21 August 2020

By Maynard Paton

Results summary for Mincon (MCON):

- A generally satisfactory update given the pandemic, with underlying revenue up almost 5% and profit before adjustments perhaps up as much as 28%.

- The postponement of the interim dividend due to Covid-19 was disappointing after earlier statements barely mentioned the virus.

- An emphasis on “geotechnical” drills and services has reduced the dependence on mining customers to 52% of revenue.

- Modest cash generation, average margins and enormous stock levels offer significant scope for accounting improvements during the current ‘moat-rebuilding’ phase.

- Various (perhaps optimistic) assumptions alongside opportunities from new products lead to a reasonable 14.3x P/E. I continue to hold.

Contents

- Event link, share data and disclosure

- Why I own MCON

- Results summary

- Covid-19, dividend and government support

- Revenue and profit

- Geotech and Spiral Flush

- Greenhammer project

- Working capital

- Capital expenditure and cash flow

- Cash and debt

- Valuation

Event link, share data and disclosure

Event: Interim results for the six months to 30 June 2020 published 10 August 2020

Price: 80p

Shares in issue: 211,675,024

Market capitalisation: £169m

Disclosure: Maynard owns shares in Mincon. This blog post contains SharePad affiliate links.

Why I own MCON

- Designs and manufactures industrial drill bits, with sales supported by established reputation, engineering excellence, product patents and technical innovation

- Boasts veteran family management with 43-year tenure, 57%/£95m shareholding and long-term perspective

- New product developments starting to generate extra contracts, diversify revenue and perhaps extend the company’s competitive edge

Further reading: My MCON Buy report | All my MCON posts | MCON website

Results summary

Covid-19, dividend and government support

- After the 2019 full-year statement declared a final dividend, these results disappointingly postponed an interim payout.

- MCON admitted:

“In light of the global Covid-19 pandemic, the board of directors have adopted a prudent approach and have decided to postpone a decision on an interim dividend to later in the year.”

- The deferred dividend was possibly prompted by the receipt of government grants.

- The RNS small-print revealed:

“5. Financial Reporting impact due to the Covid-19 Pandemic:

a. Government Grants

The Group received government grants in certain countries where the Group operates. These grants differ in structure from country to country but primarily relate to personnel costs.”

- Companies should not of course be declaring dividends if they are receiving state benefits.

- MCON’s previous announcements had not really suggested any pandemic-related problems.

- Published during March and April, the 2019 results and full annual report barely mentioned Covid-19. The Q1 update published during May was not too alarming either.

- I had therefore assumed many of MCON’s customers — mining groups operating in remote locations — had not been too affected by any lockdowns.

- In reality, productivity at various mines was reduced and income from mining customers fell 9%:

“The Group’s supply and service to the mining industry contracted in the period by 9% due to the impact of temporary mine closures in the efforts to suppress the spread of Covid-19. This was mostly experienced in Southern Africa, Central and South America. The Group also experienced a weakness in the APAC mining industry due to the lockdowns in these areas where mining activity was affected by several lockdown-related factors.”

- An increase to net debt (see Capital expenditure and cash flow below) following the €8m purchase of Lehti earlier this year may have also influenced the dividend deferral decision.

- I am not sure whether MCON postponing the interim dividend will actually result in a payment “later in the year“.

- I would have thought any news of a revived payout would accompany the Q3 update scheduled for late October.

- Note that the final dividend declared in March was due to be paid during June, but has yet to be paid following a delayed AGM (payment is due in September).

