11 December 2020

By Maynard Paton

Results summary for System1 (SYS1):

- A pandemic-disrupted first half, albeit with headline numbers that disguised a remarkable return to profitability during Q2.

- Revenue improvements within the Communications and UK segments suggest the tie-up with ITV is working.

- A bold pricing structure, greater ambition clarity and even improved film-making may explain why adidas has become a client.

- The accounts are in reasonable shape, with significant net cash, positive cash generation and perhaps a decent profit margin following various cost savings.

- Extrapolating the Q2 profit leads to a lowly 8x multiple and intriguing recovery/upside possibilities. I have bought more shares.

Contents

- Event links, share data and disclosure

- Why I own SYS1

- Results summary

- Coping with Covid-19

- Revenue and profit

- Divisions and geographies

- Test Your Ad

- Achtung!

- Financials

- Valuation

- Portfolio trade

Event links, share data and disclosure

Event: Interim results and presentation for the six months to 30 September 2020 published 17 November 2020

Price: 185p

Shares in issue: 12,659,784

Market capitalisation: £23.4m

Disclosure: Maynard owns shares in System1. This blog post contains SharePad affiliate links.

Why I own SYS1

- Market-research agency that predicts the effectiveness of television adverts, with progress resting upon “the most accurate tool available for predicting long-term, brand-building, profitable growth.”

- Boasts founder/entrepreneurial/owner-friendly chief exec who has overseen acquisition-free growth, retains a 23%/£5m shareholding and has declared five special dividends.

- Conversion from consultancy work to supplying data alongside a deal with ITV plus a remarkable return to profit leads to tantalising recovery possibilities.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

Coping with Covid-19

- Annual results published during June had already warned this H1 performance would be disrupted by the pandemic.

- SYS1 admitted at the time:

“In the two months to end May, Revenue and Gross Profit were 36% and 38% respectively below the same period of last year. Over these months the business as a whole incurred a Pre-Tax loss of some £0.7m as we pursued our short-term objectives of continuing to develop our new automated product set, while conserving cash by shrinking the cost base to offset lower sales.”

- The losses arising during April and May led to the axing of the dividend, the furloughing of staff and the deferral of 20% of board salaries.

- A trading statement during October then implied a remarkable profit recovery had occurred.

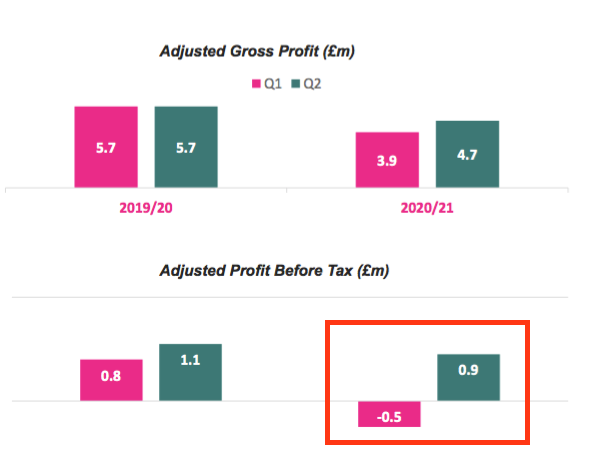

- October’s update signalled a £0.6m pre-tax, pre-impairment profit for this H1, which suggested June, July, August and September had registered an astonishing £1.3m pre-tax, pre-impairment profit versus the £0.7m loss for April and May.

- Sure enough, the results presentation confirmed the return to profitability for Q2:

- These results actually declared a £0.4m adjusted pre-tax profit for the half — £0.2m less than was signalled within October’s update due to additional adjustments (see Revenue and profit below).

- SYS1 said trading had indeed picked up after May:

“From June, as sales began to recover, arrangements put in place to reduce employees’ hours were progressively reversed, and the partial deferral of some senior employees’ salaries ended in August. In summary, the business emerged from H1 stronger than it started, with Q2 Revenue, adjusted Profit Before Tax and Net Cash well up on the preceding quarter.”

- But the general outlook was cagey:

“[C]ontinued uncertainty over the medium- and longer-term impact of Covid-19 on the major economies in which System1 operates, heightened by recent “lock-down” measures, leads us to continue to suspend financial guidance.”

- The dividend remains suspended, too.

- SYS1 said the “widespread adoption of new ways of working” during the pandemic had prompted the closure of certain overseas offices, with the associated staff now working from home.

- SYS1 reckoned reduced office requirements should lead to annual savings of £0.4m.

- This H1 also witnessed a 12% reduction to the workforce.

- The cost reductions and remarkable Q2 profit rebound may be related to the appointment of a new finance director during April…

- …although few would have said at the time recruiting an FD once fined by the FCA and FRC was very promising.

- During the half SYS1 received government benefits of £0.6m, mostly from the United States.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue and profit

- SYS1 used the word “disappointing” to describe this H1 financial performance.

