30 June 2020

By Maynard Paton

I trust your shares have recovered during the last three months.

A quick summary of my portfolio’s second-quarter and year-to-date progress:

- Q2 gain: +7.8%*

- Q2 trades: None.

- YTD loss: -0.9%* (FTSE 100: -16.9%**)

- YTD winners/losers: 3 winners vs 9 losers

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees and paid dividends. **Includes reinvested dividends)

I am thankful the news from my shares during Q2 was relatively positive. In particular, four of my holdings declared dividends — which seems encouraging given the numerous payout suspensions witnessed of late.

Mind you, I did not escape the dividend cancellations entirely. One of my shares sadly scrapped its payout after admitting the pandemic had led to weaker sales and operating losses.

Just how the market will fare from here is impossible to say. I did not buy during the March lows and remain 25% in cash… so I am naturally hoping the bargains have not dried up just yet!

Let me now outline what has happened within my portfolio during April, May and June. (Please click here to read all of my previous quarterly round-ups). I will then follow up with the 10 lessons I learned from holding a 10-bagger.

Contents

Disclosure

Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S&U, System1, Tasty, FW Thorpe, Tristel and M Winkworth. This blog post contains SharePad affiliate links.

Q2 share trades

None.

Q2 portfolio news

As usual I have kept an eye on all of my shareholdings. The Q2 developments are summarised below:

- Creditable results (and a dividend) from Andrews Sykes;

- Acceptable numbers (and a dividend) from M Winkworth;

- Record figures (and a dividend) from S & U;

- Resilient progress (and a dividend) from Mountview Estates and Mincon;

- Weak trading and pandemic losses (and a cancelled dividend) at System1;

- A significant (but not-too-radical) merger between City of London Investment and Karpus Management;

- The re-opening of some restaurants at Tasty, and;

- Nothing from Bioventix, FW Thorpe and Tristel.

Q2 portfolio returns

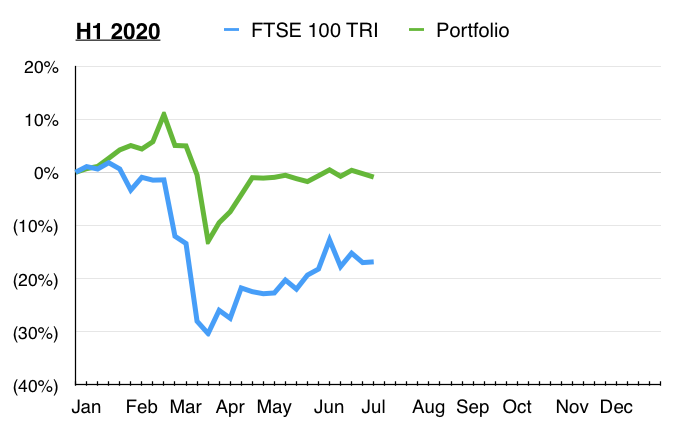

The chart below compares my portfolio’s weekly 2020 progress (in green) to that of the FTSE 100 total return index (in blue):

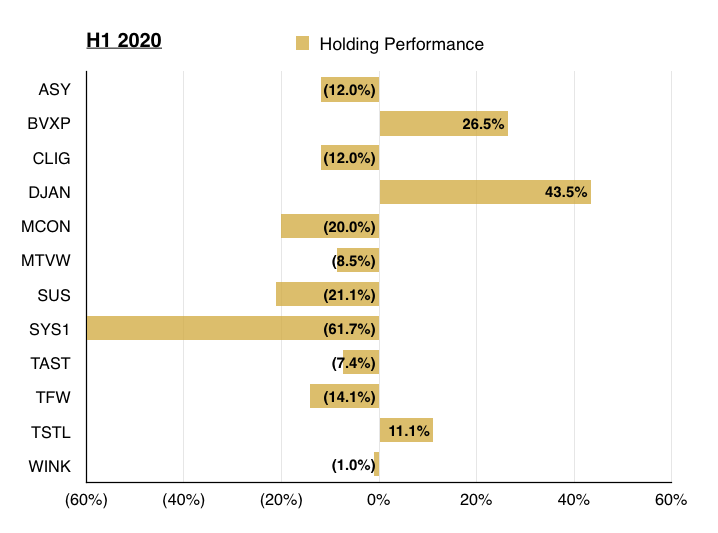

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me year to date:

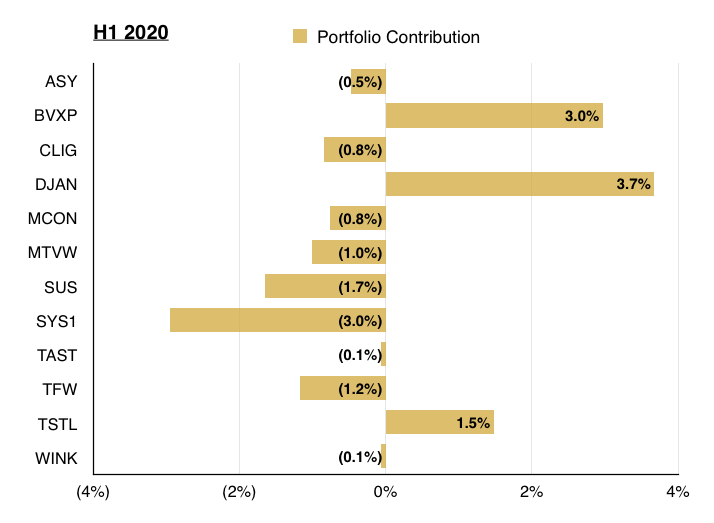

This chart shows each holding’s contribution towards my overall 0.9% loss:

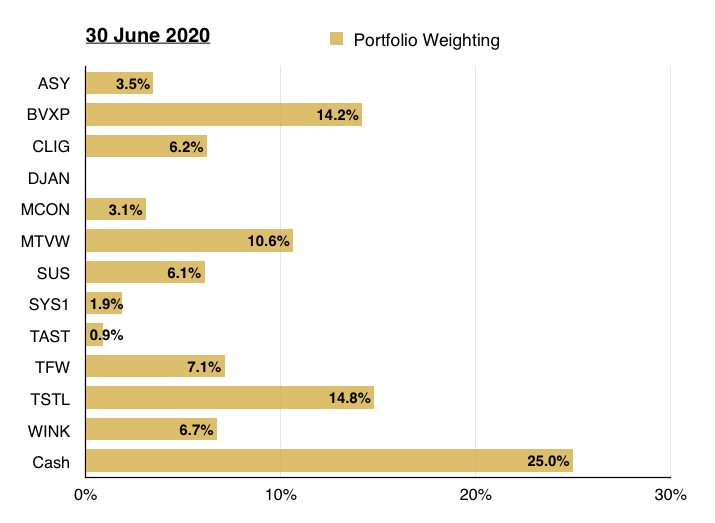

And this chart shows my portfolio’s holdings and their weightings at the end of Q2:

10 lessons from a 10-bagger

I am tempting fate with what follows next.

I have invested for more than 25 years, and my portfolio always seems to fall apart whenever I write about owning a big share winner.

This phenomenon could be due to investment success often leading to overconfidence, complacency and eventually bad decisions. Or perhaps the market gods simply dislike acts of boasting and self-importance.

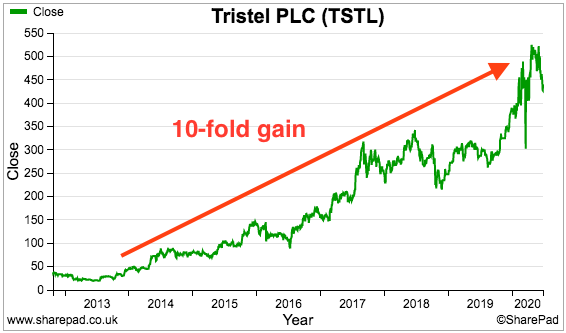

I trust I will not upset the market gods with this write-up. Yes, the share has rallied 10-fold, but the gains came with plenty of luck and my portfolio has endured a few nightmares during the same time. I simply want to recap the lessons to help us all find more big winners.

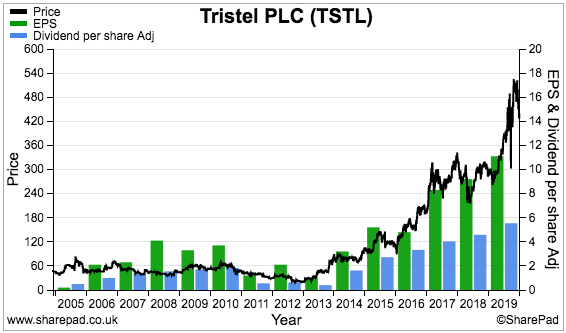

The 10-bagger in question is Tristel, the manufacturer of high-level disinfectants.

I first bought Tristel shares on 17 December 2013 at 42p and bought on several further occasions until April 2014. I paid as much as 49p and my average purchase price was 46p including all costs. I have never bought any Tristel shares since.

I explained my Tristel investment within this blog post published during March 2014. I have since published 18 blog posts covering Tristel’s results and company meetings, so no hindsight is involved. The share price now is 420p and has been as high as 520p.

I trust these 10 lessons can help you find — and keep hold of — your own 10-bagger:

1) You may have to do your own research and read the daily RNS to find the best buying opportunities

I did not discover Tristel from a discussion board, social media or investment magazine.

The company instead first appeared on my radar after reading the daily RNS. Skimming stock-exchange announcements for unfamiliar shares and intriguing statements can occasionally unearth compelling opportunities.

The Tristel RNS that caught my eye was an AGM statement published on 10 December 2013. Here is the full text:

“At the meeting Paul Swinney, Chief Executive Officer, will provide shareholders with the following update:

“I am very pleased to report that the strong trading highlighted at the time of our preliminary results has continued.