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue and profit

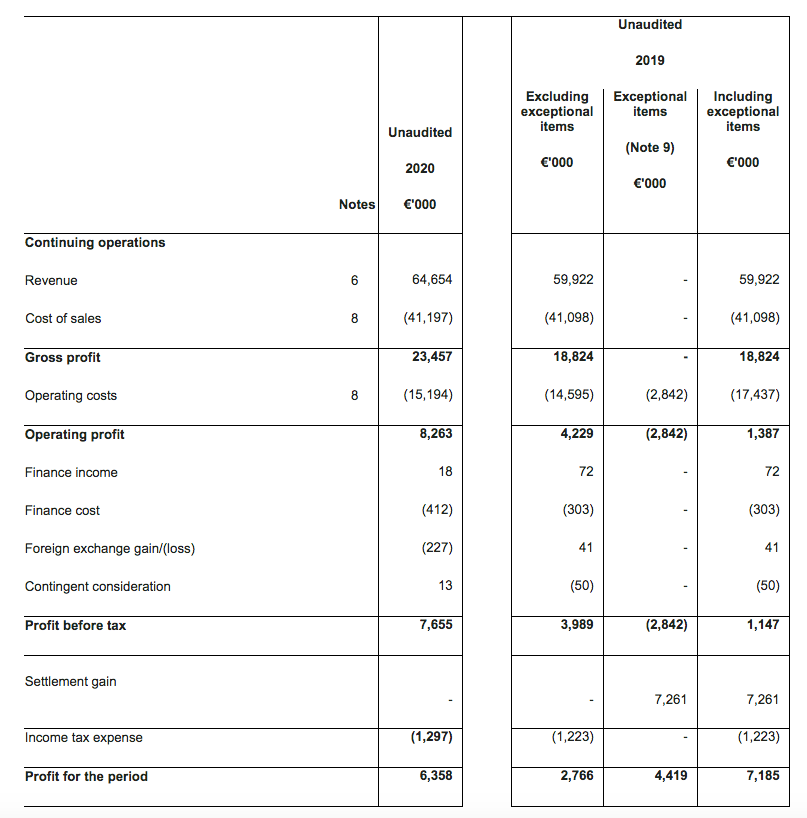

- These H1 figures were easier to interpret than the muddled 2019 numbers published during March.

- That said, this H1 performance was distorted slightly by the Lehti purchase, certain impairments and a minor restatement of last year’s exceptional items.

- Total revenue gained 8% to €65m to set a new H1 record, and MCON claimed underlying turnover growth was almost 5%.

- Note that MCON’s sales of third-party equipment fell 4% during the half:

- The underlying revenue growth rate achieved by MCON’s own-branded products may therefore have been approximately 6%.

- MCON’s own-branded products now represent 86% of total sales — the highest proportion since at least 2010.

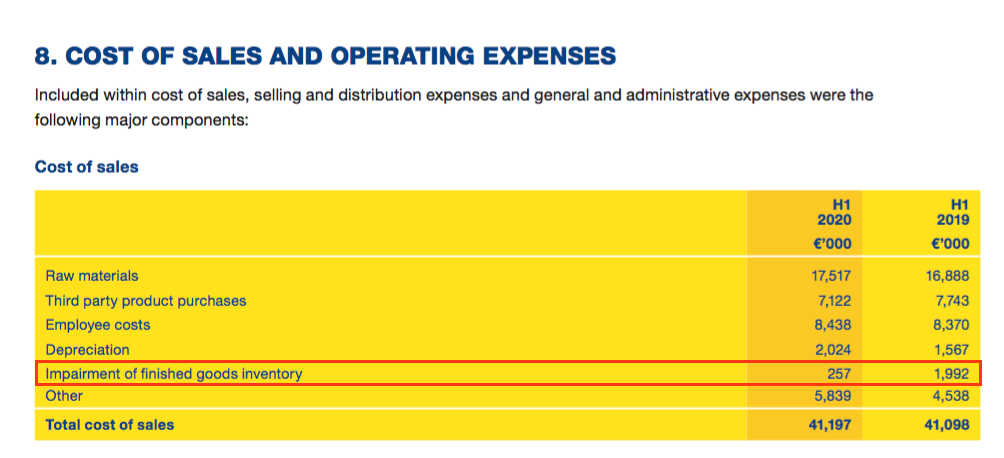

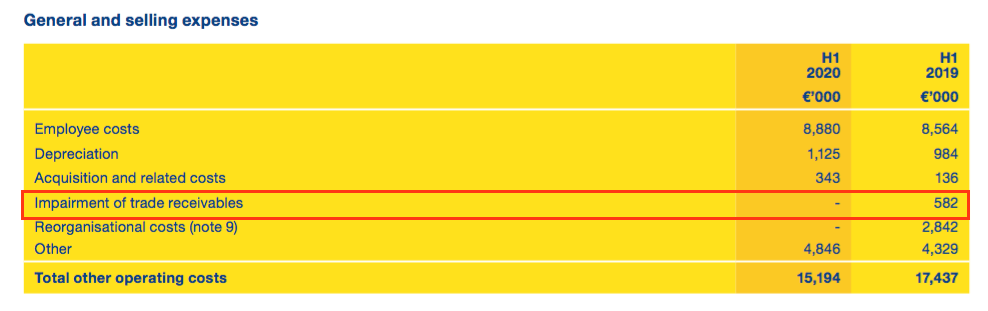

- Last year’s first-half included stock/debtor impairment charges of €2.6m, which were not deemed to be exceptional. This H1 included a stock impairment charge of just €0.3m:

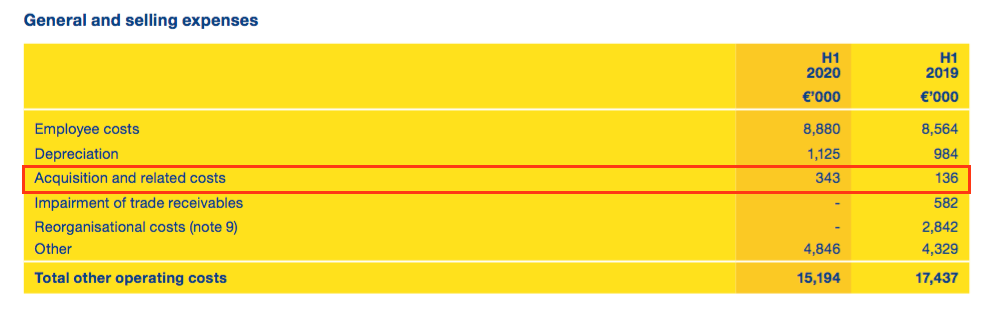

- Last year’s first half also included a €136k exceptional item relating to acquisition costs, which was not deemed exceptional when the 2019 figures were used as a comparison this time around. This H1 included acquisition costs of €343k:

- Adjust for exceptional items and stock/debtor impairments, and H1 profit jumped 25% from €6.8m to €8.5m:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Operating profit before adjustments (€k) | 8,087 | 8,265 | 6,939 | 7,362 | 8,863 | ||

| Adjustments | |||||||

| Stock impairment (€k) | - | 747 | (1,992) | 300 | (257) | ||

| Other impairments (€k) | - | - | (582) | (217) | - | ||

| Acquisition costs (€k) | (268) | 102 | (136) | 136 | (343) | ||

| Other exceptional costs (€k) | - | - | (2,842) | (1,686) | - | ||

| Operating profit after adjustments (€k) | 7,819 | 9,114 | 1,387 | 5,895 | 8,263 |

- Adjust for exceptional items, stock/debtor impairments and acquisition costs as well, and H1 profit jumped 28% from €6.9m to €8.9m.

- The reported H1 profit of €8.3m was in fact the highest first-half profit since at least 2013.

- The Lehti purchase brought the supplier’s margin in-house and helped improve profitability:

“The increase in margin was due to Mincon DTH [‘down the hole’] and Mincon Geotech products together accounting for a larger amount of the sales mix in the current period. These two product ranges now earn comparative margins since the Group acquired the remaining manufacturing of the Geotech products through the strategic acquisition of the Lehti Group in January 2020.”

- Last year’s group restructure also assisted the margin increase:

“The increase in profits are attributable to better gross margins and the improved operating leverage arising from the reorganisation of the business undertaken in 2019. The Group also incurred less travel costs due to the international travel ban imposed across the Group in light of the global Covid-19 pandemic.”

- Further analysis reveals lower raw material and employee costs as a proportion of revenue assisted the margin improvement versus H1 2019:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Raw materials (€k) | 16,246 | 16,975 | 16,888 | 22,302 | 17,517 | ||

| Employee costs (€k) | 15,710 | 17,391 | 16,934 | 13,010 | 17,318 | ||

| Raw materials/Revenue (%) | 29.2 | 27.1 | 28.2 | 36.7 | 27.1 | ||

| Employee costs/Revenue (%) | 28.2 | 28.1 | 28.3 | 21.4 | 26.8 |

- The H1 2020 operating margin was somewhere between 13% and 14% depending on which impairment and acquisition-cost adjustments are made.

- MCON has reported margins generally between 13% and 14% since 2015.

- The 19%-plus margins of 2014 and before — which suggested the presence of an operational ‘moat’ and attracted me to the company in the first place — remain a distant memory.

Geotech and Spiral Flush

- MCON’s 2019 results heralded a distinct change of tone about the “Challenger model”.

