12 December 2019

By Maynard Paton

Results summary for Tristel (TSTL):

- Record annual figures for the sixth consecutive year, supported by satisfactory progress both within the UK and abroad.

- The underlying performance was complicated by Brexit stock-piling, an acquisition, US regulatory costs and option expenses.

- The publication of new three-year financial targets was impressive, and suggested the company could grow organically at 10-15% per annum.

- The accounts are still healthy with high margins, net cash and respectable cash generation.

- The valuation remains understandably rich with an estimated underlying P/E of 30. I continue to hold.

Contents

- Event links and share data

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Ecomed

- UK

- Overseas

- Italy

- United States

- Non-core

- Three-year financial targets

- MobileODT

- Share options

- Financials

- Valuation

Event links and share data

Event: Annual results for the twelve months to 30 June 2019 published 16 October 2019 and City presentation hosted 16 October 2019

Price: 340p

Shares in issue: 44,715,823

Market capitalisation: £152m

Why I own TSTL

- Develops medical-instrument disinfectants that are repeat-purchase and face limited direct competition due to multiple patents, instrument-manufacturer approvals, scientific testimonies, secret ingredients and regulatory hurdles.

- Enjoys a sizeable and resilient UK market position alongside significant expansion opportunities abroad.

- Boasts financials that showcase high margins, robust returns on equity, decent cash flow and no debt.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary

Revenue, profit and dividend

- July’s open-day trading statement had already indicated TSTL would report upbeat progress.

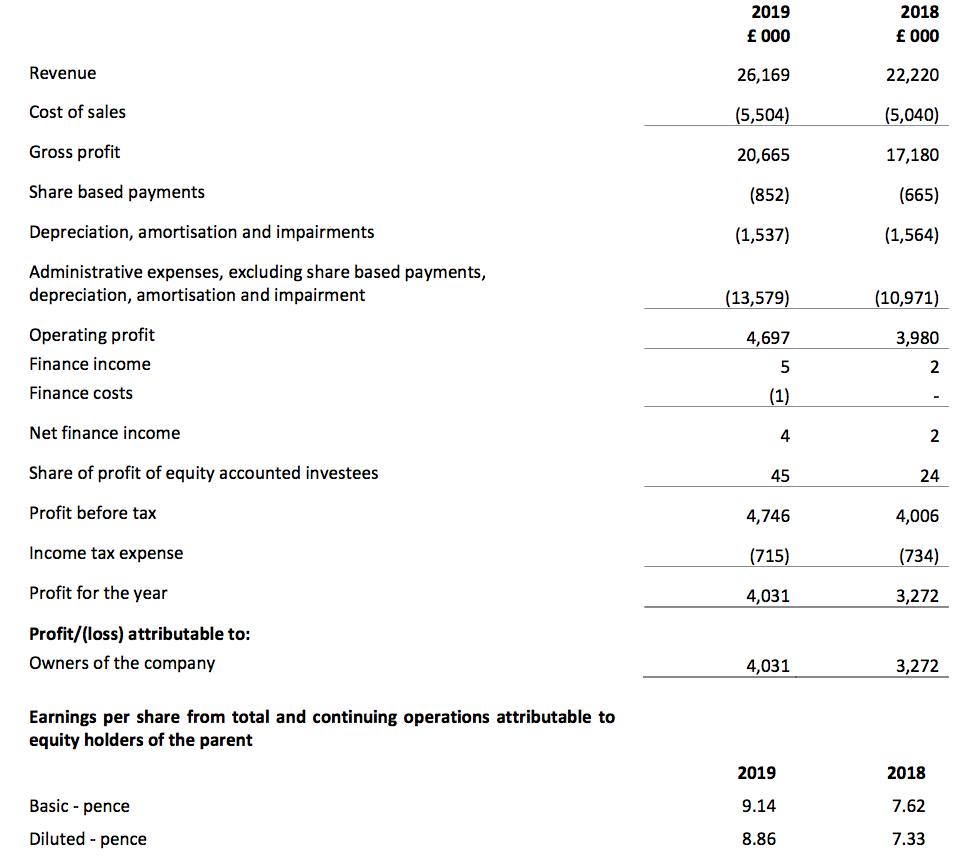

- Full-year revenue topped the predicted £26m at £26.2m (up 18%) while pre-tax profit before share-based payments was indeed “at least £5.5m” at £5.6m (up 20%) .

