13 August 2020

By Maynard Paton

Results summary for Mountview Estates (MTVW):

- Standstill 2020 figures that showed 8% more properties sold at prices 9% lower than last year.

- A maintained dividend, a lack for furloughed staff and the directors currently being “happy in the auction room” underline some pandemic-resilient qualities.

- Net debt representing a very modest 8% of the group’s property estate suggests significant scope to pick up any property bargains.

- This week’s AGM witnessed a further bout of protest votes against the independent non-executives, the board’s pay and the auditors.

- MTVW’s book value increased by 3% to a record £97 per share, although my calculations suggest the balance sheet could be worth £200-plus per share. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own MTVW

- Results summary

- Covid-19 and online auctions

- Revenue, profit, dividend and net asset value

- Gross margin

- Allsop valuation

- Financials

- Corporate governance and protest votes

- Valuation

- Grainger comparison

Event links, share data and disclosure

Event: Preliminary results and annual report for the twelve months to 31 March 2020 published 18 June 2020

Price: £109

Shares in issue: 3,899,014

Market capitalisation: £425m

Disclosure: Maynard owns shares in Mountview Estates. This blog post contains SharePad affiliate links.

Why I own MTVW

- Buys, holds and sells regulated-tenancy properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to boast an aggregate 50%/£212m shareholding.

- Simple accounts carry properties at cost, which if sold at their potential ‘reversionary’ values may be worth significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

Covid-19 and online auctions

- MTVW thankfully appears to have escaped the worst of the pandemic.

- MTVW buys and sells residential properties, and I had wondered whether the lockdown — and resultant mothballed housing market — would hamper trading and valuations.

- These results were not affected by Covid-19:

“[T]he trading results for the year ended 31 March 2020 were not influenced by the Covid-19 pandemic and that any influence or effects should be considered as post balance sheet events.”

- As it turns out, trading following the March year-end seems not to have been affected either:

“This keen eye on purchasing has continued into the new financial year, despite Covid-19, and we have been active in auctions, both buying and selling properties at prices that we would have been pleased with at any time in recent years.”

- Similar to many activities at present, property auctions have migrated entirely online:

“Auctions are now all conducted remotely and the auctioneers are becoming more successful at replicating the ballroom atmosphere. So far this financial year we have been happy in the auction room both in terms of sale prices achieved and the prices at which we have been able to make purchases.”

- Housing activity in general has revived quickly, in part due to stamp-duty reductions and lifestyle changes.

- Fellow portfolio holding M Winkworth said the other week:

“This has now been our busiest July in at least the past five years. The changes in stamp duty have turbo-charged the market. Our network is reporting a significant uplift in activity at all price levels, with a focus not only on London and the commuter belt, but also on towns and cities with a longer commute, reflecting the move to a more flexible working landscape.”

- A full complement of employees underlined MTVW’s resilience to the pandemic:

“We have not had to furlough any staff or reduce staff numbers in any other way and I remain confident that our years of financial prudence will enable us to continue to conduct the business successfully and to maintain our dividend payments.”

- MTVW also implied tenants would continue to pay their rent:

“Over 80% of our rents are paid directly into the bank and regulated rents are set at a modest level. Provided tenants pay their rent they have absolute security of tenure and a significant number have help from social services.”

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue, profit, dividend and net asset value

- November’s dull interim results had already suggested these 2020 figures would not be spectacular.

- Brexit “uncertainties” were then cited for the standstill H1 revenue and profit performance.

- This full-year statement cheered the election result:

“Happily on 12 December 2019 Boris Johnson was elected with a big majority that enabled us to leave the European Union on 31 January 2020 but the details of the withdrawal will not be certain until 31 December 2020.”

