07 November 2019

By Maynard Paton

Results summary for Tasty (TAST):

- Woeful figures showed weaker revenue and greater losses — with the excuses this time including Brexit rather than unfavourable weather and the World Cup.

- A £3m equity placing has shored up the balance sheet, while an absence of further write-offs and utilised provisions lends support to turnaround hopes.

- This year’s Christmas performance is crucial, with TAST going all out to capture festive-party bookings. Management’s outlook remarks seemed encouraging.

- Poor Christmas trade causing further cash flow traumas could leave TAST no option but to de-list.

- The market cap is £4.1m for sales of £45m from 57 restaurants. I continue to bravely/stupidly hold.

Contents

- Event link and share data

- Why I own TAST

- Results summary

- Revenue and losses

- Glimmer update

- Cash flow and balance sheet

- Christmas Focus

- Valuation and outlook

Event link and share data

Event: Interim results for the 26 weeks to 30 June 2019 published 24 September 2019

Price: 2.9p

Shares in issue: 141,089,758

Market capitalisation: £4.1m

Why I own TAST

- Experienced family management has already built and sold two quoted restaurant chains for £200m-plus (ASK Central and Prezzo).

- Bombed-out share price may provide substantial upside if cash generation can improve to stave off bankruptcy or de-listing.

- Just too late to sell. TAST now represents just 1% of my portfolio, with the investment already losing more than 80% of its value.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary

Revenue and losses

- These interim figures were always going to be woeful — but in fact were worse than I had anticipated.

- Annual results published during March had admitted “the uncertainty of Brexit has meant that 2019 has started slowly.”

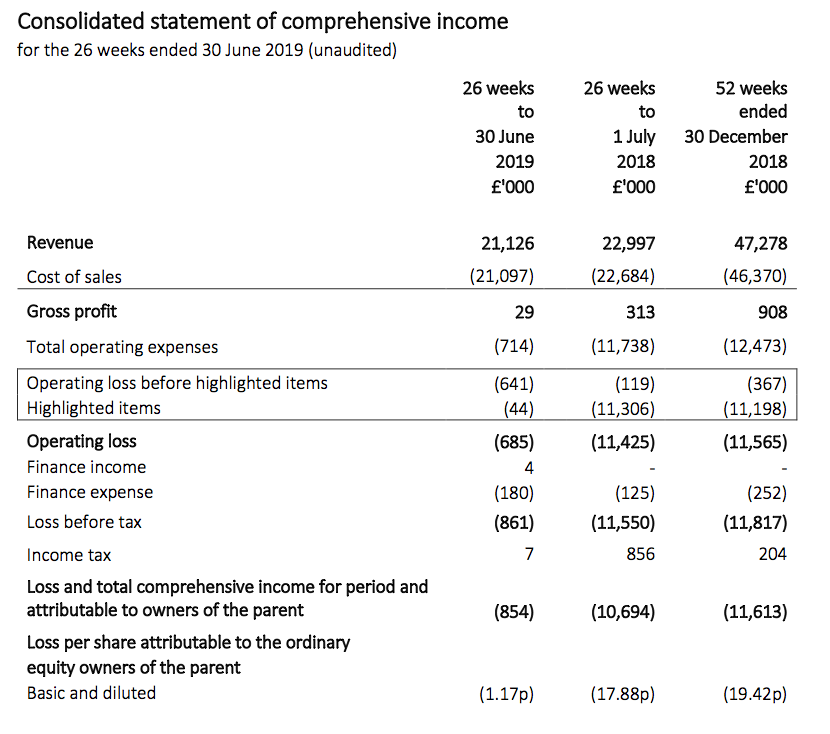

- Sure enough, first half revenue dropped 8% to £21.1m while operating losses before various items widened to £658k:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | |||

| Revenue (£k) | 24,375 | 25,934 | 22,997 | 24,281 | 21,126 | ||

| Gross profit (£k) | 893 | 1,014 | 313 | 595 | 29 | ||

| Operating profit*(£k) | 494 | 607 | (184) | (294) | (658) | ||

| Gross margin (%) | 3.7 | 3.9 | 1.4 | 2.5 | 0.1 | ||

| Operating margin* (%) | 2.0 | 2.3 | (0.8) | (1.2) | (3.1) |

(*before pre-opening costs, property disposals and various write-offs)

