31 May 2020

By Maynard Paton

Results summary for M Winkworth (WINK):

- Acceptable full-year figures that showed revenue up 8% and profit up 12% following an encouraging second half.

- The declaration of a Q1 dividend for 2020 implies possible resilience to Covid-19 and hints at a better-than-expected pandemic performance.

- Very impressive market-share gains continue to be won from London rival Foxtons.

- Despite a number of accounting niggles, the books remain in pretty good shape with high margins and net cash.

- A possible P/E of 8-12 and a potential income of 6% may offer upside should earnings revive and then one day thrive following Brexit, stamp-duty changes and Covid-19. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own WINK

- Results summary

- Covid-19 and Q1 dividend

- 2019 revenue, profit and dividend

- Accounting restatements

- Tooting acquisition

- Foxtons comparison

- Financials

- Valuation

Event links, share data and disclosure

Event: Final results and annual report for the twelve months to 31 December 2019 published 06 April 2020 and Q1 2020 dividend declared 15 April 2020

Price: 110p

Shares in issue: 12,733,238

Market capitalisation: £14.0m

Disclosure: Maynard owns shares in M Winkworth. This blog post contains SharePad affiliate links.

Why I own WINK

- Operates a London estate-agency franchising business, where progress is buoyed by motivated franchisee owners taking market share from conventional rivals.

- Franchising set-up leads to high margins, low capital requirements and a cash-rich ‘pandemic-proof’ balance sheet.

- Seasoned family management boasts £7m/50% shareholding and rewards investors through resilient quarterly dividends.

Further reading: My WINK Buy report | All my WINK posts | WINK website

Results summary

Covid-19 and Q1 dividend

- A subdued first-half performance followed by an encouraging statement in January — “profits before tax are expected to be modestly ahead of market expectations” — had signalled these 2019 figures might show a bit more promise for 2020.

- The pandemic then left the results somewhat redundant as the housing market shut down. WINK stated:

“We have entered a period of considerable uncertainty as measures are taken to defend the UK against the spread of COVID-19. These are having an increasingly severe impact on the business of each and every one of our franchisees and it is too early to predict what the full effect will be on activity in the remaining nine months of 2020.”

- WINK’s income comes from receiving a proportion of the sales and lettings commissions earned by its estate-agent franchisees.

- Headlines such as A Quarter Of Agency Branches May Be Closed Forever underlined my worry that the sector would be thumped during the lockdown.

- The annual report small-print (point 6) thankfully revealed WINK is/was not under immediate pressure:

“Whilst the timing and ultimate impact [of COVID-19] cannot be assessed with any precision at the time of writing, various scenarios, reflecting the closure of franchisee shops for at least a three month period, have been run on the potential impact of COVID-19, as detailed in the Report of the Directors on page 12, which demonstrate that the group has sufficient working capital for the foreseeable future.

The group has a strong cash base and no borrowings, with a high level of discretionary expenditure, which can be cut at short notice. Income would need to fall very substantially for a prolonged period, beyond six months, before a cash shortfall arose, at which point stronger measures would be taken to cut costs.”

- In fact, WINK’s scenario planning heralded the declaration of a Q1 2020 dividend a week after the publication of these results.

- The Q1 dividend provided genuine evidence of the business coping relatively well with the pandemic.

- True, the Q1 payout for 2020 was reduced by 12% to 1.68p per share.

- However, many quoted companies have instead axed their payouts completely.

- I had earlier felt WINK would be a potential “heavy casualty” of the pandemic and expected the dividend to be chopped to zero.

- But WINK stated:

“The board remains committed to paying a quarterly dividend. While the intention is to resume a progressive payment once trading conditions permit, the reduction in the first quarter dividend reflects the element of caution required as a result of the Covid-19 crisis. As it is the board’s objective to ensure that dividend pay-outs are covered by post-tax profits, the total distribution for 2020 is expected to be lower than 2019.”

- I would happily accept a 12% reduction to the three remaining 2020 quarterly payouts.

- These company FAQs published during April confirm the business was/is operating during the lockdown:

“Q. Is the company still open for business?

A. Absolutely. Although in line with government advice all of our Winkworth offices are closed, we are still very much here for you and business as usual, as much as the ‘new usual’ looks. We are still contactable and can talk to you by telephone, email, or even video call.

Q. Can you market my property for sale?

A. Although the press is reporting dramatic headlines on the property marketing stalling, in reality it appears that things are working as usual behind the scenes.

We have a range of digital tools at our disposal to help the process along and are pioneering the use of these to ensure that we progress everything that we can. Although we can’t come to your house for a valuation or viewings, we can now offer these virtually. It has been shown recently that buyers are just as enthusiastic about viewing a property through a video call, and interest in properties has not gone away.

Q. Can you sell my property at this time?

A. Yes we can. We are still agreeing new sales and reports are showing that the buyer demand is still there and the level of enquiries we are receiving is very encouraging.”

Enjoy my blog posts through an occasional email newsletter. Click here for details.

