19 April 2020

By Maynard Paton

Results summary for S & U (SUS):

- Another set of record annual figures that showed steady progress — albeit overshadowed entirely by the potential impact of Covid-19.

- The boardroom’s confidence is encouraging. The final dividend was reduced only slightly and no staff have been furloughed.

- Some £302m has been loaned to customers with patchy credit histories, and recouping that money has become vital. Management says collections are “very good”.

- Net debt of £118m and a 26% net-interest margin lead to respectable returns on capital, but the borrowings will not prove ideal if defaults increase and profits fall.

- Current-year earnings have become anyone’s guess, and a bargain-basement P/E may be rather less than the current 10x trailing multiple. I continue to hold.

Contents

- Event link and share data

- Why I own SUS

- Results summary

- Coping with Covid-19

- Revenue and profit

- Advantage Finance

- Aspen Bridging

- Financials

- Valuation

Event link and share data

Event: Preliminary results and presentation for the twelve months to 31 January 2020 published 08 April 2020

Price: 1,700p

Shares in issue: 12,120,093

Market capitalisation: £206m

Why I own SUS

- Provides ‘non-prime’ credit to used-car buyers and property developers, where disciplined lending and reliable service have supported an enviable track record.

- Boasts veteran family management with 40-year-plus tenure, 50%-plus/£103m-plus shareholding and a “steady, sustainable” and organic approach to long-term growth.

- Offers some hope for a resilient Covid-19 performance following recent dividend declaration and decision not to furlough staff.

Further reading: My SUS Buy report | All my SUS posts | SUS website

Results summary

Coping with Covid-19

- How S&U has so far coped with the Covid-19 pandemic was the most pressing matter within these results.

- The company provides ‘non-prime’ loans to used-car buyers and property developers with patchy-but-improving credit histories.

- The economic disruption resulting from the pandemic could mean S&U suffers significant defaults and becomes nervous about its own borrowings.

- The latest balance sheet showed outstanding customer loans of £302m and net debt of £118m.

- Given the circumstances, the management narrative was relatively reassuring.

- S&U said (my bold):

“Our collections performance for March 2020 remains just below normal, although declining incomes and a temporary increase in unemployment, will undoubtedly see customer payments lower than last year and many falling into arrears.

Forbearance and the extra work on customer contact and relations being done by our collections teams… should encourage customers to “stay in their cars“, minimise any decline and encourage customers to resume normal payments when the pandemic recedes.”

- The company reckoned customers would pay back their loans, and debt would then fall:

“We expect our borrowing requirements to accelerate the trend evident since year-end by falling significantly over the next four months, as demand for our products falls and our collection performance proves relatively resilient.”

- Mind you, S&U did admit “consistent trends are impossible to discern”.

- The firm also admitted only a “nominal” number of new loans would be issued until at least 1 July 2020.

- Management’s confidence was underlined by the declaration of a final dividend.

- The 50p per share payout was a penny less than last year’s final, but could easily have been 51 pennies less at zero.

- S&U justified the payment by claiming:

“Whilst cash conservation is sensible, our strong treasury position and relatively low gearing give us a firm base for the preservation and renewed expansion of our business. Indeed, on current trends the next few months should be cash generative for the Company.”

- Even though the final divided was reduced by 1p per share, the payout for the full-year was 2p higher at 120p per share following earlier interim-dividend increases.

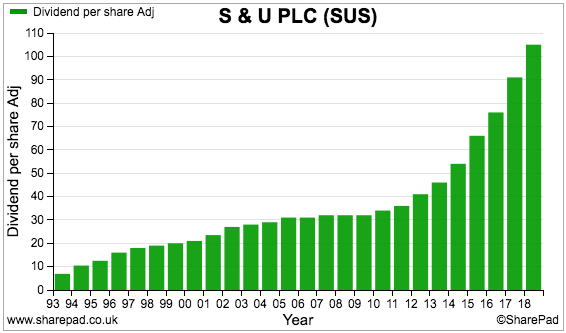

- S&U has an illustrious long-term dividend record, having never cut the payout since at least 1987:

- Keeping that growth record intact will be tough, given the next few months are likely to see collection rates decline and next-to-no new business come in to compensate.

- Management confidence was also expressed by staff being kept on and being paid in full during the pandemic (my bold):

“Nearly 90% of staff at Advantage, Aspen and Head Office are working from home with some staff redeployed to collections – none are being furloughed”

- For now at least, management’s remarks and actions are not sounding an alarm of imminent deep trouble.

Revenue and profit

- First-half figures from September and a trading update during December had already heralded a steady full-year performance.

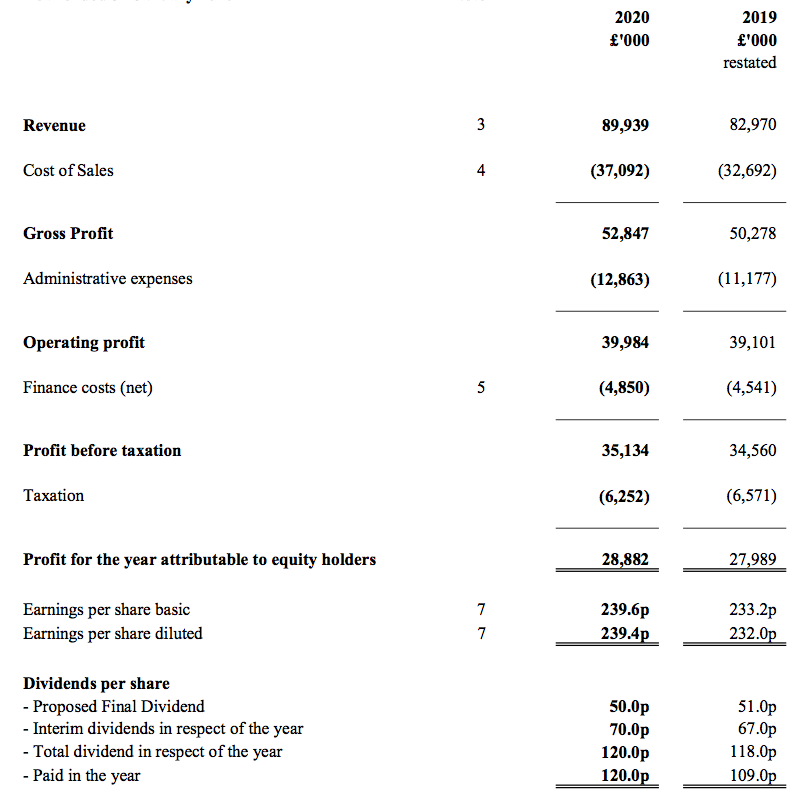

- Revenue gained 8% while operating profit climbed 2%:

| Year to 31 January | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 45,182 | 60,521 | 79,781 | 82,970 | 89,939 |

| Operating profit (£k) | 23,643 | 26,871 | 32,978 | 39,101 | 39,984 |

| Other items (£k) | - | - | - | - | - |

| Finance cost (£k) | (3,243) | (1,668) | (2,818) | (4,541) | (4,850) |

| Pre-tax profit (£k) | 20,400 | 25,203 | 30,160 | 34,560 | 35,154 |

| Earnings per share (p) | 133.6 | 170.7 | 203.8 | 233.2 | 239.6 |

| Dividend per share (p) | 76.0 | 91.0 | 105.0 | 118.0 | 120.0 |

- Revenue, profit and the aforementioned full-year dividend all registered new highs.

- The results extended SUS’s run of growth following the sale of the group’s home-credit business during 2015.

- The figures were distorted somewhat by revised accounting for the main motor-finance operation.

