08 April 2020

By Maynard Paton

Results summary for Mincon (MCON):

- A rather muddled and subdued update, the highlight of which during the present Covid-19 uncertainty was a maintained dividend.

- Impairments, exceptionals, accounting quirks and profit diving 28% may all be forgiven if, as seems to be the case, operations have not been too affected by the pandemic.

- An emphasis on “geotechnical” drills and lack of “challenger model” references imply new priorities as the business remains in a ‘moat-digging’ phase.

- Appealing management remarks about product quality, patents and future innovation have yet to make any impact on the somewhat messy financials.

- A post-results acquisition leaves the business with net debt while the underlying P/E of 16 is not an obvious bargain. I continue to hold.

Contents

- Event link and share data

- Why I own MCON

- Results summary

- Revenue, profit and dividend

- H1 versus H2

- Diversification strategy replaces challenger model

- Greenhammer project

- Working capital

- Capital expenditure and free cash flow

- Cash and debt

- Valuation

Event link and share data

Event: FInal results for the twelve months to 31 December 2019 published 23 March 2020

Price: 73p

Shares in issue: 210,973,102

Market capitalisation: £154m

Why I own MCON

- Designs and manufactures industrial drills and bits, with sales supported by established reputation, quality engineering, product patents and technical services.

- Boasts veteran family management with a 43-year tenure, 57%/£88m shareholding and long-term perspective.

- Operations may be resilient to Covid-19 and offer new expansion opportunites within “geotechnical” drilling and direct-supply contracts.

Further reading: My MCON Buy report | All my MCON posts | MCON website

Results summary:

Revenue, profit and dividend

- The preceding first-half statement and Q3 update had already suggested these 2019 results would not be spectacular.

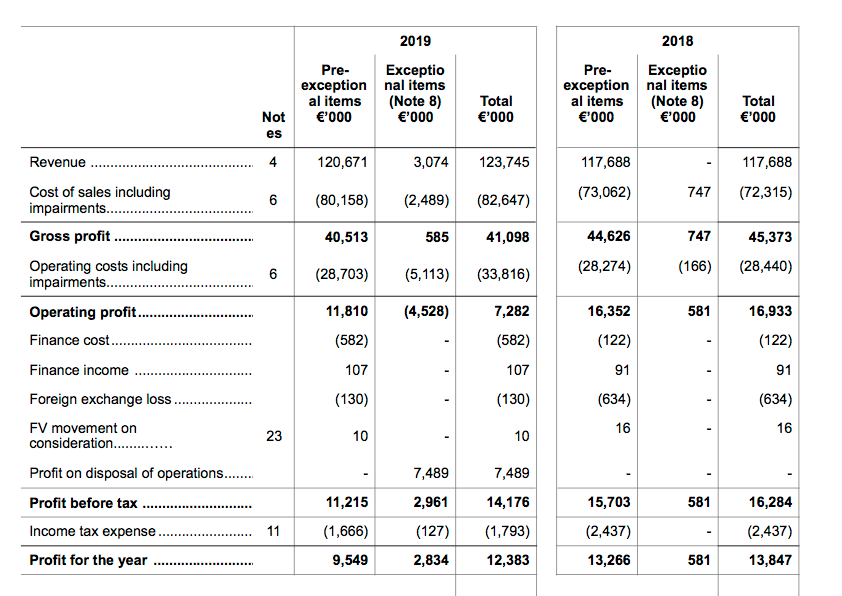

- The headline figures were distorted by acquisitions and disposals alongside a number of other items, which made the accounts very muddled and interpreting underlying progress rather difficult.

- In particular, the comparable 2018 results included:

- Only a nine-month contribution from Driconeq — a Swedish drill-pipe specialist acquired during March 2018 — which at the time brought additional annual sales of €25m.

- A full twelve-month contribution from various subsidiaries that were sold during 2019, the contribution from which for 2018 was not disclosed.

- The accounting of the disposals was unusual.

