18 May 2020

By Maynard Paton

Results summary for FW Thorpe (TFW):

- Acceptable 7-9% first-half growth, although profitability has essentially stalled for the last 2-3 years as the LED mini-boom subsides.

- A 2% dividend lift, net cash and investments of £47m, a “strong” order book plus an outstanding response to government assistance do not imply immediate Covid-19 problems.

- However, trading is not perfect, as margins at the largest division continue to decline while overseas cross-selling progress remains slow and small.

- The SmartScan light-monitoring system could be a ‘hidden gem’, with sales up 50% last year to represent 20% of total revenue.

- A P/E of 22-25 feels warm, but may reflect the ‘pandemic-proof’ balance sheet, SmartScan potential and/or resilient profit history. I continue to hold.

Contents

- Event link, share data and disclosure

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Thorlux

- Lightronics and Other

- Financials

- Valuation

Event link, share data and disclosure

Event: Interim results for the six months to 31 December 2019 published 25 March 2020

Price: 315p

Shares in issue: 116,330,497

Market capitalisation: £366m

Disclosure: Maynard owns shares in FW Thorpe. This blog post contains SharePad affiliate links.

Why I own TFW

- Manufactures commercial lighting systems with a long-established reputation for high product quality, leading technical innovation and tip-top customer service.

- Board led by a veteran executive and assisted by family non-execs that steward a 50%-plus/£183m-plus shareholding.

- Conservative accounts showcase ‘pandemic-proof’ balance sheet, resilient profit history and confident dividend lift.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary:

Revenue, profit and dividend

- Phrases such as “order levels are good” within November’s AGM statement had already hinted this first-half performance would be acceptable.

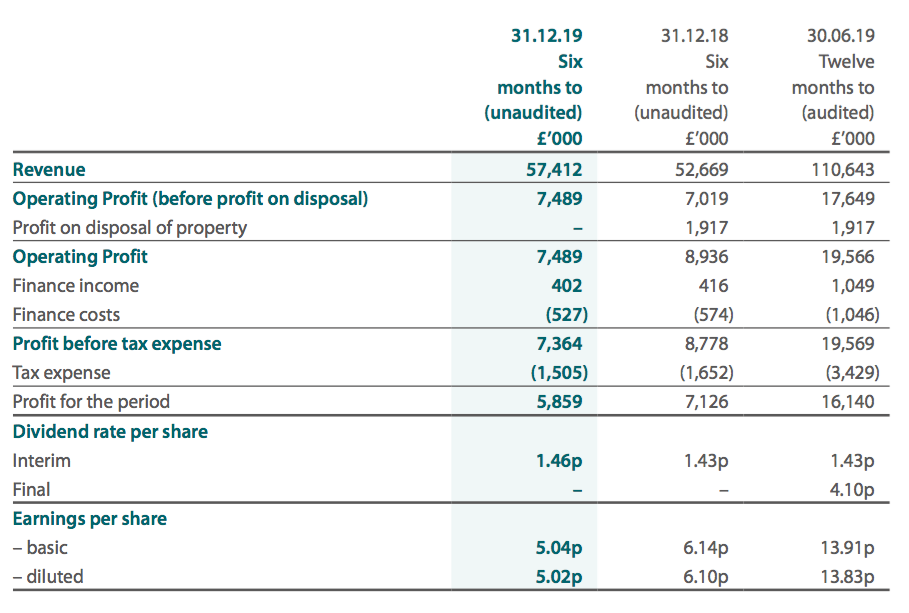

- The results showed H1 revenue up 9% and H1 operating profit up 7%.

- The positive progress was due mostly to the group recovering from a particularly weak first half during 2019.

- Although revenue at £57m reached a new H1 record, operating profit remains lower than the H1 level struck in 2018 (and 2017):

| Group | H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | ||

| Revenue (£k) | 53,170 | 56,444 | 52,669 | 57,974 | 57,412 | ||

| Operating profit (£k) | 7,829 | 11,396 | 7,019 | 10,338 | 7,489 |

- The performance was not skewed by acquisitions. Progress during 2019 was distorted by the purchase of Famostar and during 2016 was distorted by the purchase of Lightronics.

- The most welcome feature of these results was the 2% lift to the interim dividend.

- A 2% dividend increase would normally be somewhat disappointing.

