05 November 2020

By Maynard Paton

Results summary for Tristel (TSTL):

- Revenue and profit reached new highs following very satisfactory 20%-plus growth, bolstered in part by the pandemic.

- The UK performance appeared odd, given H2 sales were lower than H1 despite the Covid-19 boost.

- Overseas sales surged 35% during H2, with the purchase of Ecomed during 2018 now proving to be a great success.

- The accounts remain in good shape with high margins, appealing equity returns, net cash and respectable cash generation.

- A possible P/E of 39 might be justified if the pandemic leads to permanently greater demand for hospital disinfectants. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own TSTL

- Results summary

- Capitalising on Covid-19

- Revenue, profit and dividend

- UK

- Western Europe

- Tristel Italia

- United States

- Other overseas markets

- Cache, Rinse Assure, Byotrol and MobileODT

- Share options

- Financials

- Valuation

Event links, share data and disclosure

Event: Final results, online presentation and annual report for the twelve months to 30 June 2020 published 19 October 2020

Price: 480p

Shares in issue: 46,485,508

Market capitalisation: £223m

Disclosure: Maynard owns shares in Tristel. This blog post contains Sharepad affiliate links.

Why I own TSTL

- Develops medical-instrument disinfectants that are repeat-purchase and face limited direct competition due to multiple patents, manufacturer approvals, scientific testimonies, secret ingredients and regulatory hurdles.

- Enjoys a sizeable and resilient UK market position alongside significant expansion opportunities abroad.

- Boasts financials that showcase high margins, robust returns on equity, decent cash flow and no debt.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary

Capitalising on Covid-19

- Management remarks at February’s H1 presentation included strong hints that TSTL would enjoy a good pandemic.

- A trading statement during July then revealed additional revenue of £1.5m was earned between March and June due to Covid-19.

- TSTL said the £1.5m Covid boost was a result of hospitals spending £2m more on surface disinfectants and £0.5m less on medical-device disinfectants.

- The July update was perhaps not the sensational statement some had expected.

- Encompassing the March-June period, total H2 revenue gained 20% but would have advanced only 10% without the £1.5m Covid boost.

- The 10% ex-Covid growth rate for H2 was at the bottom end of TSTL’s 10%-15% guidance for annual sales growth.

- July’s statement disclosed March-June revenue surged 30% to £11.8m, which implied January-February revenue gained only 4% to £5.2m:

| Jan-Feb 2019 | Mar-Jun 2019 | H2 2019 | Jan-Feb 2020 | Mar-Jun 2020 | H2 2020 | ||

| Revenue (£k) | 5,051 | 9,100 | 14,151 | 5,244 | 11,800 | 17,044 | |

| Covid-19 boost (£k) | - | - | - | - | (1,500) | (1,500) | |

| Less Covid-19 boost (£k) | 5,051 | 9,100 | 14,151 | 5,244 | 10,300 | 15,544 |

- July’s numbers also implied March-June revenue climbed 13% excluding the £1.5m Covid boost.

- TSTL was confident the pandemic would be positive for the group.

- This FY 2020 statement declared:

“We expect the legacy of COVID-19 to be that hospitals will be more rigorous in their selection of the best performing and most scientifically validated disinfectant products, which will benefit our Company, and that the frequency of cleaning and disinfection practice will increase.”

- Mind you, the postponing of hospital appointments — which in turn lowers demand for TSTL’s medical-instruments disinfectants — may continue should lockdowns re-occur. The results admitted:

“…Hospital diagnostic medical procedures which create the demand for the Group’s medical device disinfectants fell during the pandemic as hospital out-patient departments closed…

The Board expects the medical device disinfectant custom base to remain intact and sales to recover, however, the timing of this bounce-back is dependent upon hospital medical procedures returning to pre-COVID-19 numbers.

The key risk to the business is that medical device sales do not return at a pace which allows the Group’s sales to continue at their existing growth trajectory.”

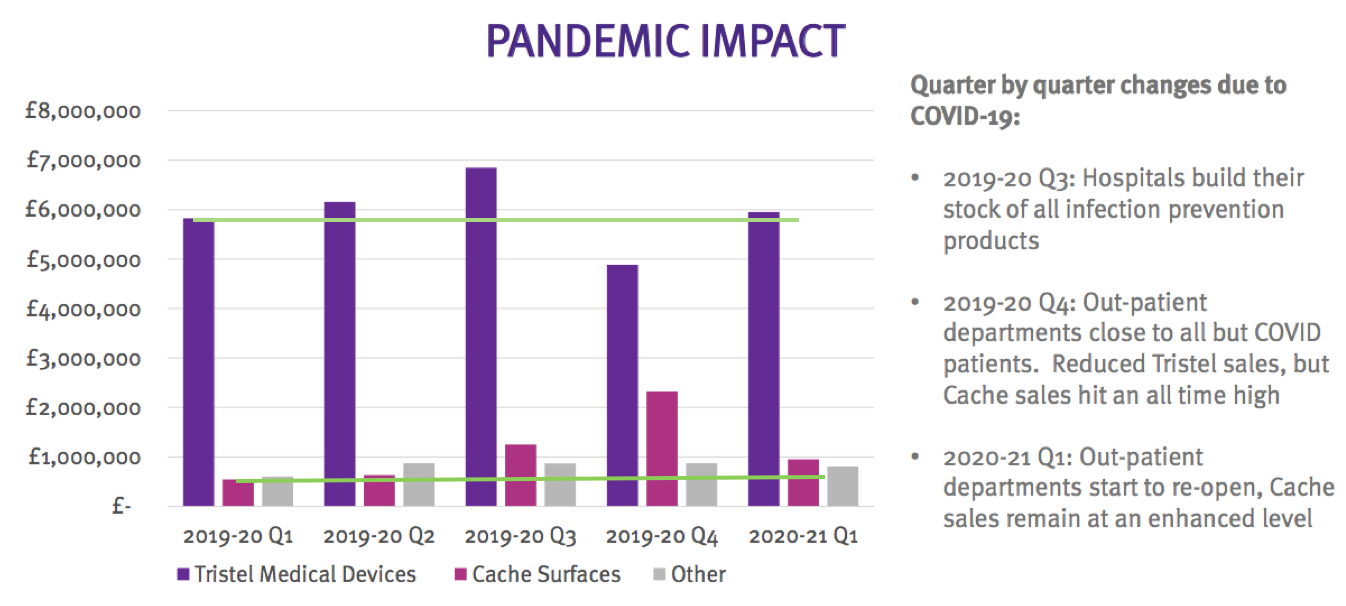

- The results presentation commendably outlined the group’s revenue for the first quarter of the current year (July-September 2020):

- My green lines show Q1 2021 revenue from medical-device disinfectants (purple bars) and hospital-surface disinfectants (red bars) are above the corresponding levels of Q1 2020 — although not by huge amounts.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue, profit and dividend

- July’s update said these annual results would show revenue of “no less than £31.6m” and adjusted pre-tax profit (before share-based payments) of “at least £6.8m”.