- The model refers to dealing with mining clients direct and this time last year, MCON mentioned “Challenger” six times, including:

“Under the “Challenger” model, we engage directly with mines in a similar way as the market leaders, and with primary contractors in construction activities, and this approach is winning us business.”

- This H1 statement did not mention “Challenger” once, although MCON did say “full-service mining contracts… are continuing to come our way”.

- Instead, this H1 statement mentioned “geotech” seven times as opposed to zero mentions last year.

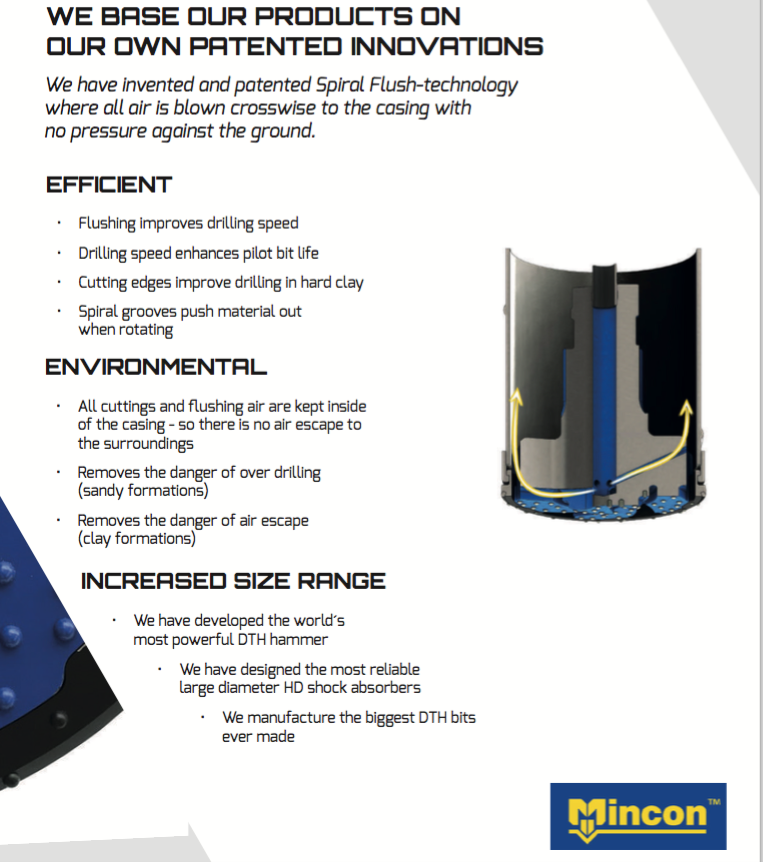

- MCON’s website explains geotechnical drilling in more detail:

“In today’s geotechnical drilling market, foundation drilling contractors face the challenge of operating in complex environments projects with tight deadlines, on even tighter margins. With the expertise of the Mincon Group Geotechnical Centre in Finland, our customer support centres can offer you class-leading drill string consumables for all geotechnical drilling projects. This includes our patented Spiral Flush air control systems that enable DTH drilling operations in tight urban spaces and sensitive ground conditions.”

“The unique design on the face of a Spiral Flush bit forces cycled air back through the casing – rather than allowing it to escape into the ground. By containing this airflow and correctly channeling it, disruption of rock strata and any adjacent foundations is avoided. ”

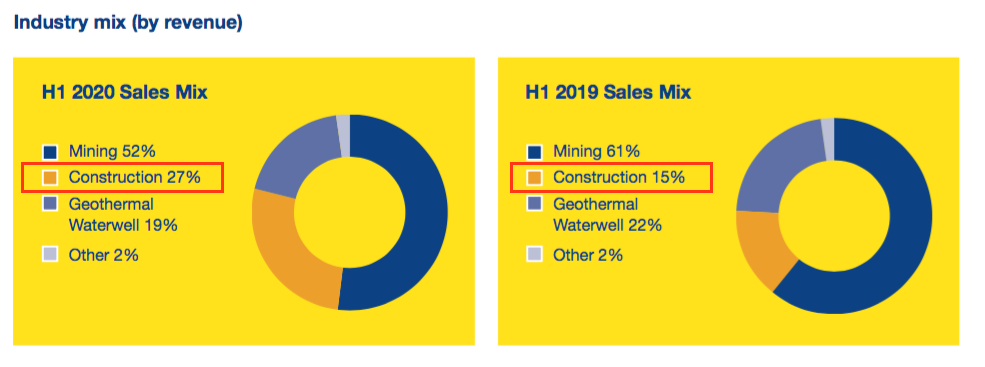

- The significance of geotech contracts prompted MCON to publish its first industry-mix charts:

- The construction market (which include geotech customers) almost doubled its revenue contribution to €17m during this H1. MCON claimed organic construction growth was 74%.