- But when many other quoted companies have cancelled or withdrawn their payouts due to Covid-19, TFW’s 2% advance should encourage outside shareholders.

- TFW’s dividend confidence was based upon its “strong” balance sheet:

“[T]he Group has always maintained a strong balance sheet with sufficient cash and other liquid assets to protect business continuity from the impact of sudden economic impacts and unforeseen risks. Although the impact of the current crisis is uncertain, we cannot foresee a downside scenario where we are unable to manage business continuity for the foreseeable future by utilising our current resources.”

- Companies often describe their balance sheets as “strong” when they are in fact laden with debt.

- However, the “strong” adjective was very appropriate for TFW.

- These H1 accounts showed cash and various investments of £61m versus debt of just £1m and earn-out obligations of approximately £12m. (see Financials below).

- In the past I have written: “[TFW’s] management has never really explained why such a huge level of cash is needed.”

- I no longer need an explanation.

- Instead, I should applaud Andrew and Ian Thorpe — both grandsons of founder Fred and current TFW non-execs — for insisting on a “strong” balance sheet that protects their family’s 50%-plus/£183m-plus shareholding.

- TFW admitted the pandemic had caused some disruption:

“The current coronavirus situation provides us with further challenges that had not been anticipated at the time of previous announcements… Group companies also reacted early and took proactive measures to reduce infection risk within the workplace for the good of the employees and the business; these measures are under constant review.

We continue to support our customers where practical… highly likely that Group companies will see considerable disruption to delivery schedules.”

- However, TFW’s factories remain open. The company has recorded this informative video:

- TFW is not relying on government support during the pandemic.

- This Covid-19 statement from a subsidiary website is worth repeating in full:

“We have decided that we will not apply for compensation for furloughed employees during this initial period of lockdown, and we will continue to offer all employees normal pay whilst they are not working.

The Job Retention Scheme was introduced to save jobs which, during the Covid-19 lockdown, would otherwise have been made redundant because of a company’s inability to stay afloat, thus keeping people and critical skills within a business.

We believe the scheme is not intended to support businesses that otherwise have sufficient resources to pay their employees and intend to bring their employees back to work after a reasonable period when the crisis ends.

Thorlux is committed to supporting its excellent workforce and, through prudent management of the business over many successful years, has a strong balance sheet with sufficient reserves. Thorlux prides itself on being a responsible corporate employer, and during this time we feel it is important that we contribute to supporting the national effort. This can be done by continuing to provide our goods and services where they are needed, such as our work with the NHS, but also by enabling the government to target its remaining funds to those areas where they are required the most.“

- Hats off to TFW for that outstanding response.

- TFW admitted the current H2 performance remains anyone’s guess:

“It is therefore difficult for us to determine the impact on second half performance and beyond.”

- At least TFW said a “a strong order book” provided “an excellent reservoir to smooth current turbulence”.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Thorlux

- TFW largest subsidiary — Thorlux — reported revenue up 14% and profit up 4% during the half:

| Thorlux | H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | ||

| Revenue (£k) | 32,298 | 32,347 | 28,442 | 33,862 | 32,363 | ||

| Operating profit (£k) | 5,948 | 7,663 | 4,659 | 6,919 | 4,839 |

- Thorlux’s margin was an unspectacular 13%.

- TFW cited larger projects for the lower margin during this H1:

“Orders at Thorlux remain hard-fought; however, underlying revenue is good, and some additional one-off project work has been completed which has provided a welcome boost. The larger size of projects has consequently led to tighter margins. In some cases, projects involve services including survey work and project management, leading to increased overheads.”

- Thorlux’s £4.8m H1 profit was equal to that recorded for H1 2014 and compares to the bumper £5.9m reported for H1 2018.

- Thorlux usually reports a better profit and margin during H2.

- Thorlux’s margin was 18.0% during H1 2012, and has since declined to 17.5%, 17.2%, 16.9%, 15.7%, 14.9%, 14.7%, 13.3% and now to 13.0% during the subsequent eight years.

- The division’s margin trend is not great. Indeed, Thorlux’s full-year margin for 2019 was 18.6% — the weakest for at least ten years.

- An obvious concern is whether Thorlux has gradually lost its technical competitive advantage and must now fight harder on price.

- Perhaps the shift from traditional lighting to LEDs during recent years created an industry mini-boom— and with it higher margins — that has now subsided.

