12 November 2020

By Maynard Paton

Results summary for Bioventix (BVXP):

- Very satisfactory FY 2020 figures, although H2 growth subsided to mid-single-digits after the pandemic reduced demand for routine blood tests.

- A 21% final-dividend lift plus a special payout for the fifth consecutive year underpinned a generally positive outlook.

- Revenue from vitamin D gained 10% and may finally have “plateaued”, while troponin sales quadrupling within the next two years is apparently “plausible“.

- The books remain in excellent shape with record 79% margins, robust cash flow, a £5m cash buffer and no debt.

- The ace financials and predictable customer income leaves an understandably lofty P/E of 32. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own BVXP

- Results summary

- Coping with Covid-19

- Revenue, profit and dividend

- Vitamin D

- Troponin

- Other antibodies

- Pipeline developments

- Other webinar remarks

- Financials

- Valuation

Event links, share data and disclosure

Event: Preliminary results and presentation for the twelve months to 30 June 2020 published 19 October 2020 and ShareSoc webinar hosted 28 October 2020 (ShareSoc membership required)

Price: £41

Shares in issue: 5,209,333

Market capitalisation: £214m

Disclosure: Maynard owns shares in Bioventix. This blog post contains SharePad affiliate links.

Why I own BVXP

- Develops diagnostic antibodies for blood-test machines, direct competition for which is limited due to regulatory hurdles, scientific innovation, customer switching costs and revenue ‘lock in’ through ‘captive’ hospitals.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 8%/£17m shareholding and has declared five special dividends.

- Employs asset-light royalty model that encompasses terrific margins, super returns on equity, decent cash flow and no debt.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Coping with Covid-19

- Interim results issued during March suggested Covid-19 would affect BVXP.

- BVXP said at the time:

“Covid-19 could have an impact on sales as routine blood-testing at hospitals continues but at a lower volume as resources are switched to Covid-19 patients.”

- Sure enough, this FY 2020 statement admitted:

“The Covid-19 pandemic impacted sales during Q2 2020 as routine blood-testing at hospitals continued but at a lower volume. The timing of a return to normality remains uncertain.”

- BVXP did not disclose exact details of the impact, but instead implied blood-test numbers had fallen 15-20%:

“There have been reports in the market that the routine global IVD market suffered a 15-20% reduction in activity during the period April to June 2020 (eg Siemens Healthineers Q2.2020 revenues as reported on 2 August). The six-monthly nature of our customer royalty reporting limits our visibility but we can see clear evidence from our physical product sales during this Q2.2020 period that corroborate such a pandemic effect.”

- BVXP’s H2 performance (see Revenue, profit and dividend below) was very subdued compared to the bumper H1 display.

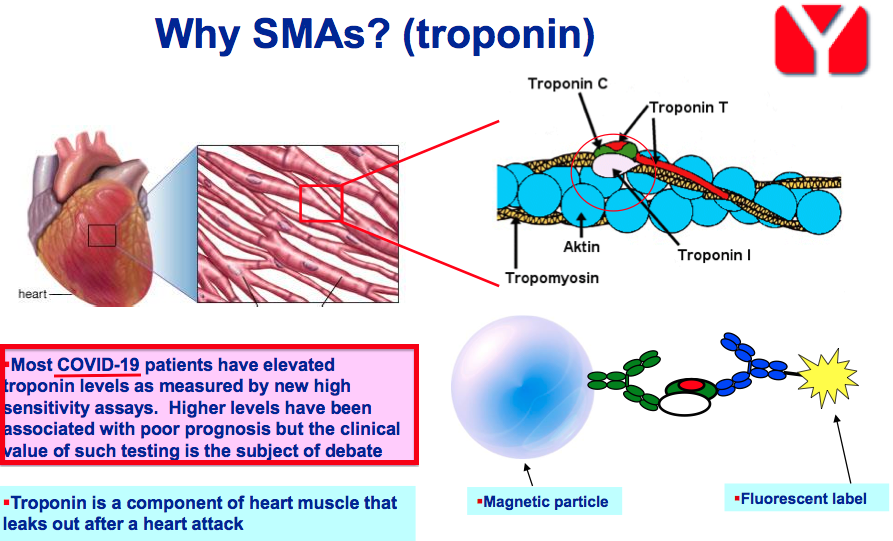

- March’s results presentation included some vague remarks about elevated troponin levels associated with potential Covid-19 infections:

- The vague remarks were not repeated within these results.