- S&U said:

“On reviewing its accounting policies in preparing the 2020 financial statements, the group has determined that revenue should be recognised ‘net’ of the impairment provision to align the accounting treatment under IFRS 16 with the requirements of IFRS 9 and also with the treatment adopted for similar assets in Aspen.”

- The prior-year 2019 results were therefore restated. Group revenue of £89m was reduced to £83m while the total loan impairment — effectively a charge for likely bad debts — was reduced from £23m to £17m.

- The restatement did not affect S&U’s 2019 profit — the prior-year operating profit remained at £39.1m. Nor was the prior-year balance sheet or cash flow altered.

- The revised accounting led to a £6m reduction to the 2019 impairment charge for car loans, which therefore distorted the analysis of whether S&U’s lending quality had improved.

- SUS suffered from rising loan impairments during the second half of 2018 and throughout 2019, but the bad loans started to subside during the first half of 2020.

- S&U’s interim 2020 figures applied the old accounting standard, which meant the first-half/second-half splits for motor-finance revenue and impairments were not directly comparable (see Advantage Finance below).

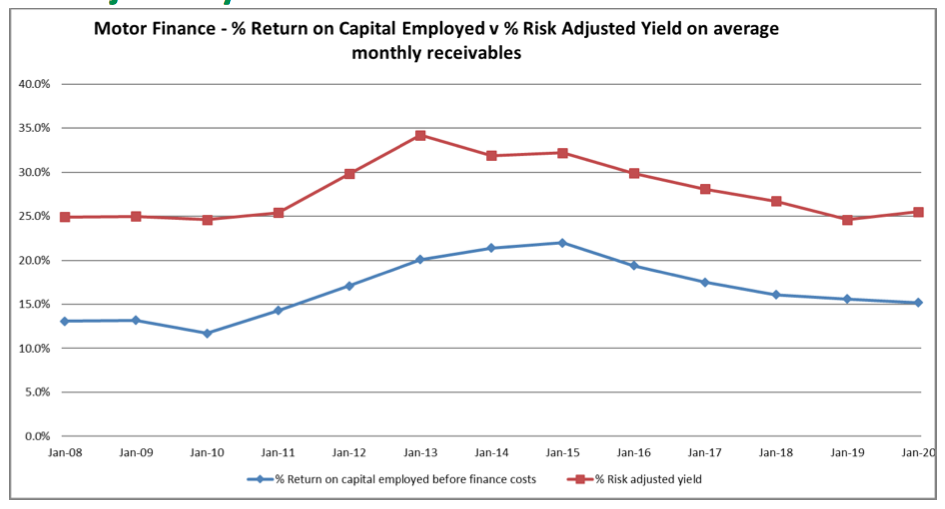

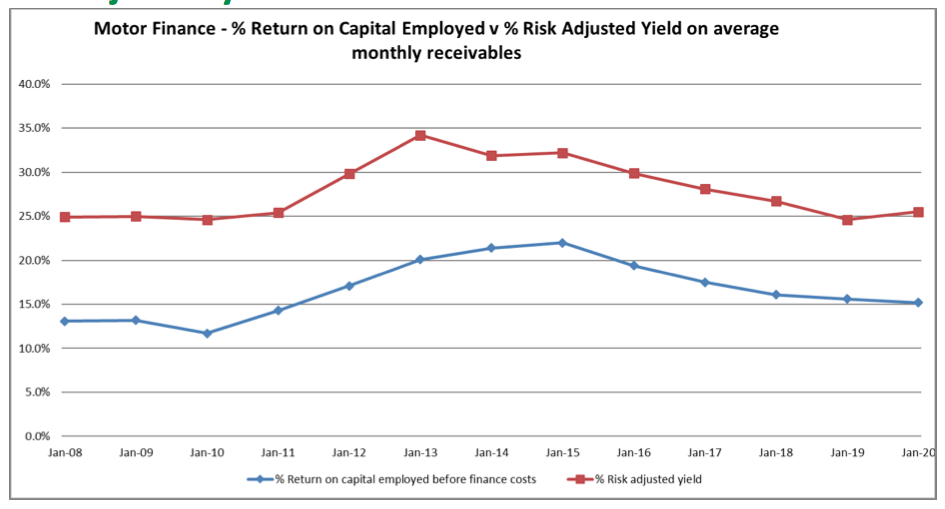

- At least S&U’s ‘risk-adjusted yield’ calculation remained consistent.

risk-adjusted yield is a ‘profit margin’ KPI used by SUS and is calculated as: (revenue - impairment provision) / average outstanding customer loans

- Risk-adjusted yield represents the net return SUS enjoys (before administration costs and broker commissions) on the money the group lends to customers.

- The higher the risk-adjusted yield, the healthier the loan book.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Advantage Finance

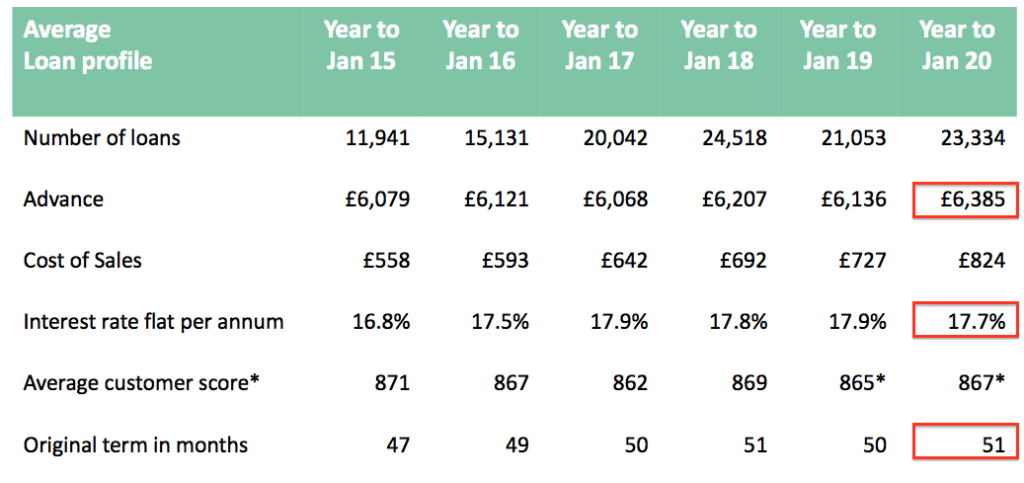

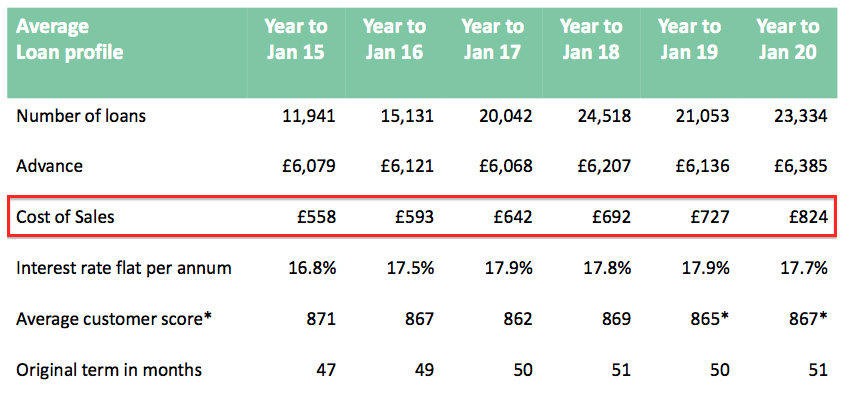

- The typical Advantage Finance customer has a patchy-but-improving credit history and borrows £6.4k to buy a five-year-old used car.

