16 June 2020

By Maynard Paton

Results summary for Andrews Sykes (ASY):

- Creditable full-year figures that showed revenue down 2% and profit down 7% due to less extreme weather.

- The decision to furlough 50% of UK staff feels odd given management talks of “resilient” trading, kept company depots open during lockdown and has declared a final dividend.

- A commendable cash flow projection raises pandemic-profitability questions but suggests extra funding is not needed.

- An impressive second half ensured the accounts remained healthy with high margins and an appealing return on equity.

- A possible P/E of 12-14 and yield of 4.5% does not seem expensive if indeed ASY does “return to normal levels of trading” for 2021. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own ASY

- Results summary

- Covid-19, furloughed employees and declaring dividends

- ‘Going concern’ cash flow projection

- 2019 revenue, profit and dividend

- H1 vs H2 and Europe

- IFRS 16

- Financials

- Valuation

Event links, share data and disclosure

Event: Preliminary results and annual report for the twelve months to 31 December 2019 published 12 May 2020.

Price: 500p

Shares in issue: 42,174,359

Market capitalisation: £211m

Disclosure: Maynard owns shares in Andrews Sykes. This blog post contains SharePad affiliate links.

Why I own ASY

- Supplies air conditioners, portable heaters and industrial pumps for hire, with success based on a prompt 24/7 service, high-quality rental fleet and commercial-only customer base.

- Accounts regularly showcase high margins, generous cash flow, net cash and attractive returns on equity.

- Chairman and family are 90%/£189m shareholders and ensure management focuses on “long-term shareholder value creation”.

Further reading: My ASY Buy report | All my ASY posts | ASY website

Results summary

Covid-19, furloughed employees and declaring dividends

- A late-March trading update had already hinted ASY may have escaped the worst effects of the pandemic:

“Compared to many sectors of the economy, such as hospitality and retail, the impact [of Covid-19] on the Company to date has not been severe…”

- The management narrative within this 2019 statement used the adjective “resilient”:

“Andrews Sykes Group plc (the “group”) remains resilient as sectors in which we trade have shown continuous demand whilst facing an unprecedented challenge in the form of the coronavirus pandemic.

“Certain product lines are more resilient than others and we are experiencing an increase in demand in certain sectors, notably healthcare, emergency temporary hires to cover the breakdown of customer equipment and the hire of dewatering equipment in the UAE to enable construction work to continue.”

- The business remained open during the lockdown and the very early impact did not appear catastrophic:

“In the UK we have temporarily closed some of our smaller depots, introduced social distancing measures in our larger depots and embraced at home working employees.

The impact on the business as of the end of March has been limited with trading levels close to expectation.”

- The company’s blog suggests ASY has been busy supplying equipment to hospitals:

“One hospital contacted [ASY] on Good Friday in the hope that we could provide some cooling relief to staff working on a COVID-contaminated ward. A regional expert arrived on site almost immediately to ascertain the size of the areas the estates team intended to address, pre-empting the creation of specific zones which staff could visit to cool down. This was handled with a great deal of urgency and the delivery of multiple Polar Wind portable air conditioning units followed later that same afternoon.”

- Given ASY’s “resilient” trading, I was surprised the results small-print revealed half of the domestic workforce had been furloughed:

“In the UK, approximately 50% of our employees are furloughed.”

- The 2019 results made no reference to ASY receiving UK government help.

- However, many European ASY staff are seemingly receiving state support:

“In France, Italy, Belgium and Luxembourg we are currently working with significantly reduced staff levels, with the most of our staff enlisted to the appropriate government employment retention schemes.”

- ASY declared a slightly reduced final dividend within these results.

- This dividend feels questionable to me given the apparent receipt of overseas government assistance.

- I suppose ASY could argue the final dividend relates to trading during the July-December 2019 period — and before Covid-19.

- Mind you, ASY is projecting further dividend payments for later this year:

“For the purposes of the cash forecast only, we have assumed that a normal level of dividends will be resumed in November 2020.”

- I can only trust ASY stops collecting any government subsidies before making further payouts.

‘Going concern’ cash flow projection

- ASY commendably included a cash flow projection within the ‘going concern’ small print.

- Management described this “bottom-up”… cash flow forecast for the 24 months ending 31 December 2021 as “cautiously realistic”.

- The key estimate was:

“[T]he group’s net cash outflow in the nine months ending 31 December 2020 is forecast to be approximately £10 million.”

