01 May 2020

By Maynard Paton

Results summary for Bioventix (BVXP):

- Very satisfactory 26% first-half profit growth led by continued demand for the group’s vitamin D antibody.

- A 20% dividend lift alongside presentation references to broker forecasts were very reassuring given the current Covid-19 uncertainty.

- The fledgling troponin product seems to have gained momentum while an emerging pollution-biomonitoring project offers intriguing long-term potential.

- Despite a part-time FD and an accounting error, the books remain in excellent shape with terrific 80% margins, a notable cash buffer and no debt.

- The seemingly ‘pandemic-proof’ outlook leaves the valuation remaining understandably rich with an underlying P/E of 34. I continue to hold.

Contents

- Event links and share data

- Why I own BVXP

- Results summary

- Revenue, profit, dividend and correction

- Vitamin D

- Troponin

- Other antibodies

- Pipeline developments

- Financials

- Valuation

Event links and share data

Event: Corrected interim results and presentation for the six months to 31 December 2019 published 31 March 2020

Price: £42

Shares in issue: 5,207,835

Market capitalisation: £219m

Why I own BVXP

- Develops diagnostic antibodies for blood-testing machines, direct competition for which is limited by regulatory hurdles, scientific innovation, customer switching costs and revenue ‘lock in’ through ‘captive’ hospital end-customers.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 8%/£17m shareholding and has declared four special dividends.

- Employs asset-light royalty/licence model that encompasses terrific margins, super returns on equity, decent cash flow and no debt.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Revenue, profit, dividend and correction

- These first-half results were very satisfactory.

- Unlike many quoted companies of late, BVXP not only declared a dividend — but actually lifted the payout by 20%.

