15 April 2015

By Maynard Paton

Today I’m revealing one of the two new investments I’ve made during recent months.

The company in question is Mincon (MCON), a specialist engineer that designs, manufactures and sells drilling equipment for miners. I bought the shares during February and March 2015 at an average of 44.6p including all costs. The mid-price is now 54p.

All told, I feel this £114m Irish business is an excellent fit for my portfolio. Important attractions include a respectable competitive position, high margins, a cash-flush balance sheet and very favourable family management. A languishing share price and a possible P/E of just 10 also clinched it for me.

However, MCON is by no means perfect. In particular, the group is dependent on the vagaries of the mining sector, has an ambitious acquisition plan and does not boast the greatest of free cash flow.

A wide bid-offer spread and 71% boardroom ownership may put some people off, too.

At A Glance

- Prominent designer and manufacturer of mining drills and equipment

- Accounts blessed with high margins and substantial funds raised through the group’s recent flotation

- Dominant family management appears focused on the longer term

Top-quality products that rescued 33 trapped miners

Mincon (MCON) was established during 1977 when Patrick and Mary Purcell began manufacturing spare parts for rock-drilling rigs used by Irish mining firms.

By the mid-80s, Mincon had launched its own range of ‘Down-the-Hole’ (DTH) drills while about ten years ago, the firm developed what it calls ‘Reverse Circulation’ (RC) hammers.

(Just so you know, DTH drills are those fitted with percussion mechanisms powered by compressed air, while RC hammers are built to capture rock dust and cuttings for subsequent analysis).

MCON’s DTH and RC hammers are used within the mining, quarrying, construction and oil and gas industries, and sell for as much as €36,000. MCON also makes and supplies the associated drill bits, which can be as wide as 22 inches and cost up to €11,000.

MCON claims its hammers generally have a useful life of between 20,000 and 40,000 ‘drill metres’, and will require ‘a number’ of drill bits during that time.

Importantly for investors, MCON reckons it enjoys a good competitive advantage.

The group claims its “top-quality equipment” is based on “superior designs, unique processes and the highest engineering standards, coupled with a rigorous quality-control culture and an excellent understanding of the demanding and diverse conditions in which our hammers are expected to work”.

The upshot for customers include “increased drilling speeds, longer service life, greater reliability with ease of maintenance, and maximum operating-cost effectiveness.”

Sales are now made across North America, Australia, Europe and Africa.

I must admit, I have no insight into MCON’s drills and bits, but I have come across independent articles, such as this one, that cite happy customers:

“We’ve been using Mincon hammers from Rock Drill Engineering for more than seven years, and they’re all impressive performers. Although we have used other products, we know from experience that these offer better levels of performance and reliability.’”

Perhaps the greatest advert for the group’s products was the rescue of 33 trapped miners in Chile back in 2010. MCON made the RC hammer and bit systems that drilled the initial ‘lifeline’ hole some 700 metres deep. (You can read more about MCON’s involvement in the rescue by clicking here and here)

Notably, Patrick Purcell was reported to have said at the time:

“There are only three companies that have the level of expertise to produce the hammer drills used in this operation, which allowed a hole to be created to pass food and water to the miners.”

“We have taken out patents on these drills and drill bits.”

Having the company’s equipment selected for such a high-profile operation gives me a positive feeling about the product range here.

You can see full details of MCON’s history and products for yourself on the group’s website.

My financial information goes back to only 2010

I have to confess that I’ve been unable to determine MCON’s long-term financial history.

The group floated in November 2013 and the associated admission document provides accounts back to only 2010. My pre-2010 downloads from the Companies Registration Office (the Irish equivalent of Companies House) sadly did not disclose much in the way of useful information.

As such, I am trusting the business has a respectable track record since its formation — which may not be the case of course.

