative returns. The shares presently trade at 18 times my August earnings guess, which suggests other investors also appreciate the long-term possibilities.

My MCON buy report | All my MCON posts

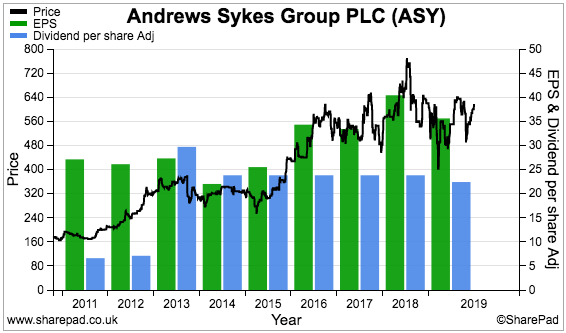

10) Andrews Sykes (ASY), 570p, £240m

ASY provided one of the most surprising RNSs of 2020. The equipment hire business said in July it would pay a special dividend of £10m — a sum equivalent to a normal year’s payout.

Special dividends are of course always welcome, especially during pandemics when many companies reduce or scrap their payouts.

But what made this special dividend so surprising was the small-print within the 2019 results — which claimed 50% of UK staff were furloughed and overseas employees had received state benefits.

Handing out extra cash to shareholders while receiving government subsidies does not feel right to me, and I like to think ASY has repaid the benefits received.

September’s first-half figures showed the special divvy was paid partly through bumper cash flow, which leads to questions about how this business was so cash generative when so many workers were furloughed.

H1 profit actually improved 2% despite the lockdown, so maybe ASY discovered how to operate more effectively with fewer employees. ASY’s blog showcases a busy year helping out hospitals, clinics and Covid test centres with heaters, chillers and air conditioners.

Similar to other portfolio holdings, ASY’s pandemic resilience is due partly to owner-management sustaining a cash-flush balance sheet. The children of the 100-year-old chairman (yes, he is 100 years old) control 86% of the business while net cash following the special dividend was £19m.

I bought ASY during 2013 at 233p and subsequent dividend payments now represent a super 85% of my purchase price. Assuming the ordinary dividend is maintained, another 18 months will see my entire investment recouped through payouts.

My October sums pointed to a possible P/E of 17, which I felt was not completely outrageous for a cash-rich and apparently pandemic-resilient business that delivers margins and returns on equity consistently greater than 20%.

ASY is another share I could buy during 2021 at the appropriate valuation. Note that the dominant shareholding of the chairman’s family creates a wide bid-offer spread.

My ASY buy report | All my ASY posts

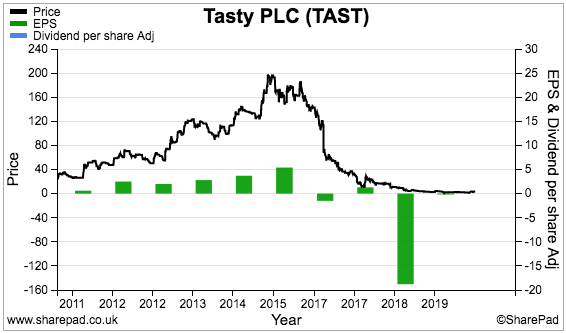

11) Tasty (TAST), 3p, £4m

A property disposal announced on the first trading day of 2020 probably saved my TAST investment.

The ailing restaurant chain raised £2m by selling a prime London site, which left the balance sheet clear of debt just in time for the pandemic and the closure of the entire sector.

I spent most of my time on TAST last year guessing when the company’s money would run out. I reckoned in July the cash would last until November. Partial re-openings, government aid and the apparent non-payment of any rent then extended my estimate to June 2021.

TAST’s shares held up remarkably well last year, which just goes to show how bad TAST had performed prior to the lockdown.

I have been questioning the group’s viability since 2017 after profits turned to losses and the shares crashed from 200p to 3p. Some may argue the lockdown closure was actually a blessing for TAST, as more money would have been lost by operating normally.

The pandemic certainly forced TAST to act and should allow a full estate re-jig. Jettisoning loss-making sites through a CVA is one option, and is becoming more likely given discussions with landlords about owed rents are taking longer than expected.