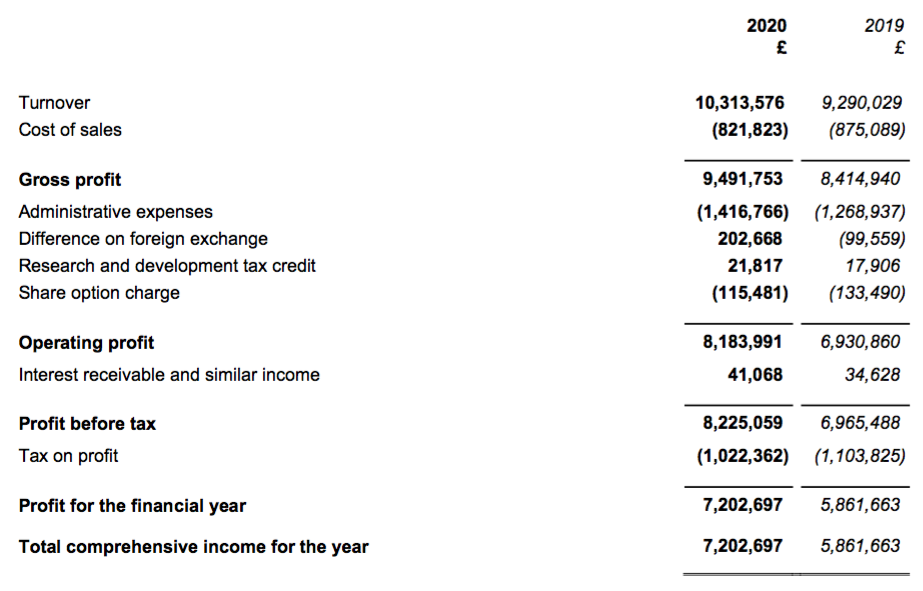

Revenue, profit and dividend

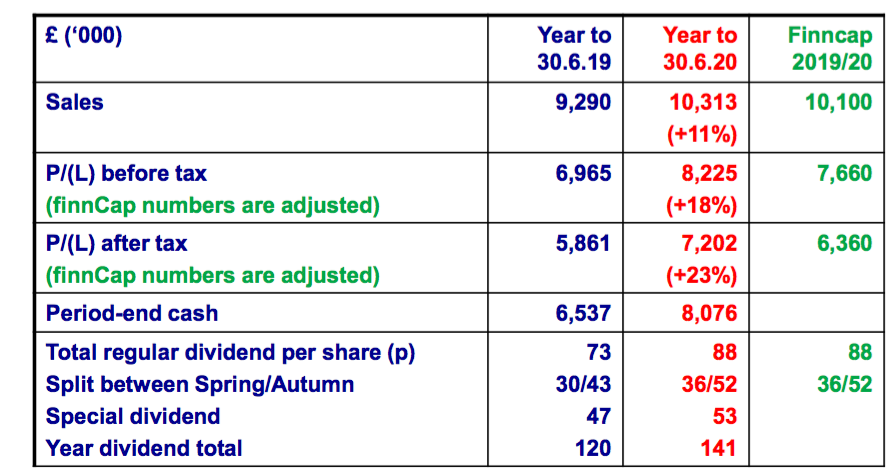

- These FY 2020 figures were very satisfactory in the circumstances.

- Revenue gained 11% and reported operating profit climbed 18%.

- The results registered new all-time highs for revenue and profit for the tenth consecutive year:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 5,517 | 7,246 | 8,752 | 9,290 | 10,314 |

| Operating profit (£k) | 4,205 | 5,716 | 6,833 | 6,931 | 8,184 |

| Other items (£k) | - | - | - | - | - |

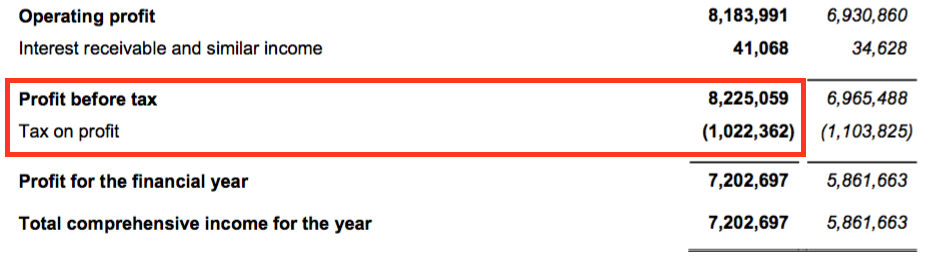

| Finance income (£k) | 14 | 56 | 34 | 35 | 41 |

| Pre-tax profit (£k) | 4,219 | 5,772 | 6,867 | 6,965 | 8,225 |

| Earnings per share (p) | 69.2 | 96.4 | 110.2 | 114.0 | 139.4 |

| Dividend per share (p) | 42.5 | 51.0 | 61.0 | 73.0 | 88.0 |

| Special dividend per share (p) | 20.0 | 40.0 | 55.0 | 47.0 | 53.0 |

- The performance was distorted only by foreign-exchange gains/losses.

- A £203k foreign-exchange gain this year compared to a £100k loss for FY 2019:

- The foreign-exchange movements bolstered H2 in particular:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Revenue (£k) | 4,365 | 4,925 | 9,290 | 5,099 | 5,215 | 10,314 | |

| Operating profit (£k) | 3,236 | 3,695 | 6,931 | 4,079 | 4,105 | 8,184 | |

| Difference on FX (£k) | 25 | (124) | (100) | 80 | 122 | 203 | |

| Operating profit before FX (£k) | 3,212 | 3,819 | 7,030 | 3,999 | 3,982 | 7,981 |

- H2 profit advanced 11% with the FX movements, but just 4% without.

- After H1 revenue surged 17%, H2 revenue gained just 6% to reflect the aforementioned Covid-19 impact.