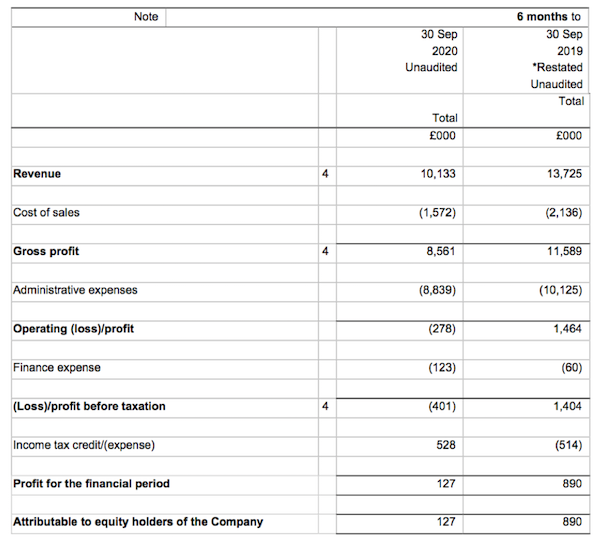

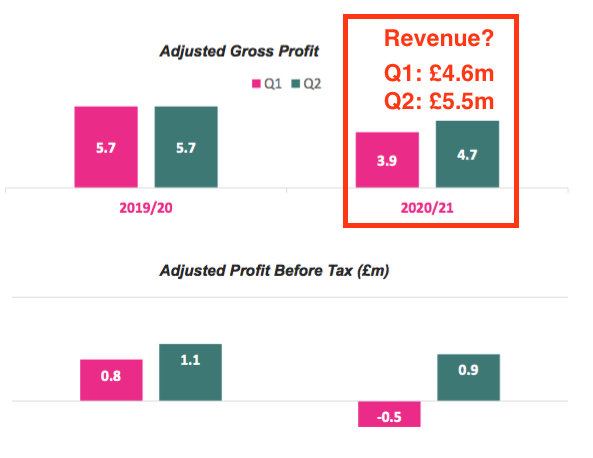

- Revenue fell 26% and led to a reported loss:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Revenue (£k) | 13,182 | 13,717 | 13,182 | 13,714 | 10,133 | ||

| Operating profit (£k) | 1,128 | 928 | 1,464 | (1,046) | (278) |

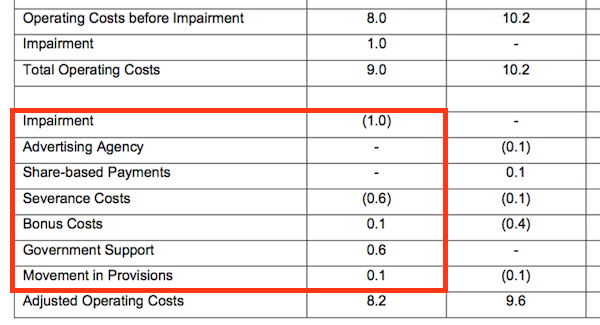

- The results were complicated by a number of adjustments:

- The £1m impairment related to the aforementioned office closures and is arguably a one-off charge.

- The £0.6m government support is I trust a one-off benefit.

- Severance costs of £0.6m could be deemed one-off, but SYS1 has recorded severance costs every year since 2012 that have totalled £2m.

- Reversing the bonus and provision gains seems a sensible adjustment.

- Taking the adjustments at face value, adjusted operating profit dived 79% to £0.4m.

- SYS1’s start-up Test Your Ad service (formerly ‘AdRatings’) hampered the interpretation of the performance.

- During FY 2019 and FY 2020, £5m was spent developing Test Your Ad in exchange for revenue of only £56k.

- SYS1 had previously reported progress including and excluding Test Your Ad expenditure, but these results were the first not to disclose Test Your Ad’s financials.

- However, the commentary on Test Your Ad did appear relatively positive (see Test Your Ad below).

- Trying to guess the contribution from Test Your Ad during this H1 versus the comparable H1 is thankfully not that necessary given the aforementioned level of adjusted Q2 profitability and the group’s market cap (see Valuation below).

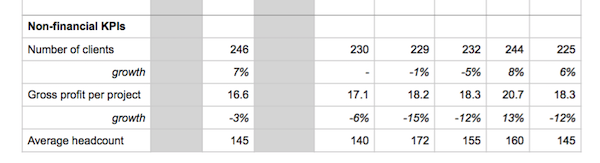

- Note, too, that these results did not disclose various KPIs that were previously regular results fixtures:

Divisions and geographies

- SYS1 operates three market-research divisions.

- The most attractive division is Communications, which evaluates television adverts and which SYS1 has previously claimed has:

“developed market-research techniques [that]… are better able to predict the long-term effectiveness of advertising than anyone else.”

- The Brand division tracks ongoing client-brand popularity, while the Innovation division tests new marketing concepts.