- Bear in mind that the first-half industry conditions of 2018 were at the time described by TAST as “challenging and [had] been exacerbated by unfavourable weather conditions and the World Cup”

- Despite a lack of heavy snow, heatwaves and major sports events during this half, revenue per restaurant dropped by an estimated 3% to £722k:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | |||

| Revenue (£k) | 24,375 | 25,934 | 22,997 | 24,281 | 21,126 | ||

| Average number of units | 63 | 64.5 | 62 | 60 | 58.5 | ||

| Average revenue per unit (£k) | 774 | 804 | 742 | 809 | 722 |

- Revenue of £722k per restaurant compares to £839k for H1 2016, £874k for H1 2015 and £920k for H1 2014.

- The statement revealed TAST’s estate includes non-trading sites, one of which was sublet during the half and the other sublet afterwards.

- If every site was in fact trading during the comparative H1 2018, then perhaps revenue per trading site during this H1 2019 was maintained around the £740k level.

- TAST’s fundamental problem remains as before — operating a number of under-performing restaurants due to a mix of:

- fierce competition;

- regular discounting;

- greater costs, and;

- hit-and-miss menus.

- These results said: “Our focus is on optimising the current estate and turning around under-performing sites.”

- TAST has referred to “turning around under-performing sites” (or similar) ever since the company first owned up to major trouble during March 2017.

- However, not every restaurant business is suffering at present.

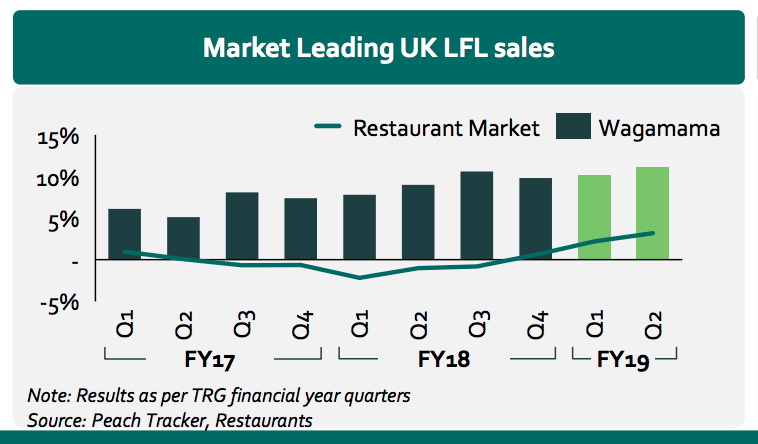

- Interim results from Restaurant Group showed its Wagamama subsidiary delivering wonderful c10% like-for-like sales growth:

- Restaurant Group as a whole reported 3.7% like-for-like sales growth during H1 2019.

- So people are still dining out — just not so much at TAST’s Wildwood restaurants.

Glimmer update

- TAST’s second-half performance of 2018 had displayed three glimmers of hope:

- Improved revenue per restaurant;

- An improved gross margin, and;

- Minimal write offs.

- The first two of those glimmers have been extinguished — at least for now.

- But the glimmer of minimal write-offs remains:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | |||

| Profit on disposal (£k) | - | 1,237 | 1,942 | 190 | (27) | ||

| Onerous leases (£k) | - | (1,635) | (1,688) | 1 | - | ||

| Lease impairment (£k) | (172) | 76 | (890) | (7) | - | ||

| Asset impairment (£k) | (9,320) | (142) | (10,294) | 231 | - | ||

| Goodwill impairment (£k) | - | - | - | (115) | - | ||

| Restructure (£k) | - | - | - | (457) | - |

- Wishful thinking perhaps, but the absence of major exceptional items during the past twelve months might indicate trading has now stabilised.