In relation to the six months ending 31 December 2013, unaudited revenues are expected to be in excess of £6 million, which is 36% ahead of the same period last year. We expect unaudited pre-tax profit to be no less than £0.6 million for the period, compared to adjusted pre-tax profit of £0.5 million for the full year ended 30 June 2013 and adjusted pre-tax loss of £0.6 million for the same period last year. As a result we are confident that our full year results for the year ending 30 June 2014 will be ahead of current market expectations.

The growth has come from all areas of the business, both within the UK and overseas. We have seen a significant increase in sales of the Tristel Wipes System globally, the Crystel clean room product range has shown encouraging performance and is now contributing to Group profit, and we are seeing the impact of our restructured cost base. We believe that the pattern of growth will continue in the second half.”

I calculated pre-tax profit was running at £1.7m a year, which I believed would support a P/E of about 12 given the then £16m market cap.

The 12x multiple looked very modest for a business with 36% sales growth and upbeat management expectations. The valuation and commentary were enough to prompt further research.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

2) You will probably have to study companies with imperfect histories and small market caps

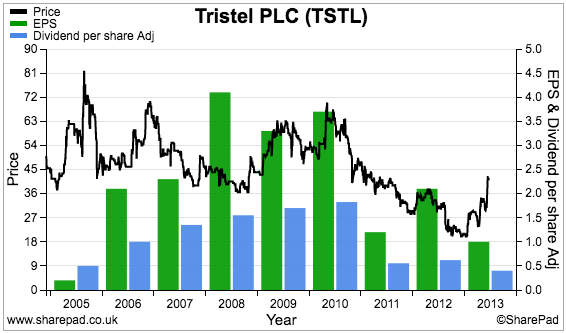

Tristel did not exhibit obvious ‘quality’ at the time of my purchase. The company floated during 2005 and hit trouble a few years later:

| Year to 30 June | 2009 | 2010 | 2011 | 2012 | 2013 |

| Revenue (£k) | 6,847 | 8,764 | 9,287 | 10,939 | 10,558 |

| Operating profit (£k) | 1,283 | 1,504 | 522 | 757 | 493 |

| Other items (£k) | - | 233 | - | (174) | (2,231) |

| Net finance income (£k) | 2 | (13) | (16) | (6) | (14) |

| Pre-tax profit (£k) | 1,285 | 1,724 | 508 | 578 | (1,750) |

| Earnings per share (p) | 3.42 | 3.84 | 1.27 | 1.77 | (3.16) |

| Dividend per share (p) | 1.70 | 1.83 | 0.56 | 0.62 | 0.40 |

Extra investment in cleanroom facilities and overseas operations knocked both earnings and the dividend during 2011. The haphazard performance continued into 2012 and 2013, as demand for certain legacy products collapsed and a manufacturing agreement was terminated.

The absence of a reliable track record was reflected by the lowly £16m valuation — too small for most investors to bother with… which created the upside potential for anyone enterprising enough to look beyond the shaky headline numbers.

3) You will almost certainly require companies that have a quality product

Tristel did not deliver 10-fold returns just because the shares were cheap. The business had to deliver decent profit growth, and encouraging signs had already been presented within the preceding 2013 results.

The business carried net cash and was still paying a (smaller) dividend, and therefore was not a complete basketcase. The results narrative also contained some very enlightening remarks about the company’s products and potential. This paragraph in particular stood out:

“During the year, over 1.7 million disinfection procedures were undertaken by Tristel’s proprietary wipe in the 27 countries in which it is commercially available. The Wipes System can fairly be described as having become the principal method of decontamination of nasendoscopes, cardiology and ultrasound probes in those markets it has gained a commercial foothold. However, the potential for substantially higher procedure numbers, even in the markets in which the Wipes System is most established, and in those markets where it has only recently been launched, is great.”

I translated all that as follows:

- “disinfection procedures” = healthcare = not obviously cyclical;

- “proprietary” = competitive advantage;

- “27 countries” = can be sold overseas = not limited to the UK;

- “principal method” = market leading;

- “the potential for substantially higher procedure numbers” = growth opportunities.

I also realised Tristel’s disinfectants were repeat-purchase items, so revenue would be relatively predictable as well. The underlying products — despite the headline financials —appeared pretty good to me.

4) You may have to meet management for useful snippets to keep you invested

I have followed Tristel carefully for the last six years. The company has hosted numerous results webinars, City presentations and head-office opens days and I have attended most (if not all) of those events during my time as a shareholder.

Interesting snippets can often be picked up when meeting management. For instance, the directors at the first presentation I attended predicted 17% per annum sales growth and pre-tax margins rising to 15% — none of which was disclosed in the results RNS or the presentation slides.

The Q&A is usually the most enlightening part of any company slideshow.

Tristel’s management has over time batted away all sorts of questions about patents and competition, and as a result I have developed a greater understanding of the products’ inherent strengths. I have in turn become less concerned about short-term growth rates, valuation multiples and the weighting of the investment in my portfolio.