Anyway, this table summarises the figures I have:

| Year to 31 December | 2010 | 2011 | 2012 | 2013 | 2014 |

| Revenue (€k) | 33,821 | 41,145 | 63,143 | 52,343 | 54,544 |

| Operating profit (€k) | 5,789 | 12,555 | 12,724 | 15,012 | 10,350 |

| Exceptional and other items (€k) | 130 | (883) | 416 | (2,527) | 364 |

| Finance income (€k) | 287 | (406) | 88 | 52 | 535 |

| Pre-tax profit (€k) | 6,206 | 11,266 | 13,228 | 12,537 | 11,249 |

| Earnings per share (c) | 2.28* | 4.31* | 4.81* | 4.80* | 4.40 |

| Dividend per share (c) | - | - | - | - | 2.00 |

(*calculated using the post-flotation share count)

Revenues surged 87% between 2010 and 2012, which MCON explained was due to “geographic expansion”. Turnover in Europe, the Middle East and Africa during that time soared from €16m to €40m.

I should add that, during the last five years, about 75% of MCON’s top line has come from sales of its own products — the balance comes from sales of third-party drilling equipment.

Group profits since 2010 have tracked revenues higher, but did fall during 2014.

MCON mostly blamed adverse currency movements for the profit setback. Some 50% of sales last year were paid in South African Rands, Australian Dollars or Swedish Krona, the value of which all weakened against the group’s Euro-denominated cost base.

I’ve seen nothing untoward within MCON’s exceptional and other items. The negative figure for 2011 related to the sale of an under-performing joint venture, while the negative figure for 2013 consisted of a €1.2m staff flotation bonus and a €1.3m adverse currency movement on the group’s assets.

Looking ahead, MCON has hinted 2015 may be a year when the business treads water:

“In Q4 2014, we saw a marginal improvement in invoiced sales compared to Q3 2014 and Q4 2013. However, this improved trading was against a background of increased pressure on prices. We expect the primary factors driving revenue and margins to remain broadly consistent with levels experienced in 2014. The risk posed by the volatility in currency markets and the weakness in metal prices remains a concern.”

The shares, which started out at 73p, have since slid to a 54p mid-price after briefly trading below 40p.

They have £65m riding on the company…

and did not sell a share at the flotation

An important attraction to MCON for me is its long-time family boardroom.

The aforementioned Patrick Purcell is now a non-executive following his decision to step down from the role of executive chairman during 2012. Looking after the business now are his sons, Joseph and Thomas, who serve on the board as MCON’s chief technical officer and sales director respectively.

Notably, the Purcell family did not sell any shares at the flotation and retain a sizeable 57%/£65m stake.

That investment is set to produce a £1.7m annual dividend, which ought to give the family the ‘owner’s eye’ — especially when the 2013 annual report shows the Purcell executives collecting relatively modest basic salaries of close to £120,000.

I’m also pleased about the lack of any option scheme and the lack of declared bonuses for 2013. (The 2014 annual report is still to be published).

Both Joseph and Thomas Purcell are in their 40s and have held senior or board positions for the last 15 years or so — and I feel both men could be leading this business for some time to come.

Here’s an extract from the 2013 annual report, written by founder Patrick Purcell (my bold):

“My aim in founding Mincon in 1977 was to exploit the opportunity to manufacture and supply quality replacement spare parts for the rock-drilling sector of the mining industry, initially in Ireland, which then had five active mines and as soon as the products were proven on the home market, to commence our export drive.

The success of the venture in the long run was to be predicated on three core objectives:

1. A continuous programme of product and process development leading to quality products, profits and positive cash flow

2. After sales customer service and support

3. A recognition of the importance of all our people in the success of our business.

36 years later, the objectives of the Company remain the same. It is these three core objectives that we believe have driven the success of the Company over the past four decades, and will continue to drive the success of the Company for decades to come.”

And here’s an extract from the 2014 preliminary results (my bold):

“We take a medium to long term outlook of our Company and the markets that we serve. The fundamentals of profits and cash flow are healthy in Mincon. Industry cycles are a fact of life and it is the objective of the management team to ensure the effects of the troughs of these cycles are controlled and minimised. In this context, availing of opportunities in the best long-term interest of the Company and shareholders is the key objective of the Company and the Board.”