- The outflow calculation included dividends:

“For the purposes of the cash forecast only, we have assumed that a normal level of dividends will be resumed in November 2020.”

- The payment of the 2019 final dividend will cost £4.4m.

- If indeed a “a normal level of dividends will be resumed in November 2020”, then the November 2020 first-half payment will cost £5.0m.

- The net cash outflow before dividends could therefore be £0.6m (i.e. the £10m projection less dividends of £9.4m).

- That calculation implies the business may not be profitable or cash-generative during the nine months to 31 December 2020.

- I can’t fathom why a cash-flow forecast predicting a breakeven-ish business performance would also include dividend payments of £10m.

- Maybe I have misinterpreted the numbers. ASY claims the business should be profitable this year:

“Group turnover for the 12 months ending 31 December 2020 is forecast to be lower than 2019. Operating profit is therefore consequently likely to reduce, however the group still expects to produce a profit for 2020.”

- I suppose the business could report a profit but not generate much cash. ASY admitted:

“Our cash flow forecast assumes that cash collections will reduce over the next nine months as customers take longer to settle their debts.”

- Or perhaps the cash flow forecast was not meant to be a “cautiously realistic” projection to help guess 2020 earnings — but instead was purely a way of showing the balance sheet would not require extra funding.

- ASY implied its balance sheet would carry net cash of £17m at the 2020 year-end following the projected £10m cash outflow.

- ASY added the balance sheet would remain cash-positive were the business to suffer a bad 2021:

“Even in an extreme scenario and this trend continued throughout 2021 resulting in an additional cash outflow of c£12 million, the group would still have cash reserves* of c£5 million at 31 December 2021”

- ASY does in fact believe 2021 may not be so bad:

“In 2021 we expect to return to normal levels of trading.”

- I can only really conclude the following from the projection small-print:

- The balance sheet should not require extra funding, and;

- Management aims to continue paying dividends.

2019 revenue, profit and dividend

- ASY’s comments on Covid-19 and the group’s prospects for 2020 naturally overshadowed these 2019 figures.

- Subdued first-half results due to a “milder winter” that provided “less opportunities for… heating and boiler hire products” meant the full-year outcome was never going to set any records.

- In the event, ASY reported a creditable performance:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (£k) | 60,058 | 65,389 | 71,300 | 78,563 | 77,246 |

| Operating profit (£k) | 13,208 | 15,816 | 17,589 | 20,681 | 19,268 |

| Finance income (£k) | 159 | 1,725 | (304) | 364 | (738) |

| Other items (£k) | - | - | - | - | - |

| Pre-tax profit (£k) | 13,367 | 17,541 | 17,285 | 21,045 | 18,560 |

| Earnings per share (p) | 25.6 | 34.3 | 33.4 | 40.4 | 35.6 |

| Dividend per share (p) | 23.8 | 23.8 | 23.8 | 23.8 | 22.0 |

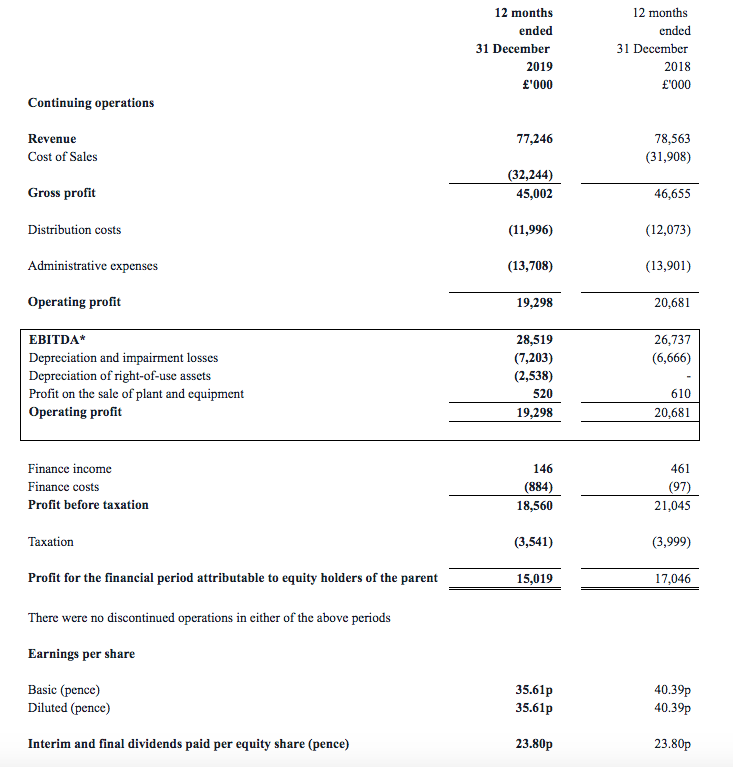

- Revenue fell 2% while reported operating profit dropped 7%.