2019 revenue, profit and dividend

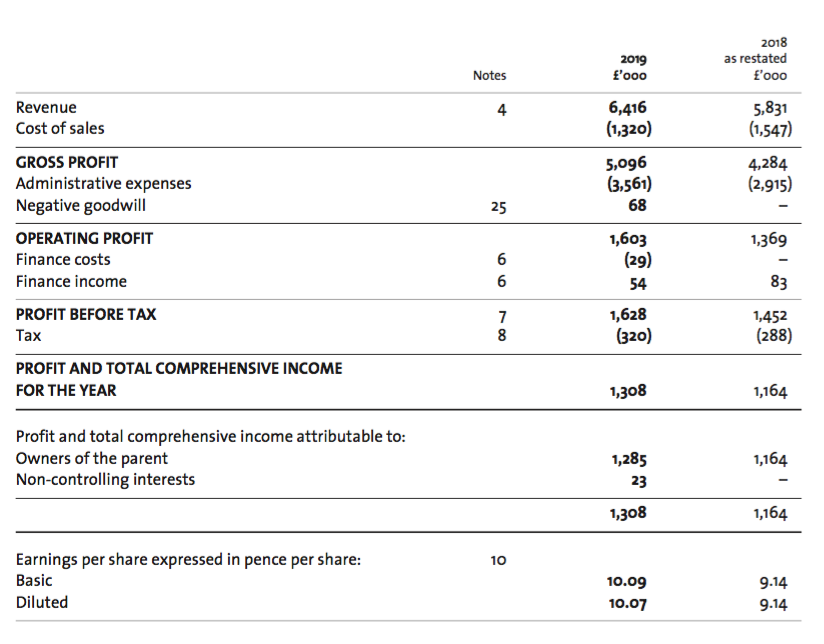

- WINK reported full-year revenue up 8% and profit up 12%:

| Year to 31 December | 2015* | 2016* | 2017* | 2018* | 2019 |

| Gross Franchisee Sales & Lettings (£k) | 49,010 | 46,120 | 46,200 | 46,500 | 48,300 |

| Revenue (£k) | 5,865 | 5,566 | 5,423 | 5,979 | 6,416 |

| Operating profit (£k) | 1,817 | 1,346 | 1,302 | 1,369 | 1,535 |

| Net finance income (£k) | 90 | 71 | 74 | 83 | 25 |

| Other items (£k) | - | - | - | - | 68 |

| Pre-tax profit (£k) | 1,907 | 1,417 | 1,376 | 1,452 | 1,628 |

| Earnings per share (p) | 11.95 | 8.84 | 8.66 | 9.14 | 10.09 |

| Dividend per share (p) | 6.50 | 7.20 | 7.25 | 7.45 | 7.80 |

| Special dividend per share (p) | 1.80 | - | - | - | - |

| Return of capital per share (p) | - | - | - | 9.00 | - |

(*unadjusted for intangible restatement and IFRS 16)

- The 2019 figures were affected by:

- An unusual restatement of intangible assets;

- The implementation of the IFRS 16 Leases accounting standard, and;

- The 55% purchase of a group franchisee.

- See Accounting restatements and Tooting acquisition below.

- Full-year revenue reached a new record although operating profit remained well below the £1.8m level of 2014 and 2015.

- Brexit and stamp-duty changes have kept a lid on the London property market since 2016. Some 78% of WINK’s income is dependent on franchisees operating within the capital.

- Revenue for 2019 improved following an “8% increase in [sales] transactions across the board, increasing… market share both nationally and in London in particular, where we ranked second in Sales Subject to Contract with a market share of 4.2%, up from 3.6% in 2018.”

- Market share gains — at least against quoted rival Foxtons (FOXT) — remain very impressive (see Foxtons comparison below).

- Lettings income performed well:

“Lettings and management services underwent a significant year with the ending of tenant fees in June. Our revenues continue to grow despite this, with overall UK income up by 6% on 2018, driven by our country offices growing at 16%.”

- WINK’s network of franchisees witnessed their gross turnover advancing 4% to £48.3m, of which 12.3% (adjusted for the 55% purchase of a group franchisee) went to WINK:

| Year to 31 December | 2015* | 2016* | 2017* | 2018* | 2019 |

| Gross Franchisee Sales & Lettings (£k) | 49,010 | 46,120 | 46,200 | 46,500 | 48,300 |

| Revenue (£k) | 5,865 | 5,566 | 5,423 | 5,979 | 5,918 |

| Revenue/Gross Franchisee Sales & Lettings (%) | 12.0 | 12.1 | 11.7 | 12.9 | 12.3 |

(*unadjusted for intangible restatement)

- The network split between sales and lettings income was 49%/51% during 2019:

| Gross Franchisee Revenue | H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | |

| Sales (£m) | 10.8 | 12.6 | 23.4 | 10.0 | 13.8 | 23.8 | |

| Lettings (£m) | 10.3 | 12.8 | 23.1 | 11.4 | 13.0 | 24.4 | |

| Total (£m) | 21.1 | 25.4 | 46.5 | 21.4 | 26.8 | 48.3 |

- Franchisees pay WINK 8% of all sales commissions/letting income they receive alongside variable contributions towards advertising and IT. Franchisees also pay WINK for introductions to new landlords and tenants.

- The 2019 dividend set a new payout record, although the aforementioned Q1 payout has signalled a reduction for 2020.