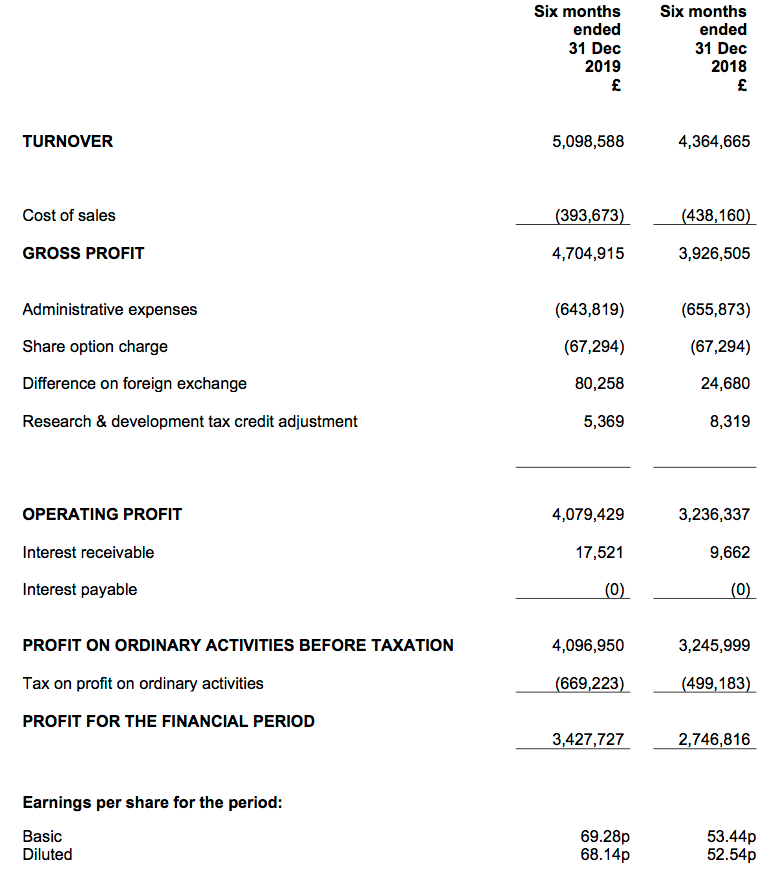

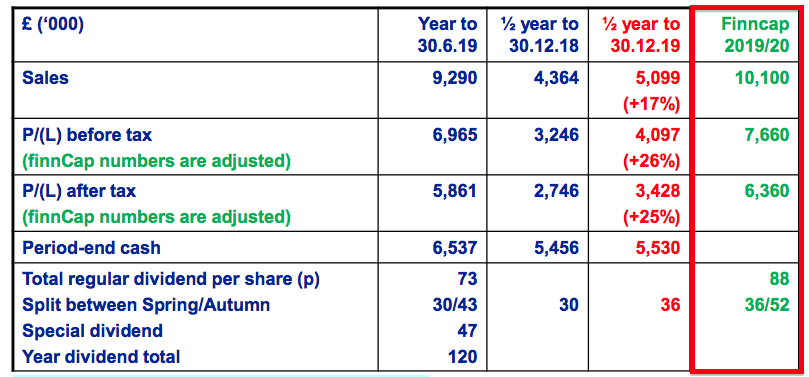

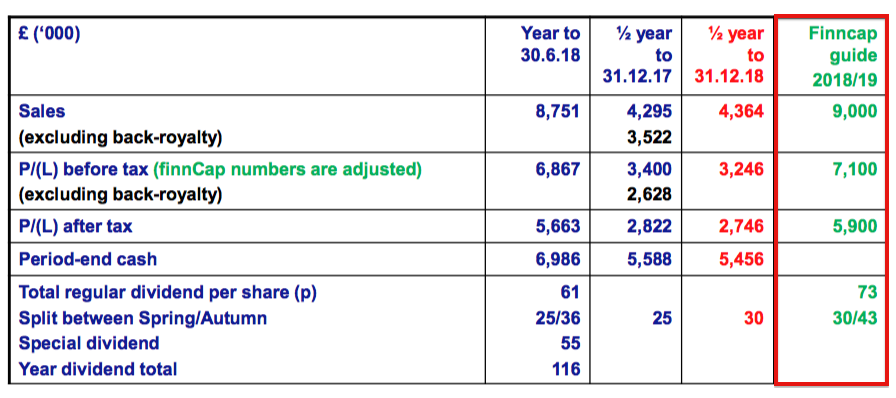

- The dividend increase was accompanied by reassuring remarks about the impact of Covid-19 (see Valuation below) alongside news that revenue had climbed 17% and operating profit had advanced 26%:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Revenue before back-dated royalties (£k) | 3,523 | 4,457 | 4,365 | 4,925 | 5,099 | ||

| Back-dated royalties (£k) | 772 | - | - | - | - | ||

| Revenue (£k) | 4,295 | 4,457 | 4,365 | 4,925 | 5,099 | ||

| Operating profit before back-dated royalties (£k) | 2,599 | 3,461 | 3,236 | 3,695 | 4,079 | ||

| Back-dated royalties (£k) | 772 | - | - | - | - | ||

| Operating profit (£k) | 3,372 | 3,461 | 3,236 | 3,695 | 4,079 |

- Unlike the previous year, these figures were not distorted by back-dated royalties or income from now-terminated products.

- Nor were the figures distorted by currency movements.

- I understand BVXP’s royalty income (representing up to 68% of 2019 revenue) is translated into GBP when overseas customers “self-declare” (point 3) their royalties during February (for H1) and August (for H2).

- BVXP’s predominant overseas currency is USD, which traded at an 1.30 average to GBP during both February 2019 and February 2020.

- This H1 performance was somewhat better than the preceding H2 achievement, during which revenue and profit gained 11% and 8% respectively.

- The downside to these numbers was an accounting error within the original RNS.

- BVXP first published the results at 7am on Monday 30 March and declared revenue of £5.3m and a pre-tax profit of £4.3m.

- BVXP then published the corrected results at 5:47pm on Tuesday 31 March, and admitted an “administrative error” allowed a £167k cost “not to be entered into the accounting system”.

