23 October 2020

By Maynard Paton

Results summary for FW Thorpe (TFW):

- “Creditable” figures that revealed second-half profit sliding 17% due to the lockdown.

- A 2% final dividend lift, cash reserves of £63m plus the commendable funding of furloughed staff did not imply imminent financial difficulties.

- The SmartScan light-monitoring system provides exciting potential, with sales up 18% to represent 23% of total revenue.

- Talk of a “global recession” and a “downturn in orders” suggests trading during 2021 will be challenging.

- A P/E of 21-25 seems generous but may reflect the ‘pandemic-proof’ balance sheet, SmartScan growth and/or resilient profit history. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own TFW

- Results summary

- Coping with Covid-19

- Revenue, profit and dividend

- Thorlux and SmartScan

- Lightronics and Famostar

- Other divisions

- LEDs

- Financials

- Valuation

Event links, share data and disclosure

Event: Final results and annual report for the twelve months to 30 June 2020 published 01 October 2020

Price: 290p

Shares in issue: 116,593,336

Market capitalisation: £337m

Disclosure: Maynard owns shares in FW Thorpe. This blog post contains SharePad affiliate links.

Why I own TFW

- Manufactures commercial lighting systems with a long-established reputation for high product quality, leading technical innovation and tip-top customer service.

- Board led by a veteran executive and assisted by family non-execs that steward a 50%-plus/£169m-plus shareholding.

- Conservative accounts showcase ‘pandemic-proof’ cash reserves, resilient profit history and confident dividend advance.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary:

Coping with Covid-19

- Interim results from March had already signalled a rather uncertain finish to these FY 2020 figures:

“At the time of writing, the [pandemic] situation is dynamic and uncertain, but we continue to support our customers where practical, whilst being mindful of employee wellbeing and government guidance. It is highly likely however that Group companies will see considerable disruption to delivery schedules due to customers’ and government containment actions, for at least the next few months. The extent of this disruption and the period over which the impact is felt, cannot be estimated at this time.”

- However, those March interims also stated:

“We feel our robust balance sheet is structured more than adequately to deliver an increased interim dividend of 1.46p (Interim 2019: 1.43p) for the six months to 31 December 2019.”

- The 2% interim dividend lift suggested TFW would not face a catastrophic lockdown.

- These FY 2020 results confirmed the lockdown had prompted some employees to be furloughed:

“No factory staff have been on furlough since early June.”

- However, TFW commendably did not rely on government handouts:

“ The Board decided not to apply for any government support for furloughed employees during lockdown; this impacted operating costs by £0.6m, as the Group paid all employees normal salary whilst they were not working. This decision was duly considered and leaves the Group free of debt to external supporters, protects its reputation, and gives management ongoing freedom to make choices for the good of the business and its shareholders.”

- The £0.6m spent in lieu of government support represented 2% of the total £28m paid as staff wages for the year.

- The outlook for the current year was very mixed.

- Although recent trading has been supported by a backlog of orders…

“Whilst the Group’s present order book is healthy and daily orders are good, this is partly attributable to an amount of pre-COVID work carried forward and to pent-up demand in the market”

- …the talk further out was gloomy:

“It seems inevitable, however, that there will be a global recession, and that the UK, against a backdrop of Brexit uncertainly and the intense lockdown enforced by the Government, could be affected worse than many countries.

It is difficult to predict anything other than a downturn in orders at the end of the 2020 calendar year.”

- A fire at the Dutch Lightronics subsidiary during September has not helped matters. At least TFW claimed the disruption would not cause a “significant impact” on the division.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue, profit and dividend

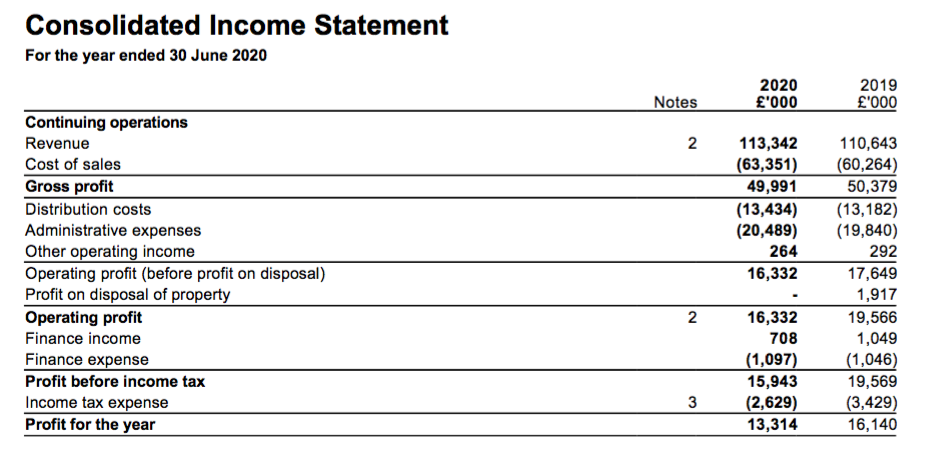

- TFW described the FY 2020 performance as a “creditable result”.