- ASY’s profit numbers were distorted slightly by IFRS 16, the new accounting standard that treats lease costs as a mix of depreciation and interest.

- Operating profit would have declined by 8% on a consistent non-IFRS 16 basis.

- The 2019 performance was all the more satisfactory given the comparable year was bolstered by a scramble for ASY’s heaters during heavy snow and then for ASY’s air conditioners during the heatwave.

- ASY’s concerns about Covid-19 prompted the final dividend to be reduced by 12% to 10.5p per share to give a full-year payout of 22.4p per share.

- The annual dividend had been 23.9p per share since 2015.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

H1 vs H2 and Europe

- ASY’s second half was very impressive:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (£k) | 37,815 | 40,748 | 78,563 | 34,974 | 42,272 | 77,246 | |

| Operating profit (£k) | 9,280 | 11,401 | 20,681 | 6,918 | 12,380 | 19,298 |

- H2 revenue and profit gained 4% and 9% respectively.

- The H2 2019 performance set a new H2 record — despite the comparable H2 2018 enjoying bumper demand for air conditioners during that year’s heatwave.

- ASY explained the improved H2:

“The wet weather in the final quarter enabled the pump hire business to recover after a slow start to the year and the results of our heating business were also better than expected.

This [Middle East] result was driven by several large projects in the region including the 2020 Expo which is planned to be held in Dubai.”

- ASY also cited a “long hot summer” in Europe.

- The annual report small-print reported encouraging performances throughout Europe:

- The Netherlands: “performed well“;

- Belgium: “strong performance“;

- Luxembourg: “produced growth“;

- Italy: “another record result“;

- France: “a region of potential growth“, and;

- Switzerland: “another improved performance“.

- During H2, UK revenue was flat, European revenue gained 7% while Middle Eastern revenue advanced 19%.

- Since 2014, annual overseas revenue has jumped 104% while UK revenue has climbed only 11%.

- Group revenue is now 59% represented by the UK, 24% represented by Europe and 17% represented by the Middle East.

- Expansion continues in France, with a depot opened in Nantes last month and a depot in Toulouse opened during January.

IFRS 16

- ASY’s financials were affected by the introduction of IFRS 16.

- IFRS 16 dictates how companies should recognise, measure, present and disclose operating leases within their accounts.

- Before IFRS 16, lease costs were identified as an individual operating expense.

- Under IFRS 16, lease costs are charged mostly through a mix of depreciation on ‘right-of-use’ assets and interest on ‘right-of-use’ leases.

- The ‘right-of-use’ assets reflect the ‘fair value’ of the leases while the ‘right-of-use’ leases represent the total future lease obligation discounted into today’s money.

- If the value of the ‘right-of-use’ assets is much lower than the value of the ‘right-of-use’ leases, then the company could have locked itself into expensive/onerous lease agreements.