I like that long-term focus.

Assisting the Purcells is Kevin Barry, who has served as chief executive since 1990 and is a 14%/£16m shareholder. Published in March, MCON’s 2014 results sadly revealed that Mr Barry has decided to retire — and I have to say it’s a shame to lose such an experienced executive.

At least Mr Barry is staying on at the helm until a successor is found — suggesting the departure is amicable.

High margins and asset-rich… but free cash generation is not the greatest

The foundation of MCON’s accounts is the group’s substantial cash position. After raising a net €47m at the flotation, money in the bank now stands at €45m while borrowings are just €3m.

Balance-sheet bonuses include land and buildings with a €7m book value and an absence of any defined-benefit pension obligations.

Within the income statement, high margins underpin the notion that MCON has a respectable competitive advantage. The group converted 19% of revenues into profit during 2014 and above 20% during 2011, 2012 and 2013.

The superior margins also contribute to some attractive return on equity calculations.

During 2014 for example, average net assets (excluding net cash) of almost €46m generated after-tax profits of nearly €9m — a return of 20%. The same calculation has topped 20% since 2011.

However, the downside to MCON’s accounts is cash flow:

| Year to 31 December | 2010 | 2011 | 2012 | 2013 | 2014 |

| Operating profit (€k) | 5,789 | 12,555 | 12,724 | 15,012 | 10,350 |

| Depreciation and amortisation (€k) | 1,244 | 1,422 | 1,708 | 1,874 | 2,053 |

| Cash capital expenditure (€k) | (4,679) | (1,399) | (5,050) | (2,170) | (2,365) |

| Working-capital movements (€k) | (1,241) | (4,600) | (7,315) | (389) | (6,503) |

| Net cash (€k) | 3,109 | 6,682 | 7,396 | 48,600 | 41,754 |

The last five years have seen a substantial €20m sucked into working capital — of which €16m went into stock. I calculate stock-turn during 2014 was a massive 276 days — in other words, it takes around nine months before the average drill transforms from raw material into sold product.

Such high levels of stock can be a bad sign — they suggest customers aren’t buying and/or poor financial controls. But I am not sure this is the case with MCON.

The 2013 annual report provides this explanation (my bold):

“The nature of the industry in which Mincon operates requires the Group to maintain significant quantities of inventory on hand, both raw materials that have significant lead times for manufacturing plants, and finished goods in global locations to actively serve and service Mincon’s diverse customer base.”

That sounds reasonable to me. I mean, large supplies of tungsten carbide from China — or spare drill bits for miners operating in, say, Peru — probably can’t be delivered to or by MCON overnight.

On the subject of holding replacement equipment for customers, this extract from the 2013 annual report is relevant (my bold):

“The aftermarket service offering and spare parts and consumables supplies have become important components of mining equipment manufacturers’ revenue streams and are of increasing importance in a slower industry growth scenario. Higher utilisation of equipment as described above, coupled with the increase in mine supplies means that customers now demand effective service, spare parts and consumables, often in the form of contracts where availability and productivity are key criteria.”

So ‘availability’ again means having to sustain large amounts of stock. I would like to think MCON’s drills and bits can sit in a warehouse for some time — years probably — without becoming obsolete.

The other adverse feature of MCON’s cash flow is capital expenditure. The €16m spent on tangible assets over the last five years is almost double the aggregate depreciation charged against reported profits.

The difference is mostly due to MCON’s spend on land and buildings, which seems to me to be genuine expansion expenditure. This extract from MCON’s flotation document suggests capex will diminish in the near future (my bold):

“Mincon has adopted a long term approach to ensure that Mincon’s facilities and equipment meet the needs of future business and projects. This approach led to Mincon’s timely expansion into its modern and purpose built facilities in Benton, Illinois in the USA and Perth, Australia to adequately meet the needs of customers and suppliers in these two important markets. Mincon has invested approximately €13.0 million over the last three and a half years in capital expenditure projects resulting in spare capacity for future growth and significantly lower capital expenditure being anticipated on existing facilities over the next three years.”