- The Communications division offers the widest potential ‘moat’ to shareholders.

- The fledgling Test Your Ad service — on which SYS1 is pinning its longer-term hopes — is part of Communications.

- Brand has in the past been the more reliable of the three income sources, while Innovation caters for ad-hoc work and is the most unpredictable.

- The table below summarises the revenue contributions from each department:

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 | |||

| Comms (£k) | 3,606 | 4,870 | 4,068 | 4,987 | 4,054 | ||

| Brand (£k) | 2,363 | 2,622 | 2,311 | 2,326 | 1,701 | ||

| Innovation (£k) | 6,166 | 5,029 | 5,824 | 4,005 | 3,864 | ||

| Other (£k) | 1,047 | 1,196 | 1,522 | 432 | 514 | ||

| Total (£k) | 13,182 | 13,717 | 13,725 | 11,750 | 10,133 |

- Communications was the only division to have delivered revenue higher during this H1 than the H1 of two years ago.

- Revenue from Communications represented 40% of total revenue during this H1, versus 27% two years ago.

- Innovation revenue during this H1 dropped 33% as new marketing concepts were put on hold during the lockdown.

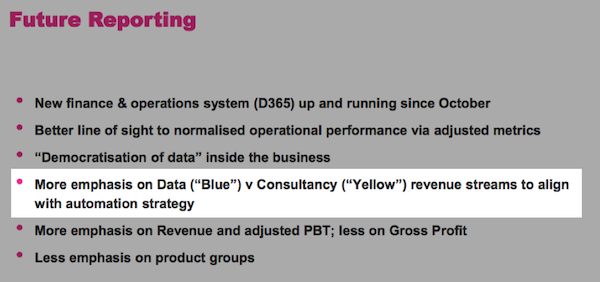

- The presentation hinted that the divisions may soon consolidate into just Data and Consultancy:

- Somewhat astonishingly, UK and Asia-Pacific (APAC) revenue both managed to improve during this H1:

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 | |||

| Americas (£k) | 5,562 | 6,098 | 7,177 | 5,613 | 3,618 | ||

| UK (£k) | 2,952 | 3,644 | 2,758 | 2,757 | 2,983 | ||

| Europe (£k) | 3,653 | 3,117 | 3,048 | 2,580 | 2,536 | ||

| APAC (£k) | 1,015 | 858 | 742 | 800 | 996 | ||

| Total (£k) | 13,182 | 13,717 | 13,725 | 11,750 | 10,133 |

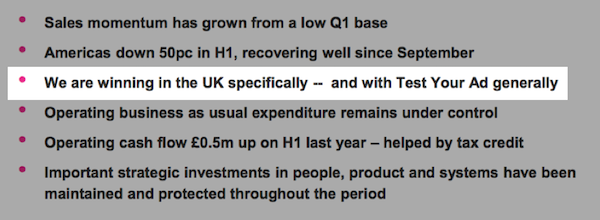

- Americas revenue almost halved, due in part to the region’s three largest clients reducing their budgets.

- Wishful thinking perhaps, but the out-performance of Communications and the UK may be linked to ITV’s involvement with the Test Your Ad service (see Test Your Ad below).

- This presentation bullet-point was encouraging:

Test Your Ad

- The revamped Test Your Ad website describes the service as “the most accurate tool available for predicting long-term, brand-building, profitable growth”.

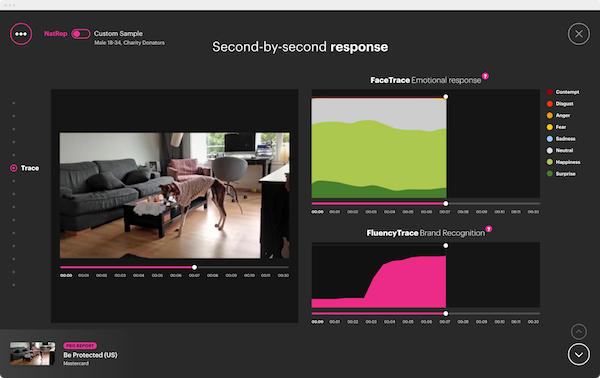

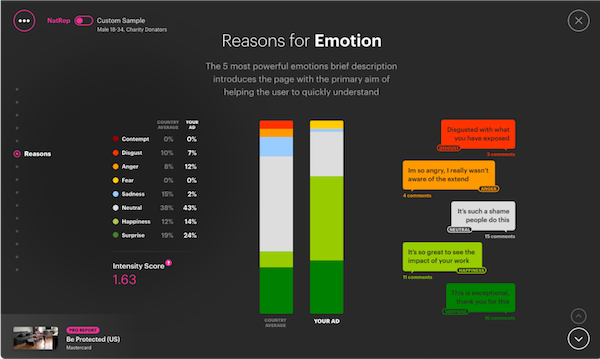

- Test Your Ad captures the second-by-second responses to television adverts from 150 members of SYS1’s online panel:

- According to SYS1, the greater the panel’s ‘feel-good’ response, the more likely the advert will generate long-term additional sales:

- At least two years of Test Your Ad development had resulted in scant extra revenue and significant losses.