- True, revenue and profit being revised down by £167k did not significantly alter BVXP’s general financial performance.

- But the accounting oversight does bring greater attention to the company’s finance function.

- BVXP’s finance director is a board non-exec and a partner at an accountancy firm, to which BVXP pays £19k a year for her FD services.

- £19k a year equates to working less than one day a week for a typical full-time FD working at an AIM-traded share.

- BVXP employs only 12 full-time equivalent staff, so the outsourced FD is unlikely to enjoy significant in-house assistance.

- I am all for companies keeping costs to a minimum.

- However, BVXP really ought to enhance its finance function to avoid further admin errors and sloppy reporting.

- Shareholder must have confidence in the accounts they are given in an RNS — and not trade the shares for two days using incorrect information.

- I wonder whether the appearance of back-dated royalties during 2014 and 2018 — when BVXP’s customers owned up to having underpaid in previous years — would have have occurred with a more alert finance function.

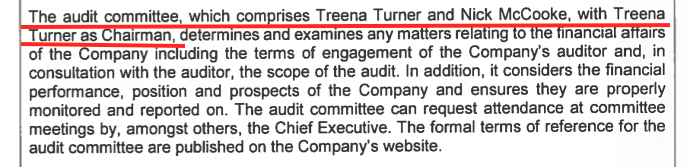

- The 2019 annual report (point 1) reveals the part-time FD is also the chairperson of BVXP’s audit committee:

- I don’t feel company FDs — even if they are non-execs — should be in charge of audit committees.

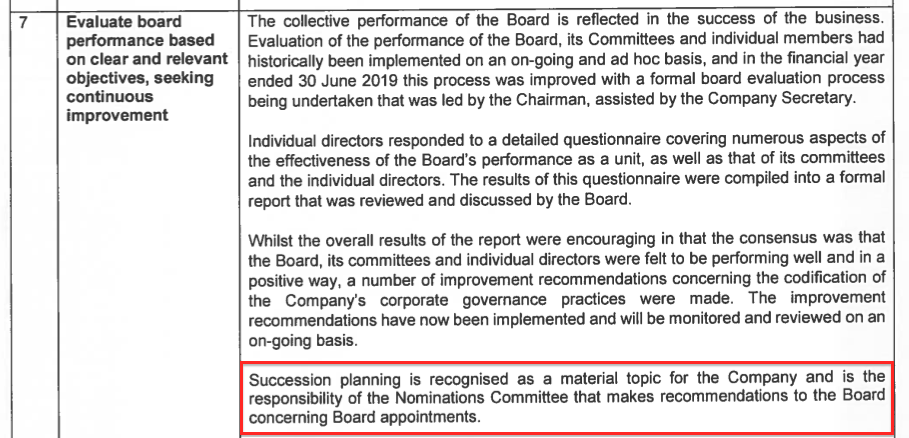

- The 2019 annual report (point 1) also mentioned “succession planning”:

- I had assumed such planning related only to the role of chief executive.

- Maybe some succession-planning thought should be given to the role of FD.

- The admin error should of course not detract from what were very positive results and the seemingly pandemic-proof outlook (see Valuation below).

- I would rather have BVXP’s sloppy reporting, higher earnings and rising dividend, than precise reporting, future losses and a scrapped payout.