My sums suggested a P/E of 10.4

I purchased MCON shares both before and after the group issued its 2014 annual results on 9 March.

My sums before the results assumed a doubling of first-half 2014 operating profits to €10.3m and that net cash was €41.2m. I also used a £:€ exchange rate of 1.37.

As it happens, the 2014 annual results showed full-year operating profits of €10.4m and net cash of €41.8m — so a fraction better than my forecasts. But the £:€ rate had moved to 1.39, which negated the increases.

Anyway, using the figures from the 2014 annual results, a €10.4m operating profit converted at £:€ 1.39 gave a £7.5m operating profit, which after MCON’s 18% tax rate produced earnings of £6.1m or 2.9p per share.

Subtracting the €41.8m (£30.0m) net cash position from the £94m market cap (at my 44.6p purchase price), I arrived at an enterprise value of £64m or 30p per share.

I then divided that 30p by my 2.9p per share earnings guess and determined the underlying P/E to be 10.4.

For a business that appeared to enjoy a respectable competitive advantage, I felt that P/E rating was too low — and could offer robust upside possibilities if or when profits regained their momentum.

Last year’s €0.02 dividend is equivalent to 1.44p per share and supported a 3.2% income on my 44.6p buy price.

At the recent 56p offer price, I make MCON’s P/E to be 14.3 and the dividend yield to be 2.6%.

Profits could easily follow these charts lower

When MCON’s profits will regain their momentum is hard to say.

The group serves the mining sector, where activity and expenditure is correlated to the direction of metal prices. Here are a few extracts from MCON’s results that emphasise the firm’s dependence:

“Mincon’s largest customer market for product sales is the global mining industry.

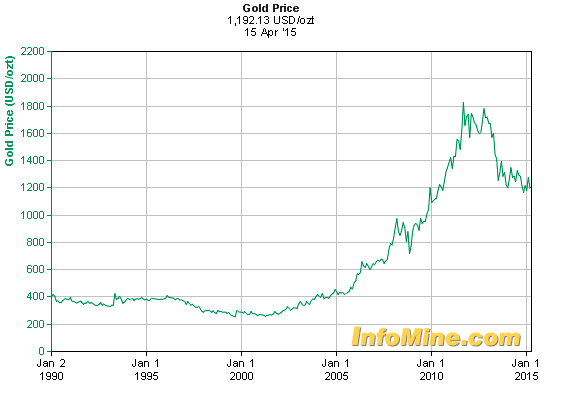

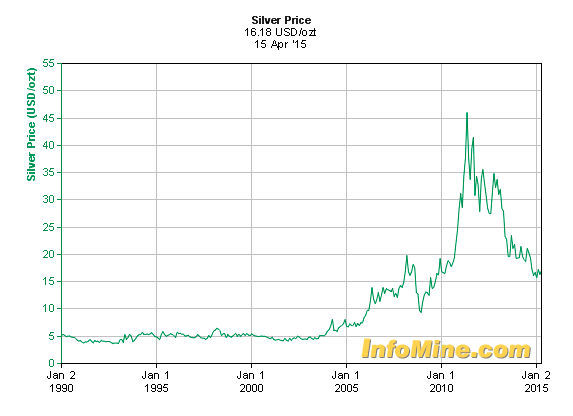

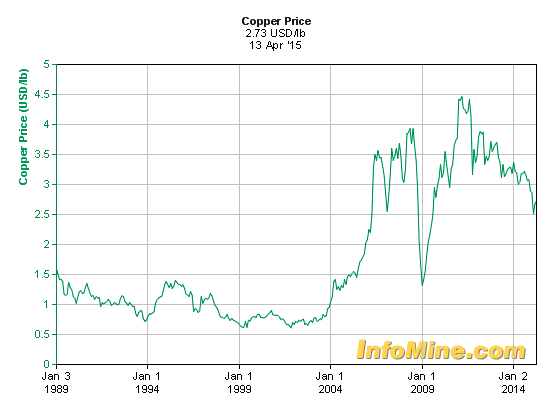

This industry is currently experiencing a period of contraction after recent years of strong growth. Metals commodities prices have fallen steadily since their peak in 2011 back to levels not seen since late 2008… These declines forced many participants in the industry to start reducing their capital expenditure spends in line with this.”

