01 July 2020

By Maynard Paton

Results summary for Tasty (TAST):

- Largely redundant annual figures that revealed revenue down 6% and another operating loss.

- TAST’s 56 restaurants were shut in March and my estimates suggest the group could survive without sales until November.

- The second half seemed encouraging after Christmas bookings were helped by a turkey-themed festive menu.

- A £2m property disposal bolstered cash and cleared debt but significant liabilities remain.

- The £2.8m market cap could be a bargain, but radical management action is now essential to keep the business afloat. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own TAST

- Results summary

- Covid-19 and cash burn

- Revenue, another loss and sales per site

- Second half and Christmas dinners

- Estate optimisation

- Financials

- Valuation

- What now?

Event links, share data and disclosure

Event: Preliminary results and annual report for the 52 weeks to 29 December 2019 published 17 March 2020

Price: 2p

Shares in issue: 141,089,758

Market capitalisation: £2.8m

Disclosure: Maynard owns shares in Tasty. This blog post contains SharePad affiliate links.

Why I own TAST

- Experienced family management has already built and sold two quoted restaurant chains for £200m-plus (ASK Central and Prezzo).

- Bombed-out share price may provide substantial upside… assuming the business does not run out of cash during (or after) the pandemic.

- Just too late to sell. TAST now represents less than 1% of my portfolio, with the investment already losing more than 80% of its value.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary:

Covid-19 and cash burn

- TAST’s 2019 results are now largely redundant following the Covid-19 outbreak.

- TAST operates 56 restaurants, all of which were closed from 24 March 2020 due to the pandemic.

- The first restaurant re-opened on 28 May for takeaways and deliveries, while seven further outlets have since followed suit.

- Three of the opened restaurants are dim-ts and five are Wildwoods:

- TAST has therefore earned zero revenue for two months.

- Restaurants are allowed to re-open for indoor/outdoor dining — albeit with restrictions — from 4 July.

- TAST last week confirmed plans to have 25 sites re-open by mid-July.

- At the time of the shutdown, TAST claimed it had “sufficient financial resources for the foreseeable future”.

- The 2019 results revealed net cash of £2.9m as at 29 December 2019.

- A statement published during January 2020 revealed a restaurant had been sold for £2m and the remaining bank debt would in turn be cleared.

- Heading into the pandemic, cash may well have been £4m or more while debt should have been zero.

- TAST has not disclosed its financial position since the lockdown commenced.

- Presumably employees have been furloughed and all other expenditure reduced significantly.

- Four hospitality/leisure businesses have said their lockdown cash-burn rates were averaging 15.4% of revenue:

| Company | Stated cash burn (£k) | Annualised cash burn (£k) | Revenue (£k) | Cash burn/ Revenue (%) |

| Everyman Media | 900/month | 10,800 | 64,955 | 16.6 |

| Hollywood Bowl | 1,600/month | 19,200 | 129,894 | 14.8 |

| Loungers | 480/week | 24,960 | 152,999 | 16.3 |

| Revolution Bars | 400/week | 20,800 | 151,404 | 13.7 |

| Tasty | 132/week* | 6,849* | 44,573 | 15.4* |

(*estimated)

- 15.4% of TAST’s 2019 revenue equates to £6.8m a year/£571k a month/£132k a week of lockdown cash burn.

- TAST may have therefore burned through £1.8m since the restaurants were shut.

- At that rate TAST could survive without revenue until November before its cash runs out.

- Those four hospitality/leisure businesses only disclosed their cash-burn rates because they were asking shareholders for extra money.

- I guess everything depends on how TAST defines “the foreseeable future” when it says it had “sufficient financial resources for the foreseeable future”.

- The 2019 annual accounts were prepared on a ‘going concern’ basis. The report said:

“The Board has a reasonable expectation that the Group has adequate resources to continue in operational existence for a period of at least twelve months since the Board approved these financial statements.”

- Mind you, the results commentary did seem just as concerned about Brexit as Covid-19:

“Notwithstanding the Coronavirus (COVID-19) outbreak, the start of 2020 has continued to be encouraging. However, the full impact of Brexit remains unclear. The likely upward pressure on food cost and the reduction in the supply of labour and the availability of certain food items all remain a concern to the business. Whilst we have measures in place to reduce the anticipated impact of Brexit or COVID-19 issues, it is impossible to mitigate all potential risks but we are constantly monitoring the situation”

- The commentary was published a week before the lockdown started, so perhaps management (alarmingly) had yet to grasp what was about to happen.