- Revenue and reported operating profit both recorded new peaks for the sixth consecutive year:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (£k) | 15,334 | 17,104 | 20,273 | 22,220 | 26,169 |

| Operating profit (£k) | 2,541 | 2,568 | 3,902 | 3,980 | 4,697 |

| Associates (£k) | 8 | 13 | 19 | 24 | 45 |

| Finance income (£k) | 3 | 12 | 4 | 2 | 4 |

| Other items (£k) | - | - | 41 | - | - |

| Pre-tax profit (£k) | 2,552 | 2,593 | 3,966 | 4,006 | 4,746 |

| Earnings per share (p) | 5.44 | 5.01 | 8.06 | 7.62 | 9.14 |

| Dividend per share (p) | 2.72 | 3.33 | 4.03 | 4.58 | 5.54 |

| Special dividend per share (p) | 3.00 | 3.00 | - | - | - |

- TSTL revealed revenue would have been £24.5m (up 10%) without the purchase of Ecomed (see Ecomed below).

- TSTL’s underlying profit advance was harder to determine. The figures were complicated by:

- Costs associated with the US regulatory project (see United States below);

- Significant share-based payments (see Share options below);

- An undisclosed Ecomed contribution (see Ecomed below), and;

- A fair-value investment gain (see MobileODT below).

- TSTL confirmed the cost of the US regulatory project was once again £500k, and also revealed a hefty £852k share-based payment charge:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Operating profit before SBP and US costs (£k) | 2,504 | 2,641 | 5,145 | 2,485 | 3,564 | 6,049 | |

| Share-based payments (£k) | (164) | (501) | (665) | (196) | (656) | (852) | |

| US costs (£k) | (500) | - | (500) | (100) | (400) | (500) | |

| Operating profit (£k) | 1,840 | 2,140 | 3,980 | 2,189 | 2,508 | 4,697 |

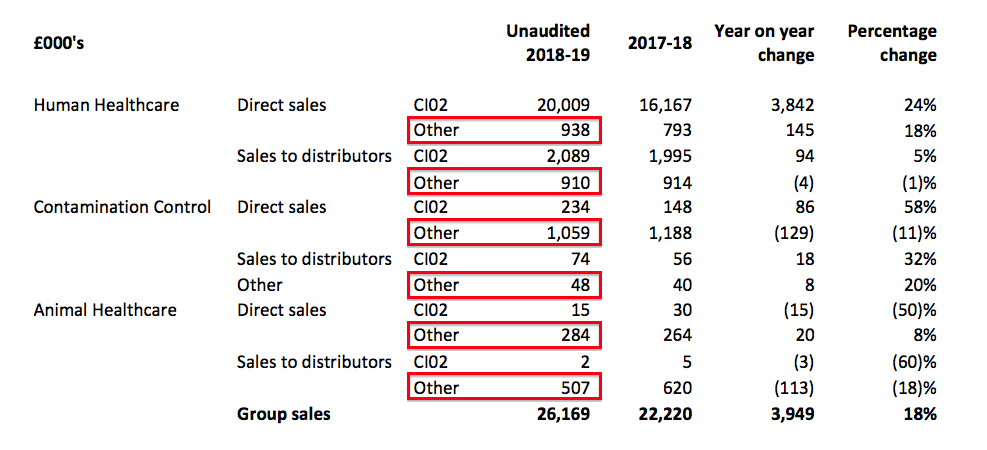

- UK revenue advanced 9%, with the second-half witnessing a bumper 13% jump.

- Overseas revenue, including Ecomed, rallied 26% to represent 55% of the group’s top line.

- The full-year dividend was raised 21% to 5.54p per share, with a 17% advance applied to the final payout.