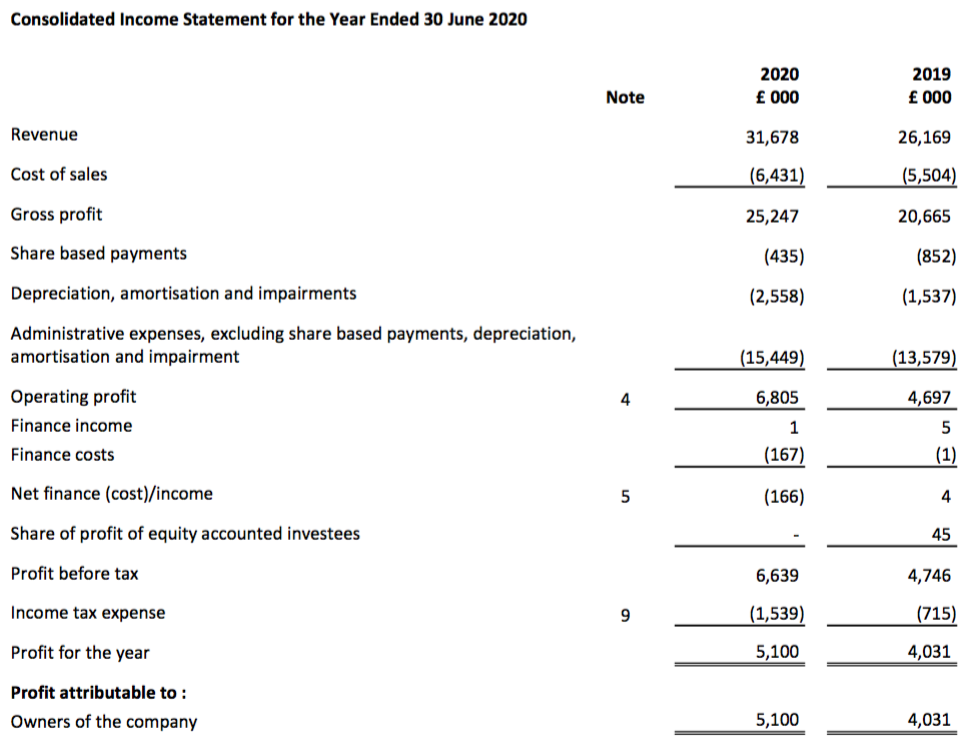

- In the event, revenue was indeed no less than £31.6m at £31.678m (up 21%) while adjusted pre-tax profit (before share-based payments) was indeed at least £6.8m at £7.074m (up 26%).

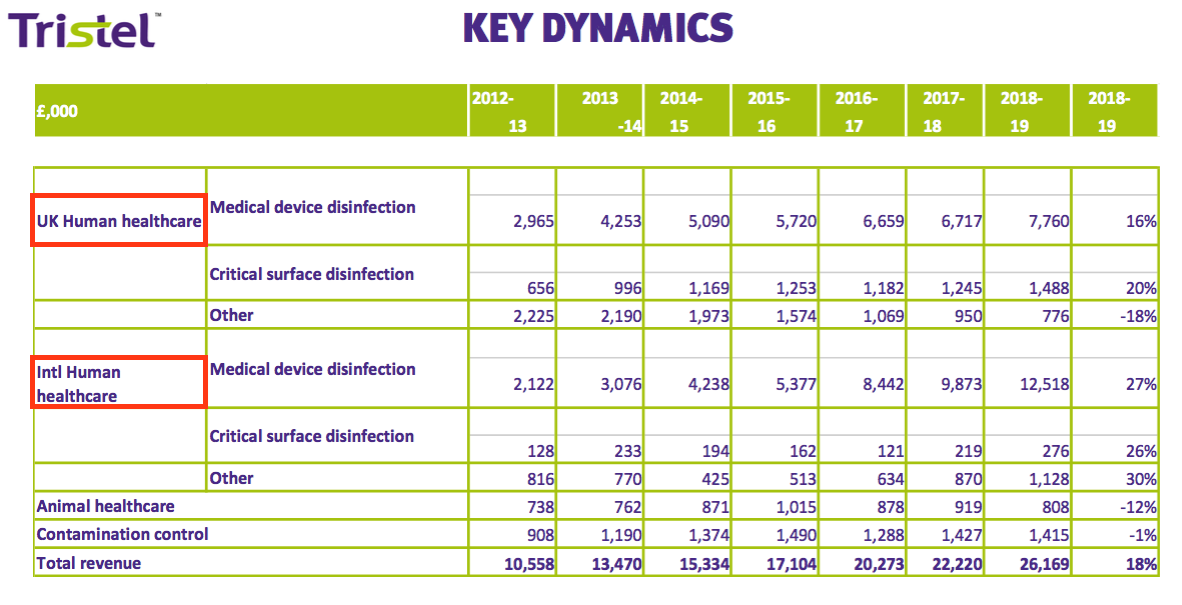

- The results registered fresh all-time highs for revenue and profit for the seventh consecutive year:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 17,104 | 20,273 | 22,220 | 26,169 | 31,678 |

| Operating profit (£k) | 2,568 | 3,902 | 3,980 | 4,697 | 6,805 |

| Associates (£k) | 13 | 19 | 24 | 45 | - |

| Finance income (£k) | 12 | 4 | 2 | 4 | (166) |

| Other items (£k) | - | 41 | - | - | - |

| Pre-tax profit (£k) | 2,593 | 3,966 | 4,006 | 4,746 | 6,639 |

| Earnings per share (p) | 5.01 | 8.06 | 7.62 | 9.14 | 11.38 |

| Dividend per share (p) | 3.33 | 4.03 | 4.58 | 5.54 | 6.18 |

| Special dividend per share (p) | 3.00 | - | - | - | - |

- Alongside Covid-19, the FY 2020 performance was bolstered by the purchases of Ecomed (‘Western Europe’ — Belgium, the Netherlands and France) during November 2018 and Tristel Italia during July 2019:

- Excluding Ecomed and Tristel Italia, full-year revenue gained 10% to £26.4m and H2 revenue advanced 11% to £13.8m.

- Management claimed during the online presentation that Ecomed experienced underlying revenue growth of 34% (see Western Europe below).

- UK revenue advanced 7%, although the improvement was weighted significantly towards the first half (see UK below).

- A re-jig of TSTL’s divisional reporting made certain comparisons with previous years impossible.

- The UK and Europe are now lumped together…

- …whereas before the UK was separate and Europe was part of ‘International’:

- TSTL’s underlying profit advance was again tough to interpret. The figures remain complicated by:

- Notable share-based payments (see Share options below);

- Costs associated with the US regulatory project (see United States below);

- Fair-value investment gains (see Financials below), and;

- Undisclosed contributions from acquisitions (see Western Europe and Tristel Italia below).

- The following table calculates operating profit before share-based payments, US costs and fair-value investment gains:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Operating profit before SBP, US costs and FV gains (£k) | 2,485 | 3,466 | 5,951 | 3,106 | 4,103 | 7,209 | |

| Share-based payments (£k) | (196) | (656) | (852) | (234) | (201) | (435) | |

| US costs (£k) | (100) | (400) | (500) | (150) | 70 | (80) | |

| Fair-value gains (£k) | - | 98 | 98 | 111 | - | 111 | |

| Operating profit (£k) | 2,189 | 2,508 | 4,697 | 2,833 | 3,972 | 6,805 |

- Full-year operating profit before share-based payments, US costs and fair-value investment gains advanced 21%, with H1 up 25% and H2 up 22%.

- After the interim dividend was lifted 15%, the final dividend was raised only 10% to 3.84p per share.

UK

- UK revenue gained 7% for the year, with a 14% uplift during H1 receding to just a 2% improvement for H2:

| Revenue | H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | |

| UK (£k) | 5,610 | 6,186 | 11,796 | 6,380 | 6,290 | 12,670 | |

| Overseas (£k) | 6,408 | 7,965 | 14,373 | 8,254 | 10,754 | 19,008 | |

| Total (£k) | 12,018 | 14,151 | 26,169 | 14,634 | 17,044 | 31,678 |

- No explanation was given as to why UK H2 revenue was slightly lower than the level set during H1.

- The lower UK H2 performance is very surprising given the inclusion of the March-June Covid-19 boost.

- February’s results denied Brexit stock-piling had caused the bumper H1 performance, so that explanation for a lower H2 can be ruled out.