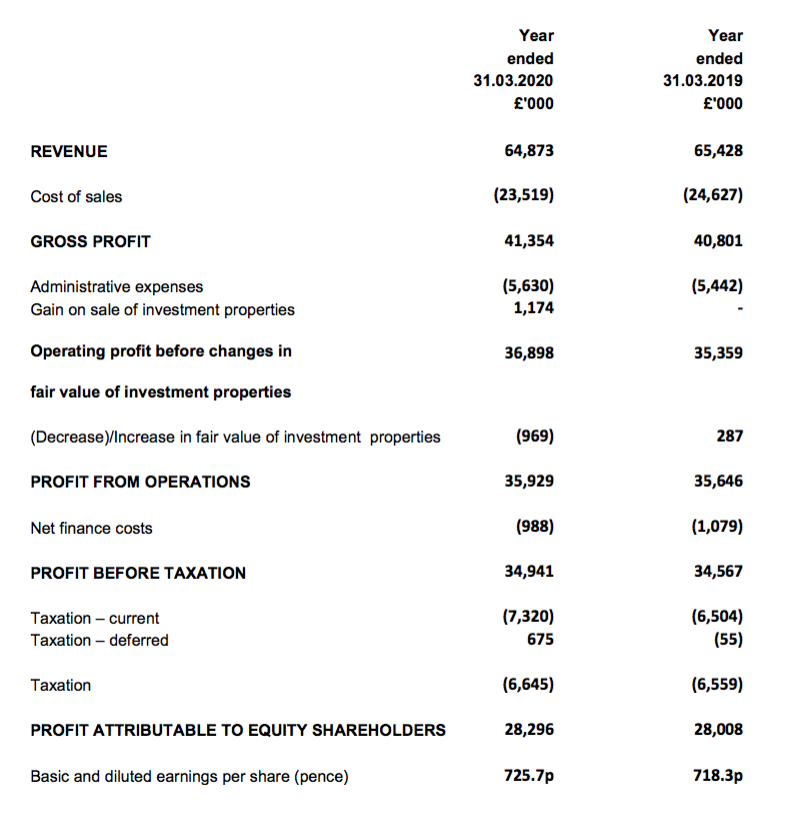

- Revenue fell 1% and operating profit gained 1% after MTVW sold 8% more properties at prices 9% lower than last year:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Net asset value (£k) | 311,752 | 336,279 | 354,462 | 366,874 | 379,574 |

| Net asset value per share (p) | 7,996 | 8,625 | 9,091 | 9,409 | 9,735 |

| Revenue (£k) | 79,765 | 78,232 | 70,272 | 65,428 | 64,873 |

| Gross profit (£k) | 53,014 | 52,056 | 43,357 | 40,801 | 41,354 |

| Operating profit (£k) | 47,866 | 46,825 | 37,850 | 35,359 | 35,724 |

| Net valuation gain (£k) | 1,504 | (1,020) | (376) | 287 | (969) |

| Finance income (£k) | (1,179) | (819) | (714) | (1,079) | (988) |

| Other items (£k) | 197 | - | 145 | - | 1,174 |

| Pre-tax profit (£k) | 48,388 | 44,986 | 36,905 | 34,576 | 34,941 |

| Earnings per share (p) | 993 | 929 | 766 | 718 | 726 |

| Dividend per share (p) | 300 | 300 | 400 | 400 | 400 |

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Gross sales of properties (£k) | 61,442 | 60,154 | 51,840 | 46,430 | 45,651 |

| Properties sold | 209 | 182 | 170 | 154 | 167 |

| Average price (£k) | 294 | 331 | 305 | 301 | 273 |

- Remember that MTVW sells its regulated-tenancy properties only when the tenancy ends — which typically occurs when the tenant has died.

- The number of properties becoming available for sale — and the total proceeds MTVW earns from one set of results to the next — can therefore be unpredictable.

- The 167 properties sold during 2020 compares to an average of 172 per annum during the last ten years, with a low of 137 sold in 2012 and a high of 209 sold in 2016.

- The £273k average sale price reflected a lower number of properties sold for £500k or more:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Sales price range | |||||

| Below £500k | 181 | 152 | 145 | 132 | 151 |

| Between £500k and £1m | 26 | 28 | 22 | 19 | 15 |

| Above £1m | 2 | 2 | 3 | 3 | 1 |

| Total | 203 | 182 | 170 | 154 | 167 |

- Rental income increased 1% to £19m — equivalent to 30% of total revenue and the highest proportion since 2012.

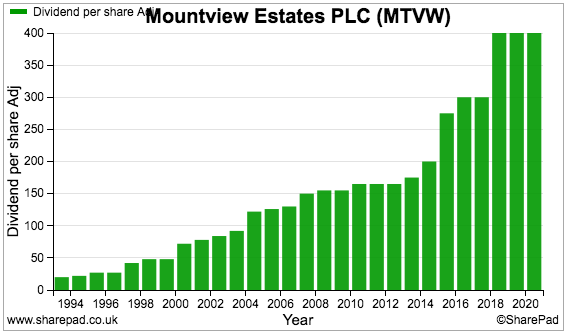

- The dividend was held at 400p per share for the second successive year.

- Documents at Companies House show the dividend has never been cut since at least 1979 — after which the payout has risen 267-fold:

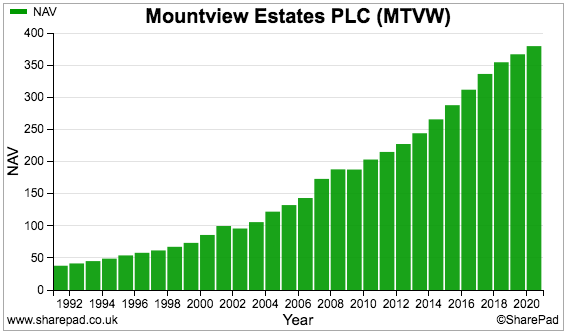

- Net asset value (NAV) improved by £13m to £380m — equivalent to £97.35 per share and a fresh NAV record:

- The 3% NAV advance was the lowest annual percentage gain since NAV dipped slightly during 2009.

- NAV per share growth has slowed over time.

- NAV per share has compounded at a 6% average during the last five years, 7% during the last ten years, 9% during the last 20 years and 10% during the last 30 years.

Gross margin

- MTVW’s balance sheet is dominated by 1,955 regulated-tenancy (and similar) properties that boast an aggregate £315m book value.

- Assured/life tenancy properties plus freehold/leasehold ground rent properties represent a further £77m.

- The group’s properties are held on the balance sheet at their cost price.