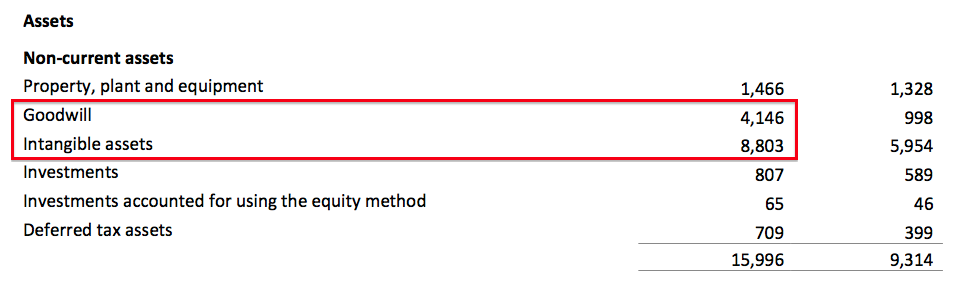

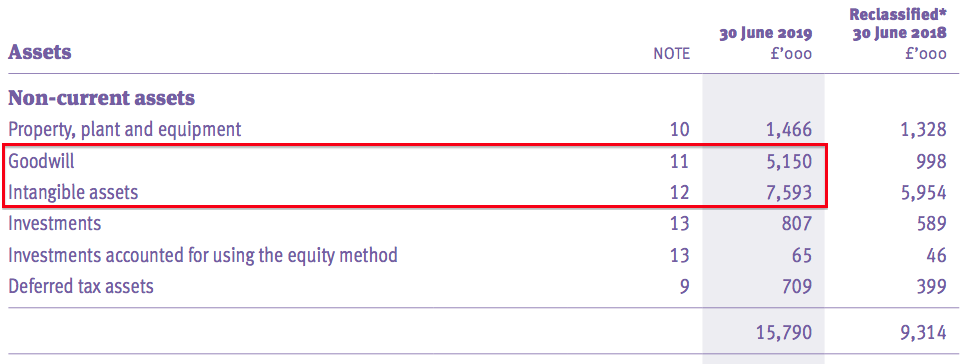

- The results RNS carried a handful of balance-sheet differences to the subsequent annual report.

- In particular, the RNS said goodwill was £4,146k and intangible assets were £8,803k…:

- …while the annual report declared goodwill of £5,150k and intangible assets of £7,593k:

- At least both the RNS and the annual report said net assets were £23,359k.

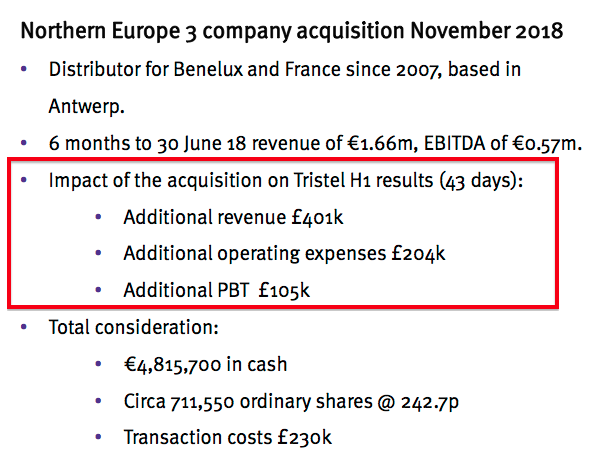

Ecomed

- TSTL purchased Ecomed — the distributor of TSTL’s products in Belgium, the Netherlands and France — for £4.7m during November 2018.

- TSTL confirmed Ecomed’s revenue following the purchase amounted to £2.1m:

- Revenue of £2.1m for 7.5 months is equivalent to £3.4m for a full twelve months.

- Prior to purchase, Ecomed’s annual sales were €3.1m or approximately £2.7m.

- My sums (if accurate) indicate Ecomed’s revenue may now be running 25% (£3.4m / £2.7m) higher than they were before the acquisition.