- Other possible explanations for so-so UK revenue during H2 include:

- Reduced income from ‘legacy’ products;

- Unpredictable order timings from the NHS supply chain and;

- Distortions arising from one-off price increases implemented during January 2019.

- Revenue earned from the NHS supply chain, TSTL’s largest customer, fell 2% during the year:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue from largest customer (£k) | 4,828 | 5,138 | 5,357 | 6,595 | 6,487 |

| Proportion of total revenue (%) | 28.2 | 25.3 | 24.1 | 25.2 | 20.5 |

- Reduced revenue from the NHS supply chain is another surprising development given the Covid-19 boost.

- The UK H1/H2 revenue split alongside the lower income from the NHS supply chain suggest something untoward is developing within the UK division.

- Perhaps that is why TSTL decided to re-jig the segmentation reporting and lump the UK together with Europe — that way any adverse UK developments would not be so obvious to outsiders.

- But is something really untoward occurring within the UK division? I am not sure.

- UK H1/H2 revenue growth has shown marked variations in the past, with year-on-year declines recorded for H2 2017 and H1 2018:

| Revenue growth (%) | UK H1 | UK H2 | UK FY | Overseas H1 | Overseas H2 | Overseas FY |

|

| 2012 | 2.6 | 10.6 | 6.5 | 100.8 | 117.0 | 110.8 | |

| 2013 | (28.9) | (9.5) | (18.9) | 74.7 | 52.8 | 60.8 | |

| 2014 | 47.3 | 8.3 | 24.9 | 44.1 | 25.9 | 33.1 | |

| 2015 | 11.5 | 8.5 | 10.0 | 23.3 | 20.0 | 21.4 | |

| 2016 | 2.2 | 8.7 | 5.4 | 20.2 | 24.2 | 22.5 | |

| 2017 | 8.6 | (2.5) | 3.0 | 44.9 | 40.6 | 42.4 | |

| 2018 | (3.6) | 7.1 | 1.5 | 28.1 | 11.2 | 18.6 | |

| 2019 | 4.8 | 12.9 | 8.9 | 19.3 | 32.5 | 26.2 | |

| 2020 | 13.7 | 1.7 | 7.4 | 28.8 | 35.0 | 32.2 |

- TSTL’s UK division then performed very well after those 2017/2018 fluctuations.

- TSTL’s competitive ‘moat’ — a large collection of patents, industry verifications and manufacturer approvals — presumably ensured the 2017/2018 ups and downs evened out thereafter.

- Assuming TSTL’s competitive ‘moat’ remains wide, I am hopeful the FY 2020 UK performance should not prove cause for concern.

- My ten-bagger experience with TSTL (point 4) tells me not to worry too much about short-term revenue variations:

“Tristel’s management has over time batted away all sorts of questions about patents and competition, and as a result I have developed a greater understanding of the products’ inherent strengths. I have in turn become less concerned about short-term growth rates, valuation multiples and the weighting of the investment in my portfolio.”

- Mind you, I have my fingers crossed the UK fluctuations are due to nothing more than lower legacy income and/or unpredictable NHS ordering and/or distortions following price increases.

Western Europe

- TSTL purchased Ecomed — the distributor of TSTL’s products in Belgium, the Netherlands and France — during November 2018 for £6.4m including subsequent earn-outs.

- FY 2020 was therefore the first year during which Ecomed contributed for the full twelve months.

- Ecomed (‘Western Europe’) registered annual revenue of £4.6m, with H2 sales surging 64% to £2.85m:

| Overseas revenue | H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | |

| Australasia (£k) | 1,660 | 1,639 | 3,299 | 1,700 | 1,830 | 3,530 | |

| China & Hong Kong (£k) | 560 | 622 | 1,182 | 620 | 1,000 | 1,620 | |

| Germany/Central Europe (£k) | 2,230 | 2,380 | 4,610 | 2,490 | 2,830 | 5,320 | |

| Western Europe (£k) | 400 | 1,740 | 2,140 | 1,750 | 2,850 | 4,600 | |

| Italy (£k) | - | - | - | 300 | 370 | 670 | |

| Total in-house (£k) | 4,850 | 6,381 | 11,231 | 6,860 | 8,880 | 15,740 | |

| Distributors (£k) | 1,560 | 1,582 | 3,142 | 1,390 | 1,880 | 3,270 | |

| Total (£k) | 6,410 | 7,963 | 14,373 | 8,250 | 10,760 | 19,010 |

- New regulatory rules in France, which management claimed in February had created a “fantastic vibrant market”, underpinned the performance.

- Ecomed revenue of £4.6m is equivalent to €5.3m at the average 1.16 GBP:EUR seen during the year.

- Prior to purchase, Ecomed’s annual sales were €3.1m.

- Ecomed’s revenue may therefore be 71% (€5.3m / €3.1m) higher than two years ago.

- Prior to purchase, 18% of Ecomed’s revenue related to non-TSTL products. The improvement to TSTL-product sales may therefore be greater than my 71% calculation.

- TSTL has never disclosed Ecomed’s profit contribution, so how much of the FY 2020 profit lift was due to buying Ecomed remains guesswork.

- Still, Ecomed’s surging sales suggest the purchase has been a great success.

- The appointment of Bart Leemans, Ecomed’s former owner, as a TSTL executive director could explain the division’s upbeat progress.

- Mr Leemans enjoys a 2%/£5m TSTL shareholding, which may also explain Ecomed’s performance.

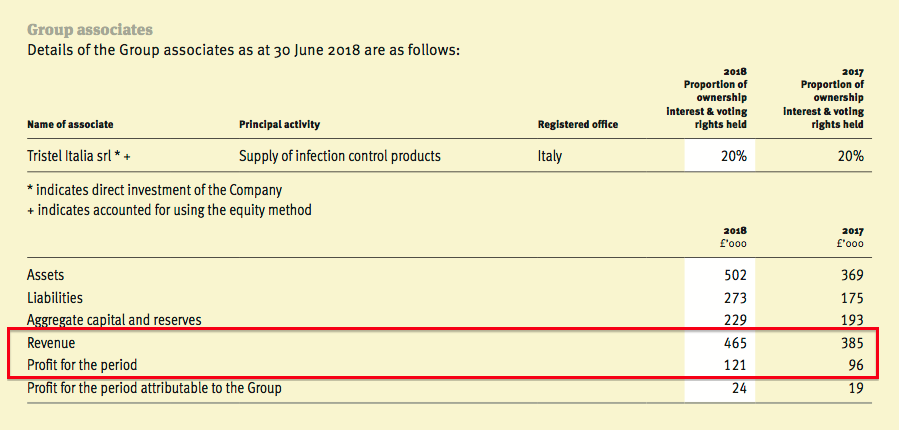

Tristel Italia

- TSTL previously owned 20% of the Italian distributor, and paid £595k for the other 80%.

- During FY 2019, the 20% investment gave TSTL a £45k share of the operation’s £225k profit:

- Neither this results RNS nor the online presentation mentioned the profit impact of Tristel Italia for FY 2020.

- Tristel Italia had been expanding fast prior to its acquisition:

| Year to 30 June | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 207 | 238 | 285 | 385 | 465 |

| Profit (£k) | 40 | 38 | 66 | 96 | 121 |

- The purchase announcement said Italian sales for FY 2019 were €700k, equivalent to approximately £620k at the average 1.13 GBP:EUR seen during those twelve months.

- The FY 2020 powerpoint showed Tristel Italia revenue of £670k — an 8% increase on my £620k calculation for FY 2019.

- An 8% revenue increase for Italy does not seem great when Western Europe (Belgium, the Netherlands and France) apparently enjoyed 34% underlying growth while Central and Eastern Europe (mostly Germany) advanced sales by 15%.