- As usual, the second half was more profitable than the first:

| H1 2018* | H2 2018* | FY 2018* | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (£k) | 2,798 | 3,181 | 5,979 | 2,727 | 3,689 | 6,416 | |

| Operating profit (£k) | 551 | 818 | 1,369 | 576 | 959 | 1,535 |

(*unadjusted for intangible restatement and IFRS 16)

Accounting restatements

- WINK’s 2019 figures were distorted slightly by two restatements.

- However, the awkward details explained below can be overlooked assuming WINK’s Q1 dividend does indeed imply good resilience to Covid-19.

- Feel free to skip to the Tooting acquisition section to avoid this accounting recap.

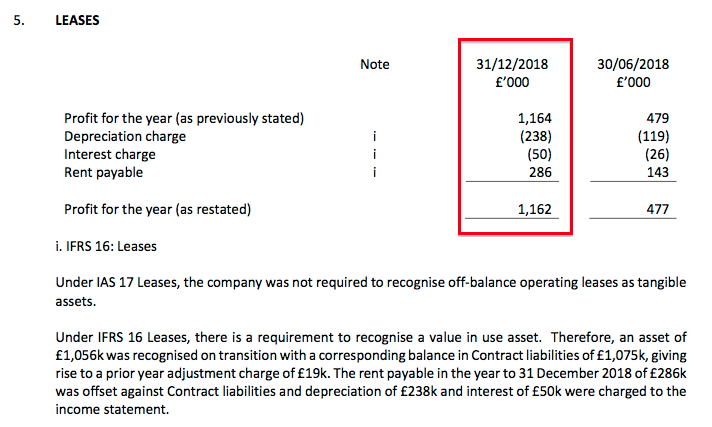

- These 2019 figures were WINK’s first annual results to reflect the new IFRS 16 standard.

- Under IFRS 16, the cost of a lease is accounted for as a mix of depreciation and interest rather than as an operating expense.

- WINK had restated its 2018 accounts for IFRS 16 within its half-year statement:

- But strangely, the 2018 figures were not restated for IFRS 16 within this full-year announcement.

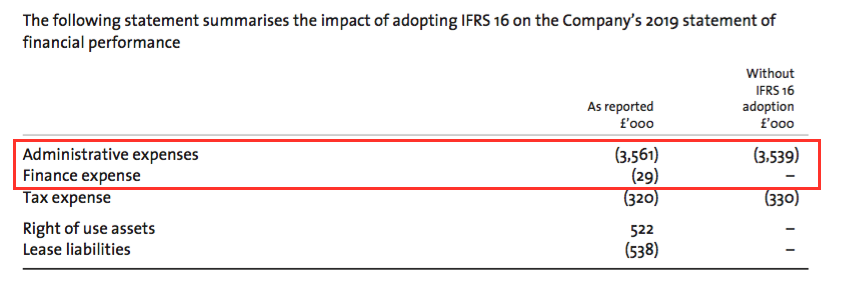

- WINK outlined the minor effect of IFRS 16 on its 2019 accounts:

- Under IFRS 16, administrative costs came to £3,561k.

- Pre-IFRS 16, administrative costs would have been £3,539k — or £22k less.

- Operating profit on a pre-IFRS 16 basis therefore gained 14% during 2019.

- IFRS 16 does not affect cash generation.

- However, IFRS 16 does create irritating analysis issues, including:

- Valuations based on operating profit will no longer include the full rent expense;

- Depreciation will now include some rent expense, and therefore will no longer be directly comparable to cash capital expenditure on new tangible assets, and;

- Interest costs will now include some rent expense and may suggest bank debt has become more expensive.

- WINK’s bookkeeping also involved restating certain amortisation of intangible assets as a deduction to revenue.

- WINK gave this explanation for what the annual report small-print (point 15) admitted was a “historical error”:

“The directors have reconsidered the nature of the payments made to franchises on inception of a franchise arrangement, which are intended to assist with branding and other costs. These had previously been presented as an intangible asset under IAS 38, but the directors are now of the view that the payments do not result in the group receiving a distinct good or service from the franchisee and, in consequence, consider them to meet the definition of consideration payable to a customer under IFRS 15.”

“Consequently, this asset is described as “Prepaid assisted acquisitions support” on the Group statement of financial position. The asset continues to be amortised over 10 years on a straight-line basis, however, the amortisation is now recognised as a deduction in revenue rather than an amortisation charge to administrative expenses. As a result, revenue and administrative expenses reported at 31 December 2018 have been restated by £148,639. There is no impact on the profit or net assets reported for the year in 2018.”

- This line is important:

“…the directors are now of the view that the payments do not result in the group receiving a distinct good or service from the franchisee and, in consequence, consider them to meet the definition of consideration payable to a customer under IFRS 15”.

- WINK effectively equates the payments — or “prepaid assisted acquisitions support” — to ‘brand building’:

“Prepaid assisted acquisitions support represents amounts paid to franchisees on the incorporation of their business into the Winkworth brand. The amounts paid to franchisees are contributions towards their growth plans, which in turn will grow the Winkworth brand.”

- The restatement therefore boils down to ‘brand building’ not being classed as a “distinct” good or service under the accounting rules.