- TSTL revealed group revenue would have been £24.5m without the Ecomed purchase — or £1.7m lower than the revenue actually reported.

- We can therefore infer distributor sales to Ecomed would have been £2.1m less £1.7m = £0.4m had Ecomed not been acquired.

- Purchasing TSTL products for £0.4m and then selling them for £2.1m implies Ecomed enjoyed a wonderful 81% gross margin.

- That said, Ecomed continues to sell non-TSTL products — which flatters that 81% calculation.

- Management said at the City presentation:

- Non-TSTL products represented revenue of approximately £0.2m for the year, and would be “wound down”, and;

- Ecomed has distributed TSTL products since 2005, and subsequent arrangements with other distributors were agreed on more favourable terms for TSTL.

- At the time of purchase, TSTL claimed Ecomed could “contribute incremental earnings in its current financial year of at least £250,000 after transaction and integration costs.”

- At the half-year stage, TSTL revealed Ecomed had contributed additional profit before tax of £105k:

- But neither this results RNS — nor the annual report — disclosed Ecomed’s actual full-year profit contribution.

- Assessing profit contributions from acquisitions is important because acquisitions do not always perform as expected.

- Management said at the City presentation that Ecomed’s 7.5-month profit contribution was between £300k and £400k.

- Between £300k and £400k equates to approximately £550k on a twelve-month basis.

- The annual report did reveal “acquisition-related costs” of £277k were charged against earnings:

- So perhaps a full-year contribution before “acquisition-related costs” would have been around £800k (i.e. £550k plus £277k) — which matches my February estimate and seems reasonable for the £4.7m paid.

- TSTL classified the Ecomed purchase as an investment:

- Perhaps this classification allowed TSTL to side-step the typical annual report small-print for acquisitions.

- In particular, the annual report does not disclose:

- The revenue and profit contributions from the Ecomed

acquisitioninvestment, and: - The level of group revenue and profit had the Ecomed

acquisitioninvestment occurred at the start of the financial year:

- The revenue and profit contributions from the Ecomed

UK

- TSTL’s UK performance was very creditable. Domestic revenue growth of 9% compared to 2%, 3% and 5% during 2018, 2017 and 2016 respectively.

- The second half saw particularly strong trading, with revenue up 13% versus 5% during H2:

| UK revenue | H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | |

| Medical device disinfection (£k) | 3,313 | 3,404 | 6,717 | 3,608 | 4,152 | 7,760 | |

| Critical surface (£k) | 601 | 644 | 1,245 | 690 | 798 | 1,488 | |

| Other (£k) | 1,440 | 1,433 | 2,873 | 1,312 | 1,236 | 2,548 | |

| Total (£k) | 5,354 | 5,481 | 10,835 | 5,610 | 6,186 | 11,796 |

- UK sales of TSTL’s core medical-device disinfectants improved an impressive 16%, with a super 22% recorded during H1.

- UK sales of TSTL’s surface disinfectants — used to clean mattresses, bedside tables and other items that hospital patients come into contact with — rallied a terrific 20%, with a brilliant 24% recorded during H2.

- The City presentation did not repeat February’s slides describing the potential of a new UK surface-disinfectant product called Shot:

- However, management did state at the City presentation:

- The new Shot product is being used in 25 hospitals;

- The biggest area of resistance to Shot is “staff practice” — “huge change is required”, and;

- “The NHS has a clear mandate to reduce single-use plastic” — most wipes being used by the NHS at present are plastic. Those used with Shot are manufactured differently.

- UK revenue was inflated by Brexit stock-piling. The results said (my bold):

“Brexit cast its spell over the year. To forestall any potential disruption to our customers’ supply chain we built inventory of all component parts and finished products in the run up to 31 March and encouraged key domestic and overseas customers to increase their stockholdings of our products. Brexit did not take place and we believe that most of our customers’ inventory holdings were then wound down again in the final quarter of the year. We anticipate that a similar cycle will repeat as we approach 31 October 2019.”

- Management admitted at the City presentation that stock-piling had generated UK revenue of approximately £700k.