- The percentage gain on each property sold is correlated loosely to how long the property has been owned by MTVW — and that gain can vary somewhat in any particular year.

- Management comments at last year’s AGM indicated MTVW liked to purchase regulated-tenancy properties at a 25% discount to the property’s ‘unregulated’ state.

- The table below shows the gross margin achieved from selling properties during the last five years:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Group gross margin (%) | 66.5 | 66.5 | 61.7 | 62.4 | 63.7 |

| Property sales gross margin (%) | 65.8 | 66.3 | 57.9 | 59.1 | 61.3 |

- The 61.3% gross margin for 2020 is equivalent to MTVW selling a property for a 158% gain. MTVW’s five-year average gain is 166% and the ten-year average is 164%.

- Lower house prices can affect the gross margin MTVW enjoys.

- Just before the Brexit vote, MTVW’s gross margin was approximately 65% from property sales (equivalent to 185% gains) — with a record 71% gross margin (245% gain) achieved during the six months to September 2016.

- These 2020 results encouragingly showed the second-half gross margin from property sales at 61.7% (161% gain) — the highest six-monthly figure for three years:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | H2 2020 | |||

| Property sales revenue (£k) | 23,953 | 27,887 | 20,656 | 25,774 | 20,199 | 25,452 | ||

| Property sales gross profit (£k) | 14,297 | 15,721 | 11,706 | 15,571 | 12,271 | 15,694 | ||

| Property sales gross margin (%) | 59.7 | 56.4 | 56.7 | 61.1 | 60.8 | 61.7 |

- I am hopeful this gross-margin improvement can be sustained, and that gross margins can gradually return to their 65% pre-Brexit level.

Allsop valuation

- MTVW commissioned property agent Allsop to value the group’s estate during September 2014.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties carried at the time.

- The Allsop calculation was based on MTVW’s properties remaining in their regulated-tenancy state.

- The Allsop valuation was not formally applied to the accounts. MTVW’s properties remain on the balance sheet at their cost price.

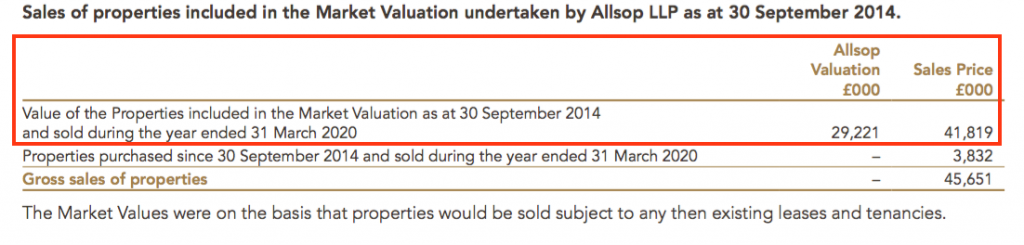

- Following the Allsop valuation, MTVW reveals the proceeds from sold properties versus their stated Allsop value:

| FY 2016 | FY 2017 | FY 2018 | FY 2019 | H1 2020 | H2 2020 | ||

| Property sales revenue (£k) | 61,442 | 57,174 | 45,156 | 41,273 | 17,361 | 24,458 | |

| Allsop valuation (£k) | 42,600 | 38,505 | 30,594 | 28,727 | 12,166 | 17,055 | |

| Sold-premium-to-Allsop (x) | 1.44 | 1.48 | 1.48 | 1.44 | 1.43 | 1.43 |

- These 2020 results showed the ‘sold-premium-to-Allsop’ multiple at 1.43x — in keeping with the previous year and the level witnessed during 2016.

- The ‘sold-premium-to-Allsop’ multiple not moving higher during the last few years suggests house prices have not moved higher either.

- The Allsop valuation is now six years old and may have become rather stale.

- Management claimed at last year’s AGM that it was “premature to conduct another valuation in the current uncertain times”.

- The “uncertain times” related to Brexit.

- This year’s AGM Q&A statement did not herald a fresh Allsop valuation:

Mountview as a property trading company is not legally obliged to value its trading stock nor does any Financial Standard require it to carry out such a valuation. The modus operandi of the company is to acquire residential properties subject to regulated tenancies and sell them when they become vacant.

Because a regulated rent is such a modest return on the investment the properties are acquired at a significant discount to vacant possession value. Because the margin between acquisition cost and sale proceeds is so substantial there is never any reason to dispose of a property while it remains subject to a tenancy.

The cost of carrying out a valuation is such that your Board are reluctant to inflict such an expense on the shareholders when the information so acquired is not a useful management tool. The uncertainties created by Brexit and Covid are such that any current valuation is unlikely to have any long term reliability. Nevertheless your Board always review any representations made by shareholders in respect of a potential valuation.

- Another reason why a new Allsop valuation has yet to be conducted could be the verdict will not show much improvement on the 2014 conclusion.

- Contrasting the 2014 valuation to any 2020 valuation could outline how clever (or not) MTVW’s post-2014 purchases have been.

- A 2020 valuation would also provide greater clarity to the inherent value of MTVW’s property estate.