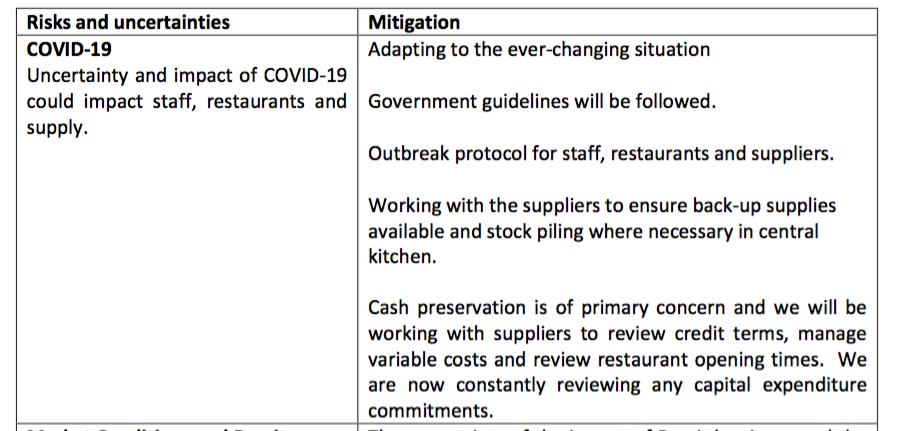

- I get the impression the formal Covid-19 risk assessment was hastily produced:

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue, another loss and sales per site

- TAST’s financials pre-Covid-19 were already in a perilous state.

- Awful interim figures had left TAST needing a decent second half to avert a cash trauma.

- In the event TAST said “trading over the Christmas period was positive” and the second-half figures showed some encouraging signs.

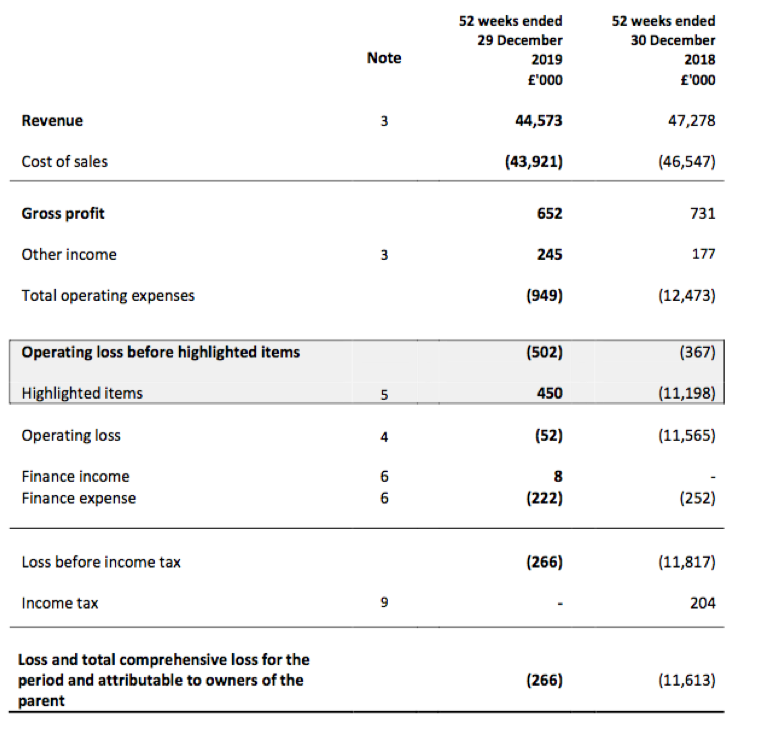

- For the full year, revenue fell 6% and another operating loss was reported:

| Year to c31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (£k) | 35,794 | 45,847 | 50,309 | 47,278 | 44,573 |

| Operating profit before pre-opening costs (£k) | 3,818 | 4,692 | 1,101 | (478) | (542) |

| Pre-opening costs (£k) | (644) | (642) | (413) | - | - |

| Operating profit (£k) | 3,174 | 4,050 | 688 | (478) | (542) |

| Net finance cost (£k) | (107) | (213) | (202) | (252) | (214) |

| Other items (£k) | - | (3,925) | (9,956) | (11,087) | 490 |

| Pre-tax profit (£k) | 3,067 | (88) | (9,470) | (11,817) | (266) |

| Earnings per share (p) | 4.64 | (1.56) | (13.84) | (19.42) | (0.23) |

| Dividend per share (p) | - | - | - | - | - |

- TAST explained the sales shortfall was “mainly due to the closure of sites and partly due to like-for-like decline”.

- Three restaurants were shut during the year to reduce the estate to 57 outlets.

- I estimate average revenue per restaurant dropped a fraction to £762k a year:

| Year to c31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (£k) | 35,794 | 45,847 | 50,309 | 47,278 | 44,573 |

| Year-end restaurants | 48 | 61 | 64 | 60 | 57 |

| Average restaurants | 42 | 54.5 | 62.5 | 62 | 58.5 |

| Revenue per restaurant (£k) | 852 | 841 | 805 | 763 | 762 |

- Between 2011 and 2014, sales per site topped £900k.