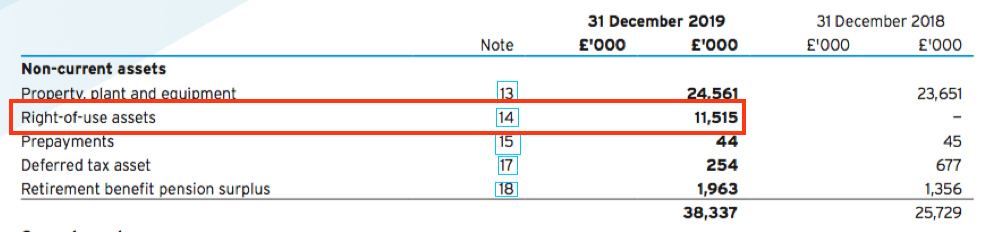

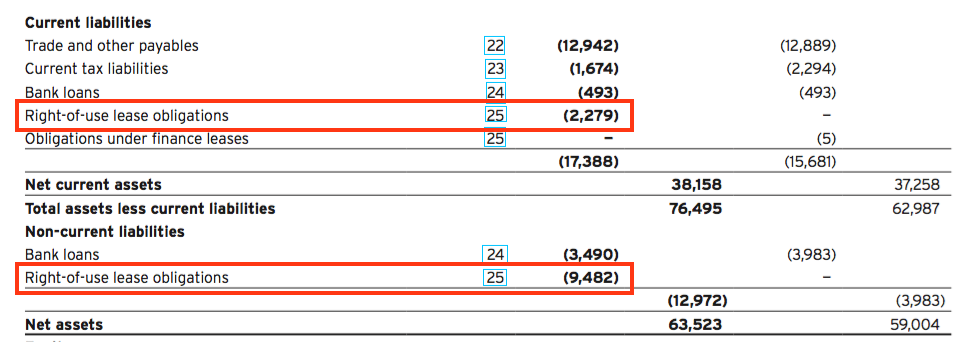

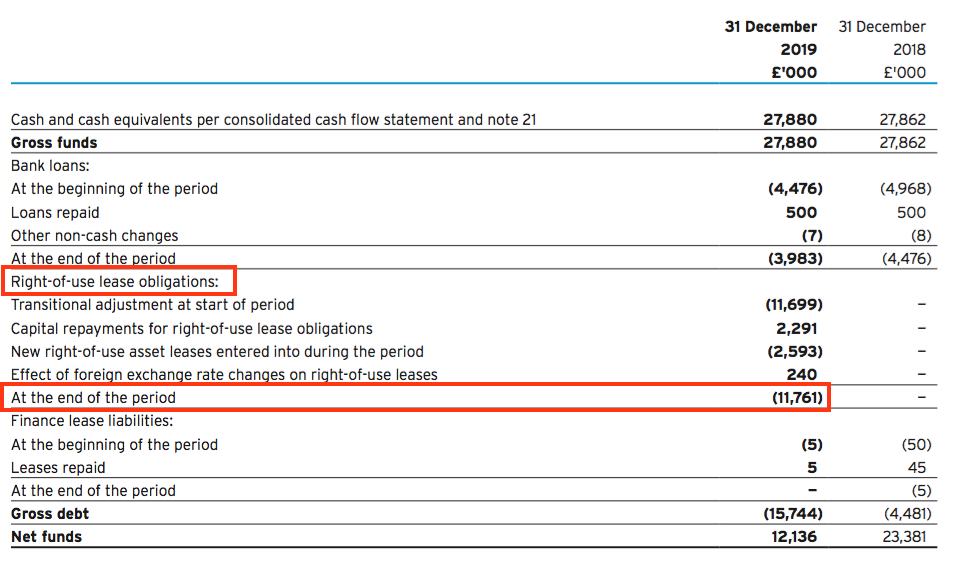

- ASY’s balance sheet shows right-of-use assets of £11.5m and ‘right-of-use’ leases of £11.7m:

- The ‘right-of-use’ leases are classified as financial obligations.

- As such, ASY must subtract lease obligations when calculating net funds:

- I ignore lease obligations for net cash calculations, and therefore my version of net cash is £24m.

- ASY’s leases relate mostly to property rents for depots.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Financials

- ASY’s accounts remain in good shape.

- Despite the lower profitability for 2019, margins and returns on equity continue to be attractive:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating margin (%) | 22.0 | 24.2 | 24.7 | 26.3 | 24.3 |

| Return on average equity (%) | 25.2 | 31.5 | 27.8 | 30.3 | 24.5 |

- The full-year operating margin has actually topped 20% since 2002.

- Before central costs, the main UK and European divisions reported a combined 28% operating margin for 2019. The Middle Eastern operation delivered a 24% margin.

- My return on equity calculation in the table above does not adjust for ASY’s £24m net cash position.

- During the five years to 2019, ASY has lifted earnings by £5.7m and increased its shareholder equity by £21.4m. The resultant incremental return on equity is a super 27%.