- The board really ought to commit to fresh Allsop valuations every (say) five years and simply say a valuation is taking place and nothing can be done about any “uncertainties”. Shareholders can then adjust the valuation for any uncertainties themselves.

- The aforementioned management remarks about being “happy in the auction room both in terms of sale prices achieved and the prices at which we have been able to make purchases ” implies MTVW’s executives — despite Covid-19 and Brexit — can still judge the fair value of a property.

- If MTVW’s executives can still judge the fair value of a property, I am sure Allsop can do likewise and therefore undertake another valuation.

Financials

- MTVW’s accounts remain very straightforward.

- Some £15m was spent during the year acquiring 57 additional properties (average cost: £271k), the lowest number of purchases since 2010:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Number of properties purchased | 90 | 118 | 119 | 105 | 57 |

| Cost of properties purchased (£k) | 28,330 | 29,800 | 47,130 | 30,731 | 15,420 |

| Average cost (£k) | 315 | 253 | 396 | 293 | 271 |

- The disposal of four investment properties during the first half raised a useful £4.2m.

- The investment properties had a combined £3.0m book value, which might suggest the remaining investment properties (book value: £24m) are undervalued.

- Mind you, MTVW incurred a £1m write-off on the investment properties due to Covid-19 influences. The annual-report small-print (point 15) admitted:

“The properties are all held for investment and Market Values are on the basis that the properties would be sold subject to any existing leases and tenancies. The valuer’s opinion of Market Value was derived using comparable recent market transactions on arm’s length terms.

The outbreak of the Novel Coronavirus (Covid-19), declared by the World Health Organisation as a “Global Pandemic” on 11 March 2020, has impacted global financial markets. Travel restrictions have been implemented by many countries.

Market activity is being impacted in many sectors. As at the valuation date, the Valuers felt that they could attach less weight to previous market evidence for comparison purposes, to inform opinions of value. Indeed, the current response to Covid-19 means that the Valuers were faced with an unprecedented set of circumstances on which to base a judgement.

The valuation is therefore reported on the basis of ‘material valuation uncertainty’ as per VPS 3 and VPGA 10 of the RICS Red Book. Consequently less certainty and a higher degree of caution should be attached to the valuation than would normally be the case.”

- Earnings of £28m plus the investment-property disposals funded a £17m debt repayment and a £16m dividend.

- Net debt dropped by £17m during the year to £30m — equivalent to 8% of the group’s £392m property estate:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Trading properties (£k) | 334,108 | 347,380 | 376,879 | 392,384 | 392,069 |

| Net debt (£k) | (41,619) | (31,217) | (44,995) | (46,519) | (29,607) |

- Net debt has at times represented 30% or more of MTVW’s property stock.

- The annual report small-print (point 12) reveals MTVW’s banking facilities allow the group to borrow up to £90m — equivalent to 23% of the property estate.

- The current low level of gearing suggests the group is ideally placed to pick up any property bargains.

- Interest costs of £1.0m remain reasonable at 2.4% of average annual debt of £41m.

- MTVW’s books are free of pension obligations.

Corporate governance and protest votes

- Despite MTVW’s illustrious, 40-year-plus history of NAV and dividend advances, not every shareholder is happy.

- The last four AGMs — including the one held this week — have seen significant c30% protest votes against re-electing the independent non-executives, the approval of the board’s remuneration and the re-appointment of the auditors.

- MTVW shareholders can be dividend into three groups:

- The Sinclair family concert party, which is led by chief executive Duncan Sinclair and represents just over 50% of the share count;

- The Murphy family and connected parties, who claim to own 24% of the share count and whose largest shareholder is the chief executive’s sister, and;

- Everybody else, who are left with 25% of the share count.

- The protest votes come from group 2.

- My review of November’s interim figures recapped the grievances of the Murphy family and how the dissident shareholders have prevented the re-election of certain non-execs at the 2017, 2018 and 2019 AGMs.

- When announcing last year’s AGM voting result, MTVW said:

“The Directors will engage with shareholders to obtain feedback on their concerns and will publish an update on that engagement within six months of the date of the Annual General Meeting. “

- A statement during February then revealed:

“Following the 2019 AGM in August and prior to the general meeting held on 18 November 2019, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. They declined to meet or engage. The Company remains committed to shareholder engagement and we will continue to offer to meet with shareholders to take into account their concerns and considerations in the future.”

- I don’t know why the Murphy family declined to meet the board.

- From my 2019 AGM notes, I recall Craig Murphy and the chairman both referring to a previous meeting between the parties, but a difference of opinion was given by each as to what was actually said.

- I can only assume relations between MTVW and the Murphys have now broken down completely.

- How the Murphys now intend to shake up the board therefore remains unclear.

- The 2020 AGM was held this week behind closed doors due to the pandemic.

- Once again the Murphys led a protest vote against the re-election of the non-executives.