Survival hopes in the meantime rest upon a loan from Barclays, orders for takeaways and a successful vaccination programme. I trust this new option scheme implies a delisting is not imminent.

TAST proves that large family shareholdings do not always lead to great investments. The Kaye family owns 31% of this business and has built and sold successful restaurant chains before, but simply could not cope with much greater competition this time around.

I first bought TAST at 50p in 2011 and again at 98p in 2014. I sold 15% of my holding during 2016 at 179p — and of course regret not selling the rest. Instead I bought more at 45p during 2017 and even more during 2018 at 15p. Today I need a 12-fold recovery just to breakeven.

My TAST buy report | All my TAST posts

Sold shares

I exited just one share during 2020, which was certainly not planned or expected. This disposal was my 21st complete exit since 2004 and the 14th to score a profit.

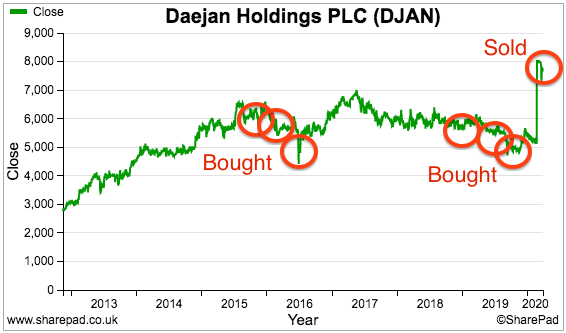

SOLD) Daejan (DJAN), £77, £1,255m

DJAN’s RNS on 21 February last year was among the most unexpected I can ever recall.

The commercial-property group had enjoyed a stock market quote since 1959… and suddenly announced it was going private. The controlling Freshwater family offered £80.50 a share to acquire the c20% free float — and that was that.

Over time DJAN had become a market relic. Diversity campaigners in particular had challenged DJAN’s male-only board, while management’s old-fashioned ways included leaving the previous chairman’s office untouched since 1980. The offer document referred to “distractions associated with being a listed company” and the executives just seemed to want a quieter life.

The business had nonetheless survived and prospered despite the quirky corporate governance. After the current chairman took charge 40 years ago, NAV had soared 87-fold (+12% average) while the dividend had advanced 29-fold (+9% average).

I was not entirely sure how DJAN would cope with the pandemic. Commercial property was going to struggle with offices, shops and restaurants lying empty, and waiting around for the deal to complete risked being stuffed through a force-majeure clause and a lower offer.

I exited at £77 in March, and to their credit the Freshwaters did pay the full £80.50 a share in May. Net asset value at the time was almost 50% greater at £120 a share, which finally proved this company was always something of a ‘value trap’.

I still made money though. I first bought Daejan in 2015 at £60, then during 2016 at £53, during 2018 at £57 and during 2019 at £53 to give an average purchase price of £54. I collected dividends of £3 a share along the way and enjoyed a 47% gain over a weighted-average holding period of approximately three years.

I have mixed feelings about the buyout. Yes, the offer bolstered my 2020 returns, but DJAN (at least pre-pandemic) was a reliable, lower-risk and no-aggro holding — characteristics that are always hard to find in the market.

My DJAN buy report | All my DJAN posts

Summary

Last year my portfolio reduced from 12 shares to 11, and my remaining companies generally offer the traits outlined in How I Invest:

- Capable management;

- Decent accounts;

- Respectable track records, and;

- Reasonable prospects.

I admit TAST no longer meets that criteria (if it ever did), but TAST’s shares have long since passed their sell-by date and a 1% position won’t do much harm even if the worst does happen.

The plan for 2021? I am hopeful my returns will improve through building further higher-conviction holdings. My portfolio has a 14% cash position to deploy, which could find its way into my mid-size investments such as SUS and WINK. My SharePad articles might of course identify some suitable alternatives.

I trust you found this annual review informative. I certainly found it useful to write.

Please click here to examine my portfolio’s 2020 performance in more detail.

Until next time, I wish you safe and healthy investing!

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Well done Maynard, thats a great performance overall for a horrible year!

As always thanks for sharing, very interesting.

best regards

David

Thanks David. Yes, not a bad performance all things considered!

Let’s hope 2021 is not quite so volatile.