- Earnings of £15m during 2019 converted into free cash flow of £11m after nearly £6m was invested into extra working capital:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit (£k) | 13,208 | 15,816 | 17,589 | 20,681 | 19,298 |

| Depreciation and amortisation (£k) | 4,959 | 5,310 | 5,917 | 6,666 | 7,203 |

| Net capital expenditure (£k) | (4,523) | (4,719) | (4,929) | (6,198) | (5,522) |

| Working-capital movement (£k) | (3,090) | (2,157) | (1,155) | (4,292) | (5,592) |

| Net cash (£k) | 14,558 | 17,673 | 20,293 | 23,381 | 23,897 |

- ASY’s working capital has absorbed £16m since 2015:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit (£k) | 13,208 | 15,816 | 17,589 | 20,681 | 19,298 |

| Working-capital movements | |||||

| Stocks (£k) | (1,024) | (2,251) | (1,022) | (2,682) | (3,834) |

| Trade and other receivables (£k) | (2,196) | (1,876) | 563 | (2,139) | (1,818) |

| Trade and other payables (£k) | 139 | 1,970 | (696) | 529 | 60 |

| Total (£k) | (3,081) | (2,157) | (1,155) | (4,292) | (5,592) |

- The £16m absorbed is equivalent to a sizeable 19% of aggregate operating profit.

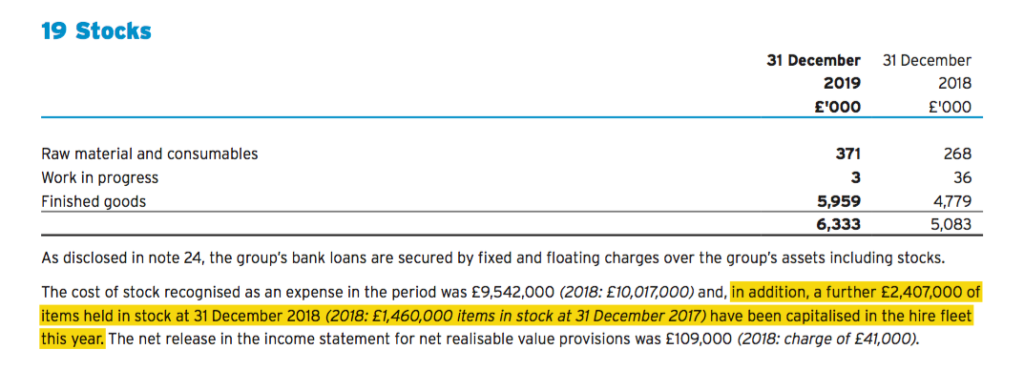

- Note that ASY’s books are complicated by the company acquiring stock and then capitalising a proportion of that stock into the hire fleet:

- Such stock-to-fixed-asset transfers are unusual, but presumably reflect ASY offering for hire any equipment that could not be sold direct.

- During 2017, 2018 and 2019, stock with an aggregate £6m value was re-classified into the hire fleet.

- This £6m is arguably capital expenditure rather than working-capital investment.

- The table below adjusts the working-capital movements and capital expenditure for the £6m:

| Year to 31 December | 2016 | 2017 | 2018 | Total |

| Operating profit (£k) | 15,815 | 17,589 | 20,681 | 54,086 |

| Depreciation (£k) | 5,310 | 5,917 | 6,666 | 17,893 |

| Working-capital change (£K) | (2,157) | (1,155) | (4,292) | (7,604) |

| Stock transferred (£k) | 2,156 | 1,460 | 2,407 | 6,023 |

| Adjusted work-cap movement (£k) | (1) | 305 | (1,885) | (1,581) |

| Net capital expenditure (£k) | (4,719) | (4,929) | (6,198) | (15,846) |

| Stock transferred (£k) | (2,156) | (1,460) | (2,407) | (6,023) |

| Adjusted net capex (£k) | (6,875) | (6,389) | (8,605) | (21,869) |

- ‘Underlying’ working capital absorbed cash of only £1.6m during those three years.

- ‘Underlying’ capital expenditure came to £22m — £4m more than the associated depreciation charge.

- That £4m difference is not outrageous given operating profit was £54m during the same three years.

- Free cash flow of £10.8m for 2019 funded dividends of £10m, reduced debt by £0.5m and added £0.3m to the bank balance.

- Cash finished the year at £27.9m while bank debt was £4.0m.