- The customer then pays back £11.6k over 51 months — equivalent to a flat c18% interest rate.

- Customers are described by management as ‘non-prime’ — “borrowers that have had a problem in the past but are on an upward trend” (point 3).

- Within the table below, the aforementioned accounting change meant the risk-adjusted yield was the sole consistent ratio during the past four half-year periods:

| H1 2019* | H2 2019 | FY 2019 | H1 2020* | H2 2020 | FY 2020 | ||

| Motor | |||||||

| Loan provision (£k) | 11,320 | 5,415 | 16,735 | 11,075 | 5,432 | 16,507 | |

| Revenue (£k) | 43,270 | 36,857 | 80,127 | 45,586 | 39,879 | 85,465 | |

| Average customer loans (£k) | 257,335 | 261,113 | 255,013 | 266,291 | 277,264 | 269,784 | |

| Loan provision/Revenue (%) | 26.2 | 14.7 | 20.9 | 24.3 | 13.6 | 19.3 | |

| Loan provision/Average customer loans (%) | 8.8 | 4.1 | 6.6 | 8.3 | 3.9 | 6.1 | |

| Revenue/Average customer loans (%) | 33.6 | 28.2 | 31.4 | 34.2 | 28.8 | 31.7 | |

| 'Risk-adjusted yield' (%) | 24.8 | 24.1 | 24.9 | 25.9 | 24.8 | 25.6 |

(*old accounting standard)

- My sums differ slightly from SUS’s official figures, which claim a risk-adjusted yield of 25.4% for 2020 and 24.6% for 2019.

- At least my calculations and SUS’s calculations suggest the risk-adjusted yield has improved slightly.

- Mind you, Advantage has some way to go to reach the yield levels of a few years ago.

- For example, the risk-adjusted yield (red line below) topped 30% during the ‘boom’ years of 2013, 2014 and 2015:

- I now view those boom years as unusually favourable rather than as a period that could be repeated easily.

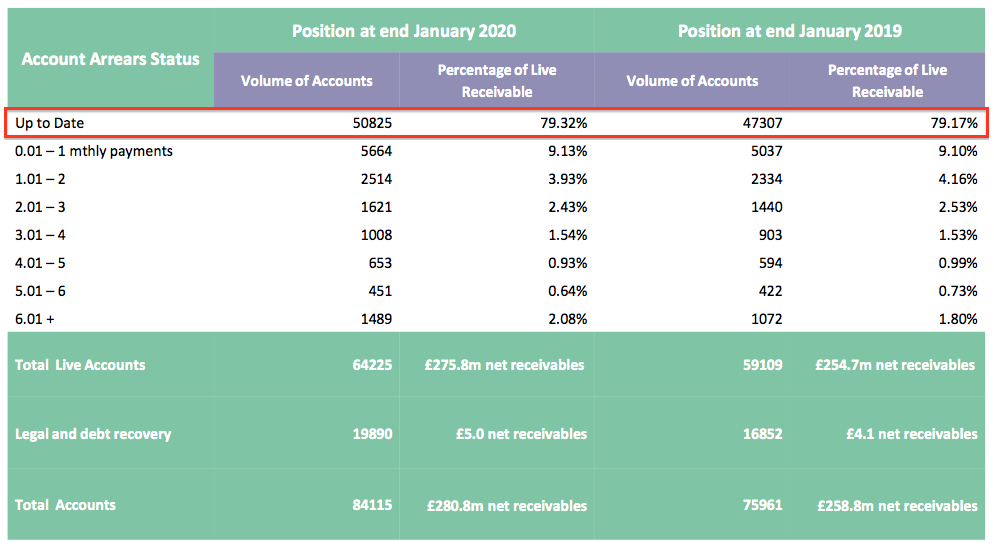

- The results powerpoint admitted a slightly higher proportion of motor-loan accounts were in arrears — 21% versus 20% for 2019:

- The interim statement had shown the number of accounts in arrears falling to 19%. The percentage was less than 10% a few years ago:

| 2016 | 2017 | 2018 | 2019 | 2020 | |

| Motor | |||||

| Up to date accounts | 29,460 | 37,447 | 45,668 | 47,307 | 50,825 |

| Overdue accounts | 3,144 | 5,620 | 8,811 | 11,802 | 13,400 |

| Total accounts | 32,604 | 43,067 | 54,479 | 59,109 | 64,225 |

| Up to date/Total (%) | 90.4 | 87.0 | 83.8 | 80.0 | 79.3 |

| Overdue/Total (%) | 9.6 | 13.0 | 16.2 | 20.0 | 20.7 |

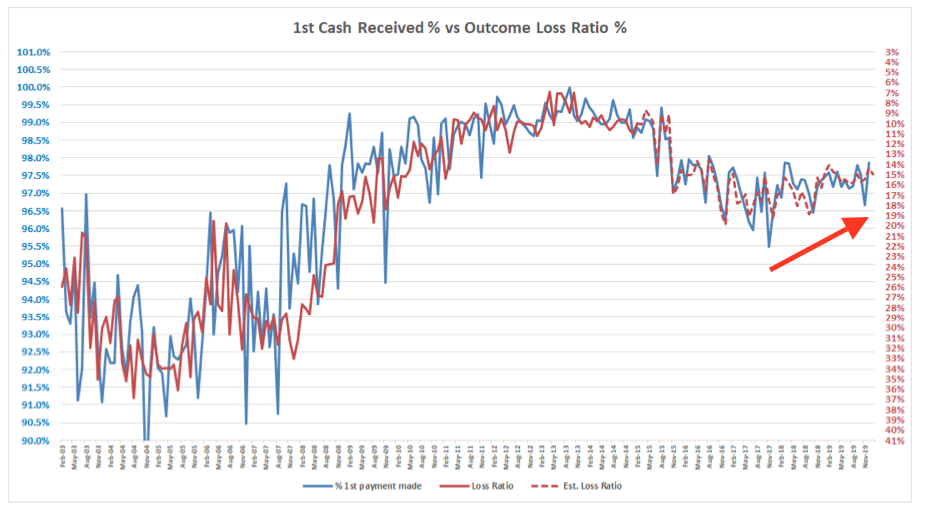

- Further hope of bad debts remaining under control comes from the proportion of car-loan borrowers making their first payment.

- The first-payment ratio (blue line, left axis) for Advantage has improved from 95.5% to almost 98% since late 2017:

- SUS believes this first-payment improvement should lead to lower future write-offs (dotted red line, right axis).