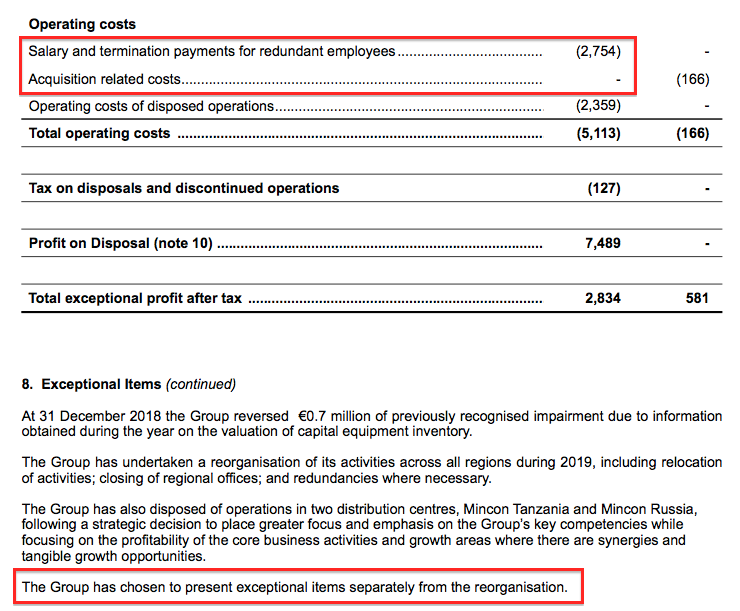

- MCON lumped the revenue and profit from the sold operations within “exceptional” items, rather than disclose them as a separate discontinued-operation entry for both the 2019 and 2018 accounts.

- Other accounting quirks included changing the definition of exceptional items through the year.

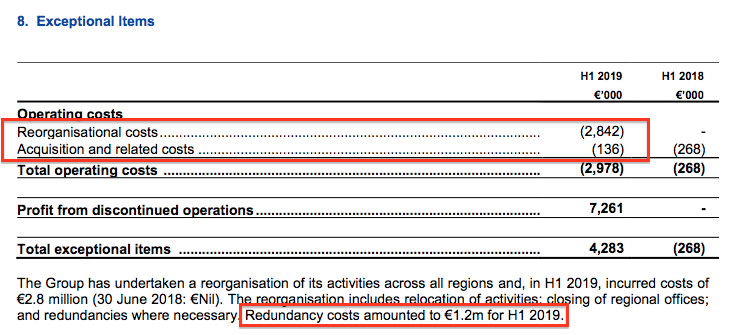

- MCON’s first-half statement included exceptional reorganisational costs of €2.8m, of which redundancy costs represented €1.2m. At the time, aquisition and related costs of €136k were also deemed exceptional:

- However, these annual figures referred only to exceptional redundancy payments:

- The small print implied other reorganisational costs were no longer exceptional.

- The absence of acquisition-related costs within the list of exceptional items implied such expenses were no longer exceptional, too.

- Affecting profit also were impairments to stock of €1.7m for the full year (comprising €2.0m during the first half and a €0.3m reversal during the second) and impairments to trade receivables of €0.8m, neither of which were deemed exceptional.

- The implementation of IFRS 16 — which changes the way companies account for lease costs — slightly distorted the 2019 versus 2018 profit comparison as well.

- Including all those distortions, MCON’s reported revenue and operating profit for 2019 gained 3% and dived 28% respectively:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (€k) | 70,266 | 76,181 | 97,358 | 117,688 | 120,671 |

| Operating profit (€k) | 9,990 | 10,178 | 14,040 | 16,352 | 11,810 |

| Exceptional charges (€k) | - | - | (3,174) | (166) | (2,754) |

| Exceptional gains (€k) | - | - | 3,124 | 747 | 7,489 |

| Discontinued operations (€k) | - | - | - | - | (1,774) |

| Other items (€k) | (481) | 1,125 | (1,273) | (618) | (120) |

| Finance income (€k) | 114 | 30 | (79) | (31) | (475) |

| Pre-tax profit (€k) | 9,623 | 11,333 | 12,638 | 16,284 | 14,176 |

| Earnings per share (c) | 3.79 | 4.39 | 4.79 | 6.45 | 5.84 |

| Dividend per share (c) | 2.00 | 2.00 | 2.05 | 2.10 | 2.10 |

- Back in March 2018, MCON purchased Driconeq and suggested group revenue would then improve to a €120m run rate.

- Continuing revenue of €121m for 2019 suggests the group has not really experienced significant underlying sales growth during the last two years.

- MCON’s longer term progress has been rather lacklustre.

- For 2011, MCON reported revenue of €41m and an operating profit of €13m.

- Revenue tripling and profit going nowhere in eight years is not a great achievement.

- The exceptional €7.5m gain for 2019 related to the somewhat remarkable disposal of a Swedish heat-treatment subsidiary reported at the half year.

- The 28% profit dive, the bevy of accounting quirks and lacklustre long-term record may all be forgiven if the business proves resistant to Covid-19.

- The most encouraging feature of these results was the declaration of a maintained, €0.0105 per share final dividend.

- Many other quoted companies are presently cancelling or suspending their payouts due to the pandemic.

- MCON meanwhile reserved only this paragraph to Covid-19:

“The Mincon Group is monitoring the Covid-19 global pandemic and is taking the advice of local governments in locations where we have a physical presence. The Group has implemented an international travel ban within the Group to all employees for their own safety. Our sales departments have been in regular contact with our customers and are working with our factories to give more flexibility on shipping products. We are conscious of the potential impact the Covid-19 virus might have on future cashflow requirements. We will continue to monitor and evaluate its impact on the business, and where necessary, we will take appropriate steps to limit any personnel and business risks if that might arise.”