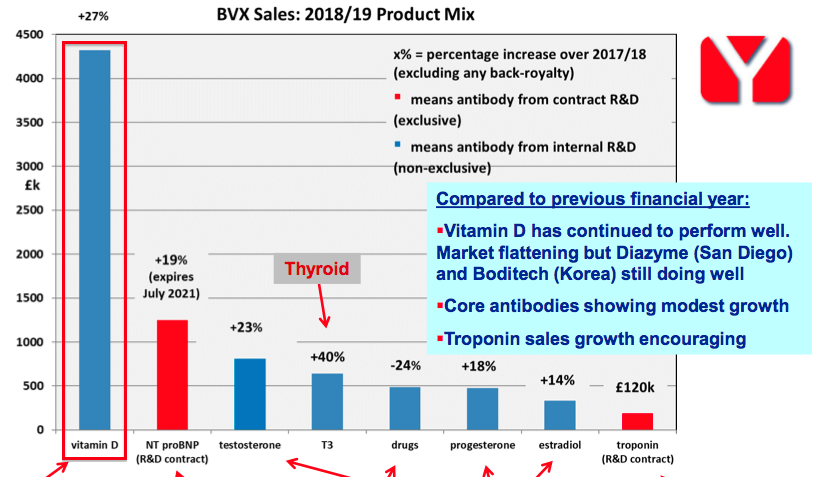

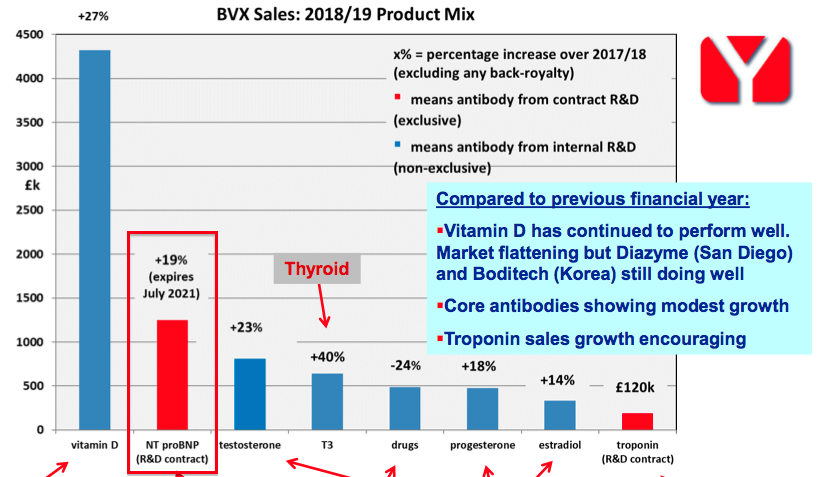

Vitamin D

- The market for BVXP’s vitamin D antibody continues to grow and defy BVXP’s caution that demand might “plateau”.

- BVXP said (my bold):

“Vitamin D antibody sales growth continued at the healthy levels seen during the previous financial year. Whilst this is very encouraging, we continue to see evidence of a plateau in the downstream global vitamin D assay market. We have previously commented on the impressive performance of two specific customers in the downstream vitamin D test market — Diazyme (San Diego, US) and Boditech (South Korea) — and their sales continued to grow.”

- Within the 2019 full-year results, BVXP said (my bold): “This is clearly evidenced by a number of our vitamin D customer revenue streams which, after a period of significant growth now appear to have reached a plateau.”

- Within the 2018 full-year results, BVXP said (my bold): “Whilst actual royalties received were once again in excess of expectations, we nevertheless perceive a plateauing of the vitamin D testing market.”

- Within the 2017 full-year results, BVXP said: “Our prudent belief is that the vitamin D market will plateau in the near future.”

- Between 2017 (when “plateau” was first mentioned) and 2019, revenue from the vitamin D antibody increased from approximately £2.8m to £4.3m — or 50%.

- Perhaps BVXP likes to under-promise and over-deliver.

- Or perhaps one day the market for the vitamin D antibody will in fact plateau.

- I understand that vitamin D “plateauing” could mean the associated growth reduces to wider industry levels of between 5% and 10% per annum, rather than stagnate completely.

- Representing 46% of 2019 revenue, the vitamin D antibody is by some distance BVXP’s best-seller — so demand for the product significantly influences the group’s progress:

- For now at least, BVXP claims vitamin D growth depends on “two specific customers in the downstream… test market”.

- BVXP has explained in the past that these two customers sell their vitamin D tests for use by “general chemistry analysers”.

- I understand these “general chemistry analysers” can be used on any blood-testing machine.