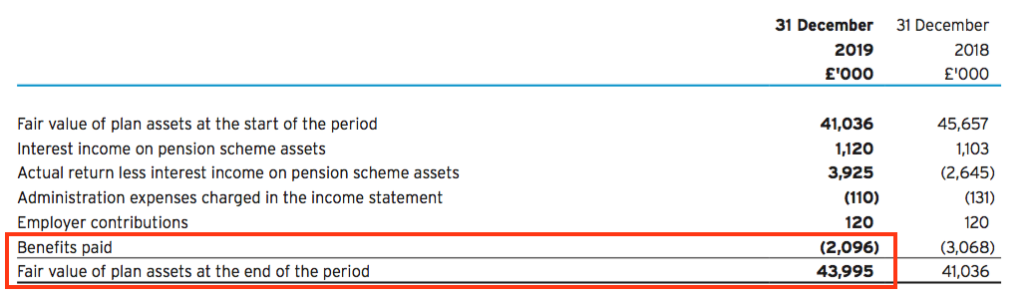

- ASY’s defined-benefit pension scheme continues to enjoy an accounting surplus. A deficit was last reported during 2007.

- I am pleased the benefits paid to the scheme’s members have reduced from £3.1m to £2.1m:

- Paying benefits of £2.1m from scheme assets of £44.0m requires an annual investment return of 4.8%.

- I am not convinced employer contributions of £120k a year are enough to sustain benefits of £2.1m while preventing the erosion of the £44.0m scheme assets.

- A formal pension funding review is underway and may prompt additional company contributions:

“As explained in note 18 to the financial statements, a triennial funding valuation for the group defined benefit pension scheme is currently being prepared by the pension scheme trustees as at 31 December 2019. Management has received an estimate of the deficit as at that date and it has been assumed that this will be agreed and paid to the pension scheme by 31 December 2020.”

Valuation

- ASY revealed a £4.6m operating profit had been recorded during the three months to 31 March 2020. Net cash increased by £3.3m during the quarter.

- ASY’s profitability during the remainder of 2020 sadly remains anyone’s guess.

- As a guide, operating profit less IFRS 16 interest costs for 2019 was £18.8m.

- Applying tax at 19% gives earnings of 36.1p per share.

- ASY remains a tightly held share with a minimal free float and wide bid-offer spread.

- The 100-year-old chairman and his family own almost 90% of ASY, leaving approximately 10% for everybody else.

- A 500p mid-price values ASY at £211m and the free float at £22m.

- Subtract the £24m net cash position from the market cap and the underlying business could be valued at approximately £187m or 443p per share.

- That said, the aforementioned cash outflow forecast of £10m for 2020 may well mean the cash position is not ‘surplus to requirements’.

- Depending on your view of the cash position, the trailing P/E could be 12 or 14 or somewhere in between based on my earnings guess.

- My sums could be refined for ASY’s pension scheme and the capital expenditure not reflected by the depreciation charge.

- However, such alterations would be rather superfluous given ASY’s pandemic performance may create more significant profit issues.

- If in fact ASY does “return to normal levels of trading” during 2021 and earnings match those of 2019, then the 12-14x rating may not seem expensive.

- The trailing 22.4p per share dividend meanwhile supplies a 4.5% income at 500p.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Andrews Sykes (ASY)

Publication of 2019 annual report

Here are the points of interest beyond those mentioned in the blog post above.

1) Additional management remarks

ASY’s annual reports always contain extra management commentary that provide a little more operational detail:

The additional text also explains the group’s competitive advantage:

For 2019, the extra text included a Covid-19 impact statement:

2) Going concern

The full going concern note referred to in the blog post above is shown below, with the key lines highlighted:

3) Risks

The Risk section was not changed from 2018 and the strategic risks remain the same:

The creditable performance for 2019 following the less extreme UK weather underlines the notion that the impact of the weather is indeed being reduced.

4) Section 172

ASY’s new Section 172 report included a few interesting snippets:

“Business critical solutions” sounds as if customers will pay a premium for prompt services:

I like the organic growth priority. The reference to “key account customers” implies regular customers — so perhaps retention levels are good.

More on the group’s ‘service’ competitive advantage:

The ‘relationship agreement’ with the chairman is worth further investigation — one risk with ASY is the chairman deciding to delist the shares. I don’t know whether these agreements include a standard clause to prevent low-ball offers.

5) Audit report

A new section from the auditor for 2019 about macro-economic uncertainties:

Materiality is a standard 5% of pre-tax profit. Scope is a reasonable 88% of profit:

A new audit matters chart was presented for 2019:

Four new/revised matters were included.

The chart for 2018 is below:

No matters changed quadrants for 2019.