- MCON’s results were published on 23 March 2020, fours days before the full lockdown within Ireland commenced.

- MCON’s website does not mention Covid-19 at all.

- I speculate that MCON’s customers — mostly miners operating in remote global locations — may not be facing the same operating restrictions as many European companies at present.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

H1 versus H2

- The aforementioned accounting distortions make the following half-year tables subject to error.

- However, the half-year splits do reveal some interesting developments.

- Re-jigging stock impairments and re-defining exceptional costs meant €0.5m was effectively added back to H2 pre-tax profit:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (own brand) (€k) | 47,406 | 43,020 | 82,327 | 50,464 | 50,322 | 100,786 | |

| Revenue (third party) (€k) | 8,315 | 9,054 | 17,369 | 9,458 | 10,427 | 19,885 | |

| Revenue (total) (€k) | 55,721 | 61,967 | 117,688 | 59,922 | 60,749 | 120,671 | |

| Stock impairment (€k) | - | - | - | (1,992) | 300 | (1,692) | |

| Other impairments (€k) | - | - | - | (582) | (217) | (799) | |

| Operating profit before exceptionals (€k) | 8,087 | 8,265 | 16,352 | 4,365 | 7,445 | 11,810 | |

| Exceptional costs (€k) | (298) | 879 | 581 | (2,978) | 224 | (2,754) |

- Also of note were MCON’s costs:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Raw materials (€k) | 16,246 | 16,975 | 33,221 | 16,888 | 22,302 | 39,190 | |

| Employee costs (€k) | 15,710 | 17,391 | 33,101 | 16,934 | 13,010 | 29,944 |

- The increase to raw-material costs during H2 was not explained within the management commentary.

- However, the H2 reduction to employee costs reflects the group reorganisation and is encouraging for 2020.

- MCON’s efforts from selling third-party equipment may have experienced a boost during the second half:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Third-party revenue (€k) | 8,315 | 9,054 | 17,369 | 9,458 | 10,427 | 19,885 | |

| Third-party product purchase (€k) | 6,569 | 7,056 | 13,625 | 7,743 | 6,461 | 14,204 | |

| Difference (€k) | 1,746 | 1,998 | 3,744 | 1,715 | 3,966 | 5,861 |

- The difference between third-party revenue and third-party product purchases — which I assume effectively equates to third-party gross profit — was notably higher (at €4m) during H2.

- MCON ironically said 18 months ago:

“We are on a path to remove third party sales from our line-up where that makes commercial sense, to either manufacture them in our own plants, or discontinue the sales.”

- Third-party revenue for 2019 was €20m, versus €17m for 2018 and €22m for 2017.

Diversification strategy replaces challenger model

- Management’s introduction to these results appeared to signal a strategy change (my bold):

“I am pleased to report that Mincon’s 2019 financial results represented a significant step forward in Group’s long-term strategy to diversify our customer base.”

- The word “diversify” was not used within the previous seven results statements.

- Instead, MCON had increasingly mentioned its “challenger brand” strategy of supplying a comprehensive range of drills and bits directly to end customers.

- For example, the 2018 results said (my bold):

“In recent years we have set out to assemble the full range of the drill string for different types of mining and construction piling. This provides it with the opportunity to deliver a full service offering to end customers, and as we now design and manufacture the key elements in the drill string, we have differentiated ourselves from the less developed businesses in low margin activities in the sector, and are stepping towards direct provision to end customers and larger contracts.”

“There is a world of difference between offering the products in a catalogue, even an online catalogue, and engaging directly with the end customers on their specific requirements to achieve their objectives”.

- Mind you, the challenger strategy appears to have borne some fruit. This RNS did state (my bold):

“Our work on filling out our product range and expanding our geographic support also saw Mincon win several large, direct-supply mining contracts. These contracts are for comprehensive drilling consumables supply, and the ability to supply the full range, together with the required service support levels to maintain them, enables us to undertake a programme of continuous improvement to increase our value-add to Mincon and to the end user.”

- However, the new direct-supply contracts could not offset lower demand for MCON’s flagship drills (my bold):

“The Group’s manufactured conventional DTH [‘Down the Hole’] product, that provides the Group its highest profit margin endured a decline of 16% in revenue during 2019 compared with 2018.”

- MCON claimed the DTH decline was “partly due to delays in commissioning heat treatment facilities”, which have now been resolved and have subsequently led to “improved revenue…during the first quarter of 2020”.

- The “long-term strategy to diversify [the] customer base” involves selling drills and bits to construction and “geotechnical” clients.