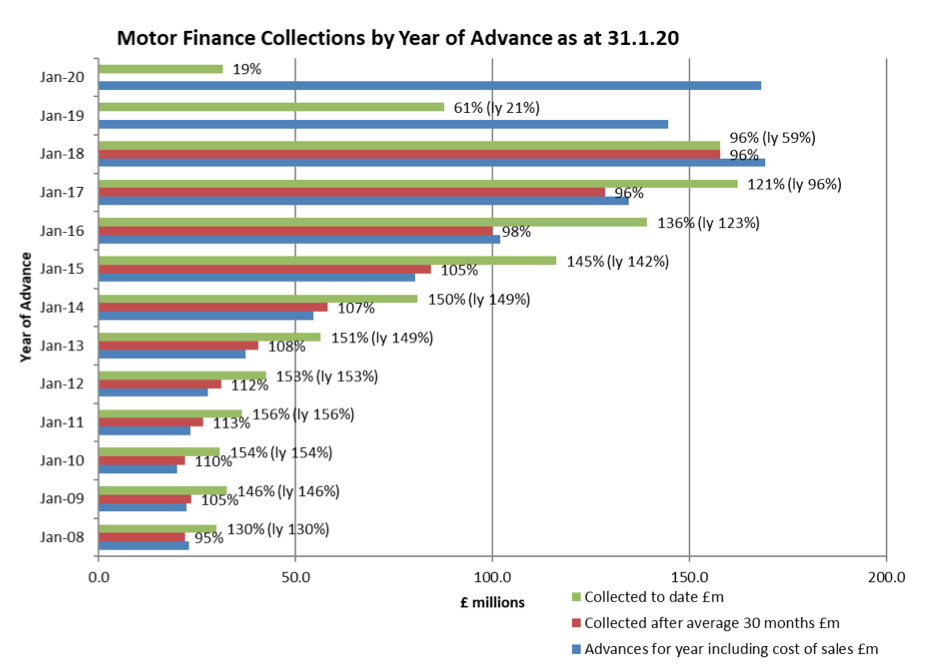

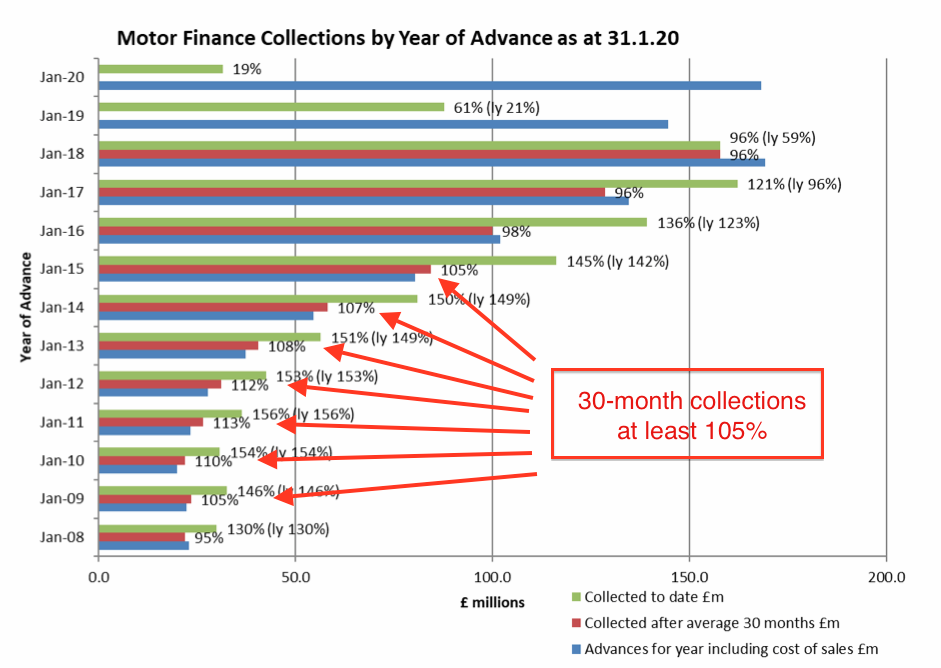

- The powerpoint slide below has taken on much more importance following the pandemic:

- The blue bars represent the money borrowed by customers during a particular year, while the red bars represent the money paid back within 30 months and the green bars represent the total money paid back.

- For example, approximately £100m was advanced during 2016, of which 98% was paid back within 30 months and 136% has since been repaid in total.

- Collections rates have deteriorated slightly during the past few years — a trend linked to the increased impairments seen during 2018 and 2019.

- Between 2010 and 2015, S&U issued loans where the subsequent 30-month repayments totalled at least 105% of the original advance:

- For 2016, the 30-month collection percentage had dropped to 98%, and then dropped to 96% for 2017 and 2018.

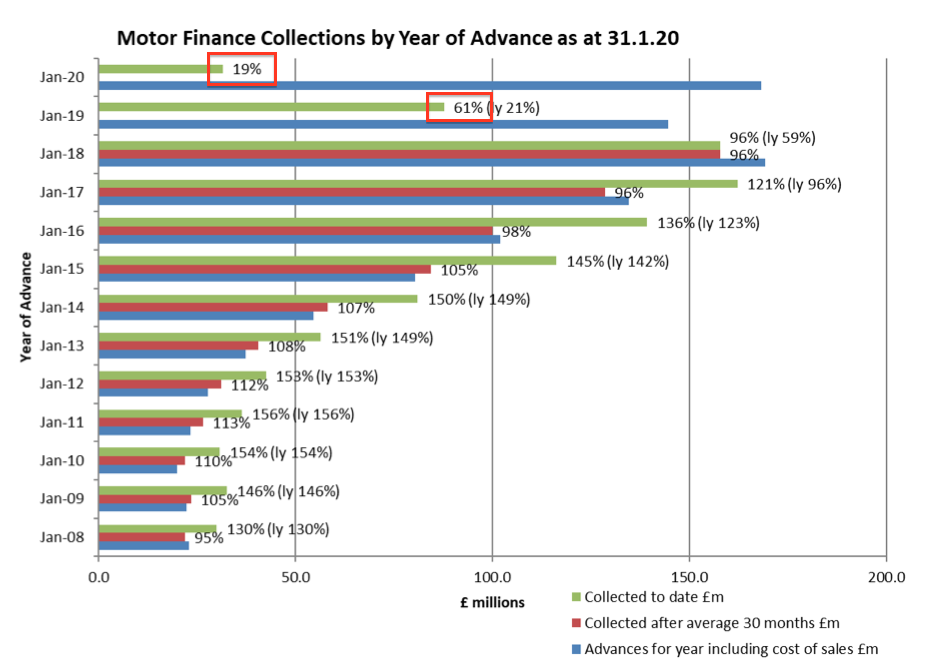

- The 19% collection rate for the latest year (2020) is not out of the ordinary. The same presentation slides for 2017, 2018 and 2019 showed current-year collections of 20%, 19% and 21% respectively:

- The 61% two-year collection rate for the previous year (2019) is not out of the ordinary. The same presentation slides from 2017, 2018 and 2019 showed two-year collections of 61%, 61% and 59% respectively.

- Exactly how collections will fare from here remains difficult to predict.

- The firm’s Covid-19 FAQs give the folowing response to the question Can I have a payment holiday?

“We are eager to discuss your individual circumstances with you in order to agree the best solution possible, and we will apply the appropriate levels of forbearance to all cases of genuine hardship. With that in mind, please call our staff on 01472 233200 Option 2 then Option 1 in order to speak to an advisor.“

- I will be very pleased if the 2021 results presentation shows current-year collections maintained at c20% and two-year collections maintained at c60%.

- I would like to think SUS will update shareholders well before next year’s presentation should future collection rates fall short of previous levels.

- “Tighter and cautious underwriting” meant the proportion of car-loan applicants that receive an approval was trimmed by two percentage points to 21%:

| 2017 | 2018 | 2019 | 2020 | |

| Motor | ||||

| Applications | over 750,000 | over 860,00 | over 1,000,000 | over 1,350,000 |

| Approvals (%) | c32% | c29% | c23% | c21% |

| Approvals | c240,000 | c250,000 | c230,000 | c284,000 |

| Loans issued | 20,042 | 24,518 | 21,053 | 23,334 |

| Loans issued/Approvals (%) | 8.4 | 9.8 | 9.2 | 8.2 |

- Applications for car loans increased significantly. More than 1,350,000 applications were received during 2020 — up at least 30% on 2019.

- Note that only 8% of approved applicants go on to collect their new loan.

- Management expalined at a presentation last year (point 3) why 92% of approvals did not conclude with a loan:

- The customer decided not to buy a car;

- The chosen car was not acceptable to Advantage (e.g. too old, too high a mileage, etc), or;

- A cheaper loan was found elsewhere.