- The re-elections were prevented because the resolutions were deemed to be ‘independent’ and the Sinclair family concert party could therefore not vote:

| 2017 | 2018 | 2019 | 2020 | |

| AGM | ||||

| Votes FOR | 126k (13%) | 223k (19%) | 180k (16%) | 236k (20%) |

| Votes AGAINST | 827k (87%) | 927k (81%) | 938k (84%) | 971k (80%) |

| Subsequent GM | ||||

| Votes FOR | 2,361k (74%) | 1,504k (62%) | 2,095k (69%) | - |

| Votes AGAINST | 826k (26%) | 941k (38%) | 939k (31%) | - |

- However, the FCA’s listing rules allow MTVW to hold a subsequent general meeting, whereby the non-exec re-elections can be proposed again — but this time with the Sinclair family concert party allowed to vote.

- The rejected non-execs have always been re-appointed at these subsequent general meetings.

- After this week’s AGM, MTVW repeated its message from last year:

“The Directors intend to engage with shareholders to obtain feedback on their concerns and will publish an update on that engagement within six months of the date of the Annual General Meeting.”

- A follow-up statement should therefore be published on or before 12 February 2021.

- Whether the Murphys will engage with the board this time remains to be seen.

- The 2020 AGM results also revealed a 31% protest vote against a new remuneration policy for the directors.

- The annual report small-print (point 10) claimed the policy was “developed in consultation with major shareholders”.

- A 31% protest vote suggests not every major shareholder was consulted.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- MTVW could be worth more than £200 per share — assuming all of the group’s regulated tenancies were to end immediately and the properties were then all sold at a fair market value.

- The following table outlines my latest sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less property stock sold since Sept 2014 (£k) | (99,098) |

| 218,553 | |

| Allsop-premium-to-book | 2.10x |

| Sold-premium-to-Allsop | 1.43x |

| 655,133 | |

| Stock purchased since Sept 2014 | 173,516 |

| Sold-premium-to-Allsop | 1.43x |

| 248,128 | |

| Possible property stock value (£k) | 903,261 |

- I have taken the original September 2014 portfolio value of £318m and subtracted the £99m book value of properties sold since that date.

- I have then multiplied the £219m remainder by my 2.1x ‘Allsop-premium-to-book’ multiple and then by the 1.43x ‘sold-premium-to-Allsop’ multiple witnessed during 2020.

- I arrived at a £655m estimated value for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has acquired additional properties with a net £174m book value.

- I have assumed all of these additional properties can be sold one day for £248m based on my 1.43x ‘sold-premium-to-Allsop’ multiple.

- Adding the £655m and the £248m together gives £903m.

- This next table adjusts that £903m for 19% taxation, other investments, net debt and other liabilities to give a possible book value of £787m or £202 per share:

| Possible property stock value (£k) | 903,261 |

| Less tax at 19% (£k) | (97,126) |

| Plus other investments (£k) | 24,122 |

| Less net debt (£k) | (29,607) |

| Less other liabilities (£k) | (13,430) |

| Possible NAV (£k) | 787,220 |

| Possible NAV per share (£) | 201.90 |

- These sums are not perfect, and the major question remains how long MTVW will take to sell all of its properties to realise my potential £202 per share NAV guess.

- Bear in mind my NAV per share estimates were £204 for 2019, £213 for 2018, £206 for 2017 and £200 for 2016.

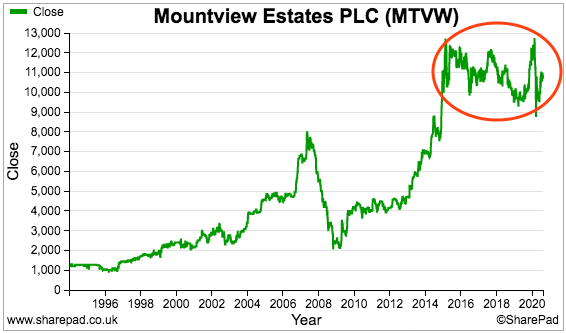

- My estimated value of MTVW’s property estate has not really improved during the last few years, which might explain why the share price has gone nowhere during the same time.

Grainger comparison

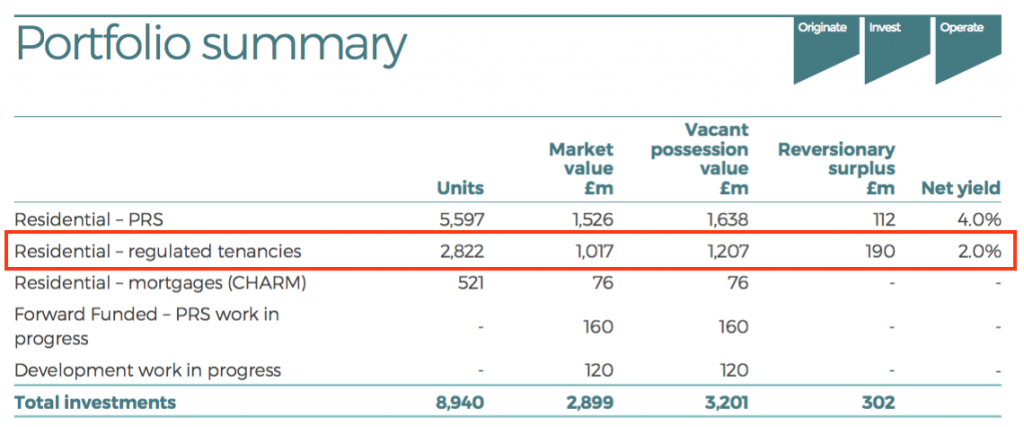

- A comparison between MTVW and Grainger (GRI), the UK’s largest listed residential landlord with a £2b market cap, is instructive.