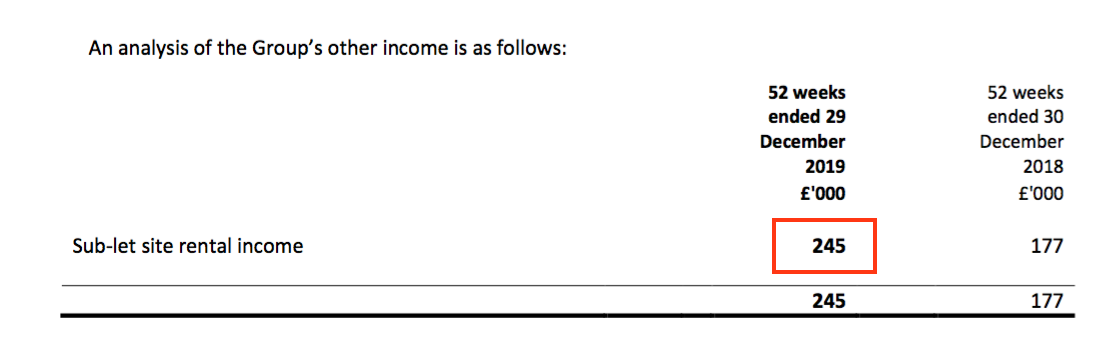

- TAST collected sub-let site rents of £245k during 2019:

- Adjust for the sub-lets, and the trading profitability of the restaurants was therefore worse than the headline numbers suggested.

Second half and Christmas dinners

- The second half showed a promising sales-per-site improvement on the comparable period of 2018:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (£k) | 22,997 | 24,281 | 47,278 | 21,126 | 23,447 | 44,573 | |

| Average number of units | 62 | 60 | 62 | 58.5 | 57 | 58.5 | |

| Average revenue per unit (£k) | 742 | 809 | 763 | 722 | 823 | 762 |

- H2 sales per site of £823k was the best six-month performance since £851k was registered during H2 2016.

- The simple idea of serving turkey at Christmas worked well:

“In Wildwood we offered four turkey-based dishes including a roast dinner which proved to be popular and we believe a better choice and more competitively priced Christmas menu than our competitors was one of the key reasons we performed well over the period.”

- The turkey-based dishes were turkey burgers, roast turkey, a Christmas pizza (which included turkey) and roasted turkey penne:

- TAST’s festive menu was priced at £17.95 per person for three courses for bookings on or before 28 November 2019. The charge thereafter was £19.95 per person.

- The half-year splits show TAST reporting an operating profit during the second half:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (£k) | 22,997 | 24,281 | 47,278 | 21,126 | 23,447 | 44,573 | |

| Gross profit* (£k) | 313 | 595 | 908 | 29 | 868 | 897 | |

| Operating profit*(£k) | (184) | (294) | (478) | (658) | 116 | (542) |

(*includes sub-let income)

- Bear in mind that H2 profit was supported by those sub-let rents, without which TAST would have reported a small H2 operating loss.

Estate optimisation

- This 2019 statement hinted that an earlier plan to “optimise the estate” may now be completed.

- The preceding half-year results said:

- “Our focus is on optimising the current estate and turning around underperforming sites.”

- “The Group continues to review the estate and further disposals will be made if appropriate.”

- Whereas this full-year statement said:

- “We have addressed optimising the estate in two key ways.“

- “The Group continues to review the estate and will consider any appropriate offers but no further disposals in 2020 are currently planned.”

- TAST reported tangible-asset impairments during 2016, 2017 and 2018, but nothing was reported for 2019:

| Highlighted items | FY 2016 | FY 2017 | FY 2018 | FY 2019 |

| Profit on disposal (£k) | - | 1,237 | 2,132 | (43) |

| Rebranding (£k) | (55) | - | - | - |

| Onerous leases (£k) | (1,635) | (1,635) | (1,687) | 564 |

| Lease impairment (£k) | (294) | (96) | (897) | - |

| Asset impairment (£k) | (3,576) | (9,462) | (10,063) | - |

| Goodwill impairment (£k) | - | - | (115) | - |

| Restructure & consultancy (£k) | - | - | (457) | - |

| Total | (3,925) | (9,956) | (11,087) | 490 |

- Wishful thinking perhaps, but perhaps the lack of 2019 write-offs indicates restaurant trading is no longer deteriorating (at least up until Covid-19).

- TAST added:

“In addition to site disposals we engaged with our landlord’s for assistance. Our collaborative approach has been well received and generally we have found landlords to be supportive and cooperative. We have been successful in achieving rent reductions and lease concessions on a number of sites.”