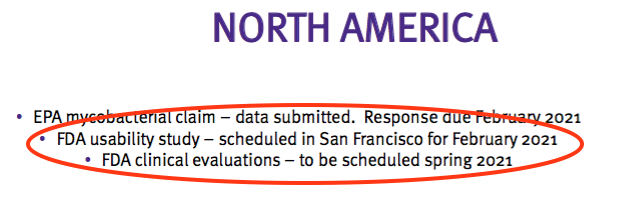

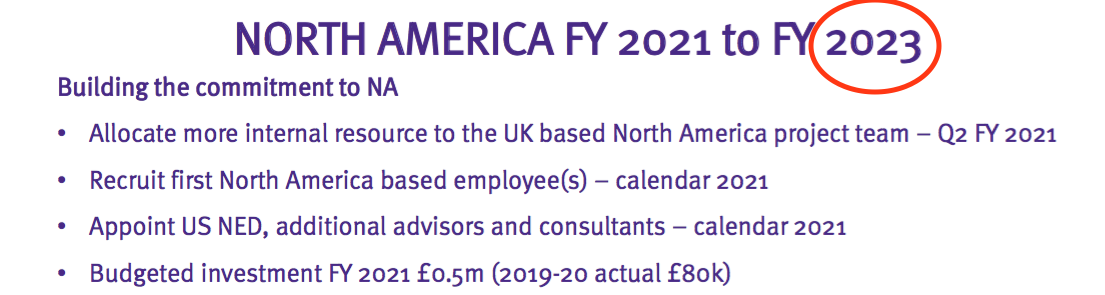

United States

- The online presentation provided the first (relatively) encouraging news about the United States for some time.

- To recap, TSTL started its US project during 2014, bungled an FDA pre-application during 2018, withdrew all timescale guidance during 2019 and is still to submit a formal product application for approval.

- Until February’s interims, TSTL had hoped to submit its Duo foam for cleaning ultrasound probes, nasendoscopes and ophthalmic instruments for FDA approval.

- February’s interims then implied the Duo applications for nasendoscopes and ophthalmic instruments had been quietly dropped.

- However, the latest slides indicate TSTL will restart its Duo applications for nasendoscopes and ophthalmic instruments:

- Wishful thinking perhaps, but the reinstatement of the two Duo applications may be due to positive noises emerging from the FDA and/or project insiders.

- Completely new FDA work for Stella and Rinse Assure is also promising, as is talk of recruiting the first US employee and a US non-exec.

- That said… the protracted progress of the US project to date prevents me from becoming too excited by the revived/new applications.

- The US project will cost £750k during FY 2021 to cover the existing and new applications.

- Total US project expenditure to date has been £1.8m, the return from which has of course been zero:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit before US costs (£k) | 2,698 | 4,402 | 4,480 | 5,197 | 6,885 |

| US costs (£k) | (130) | (500) | (500) | (500) | (80) |

| Operating profit (£k) | 2,568 | 3,902 | 3,980 | 4,697 | 6,805 |

- H1 2020 recorded US costs of £150k, indicating a £70k refund was received during H2.

- The US costs are expensed entirely against earnings.

- When exactly TSTL will submit a formal product application to the FDA remains anyone’s guess.

- The results powerpoint revealed a study and an evaluation are scheduled for the second half of FY 2021:

- The powerpoint also referred to 2023:

- I had previously guessed/hoped TSTL would submit an FDA application during calendar 2021.

- Further Covid-19 disruption to the project’s logistics could mean a submission (and perhaps approval) is postponed to calendar 2022.

- Meaningful US revenue may then occur during 2024, some ten years after the project was launched.

- No update was given on the likely US revenue model, which management has previously claimed would be through a 17.5% royalty on product sales derived from US manufacturing partner Parker Laboratories.

Other overseas markets

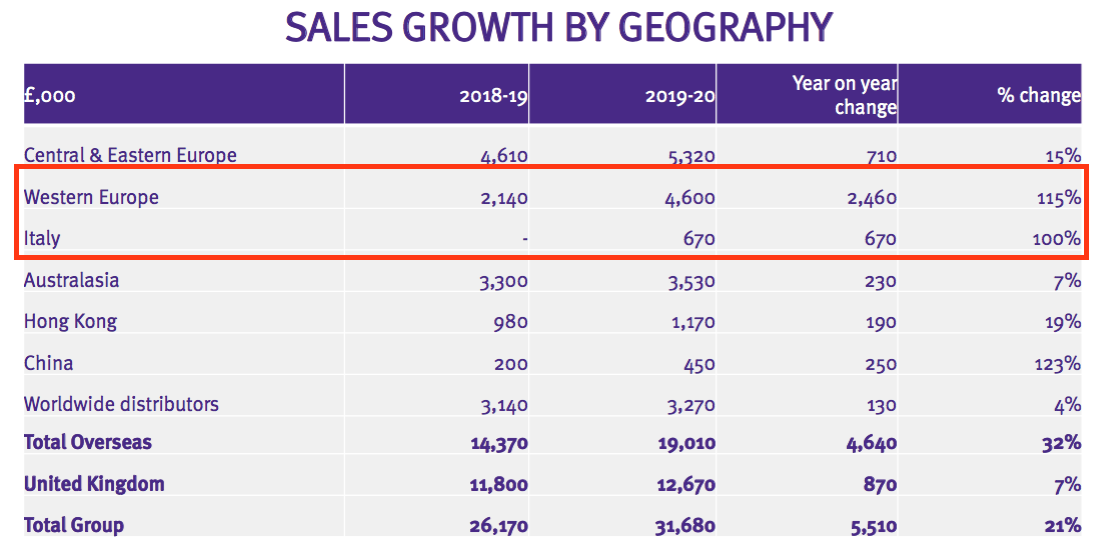

- Ecomed and Tristel Italia helped FY 2020 overseas revenue climb 32%, with a 35% uplift during H2:

| Overseas revenue | H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | |

| Australasia (£k) | 1,660 | 1,639 | 3,299 | 1,700 | 1,830 | 3,530 | |

| China & Hong Kong (£k) | 560 | 622 | 1,182 | 620 | 1,000 | 1,620 | |

| Germany/Central Europe (£k) | 2,230 | 2,380 | 4,610 | 2,490 | 2,830 | 5,320 | |

| Western Europe (£k) | 400 | 1,740 | 2,140 | 1,750 | 2,850 | 4,600 | |

| Italy (£k) | - | - | - | 300 | 370 | 670 | |

| Total in-house (£k) | 4,850 | 6,381 | 11,231 | 6,860 | 8,880 | 15,740 | |

| Distributors (£k) | 1,560 | 1,582 | 3,142 | 1,390 | 1,880 | 3,270 | |

| Total (£k) | 6,410 | 7,963 | 14,373 | 8,250 | 10,760 | 19,010 |

- Overseas income now represents 60% of total revenue, up from 36% during 2015 and 9% during 2010.

- Excluding Ecomed and Tristel Italia, FY 2020 overseas revenue from in-house subsidiaries gained 15%, with a 22% uplift during H2.

- Covid-19 ensured every overseas division reported record yearly sales.