- Last year construction customers represented revenue of €14m (12%) and €7m (6%) the year before that.

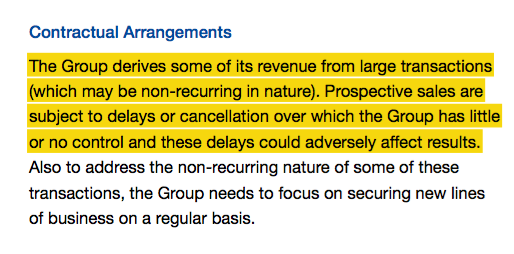

- The 2019 annual report small-print (point 6) hinted that the shift towards larger contracts could mean lumpier revenue and unpredictable profits:

- Work on the Spiral Flush underlined MCON’s ongoing innovation to sustain a competitive advantage based on “engineering excellence”:

- Notable quotes from the annual report (point 1) included:

- “relentlessly insisting on engineering excellence”;

- “our continued dedication to engineering excellence”;

- “The primary focus of the Group is on engineering excellence”, and;

- “the group’s fundamental ethos of engineering excellence.”

Greenhammer project

- MCON’s Greenhammer project has stalled for the time being.

- Last year the firm described this new hydraulic drilling system as:

“a disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base”.

- MCON added:

“This is not a small system or easily replicable, and we have placed patents around the system to protect it. The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.”

- The project has been in development for eight years, and was first mentioned by MCON during 2017.

- Three years on, and the customer about to test the system has suffered one hold up after another.

- A “serious mechanical issue” on the customer-owned rig paused the trial during 2019.

- Then Covid-19 emerged and delayed the trial this year:

“Product development has also been affected by the crisis, most notably with our customer in Australia for the hydraulic Greenhammer. Site access to the Greenhammer test site is still restricted, and with the re-imposition of lockdowns in Victoria and New South Wales we are waiting to hear when we can get back onsite. ”

- MCON remains hopeful of a successful conclusion:

“Once we get this [site access] confirmation, we will mobilise our team to get the 10″ system up and running and move to commercialisation of this exciting product for Mincon and the hard rock surface mining market.”

- MCON capitalised Greenhammer development costs of €0.5m during the half to take the project total to €5.2m since 2016:

- Not a cent of that €5.2m expenditure has been charged against earnings. Amortisation will commence only when the system enters commercial use.

- The €5.2m expense represents almost 9% of the €61m aggregate operating profit before exceptional items reported during the same time.

- If the entire Greenhammer project is written off, arguably past profits were overstated by 9%.