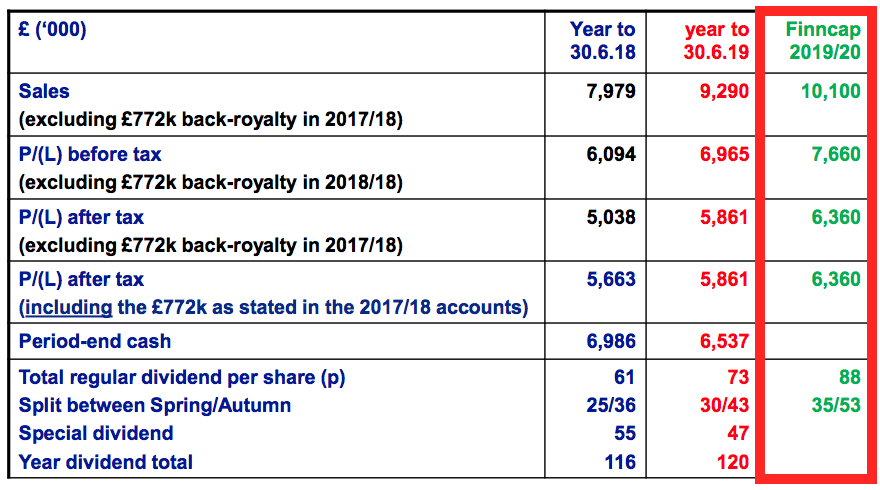

- The FY 2020 performance was in excess of the house broker’s estimates:

- Those estimates were made this time last year, and six months ago I felt the projections were “rather pessimistic”.

- Unlike previous results, these FY 2020 figures were not distorted by back-dated royalties or income from now-terminated products.

- BVXP’s sloppy bookkeeping had prompted me to write in May:

“I hope some [succession] planning goes into the role of FD, too.”

- I was therefore pleased a new finance director was appointed during July.

- After the interim dividend was lifted 20%, the final payout was hoisted 21% to 52p per share.

- For the fifth year running, the ordinary dividend was accompanied by a special payout.

- The 53p per share special dividend brought the total of special dividends declared during the past five years to 215p per share — versus 315.5p per share declared as ordinary dividends.

- BVXP has therefore distributed its entire FY 2016-2020 earnings (529.2p per share) as ordinary/special dividends.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

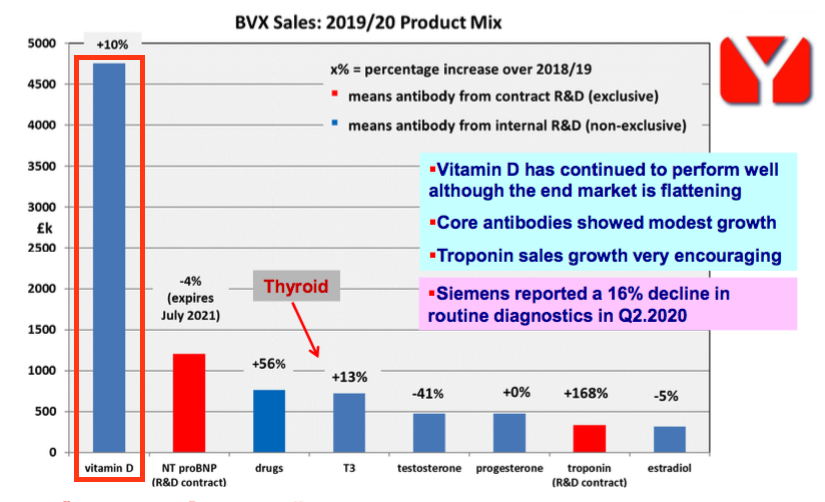

Vitamin D

- Representing 47% of revenue, BVXP’s vitamin D antibody remains by some distance the group’s best-seller:

- Vitamin D revenue advanced by 10% to £4.8m for FY 2020 — a rate considerably lower than the 20%-plus growth enjoyed during previous years.

- BXVP noted:

“[A]s we have commented previously, there is increasing evidence that the downstream market for vitamin D testing is flattening in US Dollar terms, regardless of any pandemic effects.”

- Perhaps the market for vitamin D really is flattening.

- BVXP has for some time predicted demand for vitamin D testing might “plateau”.

- Within the FY 2019 results, BVXP said: “This is clearly evidenced by a number of our vitamin D customer revenue streams which, after a period of significant growth now appear to have reached a plateau.”

- Within the FY 2018 results, BVXP said: “Whilst actual royalties received were once again in excess of expectations, we nevertheless perceive a plateauing of the vitamin D testing market.”

- Within the FY 2017 results, BVXP said: “Our prudent belief is that the vitamin D market will plateau in the near future.”

- Management provided some useful insights into vitamin D during a ShareSoc webinar:

- During the webinar, management implied the plateauing of vitamin D demand meant the annual growth rate could reduce from 20%-plus to between 5% and 10% — to match the global expansion of the wider antibody market.

- Management also claimed vitamin D testing was “here to stay”.

- Here is my best transcription of the webinar’s key vitamin D comments:

“I think there’s been a degree of interest in vitamin D and its association with coronavirus patients and how they perform in hospitals, so there might be some extra testing taking place through medical curiosity and the gathering of research.”

“That underlines an important observation, that 20 years ago, vitamin D was thought of as being something associated with rickets and that was pretty much it, but 10 years ago vitamin D changed and was perceived as something much more fundamental to human biology, the biology of the immune system and the biology of northern-latitude diseases.”

“The fact that there is quite a lot now in the media about vitamin D and its link with coronavirus underlines yet again that vitamin D is not some trivial hormone, but a fundamental part of human biology and that being the case, I think vitamin D testing is going to be here to stay. It’s not a fad, because it is so intwined with human biology. So whilst vitamin D is so important to us, I don’t sense any degree of vulnerability… because I see vitamin D testing going on for a long period of time.”

Troponin

- BVXP once again admitted future growth was dependent mostly on demand for its new troponin antibody:

“Over the next few years, the commercial development of the new troponin assays will have the most significant influence on Bioventix sales. There are no antibodies in the future pipeline that are comparable to our troponin product in clear potential value and that have the ability to influence revenues in the next few years.”