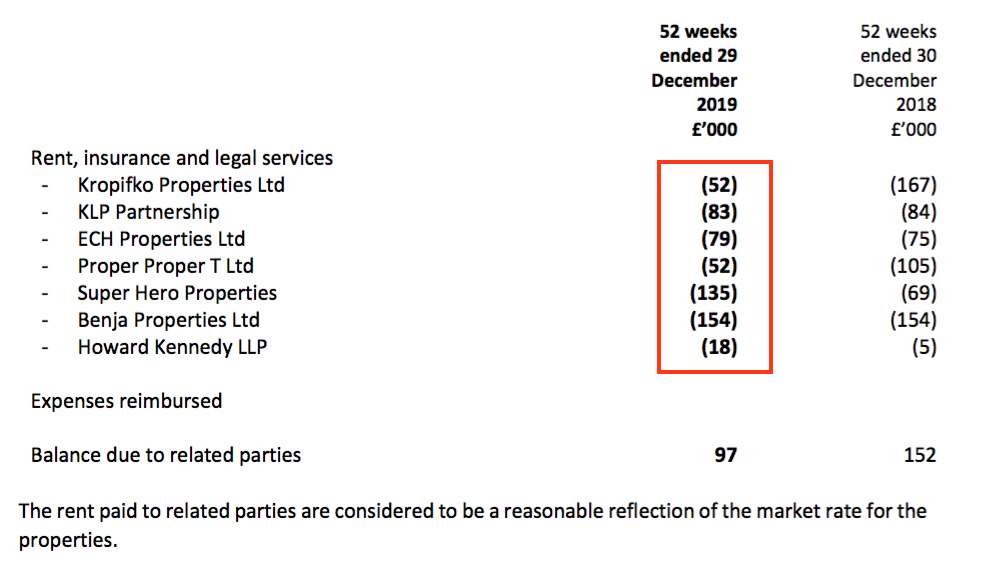

- TAST directors Adam and Sam Kaye — and their wider family — do own a number of sites occupied by TAST, and appear to have co-operated as landlords.

- Related-party transactions were reduced by 13% to £573k last year:

Financials

- The aforementioned property disposal allowed TAST to clear its remaining debt.

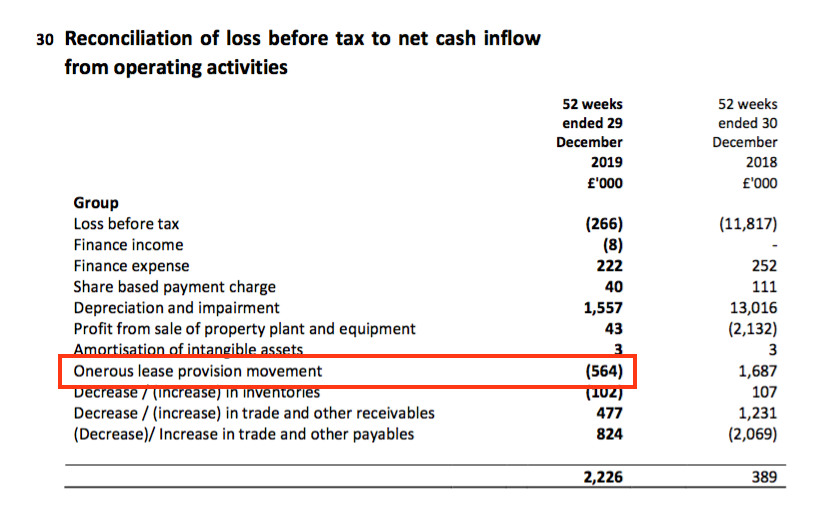

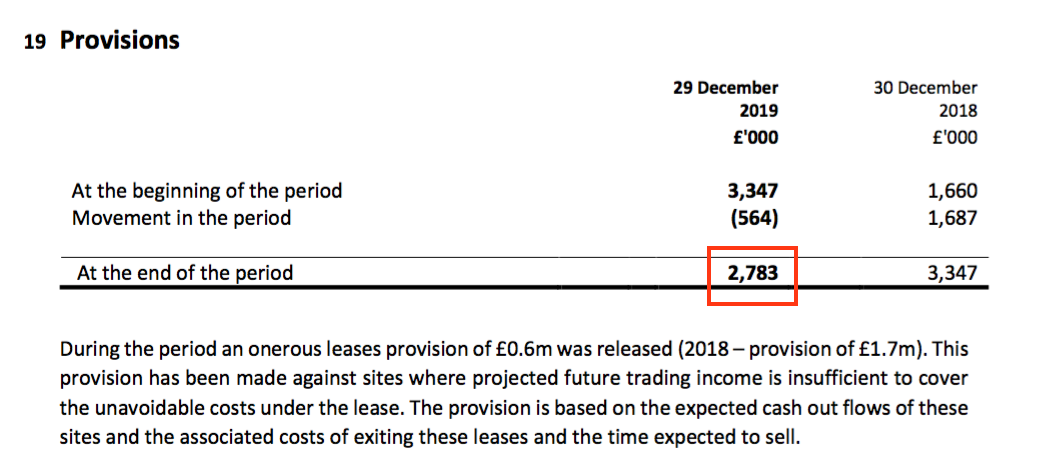

- However, a liability that has yet to be cleared is the provision relating to loss-making restaurants.

- During 2017 and 2018, TAST charged a total of £3.3m against earnings as an “onerous lease” provision.