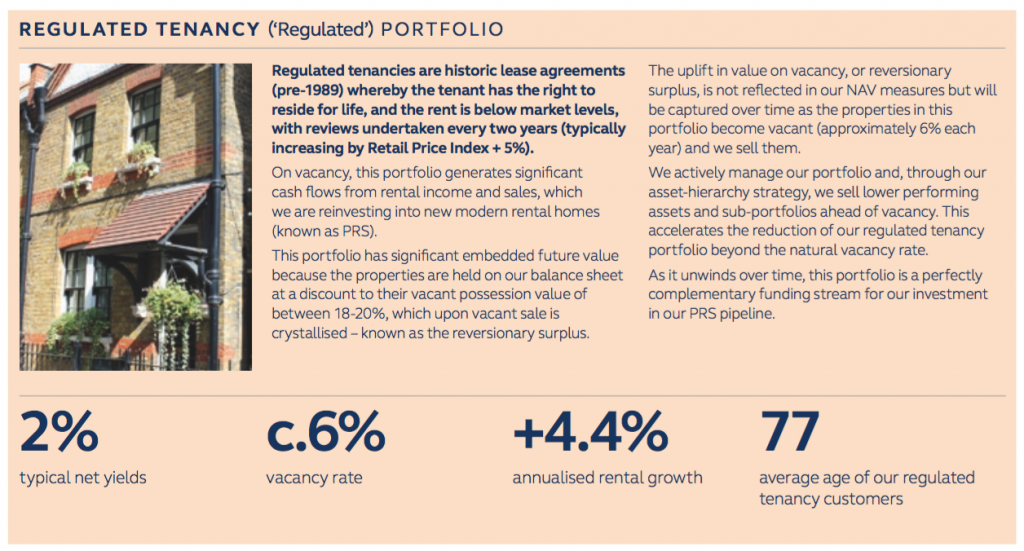

- GRI owns a regulated-tenancy portfolio consisting of 2,822 homes with a £1b market value and a £1.2b ‘reversionary’ value (i.e. the possible value of the properties were the regulated tenancy to finish):

- GRI’s annual reports and presentations provide plenty of useful sector snippets:

- Unlike GRI, MTVW does not disclose rental growth or the average age of its regulated-tenancy occupiers. (Remarks at last year’s AGM suggested MTVW’s board did not even know the average age of its regulated-tenancy occupiers).

- I estimate MTVW’s vacancy rate (i.e. the number of regulated tenancies sold as a proportion of the estate at the start of the year) has averaged 7% during the last ten years.

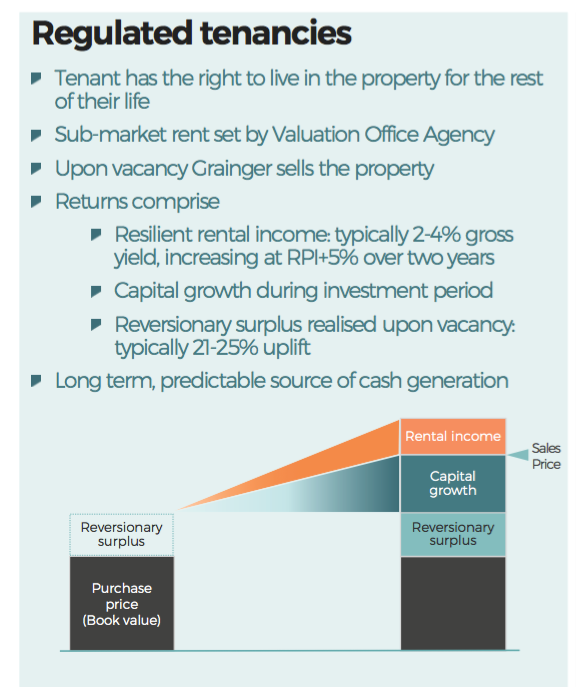

- Applying GRI’s 2% typical net yield and 1.2x ‘reversionary-premium-to-market’ multiple to MTVW’s net rental income of £13m suggests MTVW’s estate could one day be sold for £774m.

- Factoring in 19% taxation, other investments, net debt and other liabilities then gives a possible book value of £698m or £179 per share.

- Note that MTVW’s portfolio includes life-tenancy properties that management has claimed the rentals for which “can be as low as £10 a year”.

- Life-tenancy properties sported a notable £33m book value within these results, and the net yield on that sub-portfolio could be close to zero.

- As such, constructing a valuation using GRI’s 2% typical net yield could mean the overall £179 per share NAV estimate is too conservative.

- Whether MTVW’s inherent balance-sheet value is £179 or £202 per share or somewhere in between, one thing remains a constant…

- …patience is required for the underlying value of MTVW’s property portfolio to be realised.

- Mind you, the longer the disposals take, the higher house prices should rise and the greater proceeds MTVW ought to eventually achieve from future sales.