5) You may find a business with a really great product does not require exceptional management

I could have easily foregone this 10-bagger.

I will not recount the full details (you can read them all here), but during 2016 Tristel’s executives and senior managers collected a £1m options windfall following — in my view — the dubious disclosure of trading information and of the option plan itself.

I wrote at the time: “[Tristel’s] past RNS statements have now given me some doubts about the leadership quality of this business”. I sold approximately half of my then holding in response.

Tristel’s directors have since told me they “strongly rebut” the allegations of a lack of disclosure and of them “dipping their fingers into the till”.

Anyway, I also wrote in 2016:

“Why not sell more? Well, Tristel’s medical wipes and its other disinfectants are high-margin products that are used day in, day out in the vast majority of UK hospitals — so the business retains many operating and financial attractions… and may not need superb executives to do quite well.

There is decent overseas expansion potential, too.

And of course, I may be completely wrong about my suspicions about management.

But right now, I feel it’s a shame that Tristel’s boardroom now looks to be of much lower quality than the products the firm is trying to sell.”

Management has since bungled the group’s planned expansion into the United States. What was originally claimed to be a two-year project has since turned into a five-year slog with still no end in sight.

I have nevertheless kept the faith with Tristel — and overlooked the subsequent management mishaps — because I am confident the products are good enough to sell in greater volume no matter who is in charge.

6) You will almost certainly ‘take profits’ on the way up due to portfolio-weighting worries and/or valuation concerns

The best investment problem is deciding when to bank your gains.

Trouble is, top-slicing a share on a 10-bagger journey can appear extremely foolish in hindsight.

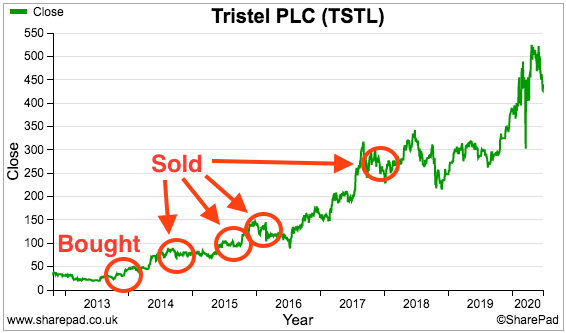

Take my first Tristel sale. I sold 19% of my original stake after six months because the share price had surged from 42p all the way to… 79p. You will never go broke taking a profit, but you will never maximise your profit either.

I top-sliced a further 5% of my original stake during September 2015 at 100p. And I disposed of 44% of my original stake during January/February 2016 at 123p due to a mix of the aforementioned options fiasco and my shareholding growing to represent 20% of my portfolio.

I last top-sliced at 289p during September 2017, when I sold 7% of my original stake due to valuation nerves:

“I calculate the near-term P/E to be close to 30 and the medium-term P/E — using somewhat confident growth projections — to be about 25.”

I should have just held tight.

I currently hold 25% of my original stake and the shares represent 17% of my portfolio. I can’t face calculating what my portfolio would now be worth had I never sold.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

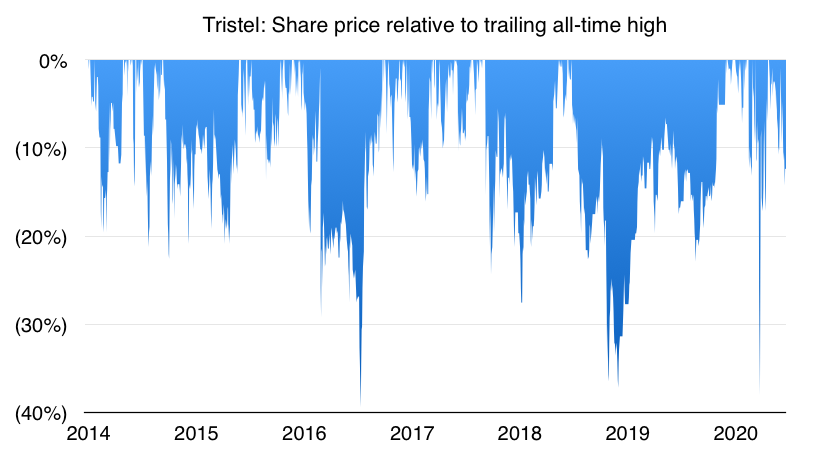

7) Your large paper gains will occasionally shrink as the share price drops significantly

A 10-bagger does not rise in a straight line. Even if you can resist the portfolio-weighting worries and valuation concerns, the share price will experience substantial falls as everybody else frets about the same issues.

The chart below shows Tristel’s share price relative to the trailing all-time high:

On three occasions as a shareholder I have watched the price plunge more than 30% from the trailing high. I have learned prospective 10-bagger investors must keep their nerve when markets turn lower.

I was surprised to discover Tristel’s shares have traded at 10% or more below their trailing high during half of my time as a shareholder. I therefore can’t imagine anyone who follows a ‘momentum’ strategy could have held on for the full 10-bagger outcome.