- MCON said sales to such clients doubled during 2019 to an implied €14m:

“In 2019 revenue generated in this [construction and geotechnical] market accounted for 12% of the Group’s revenue within continuing operations, while in 2018 the corresponding figure was 6%.”

- MCON explained its geotechnical product technology had caught its customers’ attention (my bold):

“This increase in geotechnical revenue was achieved due to customers responding favourably to the unique and predominantly patented features of the Mincon product range, which ensures minimal ground disturbance.”

- The primary geotechnical product appears to be MCON’s patented “Spiral Flush” air control system, which enables “drilling in tight urban spaces with sensitive ground conditions”.

- Work on the Spiral Flush underlined MCON’s ongoing innovation to develeop a sustainable competitive advantage.

- Notable quotes in this RNS included:

- “product line-ups… remain at industry highest standards”;

- “market-leading performance”, and;

- “the next generation of drilling tools” that may have a “transformational effect on Mincon and [its] customers”.

- The 2018 annual report (point 1) carried plenty of similar quotes. For example (my bold)

“It is our belief that the building up of our intellectual property, the increased quality of our manufacturing, and the investment in our service is a combination that protects and develops our products, our people and our margins.”

- MCON said the geotechnical and foundation drilling market “remains a large, exciting, and lucrative opportunity”.

Greenhammer project

- Progress remains slow at MCON’s Greenhammer project.

- This time last year the firm described the new hydraulic drilling system as “a disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base”.

- MCON added: “This is not a small system or easily replicable, and we have placed patents around the system to protect it. The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.”

- The new system can also address problems that occur when drilling hard rock or drilling at high altitude.

- The project has been in development for eight years, and was first mentioned by MCON within its 2016 results.

- Three years on, and the customer about to test the system has suffered problems:

“Since the beginning of 2020 we have been working on a schedule of commercialising the system on the customer owned rig by the end of Q1 2020. This has been delayed due to a serious mechanical issue arising on the customer owned rig, prior to its handover to us, which has necessitated an extensive rig overhaul, making the rig unavailable to us until Q2 2020.”

- But MCON remains positive:

“We remain excited about the transformational benefits of this system for Mincon and the hard-rock mining industry and we look forward to commercial release once we can get back drilling.”

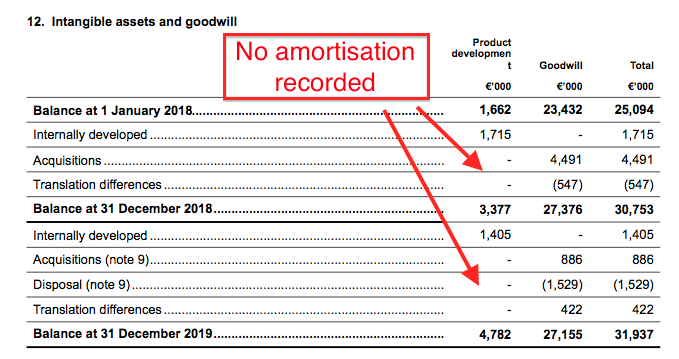

- MCON capitalised Greenhammer development costs of €1.4m during the year to take the project total to €4.8m since 2016.

- In comparison, aggregate operating profit before exceptional items since 2016 has been €52m.

- Not a cent of that €4.8m expenditure has been charged against earnings. Amortisation will commence only when the Greenhammer system enters commercial use:

Working capital

- For some years now, MCON has operated with significant amounts tied up in working capital (stock plus trade and other receivables less trade and other payables).

- For 2019, year-end working capital represented almost 50% of revenue:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Working capital (€k) | 38,286 | 45,186 | 41,690 | 58,041 | 58,083 |

| Revenue (€k) | 70,266 | 76,181 | 97,358 | 117,688 | 120,671 |

| Working capital/Revenue (%) | 54.5 | 59.3 | 42.8 | 49.3 | 48.1 |

- For some perspective, FW Thorpe — a fellow portfolio holding that manufactures lighting systems — operates with approximately 23% of its revenue as working capital.

- Stock is the largest component of MCON’s working capital:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Stock (€k) | 32,045 | 35,310 | 31,851 | 49,357 | 48,590 |

| Revenue (€k) | 70,266 | 76,181 | 97,358 | 117,688 | 120,671 |

| Stock/Revenue (%) | 45.6 | 46.4 | 32.7 | 41.9 | 40.3 |

- MCON has previously stated high stock levels are required to ensure tip-top customer support.

- The preceding half-year results had included a €2.0m charge for outdated stock and suggested further stock write-offs could not be ruled out.

- However, these figures encouragingly revealed a €1.7m charge for outdated stock — meaning stock of €0.3m was not outdated after all. That €0.3m was added back to second-half profit.

- These results also disclosed a €0.8m impairment to trade and receivables (versus zero for 2018).