“The weakness in the global exploration and mining market, driven by the decline in the price of precious metals, which was a feature of 2013 and, as indicated in our annual results published in April 2014, continued into 2014 impacting the drilling products market in which we operate, particularly in relation to third party product.”

“The decline in the commodity prices of base and precious metals such as gold, iron ore and copper has had a major impact on the global exploration and mining market and has also been a factor in the significant devaluation of certain key currencies in which we trade, particularly the South African Rand and the Australian Dollar.”

The following charts show a range of metal prices all well below their peaks:

I have no insight as to when such commodities could rally — or whether they could even decline further. Indeed, there’s a real chance MCON may find trading tough going for some time to come.

That said, global miners continue to mine and their hammers and drill bits will all need replacing at some point. And MCON does serve other sectors — such as construction and utilities — where demand is not correlated to metal prices.

This ambitious plan could hammer my investment

The other risk to my investment is acquisitions.

I am not a great fan of companies that grow by acquisition — all too often such strategies go badly wrong for shareholders — but I recognise a few class operators can get it right over the long run. Halma is one great example.

Nonetheless, MCON set out an ambitious acquisition plan within its flotation document that could see that aforementioned cash pile all spent on new businesses:

“Mincon has identified a pipeline of acquisition targets which are designed to: (i) extend the existing product range; or (ii) defend margins or secure the supply of raw materials; or (iii) add new products which are complementary to the existing product range or which add new customers and/or new geographic markets. Preliminary discussions have taken place with a number of candidates which are well known to Mincon. These represent a good geographic spread of opportunities and consideration payable on individual acquisitions is expected to be based on enterprise value in the region of €10-30m.”

Last year MCON spent (or committed to spend) about €13m on a trio of deals, which could add a further €8-9m to 2014 sales during 2015.

At the time of the purchases, MCON claimed the acquisitions were “expected to be profit enhancing from H1 2015” — so at least I have that contribution to look forward to in the next results.

To date, MCON’s deals have all been small affairs and I am quite happy with the acquisition progress made. Indeed, I get the impression MCON timed its flotation very well — raising a €47m war chest to buy smaller rivals and suppliers when valuations in the sector may not be that outlandish.

But there is a real danger that MCON’s ambitions — the group has said it wants to double its size between 2013 and 2015 — could put pressure on the executives to rush into an awful deal that puts the entire cash pile at risk.

I would like to think MCON’s family board will be able to resist the temptation to do something incredibly silly, but you never can tell with company directors.

I would have bought more had the price not risen

I feel there’s a lot to like about MCON. The family management has appeal, the competitive position appears attractive, the high margins and cash in the bank are very welcome, while my P/E valuation at the time of purchase offered good re-rating potential.

True, MCON’s financial track record is not entirely clear and I have taken for granted the boardroom can produce worthwhile returns for investors.

Nonetheless, the business has been running since 1977, has grown into a significant operation and — quite notably — the executives did not sell a single share at the float. So at least those signs are positive.

I’m also taking a gamble with MCON’s acquisition plan. The cash pile, which currently represents about a quarter of the market cap, could soon be exchanged for a few new subsidiaries — the expected benefits from which may not be realised. I guess it’s also possible MCON could take on some debt to fund a major deal.

Plus cash flow is not the best I have ever seen. A lot of profit is being tied up in extra stock and I hope such expenditure can moderate from here. Otherwise I may have to consider whether MCON’s cash generation is enough to support reported earnings.

All that said, I think the upsides here outweigh the downsides and my purchases currently leave MCON representing about 3-4% of my portfolio. I would have bought more had it not been for the price rising after the results.