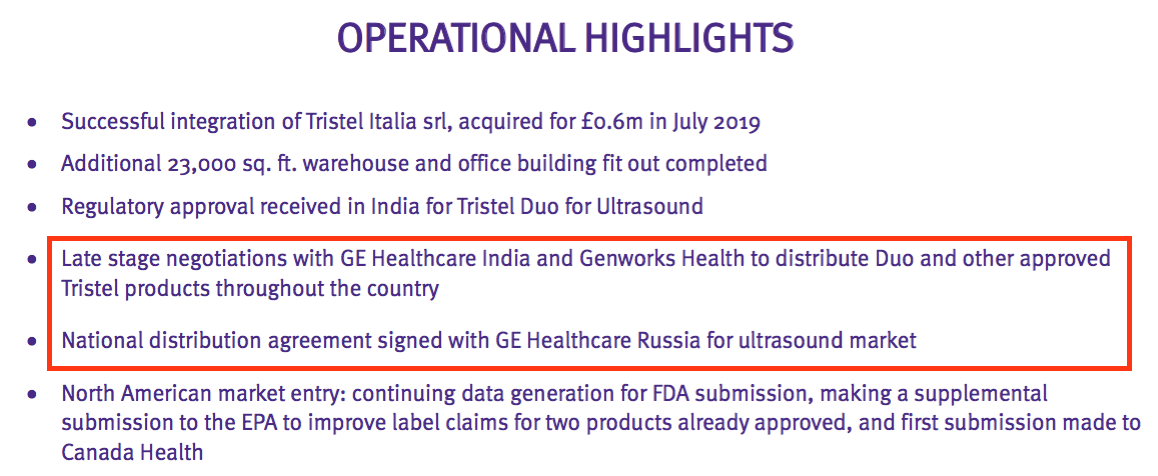

- Two new in-house international subsidiaries ought to help progress during FY 2021.

- The Malaysian distributor joined TSTL after the year-end and management remarks during February’s presentation claimed the operation enjoyed “close on £1m of gross sales to hospitals”.

- The subsidiary in India should commence trading during FY 2021 following approval of the group’s Duo foam for disinfecting ultrasound probes, ophthalmic instruments and colposcopes.

- The online presentation highlighted a tie-up with GE and a GE-backed healthcare business to kick-start Indian sales:

- GE is also helping TSTL within its fledgling Russian market.

- Future overseas markets can be gleaned from the annual report, which for the first time mentions an inactive subsidiary in Ireland alongside the United States and Japan:

Cache, Rinse Assure, Byotrol and MobileODT

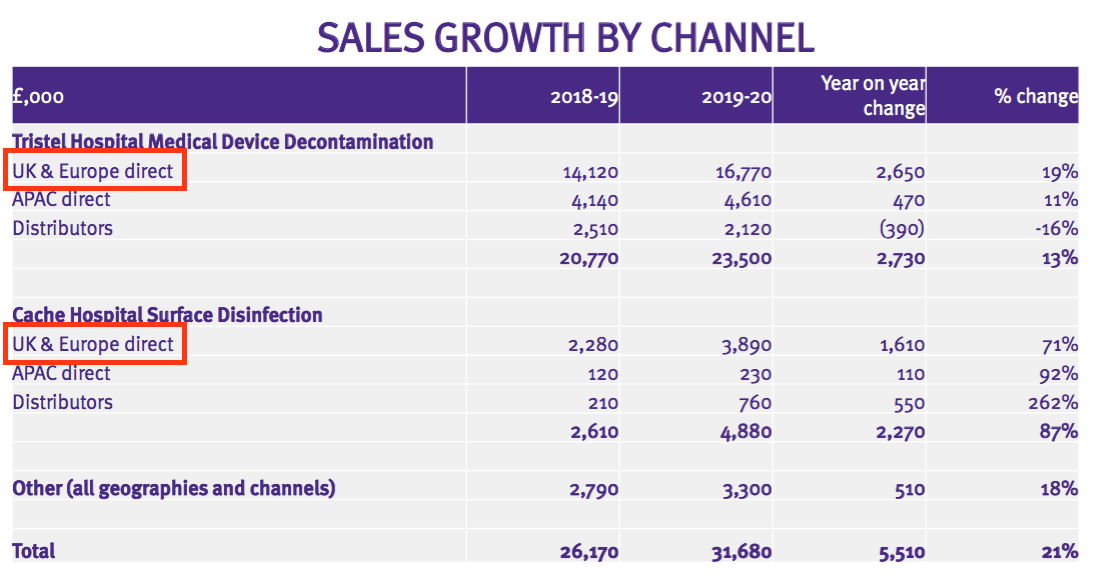

- This year’s star product was Cache, a disinfectant used by hospitals for cleaning mattresses, bedside tables and other surfaces touched by patients.

- Total hospital-surface disinfectant sales surged by £2.2m, or 87%, to £4.9m.

- As mentioned earlier, £2m of that £2.2m surge was due to Covid-19.

- Still, the Cache product has finally come good after some years in the doldrums.

- Back in February 2018, Cache was called Shot and featured prominently within results presentations:

- The product was then revamped (here and here) before going quiet during 2019…

- …only to burst into life following the pandemic.

- The eventual success of Shot (now Cache) gives hope of other TSTL products one day coming good.

- In particular, Rinse Assure was touted as a possible money-spinner in February…

- … but the product was barely mentioned this time around.

- The post-results Q&A document revealed Rinse Assure revenue of £175k, split £72k for H1 and £103k for H2.

- In addition, an arrangement with Byotrol prompted an RNS in March… yet the arrangement was not mentioned in these results.

- Another slow-burner is the MobileODT investment.

- This investment was made during 2017, and subsequent presentations showcased persuasive slides about disinfecting mobile colposcopes:

- Yet for the last year or two, TSTL has barely mentioned its £807k MobileODT shareholding.

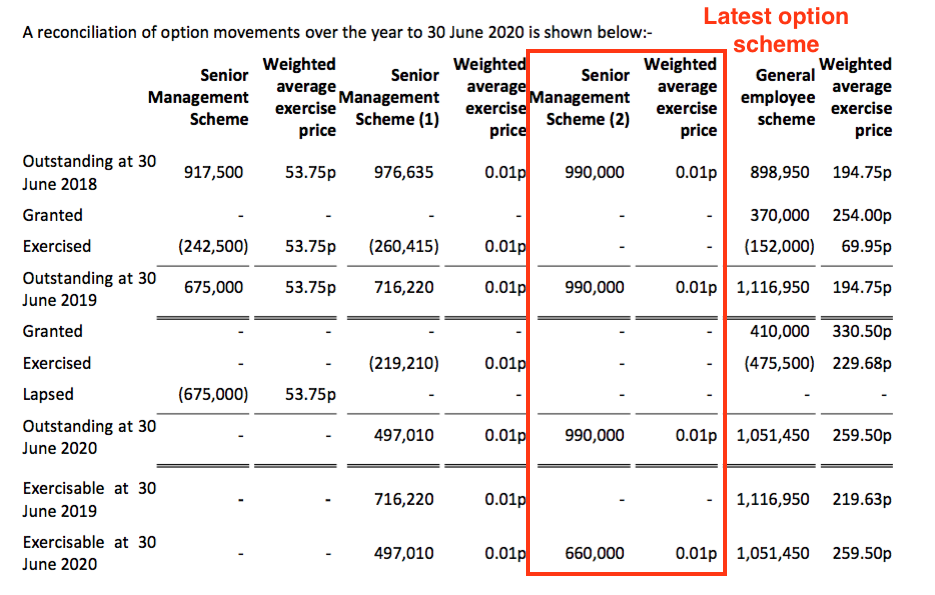

Share options

- Significant share-based payments have featured regularly within TSTL’s accounts:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit before SBP (£k) | 3,242 | 4,023 | 4,645 | 5,549 | 7,240 |

| Share-based payment (£k) | (674) | (121) | (665) | (852) | (435) |

| Operating profit (£k) | 2,568 | 3,902 | 3,980 | 4,697 | 6,805 |

- Between 2016 and 2020, share-based payments reduced total operating profit by £2.7m, or 11%.

- TSTL has form with share options. During 2016, the executives and senior managers collected a £1m options windfall following — in my view — the dubious disclosure of trading information and of the option plan itself.

- The directors have since told me they “strongly rebut” the allegations of a lack of disclosure and of them “dipping their fingers into the till”.