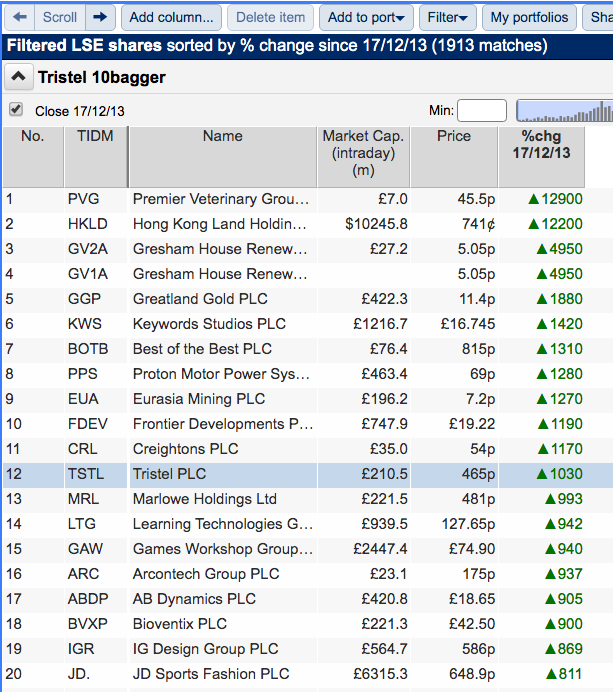

8) You will discover 10-baggers are very rare and you should not correlate the attention given to them to the probability of owning one

You are reading this article because the headline mentioned ‘10-bagger’ and you want to know how you can enjoy 10-fold returns.

Bad news I’m afraid — 10-baggers are extremely rare.

Since I first bought Tristel, only 17 out of 1,358 other UK shares have 10-bagged — and a few of those 17 might be erroneous due to suspect SharePad data:

For further perspective, SharePad shows 27 out of 1,167 shares have 10-bagged over 10 years. The 10-bagger count is 37 out of 831 over 15 years and 41 out of 574 over 20 years.

However, these stats do exclude shares that:

- Once 10-bagged only to fall back;

- Once 10-bagged and were then acquired, or;

- Have 10-bagged since 17 December 2013.

But the stats also exclude all the shares that have sunk without trace — which I suspect evens out the odds.

Tristel is the first 10-bagger I have enjoyed during my 25-plus years of investing. That timescale might tell you something about the likelihood of capturing a 10-bagger for yourself. Those 25 years also explain why I have drawn attention to my Tristel 10-bagger — I do not want to wait until 2045 for the next 10-bagger blog opportunity.

9) You will almost certainly require an elevated P/E rerating as other investors become very optimistic

Earnings growth can only take a share price so far. Tristel’s underlying earnings have tripled during my time as a shareholder — which would have delivered a 3-bagger had other investors not been prepared to pay a higher multiple for those growing profits.

I first bought Tristel when the P/E was approximately 12. Today the trailing multiple exceeds 40. That P/E ‘rerating’ is what really drove the share price to 10-bagger status.

As more investors latched onto Tristel’s progress and recognised the company’s attractions, the valuation has become ever more extended. Enjoying a 10-bagger almost always requires other investors to become very optimistic.

I am hopeful the optimism is justified. Covid-19 ought to have generated significant sales of Tristel’s high-level disinfectants, and I am convinced demand will be sustained as hospitals maintain their new disinfection regimes. But that may be wishful thinking.

10) You will need a lot of luck

The pandemic was of course pure luck for Tristel shareholders — nobody foresaw Covid-19 six months ago let alone when I invested six years ago.

In fact I never dared think the shares would ever get close to 500p and a P/E of 40-plus. My Buy report instead hoped for 100p before 2017.

I was also lucky to read that RNS back in 2013 and fortunate enough to recognise the attractions of the products. I could also attend the company presentations in central London — an option not available to everyone.

I could have easily sold out entirely during 2016, or exited the share on valuation grounds during the following few years. Somehow I stayed in — and rode one of the market’s very few 10-baggers.

During my time as a Tristel shareholder I have bought disasters such as System1 and Tasty and bought other shares that have gone nowhere. My portfolio performance during the same six years has been very average despite owning a 10-bagger. I am therefore not an ace stock-picker and can only conclude luck must have played a significant role.

Let me round off by wishing you the best of luck with finding your own 10-bagger. In the meantime I have my fingers crossed that this write-up has not upset the market gods.

Until next time, I wish you safe and healthy investing.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Great story, Maynard. Very helpful analysis of a unusual set of circumstances. Would you also say that a very important part of being involved in a ten-bagger is your entry-point?

Hello Mark,

Yes, the price you pay is important. I bought at a modest P/E and that multiple has been re-rated much higher as other investors latched onto the unfolding story. This ‘multiple expansion’ combined with earnings growth is what creates the big share winners.