Finally, let me just explain that MCON is dual traded on AIM and in Dublin. I could buy only the AIM-traded MCON shares through my cheap online brokers, but I see the Dublin-quoted MIO shares do tend to have a much smaller bid-offer spread. I must add that Irish shares attract 1% stamp duty — which I’d forgotten about until I saw my first MCON contract note!

Until next time, I wish you happy and profitable investing!

Maynard Paton

Disclosure: Maynard owns shares in Mincon.

Pays the divvy in euros as well as the 1% :-(

apad

2014 annual report now published and available:

http://www.mincon.com/wp-content/uploads/2015/04/Mincon-Annual-Report-2014.pdf

Something I noted in MCON’s annual report is the management commentary it contains is far more comprehensive than the commentary issued within the original results RNS. As such the report is certainly worth inspecting.

Here are the points that interested me:

1. RC hammer sales

This is the first time I think that MCON has disclosed sales of RC hammers (before, they were lumped in with HDD product sales). 7% of €54,544k is €3,818k of RC sales. Figure for 2013 was €4,711k. So total RC hammer revenue down 19%. It seems as if Rotary product sales were €3,250k which leaves HDD product sales (for utilities drilling trenches) of €2,750k.

2. Lower capex

I am pleased there is lower capex forecast for the next three years.

3. Acquisition target extended for a year

MCON says it is still looking for deals in the range of €10-30m but I see the objective may extend for up to another 24 months. At the flotation, MCON’s target to double the size of the company was to be achieved by the end of 2015. I am pleased the board has not become fixated about sticking to the end-2015 target and I hope the executives remain disciplined with any deals. I see total sales from acquisitions would have been almost €16m for the full year.

4. Dividend might not be lifted

This is a slightly odd statement about the dividend — it reads as if the payout will be held at the current ¢0.02 level for the foreseeable future. I suppose that could happen.

5. Director pay

I could not see much to worry about here. Joseph Purcell’s €175k wage is equivalent to £127k and does not look excessive for running a business with profits of c£7m. I see no bonuses were paid in 2013 and 2014, too. It will be interesting to see the level of pay the replacement for Kevin Barry receives.

6. Contractual risks may have diminished?

The small print in the Risks section contained a slight change from the 2013 annual report. The line “The Group must often negotiate complex terms and conditions in large sales transactions and in many instances contracts are of a fixed price nature” was dropped for 2014, suggesting such a risk may be less likely from now on. Well, here’s hoping.

I’ll post a further comment if I find anything else of interest.

Maynard

New chief executive appointed:

http://www.investegate.co.uk/mincon-group-plc–mcon-/rns/appointment-of-new-chief-executive-officer/201505110700247145M/

The Board of Mincon is pleased to announce the appointment of Joe Purcell as the new Chief Executive Officer of the Group, effective from 28 May 2015 after the conclusion of the 2014 Annual General Meeting for Mincon Group plc. Joe is appointed CEO Designate with immediate effect.

I am happy with this decision. Joe Purcell is the son of the group’s founder, has worked at the firm for 31 years and was responsible for a lot of product development as Chief Technical Officer. He seems to be a safe pair of hands to me, and I do like to see a product person (as opposed to an accounting person) in charge at my shares. I see today’s announcement also reveals “two senior appointments” have been made to the R&D team, which hopefully can sustain MCON’s product development as Joe Purcell takes on the chief exec duties.

Maynard

Just been told by my broker that my final dividend will be two weeks late :-(

This EUR cheque was paid to us on 29th, we have to wait for this to clear and then convert the dividend into sterling. This will due to be credited around 9th or the monday after this on the 12th. Sorry for the delay but we are trying to process this as soon as possible.

Should have been paid on the 26th June.

Ok, so my final dividend from the broker above was received on 8th July and backdated to 26th June.

Chased up my other broker on 9th July after realising I had some MCON shares under its administration. Here is that broker’s reply:

“I can confirm we are currently waiting for our Custodians to receive the dividend. I have passed a chaser to the relevant department and they have ensured me as soon as the dividend arrives it will be applied to your account.”

I will confirm when this dividend is paid. Certainly this is an interesting comparison between broker administration of a EUR-based share and dividend payer.