- This time the terms of the award were announced very clearly and the new scheme was in fact put to an AGM vote.

- This latest option batch is divided into three tranches and will come good if the share price trades at an average of 350p (tranche 1), 425p (tranche 2) and 500p (tranche 3) for at least three months before 30 June 2021.

- I welcome option plans that are based on share prices. Everyone knows exactly when the options have vested and shareholders can always take advantage of the higher price and sell.

- Of course, a share price may not always reflect the long-term value of a business.

- But alternative measures such as earnings per share and return on equity can be fudged to trigger option payouts — and subside thereafter — too.

- One drawback to TSTL’s latest option batch is the 1p exercise price. If the company is acquired for peanuts, the options will vest, management will receive extra money — yet shareholders will be mugged.

- The 2020 annual report shows 2,538k outstanding options:

- 2,538k options could turn into shares worth £12m at the recent 480p share price.

- TSTL’s aggregate share-based payment charge is nowhere near £12m.

- The annual report confirms two-thirds (i.e. two tranches) of the latest options award have already vested (660k options out of 990k options granted).

- The first tranche vested during February 2020 after the share price traded at a three-month 350p average, while the second tranche vested during May 2020 after the share price traded at a three-month 425p average.

- The present three-month average share price is approximately 452p.

- Given the first two tranches have vested, assuming every granted option vests and is exercised seems a more practical approach to assessing TSTL’s valuation than applying a theoretical IFRS 2 charge to earnings.

- The share count would increase by almost 6% to 47,835k if all 2,538k outstanding options were exercised.

- Those 2,538k outstanding options have exercise prices ranging from 1p to 412p and would raise approximately £2.7m for TSTL if they were all exercised.

- Any earnings guess would then use the 47,835k share count to determine a per share figure, while the cash position would increase by £2.7m.

- Whether the directors and employees deserve 2,538k options — and the potential to convert them into shares worth £12m — is debatable.

- When the shares were 340p during December, I wrote: “I would nevertheless be very happy if the latest option batch vests entirely — that outcome requires the share price to trade at an average of 500p (or more) for at least three months before 30 June 2021.”

- TSTL’s directors have less than eight months to encourage the share price beyond 500p and trigger the third and final option tranche.

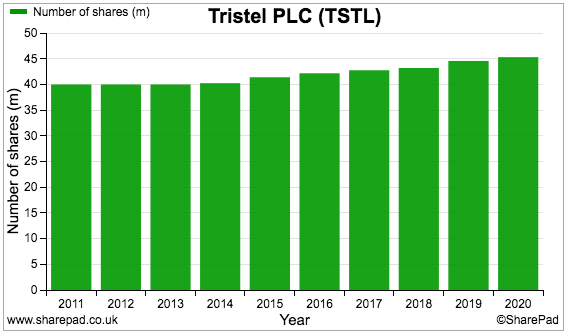

- TSTL’s share count increased by 1.6% last year and has expanded at a 1.4% annual average since 2011:

***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

Financials

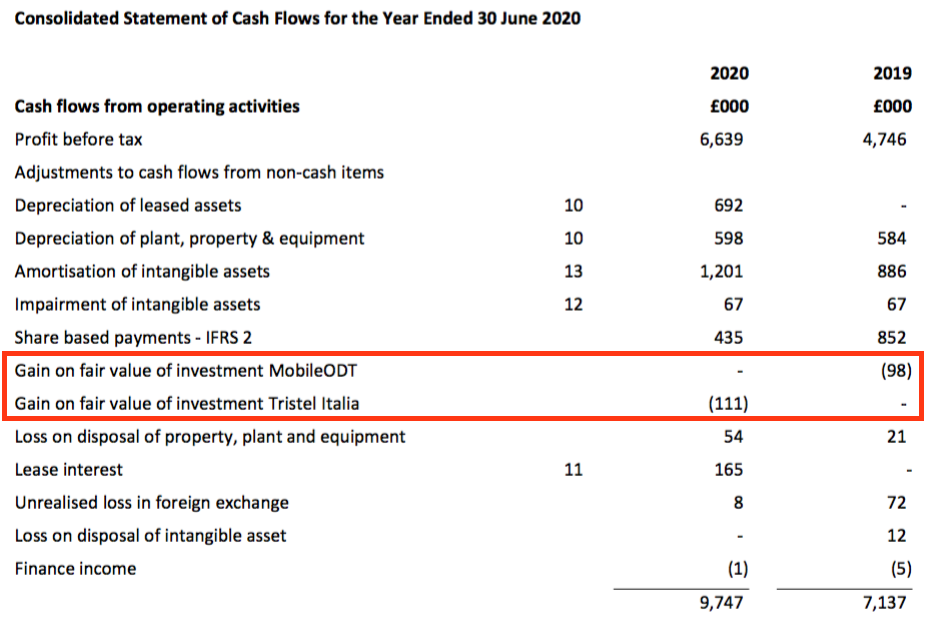

- The cash flow statement revealed fair-value investment gains flattering reported operating profit by c£100k during the past two years:

- Such gains ought to be disclosed as financial income rather than cheekily enhance operating profit.

- Those gains aside, TSTL’s accounting remains straightforward and the books are kept in good shape.

- Cash conversion remains respectable:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit (£k) | 2,568 | 3,902 | 3,980 | 4,697 | 6,805 |

| Depreciation and amortisation (£k) | 966 | 1,243 | 1,498 | 1,470 | 1,799 |

| Net capital expenditure (£k) | (889) | (959) | (1,450) | (1,347) | (2,380) |

| Working-capital movement (£k) | 467 | (530) | (520) | (780) | (1,453) |

| Net cash (£k) | 5,715 | 5,088 | 6,661 | 4,170 | 6,212 |

- During the last five years, total expenditure on tangible and intangible assets has been matched by the combined depreciation and amortisation expensed against earnings.

- The larger FY 2020 working-capital movement related to stock building. The annual report explained:

- The year ended with cash at £6.2m (13p per share), up £2.0m, after £1.2m was raised through options, £0.6m was spent on Tristel Italia and £2.6m was paid as dividends.

- TSTL carries no bank debt and no final-salary pension obligations.

- The implementation of IFRS 16 prompted a £167k lease-finance charge, which might rise to £184k for FY 2021 based on the H2 cost.

- Margins and returns on average equity continue to appeal and underline the notion of TSTL enjoying a competitive advantage:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating margin* (%) | 15.8 | 21.7 | 20.2 | 19.9 | 21.7 |

| Return on average equity (%) | 14.4 | 22.0 | 19.0 | 19.3 | 19.7 |

(* before US regulatory costs)

Valuation

- TSTL repeated the FY 2020/21/22 financial guidance issued this time last year.

- TSTL expects revenue to grow at an annual compound rate of between 10% and 15% for the three years.

- The guidance predicts FY 2022 revenue of at least £34.8m — which will now be achieved should the top line increase by 5% during FY 2021 and 5% again during FY 2022.

- 5% annual revenue growth seems very achievable in light of the FY 2020 performance, and could be even more achievable if further distributors are purchased.

- The other three-year targets are:

- Ebitda (before share-based payments) remaining at 25% or more, and;

- Profit before tax (and share-based payments) increasing each year.

- TSTL’s present market cap appears to be looking far beyond the firm’s guidance to FY 2022.

- TSTL’s reported operating profit was £6.8m for FY 2020.

- The following adjustments give an ‘underlying’ operating profit of £7.0m:

- Adding £80k for US regulatory costs;

- Subtracting £111k to eliminate the Tristel Italia gain;

- Adding £435k to ignore share-based payments, and;

- Subtracting £167k to reflect IFRS 16 lease finance costs.

- Applying the standard 19% UK tax rate leads to earnings of £5.7m.