- This £3.3m represented the estimated cash outflows from underperforming restaurants and/or the associated costs of exiting the leases.

- During the second half of 2019, cash of £564k was absorbed by the underperforming restaurants and/or the associated costs of exiting the leases:

- TAST’s “onerous lease” provision now stands at £2.8m, which suggests a further £2.8m must be spent to handle the troubled outlets:

- This £2.8m will be reflected within future cash flow statements but not within TAST’s future income statements (because the sum was expensed during 2017 and 2018).

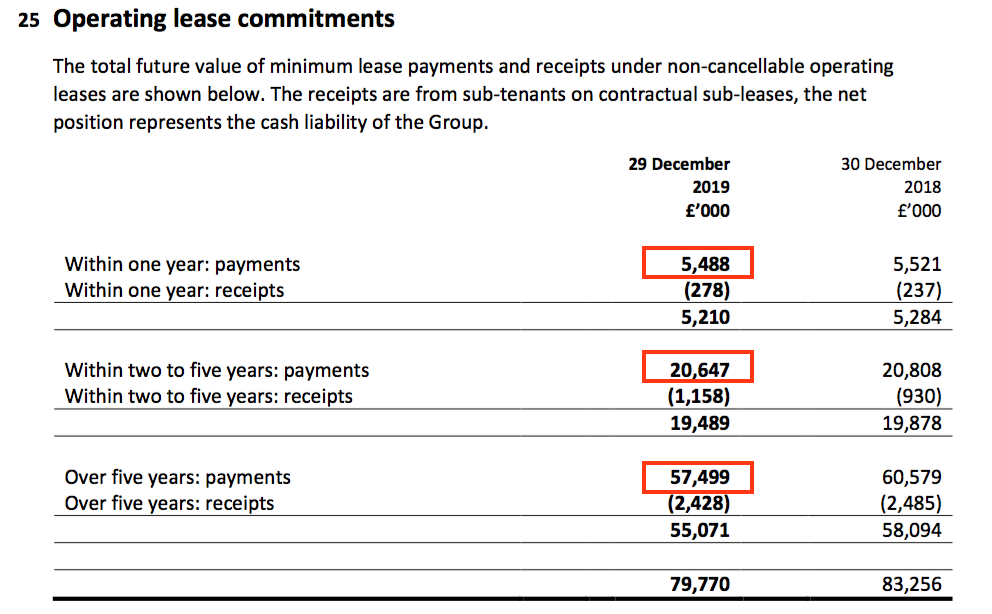

- Remember also that TAST carries long-term lease obligations that at the last count totalled £84m before sub-let income:

- Lease obligations for 2020 of £5.5m suggest TAST’s average lease length is 15 years.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

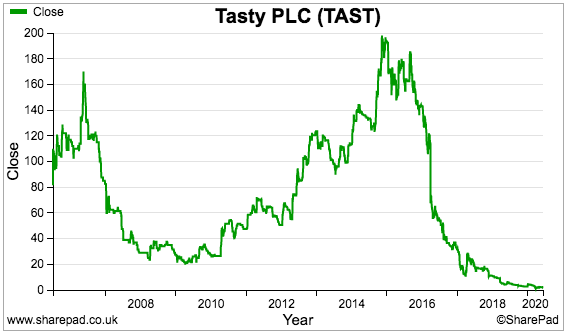

- The recent 2p share price supports a £2.8m market cap.

- A £2.8m market cap compares to trailing revenue of £44m and a net book value of £13m.

- The estate currently comprises 51 Wildwood restaurants and 5 dim-t restaurants. Each site is therefore valued at £2.8m / 56 = £50k.

- For comparison, three outlets were disposed of during 2019 for cash proceeds of £0.5m.

- The restaurant sold during January — albeit a prime site overlooking Tower Bridge in London — raised £2m.

- TAST could of course have sold its best sites and those that remain may not be worth as much — assuming they are worth anything at all.

- Bear in mind the aforementioned £2.8m provision indicates some restaurants had a negative value at the 2019 balance-sheet date.

- The pandemic will undoubtedly prompt management and/or the auditors to review the carrying value of TAST’s estate and possibly declare additional provisions/write-offs.

- The £2.8m market cap also compares to 2019 free cash flow of £1.8m before interest costs:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Cash generated from operations (£k) | (2,259) | 2,648 | 389 | (460) | 2,686 | 2,226 | |

| Tax received (£k) | - | 26 | 26 | - | - | - | |

| Capital expenditure (£k) | (670) | (591) | (1,261) | (227) | (226) | (453) | |

| Free cash flow before interest (£k) | (2,929) | 2,083 | (846) | (687) | 2,460 | 1,773 | |

| Net interest paid (£k) | (125) | (127) | (252) | (176) | (38) | (214) | |

| Free cash flow (£k) | (3,054) | 1,956 | (1,098) | (863) | 2,422 | 1,559 |

- Interest costs with debt being cleared should now be zero.