- Management reckoned the third reason was the most common — but hinted the cheaper lender was likely to lose money on such deals.

- The 8% take-up suggests Advantage has the best rates for only a small proportion of potential borrowers.

- Despite the tighter underwriting, the 30%-plus increase to applications meant the level of new loan agreements recovered to 23,334 for 2020 — second only to the 24,518 issued during 2018:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | H2 2020 | |||

| Motor | ||||||||

| New agreements | 12,542 | 11,976 | 11,822 | 9,231 | 12,065 | 11,269 | ||

| Active customers | 49,000* | 54,479 | 58,008 | 59,109 | 62,032 | 64,225 | ||

| Net customer increase | 5,933 | 5,479 | 3,529 | 1,101 | 2,923 | 2,193 | ||

| Customer loans (£k) | 226,807 | 251,215 | 263,455 | 258,810 | 273,771 | 280,757 | ||

| Change to customer loans (£k) | 33,278 | 24,408 | 12,240 | (4,645) | 14,961 | 6,986 |

(*SUS rounded)

- SUS does not disclose the number of car-loan customers lost every year due to non-payment or full repayment.

- However, my sums suggest the net increase to car-loan customers had run at 11,412 during 2018.

- The net increase to car-loan customers then fell to 4,630 during 2019 and then rebounded slightly to 5,116 for 2020.

- Total outstanding car loans (less impairments) advanced by £22m to £281m during the year.

- 90% of Advantage’s business comes from loan brokers, with 5% direct from motor dealers and 5% being previous customers.

- Commissions paid to loan brokers continue to rise:

- Advantage’s cost of sales has jumped to £824 per loan, from £727 last year and £558 back in 2015.

- SUS commented upon the appointment of Advantage’s new managing director Graham Wheeler (my bold):

“In terms of leadership, this year saw the passing of the baton from Guy Thompson, Advantage’s founder MD, and inspiration for the past twenty years, to Graham Wheeler, an equally iconic figure in the motor finance industry and the driving force behind the expansion of Volkswagen motor finance in the UK a decade ago. The transition has, as expected, been smooth and seamless, and, irrespective of the current market disruption, promises still more of the continuous improvement in customer service and sensitivity to the market it serves that has characterised Advantage’s history.”

- Mr Wheeler’s predecessor established Advantage during 1999 and led the subsidiary to 20 years of uninterrupted profit growth.

- Within my previous SUS write-up, I wrote: “I trust Mr Wheeler can continue the same approach”.

- Now I am hoping Mr Wheeler can simply keep the collections coming in.

- Mr Wheeler’s social-media account is worth monitoring.

- In among messages about his back garden and daughter’s books, he sometimes lets slip details of company activity:

- 1,000 applications a day compares to last year’s 1,350,000 total — or c3,700 a day (spread over 365 days).

- I assume these 1,000 applications will not result in eventual loans because car dealers should be closed at present.

Aspen Bridging

- Established three years ago, Aspen offers property bridging loans aimed at small/individual property developers/investors with awkward financial circumstances.

- The average bridging loan to date has been c£450k with a monthly interest rate of “just over” 1% and a term of between 6 and 16 months. These case studies give a flavour of the borrowers involved.

- Management said the average transaction size at Aspen “rose to just over a half a million pounds as the business targeted more professional, and therefore reliable, residential developers and refurbishers”.

- A recent Aspen survey indicated many brokers wanted the £1.5m maximum loan size increased. The subsidiary’s website suggests the maximum is now £2m.

- Revenue and profit increased by more than 40% after total bridging loans climbed 35%:

| FY 2018 | FY 2019 | FY 2020 | |

| Property | |||

| Revenue (£k) | 899 | 2,843 | 4,474 |

| Pre-tax profit (£k) | (298) | 838 | 1,205 |

| Loans advanced (£m) | 12.9 | 23.1 | 31.3 |

| Agreements | 35 | 62 | 57 |

| Loans advanced/agreements (3k) | 369 | 373 | 549 |

- The second half was more profitable than the first:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Property | |||||||

| Revenue (£k) | 1,190 | 1,653 | 2,843 | 2,073 | 2,401 | 4,474 | |

| Pre-tax profit (£k) | 279 | 559 | 838 | 502 | 703 | 1,205 |

- Although bridging-loan impairments more than tripled to £713k, the amount remained small (at less than 4%) compared to the average level of bridging loans outstanding during the year:

| FY 2018 | FY 2019 | FY 2020 | |

| Property | |||

| Loan provision (£k) | 162 | 206 | 713 |

| Revenue (£k) | 899 | 2,843 | 4,474 |

| Average customer loans (£k) | 5,421 | 14,547 | 19,623 |

| Loan provision/Revenue (%) | 18.0 | 7.2 | 15.9 |

| Loan provision/Average customer loans (%) | 3.0 | 1.4 | 3.6 |

| Revenue/Average customer loans (%) | 16.6 | 19.5 | 22.8 |

| 'Risk-adjusted yield' (%)* | 13.6 | 18.1 | 19.2 |

- Fractionally higher revenue (i.e. interest) earned from customer loans helped Aspen’s risk-adjusted yield improve a percentage point to 19%.

- The half-year splits show a similar trend:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Property | |||||||

| Loan provision (£k) | 98 | 108 | 206 | 318 | 395 | 713 | |

| Revenue (£k) | 1,190 | 1,653 | 2,843 | 2,073 | 2,401 | 4,474 | |

| Average customer loans (£k) | 13,584 | 17,290 | 14,547 | 21,472 | 22,842 | 19,623 | |

| Loan provision/Revenue (%) | 8.2 | 6.5 | 7.2 | 15.3 | 16.5 | 15.9 | |

| Loan provision/Average customer loans (%) | 1.4 | 1.2 | 1.4 | 3.0 | 3.5 | 3.6 | |

| Revenue/Average customer loans (%) | 17.5 | 19.1 | 19.5 | 19.3 | 21.0 | 22.8 | |

| 'Risk-adjusted yield' (%) | 16.1 | 17.9 | 18.1 | 16.3 | 17.6 | 19.2 |

- Note that Aspen’s outstanding loans increased from £18m to £25m during the first half, then fell to £21m during the second. Those movements explain why average customer loans for the year were £20m — less than the averages for H1 and H2.

- SUS confirmed 112 of the 154 property loans issued during the last three years had been repaid in full.

- 42 loans therefore remain outstanding, with an average size of £467k.

- SUS admitted the remaining property-loan book was “smaller than anticipated” after the “interminable Brexit process dampened consumer and developer confidence”.

- Maybe the “smaller than anticipated” book has become a blessing following the pandemic.

- Management not surprisingly said: “Covid-19’s effect on the property market has seen Aspen rein back its lending and concentrate its energies on collections.”

- At the half year, management was very bullish on Aspen’s near-term future: “The current pipeline augurs a good second half, and a significant contribution by Aspen to Group profits in the next two years.”

- No such optimism was issued within this RNS.

- Aspen contributed 3% of group profit during 2020.

Financials

- Net debt increased by £10m to £118m during the year:

| Year to 31 January | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit (£k) | 21,251 | 26,871 | 32,978 | 39,101 | 39,984 |

| Depreciation (£k) | 426 | 253 | 294 | 414 | 450 |

| Net capital expenditure (£k) | (396) | (308) | (1,040) | (785) | (265) |

| Working-capital movement (£k) | (6,057) | (48,488) | (68,881) | (19,041) | (24,067) |

| Net debt (£k) | (11,901) | (49,167) | (104,990) | (108,037) | (117,844) |

- Of the £40m operating profit generated, a net £24m was reinvested back into working capital (i.e. to fund new loans) while £5m was paid as interest, £7m was paid as tax and £14m was paid as dividends.