Maynard

Thanks very much for sharing the review of your portfolio which I am sure is very helpful to many investors including me. Am I correct in assuming that you concentrate on smallcaps (all your holding are now below £500M market cap) or is it the case that you do screen larger companies as well, but do not find what you want? One interesting aspect of your portfolio is that by my reckoning, 7 of the 11 companies qualify for inheritance tax relief and, furthermore, the type of companies you select are the “steady-eddy”, “buy and hold” type of company which many people investing to minimise IHT liabilities seek out. I would therefore argue that your portfolio not only represents an attractive investment strategy, but also an effective approach to minimising IHT liability. Bearing in mind the high cost charged by some fund managers for running portfolios intended to minimise IHT, I think this is a valuable attribute of your portfolio.

All the best for a healthy 2021,

John Scrivens

Hi John

Yes, I tend to concentrate on small-caps as they are more likely to have the ‘owner-management’ that I prefer. Larger companies tend to have pro managers, who can come and go and not always have the same dedication to long-term shareholder returns. But I am not averse to investing in a larger company if everything stacks up. Smaller companies have other advantages, such as simpler accounts, greater access to management and less City attention that can create more mis-pricing opportunities.

I must admit I have never considered the IHT aspect to my shares. I started investing in my 20s and such matters were never at the forefront of my mind. I trust my beneficiaries will not need to look closer at the rules for some time though!

Best wishes for 2021,

Maynard

Hi Maynard – Very respectable return.Well done!

Have you run your slide rule over smj (J.Smart).

I`d very much appreciate your view.

All the best for 2021.

Giles.

Hi Giles,

Every share I have written about on this blog and for SharePad can be found through this helpful link: https://maynardpaton.com/companies-a-z/

And yes, I have written about J Smart — albeit in 2015:

https://maynardpaton.com/companies-a-z/#j-smart-co

https://maynardpaton.com/2015/07/10/j-smart-co-20-years-of-dividend-advances-but-still-not-for-me/

Not looked at it since, and not currently on the radar for a revisit.

Best wishes for 2021,

Maynard

I can’t see how you arrive at a figure for TFW – Fw Thorpe of £57mn net cash in the pre-lockdown period? I have only glanced at the end June finals and the December 19 interim b/s but I can’t get to your number even with arm twisting. I do see the company is well furnished with cash and near, though – and always worth remembering that cash balances tend to suppress RoE etc which I use a lot as with RoCE.

Thanks for the write-ups

Hi Stephen,

Very good spot! Figure should have been £52m as per the sums here. Article now corrected.

Maynard

Maynard, any reason that you do not own British American Tobacco?

Hi Mike

BATS does not really meet the criteria I set out in How I Invest.

Also, I spent a few weeks in hospital the other year in a respiratory ward and I saw first hand i) the long-term damage smoking can do and ii) how the NHS resources required to treat smoking-related illnesses can detract from the treatment of illnesses caused through no fault of the patient.

So not for me I am afraid.

Maynard

Congratulations on a profitable year for yourself. It must have taken some doing under the circumstances.

Well done and Happy New Year.

Thanks Charlie. Happy new year!

Maynard

“The 100-year-old chairman… controls 86% of the business… Note that the chairman’s dominant shareholding creates a wide bid-offer spread, and what happens after his family inherits his shares remains unknown.”

The centenarian chair of Andrews Sykes transferred his controlling ownership to his two sons back in 2008, as was RNS’d at the time:

https://www.investegate.co.uk/andrews-sykes-group/rns/director-pdmr-shareholding/200811041756494533H

Oh dear — I missed that completely. Thanks for informing me. Reassuring that the children are now the major shareholders. Article now updated.

Maynard

Great post, Maynard. And well done for strong performance both in absolute terms and relative (to FTSE-250, at least) terms.

Have you thought about which sectors to go hunting in post covid? Pubs/entertainment? Travel? Healthcare? Other?

Hi FvL,

Thanks for the message. I rule out a lot of companies due to their sector, and I have not really thought about the best sectors post-Covid. Pubs, travel etc were average sectors anyway pre-Covid, and while some winners may emerge from such industries post-Covid, I prefer to tread in the middle-ground — sectors not in the direct Covid firing line but not major beneficiaries either. I think the likes of WINK, ASY, SYS1, MCON, SUS fall into that category, i.e. impacted by Covid, but still operating reasonably normally.

Maynard