- Assuming every outstanding option is exercised:

- Earnings of £5.7m convert into 11.9 per share, and;

- The £6.2m cash position increases by £2.7m to £9.0m — equivalent to almost 19p per share.

- Subtract that 19p per share cash from the 480p share price, and the ‘underlying’ cash- and option-adjusted P/E could be 461p/11.9p = 39.

- My profit calculations could be fine-tuned further, but an elevated 39x multiple already tells a story.

- A premium share-price rating is justified given:

- Covid-19 has possibly created an irreversible trend of hospitals enhancing their disinfection regimes;

- And even if disinfection regimes are not enhanced, demand for disinfectants ought to remain predictable and uncorrelated to wider macro-economic factors;

- Notable sales opportunities continue within immature markets such as France, greenfield markets such as India and hypothetical markets such as the US, and;

- The accounts emphasise TSTL’s disinfectants enjoying attractive economics and a worthwhile competitive position.

- However, only time will tell the amount of future progress already priced into the 39x rating.

- The trailing 6.18p per share annual dividend meanwhile supports a modest 1.3% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Fantastic summary as usual. Thankyou

Thanks Stephen. Glad you liked it.

Maynard

Excellent as ever Maynard. Ive been in Tristel for a long time but having nothing like your intimate knowledge.

Possibly the only things I might add are:

Over the years the Tristel share price seems to dip in the couple of months prior to the results and picks up afterwards. I’ve used this as a buying/trading opportunity.

The US saga – how can it be this difficult!!!! We are not talking about a new aeroplane (poor example maybe). I suspect there is an existing US competitor that is lobbying behind the scenes. If I recall several years back Tristel had a similar situation in France – where they decided not to bother trying to get certified due to a local competitor – things have changed however.

Thanks Steve.

On the US, my take from sitting in on various presentations is TSTL having adopted poor advice from consultants (or ignored good advice from consultants) rather than any lobbying from competitors. One striking example was TSTL being very late in the day to start a ‘shelf life’ test — i.e. the FDA wanted actual proof that the disinfectant would work as normal until the ‘use by date’. So TSTL, or so I infer, had to carry out a proper study lasting a year (was going to be two) to produce formal evidence for the FDA that the disinfectants had sat untouched for all that time and then worked. Not going the de novo application route was another blunder.

Maynard

I sold mine as I thought the management were far too greedy. It was a financial mistake to do so but there are plenty of excellent fish in the sea and I prefer a clean palate.

Thanks Stephen. I sold loads too. I kept a few because the products seemed very good (see point 5).

Maynard

Tristel (TSTL)

Update to Executive Performance Share Plan 2021 published 02 December 2020

An interesting announcement, not least because this Plan was not announced initially through the RNS but through an AGM notice published on the website on or after 19 November.

Note the preceding (2018) option Plan was announced through the RNS!

Anyway, this 2021 Plan has been revised. Here is the text of the announcement:

——————————————————————————————————————

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, announces that the terms of the options to be granted under the rules of the Tristel plc Executive Performance Share Plan 2021 (the “Plan”) to be put to shareholders for approval at the Annual General Meeting of the Company to be held on 10.00 a.m. on 15 December 2020 (the “AGM”) will be amended to include more onerous performance targets for the vesting of the options.

A revised copy of Appendix I of the Notice of AGM summarising the principal terms of the Plan and of the options to be granted under the Plan and copies of the proposed option agreements incorporating, in each case, the more onerous performance targets, together with the full text of the Plan, the Notice of AGM and the Form of Proxy, are available for inspection on the Company’s website at https://www.tristel.com/uk/investor-centre/agm-notices-proxies.

Any shareholder who wishes to change any proxy instructions already submitted, may do so by submitting a new proxy appointment using the methods set out in the notes to the Notice of AGM.

Shareholders are reminded that proxies must be received no later than 10.00 a.m. on 11 December 2020. ——————————————————————————————————————

Credit to TSTL for publishing the revised Plan document with the changes marked-up. The revised document is here.

The main changes are below:

The minimum £10m profit before tax and share-based payments for FY 2024 compares with £7.074m for FY 2020.

Profit therefore has to compound at 9% per annum for four years before this profit-related option batch can vest (previously 7.7%). 100% vesting occurs at 12.9% profit growth per annum (previously 11.7%).

Notice the tight profit bands. If £10m is achieved (4-year profit up 41%), then 25% of this batch vests. But if £10.4m is achieved (4-year profit up 47%), then 75% of the batch vests. In other words, tripling the options collected takes only another £0.4m of PBT (i.e. a 4% increase from £10m).

The share-price option batch looks easier to collect, especially if the profit targets are met.

While the profit-related batch requires 4-year profit to advance 41% before vesting, the price-related options require the share price to advance only 20% before vesting.

For this 2021 Plan, 800k options will be granted at 1p, so assuming full vesting with the share price at 750p, the windfall comes to £6m for the three executives.

In exchange TSTL’s market cap would have advanced by £136m (from £232m at 500p to £368m at 750p) assuming the existing 2.5m options are all exercised in the meantime.

Is a £6m windfall via 800k options — or < 2% dilution on the current fully diluted share count of 49m — a reasonable cost for a £136m increase to the market cap? Put it this way — no TSTL shareholder is complaining about the share price going from 275p to 500p since the last options were awarded three years ago.

Tristel (TSTL)

AGM Statement published 15 December 2020

A satisfactory statement, with more detail than previous AGM updates. Here is the full text:

——————————————————————————————————————

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, will hold its Annual General Meeting at 10am at Lynx Business Park, Fordham Road, Newmarket, Cambridgeshire CB8 7NY. It will be a closed meeting due to COVID-19 restrictions.

Paul Swinney, Chief Executive Officer, will address the meeting with the following update:

“We expect unaudited first half pre-tax profit (before share-based payments) to increase by 10%, being no less than £3.3 million compared to £3 million for the same period last year. We also expect first half revenue to increase by 10%. All sales growth has been organic.

Whilst we have continued to win many new customers around the world for our medical device decontamination products, first quarter sales were lower than budgeted due to the deferral of patient procedures resulting from COVID-19 restrictions. However, from October to date we have experienced a substantial recovery in demand. A contributory factor has been NHS purchasing in preparation for Brexit and we have seen continued significant growth in our newer markets of France, Belgium, Netherlands, Italy, and Malaysia.

We anticipate that the strong long-term growth trend for our medical device decontamination products will re-establish itself during the second half as vaccination programmes and improved COVID-19 treatment outcomes gradually take effect around the world. We look forward to our business maintaining its robust growth profile in 2021 and beyond.

Sales of our new Cache product range will be approximately double their level of the first half last year. With Cache, our goal is to become a global market leader in the segment of the hospital environmental hygiene market which we describe as sporicidal surface disinfection.

In North America very encouraging progress has been made in our FDA test programme for Duo for Ultrasound, and we have received positive feedback from the Canadian regulator on our Duo for Ophthalmology submission. In India we expect to conclude distribution arrangements for our entire Duo product range before Christmas. The Duo product range was approved by the Indian regulator in August this year.

And finally, Paul Barnes has been an Executive and Non-Executive director of the Company since before our IPO in 2005. He retires today. We thank him for the great contribution he has made over the years and wish him well. Our Board is examining how its expertise, experience and diversity can be developed further to equip itself for the exciting future we believe lies ahead.”

At 10am, a short recording by Paul Swinney, CEO, will be made available at: http://www.tristelresults.com. ——————————————————————————————————————

The AGM statements for 2015, 2016, 2017, 2018 and 2019 did not reveal a H1 sales projection, so I welcome TSTL disclosing the additional information. TSTL did disclose a H1 sales projection within the 2014 AGM update.

H1 revenue up 10% (to c£16.0m) does not sound too bad given 2020 revenue climbed 13% (excluding acquisitions) and Q1 sales being lower than budgeted due to the deferral of patient procedures.