- As such, WINK’s ‘brand building’ payments to franchisees are deemed to be a “consideration payable to a customer” — and therefore must be offset against the franchisee’s payments to WINK. According to annualreporting.info:

“Consideration payable to a customer is accounted for as a reduction of the transaction price (and hence, a reduction of revenue), unless the payment to the customer is in exchange for a distinct good or service that the customer transfers to the vendor.”

- At least this “historical error” was relatively small.

- 2018 revenue was revised down by £149k, or 2%, to £5,831k. Note that a matching £149k reduction to costs meant 2018 operating profit was not affected.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

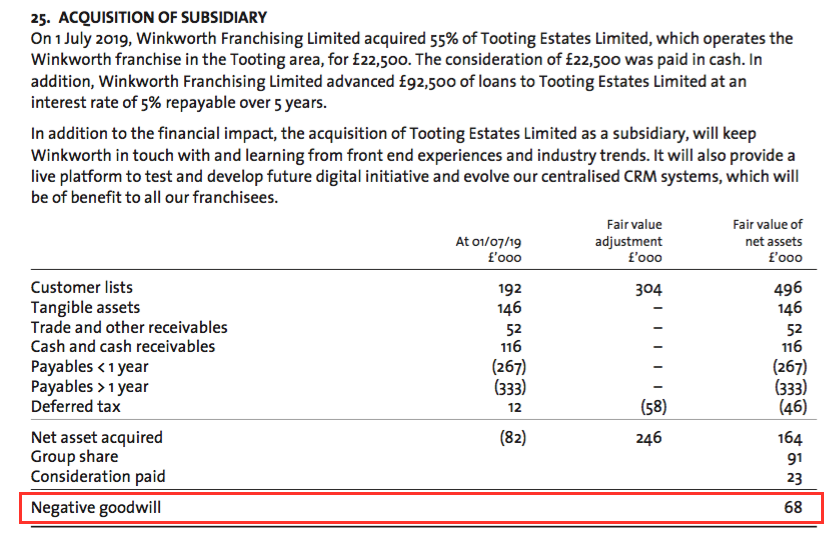

Tooting acquisition

- WINK purchased 55% of Tooting Estates for £23k cash plus a £92k loan at the start of the second half.

- Tooting Estates operates the WINK franchise in Tooting, London, and the purchase heralds WINK’s return to running agency branches.

- WINK claimed the deal was to gather ‘front line’ insight:

“The acquisition of Tooting Estates… will keep Winkworth in touch with and learning from front end experiences and industry trends. It will also provide a live platform to test and develop future digital initiative and evolve our centralised CRM systems, which will be of benefit to all our franchisees.”

- WINK hinted further deals could follow:

“We backed one new franchisee through equity participation… looking to increase our financial return to above the 8% that we receive as part of our regular franchise agreement, and we remain open to repeating this approach where we find the right local market and the right operator… Having analysed the data across all our London offices, we see further opportunities to develop this approach in due course.”

- I am not quite convinced about this course of action.

- A top attraction to WINK’s franchisor status is its business remaining lean and efficient as a small army of franchisees operates the branches and do all hard revenue work.

- I am also aware that the track records of quoted conventional estate-agency chains are not great.

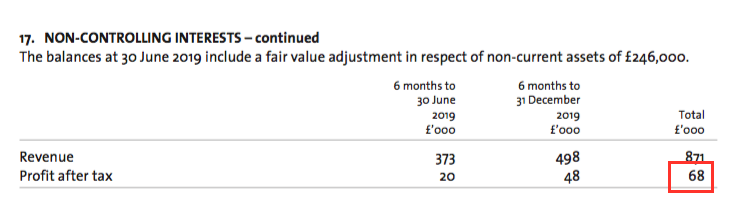

- Mind you, WINK’s £115k investment would have returned a profit of £37k (£68k * 55%) had Tooting Estates been owned for the full year:

- So maybe WINK should indeed seek out further Tooting-type opportunities if the annual return on investment is 32% (£37k/£115k).

- The Tooting transaction created the rare accounting concepts of ‘negative goodwill’ and ‘bargain purchase’:

- WINK said:

“The bargain purchase arose due to the vendor, a related party of the Group, valuing the intangible assets of the company, consisting of its customer lists, at lower than current fair value, being the amount paid when the business was previously purchased. The transaction benefitted the vendor through enabling it to recover debt from the business.”

- The Tooting purchase added £498k to H2 revenue and approximately £59k to H2 operating profit.

- Without the Tooting deal, group revenue would have advanced just 1% and operating profit would have gained 8%.

Foxtons comparison

- WINK continues to outperform FOXT, which claims to be “London’s leading estate agent”:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Winkworth | |||||

| Gross Franchisee Sales Revenue (£m) | 30.1 | 26.0 | 24.8 | 23.4 | 23.8 |

| Gross Franchisee Lettings Revenue (£m) | 18.8 | 20.1 | 21.3 | 23.1 | 24.4 |

| Total Gross Franchisee Revenue (£m) | 49.0 | 46.1 | 46.2 | 46.5 | 48.3 |

| Foxtons | |||||

| Sales Revenue (£m) | 72.5 | 55.5 | 42.6 | 36.2 | 32.6 |

| Lettings Revenue (£m) | 69.0 | 68.3 | 66.3 | 67.0 | 65.7 |

| Total Sales & Lettings Revenue (£m) | 141.5 | 123.8 | 108.9 | 103.2 | 98.3 |

| Winkworth / Foxtons | |||||

| Sales Revenue (%) | 41.5 | 46.8 | 58.2 | 64.6 | 73.0 |

| Lettings Revenue (%) | 27.2 | 29.4 | 32.1 | 34.5 | 37.1 |

| Total Revenue (%) | 34.6 | 37.3 | 42.3 | 45.1 | 49.1 |

- During 2015, WINK’s total franchisee revenue represented 34.7% of FOXT’s property sales and lettings revenue.