- The half-year cash-flow split is informative:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Operating profit (£k) | 18,813 | 20,288 | 39,101 | 19,410 | 20,574 | 39,984 | |

| Working-capital movement (£k) | (21,056) | 2,015 | (19,041) | (20,717) | (3,350) | (24,067) | |

| Other cash-flow movements (£k) | (4,649) | (4,881) | (9,530) | (5,234) | (5,737) | (10,971) | |

| Operating cash flow (£k) | (6,892) | 17,422 | 10,530 | (6,541) | 11,487 | 4,946 |

- The second half of 2020 witnessed only a net £3m reinvested back into working capital (i.e. to fund new loans), which left H2 operating cash flow at £11m and helped reduce debt during the six months by £7m.

- The second half of 2019 also showed positive cash generation, this time with £2m returned from working capital after collections exceeded new loans issued.

- The current year should also witness positive working-capital movements that lead to favourable cash generation, given few new loans are being issued as repayments come in.

- As such, current-year net debt should reduce.

- For now, though, net debt of £118m equates to more than 4x 2020 earnings of £29m.

- Servicing the debt did not appear problematic last year. Bank interest payments of £4.7m were covered a reasonable 8-9x by operating profit.

- The prospect of positive working-capital movements should ensure interest cover on a cash basis is higher than 8-9x during 2021.

- Paying interest of £4.7m on debt that averaged £113m during 2020 implies an interest rate of 4.2%.

- The 2019 annual report (point 11) claimed SUS borrows money from mainstream banks at 4% to then lend out at 30%.

- The wide, 26% net interest margin is required to cover debt impairments and operating costs, and in turn earn a respectable return on the capital employed.

- SUS reckons the return on capital employed (ROCE) within Advantage was 15% for 2020 (blue line):

- The 26% net-interest margin and reasonable ROCE are reflected in my operating margin and return on equity (ROE) sums:

| Year to 31 January | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating margin (%) | 47.0 | 44.4 | 41.3 | 47.1 | 44.5 |

| Return on average equity (%) | 15.1 | 15.2 | 16.7 | 17.6 | 16.8 |

| Return on average equity (%)* | 12.6 | 13.2 | 12.0 | 11.9 | 11.5 |

(*adjusted for debt and interest payments)

- The 3% difference between my ROE calculation and SUS’s ROCE calculation is due mostly to my calculation including tax.

- For the record, since 2015, shareholder equity has advanced by £98m to £179m while earnings have advanced by £17m to £29m.

- The resultant incremental return on equity during those five years is a respectable £17m/£98m = 17%.

- SUS maintains a tiny defined-benefit pension scheme that last carried a surplus.

Valuation

- The pandemic has meant current-year earnings have become anyone’s guess.

- Management would not make any projections (my bold):

“The onset of the Covid-19 virus and the unprecedented disruption surrounding it, pose great challenges for consumers both in Britain and the wider world. S&U has strategies in place and the skills, resilience and experience to meet these challenges. However, they are unprecedented and their effect on the economy at present is unknown, as a result the Group is withdrawing future guidance.”

- Executive Chairman Anthony Coombs was interviewed by Proactive Investors after the results:

- Mr Coombs delivered a few positive snippets:

- “Some of our competitors have actually shut up shop completely — in fact the largest introducer is no longer doing business for the next two or three weeks”

- “Collections, however, still go on… and they have been very good. Altogether we’re becoming very cash generative…so on that basis we are pretty confident”

- “Covid has put the company behind by about 18 months on our development plans”

- “Our covenant level is about 50% higher than the current [65% gearing] level”

- “Cash is not a problem… we will probably repay overdraft facilities to reduce non-utilisation fees… we are very strong financially”

- For the record, operating profit of £40m taxed at the 18% applied in these results gives earnings of £33m or 272p per share.

- Adding the £118m debt to the current £206m market cap gives an enterprise value of £324m or £27 per share.

- Dividing the £324m enterprise value by my £33m earnings figure leads to a trailing multiple of almost 10x.

- A 10x multiple would normally seem appealing, but these times are not normal.

- The shares have not typically sported a premium rating. For perspective, the multiple was 14x when the price was almost 50% greater at £25 during 2018.

- A bargain-basement purchase ahead of any post-pandemic recovery may therefore require a P/E of rather less than 10x trailing earnings — assuming of course that earnings do one day recover.

- If maintained, the trailing 120p per share dividend supports a 7.1% income at £17 a share.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in S & U.

S & U (SUS)

Publication of 2020 annual report

Here are the points of interest beyond those mentioned in the blog post above.

1) Strategic report and review

I did not know quoted companies are now obliged to produce a Section 172 report (see point 2):

I note SUS now says a car loan ranges between £2k and £15k — last year the minimum was £3k.

Also, 1 million used cars are financed on HP each year — the 2019 report said 900,000. The market size remains c£17 billion a year.

The strategic review includes a new paragraph outlining the group’s “purpose and vision”

The review covers commentary on electric vehicles. SUS believes such vehicles are unlikely to have a medium-term impact on trading.

Other snippets include how Aspen may earn a “competitive edge“, the bridging-loan sector growth and a reminder of the group’s 80-year heritage and “business philosophy“:

2) Section 172

Here is the Section 172:

No great revelations.

3) Case studies

For the third consecutive year, ‘Natalie’ at Advantage enjoys a namecheck in the annual report case studies:

The timescales of the Aspen case study seem impressive:

4) Risks

No change to the principal risks section save for a line about Covid-19:

I must admit this report did not really mention Covid-19. The audit report briefly touched upon the subject (see point 9) and this post balance-sheet event had to mention it as well:

5) Ombudsman

Formal complaints remain less than 100 a year:

The HP rules mean SUS is on the hook for vehicle quality should the car be faulty at the point of sale.

Would be useful to know the type of non-vehicle complaint that reaches the Ombudsman.

6) Director pay

I am never quite sure whether SUS really needs three executives on £300k-plus each:

Mind you, the Coombs brothers have guided SUS well over time and perhaps the pay arrangements are required for the family to maintain the “steady, sustainable growth” approach.

Allowances and benefits of c£40k seem chunky. The bonuses seem under control, although the small print does say the c£25k payments were “fair and reasonable” after profit before tax increased by 1.7%:

The remuneration report reveals the PBT “stretch” target for 2020 was £36.5m — or growth of 5.6%.

Bear in mind Guy Thompson, the MD of Advantage for the last 20 years, retired from the role and has since become a non-board “adviser”:

Graham Wheeler, Mr Thompson’s replacement, is not (yet?) a board member and so his pay was not disclosed.

The chairman enjoyed a 4.4% pay rise versus 5.2% for the wider workforce.

The execs will enjoy up to a 3.3% pay rise for 2021.

“Stretching” targets will be set for 2021, too.

A new remuneration policy will be drawn up for next year to cover 2022, 2023 and 2024.

Shareholders were mostly happy with the 2019 remuneration report:

The chairman’s total pay has remained broadly similar during the past 10 years — so I can’t really gripe given how the company has performed in the meantime:

7) Corporate governance

A reminder that SUS is proud of its “family investment and management” and “non-bureaucratic” working culture:

Confirmation, also, that the Coombs family owns a “majority holding”. The declared Coombs shareholdings total less than 50%.

SUS deviates from corporate-governance guidelines because of the appointment of an executive chairman. The company makes a plea to corp-gov ‘box tickers’:

A useful snippet that revealed Graham Wheeler, the new Advantage MD, was one of very few appropriate candidates for the job:

Nice to see more audit meetings than remuneration meetings:

9) Audit going concern

Just a passing reference to Covid-19 from the auditor:

I am hopeful this means shareholders should not be worried too much about the effect of the pandemic on SUS, but then again the auditors are no doubt guessing like everyone else.