- The 2019 annual report (point 6) revealed 90% of group sales are now generated by LED products.

- TFW admitted within the 2019 results:

“Customer interest in LED luminaire technology has peaked because of the smaller improvements in LED chip performance.”

- Thorlux’s SmartScan product may take up where LEDs left off.

- SmartScan is a control platform that monitors and controls lighting systems. The service provides customers with energy reports, emergency lighting tests, “occupancy profiling” information and even air-quality data.

- The 2019 annual report (point 1) — but not the 2019 results RNS — revealed revenue from SmartScan improved more than 50% last year to £22m (20% of total revenue).

Lightronics and Other

- Lightronics reported subdued progress:

Lightronics| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 |

| ||

| Revenue (£k) | 10,210 | 10,650 | 11,869 | 11,285 | 11,147 | ||

| Operating profit (£k) | 1,102 | 948 | 1,066 | 1,291 | 1,074 |

- The Dutch operation’s revenue fell 6% while its profit advanced just 1%.

- The H1 performance matched that of H1 2019 and H1 2018.

- Following a sparkling first year under TFW’s ownership, Lightronics has not really excited thereafter.

- One issue is the lack of product cross-selling with the main Thorlux subsidiary.

- The 2019 annual report (point 4) disclosed sales of only £0.4m were generated on behalf of TFW’s main division.

- TFW’s eight smaller operations delivered aggregate revenue up 12% and profit up 10%:

| Other | H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | ||

| Revenue (£k) | 10,662 | 13,447 | 12,358 | 12,827 | 13,902 | ||

| Operating profit (£k) | 782 | 2,625 | 1,220 | 2,441 | 1,347 |

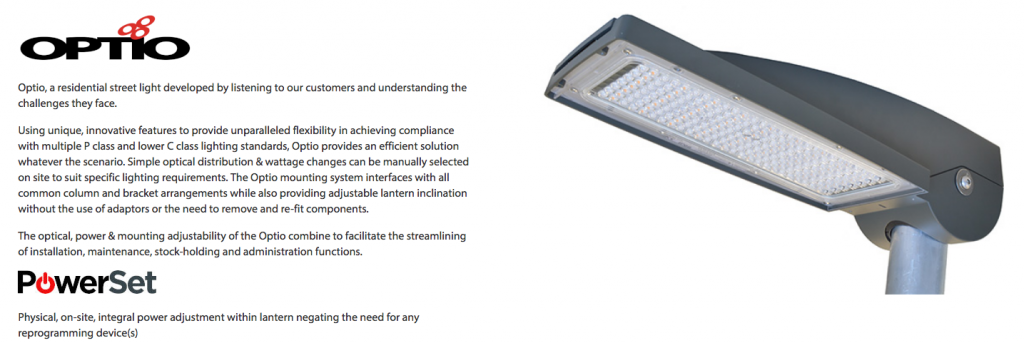

- The results RNS revealed an “improved performance at both TRT and Famostar”.

- TRT is TFW’s road and tunnel lighting subsidiary and its “improved performance” may have followed the launch of a new street light called Optio:

- TFW reported Dutch subsidiary Famostar had an “excellent” 2019 and presumably that momentum continued into 2020.

- Bear in mind that TFW’s smaller operations supply lighting that illuminate shops, advertising hoardings, universities and public buildings. Demand for such lighting during the pandemic may well have dimmed.