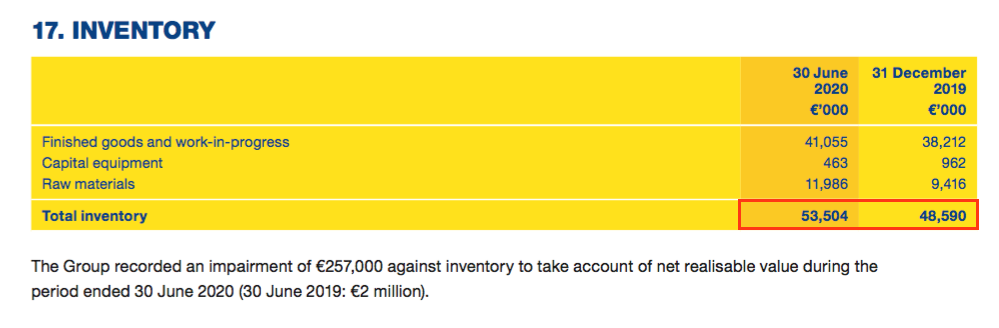

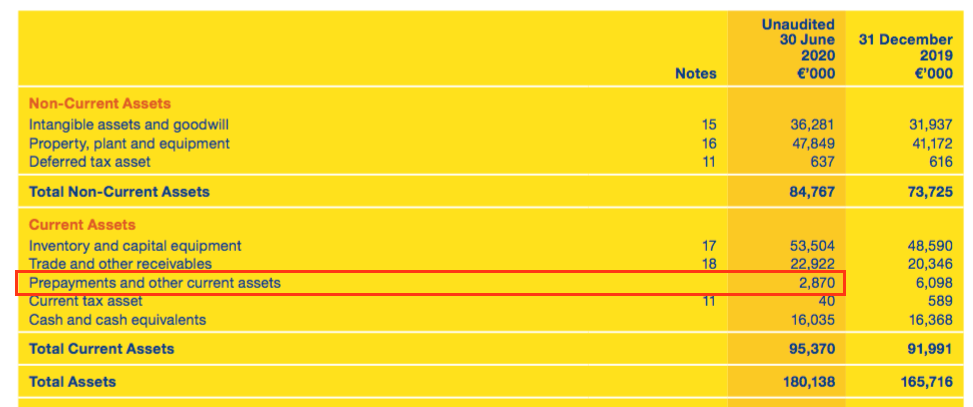

Working capital

- MCON has operated with significant working capital (stock plus trade and other receivables less trade and other payables) for some years.

- At the end of this H1, working capital represented 50% of revenue:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 | H1 2020 |

| Working capital (€k) | 38,286 | 45,186 | 41,690 | 58,041 | 58,083 | 65,229 |

| Revenue (€k) | 70,266 | 76,181 | 97,358 | 117,688 | 120,671 | 129,308* |

| Working capital/Revenue (%) | 54.5 | 59.3 | 42.8 | 49.3 | 48.1 | 50.4 |

(*H1 2020 revenue doubled)

- Stock is by far the largest component of MCON’s working capital:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Stock (€k) | 32,045 | 35,310 | 31,851 | 49,357 | 48,590 | 53,504 |

| Revenue (€k) | 70,266 | 76,181 | 97,358 | 117,688 | 120,671 | 129,308* |

| Stock/Revenue (%) | 45.6 | 46.4 | 32.7 | 41.9 | 40.3 | 41.3 |

(*H1 2020 revenue doubled)

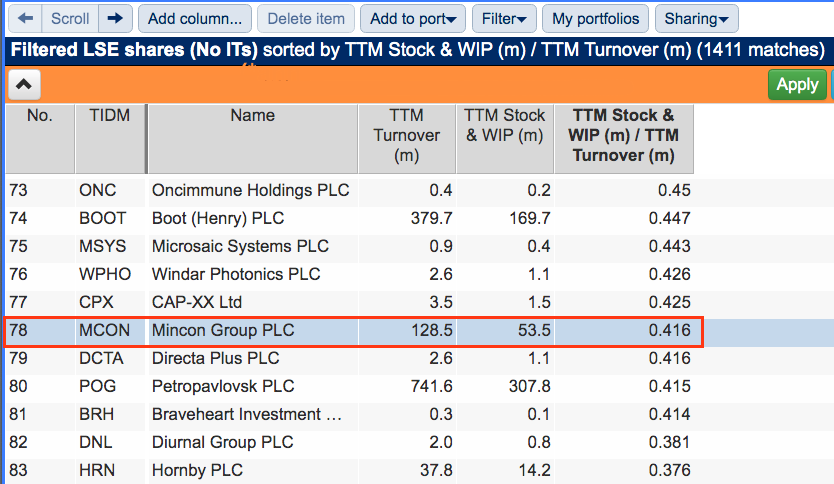

- For some perspective, SharePad shows MCON ranking 78th out of 1,411 shares on a stock-versus-revenue basis:

- Many of the companies with greater stock-versus-revenue percentages than MCON are property firms (which carry their land/buildings for sale as stock) or very small entities with minimal sales.

- The annual report small-print (point 2) said “management expects that the Group’s inventory will continue to decrease”.

- Stock levels instead advanced by €5m, or 10%, during the six months, although MCON did admit “net working capital increased… by 5%, mostly due to acquisitions”:

- Operating with stock levels representing 41% of revenue will not win any prizes for efficient returns on capital.

- Such levels often suggest the presence of slow-moving or obsolete stock, and last year MCON did incur a €1.7m stock write-off.

- MCON’s annual report implies high stock levels are required to ensure tip-top customer support and deliveries.