Maynard

Great to read of your buying success here with your first 10 bagger. I’ve been investing for around 20 years and have been fortunate to see 3 10 baggers – GAW, FOUR and FENR (now taken over). Admittedly I have a more diversified portfolio than you.

My experience agrees with yours in terms of having faith and holding them through significant downturns. For the instance of FOUR my trading history shows that when I had automated stop losses my original holding sold out. Thankfully I bought back in then top sliced c.50% early in the rise in price. Had I held that other 50% I would see an exceptionally nice size holding.

I’ve been in and out of GAW a couple of times over the last decade. The rapid climb in recent years is due to new strategy and a rerating of the P/E, as you’ve experienced. Also looking at the sudden market downturn in March this year you could pick them up for less than 50% of the price they are today!

Hello Steven

Thanks for the comment. Funnily enough I owned GAW between 1998 and 2007, and lost patience with the business that at the time was going nowhere: https://knowledge.sharescope.co.uk/2019/01/30/screening-for-my-next-long-term-winner-games-workshop/ My original £8 purchase would now be a c10-bagger. I sold out of LSE in 2007 having bought a few years earlier under £4 — now a 20-bagger. Oh well. I think looking back at your larger portfolio winners, how you found them and why you held on can be helpful to find and hold other winners.

Maynard

I enjoyed reading your piece on 10-baggers. I’ve been investing as long as you and have had my share of them over the years but I differ from you in that I don’t take continual profits ever, on anything, so as a result I have had a few turkeys as well. I think that you can’t predict which stock is going to be a 10-bagger or a turkey, a frightening prospect maybe! I let the market relieve me of stocks through take-overs etc. I like to keep pretty much everything I’ve bought to teach me a continual lesson that I’m involved in a very risky hobby! My “Money Making Hobby” as I call it has made me financially comfortable over the years but I’m not really sure if not doing any profit taking as benefited me or not. I think to be successful you just have to keep buying a few young companies. Over time a few will be 10-baggers and a few will be turkeys, you just have to keep your nerve.

KayD

Hello KayD,

Glad you liked the post. Yes, very difficult to tell in advance which shares will do really well. As you say you just have to keep your nerve. Hold a spread of shares and the really big winners ought to offset the prize turkeys and the numerous other shares that just go nowhere. I tend to cull my turkeys but remind myself of the lessons by listing all my past and present holdings here: https://maynardpaton.com/portfolio/#individual-share-returns I am not sure either whether profit-taking has benefited me or not. I am now looking for the ‘next Tristel’ :-)

Maynard

Interesting article as I have recently been reflecting upon the lessons to be learnt from my own investing experience which I hope will make at least mildly interesting reading for some. I primarily started investing circa 2007, with a bit of dabbling before that from about 2000. In that time I have made some very stupid and costly investments and have on three occasions seen the largest holding in my portfolio fall off a cliff. These being Telewest (a very early mistake which halved my Sipp fund), RBS and TSCO. In addition to these disasters, I’ve also lost significant sums in total wipe outs Monitise and CLLN. Yet despite the major mishaps, my long term investing record is one of substantial profitability. For this I have to thank 3 ten baggers and a few 3-6 baggers within my portfolio. Amazingly the profit from the best of my ten baggers is greater than the sum of all the losses for the 5 shares mentioned above, despite my investment in that share to date being a tiny fraction of what I put into the 5 loss makers. One obvious lesson for me is clearly not to invest a large proportion of my capital in supposedly safe trendy large caps of the day, as both RBS and TSCO were when I bought them. However on current valuations there is a strong argument for saying that these are nowhere near the most expensive investing mistakes I’ve made. For that we have to look at what I should not have sold.

First I have to explain that I’m very much a buy and hold investor and that in a typical year my sales are primarily determined by the need to take advantage of the Capital Gains tax allowance, with the odd speculative sale occurring in my ISA or pension. So 3-4 sales a year are quite typical.

The sells I wish I hadn’t made all relate to the ten baggers, which are AMZN, DNLM and LGEN. In the case of AMZN I sold 40% of my holding at a point when that 40% equalled slightly more than I’d paid for the whole tranche. At the time I’d read several articles by respected “expert” analysts pointing out that the company had never made a profit, didn’t look like doing so for the foreseeable future, that the CEO didn’t care about doing so and that the share was crazily overpriced. The sale made it a risk free investment as I’d already banked a profit regardless of what happened to the remaining 60%. Of course, AMZN is now a twenty bagger and I’d be sleeping very soundly indeed if I’d only retained that other 40%. It’s a similar storey with DNLM, which I purchased on the basis of a shopping trip to one of their stores. I loved what they were doing, they floated and the price dropped soon after, so I bought some. The price more than doubled, but they were still quite a small newly floated risky company and I sold half the shares to bank a profit. The half I kept is now a big holding, but the other 50% along with a string special dividends would have made it my biggest and most profitable holding. With LGEN I have less regret as it wasn’t a company I was attracted to, I simply took a gamble based on price. At the bottom of the banking crisis, it dropped to 25p. At that price I could buy a whole lot of shares for little money and so I did. I just thought they were being punished as if they were a bank and they weren’t a bank. It’s the only time in my life that I’ve traded rather than invested in a share. I think I sold at 40p, bought back at 35p, sold again at 65p bought back at 50p and so on up to roughly 135p. After that I held on for a while, but then started pairing back. The price however, carried on rising for a long time until recently and all along has paid out generous dividends. Despite the huge rises in my AMZN and DNLM shares, I’ve actually made more on LGEN due to the trading profits and high dividends in addition to ten bagging.