- Revenue from the troponin antibody — used to help detect potential heart attacks — gained 175% to represent 3% of total group income:

“Total troponin sales from Siemens Healthineers and another separate technology sub-license were £0.33 million (2018/19: £0.12 million). This significant increase clearly demonstrates a gathering momentum of product roll-outs for the new high sensitivity troponin assays supported by SMAs and we believe that these revenues will continue to grow in the next financial years.”

- This FY 2020 statement did not repeat the “below our expectation” message about troponin contained within March’s interims.

- My H1 write-up included an “understanding” that BVXP expected troponin sales of £500k for FY 2020.

- My “understanding” was clearly optimistic given actual troponin sales were £330k.

- Management provided some useful insights into troponin during the ShareSoc webinar.

- In particular, troponin revenue reaching £1.2m during FY 2022 — to replace lost income from another product — is apparently “entirely plausible”.

- Troponin revenue going from £330k to £1.2m in two years is equivalent to 90% growth this year and next.

- Here is my best transcription of the webinar’s key troponin comments:

“During 2018 and 2019 [Siemens] slowly rolled out this new [troponin] test replacing the old test… it has been a slow and steady process and it has been very pleasing to see the steady increases in that rollout and the consequent royalties and revenue we have enjoyed as a result of that… they have gone up very significantly in the last financial year. I can foresee yet more growth in the current financial year 2020/21”

“The key milestone… will be 2021/22, whereby troponin revenue replaces the [expiring] NT proBNP revenue, so £1.2 million, so… that is a key milestone that is entirely plausible. Our friends at Finncap predict revenues that are around £3m for troponin going into the future.”

“There is a clear new application for troponin testing, which is in addition to the current application, which is chest pain in accident and emergency clinics. This [new application] relates to people who have had some form of cardiac event but are regular visitors to their cardiologist for routine follow-ups.”

“Troponin levels when measured on those people [who have experienced a cardiac event] enable cardiologists to stratify the risk of those patients into low, medium and high of a secondary event, which enables the cardiologist to better allocate their time and resource to the people who need it and also consider in more detail the therapy of people who are at risk of an impending secondary event.”

- Management also confirmed during the webinar that troponin revenue would terminate during the summer of 2032.

Other antibodies

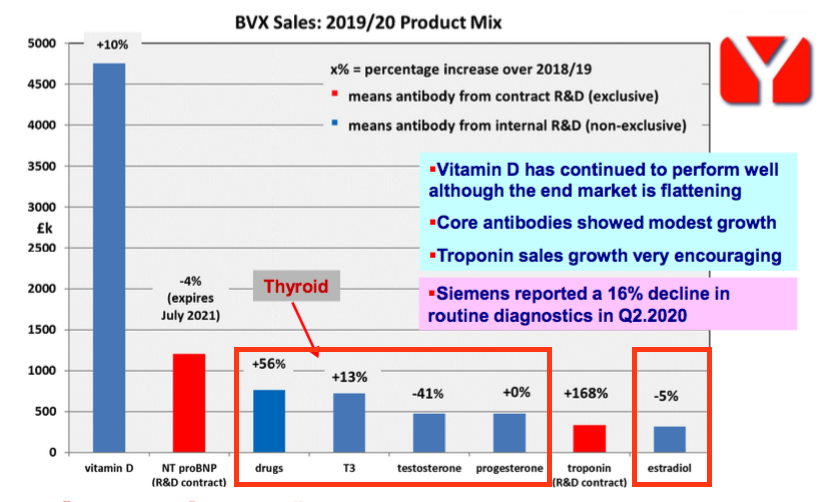

- The results RNS and accompanying powerpoint said nothing about the progress of BVXP’s other “lead” antibodies, other than to show their respective revenue performances:

- Changes ranged from +56% to -41% and overall revenue remained at approximately £2.7m.

- The ShareSoc webinar did yield this management insight about these five other products:

“Each year they will tend to go up and down, but if they are grouped together as a core, they tend to go up by 5 to 10% per annum and I think that will be the pattern for the future going forwards.”

- My numbers show the five antibodies have lifted their collective revenue by 69% between 2016 and 2020:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue | |||||

| Testosterone (£k) | 512 | 574 | 660 | 800 | 480 |

| T3 (£k) | 372 | 495 | 460 | 640 | 720 |

| Drug testing (£k) | 323 | 485 | 640 | 490 | 760 |

| Estradiol (£k) | 256 | 333 | 290 | 330 | 320 |

| Progesterone (£k) | 159 | 178 | 400 | 470 | 470 |

| Total (£k) | 1,623 | 2,064 | 2,450 | 2,730 | 2,750 |

- These results confirmed revenue from NT proBNP will expire during July 2021. That income represented 12% of the top line, and the aforementioned webinar comments claimed the revenue shortfall could be recouped entirely by troponin:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue | |||||

| Vitamin D (£k) | 2,218 | 2,750 | 3,400 | 4,300 | 4,800 |

| Troponin (£k) | - | - | - | 120 | 330 |

| Other 'lead' antibodies (£k) | 1,623 | 2,100 | 2,450 | 2,730 | 2,750 |

| Contract NT proBNP (£k) | ?? | 610 | 1,050 | 1,250 | 1,200 |

| Terminated product (£k) | 800 | 1,000 | 125 | - | - |

| Other (£k) | 877 | 786 | 1,727 | 890 | 1,234 |

| Total (£k) | 5,517 | 7,246 | 8,752 | 9,290 | 10,314 |

- The NT proBNP shortfall could be recouped instead by revenue from troponin and all other sources rising 6-7% during both FY 2021 and FY 2022.