10) Audit materiality and scope

Materiality at a standard 5% of profit and a 100% scope:

11) Key audit matters

The two key audit matters — calculating the loan-loss provision and revenue recognition — remain the same.

But the auditors have been performing extra/revised checks on both. In particular, IT controls are tested:

A line about Covid-19 was inserted, too. Not sure how the auditors could in reality challenge management’s view in what is an unparalleled situation.

12) Audit tenure

22 years and counting for Deloitte as auditor:

The arrangement has to be put to tender by January 2024.

13) Performance measurements

A useful snippet that shows management thinking — a new performance measure for 2019:

Perhaps no surprise that “group collections” have come to the fore now that Covid-19 may have increased the likelihood of defaults.

14) Employees

Nothing too concerning here:

Total employee costs remain c10% of revenue. Average cost per employee was c£50k/year versus £45k for 2019 and £50k-plus for 2016, 2017 and 2018.

Revenue per Advantage employee was £528k versus £498k for 2019, but below the £550k and £611k for 2017 and 2018.

What is impressive was revenue per Advantage employee was below £300k for 2014 and earlier, so a vast productivity improvement was implemented from 2015 (at least according to my sums).

15) Loan loss provisions

Difficult to read too much into this note as the IFRS 9 format was introduced only last year. But two observations can be made:

First, the ‘new loans originated’ lines. These represent the estimated charge for bad loans relating to new loans issued during the year (the figures relate almost entirely to motor loans).

SUS advanced motor loans of £129m for 2019 and £149m for 2020.

‘New loan’ provisions of £11.8m therefore represented 9.1% of the advances for 2019.

‘New loan’ provisions of £14.5m therefore represented 9.7% of the advances for 2020.

So a small percentage increase and nothing obviously too sinister, but something to monitor.

Second, the ‘utilised provision on write-offs’. These represent loans that have actually been written off. When a loan is written off, the earlier estimated bad-loan provision is ‘utilised’ — i.e. is subtracted from the cumulative provision for estimated future bad loans (which for 2020 was £64.3m).

Anyway, the ‘utilised provision of write-offs’ increased by 46% to £18.4m for 2020, which is a large leap. Perhaps these write-offs related to loans issued during 2018 or 2019, when the underwriting was not as tight as it should have been in retrospect. Again, another number to monitor. If the ‘utilised provision on write-offs’ keeps increasing at a significant rate and the overall loan loss provision decreases notably, then questions would be raised about the suitability of the provisioning estimates.

16) Borrowings and interest

Confirmation that SUS still borrows at 4% and lends at 28%:

SUS paid interest of £4.7m during 2020 on average bank debt of £113m giving an effective rate of 4.2% — up from 4.1% for 2019.

Certain loans have been extended or replaced after the year end:

17) Options

Not many outstanding options:

I suspect the board’s new remuneration policy — to be set next year — will include a fresh LTIP scheme to motivate Graham Wheeler, the new Advantage MD.

18) Pension

No concerns here:

This small scheme has assets of £1.1m and pays out benefits of £41k a year. The figures are trivial compared to the size of annual profits.

Maynard

S & U (SUS)

AGM Statement and Trading Update

Here is the full text:

————————————————————————————————————

S&U, the motor finance and property bridging lender, issues a trading update for the period 1 February 2020 to 8 June 2020 prior to its AGM today. Covid-19 restrictions dictate a closed AGM, but the company will be holding a question and answer session for shareholders today at 2pm and details are in the notice of AGM.

In our Chairman’s Statement of 8th April, the Group withdrew future market guidance due to the uncertainty regarding Covid-19’s future impact.

The current economic recession brought about by the Covid-19 lockdown and the uncertain path out of it confirms our decision on future guidance, although we aim to update the market further in our trading update on 11th August 2020.

What is clear, however, is that S&U has been able to protect the safety and morale of our employees and the operations which depend upon them. All are safe and have adapted very well to working from home, so that we are proudly amongst only a fifth of firms in the UK who have not relied upon Government support during the epidemic. Nevertheless, the plunge in the economy and the long-term effects caused by Covid-19, and by the Government’s actions to overcome it, have understandably affected our customers.

Advantage Finance

Thus, at Advantage, our motor finance operation, sales initially fell to just 15% of normal levels as car dealers and broker introducers closed, deliveries ceased and car usage plummeted. In addition, Advantage sensibly restricted the categories of customer it was prepared to approve, restrictions which are likely to remain in place given the current uncertainties regarding employment and the labour market. Nevertheless, transactions have now steadily recovered to just over nearly 40% of normal. This improvement is expected gradually to continue as car sales outlets re-opened last week.

Similarly, collections have been affected by both lower consumer confidence and by the FCA measures put in place at the end of April offering borrowers a repayment “holiday” of up to 3 months. Whilst this remains under review it was both impulsive and, given the lenders’ responsibilities under CONC and Treating Customers Fairly principles, unnecessary for consumer protection. The effect so far is to see regular monthly collections fall in the most recent month by about 20%. Over the period as a whole, regular monthly collections reduced by about 9%. New “holiday” applications are now dwindling; these have accounted for virtually all of the short fall experienced in monthly collections and these are now stabilising.

Whilst these trends have yet to have their expected effect upon either bad debt or voluntary terminations, future collections and hence our provisioning for book debt impairment will largely be determined by the speed of economic recovery; in turn this will depend upon the extent of the labour market shake out after furlough measures come to an end. In the meantime, additional impairment provisions are being made which will inevitably have a significant effect on Advantage results this year.

Aspen Bridging

At Aspen, our property bridging business, greater optimism in the residential property market following the General Election result late last year, has been deflated by Covid-19, although, given the fundamentals under-pinning the residential market, it has not dissipated entirely. Thus, whilst transaction numbers have been under a quarter of those budgeted this year, recent applications have been robust allowing a good quality pipeline to increase. These trends are reflected in recent Right Move statistics on housing enquiries released late in May.

Better sentiment has also seen regular collections beating budget, whilst a longer “tail” of late or defaulted cases has also recently shown a promising reduction. Nevertheless, we remain sensibly cautious in our new business approach.

Treasury

The operational sustainability of our business continues to be reflected in our strong treasury position. As predicted, recent cash generation has seen group borrowings fall to £98m, some £30m less than budget. Gearing is now around 55%. We have therefore taken the opportunity to repay £25m of group facilities slightly early, which reduces financing costs and still leaves over £30m of headroom.

Commenting on S&U’s trading outlook, Anthony Coombs, S&U Chairman said:

“Given the challenges surrounding the economy and the future direction of the labour market, it would be unwise to attempt specific predictions. S&U’s conservative style of management, its strong treasury position and most of all the dedication and flexibility of our people and their relationship with our customers, will now pay dividends, both literally and figuratively. Despite the current uncertainties we face the future with our usual confidence and determination.”

————————————————————————————————————

The key parts are Advantage and Treasury.

Advantage collections were down 9% for February to May and down 20% for May. My sums indicate February, March and April must have seen collections down 5% on average to arrive at the four-month 9% decline. February was pre-lockdown, so if collections for that month were flat on 2019, then perhaps March collections fell 5% and April collections fell 10% to arrive at the four-month 9% decline.

SUS is clearly not happy with the repayment “holidays”, which will last until July and presumably ensure collections will continue to run at 20% lower than last year for June and July. What happens beyond then remains guesswork.