- Write-offs, impairments and provisions totalled a negative £3.9m during 2016, a negative £11.2m during 2017 and a negative £12.6m during 2018.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Cash flow and balance sheet

- The half-year saw TAST’s balance sheet shored up by the £3m raised through a rescue equity placing.

- The proceeds went towards reducing debt by £4.6m.

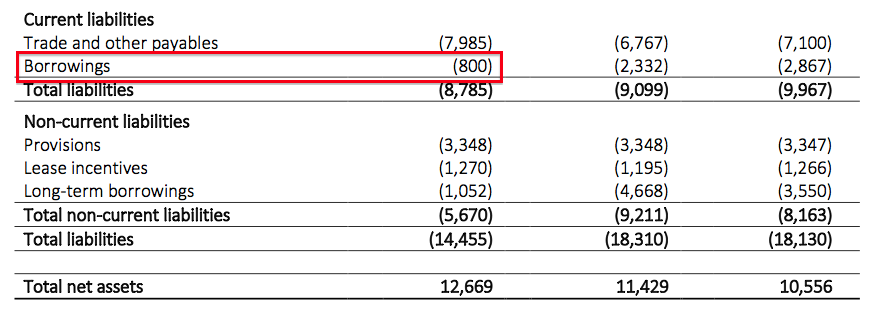

- At this half-year (and following the placing), cash was £2.4m and debt was £1.9m to leave net cash at £0.5m.

- Free cash flow during the half was a negative £863k, meaning a positive £1,093k was produced during the past twelve months:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | |||

| Cash generated from operations (£k) | 1,075 | 1,710 | (2,259) | 2,648 | (460) | ||

| Tax received (£k) | - | - | - | 26 | - | ||

| Capital expenditure (£k) | (4,414) | (2,338) | (670) | (591) | (227) | ||

| Net interest paid (£k) | (125) | (77) | (125) | (127) | (176) | ||

| Free cash flow (£k) | (3,464) | (705) | (3,054) | 1,956 | (863) |

- Debt of £800k is due to be repaid by June 2020, which should be covered — just — by a repeat of that twelve-month £1,093k free cash flow:

- Future free cash flow should be bolstered by much lower interest payments (last reported at £303k a year) following a £4.6m repayment of debt.

- The 2018 annual report states interest payable on debt from July 2019 is between 2.5% and 4% over LIBOR.

- Assuming 6% interest, interest payable on the remaining debt of £1.9m would be £114k a year.

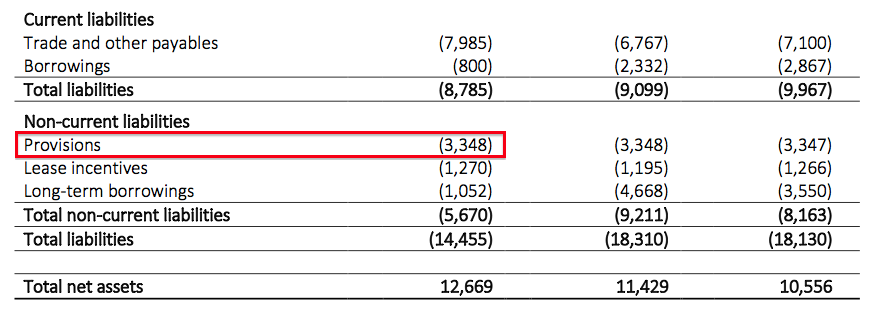

- A lingering issue concerns provisions of £3.3m:

- The 2018 annual report states:

“During the period a provision for onerous leases was made of £1,687,000 (2017 – £1,625,000). This provision has been made against sites where projected future trading income is insufficient to cover the unavoidable costs under the lease. The provision is based on the expected cash out flows of these sites and the associated costs of exiting these leases. The provision covers a three year period and it is expected the majority of the provision will be utilised over the next 24 months.”

- TAST essentially took a £1.7m charge during H1 2018 and a £1.6m charge during H2 2017 as its best guess of the cash expenditure required to jettison loss-making restaurants.