- In the meantime, two valuation measures are not subject to significant guesswork:

- MTVW’s £97 per share book value — calculated with the properties accounted for at cost — covers 89% of the £109 share price.

- The 400p per share annual dividend supplies a 3.7% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Mountview Estates (MTVW)

Publication of 2020 annual report

Here are the points of interest

1) Extra commentary

The report provided some management commentary beyond that published within the original results RNS:

The more interesting snippets from the extra chairman’s statement referred to buying and selling during the pandemic:

Confirmation that life-tenancy properties have nominal rents, which makes comparative valuations based on net yields a little tricky (see Grainger comparison in the blog post above):

The extra ‘summary prospects’ text provided an encouraging view of trading during the pandemic:

2) Risks

The Risks section contains the same seven risks as before. But each risk now has an added Covid-19 impact.

The following two impacts were the most informative:

MTVW appears to suggest Covid-19 could provide greater vacancies among regulated properties — and perhaps more opportunities to buy and sell.

3) Covid-19 response

The report commendably included a full-page review of actions taken in response to Covid-19. I note MTVW is open to re-jigging rents:

I also note MTVW describes its tenants has having an “elderly profile”:

So while the directors claimed at last year’s AGM not to know the average age of the tenants, they do know the tenants are “elderly”.

4) Audit key matters and materiality

The three key audit matters remained the same as last year. But additional verification work was added for the revenue recognition matter.

Additional Covid-19 guesswork was included within the valuation checks for both the trading and investment properties:

Group materiality remained at £4.2m:

But the materiality level for income statement items and director transactions increased by c2.5x.

Large increases to materiality levels are never ideal — they suggest the auditors will not dig as deep as they once did. But MTVW’s accounts are quite straightforward, the new £1.7m income-statement materiality equates to the standard 5% materiality of pre-tax profit while any shenanigans from the long-standing executives would surely have emerged well before now.

5) Corporate governance

This report contained lots of new text concerning corporate governance. Explanations were given for various non-compliances, but the board reckoned MTVW operates “within the spirit” of the principles given the firm’s size:

6) Our purpose

The text below is all new for 2020:

I quite like the reference to “A long-term view, underpinned by family values and ownership”.

7) Concert party

This is interesting. The Sinclair concert party has a combined shareholding of “over 50%” and the cumulative holdings “reflect a reduction” on the previous year:

For years the concert party held “approximately 53%” of the shares, but this holding reduced to “approximately 52%” for 2018 and reduced again to “approximately 51%” for 2019. The concert-party shareholding is therefore being chipped lower, either by shareholders leaving the party or simply selling their shares.

I am not sure what will happen if the concert-party holding goes below 50%. In theory the dissident investors referred to in the blog post above could garner more votes than the concert party and then oust the board.

8) General meeting

Confirmation the dissident shareholders did not engage with the board after last year’s protest vote:

9) Section 172

MTVW has commendably include a comprehensive Section 172 statement. The statement confirmed the “largest shareholders” were consulted on the new pay policy:

MTVW seems to have little day-to-day contact with the majority of its tenants:

10) Director remuneration

This section always provides interest. The directors are handsomely paid:

A new pay policy has been introduced. The major changes appear to be reducing the maximum annual bonus payout from 250% to 150%, and reducing pension contributions from 20% of salary to the wider workforce’s 3%:

The new pay policy was “developed in consultation with major shareholders”:

The 2020 AGM votes published on 12 August 2020 and referred to in the blog post above revealed a 31% protest vote against the new remuneration policy.

Clearly not every major shareholder was consulted about the new pay arrangements.

The same protest vote (32%) was made at the 2019 AGM:

The executives enjoyed pay rises of 4.7% during 2020:

The chief exec’s pay has advanced at an average 9% per annum during the last five years. The dividend meanwhile has risen an average 8% per annum during the same time.

Bonuses remain chunky. The chief exec’s bonus represented 81% of his salary — which matches the typical proportion from previous years.

The chief exec has been on a nice £1m or so a year since 2016:

The remuneration committee now takes less notice of how peer-group companies are performing due to Covid-19:

The directors have predictably left their pay arrangements unchanged during the pandemic.

Pay rises of 3% are due for 2021.

The following text says the group’s annual performance is “beyond the control of the… Executive Directors”:

Exactly how the chunky 81%-of-salary bonuses were determined was sadly not explained.

At least the directors do not bother with options and pensions:

The related party transactions are the usual loans:

Can’t really say MTVW is being overcharged on the director loans at 0.5%.

Why exactly MTVW continues with these relatively small loans remains unclear.

11) Allsop valuation

Confirmation of the ‘sold-premium-to-Allsop’ multiplier referred to in the blog post above:

£41,819k / £29,221k = 1.43x.

12) Debt

The average rate on MTVW’s debt ticked up a few basis points last year:

Confirmation that the available borrowing facilities add up to £90m:

Headroom was £57m at the year end.

13) Employees

This report carried an extended note on employees:

I like the reference to “family roots” and an “environment in which every member of staff meets and talks with one or both of the Executive Directors”

Total employee costs continue to move higher:

Exclude the directors’ remuneration, and the average employee costs £80k a year — up from £75k last year and £66k five years ago. Total employee costs as a proportion of revenue was 6.3% — the highest for at least 20 years and compares to less than 5% between 2013 and 2017.