- During 2019, the proportion had increased to 49.1%.

- During H2 2019, the proportion had increased to 52.3%.

- Amazingly enough, WINK’s network income from property sales of £13.8m during H2 2019 represented 80.2% of FOXT’s £17.2m equivalent.

- For perspective, the proportion was only 42.9% for H2 2015 (£16.5m of £38.5m).

- The improvement to 80.2% implies WINK has performed really well and/or FOXT has performed really poorly during the last few years.

- The FOXT comparison is not strictly like-for-like. FOXT generates almost all of its revenue from branches within London while WINK generates 78%.

- Nonetheless, WINK’s self-employed franchisees appear to have handled London’s standstill property market far better than FOXT’s conventional employees.

Financials

- WINK’s accounts remain in satisfactory shape.

- Margins and returns on equity have been kept high:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating margin (%) | 31.0 | 24.2 | 24.0 | 22.9 | 23.9 |

| Return on average equity (%) | 30.5 | 21.0 | 19.8 | 22.6 | 26.8 |

- WINK’s operating margin has declined during the last few years, due mostly to the additional cost of extra employees:

| Year to 31 December | 2015* | 2016* | 2017* | 2018* | 2019 |

| Revenue (£k) | 5,865 | 5,666 | 5,423 | 5,979 | 6,416 |

| Employee costs (£k) | 1,528 | 1,492 | 1,600 | 1,784 | 2,208 |

| Employees | 34 | 32 | 33 | 33 | 44 |

| Employee costs/Revenue (%) | 26.1 | 26.8 | 29.5 | 29.8 | 34.4 |

(*unadjusted for intangible restatement)

- I presume the Tooting deal caused employee numbers to increase by a third during 2015.

- The payment of that Q1 2020 dividend was underpinned by a cash-rich balance sheet.

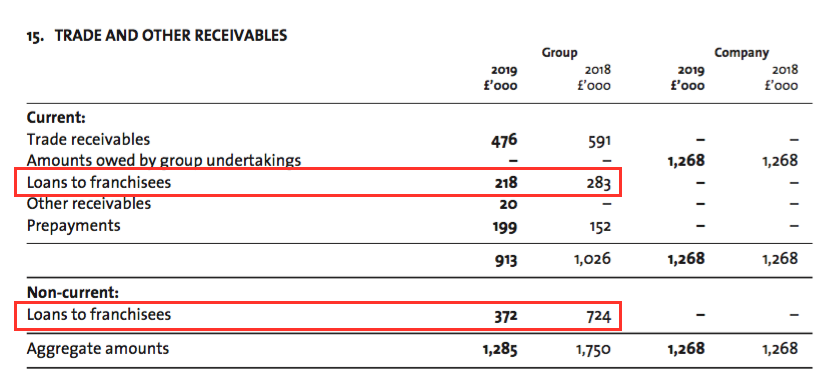

- Cash and investments finished 2019 at £3.6m (28p per share). The balance sheet carries no bank debt and no pension obligations.

- Start-up loans to franchisees reduced from £1.0m to £0.6m (5p per share) during the year. I would not mind if all of these loans were paid off:

- Reflecting the lower loans, finance income fell from £83k to £54k and — at the 5% applied to the loan issued as part of the Tooting deal — could drop to £30k for 2020.

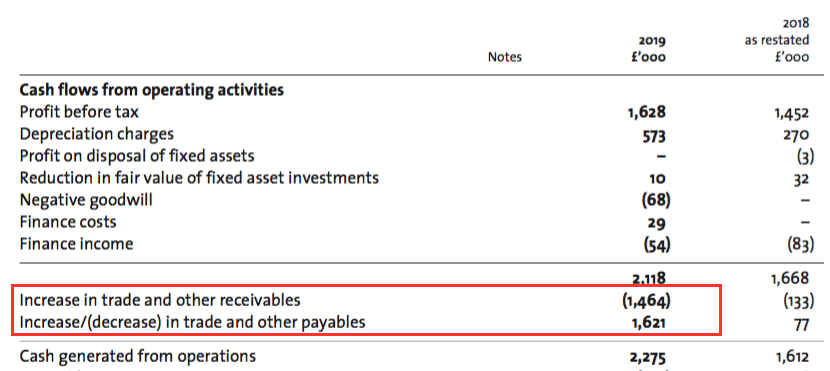

- Cash flow appeared sound:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit (£k) | 1,817 | 1,346 | 1,302 | 1,369 | 1,535 |

| Depreciation and amortisation (£k) | 275 | 368 | 246 | 270 | 288* |

| Net capital expenditure (£k) | (108) | (250) | (247) | (189) | (277) |

| Working-capital movement (£k) | (195) | (145) | 567 | (56) | 157 |

| Net cash and investments (£k) | 3,175 | 2,979 | 3,586 | 2,988 | 3,614 |

(*excludes IFRS 16 depreciation)

- Expenditure on tangible and intangible assets (websites and “prepaid assisted acquisitions support”) just about matched the (non-IFRS 16) depreciation and associated amortisation charged against earnings.