- Very encouragingly, MCON generated a net cash inflow from working-capital movements for the first time since at least 2010:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit (€k) | 9,990 | 10,178 | 14,040 | 16,352 | 11,810 |

| Depreciation and amortisation (€k) | 2,346 | 2,332 | 3,014 | 3,896 | 5,242 |

| Net capital expenditure (€k) | (1,768) | (5,246) | (5,639) | (12,552) | (7,930) |

| Working-capital movements (€k) | (2,837) | (1,152) | (4,408) | (14,870) | 2,095 |

| Net cash (€k) | 38,610 | 34,960 | 26,142 | 846 | 1,446 |

Capital expenditure and free cash flow

- Previous company remarks had suggested MCON’s capital expenditure would be less than depreciation during 2019.

- For example, the 2018 annual report (point 7) said (my bold):

“Capital expenditure is expected to run at or below depreciation in the coming three year cycle unless we see the type of growth that we achieved in the last three years or unless we decide building a new factory makes sense. We will flag that some months in advance if we do, otherwise the plan for 2019 is to return to cash generation as we stabilise our growth.”

- Furthermore, October’s Q3 statement said (my bold):

“Capital expenditure at present, after some years of build out, has fallen to half the depreciation rate, and is likely to remain there for a couple of years outside of decisions and opportunities in the GeoTech side.”

- In the event, capex of €8m compared to depreciation of €5m.

- The €8m expenditure was not explained within the management narrative. I can only presume the capex related to the group reorganisation and/or the shift to supplying the geotechnical market.

- During the last five years, MCON has spent €33m on tangible assets but charged only €17m as depreciation against earnings.

- The hefty working-capital movements and hefty capex has resulted in poor free cash conversion.

- Since 2015, MCON has reported a cumulative post-exceptional operating profit of €55m yet generated free cash over the same time of just €12m.

- The €43m gap is represented mostly by working-capital movements of €21m, capital expenditure in excess of the depreciation charge of €16m, and Greenhammer development costs of €5m.

- Add on net acquisition spend of €17m and dividends of €21m, and the €47m raised at the 2013 flotation has now mostly disappeared.

Cash and debt

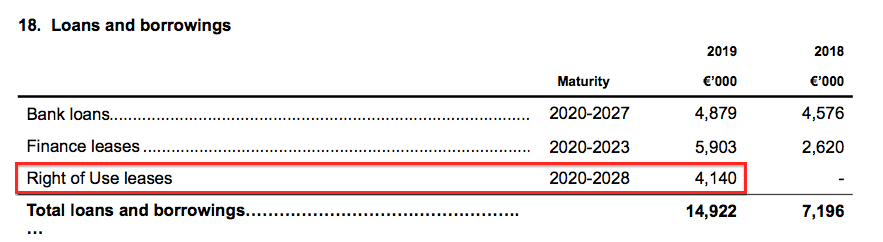

- Year-end cash of €16m exceeded year-end loans and borrowings of €15m by just €1m.

- Bear in mind property leases under IFRS 16 are now accounted for as debt:

- Conventional borrowings are therefore €11m.

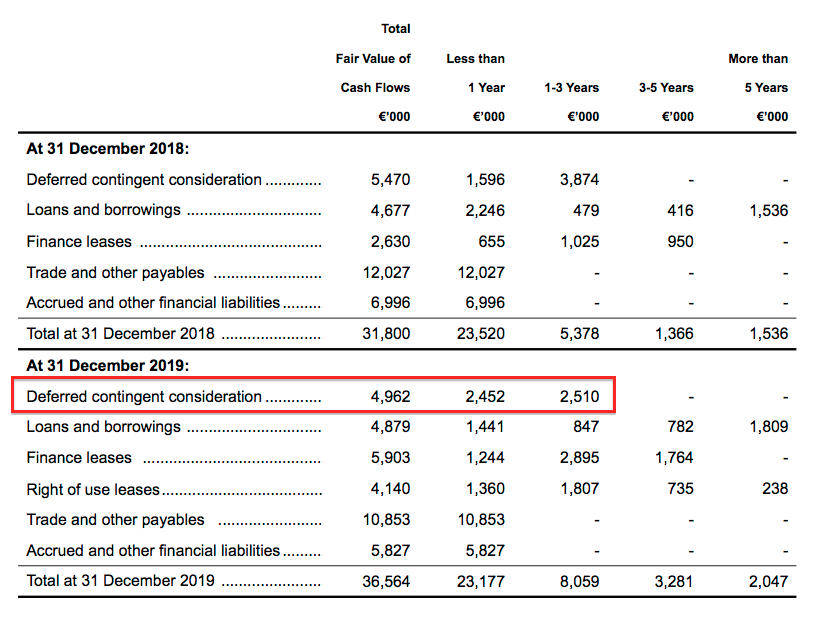

- Bear in mind, too, that MCON remains on the hook for €5m of contingent acquisition payments — all of which are due within the next two years:

- Ignore property leases and include the contingent payments, and net cash is effectively zero.