- But a tie-up with ITV at the start of 2020 appeared to validate the Test Your Ad philosophy, data and conclusions.

- Finally… a large organisation (ITV) had determined Test Your Ad was actually useful!

- The pandemic unfortunately led to the axing of a SYS1-ITV summer advert competition.

- But client interest in Test Your Ad — albeit from a small base — appears to have grown.

- The following remark from this H1 statement was very encouraging:

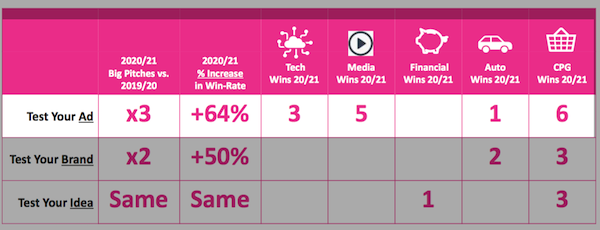

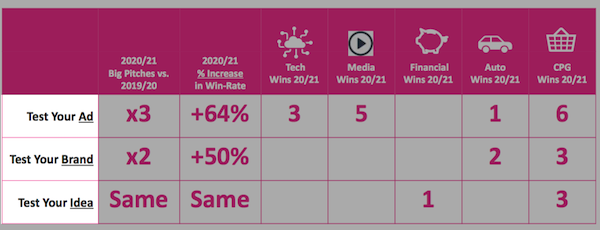

“…the high new business win-rate of our Test Your Ad predictive products…”

- The win-rate actually jumped 64% on three times as many “big pitches”:

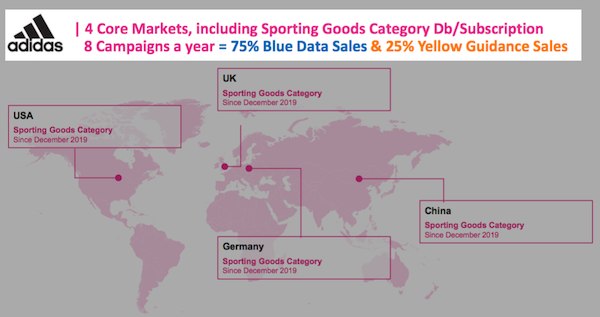

- New clients apparently include adidas:

- I am convinced ITV’s involvement has sparked this much-needed attention towards Test Your Ad.

- After all, ITV has links with many more deep-pocketed advertisers than SYS1…

- …and the broadcaster’s new desire to show more effective ads must have some bearing within the industry.

- ITV’s Q3 update encouragingly showed advertising spend returning to almost 2019 levels…

“We saw advertising trends improve in Q3 with total advertising spend down 7% year on year. July was down 23%, August up 3%, September down 2% and October down 1% compared to the same periods in 2019. September and October were against the Rugby World Cup in 2019. A number of categories spent more year on year in Q3 including FMCG, Supermarkets, Publishing and Broadcasting, Telecommunications, Food, Government, Charities and Other, and Household Stores.“

- …which seems to tie in with SYS1’s much better Q2 (July August and September).

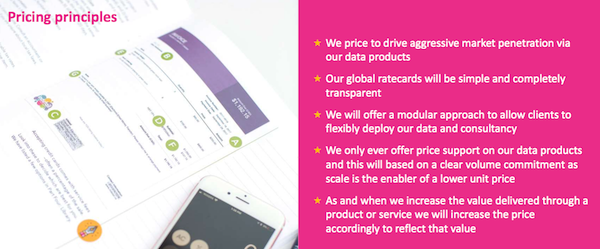

- A very promising development is SYS1’s Test Your Ad pricing:

- SYS1 is going all out to disrupt the ad-testing market with low, simple and transparent pricing.

- I am all for this ‘challenger’ proposition — assuming of course Test Your Ad really is better, faster and cheaper than the established alternatives.

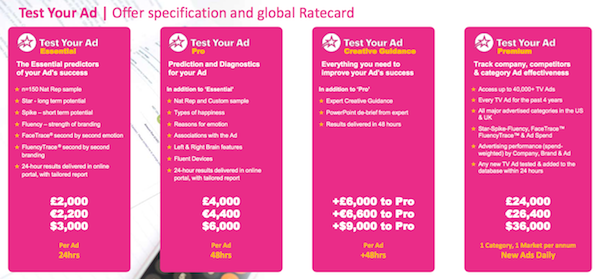

- SYS1 even published its Test Your Ad rate card:

- The Test Your Ad pricing reminded me of the 2019 SYS1 AGM, when management was quizzed about the lack of Test Your Ad progress:

“Potential clients were apparently not interested in the [Test Your Ad] service as the price was ‘too cheap‘ — with the implication that the service would be poor.”