- Some unusually large movements resulted in a favourable £157k working-capital cash inflow:

- However, that £157k movement did include the aforementioned £0.4m repayment of start-up franchisee loans.

- Following all the inflows and outflows — including dividend payments of £1.0m — cash ended the year £0.6m greater.

Valuation

- The annual report small-print (point 2) admitted:

“Whilst the year has started strongly and broadly in line with Board expectations, COVID-19 will inevitably impact on the market in the remainder on 2020 and the current outcome for the next few months is extremely uncertain.”

- Earnings for this year are therefore anyone’s guess.

- As a guide, operating profit for 2019 (including IFRS 16 lease/interest costs) was £1.5m, which after standard 19% tax gives earnings of £1.2m or 9.3p per share.

- A market cap of £14.0m less cash/franchisee loans of £4.2m gives an enterprise value of £9.8m, or 77p per share.

- Dividing the 77p per share enterprise value by the 9.3p per share earnings guess leads to a possible multiple of 8.

- Assume the cash and franchisee loans are inherently required for the business to operate successfully, and the P/E comes to 12.

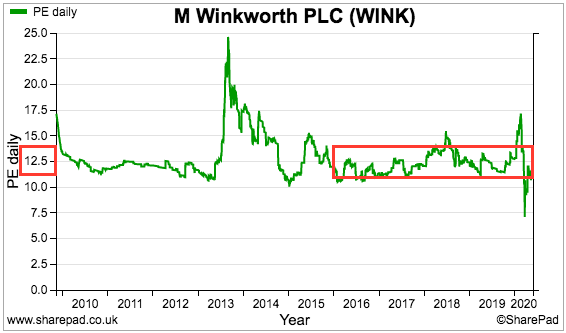

- Neither the 8x nor 12x rating seems expensive, but operating profit for 2016, 2017, 2018 and 2019 were at least 15% below that reported for 2014 and 2015.

- Earnings retained by the business since 2015 have therefore not created much obvious value to date.

- The absence of profit growth after 2015 is why the shares have never subsequently looked that expensive on a P/E basis:

- Covid-19 means 2020 will be another year where profit goes nowhere (at best).

- WINK has reinvested earnings at high rates in the past.

- During the five years to 2015 for example, earnings improved by £0.7m after £3.3m was added to shareholder equity. The resultant incremental return on equity was £0.7m / £3.3m = 22%.

- Were WINK to ever repeat such reinvestment returns, the present P/E offers scope for a positive re-rating.

- Trouble is, repeating such reinvestment returns is somewhat dependent on WINK benefiting from a healthier London property market.

- The impact of Brexit, stamp-duty changes and now Covid-19 on London house prices may take some time to dissolve.

- WINK could instead prosper at the expense of rival agents.

- Further market-share gains against FOXT (and others) might prompt a return to growth even if London’s property market stagnates further.

- Assuming the 1.68p per share Q1 2020 dividend is repeated for the following three quarters, a prospective 6.7p per share full-year payout would offer a possible 6.1% yield.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

M Winkworth (WINK)

Publication of 2019 annual report

Here are the points of interest beyond those mentioned in the blog post above.

1) Corporate governance

Short reminder from the chairman that “culture, value and behaviour” underpin the group’s progress:

2) Principal risks and uncertainties

A few changes in this section from 2018.

No surprise to see a new Covid-19 risk:

Market risk now contains this management action:

Competition risk now contains this management action:

Reputation risk continues to refer to the “potentially embarrassing adverse history” of new franchisees:

3) Section 172 statement

This section is all new for 2019:

Suggests WINK is not departing from its “traditional franchising approach”.

A nice line about significant shareholders discussing the dividend, too.

4) Audit report

No obvious concerns. Materiality at a standard 5% of pre-tax profit and scope at 100%:

5) Key audit matters

Some changes from 2018.

No surprise that a new key matter is the Covid-19 going-concern assumption:

The “completeness of revenue” matter now involves the auditor performing an additional ‘8%’ check:

The “business combination — valuation of intangible” matter is new for 2019 and replaces the “recoverability of trade receivables” matter:

However, “recoverability of trade receivables” remains a critical accounting estimate, so has not been entirely forgotten.

An eye needs to be kept on trade receivables, as the franchisees can be tardy payers.

6) Going concern and post-balance-sheet event

WINK has stress-tested its balance sheet for Covid-19 by assuming a three-month shutdown (which seems appropriate to me):

A “range of scenarios” were evaluated:

7) Revenue recognition

A new line for 2019 confirms commissions are earned at a straight 8% of the franchisee’s income:

8) Critical estimate

This estimate is new for 2019:

Reveals how customer lists are valued by the industry. The customer list was acquired through the Tooting deal. Not quite sure what to make of the assumption that cash flow from Tooting’s lettings business will decline by 7% a year. I would like to think the projection is deliberately pessimistic.