- The shares appear to be a bargain — assuming the cash does not run out during the pandemic and the business can become profitable once social-distancing measures are scrapped entirely.

What now?

- Returning TAST to profit post-Covid-19 requires some radical management thinking.

- The business lost money during the two years before the pandemic, so going back to the same menu with the same discounts with the same way of working at the same locations does not seem viable.

- The pandemic has instead brought an opportunity to reshape the group entirely.

- Possible ways to lower costs and/or increase staff productivity include:

- Go takeaway/delivery only;

- Adopt a very simple menu and self-service dining (see Toby Carvery);

- Implement a CVA to jettison all the problem sites, or;

- Become a franchisor and let others run the restaurants.

- TAST did conduct an email survey on 19 May asking customers for their post-lockdown intentions:

- Questions included:

- When government restrictions are reduced/lifted, how soon are you likely to dine out again?

- What would be most important to you in choosing to dine out with Wildwood in future?

- What type of food would you most want to be available?

- I would not like to be served a meal by an employee wearing a mask and gloves.

- At least the 2019 results commendably included this new goal:

“Our aspiration is to be the high street brand with [the] highest standard of customer service in the casual dining sector.”

- That target seems more achievable than possessing the most attractive and/or profitable menu in the casual dining sector.

- Whether the “highest standard of customer service in the casual dining sector” revives TAST’s fortunes post-pandemic remains to be seen.

- For now, the over-riding issue is whether TAST will survive the pandemic.

- TAST raised £3m from shareholders last year to shore up the balance sheet, and the appetite to inject further money to keep the business afloat has to be questioned.

- A lack of funding could leave the door open for TAST to de-list.

- Management (and connected parties) control 40% of TAST, and the same individuals voted for Richoux to give up its AIM quotation last year with the following justification:

“The Directors have concluded that the Cancellation will enable the Company to reduce significantly administrative costs, enabling Richoux to continue trading as a private company, possibly without the requirement for external funding whilst the Company focusses on improving its estate.”

- TAST represents less than 1% of my portfolio, with the investment having lost more than 80% of its value. I am resigned to holding on with the vague hope of a recovery.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Tasty (TAST)

Publication of 2019 annual report

Various interesting snippets, most of which were not mentioned in the blog post above;

1) Going concern

Confirmation of the ‘going concern’ narrative. The board has a “reasonable expectation” — the same term used for the previous two years:

2) Audit

Haysmacintyre replaced BDO as auditor for 2019:

The new auditor appears to have evaluated certain management assumptions in greater depth.

In particular, impairments and lease provisions are now double-checked with 10-year projections:

The ‘going concern’ basis was also checked for 2019:

A good sign — audit materiality was reduced significantly. Scope remains 100% as well:

3) Corporate governance

New for 2019 — a full corporate governance statement:

Lots of corporate-governance commentary on employees, which noted the benefits of staff training have yet to be realised in full:

The Kayes like to skip the occasional board meeting:

Would be useful to know more about the “effective procedures” to monitor the conflicts of interest.

A useful line on the group’s culture:

‘Tri for life’ is an organisation associated with director Sam Kaye.

4) Debt

Confirmation that the debt has all been paid off:

5) Director pay

Probably the most encouraging note in the accounts this year. The Kayes have waived their fees and the two other long-time directors have reduced their fees by 75%:

6) Employees

TAST’s employee stats showed good productivity improvements during 2018, but the ratios declined a fraction for 2019:

Revenue per employee was £43k versus £45k for 2018, while employees per outlet were 17.6 versus 16.9 for 2018.

I had hoped those 2018 stats would be maintained for 2019, although perhaps 2018 was a freak result and/or the figures are skewed by part-time workers. The average cost per employee was £17.7k, versus £18.3k for 2018.

Total staff costs remain at 41% of revenue. Was 36% in 2014.

7) Fixed assets

This accounting looks somewhat suspect:

A 10% straight-line reduction could be equivalent to a useful life of 10 years, which feels optimistic for restaurant fittings. Restaurant Group applies an equivalent useful life of 3-10 years.

A 5% straight-line reduction for computer equipment — indicating perhaps a useful life of 20 years — seems ridiculous.

Too late to bother with this bookkeeping policy now. But had I noticed the policy a few years ago, I may have questioned the accounting optimism — and perhaps considered other aspects of TAST where management were (in hindsight) too ambitious.

8) Goodwill

If you believe the accounting, two restaurants enjoy a total carrying value of £326k:

My blog post above calculates the market cap per restaurant to be £50k.

9) Inventories

The £11.4m of stock expensed through the P&L represented 26% of revenue — matching the proportion for the previous two years.

The level was 23% for 2016 — Brexit year — which indicates TAST has indeed lost some margin due to Brexit if (as I suspect) most stock is bought in from overseas.

The £871k of raw materials and consumables suggests TAST carries c28 days of stock.