- Revenue gained 2% to set an all-time high, while profit fell 7% to a level last seen during 2016:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 88,946 | 105,448 | 109,614 | 110,643 | 113,342 |

| Operating profit (£k) | 15,959 | 18,189 | 19,225 | 17,357 | 16,068 |

| Net finance income (£k) | 75 | (249) | 101 | 3 | (389) |

| Other items (£k) | 235 | 411 | 241 | 2,209 | 264 |

| Pre-tax profit (£k) | 16,269 | 18,351 | 19,567 | 19,569 | 15,493 |

| Earnings per share (p) | 11.24 | 12.54 | 13.91 | 13.91 | 11.45 |

| Dividend per share (p) | 4.05 | 4.90 | 5.40 | 5.53 | 5.66 |

| Special dividend per share (p) | 2.0 | - | - | - | - |

- Once again TFW said its “robust” balance sheet allowed a dividend improvement, with the final payout lifted 2%.

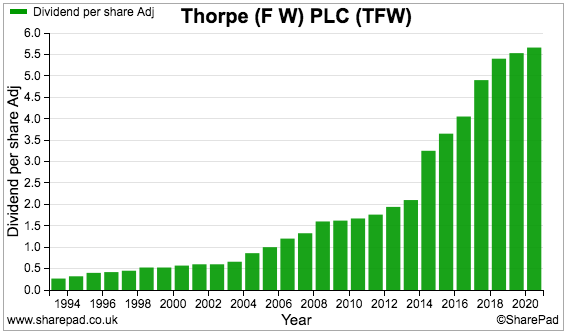

- TFW has now raised its dividend for 18 consecutive years:

- Raising the dividend through both the banking crash and the pandemic is some achievement.

- The lockdown impact was reflected within TFW’s second half, during which profit dived 17%:

| Group | H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | |

| Revenue (£k) | 52,669 | 57,974 | 110,643 | 57,412 | 55,930 | 113,342 | |

| Operating profit (£k) | 7,019 | 10,338 | 17,357 | 7,489 | 8,579 | 16,068 |

- The quote below is encouraging. TFW remained profitable during the lockdown:

“During each of the worst months — in March, April and May — the Group still returned an operating profit. Inevitably, however, profit in those months was much reduced, dampening the year-end result, which, until the COVID pandemic, the Board had expected to be an improvement on the previous year.”

- TFW’s main division, Thorlux, suffered a deeper H2 profit slump than the rest of the group:

| Thorlux | H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | |

| Revenue (£k) | 28,442 | 33,862 | 62,304 | 32,363 | 33,252 | 65,615 | |

| Operating profit (£k) | 4,659 | 6,919 | 11,578 | 4,839 | 5,311 | 10,150 |

- Thorlux’s H2 profit fell 23%.

- Although Thorlux delivered a respectable-in-the-circumstances 16% H2 margin, the previous five years witnessed H2 margins of 20% or more.

- As well as the lockdown, “some major contracts” that had “attracted lower margins” held back Thorlux’s profitability.

- Other parts of the group — covering Dutch subsidiaries Lightronics and Famostar alongside various smaller UK operations — witnessed their collective H2 profit slide only 4%:

| Non-Thorlux | H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | |

| Revenue (£k) | 24,227 | 24,112 | 48,339 | 25,049 | 22,678 | 47,727 | |

| Operating profit (£k) | 2,360 | 3,419 | 5,779 | 2,650 | 3,268 | 5,918 |

Thorlux and SmartScan

- Thorlux manufactures a range of commercial lighting equipment as the video below shows:

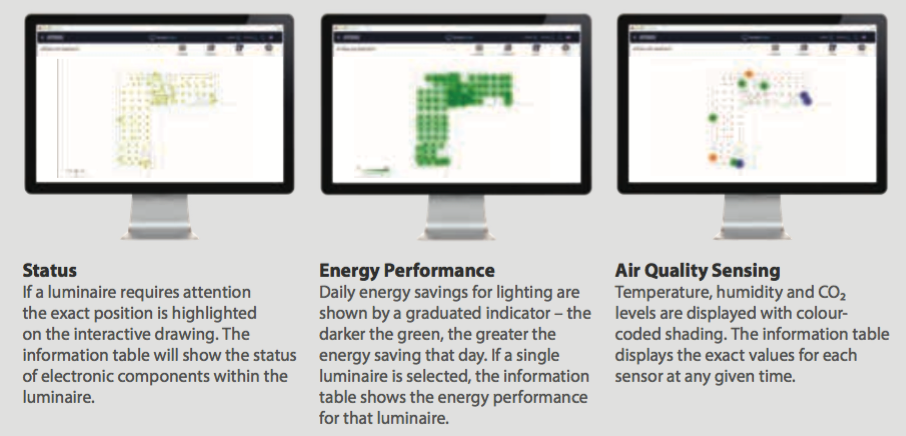

- Thorlux’s most exciting product is not actually a light, but a lighting control system called SmartScan.

- SmartScan provides customers with energy reports, emergency lighting tests, “occupancy profiling” information and even air-quality data:

- More features were added last year, including “vehicle activity monitoring”:

“This [SmartScan] solution has been developed further this year, outside pure lighting controls technology, by integrating new sensor technology such as dock usage and vehicle activity monitoring. Some third party technologies have also been included to enable mains electricity usage monitoring and solar photovoltaic generation data, all reporting back to the end user via the SmartScan website.”

- Clearly the SmartScan service is no longer just about controlling lights. The annual report talked of “Built Environment Analytics”:

“Working closely with a particular client, Thorlux has taken this a step further and introduced the provision for Built Environment Analytics (BEA). Built Environment Analytics was created for building tenants, to give them a greater understanding of how their facility performs in operation.”

- Customers seem to like SmartScan. The annual report disclosed product revenue gained 18% to almost £26m during the year.

- Launched only in 2016, SmartScan has become an increasingly significant source of revenue:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| SmartScan revenue (£k) | - | 7,000 | 14,000 | 22,000 | 25,900 |

| Proportion of Group revenue | - | 7% | 13% | 20% | 23% |

| Proportion of Thorlux revenue | - | 11% | 22% | 35% | 39% |

- This remark from the annual report is important:

“Development work was undertaken in-house.”

- Perhaps TFW’s first-class lighting products will be complemented by equally first-class building-monitoring services, the revenue from which ought to be recurring and hopefully quite predictable.

- Wishful thinking perhaps, but ongoing SmartScan success could lead to TFW becoming more of an IT/data/analytics business than a lighting manufacturer.

- Emphasising the importance of SmartScan, four pages of the annual report were devoted to the product’s new features:

Lightronics and Famostar

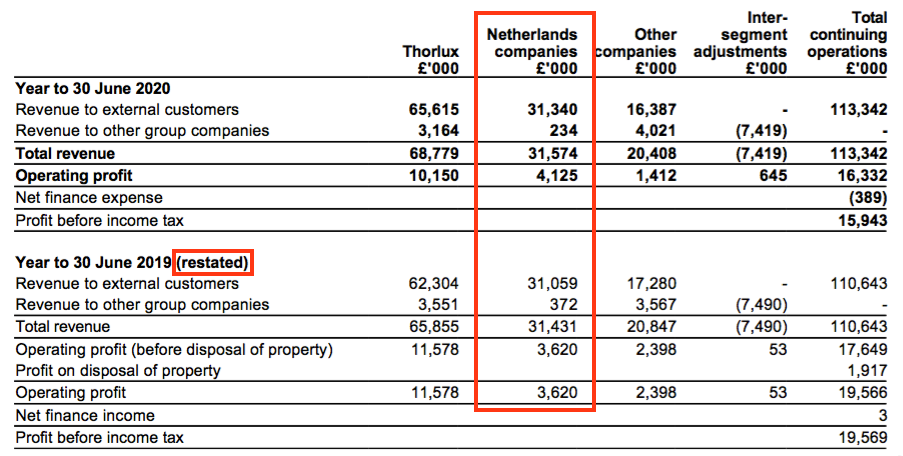

- TFW now lumps Dutch subsidiaries Lightronics and Famostar together within its financial reporting:

- The aggregate Dutch performance was encouraging in the circumstances. Total full-year Dutch revenue climbed 1% but profit gained 14%.

- The Dutch businesses represent approximately a quarter of the wider group.

- The annual report revealed Lightronics, which manufacturers street lights, produced a “slightly subdued performance”.