The “uncollected hire revenue” matter replaces the “revenue recognition” matter and concerns the potential for fudging the figures to earn bonuses:

New for 2019 — understandable the auditors wanted a closer look at IFRS 16:

Revised for 2019 — the auditors now pay greater attention to the pension scheme’s liabilities rather than the whole scheme.

Brand new ‘audit work performed’ details for 2019:

6) Oldest director of a quoted company?

Yay, the chairman has celebrated his 100th birthday!

7) Director pay

The MD is not underpaid, but was paid more (in excess of £500k) during 2017 and 2018 than in 2019. Presumably his bonus for 2019 was reduced.

8) Employees

Nothing too concerning here:

Revenue per employee fell from £137k to £131k, but the decrease is not surprising given the revenue dip. The general trend is up — the figure bobbed between £111k and £125k between 2010 and 2016.

Average cost per employee was £36k — the same as 2018. Employee costs as a proportion of revenue was 28% versus 27% for 2018 and 27%-29% between 2013 and 2017.

9) Options

ASY operates quite well without an option scheme:

10) KPIs

ASY commendably maintains revenue per employee as a KPI:

EBITDA and Cash reserves were introduced as KPIs for 2019:

11) IFRS 16 adjustment

Confirmation the IFRS 16 adjustment made little difference to reported earnings:

12) Segments

Confirmation of the differing profitability within the group:

Hire & sales Europe enjoys a 28% margin, while Installation and maintenance scrapes a 6% margin.

13) Revenue split

Group revenue would have been almost unchanged had equipment sales not decreased by £1m:

14) Operational expenses

ASY still incurs lease costs under the pre-IFRS 16 method:

The £1m or so charged for 2019 relates to leases with less than a year to run and/or an aggregation of trivial leases.

15) Property, plant and equipment

An interesting note:

The current hire fleet was acquired originally for £65m but has been depreciated to £18m. I get the impression that certain hire equipment can last a long time. The £6.4m depreciation charge represented 10% of the average £63.3m historical cost of the hire assets for 2019, so can air conditioners and so on last for 10 years?

The depreciation policy refers to annual write-down rates of 10%-33% as well as “residual values” — and I’m sure a five-year-old air conditioner has some value, as perhaps a 10-year-old one does, too.

ASY reports a small but regular profit selling old equipment each year, so the residual-value accounting seems straight to me.

Also worth keeping an eye on Hire revenue versus the cost of the Equipment for hire. An adverse trend could signal lower utilisation rates.

For 2019, Hire revenue of £67.4m was 1.07x the £63.3m average historical cost of the hire equipment. For 2012, the multiplier was 1.22x. So a deterioration — but inspection of Companies House and the main UK subsidiary accounts reveals a 1.14x multiplier versus 1.09x for 2012. The deterioration then is due to immature overseas territories — where equipment is perhaps not currently utilised as much as in the UK.

16) Cash

Ah ha — this may explain why ASY operates with a lot of cash:

Some cash is ring fenced. The accounting notes sadly do not disclose how much is ring fenced, but the ring fenced money is held in deposit accounts and deposit accounts represent a majority of the cash position:

I can’t imagine business customers pay deposits in advance for hiring equipment — the trade debtors note

(point 18) suggest customers pay after the hire period.

What I am now sure about is the cash position is not entirely ‘surplus to requirements’ given the element of ring-fenced money.

17) Stocks

Confirmation of the transfer from stock to fixed assets:

I am confused about the “cost of stock recognised as an expense” of £9.5m. I can’t see this expense relating to Hire revenue, but point 13 above shows Sales revenue of less than £6m and total non-Hire revenue of £10m. Therefore these non-Hire operations do not seem to make much/any money given the stock expense.

Also, carrying stock of £6m versus “cost of stock recognised as an expense” of £9.5m suggests stock takes a lengthy 7.5 months to sell.

18) Trade debtors

No real issues here:

Net trade debtors of £18.9m represent a not insignificant 24% of revenue, but within the 21%-26% range seen during the previous ten years. The £9.6m overdue trade debtors represent 51% of total trade debtors.

This overdue percentage has come in between 48% and 51% for the previous six years. Trading in the Middle East often leads to payment delays:

Interesting to see the expected credit loss rate for trade debtors overdue for 0-3 months and 3-6 months reduce:

About a third of net trade debtors are 0-3 months overdue — in line with past years.