- In contrast, BVXP’s ‘conventional’ vitamin D sales have been limited to usage on certain blood-testing machines — which I believe to be those manufactured by Siemens, Beckman Coulter and Ortho.

- I understand BVXP’s royalty on vitamin D remains at 4% to 5% regardless of the customer. Other BVXP antibodies earn 2% royalties.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

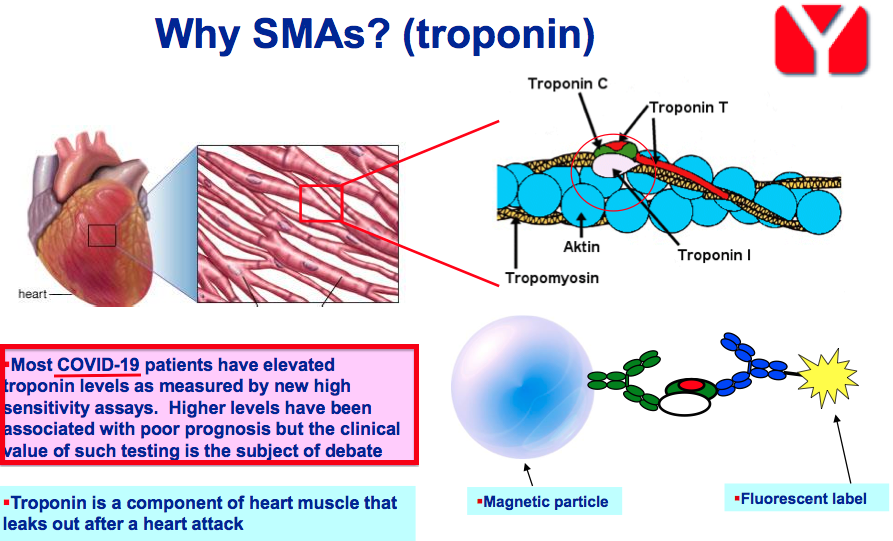

Troponin

- Revenue from BVXP’s new troponin antibody — used to help detect potential heart attacks — continues to grow:

“Sales relating to troponin antibodies grew significantly during the period. Whilst the actual sales were slightly below our expectation, the percentage growth provides further evidence of the roll-out of these new tests and encouragement for the future sales performance.”

- I understand troponin earned revenue of £50k during H1 2019 and £70k during H2 2019.

- I also understand BVXP expects troponin to earn £500k for 2020.

- As such, perhaps this H1 witnessed troponin revenue of, say, £200k, and for the forthcoming H2 will produce revenue of, say, £300k.

- The troponin roll-out has been slower than expected following BVXP’s comments of an “education period… during which clinicians become comfortable with a significant change in diagnostic practices” within the 2017 results.

- The H1 results presentation included some vague remarks about elevated troponin levels associated with potential Covid-19 infection:

- Bear in mind that the 2019 full-year results presentation suggested company growth between 2020 and 2025 would be dependent largely on troponin:

Other antibodies

- BVXP did not give much away about the progress of its other “core” antibodies:

“Other revenue streams for the core of established antibodies showed modest growth during the period. Added to this were increased sales of a number of newer antibodies to T4 (thyroxine), androstenedione (a steroid closely related to testosterone) and biotin (used as a replacement for streptavidin).”

- The presentation slides noted (my bold):

“Revenues increased for… some other core antibody products. Newer product sales (T4, andro & biotin) were individually modest but collectively additive”

- The 2019 results had revealed revenue from “core” antibodies up 14%, with lower sales from certain drug-testing products.

- This H1 statement mentioned nothing about the NT proBNP antibody.

- Revenue from NT proBNP will expire during 2021, and represented 13% of total group revenue during 2019:

- Assuming annualised NT proBNP revenue remains at £1.25m, I reckon other income sources will have to expand by a collective 14% to make up the forthcoming shortfall.