- In other words, cash of up to £3.3m could be needed during the next few years to exit problem leases.

- Eighteeen months have now passed since the first £1.6m provision, and no part of that provision (or the subsequent £1.7m provision) has been utilised (i.e. the associated cash expenditure has yet to occur).

- More wishful thinking perhaps, but TAST may have ‘over provisioned’ — and the predicted costs of exiting problem leases might not be as great as originally forecast.

- The results statement did say: “We have generally found landlords to be co-operative and supportive and our collaborative approach has been well received. We have been successful in achieving rent reductions and lease concessions.”

- TAST directors Adam and Sam Kaye — and their wider family — do own a number of sites occupied by TAST, and may have co-operated as landlords, too.

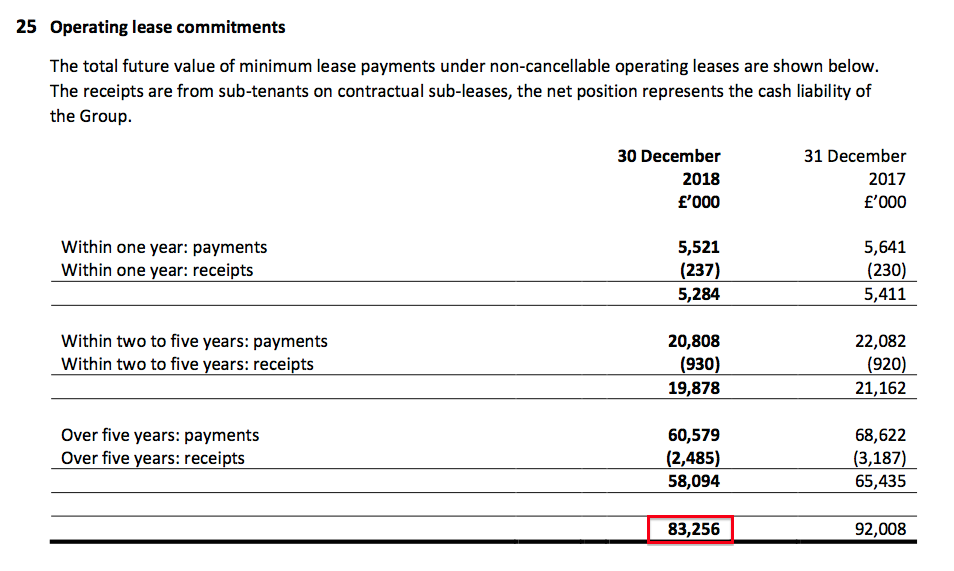

- As a reminder, the 2018 annual report showed TAST carried long-term lease obligations that totalled £83m:

- Lease obligations for 2019 of £5.3m suggest TAST’s average lease length could be 15 years.

Christmas Focus

- Management has made small changes to its turnaround plan.

- “Rationalise the estate” has become “optimise the estate” — suggesting further site disposals may not be forthcoming.

- “Streamline our structure” has been removed — suggesting the streamlining has been completed.

- “Christmas Focus” has been introduced, and Christmas appears crucial to TAST’s survival.

- The results said: “The Group is traditionally weighted to the second half, with December being the most important month of the year, which will significantly dictate the Group’s overall performance.”

- TAST started Christmas planning in August: “We published our Christmas menus online at the end of August… and have already started taking bookings. We have established a dedicated team to handle reservations, all enquiries and marketing initiatives and are well prepared to maximise revenue over the festive period.”

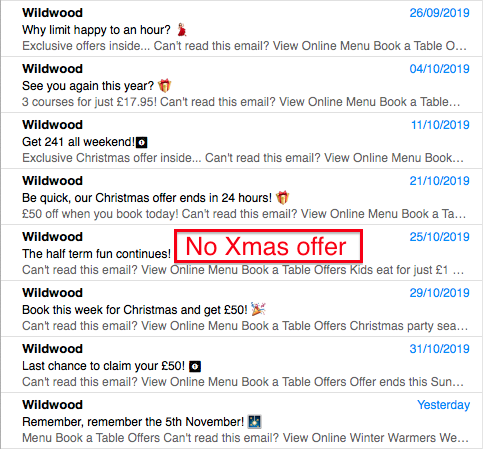

- TAST has certainly increased its promotional Christmas email activity this year.