- The purchase of Lehti for €8m at the start of 2020 has since put MCON in a net debt position.

- Lehti manufactures MCON’s geotechnical drills, and 70% of Lehti’s revenue is derived from MCON.

- The purchase logic — to protect a key supplier and take Lehti’s margin in-house — seems very sound. The price at 4x EBITDA was not extravagant either.

- Net debt of, say, €8m post-Lehti is arguably not a great position given the ongoing Covid-19 pandemic and the cash-conservation measures many other companies are currently undertaking.

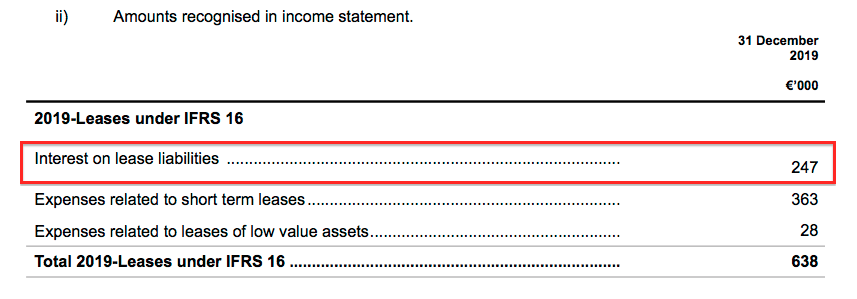

- MCON incurred finance costs of €582k during the year, of which €247k related to IFRS 16 property leases:

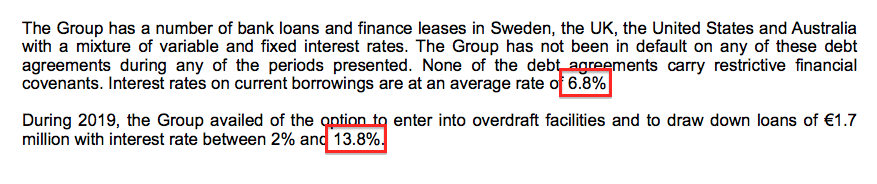

- Conventional interest of €335k (€582k less €247k) was paid on average conventional debt of €9m giving an effective interest rate of 3.7%.

- That 3.7% rate does not seem outrageous. The results small-print reveals some borrowings attract rates of 7% and 14%:

- The aforementioned impairments of stock/receivables (total: €2.5m) compressed MCON’s margin and return on equity to very modest levels:

| Year to 31 December | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating margin (%) | 14.2 | 13.4 | 14.4 | 13.9 | 9.8% |

| Return on average equity* (%) | 12.7 | 13.0 | 12.6 | 12.6 | 7.6% |

(*adjusted for net cash and contingent considerations)

- Margins may have scope to increase. MCON claimed:

“Once [restructuring is] complete, our factories will be more efficient and should earn a healthier margin…”

- ROE could improve if/when stock levels reduce and/or when recent capex generates a suitable return. Stock and property, plant and equipment represented a significant 72% of the year-end balance sheet (€90m of €126m).

- The ROE figures also suggest acquired goodwill and capitalised development costs totalling €32m (or 25% of the year-end balance-sheet value) have to date not been great investments.

- MCON carries no pension obligations.

Valuation

- MCON sounded an optimistic note for the current year (my bold):

“I hope to report continuing growth throughout this year, in both traditional and new markets. This, along with shrewd management of costs, should see a stronger result for 2020.”

- Trading prior to Covid-19 was positive (my bold):

“We have seen good growth in the first quarter of 2020 to the date of this report, with accompanying profit figures as a result of the Group reorganisation that took place during 2019. During the first quarter of 2020 we have won additional geotechnical contracts in the Americas region, and our DTH product line has seen an improved order intake, with other product lines following suit.”

- Excluding restructuring costs and stock/receivable write-offs, operating profit for 2019 was €14.3m.

- Subtract €1.4m for ongoing Greenhammer expenditure gives €12.9m.

- After estimated interest costs of €0.4m and tax applied at the underlying 15% level for 2019, earnings come to £9.7m or 4.6p per share with £1 buying €1.13.

- No adjustment has been made for the Lehti acqusition.

- The 73p mid-price price values the business at 16x my earnings estimate.

- The shares do not look an obvious bargain given the subdued trading progress, ongoing strategy changes, muddled accounts and the significant investment that continues to hamper free cash flow.

- I can only presume the stock market remains optimistic about MCON’s:

- Geotechnical venture and the further opportunities that may develop post-Lehti;

- Greenhammer project one day coming good;

- Long-term dedication to engineering quality and product leadership, and;

- Apparent resistance to Covid-19.