Pipeline developments

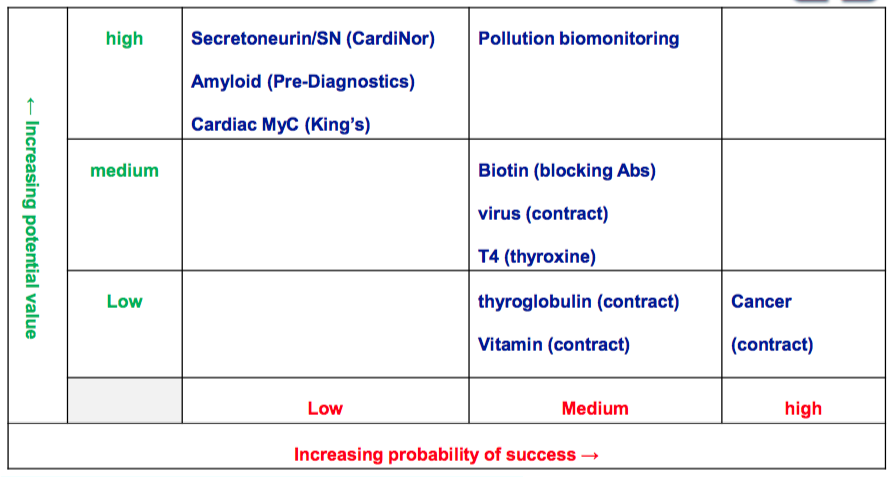

- BVXP’s product-pipeline grid remained unchanged:

- Given the position on the grid, “pollution biomonitoring” appears to be BVXP’s best risk/reward development opportunity.

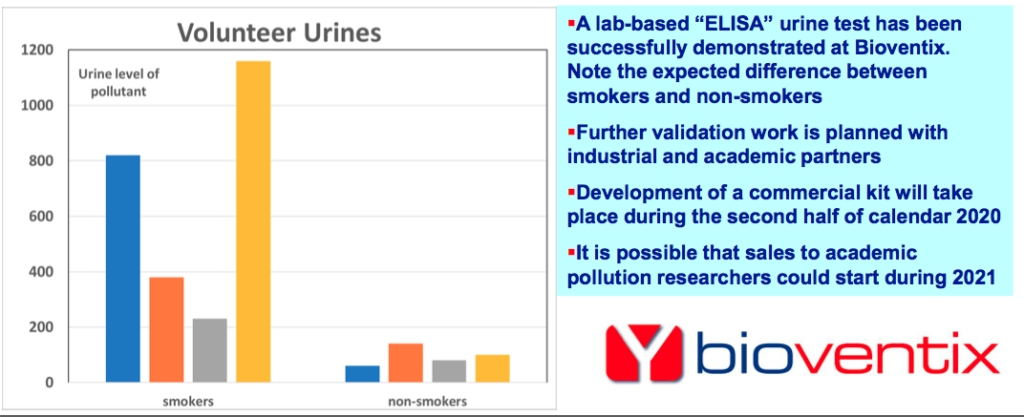

- This biomonitoring project seems to be going well. BVXP said:

“We are particularly pleased with the development of our pollution exposure assay. We have successfully tested a prototype lab-based ELISA (enzyme-linked immunosorbent assay) and this will progress towards commercial kit manufacture during the second half of calendar 2020.

Our hope is that we will have a lab-based kit available for sale to pollution researchers sometime during calendar 2021. In addition to the pollution research market, it is also possible that the test will have a degree of utility in the health and safety field (i.e. industrial worker biomonitoring). We will initially introduce the test directly to interested parties before seeking appropriate commercial partners for the future.”

- The presentation contained a slide that showed the biomonitoring results from eight people — four smokers and four non-smokers:

- The pollution results from this small study look clear to me.

- I understand the project’s testing kit will be aimed initially at research organisations and may sell for £200 a pop.

- I have also been told the biomonitoring technology is difficult to copy because it can work with low concentrations of pollutants.