“The low cost of AdRatings [now Test Your Ad] meant the service did not reach the attention of chief marketing officers (CMOs) — who could not justify their time evaluating a £12k/year service. ‘Needs to be £50k/year to be credible‘.”

- The rate-card publication suggests the pricing issue has now been resolved — or at least accepted by SYS1 that clients will still have reservations.

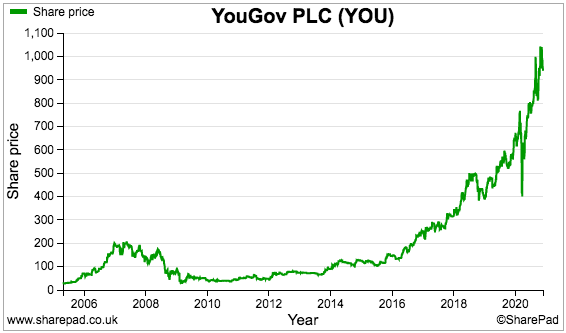

- Revisiting those AGM notes also reminded me of SYS1’s ambition for Test Your Ad — “to become the ‘YouGov of advertising data’.”

- This H1 statement said SYS1 continued to invest in “a new generation of highly predictive, lower cost, automated products” — which I hope will help the company’s YouGov ambition.

- YouGov’s share price implies the approach is a fine one to adopt:

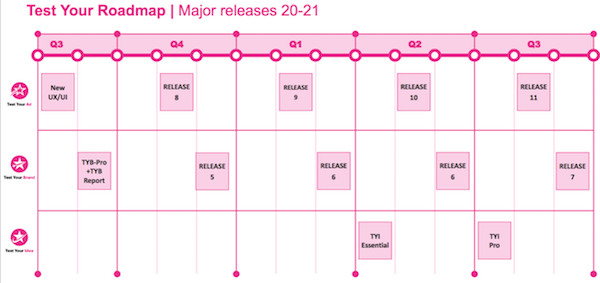

- SYS1’s ‘roadmap’ below suggests the Brand and Innovation divisions could soon have their own Test Your Ad equivalents — which will further underpin the conversion to automated/lower-cost services:

Achtung!

- I wrote in my annual-results review that “SYS1 is ironically very poor at marketing its own product.”

- I cited “Where the Lemons Bloom”, a short film written and presented by Orlando Wood, SYS1’s chief innovation officer:

- The film opens with the line “Kennst du das Land, wo die Zitronen blühn?” and then recounts the early life of German writer Johann Wolfgang von Goethe and his trip to Italy in 1786.

- I wrote:

“Experience the full 21m22s recording, and you too may think you have inadvertently tuned into a BBC4 history documentary.“

“Just how this somewhat indulgent and rather dull film that talks of “brain lateralisation” is meant to resonate with modern-day marketing folk is not clear to me.”

- The problem stemmed from the film’s System 2-type production.

- To recap:

- System 1 thinking is automatic, intuitive, emotional and reactive, while;

- System 2 thinking is conscious, effortful, logical and deliberate.

- In my view, Mr Wood wanted his audience to engage their System 2 brains, concentrate on what he said and think rationally about how they should enhance their marketing creativity.

- Trouble is, his audience were likely to have their System 1 brains engaged and become quickly fed up with 18th century German poetry.

- Mr Wood implemented some improvements to his latest film.

- The title “Achtung! How to attract and sustain attention” is certainly a much more System 1-type headline.

- Then the first line of the film — “What is it that attracts and holds our attention?” — followed by a minute of a Bugs Bunny cartoon should keep most viewers watching.

- See for yourself:

- True, Achtung! looks at famous paintings before diving into all the research data. But at least the film includes a few more obvious references to modern adverts than Where the Lemons Bloom.

- The improvements to the second film accompany enhancements to the clarity of SYS1’s overall message (which is ironic given SYS1 judges the messages conveyed by adverts).

- For instance, last year’s H1 results presentation offered the following ‘vision’ and ‘goal’ ambitions:

- The ambitions have since been reworded in a more succinct manner:

- That earlier Test Your Ad rate-card slide is another example of a clear and bold message.

- I guess half the battle to winning new ad clients is just getting through the door — and a clear and bold proposition for Test Your Ad ought to at least provide SYS1 more attention.

- Another earlier slide showed greater clarity and consistency emerging within SYS1’s product offering:

- Applying a consistent ‘Test Your’ naming convention to products could even be viewed as a System 1 fluent device.

Financials

- SYS1’s accounts finished the half in reasonable shape — bearing in mind the pandemic disruption.