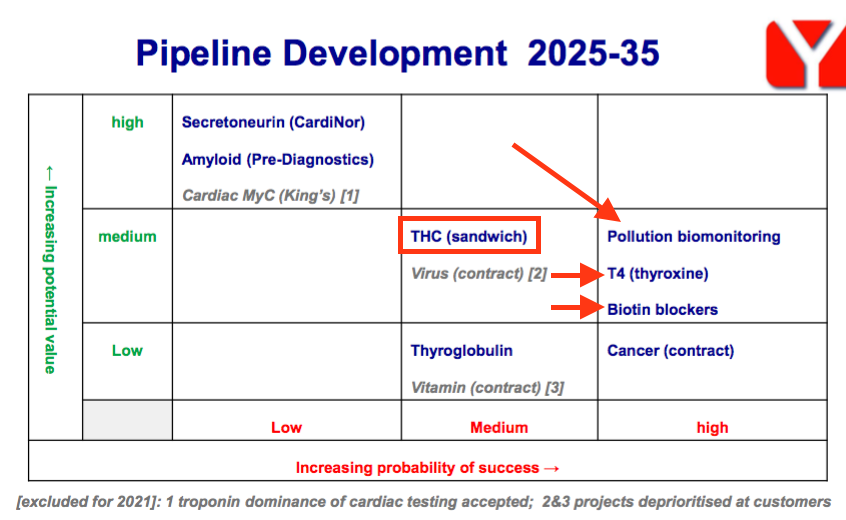

Pipeline developments

- The results powerpoint showed a re-arranged product pipeline grid:

- THC (sandwich) is a pipeline newcomer and tests for marijuana through saliva.

- T4, biotin and pollution monitoring have all had their probabilities of success upgraded from medium to high…

- …but the potential value of pollution monitoring has been downgraded from high to medium.

- BVXP said it was “particularly pleased with the progress of the pollution exposure project”. The associated kit measures atmospheric pollutants within individuals through urine samples:

- Management explained on the ShareSoc webinar that pollution studies presently employ fixed airborne sensors, the data from which can’t really be correlated to particular medical conditions.

- However, BVXP’s tests will allow researchers to measure an individual’s pollution level, cross-check it with existing medical conditions and therefore provide “much stronger research conclusions”.

- Among all of BVXP’s pipeline ventures, pollution monitoring appears the most likely to become a commercial product. Webinar commentary on pollution lasted for seven minutes, versus five minutes for troponin and four minutes for the rest of the pipeline.

- Exactly which products (if any) from the pipeline make it to market remains anyone’s guess. For perspective, the troponin antibody took more than ten years in development/testing before its commercial launch.

Other webinar remarks

- The ShareSoc webinar revealed a few useful snippets:

- On competition:

“The competition really is the antibody creation departments at the customers, so Abbot, Roche, Siemens, Beckman… they all have labs just like ours and really capable people, that make antibodies and embrace technology, and so ultimately that is the competition.”

“We are pretty much on our own with sheep monoclonal antibodies.”

- On why some antibodies are sold in physical batches and some collect a royalty:

“The way physical antibodies work is largely a function of the downstream [blood] test. Some downstream tests are incredibly efficient… and use tiny, tiny quantities per test, and for those tests, the balance of the physical antibody versus the royalty you achieve from the sale in dollars per test is vastly weighted towards the royalty, and that’s part of the rationale of having the royalty in the first place.”

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue | |||||

| Royalty and licence fee income (£k) | 4,128 | 5,321 | 5,492 | 6,280 | 6,265 |

| Product revenue and R&D income (£k) | 1,389 | 1,925 | 2,487 | 3,010 | 4,089 |

| Back-dated royalty income (£k) | - | - | 772 | - | - |

| Total (£k) | 5,517 | 7,246 | 8,752 | 9,290 | 10,314 |

- On customer ordering:

“Some customers order the same amount month after month after month and have a regular ordering pattern dictated by their SAP system, but there are other customers… who might buy two or three years’ worth of stock in one delivery, and they receive and freeze it and use it over a period of time.”

- On the impact of any management change:

“One thing that would not change is the revenue trajectory, which… is governed by Siemens, Roche and Abbot continuing to do what they will do anyway… So [new leadership] might affect things in 2025-2035… and beyond that… but we don’t insure against [the loss of the chief exec] because there would not be any financial hit for a long period of time.”

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Financials

- BVXP’s accounts remain in extremely good shape.

- Cash conversion in particular continues to be excellent:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit* (£k) | 4,205 | 5,691 | 6,060 | 6,931 | 8,184 |

| Depreciation (£k) | 42 | 39 | 58 | 76 | 134 |

| Cash capital expenditure (£k) | (21) | (22) | (108) | (85) | (340) |

| Working-capital movement (£k) | (581) | (570) | (539) | (47) | 412 |

| Net cash (£k) | 5,380 | 6,167 | 6,987 | 6,537 | 8,076 |

(*before back-dated royalties)

- The cash position was bolstered by £1.5m after operating cash flow of £7.7m and option proceeds of £0.9m together funded a £0.3m lab revamp, a further £0.2m partner investment and dividends of £6.5m.