- Christmas email promotions started in September, and seven of the eight emails sent have included a special Christmas offer for group bookings:

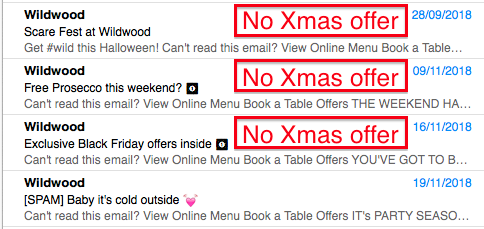

- In contrast, the same period during 2018 saw just four promotional emails — of which only one mentioned Christmas:

- Unlike last year, TAST has this year published a special Christmas menu:

- Host your festive party with TAST on or before 28 November, and you pay £17.95 per person for three courses (£19.95 per person from 29 November).

- Helping cash flow is the £5 per person festive-party deposit requirement, and the option to pre-order £2 per person party packs.

- Main-menu changes implemented this month include introducing turkey burgers, roast turkey, a ‘winter’ pizza (which includes turkey) and roasted turkey penne.

- Main-menu dishes disappearing include the four cheese arancini, the smokey BBQ ribs and the grilled asparagus:

- All told, 18 new dishes were introduced to the Wildwood menu this month, compared with 13 during April 2019, nine during October 2018 and twelve during July 2018.

- If nothing else, management remains keen on experimenting with new dishes.

- Mind you, a stable, winning menu has sadly yet to be created.

- Perhaps importantly, the pricing of almost all the maintained menu items has not changed during the latest refresh.

- Menu pricing is somewhat arbitrary anyway. Promotions of 40%-off-your-food-bill, two-for-one-on-main-meals and kids-eat-for-£1 have been regular this year.

Valuation and outlook

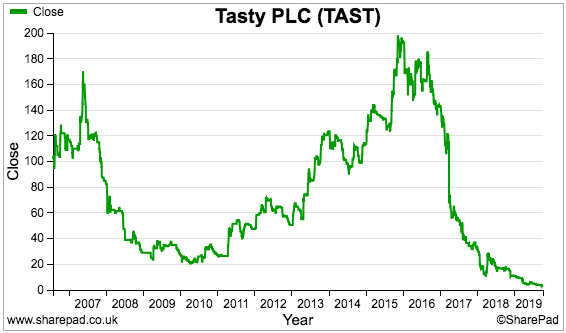

- The recent 2.9p share price supports a £4.1m market cap.

- To reiterate how badly TAST has fared, the group reported a £4.1m operating profit during 2016.

- The £4.1m market cap compares to trailing revenue of £45m and a net book value of £13m.

- The estate currently comprises 51 Wildwood restaurants and 6 dim-t restaurants. Each site is therefore valued at £4.1m / 57 = £72k.

- For comparison, three sites were disposed of during this half year for cash proceeds of £523k.

- Buoyed perhaps by the early Christmas bookings, TAST’s outlook for the rest of 2019 did not appear terminal: “The refreshed Wildwood and dim t offerings continue to be attractive to consumers, with encouraging trading in the first few weeks of the second half… [The] Board currently expects adjusted EBITDA performance for the full year to remain in-line with expectations.”

- However, the results outlook was issued in September — well before the announcement of the December general election.

- These results referred to “the uncertainty of Brexit”, and further political upheavals would be a useful excuse for Christmas trading not going to plan.

- For now, the immediate bull story boils down to:

- The possibility of upbeat Christmas trading, which should lead to;

- Improved free cash flow, which should lead to;

- Near-term debts being cleared, and;

- Perhaps stronger trading during the first half of 2020;

- Plus, the £3.3m provisioning of problem leases might actually cost a lot less.

- The upside potential from a £4.1m market cap could be substantial should TAST one day achieve a reasonable operating margin on its £45m revenue.