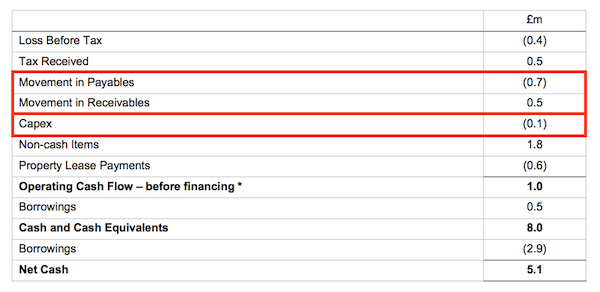

- Cash ended the half-year at £8.0m and debt at £2.9m, leaving net cash of £5.1m

- A loan of £0.5m related to the US government’s furlough scheme, which post-half-year was “fully forgiven”.

- The underlying net cash position was therefore £5.6m.

- A £0.5m R&D tax credit bolstered net cash flow to £1.0m. Another £0.5m credit may occur during the second half.

- The FY 2020 results from June said:

“Cash net of debt facilities ended May at £3.9m compared with £4.1m at 31 March”

- Net cash flow during April and May was therefore a negative £0.2m, and net cash flow during June to September was therefore a positive £0.7m excluding the tax credit.

- The important operating cash movements — working capital and capital expenditure — seemed under control during the half:

- Development on the Test Your Ad service is now expensed as incurred rather than capitalised onto the balance sheet.

- Revenue during Q2 may have been £5.5m assuming equal gross margins during Q1 and Q2:

- An adjusted Q2 pre-tax profit of £0.9m would therefore support an adjusted Q2 pre-tax margin of 16% — which is not bad for a business thumped by the pandemic during Q1.

- That 16% Q2 margin shows the office savings, staff layoffs and board-pay deferrals clearly having an impact.

- Property lease obligations on the balance sheet came to £3.2m versus an associated right-of-use asset of £1.7m.

- The £1.5m difference arguably reflects the rent SYS1 will pay in excess of the cost of commencing the same leases today.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- Although SYS1 continues to suspend its financial guidance and dividend, the results commentary included a few promising snippets:

“Client and market feedback give us confidence that our new products and infrastructure will provide a platform for accelerated growth over the years to come.”

“Our sales pipeline remains strong in the UK and is improving in the USA. These trends provide grounds for optimism.”

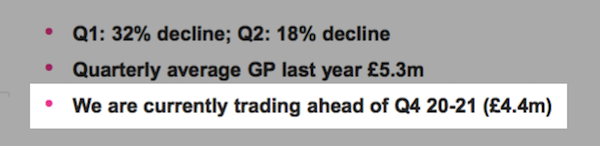

- The presentation suggested Q3 gross profit would be greater than £4.4m — i.e. close to the £4.7m reported for Q2:

- Extrapolating the Q2 adjusted pre-tax profit of £0.9m supports an intriguing valuation.

- £0.9m * 4 = £3.6m pre-tax, which after standard 19% UK tax would give earnings of £2.9m.

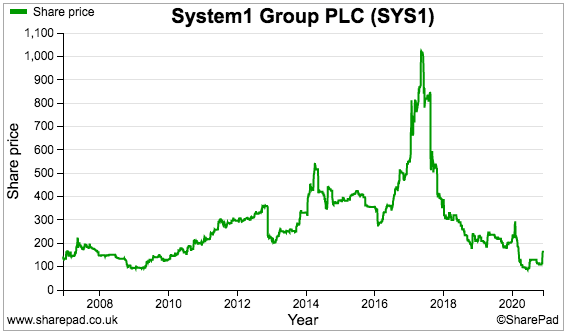

- The £23.4m market cap could therefore equate to a multiple of 8 based on that extrapolation.

- Whether that extrapolation is justified is of course up for debate.

- But an 8x multiple provides good room for error should the extrapolation prove too optimistic.

- Within my FY 2020 write-up, I said SYS1’s cash position should not really be used for valuation purposes due to the company’s then loss-making predicament.

- But Q2 witnessed SYS1 return to profitability and cash generation, and the £5m-plus net cash position is presently hard to ignore with a £23.4m market cap.

- The potential single-digit multiple and up to 20% of the market cap backed by cash makes this share far from expensive.

- The possible lowly valuation also means many finer parts of this H1 performance may not be that relevant to the longer-term share-price direction.

- Of greater relevance to investors are the progress of Test Your Ad and the general shift towards becoming a ‘data business’ with automated processes, cut-price products and more dependable revenue.

- And despite the pandemic, the transformation may now be succeeding given:

- The Test Your Ad win rate;

- The resilience of UK/Communications revenue, and;

- The 16% Q2 adjusted pre-tax margin.

Portfolio trade

- The ITV product validation, remarkable Q2, apparent lowly rating and opportunity for recovery prompted me to buy more SYS1 following these results.

- I increased my holding by more than three times at 173p per share including all costs.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

System1 (SYS1)

ITV 2020 results published 09 March 2021

A few snippets of interest from ITV, with whom SYS1 has (what I believe to be) a vital relationship (at least for SYS1 shareholders).