“The Group manufactures and sells rock drilling consumable products, and accordingly timely supply and service is key. Since the markets that we serve across the world are geographically dispersed, and the lead times for delivery are set by customer requirements and competition to a large degree, we have built a wide network of customer service centres backed by manufacturing plants in key markets.”

- Perhaps significant stock levels can support a ‘capital requirement’ competitive edge that assists the primary “engineering excellence” advantage.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Capital expenditure and cash flow

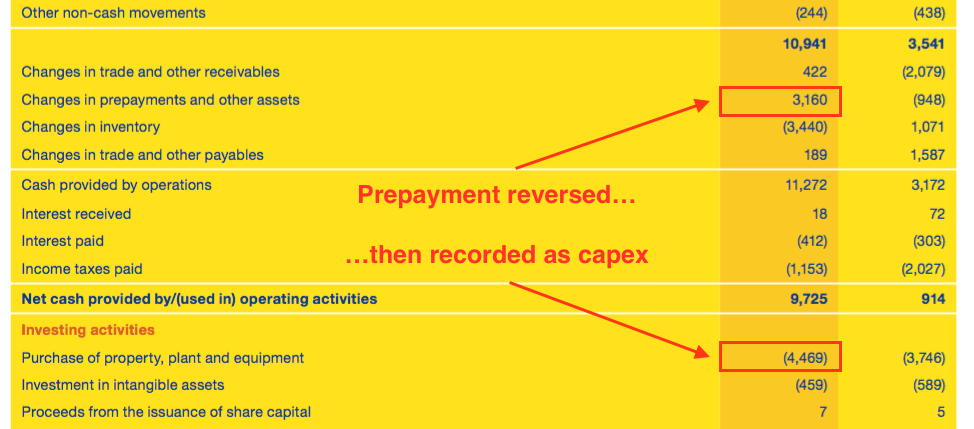

- Twelve months ago I was confused by this text within the H1 2019 results:

“Capital expenditure is held in prepayments as it is incurred, and prior to the plant and facilities being commissioned, so while the capital expenditure for the year will be significantly above depreciation, little of this will be actual cash outflow in the period.”

- I did not understand why certain capital expenditure may not be “actual cash outflow in the period”.

- I think I now know what is going on.

- Capital expenditure can indeed be held as a prepayment prior to plant and facilities being commissioned.

- And once the plant and facilities are commissioned, I reckon the prepayment entry is reversed and then recorded as capital expenditure.

- The balance sheet shows the prepayments:

- And within the cash flow statement, the appropriate prepayments are reversed and then accounted for as capital expenditure:

- Between 2015 and 2019, MCON spent €33m on tangible assets but charged only €17m as depreciation against earnings.

- MCON has in the past talked of capital expenditure moderating significantly following the recent construction of new facilities.

- For example, last year’s Q3 statement declared:

“Capital expenditure at present, after some years of build out, has fallen to half the depreciation rate, and is likely to remain there for a couple of years outside of decisions and opportunities in the GeoTech side.”

- This H1 statement is the first I can recall that actually revealed effective capex moderating.

- The positive prepayment movement of €3.2m less capital expenditure of €4.4m gave a net €1.2m cash expense, versus depreciation of €3.2m.

- Despite the prepayment movement, greater stock levels meant operating free cash flow during the half came to only €4.4m versus a reported operating profit of €8.3m.

- The Lehti purchase and earn-outs from previous acquisitions absorbed a further €8.2m.

- Tax and interest payments then left MCON with a net €1.9m cash outflow for the half.

- The usual €0.0105 per share interim dividend would have cost a further €2.2m.

Cash and debt

- MCON declared its first net-debt position following the group’s 2013 flotation.

- Half-year borrowings of €23.3m exceeded cash of €16.0m by €7.3m.

- The 2019 results implied interest costs were a reasonable 3.7%.

- Based on a doubling of this H1’s €8.3m operating profit:

- Annual interest payments of close to €0.9k would be covered approximately 20 times, and;

- Net debt would be covered 2.3 times.

- MCON’s borrowings therefore do not appear excessive, assuming of course that this H1 profit can be sustained.

- Bear in mind, too, that MCON is on the hook for contingent acquisition earn-outs of €5.4m.

- At least MCON’s liabilities are not complicated by pension obligations.