19) Trade and other payables

This note might shed light on the ring-fenced cash in point 16 above:

Deferred income may represent upfront customer payments for services ASY has not yet provided — i.e. deposits for equipment hire?

20) Debt

No worries here:

The £3m payment to clear the loan should not be a problem. The 2% rate charged is low and the £88k interest cost confirms the low rate:

21) Pension scheme

The pension scheme continues to invest in a mix of shares, bonds and gilts:

The £120k contributions just cover the scheme’s admin costs:

So the scheme’s assets of £44m require an annual return of 4.8% (or more) to pay the yearly benefits without risk of capital erosion. I reckon contributions will have to increase, especially given the scheme’s weighting to bonds and gilts.

For now the contributions stay at £120k a year:

22) Lease obligations

This note indicates ASY is not tied to lengthy operating leases:

My basic sums suggest the typical lease has 5.1 years to run (£13.9m/£2.7m).

Maynard

Andrews Sykes (ASY)

Special Dividend published 24 July 2020

I was not expecting this — a special dividend equivalent to almost a ‘normal’ full-year payout. Here is the full text:

———————————————————————————————————–

The board of Andrews Sykes (the “Board”) is pleased to announce that it has approved the payment of a special interim dividend of approximately £10 million or 23.7 pence per Ordinary Share (the “Special Dividend”).

As at 22 July 2020, the Company had net cash reserves* of approximately £29.9 million. The Board has assessed the Company’s ongoing cash requirements under a range of forecast scenarios and has concluded that, as a result of the Company’s expected robust cash generation, a portion of these cash reserves is surplus to the Company’s requirements. The Board has, therefore, decided to return such surplus capital to Andrews Sykes shareholders by way of the Special Dividend.

The Company intends to pay the Special Dividend on 28 August 2020 to Andrews Sykes shareholders on the register on 7 August 2020. The Ordinary Shares will be marked ex dividend on 6 August 2020. The Special Dividend will be funded from the Company’s existing cash balances.

* defined as cash at bank less bank loans before IFRS 16 right-of-use lease obligations

———————————————————————————————————–

Net cash of £29.9m compares to £23.9m at the end of 2019. A £4.4m final dividend was paid during June, so free cash generation for the first 29 weeks of 2020 appears to be £29.9m less £23.9m plus £4.4m = £10.4m.

£10.4m seems amazing for the first 29 weeks of 2020. For perspective, full-year free cash flow was £10.8m during 2019 and £13.0m during both 2018 and 2017.

A special dividend did not look on the cards when the 2019 results were released in May. The statement gave a cash flow forecast that indicated: “For the purposes of the cash forecast only, we have assumed that a normal level of dividends will be resumed in November 2020.”

Now shareholders will receive a (23.7p per share) special payout during August that in fact almost matches the ‘normal’ (23.8p per share) yearly level of dividends.

What has happened?

I am hopeful ASY has simply enjoyed bumper trading. The company’s blog suggests the firm has been busy.

Maybe ASY has become more efficient, too, given the 2019 results admitted 50% of its UK staff had been furloughed. The company may have inadvertently discovered it can operate with fewer employees.

I must admit, I am not comfortable with ASY paying dividends while furloughing staff. I can only trust any government money received has been handed back.

The alternative view is the 100-year-old chairman — and 86% ASY shareholder — is short on funds. He owns hotels in Miami, which may not be doing well during the pandemic.

The chairman has in the past adopted an extravagant lifestyle:

“Its most chronicled resident has long been billionaire Jacques Gaston “Tony” Murray, a World War II hero who later made a fortune in fire extinguishers. For years, Murray hosted the jet-set bash of the summer, attended by such glitterati as Ivana Trump, Naomi Campbell, Elton John and Prince Andrew. Entertainers such as Natalie Cole crooned poolside, and the tabloids provided breathless coverage. Alas, the fabulous fete is history. The centenarian’s age, not the coronavirus, is the reason.”

Bear in mind ASY declared dividends of 33.6p per share during 2008, when earnings were 24.9p per share, the business operated with net debt and the global economy was rather shaky. I get the impression the chairman may have extracted a chunky ASY dividend back then to shore up his other business interests. No/low dividends were then paid during 2009, 2010, 2011 and 2012.

Interim results in September ought to shed light on what has occurred. Bumper trading, or hoarding cash to create extra funds for the chairman?

Maynard