ITV’s ad revenue gained 3% during Q4 FY 2020 (i.e. SYS1’s Q3):

The outlook seemed mixed, though, with ad revenue down 6% for Q1 FY 2021 (i.e. SYS1’s Q4) but up 5% for Jan-Apr FY 2021:

SYS1 recorded a c£0.9m adjusted pre-tax profit during ITV’s Q3 FY 2020, and I am hopeful ITV’s ad performance during the subsequent two quarters will help SYS1 maintain that level of profitability.

SYS1 and ITV have co-hosted two recent webinars — Euro 2020 and Britain’s favourite ad — which implies ITV continues to view SYS1’s services as useful.

Nothing ground-breaking was revealed in the webinars, but perhaps worth listening to Kate Waters from ITV at 43m within the favourite ad webinar. She remains keen to ensure advertising is entertaining on ITV.

Maynard

System1 (SYS1)

Change in Executive Job Titles published 30 March 2021

Confirmation of Stefan Barden formally becoming chief executive. Here is the full text:

———————————————————————————————————–

System1 Group plc, the advertising effectiveness agency, (AIM: SYS1) announces that, in line with the continued evolution of the Company, John Kearon, previously Chief Executive Officer, has today assumed the title of ‘Founder and Executive President’ and Stefan Barden, previously Chief Operating Officer, the title of ‘Chief Executive Officer’.

Their internal responsibilities are unaffected, with John leading the Company direction, product development and external facing parts of the business, and Stefan leading the Company’s organisation, technical development and operational parts of the business. No board changes are expected to arise as a result of this development. Stefan will remain an executive director rather than reverting to the purely advisory role indicated last year.

Graham Blashill, Chairman commented:

‘The change in titles is intended to reflect current roles and responsibilities more accurately and ensure continuity of leadership within System1 as we continue to hire more top talent into our already strong leadership team. The announcement prepares the ground for the appointment to the executive team of a Chief Operating Officer, reporting to Stefan Barden, who will take on some of the operational responsibility that Stefan assumed at the start of the Covid-19 pandemic.’

———————————————————————————————————–

Probably a welcome move. Mr Barden (background here) was appointed COO last year (details here) following a stint as a ‘board advisor’ (point 4).

At the time of his board appointment I wrote:

”Mr Barden does not sound like the typical marketing-type person to me, which is perhaps what SYS1 needs in a COO to get things done.”

“Mr Barden owns 5.7% of SYS1, shares he bought at c200p — so £1.4m of his own money spent. His options come good only if the shares hit at least 500p. So unlike many executives, at least Mr Barden has some financial alignment to us ordinary investors.“

Mr Barden was appointed to the board alongside the new CFO during June 2020 — and I note the turnaround from Q1 loss to Q2 profit (within the half-year results in the blog post above) coincides with their board appointments.

Mr Kearon clearly thinks Mr Barden is doing a good job, and has effectively confirmed he has stepped back to let Mr Barden get on with the day-to-day work. Between them they own almost 30% of SYS1.

Maynard

““Mr Barden owns 5.7% of SYS1, shares he bought at c200p — so £1.4m of his own money spent. His options come good only if the shares hit at least 500p. So unlike many executives, at least Mr Barden has some financial alignment to us ordinary investors.“

I like the aggressive target on the options — they really have to make this company profitable to hope to see 500p. If they do I’ll be happy – I’m in at 300 and twice more at 240 — perhaps a further addition is warranted.

Thanks Games. The other executives have options that all require a 995p share price to pay out!

Maynard

Congrat’s on the big move up in SYS1 shares today Maynard. I’d been meaning to do some research following a skim of your articles; but never got round to it! It’s always the way!

Glad to see a strong update for you – justifies the work that goes into your write-ups.

Do you think it is still good value?

Hi James

Yes, I am glad the work on SYS1 has paid off (for now!). Early thoughts on the trading update are in the comment below.

Maynard

System1 (SYS1)

Trading Update published 21 April 2021

An encouraging update that suggested the profit turnaround witnessed during Q2 was extended throughout Q3 and Q4.

Here is the full text interspersed with my comments:

———————————————————————————————————–

Our Interim Statement released on 17 November 2020 reported that Revenue and Adjusted Profit had recovered substantially since Q1 and that the sales pipeline was strong. This improvement was maintained throughout the second half-year such that Revenue in H2 was approximately 8% above that of the equivalent prior year period, compared with a 26% decline in H1. As a result, the full year Revenue reduction was 11%.

Profitability was stronger in H2 than in H1 as sales picked up faster than adjusted operating costs which were 16% lower than last year in the second half.

We expect to report a pre-tax Adjusted Profit (which excludes impairment, share-based payments, government support, bonuses, loan interest and certain provisions) of some £2.9m for the full year (FY 2019/20: £2.0m). The business continued to generate cash, ending the period with £6.5m cash net of debt versus £4.2m at the previous year end. The net cash figure does not include a £0.5m tax credit for FY 2019/20 which was received early in April 2021.