- Lightronics’s revenue slid 3% to £22.7m during the year and the annual report did admit “Lightronics fell short of improving its figures this year”.

- Good preparation at the start of the pandemic appeared to help:

“The company was largely unaffected by COVID-19, since operational measures were put in place in the early phases to enable Lightronics to continue to service its customers during the last quarter. In fact, June operating results were some of the strongest on record.”

- Lightronics’s longer-term performance remains impressive. The division was acquired during 2015, since when revenue has more than doubled.

- The annual report claimed Famostar, a specialist emergency-lighting company, had “exceeded expectations” during the year.

- Famostar’s revenue gained 12% to £8.8m.

- Once again good preparation at the start of the pandemic appeared to help:

“Famostar has been the standout performer for the Group this year, following on from a strong performance last year. As at Lightronics, performance seemed unhampered by COVID-19 in the final quarter, actions having been taken in the initial stages of the outbreak to protect operations and ensure continued supply to customers.”

- Famostar’s progress remains impressive. The subsidiary was acquired during 2017, since when revenue has gained approximately 27%.

- TFW hinted that near-term progress at Lightronics and Famostar may not be as positive as the past:

“Economic and sector forecasts in the Netherlands are pessimistic; this will put some pressure on results in the next 12 months.”

Other divisions

- Among TFW’s smaller divisions, only TRT (street/tunnel lighting) reported positive progress.

- Full-year TRT revenue gained 14% to £10m following “several large scale projects”.

- Revenue at Portland (retail/hospitality lighting), Solite (cleanroom lighting) and Philip Payne (emergency lighting) meanwhile fell a collective 20% to £8m.

- Aggregate profit from all the ‘Other’ businesses amounted to only £1.4m for the full year, and without TRT may have registered a loss.

- Selling lighting to shops and pubs in particular could be difficult during the current year.

LEDs

- Recent years have seen TFW capitalise on an industry shift towards LEDs. The annual report revealed 90% of revenue now relates to LED products.

- Adjusting for the Dutch acquisitions, group revenue between 2013 and 2020 improved by approximately 73% supported in part by the LED boom.

- These FY results implied LEDs had practically sold themselves:

“Sales of LED luminaires were relatively easy to achieve, primarily on the basis of significant energy savings and increased reliability.”

- However, March’s interim statement admitted LED interest among customers had “peaked”.

- These FY results gave a mixed update on the LED market:

Projects that can benefit from LED technology remain firm targets, such as where projects are still lit with luminaires using fluorescent lamps…Opportunities to replace non-LED lamps are, however, fewer now. Early LED installations are now eight to ten years old, so the replacement market will soon become a target again.

Group companies need to offer features beyond energy saving and reliability alone. Options include improving the quality of the white light from LED luminaires, reducing glare, and improving the ecological impacts of our product designs.

- The LED shift underlines the technological treadmill TFW must continue to run upon.

- A lot of treadmill running does not always produce instant success. A good example is the Flex System.

- The 2019 annual report devoted two full pages to this “radical approach to lighting”…

- …yet the 2020 annual report mentioned the product just once in passing.

- Has the Flex System flopped? Or will it come good during the next few years?

- For now at least, the Flex System does not yet seem to be ‘the next SmartScan’.

Financials

- The term “robust balance sheet” was used five times within the 2020 annual report.

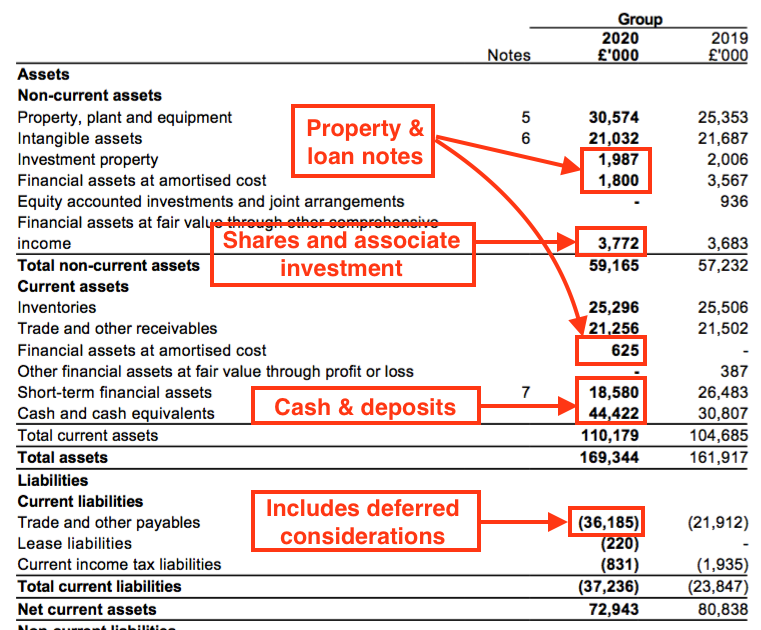

- The balance sheet continues to carry an array of financial assets as well as sizeable ‘deferred considerations’:

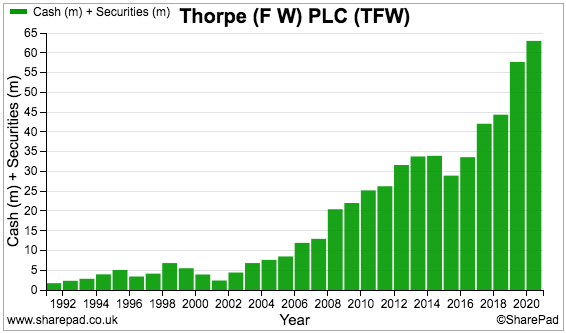

- Cash and term deposits ended the year at a record £63m. Other assets include investment property of £2m, loan notes of more than £2m plus an equity portfolio and an associate investment of close to £4m.

- Conventional debt remains at zero.

- The chart below shows how the cash and term deposits have piled up over time:

- ‘Trade and other payables’ of £36m include almost £16m earmarked as deferred considerations for the former owners of Lightronics and Famostar.

- These deferred considerations are due to be paid on or before 30 June 2021.

- Cash and the various investments less the deferred considerations come to £56m or 48p per share.

- I am sure TFW’s “robust” asset position helped reassure customers and suppliers that, during the lockdown, orders would still be completed and bills would still be paid.

- Perhaps that is why the group could say its present order book was “healthy” and its daily orders were “good”.

- Cash generation during the year was very respectable:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit (£k) | 15,959 | 18,189 | 19,225 | 17,357 | 16,068 |

| Depreciation and amortisation (£k) | 3,800 | 3,999 | 4,595 | 5,022 | 5,817 |

| Cash capital expenditure (£k) | (4,307) | (7,286) | (7,819) | (5,473) | (8,495) |

| Working-capital movement (£k) | (909) | 1 | (241) | 2,234 | 627 |

| Cash (£k) | 33,205 | 41,659 | 43,958 | 57,290 | 63,002 |

- Total capital expenditure once again exceeded the deprecation and amortisation charged against earnings.

- However, past differences have been due to TFW purchasing property — which should not lose its value in the way other plant and equipment can.

- During the last five years, TFW has spent £14m acquiring freehold assets — which more than explains the £10m variation between the aggregate capex expense (£33m) and the associated depreciation and amortisation charge (£23m).

- Working-capital management was favourable once again, and supported total cash generation of approximately £12m. Dividends of £6m left £6m to bolster the cash position.

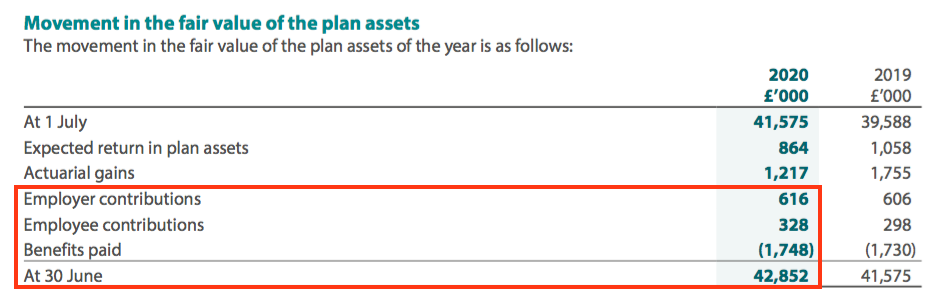

- TFW’s defined benefit-pension scheme sported a £269k surplus, although the associated accounting does not always reflect the true-life demands of a final-salary plan.

- Important pension-scheme figures to consider are the benefits being paid and the plan’s asset value:

- For TFW, paying annual benefits of £1.7m from scheme assets of £42.9m requires an investment return of 4.1%.

- Employee and employer contributions of £0.9m appear more than enough to sustain benefits of £2.1m should a market slump erode the £42.9m scheme assets.