- The £8.1m year-end cash position exceeded the £5m that BVXP stated was “sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future and to provide comfort against the ongoing impact of the pandemic and any economic uncertainty arising from it.”

- The £3.1m difference between the £8.1m cash position and the £5m “comfort” buffer equates to 59p per share — and compares to the 53p per share special dividend declared within these results.

- The fifth consecutive year of declaring a special dividend re-emphasised how BVXP seemingly grows on thin air.

- Since 2015, BVXP’s earnings have advanced £4.6m to £7.2m, while shareholder equity (i.e. earnings less all dividends declared) has advanced £5.9m to £12.5m:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Earnings (£k) | 2,557 | 3,494 | 4,922 | 5,663 | 5,859 | 7,203 |

| Shareholder equity (£k) | 6,584 | 8,207 | 10,144 | 11,011 | 10,826 | 12,521 |

- The resultant incremental return on equity is an astounding £4.6m/£5.9m = 78%.

- Bolstered in part by the aforementioned foreign-exchange gain, BVXP’s FY 2020 operating margin reached an incredible 79.4% — a new record:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating margin* (%) | 76.2 | 78.9 | 76.0 | 74.6 | 79.4 |

| Return on average equity (%) | 47.2 | 53.6 | 47.5 | 53.7 | 61.7 |

(*before back-dated royalties)

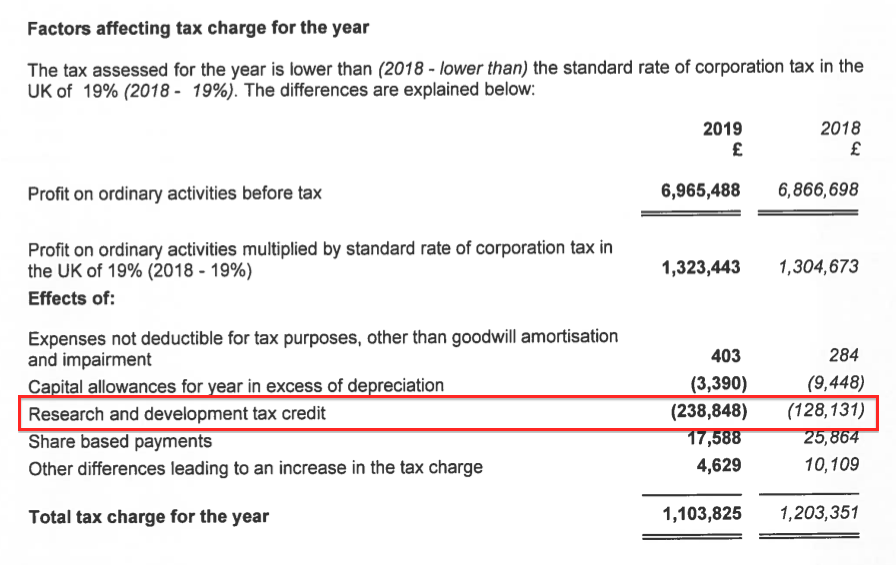

- The accounting tax charge this year represented just 12% of pre-tax profit:

- The 2019 annual report (point 5) disclosed BVXP benefitting from R&D tax credits:

- The forthcoming 2020 annual report will reveal the scale of any R&D tax credit and perhaps explain the 12% rate.

- The 12% tax charge compares to the 15-18% applied during the preceding ten years, and the standard UK 19% rate.

- The 2020 annual report small-print may suggest a 12% rate is unsustainable.

- The balance sheet carries no bank debt and no pension complications.

Valuation

- BVXP’s immediate outlook was relatively positive:

“The core business is linked to routine testing at hospitals around the world and this has undoubtedly been affected by the COVID-19 pandemic. The timing of a return to normality is uncertain but when it does, we expect our business will revert to an established trajectory, albeit without the income from NT-proBNP which will cease from July 2021. Regardless of the pandemic effects, we anticipate the continued roll-out of the high sensitivity troponin assays and the royalties associated with this.”

- BVXP also noted foreign-exchange gains could reverse during the current year:

“[T]he weakening of the US Dollar from 30th June 2020 to August 2020 (1.23 to ~1.32) will have a negative effect, currently estimated to be approximately £0.15 million on our 2020/21 results. We have no current plans to institute any hedging mechanisms and therefore any future changes in exchange rates, up or down will impact our reported Sterling revenues accordingly.”

- Excluding foreign-exchange movements, BVXP’s trailing operating profit is £8.0m.

- The £8.0m profit taxed at the average 15% applied during the last five years gives earning of £6.8m or 130p per share.

- BVXP’s £8.1m cash position equates to 155p per share and is not that meaningful for valuation purposes in light of the £5m “comfort” buffer, the regular payment of ‘surplus’ cash as special dividends and the £41 share price.

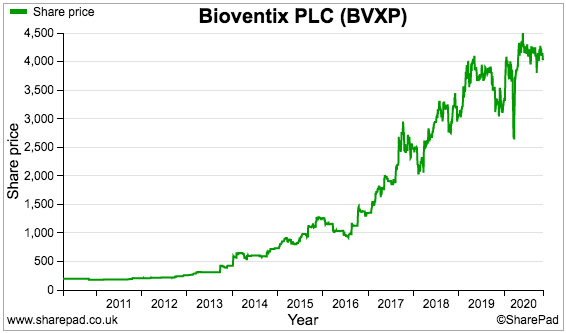

- Dividing the £41 share price by my 130p per share earnings estimate gives a trailing P/E of 32.

- The rating remains understandably lofty.