———————————————————————————————————–

H2 2020 revenue was £11.75m, so an 8% increase gives £12.69m for H2 2021 and £22.82m for the full year.

The H1 pre-tax adjusted profit was £0.4m, so H2 saw a £2.5m profit to give the reported £2.9m for the full year.

A £2.5m pre-tax adjusted profit for H2 was better than I had expected. My sums in the blog post above extrapolated Q2’s £0.9m, so I was expecting £1.8m for H2.

Difficult to work out the adjusted costs for H2, because they are compared to figures for FY 2020 that applied a different ‘underlying overheads’ definition.

But clearly something is going right here, as a H2 pre-tax adjusted profit of £2.5m implies a healthy c20% margin on H2 revenue of £12.69m.

Note that the £2.9m adjusted pre-tax profit for the full year excludes all sorts of charges, including bonuses and loan interest. But similar adjustments were made for H1, and did not seem too untoward:

Note, too, that ‘negative’ bonus costs of £0.1m were added back to adjusted costs for H1 2021.

Net cash of £6.5m compares to £5.1m at the half year, which implies the reported £2.5m adjusted pre-tax result added only £1.4m to the cash position — not ideal.

Indeed, the H1 statement said a £0.5m US pandemic loan had been forgiven during H2, so arguably the underlying net cash position advanced by only £0.9m. Cash conversion therefore requires investigation when the full results are published.

———————————————————————————————————–

Underlying the recent improvement is the success of Test Your Ad, System1’s first fully automated predictive product set. The transition to automated data products supported by data-enabled, repeatable consultancy products is well underway: data products represented 15% of Sales Revenue in Q4 – mainly Test Your Ad – compared with 1% in H1. We expect the proportion of data product revenues to increase with the rollout in 2021/22 of Test Your Brand.

———————————————————————————————————–

Well, this is remarkable. The text implies Test Your Ad produced sales of c£100k during H1 and then, assuming an equal group revenue split between Q3 and Q4, close to £1m during Q4.

After a few years of hefty expenditure and embarrassingly low sales, the Test Your Ad service has finally come good. I am convinced the ad-testing arrangement with ITV has brought Test Your Ad to a wider audience. Test Your Ad’s greatly improved revenue seems to be the first real proof that SYS1 really is transitioning from a largely bespoke consultancy business to a data business with repeat income.

———————————————————————————————————–

With the resumption of sales growth and a strong net cash position, the Company will look to reinstate the share buyback programme which was suspended in 2020 due to uncertainty over the potential impact of the Covid pandemic on our business. A return to dividend payments is not currently envisaged. More information will be provided on the proposed buyback later in the year.

OUTLOOK

System1 is focused on achieving Revenue growth over the short and medium term. In pursuit of this goal the Company will increase discretionary investment in product development, IT, marketing, and relationships with advertising agencies and advertising platform partners. We will also continue to recruit new talent, after a sizeable increase in headcount during the latter months of 2020/21 which took year-end headcount to 147 from 128 at the half year. The drive for further efficiency improvements in “run” costs will continue. We plan to remain profitable and to continue to generate cash in the 2021/22 financial year, notwithstanding that we are targeting revenue growth to be at least matched by the rate of cost growth as we prioritise scaling our automated predictive products.

———————————————————————————————————–

Referring to “advertising platform partners” suggests there may be more ITV-type deals to be won. Increasing the headcount by 15% feels bullish, too.

This line “we are targeting revenue growth to be at least matched by the rate of cost growth” was worded very oddly. I translate it to mean revenue ought to rise, but margins are likely to fall as costs increase at a greater pace. I am hopeful profits will not fall from the £2.5m-rate scored in H2.

Resurrecting the buyback is interesting, as I presume SYS1 views the share price as good value. Doubling up the £2.5m H2 profit and applying 19% UK tax gives earnings of £4m or c30p per share. At 250p the shares may therefore still be valued on a single-digit multiple — although those profit adjustments and the prospect of greater costs ought to be considered with this rating. The £6.5m net cash position meanwhile represents 20% of the £32m market cap.

EDIT 30 June 2020: I should add that I increased my SYS1 holding by 40% following this statement at 242p including all costs.

Maynard

System1 (SYS1)

Notice of results published 23 June 2021

Not ideal news. The forthcoming 2021 results will be published 15 days later than expected because the auditors need additional time to check the figures. I trust the delay is due to Covid and nothing more sinister.

Here is the full text:

——————————————————————————————————————

Further to the announcement of 21 April 2021, the Group’s auditors, RSM Auditors UK LLP, have requested additional time to complete their audit processes. As a consequence, the Company will now publish its results for the year ended 31 March 2021 on 14 July 2021. It is not expected that this delay will have any impact on the figures contained within the results.

——————————————————————————————————————

Maynard