Missing from the statement are references to risk-adjusted yield and customer receivables — figures that are regularly cited within trading updates (for example last year’s AGM statement).

No doubt the figures were not revealed this time because “additional impairment provisions are being made which will inevitably have a significant effect on Advantage results this year.”

“are being made” is the crucial point — the text reads as if the impairments are only now being determined. I guess management does not want to commit to any figures at this stage because the situation remains unpredictable. The directors also enjoy four months of breathing space before determining the impairments for the half-year release in September.

The Treasury numbers reveals some clues as to what has happened.

Group borrowings of £98m compare with £119m at the January year-end, so a difference of £21m. A dividend of 36p per share — £4m — was paid in March, so free cash flow during the four months was £25m.

Gearing of 55% implies a net asset value of £98m/0.55 = £178m — in line with the £179m at the January year-end.

SUS’s asset base must therefore be £178m + £98m = £276m — which is mostly represented by outstanding customer loans.

Outstanding loans at the January year-end were £302m. So customer loans have decreased by £302m less £276m = £26m during the four months. £26m is 9% of £302m, so the reduction reflects the 9% reduction to collections.

The £26m decrease comprises new loans issued less any extra loan-loss provisions (net of write-offs) less repayments made. Unpicking those finer loan movements is impossible.

I have to confess I can’t really be sure if SUS is coping well with Covid-19 or whether the numbers in this statement are hiding problems.

Probably the most encouraging line from the statement is “Nevertheless, transactions have now steadily recovered to just over nearly 40% of normal.”. That suggests the market for used-car finance is recovering even with SUS’s tighter underwriting criteria, implying the sector/economy has not died just yet and suggesting perhaps collections from existing borrowers may improve over time.

Maynard

Thx for update, really do appreciate all the effort.

One humorous typo re Deloitte “The arrangement has to be put to tender by January 20204”

Thanks Robbins. Good spot

Maynard

S&U (SUS)

Trading update published 11 August 2020

Not a bad statement in the circumstances. Here is the full text interspersed with my comments:

—————————————————————————————————

“S&U PLC, the motor finance and property bridging specialist, today issues a trading update for the period from its AGM statement of the 9th June to the 31st July 2020. It will announce half year results on the 30th September 2020.

Trading

It is barely two months since our AGM Trading Update in June and our business continues its steady recovery from the economic shocks initially caused by Covid-19, and the Government’s measures to combat it.

As we adjust to a gradual but uneven easing of the Lockdown, and trading volumes return nearer normal, we still feel it wise at present not to issue forward guidance. In changing times, it is wise to recall Mark Twain’s admonition — “It ain’t what you don’t know that gets you into trouble, but what you know for certain that just ain’t so”.

The mood of the British consumer is still skittish and cautious. Although recent manufacturing and financial services sectoral surveys are encouraging, uncertainty still persists about both the state of the labour market as Government support measures are dismantled, and about the deeper structural effects on the economy caused by the pandemic. We anticipate greater clarity over the next three months.

Although these trends will inevitably have a significant impact on S&U’s results this year, the Company is still profitable, paying dividends and our financial strength, experience, excellent broker partnerships and flexible and committed staff should ensure a return to a more “normal” trading environment by the end of the year.

—————————————————————————————————

“Steady recovery”, “paying dividends” and “a return to a more “normal” trading environment by the end of the year” does not sound too catastrophic.

—————————————————————————————————

Advantage Finance

As more car sales outlets recently returned to business, so sales at Advantage Finance (‘Advantage’) have recovered from around 40% of normal to nearly 80%. Loan applications are at a record high but our policy of early tightened under-writing, and a focus on customer quality has seen current transaction levels 25% less than last year.

This has produced improved early repayments, indicative of the high quality of the new customers taken on since Covid began. In the medium term this may offer the kind of significant market opportunities in the near prime field from which Advantage benefitted following the banking crisis of a decade ago.

Although collection levels this year have fallen from their usual 94% of due to just over 75%, this has entirely been brought about by the FCA mandated customer repayment “holidays”. These have involved around 16,500 or 26% of our 63,500 customers.

Although these customers are now gradually resuming repayment, the extent to which they do so — particularly in light of the further “holidays” of up to three months recently proposed by the FCA – will become clearer in the next couple of months. Current early indications make us cautiously optimistic.

In the meantime, Advantage has continued to minutely analyse customers by income, expenditure type, headroom and previous credit history, so that we can anticipate, focus on and assist those who may struggle to return to contractual terms.

—————————————————————————————————

Again, the following does not seem too catastrophic:

“our policy of early tightened under-writing, and a focus on customer quality has seen current transaction levels 25% less than last year. This has produced improved early repayments, indicative of the high quality of the new customers taken on since Covid began”

What counts for this year is collections. 26% of customers enjoying payment holidays is not ideal, but not a lot SUS can do given the FCA instructions on the matter. This line — “Current early indications make us cautiously optimistic” — provides encouragement that customers returning from payment holidays will mostly resume payments.

Note that SUS’s trading updates typically reveal Advantage customer numbers and occasionally refer to credit quality. None of those stats were divulged this time. Next month’s results will reveal all.

—————————————————————————————————

Aspen

Although activity in the housing market over the past two months has been similarly restrained by the febrile UK economy, Aspen has seen an uptake in both new transactions – with July being above budget — and in recent loan redemptions. As the current deals pipeline slowly improves, current net receivables are just below £19m compared to £15.5m in early June.

—————————————————————————————————

Seems reasonable in the circumstances.

—————————————————————————————————

Treasury

Group borrowings are £108m against £98m in June and reflect both the payment of our final dividend and slightly stronger sales growth at Advantage. We conduct regular scenario planning reviews to anticipate funding requirements over the next 4 years. With existing committed facilities of £130m, significant headroom will be maintained and further medium-term funding obtained as required.

—————————————————————————————————

The final 50p per share dividend cost £6m, so the underlying business therefore absorbed extra cash of £4m to extend net debt by £10m. June’s AGM statement revealed net debt had been reduced by c£20m since the 2020 year end as the business focused on collections, so hopefully the underlying £4m increase since June does indeed reflect “stronger sales growth at Advantage” and not collections going awry.

—————————————————————————————————

Commenting on the Group’s trading and outlook, Anthony Coombs, S&U chairman, said:

“First and foremost, I take this opportunity to record our thanks to, and admiration for, the spirit, flexibility and sheer determination of our staff to maintain our standards of customer service during unprecedented and trying times. Although recent trading trends have been encouraging, the level of uncertainty surrounding the economy, the direction of Covid-19 and the effect that it has on customers’ confidence make prudence paramount.

“What we can say for certain, is that S&U continues to make profits and has the experience, the financial resources, skilled people and tried and tested business philosophy needed to weather any further economic storms — and the ambition to grow strongly again when it is sensible to do so.”

—————————————————————————————————-

Encouraging to read the seasoned Mr Coombs can “say for certain” that SUS continues to make profits!

Maynard

Hi Maynard,

Thanks for the detailed analysis of this share. I continue to be impressed by the way management run this business and the strong long term shareholder alignment offered by the Coombs’ interests.

One question I have which if you can shed light on is the near 20% shareholding of Wiseheights Ltd. Do you know anything about this shareholder from previous interaction with the business? There are some detailed accounts on companies house which indicate that dividends from shareholding is the major source of income.

All the best and thanks again

Hi James

Thanks for the message. Wiseheights (under different names) has been a c20% shareholder since at least 1985. The charity was gifted its shares (by whom I do not know) and S&U is the only investment. Wiseheights was not mentioned in the capital markets presentation I attended last year, and I know nothing beyond the Companies House documents.

Thanks

Maynard