Note that TSTL has in the past ‘sandbagged’ its H1 profit forecast within its AGM statements. Last year for example, TSTL said profit would be no less than £2.8m, and the eventual result was £3.0m. So there is hope of profit being more than £3.3m.

Talk of cache sales doubling leads me back to this chart from the 2020 results presentation:

Cache surface sales were c£1m for H1 2020, so sales could be £2m for H1 2021.

If total revenue has gained 10%, or £1.6m, to £16.0m, then most of that advance is due to Cache.

“Very encouraging progress” sounds promising with regards to the FDA submission. The blog post above speculated that FDA progress was moving forward after the project expanded to include a handful of revived/new applications.

Maynard

Tristel (TSTL)

Publication of 2020 annual report

Here are the points of interest:

1) KPIs

TSTL has commendably included ROCE as a key performance indicator for 2020:

Safety KPIs are now used by the board:

2) Covid-19

Covid-19 was unsurprisingly added to an otherwise unchanged Risk section:

(Note: Surface disinfectant sales gained £2.27m, or £0.27m (+10%) if you exclude the £2m boost due to Covid-19.)

This line suggests future growth is dependent partly on the manufacturers of medical devices selling more products:

Most of the Covid-19 risk section was standard text.

But I thought this line about credit screening was notable…

…as was this line about stock-building.

3) Director biographies

Mr Leemans has changed his skill-set slightly from 2019:

A helpful CV from a new non-exec:

4) Director pay

The execs remain able to collect 3% of gross profit (I assume that 3% covers total salaries and not per director):

3% of 2020 gross profit was £757k.

The execs enjoyed pay rises:

The chief exec’s wage gained 9% to £250k while the finance director’s advanced 3% to £185k. Both increases were announced within the 2019 report.

However, pay increases have been waived for 2021 and a £147k bonus for 2020 was foregone:

The waived £147k bonus compares to the £186k bonus total that was paid.

Confirmation that those peculiar ‘change of control’ options have lapsed:

The 1.2 million total does not include the 800k options awarded after the AGM.

5) Corporate governance

Two new primary goals have been set:

They both replace: “To replicate market penetration achieved in targeted clinical areas in the UK in all overseas markets.”

(I am not sure what a “digital” disinfectant is.)

Also, the first goal has been modified from “increase” to “maximise” the company’s value.

TSTL now monitors online bulletin boards rather than blogs :-(

More about Covid-19:

Board reveals it now sees daily sales numbers:

The new non-exec sought here…

… was appointed just before Christmas. She is another non-exec with a useful CV:

“Caroline Stephen’s executive career has been spent in global healthcare, marketing, and digital transformation, working for Johnson & Johnson for 26 years in multiple leadership roles.”

The chief exec and finance director remain married, and although I am not sure how the pair can adhere to the new line that mentions “an attitude of independence of character and judgement”.

The company apparently met all of its financial objectives:

The line about “long-term succession plan” is new for 2020. I would not be unhappy if Mr Leemans took on the top job.

Broker forecasts were £6.5m last year:

The eventual profit figure was £7.1m before share-based payments.

TSTL also confirms being on track with the latest three-year sales target, which is not surprising as only 5% annual sales growth is needed for 2021 and then 2022.

An interesting change for 2020:

The minimum cash position has been lifted from £3m to £4m, and the ‘excess cash’ wording has been change from “is” to “may be”.

6) Audit

Recognising revenue early to prompt option vesting remains a key audit risk:

Materiality remains a standard c5% of pre-tax profit:

No exact coverage figure for scope, though last year’s was c90% and an extra subsidiary was audited for 2020.

7) Largest customer

Confirmation that revenue earned from the largest customer surprisingly declined during the year:

As per the blog post above, this income from the NHS supply chain remains something to monitor.

8) Operating expenses

This note shows the £111k fair-value gain (and the £98k gain for the year before) that TSTL sneaked in to flatter profits a little:

Also of note is the lower research costs expensed, at £458k, which is the lowest amount since 2016 (£251k). I trust TSTL is not reducing its innovation. Perhaps the higher 2017-2019 research expense (total: £2.4m) was due to developing Cache.

9) Employees

Nothing too untoward here:

Encouraging to see sales and marketing staff continue to represent more than a third of employees. Revenue per employee was a useful £193k, a new record, and up from £184k during 2019 and £152k during 2015. This business has commendably expanded its sales without commensurate additional employees.

However, such productivity improvements come with additional pay, and the average employee cost is now £64k, up from £60k for 2019 and £42k for 2015. Exclude director payments and the average employee cost is £59k, up from £51k for 2019 and £38k for 2015.

I do like TSTL’s attitude to staff options:

The text suggests employees can enjoy 4,000 options a year. Given the £6 share price, I suspect a few long-time staff members currently sit on some valuable option holdings.

10) Auditor remuneration

Basic audit fees up 50% to £232k:

Presumably the result of switching to KPMG and/or auditing six subsidiaries rather than five (see point 6).

11) Goodwill

Changed discount rates and extra disclosure relating to goodwill:

The discount rate increased to 21% from 16%, which will reduce the net present value of the estimated future cash flows from the acquired entities.

Also, TSTL now discloses the difference between the carried goodwill and the NPV calculation. Australia is apparently worth 4x book goodwill value, with Italy almost 3x and Belgium/Netherlands/France close to 2x.

12) Intangibles

Conservative figures here:

Total intangible additions for 2019 and 2020 came to £1.3m versus total amortisation of £2.1m — a notable £0.8m difference that arguably dampens reported profits.

Part of the £0.8m difference is due to the amortisation of ‘customer and supplier relationships’ created through acquisitions. Many companies choose to exclude such amortisation from their adjusted figures — commendably TSTL does not.

‘Customer and supplier relationships’ are amortised over 10 years — a long time, but not completely unusual among quoted companies, and TSTL perhaps has good evidence of supplying hospitals for a decade or more. Note the NPV discount rate for this particular intangible is 17% versus the 21% applied to calculate the standard acquired goodwill (see point 11).

13) Inventories

The year-end inventory position reflected the stock-building referred to in the Covid-19 risk section (see point 2):

Year-end stock represented 14.6% of revenue versus 10-11% for the previous four years.

Cost of inventories was £6,015k (see point 7), so 1.6x the year-average position. The ratio has topped 2x since 2015. The 1.6x ratio implies stock sits around for 7.5 months before being sold, which seems a long time. Even the 2x ratio suggests a long 6 months. I have never got the impression TSTL struggles to shift its stock and the small provisions in the note above underline that notion.

14) Trade and other receivables

A few customers may have become tardy payers.

True, year-end net trade receivables represented 15% of revenue, within the 15%-17% range seen since 2014:

But 51% of trade receivables were past due:

Those receivables past due represented 8.3% of revenue, versus sub-5% for 2017, 2018 and 2019.

(The £5,130k trade receivable figure above excludes VAT and so differs from other receivable figures in the report)

This next footnote is new for 2020. It outlines TSTL’s receivable ‘risk grading’:

15) Trade and other payables

Trade payables at 7% of revenue and trade and other payables at 15% of revenue are both similar to the ratios witnessed during the previous few years:

16) Share options

If my reading of TSTL’s option plan is correct, all 990k options granted through the 2018 scheme have now vested:

I calculate the share price exhibited a 90-day average of 501p on 18 January this year, which means the last 330k options vest. I don’t think any shareholder is complaining that all of these options have vested after they were granted when the price was 275p.

17) IFRS 16

Minor detail on IFRS 16:

A right-of-use assets figure that is lower that the lease liabilities figure suggests TSTL’s rent agreements are higher than they would be if the same leases were taken on today.

Maynard