- I am hopeful MCON can succeed. The boardroom statements within the 2018 annual report (point 1) were some of the more inspiring director commentary I read last year. Quotes included (my bold):

“As owners we believe that long-term sustainability will remain a key priority for Mincon’s business, and consequently our engineering efforts and global growth. Mincon is building a business for the future by recruiting and nurturing new engineering talent; developing its existing service and manufacturing centres; diversifying its product range; and expanding market presence.”

- At present, though, management’s annual-report ambitions and talk of “industry highest standards”, “market-leading performance” and “the next generation of drilling tools” have yet to be reflected in the accounts.

- MCON arguably remains in a ‘moat-digging’ phase — the duration and cost of which is unknown.

- Only when margins and ROE recover back to, say, levels of 15% or more, and free cash improves, will MCON demonstrate it really does boast some sort of competitive advantage.

- The trailing €0.021 per share dividend — assuming it is not cancelled — equates to 1.86p per share and supplies a 2.5% yield (before Irish withholding taxes for UK-resident investors).

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Mincon.

Mincon (MCON)

Q1 Trading Update published 05 May 2020

Confirmation that MCON may not be too affected by the pandemic. Here is the full text (my bold):

———————————————————————————————————————–

Mincon Group plc (Euronext:MIO AIM:MCON), the Irish engineering group specialising in the design, manufacture, sale and servicing of rock drilling tools and associated products, today provides an interim trading update for the period from 1st January 2020 to date, incorporating the first quarter to 31st March 2020.

Key elements (comparison of Q1, 2020 to Q1, 2019):

Q1 results show a period of steady progress –

* Revenue up 4% overall

* Gross margin up to 35.2% from 33.6% reflecting a higher proportion of Mincon manufactured product

* Covid-19 impacting on certain operations and markets but in most of the countries where we are active the factories and related customer sites are regarded as critical and remain open

* Integration of Lehti into the Mincon Group has proceeded smoothly since its acquisition in January 2020. Lehti has also experienced growth in Q1 2020 compared to Q1 2019

Trading

The Group’s strategy of improving our sales offering through the diversification of our income streams has provided us with continued revenue growth from the sale of Mincon manufactured product during the first quarter of 2020, with our Group wide revenue in line with our expectations for the period.

The acquisition of the Lehti Group in January 2020 has resulted in Mincon achieving a better consolidated gross margin as we now own the manufacturing of all Mincon designed products. The performance of the Lehti Group has been in line with our expectations during this transitional period into the Mincon Group. We expect to have completed the consolidation of our operations in Finland by September 2020.

Covid-19

We have seen restrictive measures in the Southern African market during March 2020. Our drill rod factory in South Africa had been closed in March along with much of the of the mining activity there, however, those restrictions have started to ease.

We have experienced some difficulty in moving product by air during March, mostly seen in Australia where it is very common to move specialised parts using this method. In parts of central and South America mining production has temporarily been interrupted, however this is in areas where we have a relatively minor presence.

Generally, our order book remains steady, and our factories are viewed as essential manufacturing in almost every jurisdiction we are located in. However, the effect and duration of the pandemic remains uncertain, and we have put in place additional lines of credit with our banking partners in different regions where it is felt appropriate to do so. We have not drawn on any of this additional credit, but it is available to us if needed in the future. Our balance sheet remains very strong, and we have not experienced any losses or any material effects on the inflow of debtor payments.

Product Development

Drilling with our Greenhammer systems has been delayed due to Covid-19 site restrictions implemented by the customer. The customer has restricted site access to essential employees only during the lockdown. We would hope to begin drilling on both the 10″ and 12″ system within a matter of weeks once these restrictions have been lifted.

———————————————————————————————————————–

The factories generally remain open and the pandemic issues relate mostly to logistics. I note MCON referred to debtor payments — the business does suffer from tardy customer payments, so the mention is reassuring. No need for extra loans is also encouraging.

MCON’s previous quarterly updates referred to profit performance (see Q3 2019). No such mention this time — just something on gross margin. MCON’s quarterly profit can bob up and down, and I stopped trying to work out the quarterly contibution a while ago. I do think MCON could even drop the regular quarterly updates — such reporting can lead to investors wrongly extrapolating a three-month performance.

All told, the business appears to be coping relatively well with the pandemic.

Maynard

Mincon (MCON)

Publication of 2019 annual report

Here are the points of interest

1) Extra commentary

The report provided a fair amount of management commentary beyond that published within the original results RNS.

A number of remarks encouragingly referred to tip-top engineering, significant business opportunities and organic growth:

I note the company’s ‘commitment’ bullet points from last year…

…have been beefed up to include the term “industry leading”:

2) Financial review

The annual report also provided extra commentary on the financials.