- BVXP’s appealing accounts certainly justify a premium multiple.

- But the raw numbers tell only part of the story — the elevated valuation also reflects the ongoing predictability of customers using BVXP’s antibodies.

- If I understand correctly, competing antibodies have to be much more effective than those made by BVXP to justify the protracted development/regulatory timescale required for commercialisation.

- And even if a much more effective antibody is approved and launched, not all of BVXP’s customers may be able to use it because of contractual, technical or other restrictions.

- In the meantime, BVXP collects steady royalties from existing antibodies while shareholders cross their fingers that troponin takes off and the pipeline delivers a winner.

- BVXP’s past presentations had included house-broker forecasts for the upcoming year:

- The inclusion of these forecasts was unusual and very commendable — companies typically don’t endorse broker projections just in case the projections are not met.

- However, BVXP’s latest presentation did not include a house-broker forecast for the upcoming year.

- I trust BVXP has not suddenly become wary of its near-term performance.

- Mind you, broker forecasts (at least according to SharePad) are hard to find at present:

- The full-year 88p per share ordinary dividend supports a 1.9% yield.

- Given BVXP has distributed all of its earnings as ordinary and special dividends since 2016, then perhaps the 3.2% yield based on my 130p per share earning guess is a more appropriate measure.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Excellent summary as usual – many thanks Maynard.

The success of Troponin is clearly the key to future growth (or not) but in the meantime am happy to take comfort in the track record / strength of balance sheet / returns to shareholders.

Thanks Peter. Glad you found the post useful.

Maynard

According the Johns Hopkins public health dept research, troponin may also have a role in stratifying risk in type 2 diabetes and selecting patients for sglt2 therapy…would greatly expand the market for troponin.

also should commend you, Maynard on your thorough analysis

Thanks John, I did not know the diabetes angle to troponin. Sounds positive. Glad you found the post useful.

Maynard

Hi Maynard,

Thanks for the review of BVXP. I really appreciate your detailed analysis and thoughts.

I’m a big fan of this company and I particularly like the CEO and his approach to the business. For a company that is so profitable they appear to retain a laser-like focus on costs. Nice alignment between management and shareholders here.

The pollution exposure project looks interesting. I don’t really understand the science behind this business but it looks to be a move away from the blood testing antibody development programme and commercialisation. Although it sat within the 2025 – 2035 commercialisation part of the matrix, I wonder if this would start to see revenues sooner than that? They mentioned aiming a product concept test at worker biomonitoring in a H&S setting during 2021. So I would potentially expect revenue generation sooner in this case – but what do I know!!!

Re withdrawal of Finncap guidance in BVXP presentation; I have read a broker note recently which indicated they have withdrawn guidance due to the COVID19-related disruption to testing. On the basis that this leads to poor visibility on customer royalty streams. It sounds like a bit of a cop-out to me as there is never any real visibility on the royalty revenue streams (as it is out of BVXP control).

Question, do you know how BVXP audits the correctness of the royalty downstream income from Siemens etc? It must be a concern, especially if receiving from countries with questionable records on data transparency (e.g. China).

Thanks very much

Hi James,

Thanks for the comments. Glad you found the post useful.

Pollution — yes, I agree some revenue will probably occur sooner than 2025, or at least that is the impression given by management. Revenue may be small initially, but it will be revenue nevertheless.

Finncap guidance — ok, just goes to show broker notes generally are a City charade of just parroting the RNS and going back and forth with estimates until management is happy. When times are uncertain and shareholders require greater insight, brokers go awol.

Audit — good question, and I am not entirely sure. I understand (at least with the previous FD) that audits don’t happen and Siemens etc just give BVXP the figures and pay the bill. I understand BVXP has the right to audit the customers. but whether the cost/benefit is worth it I do not know. Management has been asked about China and payments in the past on a PI World video (I think) and there was a reassuring reply (which I can’t remember).

Maynard

Hi Maynard,

I was surprised to read that Troponin royalties will expire in 2032, I don’t believe I have heard the company say this before. After the issues around proBNP expiring and the associated loss in revenue, I seem to recall somewhere previously that Peter had implied that future royalty contracts would be made on a perpetual basis?

Are you aware of any other categories that are due to expire?

Thanks,

Gavin

Hi Gavin

Thanks for the comment. Yes, I seem to recall PH saying something about perpetual contracts on a PI World video (I think) at some point. Bear in mind development for troponin started in c2006, so royalty agreements may have been decided years ago when BVXP was not in the position it is today. I would like to think deals agreed today would have perpetual royalties, but I confess I do not know. I do not know either if any other products are due to expire. PH has flagged the 2021 expiry of the NT proBNP R&D contract since at least 2018, and I would have thought any other forthcoming expiries would be flagged as well.

Maynard

Hi Maynard,

Thanks very much for your comprehensive write up of Bioventix.

The Siemens statement that the routine global IVD market suffered a 15-20% reduction in activity during the period April to June 2020 was very worrisome.

To put that into perspective, having worked in the diagnostics industry for 30 years, albeit last century, I have never seen a drop of that magnitude. In fact the diagnostics industry has chugged a long at a very reasonable growth rate of 5-7% for half a century up until last year. Clearly a lot of hospitals in the western world have reduced diagnostic testing for the first time ever and by significant amounts.

Just imagine if a financial commentator in 2019 had said, oh there’s going to be a pandemic next year and hence we are going to cut our holdings in companies supplying healthcare and diagnostics to hospitals. I suspect there would have been some ribald comments in the analyst community.