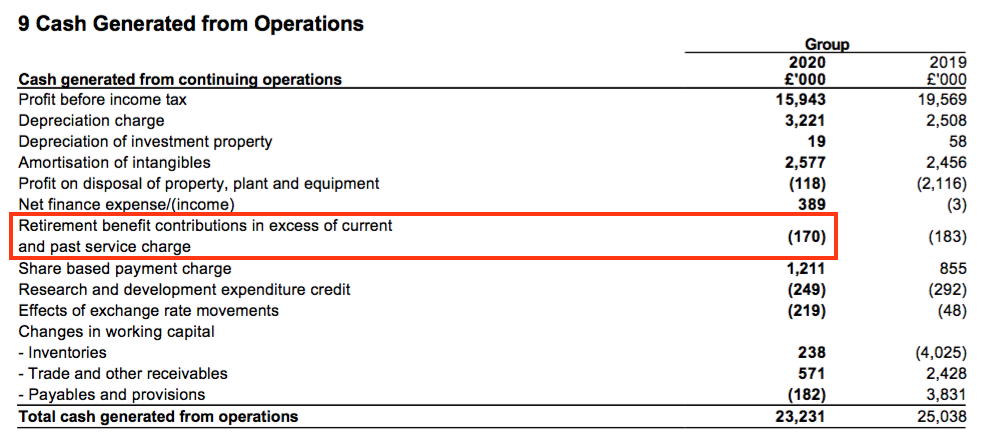

- Note that pension contributions of £170k bypassed the income statement — with the cash flow statement highlighting the expense:

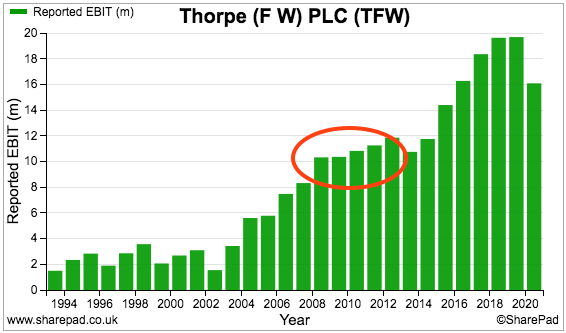

- The lockdown caused a reduction to both operating margin and return on average equity:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating margin (%) | 17.9 | 17.2 | 17.5 | 15.7 | 14.2 |

| Return on average equity* (%) | 26.2 | 27.2 | 26.5 | 24.0 | 21.2 |

(*Adjusted for cash, various investments and Lightronics/Famostar earn-outs)

- Both measures have been trending lower for a few years now.

- The aforementioned lower profitability from larger projects within Thorlux is one reason for the declining group margin.

- Other explanations (aside from the pandemic) may include:

- Greater competition/loss of technical advantage;

- Less profitable LED sales;

- Higher SmartScan/new product investment, and/or;

- The struggling/sub-scale smaller subsidiaries.

- The return on average equity figures in the table above are adjusted by excluding TFW’s significant cash and investments.

- Assume the cash and investments are essential to the business rather than ‘surplus to requirements’, and the 21.2% calculation for 2020 falls to a rather modest 10.6%.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- TFW’s gloomy remarks concerning a “global recession” and a “downturn in orders” could herald a difficult year ahead.

- Assuming a repeat of FY 2020 for FY 2021, operating profit of £16.3m translates into earnings of 11.4 per share after standard 19% UK tax.

- Subtract the 48p per share net cash and investments from the 290p share price, and the underlying P/E might be 21.

- The P/E rises to 25 if the cash and investments are in fact essential to the business and not really ‘surplus to requirements’.

- The 21-25x rating appears generous given the Covid-19 uncertainty and the likelihood of stagnant near-term earnings.

- Perhaps investors are willing to apply a premium multiple for the reassurance of TFW’s ‘pandemic-proof’ balance sheet.

- And/or perhaps investors are willing to apply a premium multiple because profits were sustained during the banking crash:

- And/or perhaps investors are willing to apply a premium multiple because of SmartScan going from nothing to revenue of £26m within four years.

- In today’s growth-obsessed market, SmartScan could represent a disproportionate part of TFW’s £338m market cap.

- The 5.66p per share dividend meanwhile provides a modest 2.0% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

FW Thorpe (TFW)

AGM statement published 19 November 2020

This statement feels a little less pessimistic than the comments given within the annual results. Here is the full text:

——————————————————————————————————————

At the Annual General Meeting of FW Thorpe Plc to be held at 3.15pm today, Chairman, Mike Allcock, publishes the following statement:

“I am pleased to report that during the first few months of the 2020/21 financial year, despite the significant issues generally in the global economy, orders and revenue remain broadly similar when compared to the same period last year.