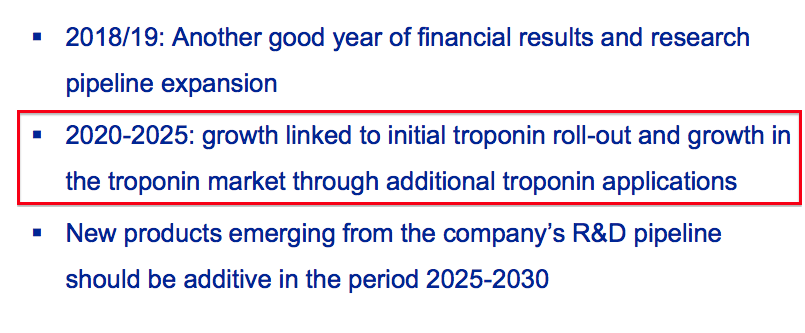

- Whether any of BVXP’s other pipeline developments ever come good remains to be seen. The 2019 full-year results implied none of them would become commercial before 2025.

- BVXP says an antibody can take between four and ten years to go from the laboratory to earning a royalty income (assuming the antibody actually becomes commercially viable).

- For some context, development of BVXP’s troponin antibody began during 2006 and started earning a return last year.

Financials

- BVXP’s accounts remain in extremely good shape:

- The 2019 full-year results had indicated margins may improve following a “transient” reduction in antibody stocks:

“The cost of sales has been influenced (i.e. increased) to some extent by a reduction in antibody stocks. This is a transient effect that should be reversed during 2019/20 of approximately £200k on external contract chemistry services linked to the biotin and pollution projects…”

- In fact, BVXP’s H1 operating margin reached 80% — the highest since the 81% achieved during H2 2016 — and underlined the incredibly lucrative economics of antibody royalties.

- Cash in the bank fell by £1.0m during the six months to £5.5m. Earnings of £3.4m for this H1 were offset entirely by cash payments of £4.6m for last year’s final/special dividends.

- In addition, £0.3m was spent on upgrading the firm’s laboratory while £0.2m was spent subscribing to extra shares in a Norwegian research partner.

- However, H1 cash flow was helped by a favourable £0.3m working-capital movement alongside next-to-nothing paid as tax.

- Half-year cash of £5.5m surpassed the “approximately £5m” that BVXP has said is “sufficient to facilitate operational and strategic agility with respect to possible corporate or technological opportunities that could arise in the foreseeable future.”

- This time last year, half-year cash was also £5.5m — and the ‘excess’ cash generated during the second half went towards funding a 47p per share/£2.4m special dividend.

- BVXP said within these results:

“Bioventix is a resilient business and the Board will continue to follow [its] established dividend policy.”

- That comment suggests any ‘excess’ cash available at the full-year stage may once again be returned to shareholders as a special dividend.

- BVXP has declared special dividends during 2016, 2017, 2018 and 2019.

- The balance sheet carries no bank debt and no pension complications.

Valuation

- BVXP’s outlook was positive (my bold):

“[W]e are encouraged by the performance for the six months ended December 2019 and pleased with the continued success of our vitamin D antibody and core antibody business. We remain optimistic about our troponin revenues and the success of these high sensitivity troponin products around the world. Whilst we are mindful as to the potential impact of COVID-19, we currently expect further progress in the second half of the year.”

- The potential impact of Covid-19 did not seem too worrying. BVXP claimed “some routine diagnostic testing could be reduced as hospitals refocus towards virus-infected patients.“

- However, BVXP did add (my bold): “In most affected countries, healthcare and associated products and services have been prioritised and so we expect that our customers will continue to operate and that we will continue to supply antibodies to them.”