9) Upcoming accounting standards

No impact:

10) Director pay and meetings

Nothing too awry with the board’s pay:

I suspect the chief exec received a c£13k bonus for 2019 given his salary (including bonus) for 2018 was £159k. No pay rises for other directors.

The non-execs do 15 days work for £20k each:

Nice to see the directors holding more audit meeting than remuneration meetings.

11) Employees

Difficult to read too much into these details following the extra staff employed through the Tooting deal:

That said, employee costs represented 34% of revenue versus 31% for 2018 and sub-30% for 2017 and earlier. Any future margin pressure is therefore likely to come from this expense.

12) Operating expenses

A couple of snippets here:

A 60% increase to the basic audit fee — presumably to do with the restatement of certain intangible assets as “prepaid assisted acquisitions support”.

A £162k bad debt was revealed. No such entry was revealed within the 2018 report. This bad debt is in addition to the trade-receivables earnings provision that reflects an estimate of bad debts every year. Past annual reports have shown the franchisees to be relatively slow payers.

13) Intangible useful life and website costs

Confirmation that website development costs that are capitalised on the balance sheet are amortised over three years:

I presume such costs relate to new franchisees and the development of their micro-sites that eventually generate sales. I can’t see why WINK should capitalise website costs for other purposes.

The costs were £170k last year but only £51k was expensed against earnings as amortisation. The £119k difference is not insignificant for WINK given 2019 profit was c£1.5m:

Also, the £51k amortisation does seem low given the historical cost of the website development was £255k at the start of the year and the useful life being 3 years.

For 2018, the amortisation charge was £74k and the historical cost the website development was £241k at the start of that year — so roughly what could be expected for a 3-year useful life.

This intangible expenditure requires ongoing monitoring.

14) Property, plant and equipment

WINK spent a remarkably low £9k on tangible assets last year:

15) Paid acquisitions assisted support and prior-year adjustment

The blog post above referred to most of the following. But here are the relevant extracts from the annual report:

The cash cost was £98k and amortisation charge against earnings was £160k. For 2018, the cash cost was again lower than the amortisation charge. As such the accounting looks fine at present.

16) Investments

WINK owns a tiny equity portfolio that did not perform too well during 2019:

Could be shares in other estate agents — Foxtons perhaps?

17) Trade and other receivables

Trade receivables of £476k represent a modest 7% of revenue:

However, the footnote says the £476k is stated net of a bad-debt provision of £306k — which seems large compared to the £476k.

The footnote also suggests an invoice has a 77% chance of not being paid if it becomes 61 days or more overdue:

These entires require further monitoring. Although WINK’s cash flow statement has never really suggested working capital movements have been problematic, this report and past ones have always indicated a sizeable proportion of trade receivables (money owned to WINK by franchisees) were overdue. I think the conclusion must be franchisees can be slow payers, but they do pay.

I was told at an AGM a few years ago that WINK collects its sales/letting commissions at the same point as the franchisee (i.e. the purchaser’s/tenant’s payments all go through the same IT system). The trade receivables must therefore relate to additional marketing and IT services that franchisees can buy from WINK, which represent a smaller part of total revenue.

18) Loans to franchisees

The trade and other receivables note also shows start-up loans to franchisees at £590k, down from £1,007k the year before:

19) Trade and other payables

Nothing much to see here. The new IFRS 16 standard has introduced lease obligations of £538k on to the balance sheet:

20) IFRS 16

The IFRS 16 note reveals that WINK — if it had to borrow money — would possibly pay interest at 4.2%:

That rate does not seem punitive, so I trust prospective lenders would see WINK as a good risk.

21) Options

No change here. 523,400 options represent 4.1% of the share count.

22) Related party disclosures

Bazmore Enterprise was the Tooting vendor:

Companies House says Mr Zaidi is in charge of Bazmore:

WINK’s website states Mr Zaidi owns 8% of WINK:

Maynard

M Winkworth (WINK)

AGM arrangements and AGM update

The AGM on the 12 May was held behind closed doors.

WINK did say:

“Should you have any questions of the board to be raised at the AGM, then please email them to the Company Secretary at the following address mdoregos at winkworth.com by no later than 5.00 p.m. on 8 May 2020. A Q&A reflecting the questions received and responses provided will be made available on the Company’s website at http://www.winkworthplc.com as soon as practicable following the AGM.”

I have only got around to reading the results, so rather shamefully I did not send any questions. Nor did anybody else it seems, as there is no Q&A on the website.

The AGM update said:

“Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that all the resolutions proposed at the Company’s annual general meeting held earlier today were approved by shareholders except for resolution 2, which concerned the reappointment of the auditors.

7,116,699 shares were voted against this resolution, amounting to 99.96% of the votes cast by shareholders who submitted votes in relation to this resolution. Accordingly, the Company will immediately begin the process of selecting new auditors for the current financial year.

The Board would like to thank Moore Stephens, now BDO, for their service as auditors since 2009.”

The statement reads as if chairman Simon Agace (42% shareholder), chief exec Dominic Agace (5% shareholder) and a few others voted out the auditors. I am not sure why the directors used the AGM to fire the auditors rather than simply tell them their services were no longer required. I can only presume the decision to vote off the auditors was due in part to the error involving the ‘prepaid acquisitions support payments’. I can’t recall another company — let alone its management — ever firing its auditor through an AGM.