As mentioned in my recent full-year statement, the Lightronics factory was significantly fire damaged on 23 September. Within a few days, local management had secured a new temporary production facility, and it was operational swiftly with only a minimal impact upon customer service. Insurance assessments have now allowed for an initial payment to be made, with funds deployed to replace damaged stock and production equipment. The areas worst affected have been demolished, and rebuilding plans are underway.

Whilst management is satisfied with the current order situation, with order books around the Group generally healthy, both the COVID-19 pandemic effect and Brexit transition concerns are foremost in our minds. We plan for the future carefully, but at this present time we remain cautious about the Group’s second-half performance.”

——————————————————————————————————————

Remaining cautious about H2 is to be expected, but orders may be holding up more than anticipated because the annual results had talks of a “downturn”:

“Whilst the Group’s present order book is healthy and daily orders are good, this is partly attributable to an amount of pre-COVID work carried forward and to pent-up demand in the market. Due to significantly reduced new-project sales visits and activity during lockdown, reduced usage of the Group’s extensive Application and Experience Centres, and the general state of the economy, it is difficult to predict anything other than a downturn in orders at the end of the 2020 calendar year.”

Maynard

FW Thorpe (TFW)

Publication of 2020 annual report

Here are the points of interest:

1) Marketplace

Several (understandable) references to ‘healthcare’ and ‘logistics’ as favourable sectors. Although I am not sure about the immediate prospects for the rail and retail sectors:

TFW now refers to ‘international economic conditions’ instead of ‘adoption of LED technology’ within its Marketplace narrative. A hint of buying struggling rivals, too.

2) Business model

This line summarises the business model very well:

3) SmartScan

The report devoted four full pages to SmartScan. The introduction below referred to the Built Environment Analytics noted within the blog post above:

4) Key performance indicators

Two new KPIs for 2020:

I cannot recall any other quoted company having C02 offset as a formal KPI alongside revenue etc. Business seems serious about going green.

5) Old machinery

Surprised to learn TFW had been using 25-year-old machinery:

I had assumed a business that prided itself on product innovation would not use dated tools.

6) Thorlux review

A few interesting snippets about TFW’s largest division:

The new Thorlux managing director was appointed during August 2020 and previously worked at JELD-WEN:

Not sure what the new MD knows about lights (he trained initially as an auditor). Has not become a main board director (see point 14)

7) Portland review

Text implies this division lost money during the initial lockdown:

“Steady decline” does not sound great. This division generated revenue of only £2.4m during 2020 and I do wonder about its future within TFW given the division’s predominantly retail/hospitality customer base. News of employing a full-time product designer suggests this business has previously lacked suitable staff.

8) TRT review

Pipeline is “healthy”, but the talk is of rail and retail sectors — the lockdown prospects for which I would say are not obviously favourable:

9) Lightronics review

The acquisition of Lightronics the other year was to help TFW sell its domestic products abroad. Very disappointing to note Thorlux sales generated through this division were just £0.4m:

10) Flex lighting and hospitals

The 2019 annual report showcased TFW’s new Flex lighting system:

I would say Flex would indeed be great in hospitals:

11) Financial review

Commendable decision on government subsidies and staff payments:

TFW’s freeholds are in the books at cost. Some were purchased 20-plus years ago. Unlikely to make a huge difference to valuation though.

12) Risks

The report carried a commendable and comprehensive two-page risk assessment of Covid-19:

The pandemic was unsurprisingly included as a new business risk:

The risk levels associated with economic conditions, price changes, cybersecurity and Brexit were all raised during the year:

13) Section 172

A new statement that did not reveal any particular revelations:

14) Board of directors

I wonder if the new Thorlux managing director will become a main board member. Would be odd if the Thorlux business development director — who presumably now reports to the new MD — remains on the board while the new MD is not given a seat:

Mind you, the Thorlux business development director is a Thorpe family member and presumably the family still want executive representation on the board.

TFW’s present executive chairman was a board member during some of his time as Thorlux MD. I also wonder whether the Philip Payne MD requires board membership given his division recorded sales of just £2.7m last year. Somebody representing the much larger Dutch divisions could be a more suitable board member.

15) Directors report

Just a “number” of objectives were achieved during 2020:

The “majority” of objectives were achieved during 2019.

16) Corporate governance

Board remains partially compliant with corporate-governance guidelines:

The somewhat unconventional board set-up has of course not prevented the illustrious dividend record.

17) Director pay

The lead executives are not underpaid.