- That said, a poor Christmas leading to further cash flow traumas might well spell the end of this investment.

- Investors may understandably be very reluctant to inject more money into the business following the earlier £3m equity raise.

- Such reluctance could leave the door open for TAST to de-list. Management (and connected parties) control 40% of the shares, and the same individuals voted for Richoux to give up its AIM quotation earlier this year.

- TAST now represents 1% of my portfolio, with the investment already losing more than 80% of its value.

- Selling now seems just too late, and I might as well bravely/stupidly hold on in hope of a recovery.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Tasty.

Stunningly good and thorough analysis, Maynard.

Thanks for all your efforts and for sharing.

Best wishes,

Kevin

Tasty (TAST)

Appointment of Finance Director announced 26 September 2019

Not exactly a big-hitter appointment to the board. TAST had been without a board-level FD since early 2018.

Here is the full text:

———————————————————————————————–

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, is pleased to announce the board appointment of Mayuri Vachhani as Finance Director, with immediate effect.

Mayuri was appointed as non-Board Finance Director to the Company in February 2018. Mayuri has over 20 years’ experience in the restaurant sector and has extensive finance and commercial experience. She has held a number of finance positions at companies including McDonald’s, ASK, Ed’s Easy Diner and Big Easy. Mayuri is a Chartered Accountant, having trained at KPMG.

The directorships and partnerships currently held by Mayuri Vachhani and over the five years preceding the date of appointment are as follows:

Ms Mayuri Kantilal Vachhani, aged 49

Current directorships/partnerships: None

Previous directorships/partnerships: Big Easy Restaurants Limited

Mayuri Vachhani does not hold any ordinary shares in the Company.

———————————————————————————————–

LinkedIn shows Ms Vachhani spending 2 years at Big Easy, 2 years at Ed’s Diners, 2 years at Canteen and 3 years at ASK (years after the Kayes sold out). The CV does not suggest a veteran, proven FD. Big Easy had annual sales of c£20m (and losses) when she left in 2017 — about half the size of TAST’s current sales.

Maynard

Tasty (TAST)

Property Disposal and Trading Update announced 02 January 2020

Phew! TAST is not going bust just yet. A property disposal and in-line Q4 trading has given the restaurant chain more time to turn itself around.

Here is the full text:

——————————————————————————————————

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, is pleased to announce the exchange of contracts for the sale of its dim t More London site for a gross cash consideration of £2 million. This disposal is in line with the Company’s strategy of reducing exposure where it is experiencing increasing property and labour costs and strengthening the Company’s balance sheet.

The More London restaurant produced an EBITDA of £106,000 for the year ended 31 December 2018 and had a net book value of £878,000 as at 30 June 2019.

The sale proceeds, net of associated costs, are expected to amount to approximately £1.95 million and will be applied towards paying off the Company’s remaining bank debt, and to fund the Group’s working capital and selected restaurant refurbishment plans. A further announcement will be made on completion of the sale.

The Company is also pleased to announce that fourth quarter sales to date remain in line with management’s expectations and, with the continued assistance of landlords, the Board remains confident that current market forecasts for the year ended 31 December 2019 will be achieved..

——————————————————————————————————

(Completion of the property disposal was announced on 07 January 2020).

Ebitda for 2018 before a net £11m of ‘highlighted items’ (write-offs, provisions etc) was £1,581k. This More London restaurant therefore produced 6.7% of group Ebitda — suggesting the site was a significant earner for TAST given around 60 other sites operated during the same year.

The £1.95m gross proceeds compare well to the £0.9m book value and the Ebitda figure. Clearly somebody is still buying restaurant sites — although the site sold has a scenic view of Tower Bridge, London, and so is not TAST’s typical provincial high street location.

The disposal follows the sale of two London sites in early 2018 for £4m. TAST now retains just four sites in London: a Wildwood on Bow Street and dim-ts on Charlotte Street (TAST’s head office), Heath Street and Wilton Road. I have been to three of those four outlets and none are as impressive as the Tower Bridge location.