10) Options

Oh dear — various subsidiary options were repurchased by the company for just £28:

I can’t be sure, but I believe those options explain why the holding company owns 53% of the main operating subsidiary:

The percentage was always 100% in previous reports. Not sure if the new auditor has applied a different calculation, or perhaps the rights issue last year has affected the percentage. Similar to the useful-life policy, not something to worry about unduly given the current questions over the group’s survival.

Option dilution is not a problem with the shares at 2p:

Options that can be exercised need the shares to rally to 31p.

11) Receivables

No problems here:

12) Payables

No problems here:

13) Related party transactions

Benja Properties was omitted from last year’s transactions but included this year:

14) IFRS 16

The adoption of IFRS 16 for 2020 will reduce profit by £1.3m:

IFRS 16 does not affect cash flow, and I will worry about the finer details should TAST ever get to publish its 2020 annual report.

Maynard

Tasty (TAST)

Statement re: Redundancies published 03 July 2020

Radical action — 32% of the workforce has been let go. The company also needs more cash. Here is the full text:

——————————————————————————————————————————-

“Further to the Company’s announcement on 26 June 2020 regarding the phased opening of a limited number of sites over the next few weeks, given the anticipated drop in footfall due to the continuing restrictions imposed as a result of COVID-19, the Board has come to the difficult decision that staff numbers need to be reduced accordingly. Consequently, some 284 staff members (representing approximately 32 per cent. of the total workforce) have been made redundant across our restaurants and Head Office. Clearly, this decision has been very difficult for everyone involved and throughout this process our priority has been to support those that have been affected.

The board of directors is exploring ways to minimise costs and to strengthen the balance sheet including investigating the possibility of new debt and / or equity capital and also discussing terms with landlords and trade creditors. Further announcements will be made as and when appropriate.”

——————————————————————————————————————————-

Would be interesting to see if “new debt” could indeed be taken on and on what terms. Not sure there will be great appetite for another equity raise. Oh dear.

Maynard

Tasty (TAST)

Paul Scott scuttlebutt published 07 August 2020

Investment blogger Paul Scott has visited Wildwood Bournemouth. “Very busy“:

———————————————————————————————————————————-

Pubs and restaurants seem to be seeing a surge in demand, thanks to the Eat Out to Help Out Govt discount scheme. Industry data suggests that sales were up 70.9% in the first 3 days of the scheme (food up 114.3%). I decided to mystery shop Wildwood, in Bournemouth, a pre-covid favourite of mine, on Weds earlier this week. I couldn’t believe how busy it was – packed downstairs, and a good smattering of groups upstairs too (which is usually empty).

I asked the waitress how business has been, she replied, “very busy, every day, since we re-opened on 18 July“. Isn’t that surprising. She said the Govt scheme has helped, but it was busy already. Bournemouth generally was busy with people at about 6pm, although being a seaside town, and the weather being pleasant, and people not going abroad, then perhaps those factors help. It looks very mixed anyway – central London is still almost deserted, but by the looks of it seaside/holiday towns are doing alright. I’m going to mystery shop Franco Manca for lunch today!

———————————————————————————————————————————-

Talking of Franco Manca, owner Fulham Shore issued this statement on 06 August 2020:

“Trading at the Group’s re-opened restaurants has started gradually, and the early signs in both businesses are promising. In the four weeks since 6 July 2020, like-for-like restaurant sales at reopened sites were approximately 72 per cent. of the equivalent weeks in the previous year.

The Group has shared approximately half the benefit of the new six month reduction in VAT on food with its customers. In addition, both Franco Manca and The Real Greek will be participating in the Government’s Eat Out to Help Out initiative, where customers will enjoy a 50 per cent. discount (up to £10 per person) when dining from Monday to Wednesday in August. Both these measures are expected to have a positive impact on the Group’s trading as sales rebuild to pre-COVID-19 levels.”

Like-for-likes (LFLs) down 28% does not seem catastrophic all things considered. Something to bear in mind is the adjustment to VAT and the government Eat Out to Help Out scheme. I am not sure how the LFL numbers will be affected by these initiatives. For example, FUL has shared half the VAT benefit with customers, implying the other half has benefited the company. So LFLs may be flattered a little by the subsidies.

Loungers, which operates a hybrid cafe/bar/restaurant chain, issued this statement on 05 August 2020:

“The Board is pleased to update on current trading having now re-opened all 165 sites in the estate, with the exception of Cosy Club in Leicester which opens this Friday. Like for like sales have been -1.7% over the period from 4 July, when our phased re-opening commenced, through to 2 August. Whilst these are still early days, we are encouraged by the initial strength of our trading performance to date and remain confident the Company will emerge strongly from this period.”

LFLs down just 1.7% is incredibly impressive.

All told, perhaps the dining-out sector has not died just yet. TAST’s next update should be interim results during September.