Staff productivity has decreased during the last few years. Revenue per head was £3.0m for 2016 and was £2.2m for 2020, the lowest since 2012.

Total property purchase and sale transactions for 2020 were 224, which equates to 7.7 transactions per employee — the lowest since at least 2005. For 2019 transactions per employee were 8.9 and before that was more than 10.

MTVW’s employees being paid more for doing less work is not great.

However, sales transactions are dictated by the availability of tenancies to sell, so productivity is to a certain extent variable each year. Also, more expensive transactions may require more employee effort than lower-value transactions, and that extra effort is not reflected in my transaction-per-head statistic.

14) Inventory and inventory to be settled

Confirmation of the Allsop market valuation from 2014:

MTVW gives an estimate of the stock that could be sold during the year ahead — but the figure is simply an average of the previous three years:

A proper estimate would be more interesting. Last year the supplied estimate was £20.4m and the actual stock sold was £17.7m.

15) Investment property Covid-19 influences and rental yield

Confirmation that the £24m book valuation of MTVW’s investment properties was calculated with Covid-19 in mind:

The rental yield from these investment properties, at £524k, represents only 2% of the £24m book value:

16) Leases

MTVW has not bothered implementing IFRS 16 Leases because its lease obligations are tiny. Instead the old IAS 17 format has been retained:

17) Trade receivables and other payables

Somewhat odd that trade receivables should jump almost 10-fold:

Typically MTVW carries next-to-no trade receivables as such items (I think) are overdue rent payments. I can’t think what else the trade receivables could be. £2m of overdue rent could be plausible at the height of the pandemic (end of March 2020) given annual rent of £19m.

Anyway, ‘other creditors’ have increased by the same c£2m amount, so in cash flow terms the movements balance each other out. I don’t know whether the movements are related. For now the figures involved are not too substantial compared to annual earnings of £28m.

18) AGM questions

An invite for AGM questions, but with no guarantee of a response:

AGM questions were answered in this comment below.

I did not submit any questions, and I understand not every question submitted was answered by email or through the website.

Maynard

Fantastic writeup! Thank you.

I suppose the only question is whether the warring parties get fed up and sell out and if so what price biders, presumably Grainger, are prepared to pay vis-a-vis the £200 true book value.

Thanks Rob. Not sure if the Murphys could sell out even if they wanted to, given the size of their stake. My understanding is they are happy with how the business is run below board level, but not with the corporate governance etc. I think Grainger is now more focused on its PRS developments rather than reversionary properties, but I could be wrong. My £200 figure is educated guesswork and any bidder may want some of the potential upside for itself of course. Bear in mind this business has been quoted for years, has looked cheap for years and yet has never attracted any bid action, so I suppose the family concert party is happy with the status quo.

Maynard

Thanks Maynard, appreciate the extra mile research and comparison with Grainger.

Thanks Robbins

Really great to see the highlighted items and your comments. I think that a takeover is very unlikely, but maybe the family will take it private. Fingers crossed.

Thanks Ian. Gearing is relatively low, so the family could raise debt to take it private then effectively shuffle the debt onto the business. I think the chance of a buyout is very small but I suppose after Daejan anything is possible.

Maynard

Mountview Estates (MTVW)

Annual General Meeting 2020 published 12 August 2020

Just capturing this MTVW statement from the company’s website onto my website.

Maynard

———————————————————————————————————

As announced on 10 July 2020, following the UK government’s introduction of social distancing measures and prohibition on non-essential travel and public gatherings, it is not possible for shareholders to attend this year’s AGM in person.

Shareholders were encouraged to submit questions in advance of the AGM. Responses to the most frequent questions can be found below. These have been considered by the Board.

Valuation of trading properties:

Mountview as a property trading company is not legally obliged to value its trading stock nor does any Financial Standard require it to carry out such a valuation. The modus operandi of the company is to acquire residential properties subject to regulated tenancies and sell them when they become vacant.

Because a regulated rent is such a modest return on the investment the properties are acquired at a significant discount to vacant possession value. Because the margin between acquisition cost and sale proceeds is so substantial there is never any reason to dispose of a property while it remains subject to a tenancy.

The cost of carrying out a valuation is such that your Board are reluctant to inflict such an expense on the shareholders when the information so acquired is not a useful management tool. The uncertainties created by Brexit and Covid are such that any current valuation is unlikely to have any long term reliability. Nevertheless your Board always review any representations made by shareholders in respect of a potential valuation.

Group structure:

This topic has been raised in the past and after investigating the procedures and costs involved and discussing these with shareholders the decision has been to retain the current structure.

The most limiting factor as far as liquidity is concerned is the percentage of the issued share capital held by the Sinclair family in their various guises. As long as the family are content to continue to hold their shares there is no real need for liquidity.

The attraction of the share is as a long term investment based on a very sound balance sheet and a good return on dividend which the company is able to continue paying. The nominal price of the shares is just 5p which would not appear to give much scope for a share split.

———————————————————————————————————