Financials

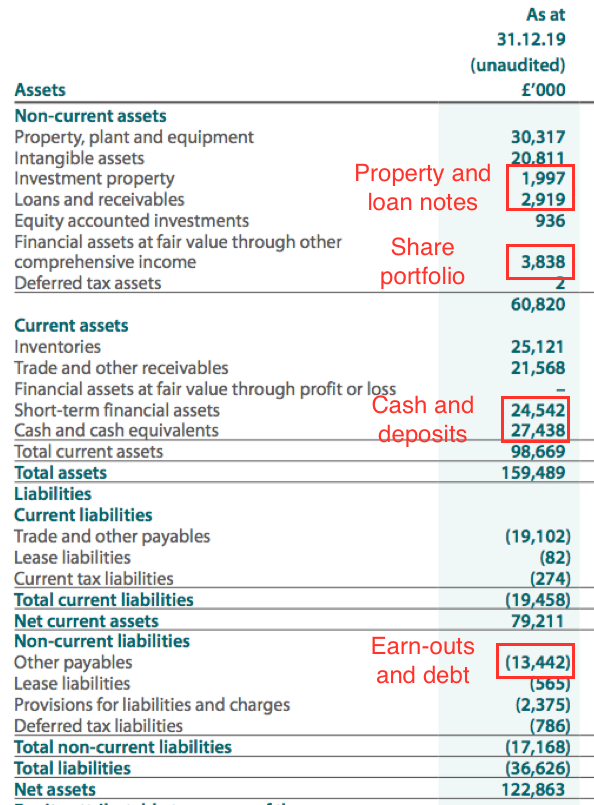

- TFW’s aforementioned “strong” balance sheet carried cash and term deposits of £52m:

- Other assets include investment property of £2m, loan notes of £3m and a share portfolio of £4m.

- Yearly rental income of £0.2m indicates the investment property is valued on a 10% gross yield.

- Yearly dividend income of £0.2m suggests the share portfolio yields 5%.

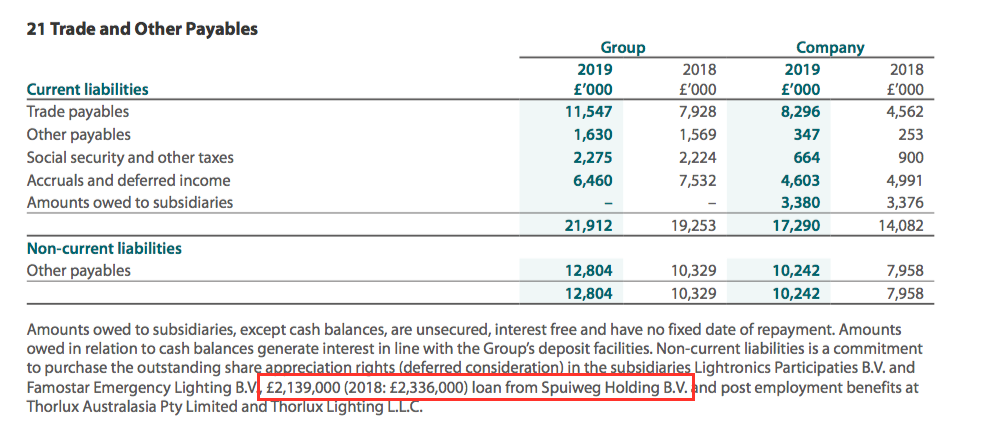

- ‘Other payables’ of £13m mostly represent the earn-outs due to the former owners of Lightronics and Famostar.

- Note 21 of the 2019 annual report (point 21) revealed ‘other payables’ includes debt of £2.1m relating to the Dutch operations:

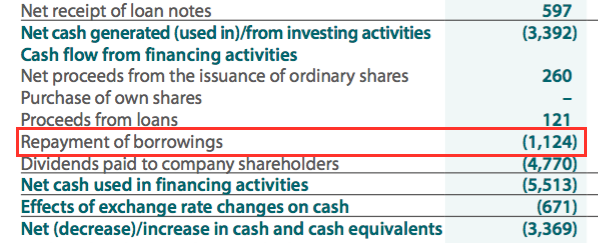

- This H1 RNS showed repayment of borrowings of £1.1m, suggesting debt has been reduced to approximately £1m:

- Cash and the various investments less the earn-outs, debt and some other financial obligations come to £47m or 41p per share.

- I am sure TFW’s asset position will reassure customers and suppliers that orders will be completed and bills will be paid during the pandemic.

- Despite the large cash/investment position and tiny borrowings, finance income of £402k during this H1 was counterbalanced by finance costs of £527k.

- Finance costs consist mostly of a “share appreciation right distribution” — which reflects the dividends associated with the earn-out payable to the former owners of Lightronics and Famostar.

- The H1 cash flow statement did not include a corresponding entry, and I believe the “share appreciation right distribution” is a bookkeeping item that is added on to the final earn-out under ‘other payables’.

- The Lightronics and Famostar earn-outs are due to be paid by TFW during 2021.

- Cash flow was hindered by capital expenditure of £5.4m — of which most was spent on property — and an adverse £1.7m working-capital movement.