I think the lessons I need to learn about ten baggers are:-

1. Don’t play safe with your winners, just run them until you are fabulously rich before selling some.

2. If you want to sleep at night, sell your big losers. After all, they are the source of your nightmares.

3. Sod rebalancing your shares, they are the gambling part of my portfolio. Rebalancing is a great idea and you should do it on your Funds, ETFs, Investment Trusts and Bond Funds.

4. Don’t pay too much attention to expert analysts.

5. Don’t buy safe large cap shares, keep the safeguarding to pooled investments.

These are hopefully lessons for my ten baggers to come. Hopefully one of SMT, EXPN, HRI or AJB will make it there one day.

Hello Kelvin,

Thanks very much for taking the time to recount your investments. More than mildly interesting, at least to me. Some blasts from the past there. I too remember when RBS etc were popular.

“Amazingly the profit from the best of my ten baggers is greater than the sum of all the losses for the 5 shares mentioned above, despite my investment in that share to date being a tiny fraction of what I put into the 5 loss makers”

Starting to see a pattern here with other investors — hold a spread of shares and the really big winners ought to offset the losers and the numerous other shares that just go nowhere.

Have to agree with your 5 lessons, although no2 can be a source of big winners if they recover! No4 goes without saying :-) I have my fingers crossed for your next 10-bagger!

Maynard

No shame in selling at 30x (re your last sale in 2017).

True.

Thank you for a very interesting article. I would have had a 10 bagger in Boo if I had not sold in March. I have only been properly investing for about 6 years.

There is a very interesting, quite old, post on Micro Cap Club which maybe of interest entitled “Conviction to Hold”

https://microcapclub.com/2014/08/the-conviction-to-hold/

And a very recent post from John Huber at Saber Capital on coffee can investing:

http://sabercapitalmgt.com/the-coffee-can-edge/

Kind regards

Michael

Hello Michael,

Thanks for the comment. Bad luck with BOO, although I am not sure whether the price is now back to where you sold.

Not a criticism of you, but many blogs talk of the theory but few blogs give actual real-life stories of holding multibaggers or using a coffee-can approach or whatever. I do wonder in particular whether Mr Cassel has ever owned a stock. He has never publicly declared a shareholding as far as I know.

Maynard

Agreed!

There seems to be this perception amongst certain people that having these 10-baggers is easy. Reading the likes of Cassell, it seems if you’re not finding these investments, then you’re not doing enough work, or you are not thinking in a long enough time horizon.

I think these opinions are clearly nonsense for a number of reasons.

Firstly, the number of shares that go up 10x over a period of let’s say 10 years is very small. In the entire universe of shares you’re looking at, only a very low single digit percentage of all shares achieve 10x. So from the outset, you’ve got to identify that small group of shares that could out-perform, a task in of itself that is not trivial.

If that wasn’t hard enough, not only have you to identify the shares that will go up 10x, but you also need to buy them at a price which will generate that return. Usually, this means buying at an early stage. 10 baggers by their nature are explosive, so that period can be very narrow.

To make it even more difficult, not only do you need to identify the shares, identify the right price to buy at, but you also need to hold for several years. This sounds trivial, until you consider that the average share is held for about 8-9 months (US statistic, I am sure the UK is similar).

So not only does the average investor need to be in the right place, at the right time, they also need to go completely against all their instinct and sit on their investment for several years to get their desired outcome. Seems clear enough to me that while 10-baggers can certainly happen, they are rare events to occur within an arbitrary 10-year time-frame.

Hello Sean,

Many thanks for the eloquent comment. Agree with everything you have written. The ‘holding on’ is probably the hardest part, at least for me. I thought I was the only one who was suspicious of Mr Cassel!

Maynard

I have had a few multibaggers on the hook but let go very early on much for the same reasons.

I bought Victoria Carpets in 2012 or so when Geoff Wilding came into the mix as it was trading at a discount to NAV, and then sold when it got to what I thought was fair value based on what I knew, making around 60-70% or so. I then watched as the stock went up 20x from my entry price, all on momentum with little foundation in fundamentals. It has since come back down to earth but probably has further to fall. I don’t categorise that as a mistake, it was a valuation-driven call.