Maynard

Tasty (TAST)

Trading update published 18 August 2020

Nothing too surprising here given the circumstances. Management still warning that another equity placing could be needed. Here is the full text:

——————————————————————————————————————

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, announces the following update, further to the announcements made on 26 June and 3 July 2020.

The Board confirms that the process of significantly reducing the workforce by more than 30% is substantially complete.

The phased reopening schedule has continued, principally to take advantage of the Government’s ‘Eat Out to Help Out’ scheme and reduced VAT. The Board expects to have up to 48 sites trading in August, which will represent approximately 86% of the estate. Most of the remaining restaurants are not planned to re-open for the foreseeable future and some of the restaurants which are currently open may need to close again should they not reach expected trading levels.

The Company has experienced a positive level of sales this month to date, temporarily supported by the increase in people staying in the UK this summer, Government initiatives and pent up demand following the relaxation of lockdown restrictions since March, however, the Board expects future trading to remain challenging.

The Board remains extremely cautious regarding trading in September and is continuing to explore ways to minimise costs and to strengthen the balance sheet including the possibility of new debt and/or equity capital. Discussions are also continuing with landlords and trade creditors to reduce current and future liabilities. ——————————————————————————————————————

The workforce reduction was announced during July.

TAST’s websites say 36 (of 51) Wildwoods and 4 (of 5) dim-ts are currently trading:

So up to another 8 sites could open to get to the 48 mentioned in the RNS.

Reducing the workforce by 30% and the estate by 14% suggests staff per outlet has reduced by almost 20%, which could mean sales per outlet has dropped by almost 20% as well. Oh dear.

Fulham Shore issued this statement today (20 August 2020):

“The UK Government’s ‘Eat Out to Help Out’ scheme has proved to be beneficial both for UK diners and Fulham Shore. Trade in the first full fortnight in August was markedly up on the same period in the previous year, with the Group achieving one of its highest weekly turnover figures in the second week of ‘Eat Out to Help Out’, despite some of its restaurants still remaining closed.

Almost all of the Group’s employees are back off furlough and the Company is recruiting and training more restaurant staff at all levels.

Since 6 August 2020, the Company has re-opened two more The Real Greek restaurants and is planning to reopen another Franco Manca next week, next to the new Harrods store in Westfield London. This will take the Group restaurant numbers that have re-opened for trading up to 50 (out of 51) Franco Manca and 16 (out of 18) The Real Greek. This will leave the Company with three unopened sites in the City and West End of London, which will re-open when office tenants and theatregoers return. The Company also remains on track to open a new Franco Manca on The Cut, near to the Old Vic theatre and Waterloo Station in London, in mid-September.”

A markedly different tone to that of TAST. FUL is even taking on more staff and opening new sites.

Whether that difference justifies FUL’s market cap of £60m versus TAST’s £3m is hard to say.

Maynard

Tasty (TAST)

Bank Facility

Looks like the much needed radical action is underway, with talk of a CVA. Also, the threat of another equity raise may have diminished as Barclays is happy to lend further money. Here is the full text:

———————————————————————————

Further to the most recent trading update announced on 18 August 2020, Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, announces the following update.

In light of the continued economic uncertainty and the impact of COVID-19 related restrictions, the Company has secured a £1.25 million, four year term loan from its existing bankers, Barclays Bank plc (the “Facility”), in order to strengthen its balance sheet and provide additional working capital support. The Facility is available to be drawn down until 7 February 2021, however, draw down is restricted until the future of the Company is assured through restaurant closures and creditor arrangements. The Facility has a capital repayment holiday of 12 months and carries interest at a rate of 4.5% per annum over the Bank of England Base Rate, following draw down.

The Board of Tasty confirms that, whilst no decision has yet been made, it is continuing to work with its advisers, KPMG, to assess the potential impact of COVID-19 on the business and the various strategic options available to the Company, including a potential company voluntary arrangement. The Company will commence consensual negotiations with landlords and other creditors shortly and anticipates that this process will be completed by the end of November 2020. The Board believes that given the recently announced additional COVID-19 related regulations and the probability of future tighter restrictions in the near future, all potential options should continue to be explored but, with creditor assistance, a more formal procedure may be avoided.

The Company will make further announcements as appropriate.

———————————————————————————

Debt costs at 4.5% + Base Rate does not feel exorbitant, although the revised facility taken on during November 2018 charged between 2.5% and 4% + LIBOR. This latest debt facility is not available until the “future of the company is assured“, which presumably is not the case at present.

A CVA looks a possibility if the landlords do not agree to rent reductions. I suspect landlords generally have little choice at present other than to accept reduced terms. TAST co-chief exec Sam Kaye and his wider family own significant property investments and let certain sites to TAST. I would like to think the negotiations between TAST and the Kayes would be very consensual. The aim of completing all the landlord negotiations within a month also suggests landlords have little option but to accept new terms.

All told, TAST’s survival is still not guaranteed but the chance of surviving has improved somewhat.

Maynard