- TFW’s defined benefit-pension scheme last sported a £2m surplus (point 22), although an annual £0.2m cash contribution continues to by-pass the income statement.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- TFW not surprisingly predicted the current second half would not be as profitable as the preceding H2:

“Group performance in the second half of 2019 was strong and will, due to the latest circumstances, prove challenging and unlikely to improve upon in 2020.”

- My sums suggest the 315p share price is looking well beyond the next six months.

- Taking the optimistic view and projecting a repeat of H2 2019 for H2 2020, full-year operating profit might be £18.1m and earnings could be £14.5m, or 12.5p per share.

- Subtract the 41p per share net cash and investments from the 315p share price, and the underlying P/E might be 22.

- The P/E rises to 25 if the cash and investments are in fact critical to the business and not really ‘surplus to requirements’.

- The ratings appear warm given profits at Thorlux and Lightronics have stalled during the last few years.

- The Covid-19 uncertainty makes the 22-25x rating all the more peculiar.

- Perhaps investors are willing to apply a high multiple for the reassurance of a ‘pandemic-proof’ balance sheet.

- Perhaps investors are willing to apply a high multiple because of SmartScan and the possibility the product could soon become a dominant force for growth.

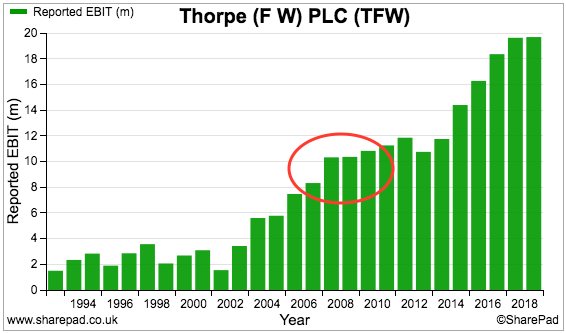

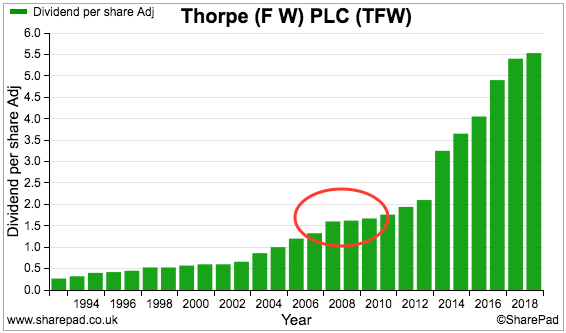

- Perhaps investors are willing to apply a high multiple because group profit and the dividend were sustained during the banking crash:

- TFW in fact went on to double in size following that downturn.

- Perhaps investors believe TFW can repeat that expansion this time around — and pick up extra business from rivals that falter during the current crisis.

- Only time will tell whether the present 315p really is appropriate for the company’s future earnings.

- The 5.56p per share trailing dividend meanwhile provides a modest 1.8% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Hi Maynard,

Great analysis, FW Thorpe have a great balance sheet, which is a rare thing to see in 2020. Their dividends are increasing each year as well.

If more people work from home moving forward I can see them making investments to home improvements, on the flip side I don’t think the next few years are going to be good for the housing market which could damper their light sales.

Great blog, keep up the good work.

Maynard,

I appreciate that in order to understand a company you need to analyse the annual report in detail. I have a holding in Thorpe and in my view the history of dividend payment with a major cut in 2013 with no change in share number indicates that the family want to keep the company going. The acquisitions just being paid out now will take a long time to benefit investors. I am not going to get rich on the dividends and the share price will take decades to make a difference.

The Thorpe family have already made a lot of money but I think that the younger generation is unlikely to be so patient.

Hello Colin,

Thanks for the message. I can’t recall a major dividend cut in 2013, but I agree the family want to keep the company going. Thorpe’s dividend payout has never made any outside investor rich, although the retained cash has proven its worth during the banking crash and the pandemic. The share price has performed in the past, but that was due in part to a P/E re-rating from the lowly multiple the shares once exhibited. The current multiple makes a further re-rating unlikely unless the company’s growth starts to accelerate. The SmartScan product could help in that regard. Thorpe is now led by a non-family executive and one area that he needs to address is overseas progress — which appears never to have really gained momentum despite the Dutch acquisitions.

Maynard