Maynard

Hello, thanks. A long post and thorough post, I will read it in more detail.

Sacking auditors is always a bad sign, in my view ! I can understand if the audit went out to tender every few years and a ‘cheaper’ firm was selected.

I’m still getting my head around the ‘prepaid acquisition …”. It smells like an expense, pure and simple.

I do remember this company from when I lived in the the UK over a decade a go, so they definitely have a recognisable brand !

Thanks again for your posts.

Hi Christian,

Thanks for the comment. Yes, the auditor departure is all a bit odd. I am prepared to give the management the benefit of the doubt, as the books generally seem fine. The ‘prepaid support’ accounting restatement seems alright — the amortised cost is now treated as a deduction to revenue and having looked at the relevant accounting standard (for payments made to customers), the treatment appears above board. But I preferred the prior method, because the amortised cost went through the P&L proper and you could see the effect on profit. Mind you, the amortisation charge will still be in the notes so the effect on the old basis could be determined. Also, the ten-year amortisation life seems fair as that is the life of the franchise agreement. Overall, a bit of a mess, but nothing overtly sinister. What really counts now is these new franchisees performing well with their ‘prepaid support’!

Maynard

Cheers ! I’ve only just gotten around to reading your response. Hope life is returning to the UK :)

M Winkworth (WINK)

Dividend Declaration published 15 July 2020

Encouraging news in the circumstances — a Q2 dividend. Here is the full text:

——————————————————————————————————————–

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.4p per ordinary share for the second quarter of 2020 to shareholders.

Winkworth traded profitably in the first half of 2020 and the Group’s net cash position at the end of the period exceeded £3m. After adhering to government guidelines and rapidly adopting all the necessary measures to ensure the safety of customers and staff, Winkworth was well positioned to restart activity at the end of lockdown on 13 May. Between that date and 30 June, Winkworth ranked second in London for both instructions and sales*.

While the outlook for the second half of the year remains hard to predict, the board remains committed to paying a quarterly dividend.

The Directors are also pleased to announce that, following a formal tender process, it has been agreed that Crowe UK LLP will be appointed as the Company’s auditor for the year ended 31 December 2020.

* Source: TwentyEA (sales subject to contract)

——————————————————————————————————————–

The 1.4p per share payout is lower than the 1.68p per share Q1 payout, and perhaps indicates 5.6p is now the ‘base’ annual level given the commitment to further quarterly payouts.

Net cash was £3,571k at the 2019 year-end, so net cash above £3m for the end of June and 3.5p per share of dividends paid in the meantime (c£445k) suggests the business was indeed profitable (just) during the first half.

Of course, Q1 could have been profitable and Q2 could have been unprofitable. We’ll probably never know.

Maynard

M Winkworth (WINK)

Market update published 03 August 2020

House buyers have rushed back to the market. Here is the full text:

————————————————————————————————————————————–

“The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to provide some commentary on residential property market activity in its franchise network of 100 offices nationwide .

Since 8 July 2020, when the Chancellor announced an easing of the stamp duty threshold from £125,000 to £500,000 until 31 March 2021, the Winkworth network has seen a significant recovery in sales interest, with sales applicants registering on the day after the announcement up 64 per cent. on the previous week. Website traffic hit the highest ever level on the day of the announcement. There has also been a material rise in the number of instructions and viewings since 8 July 2020, up 17 per cent. and 14 per cent., respectively, on the same period last year and by 13 per cent. and 22 per cent. compared to early June 2020.

Although the significant rise in activity is welcomed, it is too early to predict to what extent this will translate into completed sales and how sustained this increased activity level will be across the network. Accordingly, and although encouraging, it is not yet possible to predict the extent of any impact on Winkworth’s financial performance.

Dominic Agace, Chief Executive of Winkworth, commented : “Post-lockdown, we had already seen a sharp uptick in activity, the result of the pent-up demand caused by several years of political uncertainty, the disruption caused by the market being effectively closed for several weeks and buyers re-evaluating their future lifestyle choices.

“This has now been our busiest July in at least the past five years. The changes in stamp duty have turbo-charged the market. Our network is reporting a significant uplift in activity at all price levels, with a focus not only on London and the commuter belt, but also on towns and cities with a longer commute, reflecting the move to a more flexible working landscape.”

————————————————————————————————————————————–

Some of this recent activity will have been delayed from March/April/May, but I would like to think the London market will remain active as many residents in the capital “move to a more flexible working landscape“.

The tone of WINK’s statement feels more positive than that of London rival Foxtons. FOXT’s results issued on 28 July 2020 said:

“Sales commissions over the 4 weeks of June were down 44% and over the 4 weeks of July were down 32% against the prior year. The sales commission pipeline has strengthened since re-opening and is now broadly in line with last year. Short term future sales activity is further supported by the Government’s Stamp Duty relief effective from 8 July 2020…

With the determined action that we have taken to ensure financial and operational flexibility, as well as ensuring the safety of our employees and customers, we remain confident that Foxtons is well-placed to capitalise as the market recovers. In such challenging times, we are committed to delivering the best results for our customers.”

Maynard