Next in 2015/6 I sold Games Workshop at around £8 having made 70% or so, because I thought the business was too reliant on Tom Kirby and Kevin Rountree struck me as an ops person. It has gone up more than 20x from my entry price too. Everything that anyone now says is ‘obvious’ about GAW, eg their franchise etc, was well known then but there was no growth, an ever-present threat of displacement by video games, a history of Warhammer coming in and out of fashion, and several years of difficulty with their stores. No one knew anything about Rountree. My mistake was probably to have ignored it once I sold and not engaged my brain on Kevin Rountree’s business plan, which he articulated very well in the [2016 I think] annual report.

Most recently, Air Partner. A company I knew enough about. I had a very long, hard look at it at 15p or so in March, frantically trying to get more info out of the company about its liquidity, and also whilst I knew they may do well out of repatriation and charter work, I wasn’t sure about that and I knew the rest of their business would suffer in the short term and they had very little liquidity. So I passed, knowing that if they could remain cash positive the share price would rebound heavily. And it did – to 100p in the space of a few months for almost 7x.

So, my experience too is that it is immensely difficult to both find and fully harvest these stocks.

Thanks Jerry.

A picture is emerging about 10-baggers from these comments — not easy to find them and then hold on. London Stock Exchange and Burford Capital are among the mega-baggers that I alighted from too early.

Games Workshop, too. My history with the share is outlined here: https://knowledge.sharescope.co.uk/2019/01/30/screening-for-my-next-long-term-winner-games-workshop/

Have to agree with this:

“Everything that anyone now says is ‘obvious’ about GAW, eg their franchise etc, was well known then but there was no growth, an ever-present threat of displacement by video games, a history of Warhammer coming in and out of fashion, and several years of difficulty with their stores. No one knew anything about Rountree.”

I do think a lot of GAW shareholders have confused luck with skill. Business went nowhere for 15 years and then suddenly took off. I am sure 99% of investors in the stock have bought in the Rountree era, had no idea about the scale of the turnaround and know absolutely nothing about the games. Sour grapes? Probably. I was indecisive in that SharePad article at £31 at the start of 2019. Shares have tripled since.

Maynard

Maynard

Regarding Burford, hindsight is a wonderful thing, but things could have played out differently and probably will do yet. Woodford sprinkled some magic dust on the share price. But I have read all their annual reports and many of their call transcripts and I have to say I cannot ascertain what their true investment returns are, whether these are repeatable, how much cash they are likely to generate and most importantly whether management is honest. I don’t have the time of day for many short sellers, but I do rate Muddy Waters and they have written some compelling analysis on Burford.

Best regards

Hello Jerry

Yes, I had expected BUR to rise to perhaps only £2… and not £20. I was already confused during early 2015 at <140p: https://maynardpaton.com/2015/01/23/burford-capital-im-projecting-9-1-annualised-returns-to-2019/ That it was left to a US fund (Muddy Waters) to highlight the issues is a sad reflection of UK fund managers, brokers and analysts.

Maynard

That was an early spot re Burford, Maynard.

I enjoyed this post about multi-baggers because I think it is such a worthwhile use of one’s time to try to find these. Finding a handful over an investing lifetime makes the difference. It’s very difficult to do, eg spotting the stub equity that will survive and re-rate to its previous valuation or finding the best business in a nascent market. Difficult but worthwhile trying.

Thanks Jerry. I do think having a ‘this may one day become a 10-bagger’ mentality helps with the motivation for stock-picking.

Maynard

Maynard and all,

Thanks for the very interesting post and subsequent comments. Sorry for the late entry, but I have just seen the thread. I invested up until c. 2002 (who can forget Eidos!) and then work restrictions prevented me until about 8 years ago.

A recent 10 bagger was FeverTree, which I bough for 2.10 in Jan 15. I knew the business well even before it floated. While I liked the model, management team etc.. I thought it so over valued that I only bought 50% of my normal unit of investment (Doh!). I sold reasonable proportions at £6.32 and £23.10, but was not clever enough to sell at £40. Its valuation has always been somewheter between daft and ludicrous (even now it is on a PE of 61). I retain a stake.

Some buy and hold everything. I tend to sell when I think I have got it wrong. I don’t have time to track more than 6 or 7 stocks properly (and looking at the failures pains me). Duds include Velocity (I should have worked out it was operationaly geared/capital intensive) and Hayward Tyler, now part of Avingtrans, (I should have worked out, I would never understand it properly).

I was interested in the management thought: the business should perform even if run by the incompetent (very Peter Lynch or Buffet). These businesses are very rare. I now much prefer to see senior executives or the chair with a meaningful shareholding (3% plus) and a track record with the business.

A related point is size. Obviously this helps 10 baggers, but I am wary below an EV of less than £40m (profits of c. £4/5m). In my experience, management and operational quality of smaller businesses can be terrible. Even at my threshold, it can be very poor.

Noted re big international markets. Also, it is helpful if the product is high volume and simple to understand a wipe (Tristel), a mixer (FeverTree) or a power supply (XP Power – a more successful investment).

I doubt I will have many 10 baggers. I am too risk adverse (re size, managment, track record etc..). Constantly trying to improve the understanding of a business probably allows better decisions re selling or holding. I must try to get to more AGMs!

MTIOC