Note that the site sold operated as a dim-t and not a Wildwood. TAST has never said the dim-t format — of which there are now five locations — has suffered major problems. All the difficulties have occurred at the much larger Wildwood format.

I imagine the proceeds will pay off the debt of £800k due by June 2020, which will leave £1m or so of longer-term debt. The half-year results reviewed in the blog post above disclosed cash of £2.4m and trailing 12-month free cash flow of c£1m, so debt — I hope — may no longer be an immediate issue.

“Selected restaurant refurbishment plans” is interesting. Capex in the last H1 was just £227k — split over 57 sites was just £4k each. Many of the sites could therefore look very tired at present. For 2018, the 60 sites each received average capex of £21k.

I am pleased the Christmas party marketing referred to in the blog post above appears to have generated enough bookings to meet Q4 and FY expectations.

The wording of the RNS was odd — referring to “sales to date” when the year end was stated as 31 December (two days before the announcement). Previous year-ends have always been on Sundays, which for 2019 would have been 29 December.

Anyway, the £1.95m disposal proceeds represented 50% of TAST’s pre-announcement £4m market cap… so no wonder the shares have jumped 50% since the news. All told, TAST looks to have bought more time to reinvigorate itself. Let’s see what March’s full-year announcement reveals on the sales per site and cash flow fronts.

Maynard

Thanks Maynard,

I’m still holding some! Fingers crossed for 2020…

Regards

David

Tasty (TAST)

Restaurant Closures and Full Restaurant Closures published 23/24 March 2020

Catching up with Tasty and what seems like ancient history now. The group’s restaurants were all shut in March. Company at the time claimed it had “sufficient financial resources for the foreseeable future“. No news since.

The full text from the March announcements is below:

——————————————————————————————————–

Further to the announcement on 20 March 2020 by the UK Government that, inter alia, all pubs, bars and restaurants are required to close in light of health issues associated with COVID-19, the Company confirms that it has closed all of its 56 restaurants for in-store dining for the foreseeable future. The restaurants will remain closed until the Company receives guidance from the UK Government to the effect that restaurants are permitted to re-open.

In the meantime, the Company is offering takeaway and delivery services, where available, until such time as the Government announces that it is prohibited from doing so or the Company decides that it is not viable to continue the services. In addition, free takeaway meals are currently being offered by the Company to NHS and emergency services staff.

The Company will seek to mitigate the revenue loss by implementing cost-cutting measures such as cessation of capital expenditure and seeking preferential terms from landlords and suppliers as well as relying on Government support for employees’ pay and VAT and business rate holidays. Concurrently, the Company is taking measures to ensure staff retention where possible.

Given the Company’s existing cash position with no debt, the Directors confirm that during the period of shutdown and assuming it is successful in implementing the cost cutting and cash preservation measures referred to above, it has sufficient financial resources for the foreseeable future.

In light of these rapidly changing exceptional events, the Company will make further announcements, as appropriate.

——————————————————————————————————–

——————————————————————————————————–

Further to the announcement made by the Company on 23 March 2020, in light of the further measures announced by the UK Government in relation to COVID-19, the Board has decided to cease offering all takeaway and delivery services, across all of its restaurants. The Company has taken this decision primarily with the welfare of its employees, customers and the wider community in mind.

Even with these full closures, with the cash preservation measures previously announced, the Directors continue to believe that the Company has sufficient financial resources for the foreseeable future.

——————————————————————————————————–

Maynard

Tasty (Tasty)

Restaurant Openings published 26 June 2020

News of some restaurants re-opening. I plan to publish a blog post on Tasty next week:

——————————————————————————————————————————–

Further to the announcements made by the Company on 23 and 24 March 2020, the Company is pleased to announce that it has re-opened seven restaurants (representing approximately 13 per cent. of the estate) for takeaway services only. Over the next few weeks, the Company intends to cautiously open further units for takeaway and/or full table service, in compliance with Government regulations, and by mid-July expects to have some 25 units open for trading.

——————————————————————————————————————————–

Maynard