- Without such stock-piling, UK revenue growth would have been just 2%.

- Management admitted at the City presentation that UK growth could be 1-2% during 2020 given the stock-piling benefit — but claimed UK growth should revert back to 4-5% per annum.

- Remember that the UK figures were distorted slightly at the half-year by a reclassification of certain medical-device disinfectant revenue as non-core ‘other’.

- Remember, too, that a favourable new NHS pricing agreement commenced at the start of (calendar) 2019 and would have bolstered H2 sales.

- Management has in the past claimed “further growth opportunities are limited” for domestic sales, given TSTL’s disinfectants are already used extensively throughout the NHS.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Overseas

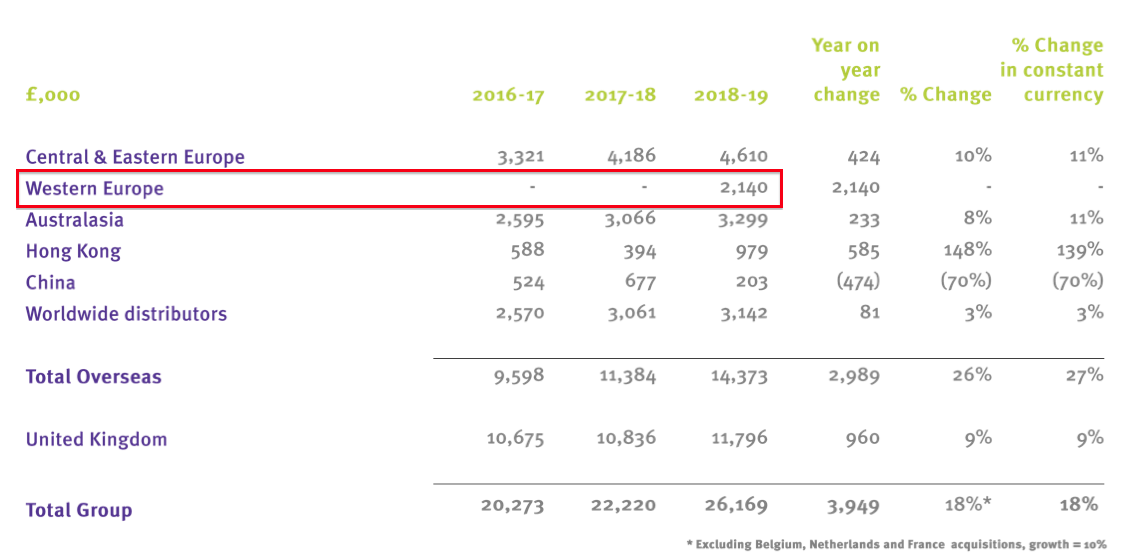

- The Ecomed purchase supported overseas revenue climbing 32% during H2:

| Overseas revenue | H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | |

| Medical device disinfection (£k) | 4,867 | 5,006 | 9,873 | 5,699 | 6,819 | 12,518 | |

| Surface disinfection (£k) | 139 | 80 | 219 | 193 | 83 | 276 | |

| Other (£k) | 367 | 926 | 1,293 | 516 | 1,063 | 1,579 | |

| Total (£k) | 5,373 | 6,012 | 11,385 | 6,408 | 7,965 | 14,373 |

- The bulk of overseas revenue (c87%) relates to the ‘core’ medical-device disinfectants, which gained 17% during H1 and 36% during H2.

- Without Ecomed, overseas progress was not that spectacular:

| Overseas revenue | H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | |

| Australasia (£k) | 1,529 | 1,537 | 3,066 | 1,660 | 1,639 | 3,299 | |

| China & Hong Kong (£k) | 519 | 552 | 1,071 | 560 | 622 | 1,182 | |

| Germany/Central Europe (£k) | 1,953 | 2,233 | 4,186 | 2,230 | 2,380 | 4,610 | |

| Northern Europe (£k) | - | - | - | 400 | 1,740 | 2,140 | |

| Total in-house (£k) | 4,001 | 4,322 | 8,323 | 4,850 | 6,381 | 11,231 | |

| Distributors (£k) | 1,372 | 1,689 | 3,061 | 1,560 | 1,582 | 3,142 | |

| Total (£k) | 5,373 | 6,011 | 11,384 | 6,410 | 7,963 | 14,373 |

- Australasian revenue gained 8%, with only a 7% advance experienced during H2.