The purchase of Lehti ought to improve ‘geotechnical’ margins, while sales of ‘down-the-hole’ drills ought to revive as well:

MCON has always carried significant levels of stock (see point 13 below) and I am encouraged the level is expected to decrease this year:

(I look at the remarks on prepayments in point 15 below).

Yet more commentary on trying to improve the quality of the business — “better margins at less risk”:

This next snippet suggests future growth will be steadier than it has been:

3) Geographic review

For the first time MCON included brief reviews of each geographical region. Here is the Americas text:

4) Corporate governance

MCON’s Irish domicile means the firm can skip a lot of standard UK corporate governance text. The annual report for instance does not contain a Section 172 operational review that has become a recent reporting standard.

However, the report does reveal some improvements being made to the board’s effectiveness:

Board effectiveness improvements were also reported within the 2018 report.

5) Chairman’s bio

The bios of non-executive can be useful. I always like to see an industry veteran or ‘mentor’ figure helping out the execs. MCON’s chairman is interesting — he is a geologist and an ex-mining boss, so presumably offers the customer perspective on the types of mining drills made by MCON:

6) Risks

The Risks section included new text about copycat competitors:

MCON continues to name its major rivals:

The shift towards larger contracts could mean lumpier revenue and unpredictable profits:

Revenue from the ten largest customers reduced from 21% to 20% last year:

A new risk about Covid-19 was unsurprisingly added:

7) Audit key matters, materiality and scope

The auditors (KPMG) perhaps surprisingly consider only one key audit matter — revenue recognition. This year the presumed risk included the possibility of fraud:

Materiality remains the standard 5% of pre-tax profit:

Audit scope is a bit odd. Last year’s report said the number of reporting components was 29, but the 2018 figure has now been restated to 44:

Just 13 of the 42 reporting components we subjected to full-scope audits, which does not sound great although many of the group’s subsidiaries are very small. MCON could helpfully publish the percentage of revenue and profit that were covered by full-scope audits, but that requirement for UK companies seemingly does not stretch to Irish firms.

8) Covid-19 and going concern

This report barely mentioned Covid-19 even though the document was published on 30 April — so a month or so into the pandemic. The ‘going concern’ note contained these two Covid snippets:

Let’s hope the lack of Covid-19 references means the business is relatively resilient to the pandemic.

9) Director pay

As well as skipping corporate-governance text, MCON also skips on remuneration-committee text. The RemCom report was very short given six meetings took place:

Would be very useful to know why the chief exec (commendably) reduced his salary by €50k:

The executives have not collected a bonus following MCON’s 2013 flotation. Nor do they own any options. Their family does own 57% of the company though.

10) Employees

MCON’s reorganisation last year left employee numbers 9% lower and bolstered productivity:

The average cost per employee (excluding ‘termination’ costs of €2.8m) was €64k, in line with 2018, 2016 and 2015. Revenue per head was €258k, and better than the €229k from last year — but this figure has topped €300k in the past.

Staff costs (excluding ‘termination’ costs) represented 25% of revenue — an improvement on last year’s 28% and in line with the proportion for 2015, 2016 and 2017.

11) Goodwill

The small-print implies MCON continues to expect 3% annual growth from its acquired businesses beyond the next three years:

I note the discount rate to calculate the goodwill has reduced considerably.

Lower discount rates increase net present values and so can be used to shore up goodwill figures to avoid an impairment. However, MCON does confirm a 5% change to the discount rate would not lead to an impairment, so the discount rate could revert to a more demanding 12% and apparently not create a write-off.

12) Greenhammer useful life

The blog post above mentioned the Greenhammer project had so far cost €4.8m, none of which had been amortised through the P&L to date. The annual report reveals any amortisation will cover between three and five years, which is typical for intangible useful lives:

13) Inventories

Confirmation of the huge levels of stock held on the balance sheet:

€49m represented 41% of revenue last year.

14) Share based payments

Outstanding options represent less than 1% of the share count:

15) Trade receivables and prepayments

Good progress with trade receivables. Customers seem to be paying more quickly:

Net trade receivables represented 17% of revenue last year — the lowest level since 2013. In addition, trade receivables less than 60 days old represented 84% of all net trade receivables — the highest proportion since at least 2009.

Receivables include prepayments, which include prepayments for plant and machinery:

I must admit, I can’t recall another company disclosing upfront payments for plant and machinery. I am not sure how the accounting works. In the cash flow statement, the prepayment movement is shown as a working-capital entry:

I don’t know exactly how a prepayment for plant and machinery then becomes accounted for as a conventional fixed tangible asset when MCON eventually takes ownership of the asset. Does the prepayment cash movement reverse, and then becomes allocated within the conventional ‘purchases of property, plant and equipment’? Something to think about.

Maynard