- The ‘outlook’ presentation slide is worth noting:

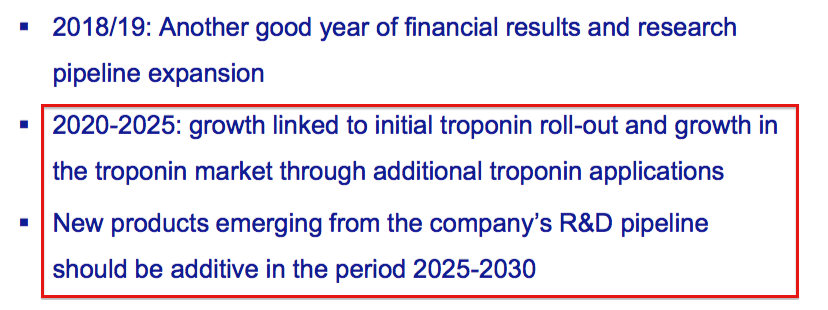

- Unlike previous presentations, the ‘outlook’ slide did not provide any long-term growth timescales.

- The full-year 2019 slides for example mentioned 2020-2025 and 2025-2030:

- Perhaps BVXP is no longer as confident about the next decade as it once was.

- BVXP’s trailing pre-tax profit of £7.8m taxed at the 16% rate applied within these results gives earning of £6.5m or 125p per share.

- BVXP’s £5.5m cash position equates to approximately £1 per share and does not make a great difference to my valuation sums when the share price is £42.

- Dividing the £42 share price by my 125p per share earnings estimate gives an underlying trailing P/E of 34.

- The rating remains lofty at more than twice the 14x market average.

- However, BVXP’s growth rate, margins and returns on equity are perhaps (at least) twice as attractive as the market average.

- Should BVXP’s earnings continue to advance throughout the pandemic, perhaps the shares can sustain a high multiple as more investors start to appreciate the company’s all-round resilience.

- BVXP’s presentation once again commendably included the house broker’s forecasts:

- The inclusion of these forecasts remains unusual — companies typically don’t want to endorse broker projections just in case the projections are not met.

- The inclusion of these forecasts at the present time is extremely unusual — most companies are currently withdrawing guidance and many broker projections have therefore become redundant.

- Nonetheless, BVXP’s broker reckons 2020 will see revenue and pre-tax profit both advance between 9% and 10%.

- The prediction implies H2 revenue will advance by just 2% while H2 pre-tax profit will drop by 4%.

- Predicting H2 profit dropping 4% feels rather pessimistic to me.

- The time last year the broker expected revenue of £9.0m and an adjusted pre-tax profit of £7.1m:

- The revenue prediction was £0.3m below the actual £9.3m recorded.

- The pre-tax profit prediction was £135k above the actual £7.0m recorded.

- The house broker also predicts the full-year dividend rising 21% to 88p per share.

- The trailing twelve-month dividend is 79p per share, which supports a 1.9% yield.

- Given BVXP has effectively distributed all of its earnings as ordinary and special dividends since 2016, then perhaps the 3.0% yield based on my 125p per share earning guess could be a more appropriate income measure.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Bioventix.

Bioventix (BVX)

Appointment of CFO

About time. Here is the full text:

——————————————————————————————————————-

Bioventix plc (BVXP), a UK company specialising in the development and commercial supply of high-affinity monoclonal antibodies for applications in clinical diagnostics, announces that Bruce Hiscock will join the Board as Chief Financial Officer with immediate effect.

Mr Hiscock was previously CEO and CFO of everyLIFE Technologies, a technology business delivering digital care planning solutions to social care providers. Prior to this he was the Managing Director of MITIE Security Systems, the CEO of Protec plc, an AIM listed security and technology services business, and held several CFO roles at both fast-growing listed and private companies over a 30-year career. Mr Hiscock is a member of the Institute of Chartered Accountants of Scotland.

——————————————————————————————————————-

I mentioned within the blog post above:

“However, BVXP really ought to enhance its finance function to avoid further admin errors and sloppy reporting.”

“Maybe some succession-planning thought should be given to the role of FD.”

Good to see the new appointment. I presume the role is full time, or at least more than the one-day-a-week of the previous FD.

Maynard