Valuation

- MCON did not provide any predictions for the second half.

- Assuming (perhaps boldly) that the second half replicates the first, and applying for various adjustments, the shares may be reasonably priced.

- Excluding stock write-offs and acquisition-related costs, operating profit for this H1 was €8.9m.

- Subtracting Greenhammer expenditure of €0.5m then gives €8.4m.

- After tax applied at MCON’s projected 17% for 2020, operating earnings come to £12.6m or 6.0p per share with £1 buying €1.11.

- Adding net debt of €7.3m and earn-outs of €5.4m to the market cap of €169m gives an enterprise value of €181m, or 85p per share.

- Dividing that 85p per share enterprise value by my 6.0p per share earnings guess gives a possible earnings multiple of 14.3x.

- The valuation does not feel outrageous, presuming of course the business can in fact sustain this H1 performance and the profit adjustments are valid.

- Other factors supporting the valuation include:

- Own-brand sales up c6% despite a pandemic;

- Notable geotech opportunities that may develop through Lehti (the annual report small-print (point 1) was bullish);

- The Greenhammer project one day coming good, and;

- Management’s long-term dedication to engineering quality and product innovation.

- I still believe MCON remains in a ‘moat-rebuilding’ phase — the duration and cost of which remains unknown.

- Only when operating margins can be maintained at, say, levels of 15% or more, will MCON demonstrate to layman shareholders that some sort of competitive advantage has been constructed.

- The share price could of course be somewhat higher than it is now if/when the moat becomes really obvious.

- The trailing dividend yield could be 0%, 1.2% or 2.3% depending on whether dividends have been cancelled completely, just the final payment will continue or the interim payout will quickly resume. (All yields are calculated before Irish withholding taxes for UK-resident investors).

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Mincon (MCON)

H1 results presentation

MCON has for the first time published a results presentation on its website.

No great revelations were revealed, but the slides do show some example contracts and the type of work the business undertakes:

Maynard

Mincon (MCON)

Interim trading update published 09 November 2020

An encouraging statement. MCON appears to be coping with Covid-19 quite well, with revenue perhaps accelerating during Q3 and the likely payment of the suspended interim dividend.

Here is the full text:

———————————————————————-

Mincon Group plc (ESM:MIO AIM:MCON), the Irish engineering group specialising in the design, manufacture, sale and servicing of rock drilling tools and associated products, today provides an interim trading update for the period from 1st January 2020 to date, incorporating the third quarter to 30th September 2020.

Trading

Building on a trend noted in the Group’s interim results, we have continued with the broadening of the business during the third quarter and the Group has achieved comparable growth to H1 2020. Our total revenue increased by 12% compared with the first nine months of 2019. Revenue from the construction sector has continued to grow, although some of this growth was achieved through the sale of non-Mincon manufactured product, with a corresponding lower gross margin.

The environment in the mining sector is positive in light of the strong prices in precious metals and iron ore. Our trading in the sector, while in line with H1 2020, remains challenged by the Covid-19 pandemic due to the difficulties in shipping product, as the recovery from the initial shock of the pandemic evolves at various speeds in different regions.

All regional government Covid-19 restrictions we experienced with our factories globally during H1 2020 have now been lifted. Our factories are fully operational and are compliant with all Covid-19 measures, and we continue to focus on the health and safety of our workforce.

Although we have had a strong trading performance during 2020 to date, the effect of the Covid-19 pandemic on global trade over the coming 6 months at least, remains uncertain. As a result, the Board has decided to adopt a prudent approach by suspending the interim dividend for 2020. However, we will continue to assess our ongoing capital requirements and, in the absence of any significant adverse impact of the pandemic in our markets in the coming months, it is the Board’s intention to increase the final dividend declared in respect of the financial year 2020 so that the final dividend will be in line with the total dividend paid for 2019.

———————————————————————-

Total revenue up 12% during the first nine months of 2020 is promising when the H1 figures in the blog post above reported revenue up 8% or up 5% on an acquisition-adjusted basis.

Not a lot of other specifics were given, but the general tone was positive.

Underlining the confidence, the suspended interim dividend should now be tacked onto the final payout. That is a welcome move.

I was quite disappointed the interim dividend was suspended given MCON had barely mentioned Covid-19 in preceding statements, but the company was receiving state benefits, so a suspension was probably wise.

Maynard