Bonuses are derived from an (unspecified) level of operating profit. The executive chairman enjoys a non-standard two-year notice period (should be one year):

Salaries for the chairman and two other executives were commendably reduced for 2020 by c10%. But the FD’s salary was increased by £5k to £240k:

Total executive bonuses for 2020 represented 61% of total executive salaries, versus 75% for 2019 for the same four execs.

The execs collect very generous pension contributions not included in the table above:

Options for 2020 were forfeited due to EPS not meeting the (rather tame) RPI+3% target:

I think this five-year ESOP has now run its course and I dare say a new scheme will be proposed soon.

18) Audit report

Materiality at a standard 5% of pre-tax profit, albeit on a three-year average due to Covid:

More notably the scope text has changed markedly from last year, when the exact percentage of revenue (91%) was cited as having been fully audited:

Following on from Tristel’s annual report, I get the impression auditors generally have not been able to conduct as thorough audits as last year due undoubtedly to Covid.

The lower-range materiality figure at the component level is £400k — versus £61k for 2019:

Again, gives the impression of the auditors not digging as deep as last year. But audit fees are up 60% (see point 23).

19) Going concern

An extra line for 2020:

Very reassuring, and not seen a similar line from any other company.

20) IFRS 16

One advantage of owning freeholds is very small IFRS 16 lease numbers:

21) Development costs useful life

Remains a very reasonable three years:

22) Capital management

This policy has come to the fore following the pandemic:

23) Audit fees

A 60% increase to basic audit fees to £210k:

Presumably the increase was pandemic related (see point 18). Fees at Tristel increased notably, too (point 10)

24) Employees

No major changes to the staff ratios, which I think is a sign of good operational management during the lockdown:

The average employee cost remained at £48k, average revenue per head remained at £165k and total employee cost remained at 30% of revenue.

25) Finance income and expense

Lower all-round income from TFW’s various assets:

The share appreciation rights relate to dividends from the Dutch operations, which increased slightly during the year — and underlines the relatively favourable performances of those subsidiaries.

26) Property, plant and equipment

Freehold book value at £19m:

As noted within the blog post above, the major difference between cash capex and depreciation relates to expenditure on freeholds.

27) Intangibles

Nothing amiss with TFW’s intangibles, with expenditure matched by amortisation:

28) Goodwill calculation

A useful snippet outlining how TFW values past/potential acquisitions on Ebitda multiples:

Goodwill from the Dutch acquisitions stands at £12m, so the £16m headroom implies i) Ebitda from the Dutch divisions has improved post-purchase, or ii) the original Ebitda purchase multiple was well below the 5-6x used for the headroom calculation.

29) Investment property

Gross £142k rental income suggests the £2m investment property is valued on a 7% yield:

The small-print (not shown above) says the River Wye and Monmouthshire sites have a £1.6m book value. The balance is represented by a site rented by a former subsidiary.

30) Loan notes

The quality of these IOUs varies significantly.

This £2m loan note has seen sporadic repayments and is effectively backed by a Brangwin family shareholding that surpasses £20m:

Loan notes involving the Dutch operations have been repaid or look on course to be repaid:

A loan note held by a joint operation in the UAE may not be repaid:

31) Financial assets

This entry had previously represented only TFW’s share portfolio, but from 2020 includes an unquoted investment in a Spanish lighting business:

The Spanish investment had a 2019 £936k book value, which was written down by £407k during 2020. The share portfolio was therefore reduced by £427k during the year, or 11% of the c£3.7m start value.

32) Inventories

Stock ratios have deteriorated slightly but nothing too worrying:

Average year-end stock was 22.4% of revenue — at the top end of the narrow 20-22% band seen during the last 10 years.

Stock turn (average year-end stock versus the cost of inventories) was 1.78x, implying stock sits in the warehouse for almost 7 months. Has been 6 months or less in previous years.

33) Trade receivables

Trade debtor ratios do not create major concerns:

Average year-end trade receivables represented 16.9% of revenue, the lowest level for at least 15 years and suggest good credit control during the pandemic. Proportion topped 20% between 2014 and 2016.

Past due trade receivables are 9% of all trade receivables — a level not unheard of for TFW but higher than the 6% typical.

34) Trade payables

Confirmation TFW is on the hook to pay almost £16m during 2021 to settle the Dutch acquisition earn-outs:

34) Options

1 million options represent dilution of less than 1%:

35) AGM questions

Alas, I did not get around to using the AGM email service:

Nor did anybody else, as TFW’s website confirms no questions were received through the email address.

Maynard