So I took Peter Harrison’s inclusion of the Siemens statement and his subsequent comment: “we can see clear evidence from our physical product sales during this Q2.2020 period that corroborate such a pandemic effect.” as a profit warning.

Yes, there will be increased use of vit D tests in a research setting ( there is remarkable progress in using vit D in the treatment of Covid but the studies are still very limited, numbering just 50 patients, https://www.sciencedirect.com/science/article/pii/S0960076020302764) but not enough to offset the effect.

I still think that Bioventix will be a brilliant investment for the future, the point that you make that BVXP has therefore distributed its entire FY 2016-2020 earnings (529.2p per share) as ordinary/special dividends is remarkable. Do you know of any other company that has achieved that? However the next year might be a bit bumpy.

Roger

Hi Roger

Thanks for the comment and I trust you are keeping well.

So I took Peter Harrison’s inclusion of the Siemens statement and his subsequent comment: “we can see clear evidence from our physical product sales during this Q2.2020 period that corroborate such a pandemic effect.” as a profit warning.

Yes, the growth rate moderated in H2 but I did not interpret PH’s comments as a profit warning — at least, not in the usual way of earnings being 20% down on what was expected. I got the impression BVXP may financially tread water during 2021, but that may prove optimistic if the 15-20% reduction is not recouped. Mind you, I am not sure why diagnostic testing would now be rebased to a lower level after so many years of 5-7% annual growth. The loss of BVXP’s proBNP income is also on the horizon.

Glad you still think BVXP will be a ‘brilliant investment’! From memory, Admiral and perhaps Hargreaves Lansdown have delivered similar dividend performances.

Maynard

Bioventix (BVXP)

Publication of 2020 annual report

1) Risks

Four years after the Brexit vote, this is the first formal mention of a Brexit risk in a BVXP annual report:

Four lines to outline the Covid-19 risk compares to two pages at FW Thorpe.

2) Section 172

New for 2020, and contained no revelations:

3) Corporate governance

New text for 2020 that suggests extra “engagement” details will be published in the future:

More new text indicating BVXP’s board may become less informal:

I never liked the outsourced/non-exec FD being in charge of the audit committee:

A change of FD has since taken place and I await the update to the audit committee membership.

4) Director pay

No real issues with director pay given the company’s performance. The chief exec’s pay increased by 7% and his bonus represented 40% of his basic pay (2019: +6%, 57%):

Interesting confirmation that the outsourced/non-exec FD retired at the end of March. Her last job for BVXP was to correct the half-year results.

This table contains multiple errors:

The £13.50 options were granted in 2017. Does note make sense the chief exec can exercise 18,500 options that were granted in April 2020 with a stated exercise period of 2023-2030 (here is the relevant RNS)

Corporate-governance standards dictate non-execs should not be awarded options, but such awards at BVXP have not hurt the company’s progress to date.

5) Key audit matters

A reminder that customers self-declare revenue:

Possibly something about nothing, but unlike 2019, the auditor this year did not include the text “and we consider the disclosures surrounding investments to be appropriate”:

The investment disclosure did not look untoward to me:

Bear in mind these investments are Norwegian and their GBP value fluctuates with NOK.

6) Audit

Materiality a standard 5% of pre-tax profit:

100% scope, too:

7) Revenue recognition

Minor revenue-recognition change for 2020:

8) Audit fees

Super-low audit fees:

No fee increase as well, unlike at FW Thorpe and Tristel.

9) Employees

Nothing too concerning here:

Average cost per employee up £4k (6%) to a record £69k, but average revenue per employee up £64k (11%) to a very impressive £645k. Employee costs as a proportion of revenue fell from 11.3% to 10.7% — the lowest percentage since BVXP first disclosed employee details in 2009.

10) Tax calculation

Highlighting this in the hope somebody who knows about tax can explain the tax credit due to share options:

11) Stocks

Stock represents a tiny 2% of revenue:

Versus cost of sales of £828k, average stock turn for the year was 3.4x, suggesting stock took a timely 3.4 months to sell. Previous years had seen stock waiting for 5 months.

12) Debtors

For the first time since 2007, the level of prepayments and accrued income declined year-on-year:

BVXP carries significant accrued income — which reflects revenue earned during the period but where the customer had not yet been invoiced at the balance-sheet date.

(Trade debtors reflect revenue earned during the period where the customer has been invoiced).

This accrued income relates to the company’s collection of royalties. From the 2016 results narrative:

“Approximately three quarters of Bioventix sales are generated from customer royalties. These are based on our customers’ global sales which are then factored by a royalty percentage and then sent to Bioventix around 2 months after the end of each half year.”

BVXP’s customers inform (or “self declare”) BVXP of their global sales after the period end, and BVXP then invoices the customers for the appropriate royalty sum.

As such, the payment to be collected is deemed to be accrued income — i.e. the revenue in question had been earned — but had not been invoiced — at the balance-sheet date.

Anyway, the year-end prepayment and accrued income figure for 2020 is equivalent to 48% of royalty revenue, which compares to between 51% and 56% for 2014-2019.

This lower percentage is favourable for BVXP — i) less money is owed by customers and ii) a lower proportion of reported revenue is based on income that had not been invoiced at the balance-sheet date.

Average trade receivables for the year were 6.5% of revenue, in line with the 6-9% seen since 2011

13) Creditors

Nothing amiss here:

Total creditors represent 7% of revenue, much of which are tax related.

14) Options

56k options represent just 1% of the share count:

Maynard