- German, Swiss and Polish revenue climbed 10%, with only a 7% advance witnessed during H2.

- Chinese and Hong Kong revenue increased 10%, although H2 revenue improved by 12%.

- Management said at the City presentation that plans were afoot to “broaden the product ranges” — in part through new product approvals — to “accelerate growth” within Australia and Germany.

- Management also said at the City presentation that Hong Kong offered “reasonable growth” and that China — with two sales people now selling direct to hospitals — should see sales “accelerate” over the next few years.

- Management noted at the City presentation that revenue from the group’s overseas distributors had increased by only 3%.

- However, the 3% increase was distorted by the purchase of Ecomed, which took distributor sales of £0.4m ‘in-house’.

- Management claimed at the City presentation that, adjusted for Ecomed, overseas distributor revenue had increased by 16% and that the company was “very pleased” with that performance.

- Annual overseas revenue has increased from 34% to 55% of total group revenue during the last five years. Overseas revenue represented 56% of total revenue during H2.

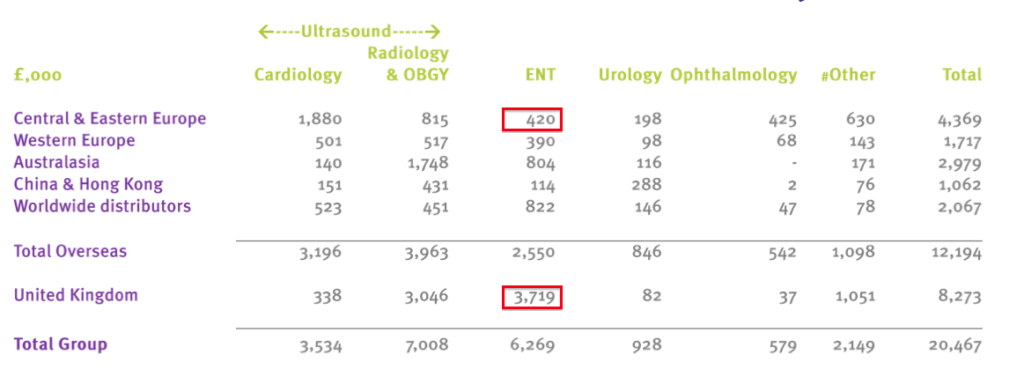

- The City presentation powerpoint included this interesting slide:

- The slide disclosed (for the first time) the revenue generated from different hospital departments both in the UK and overseas.

- Management hinted at the City presentation that the overseas hospital departments could catch up with the UK.

- In particular, management claimed that 3,000 doctors perform ear, nose and throat (ENT) examinations in Germany — the number of doctors being “many more than in the UK”.

- And yet the slide shows revenue from ENT clinics/departments in Germany, Poland and Switzerland of just £420k last year — versus £3.7m from the UK.

- Management explained at the City presentation that the modest £420k figure was due to German ENT doctors not being forced to use a high-level disinfectant on their medical instruments.

- Management claimed “it would be reasonable to expect at some point German ENT doctors having to adopt high-level disinfection”. Management also claimed “demand could then explode”.

- Something similar is currently happening in France.

- Management said at the City presentation that during the spring, new guidelines for French hospitals were published that recommended intra-vaginal probes be disinfected to a high-level standard.

- Management said demand for TSTL’s products to clean such probes in France had since become “frantic” and had created a “fantastic vibrant market”.

- Management added that French hospitals had three choices for high-level disinfection — TSTL and two machine alternatives. Management noted that TSTL’s products “could be deployed much quicker than machines”.

- No wonder Bart Leemans — the former Ecomed owner and now a TSTL director — was so confident about France at the July open day.

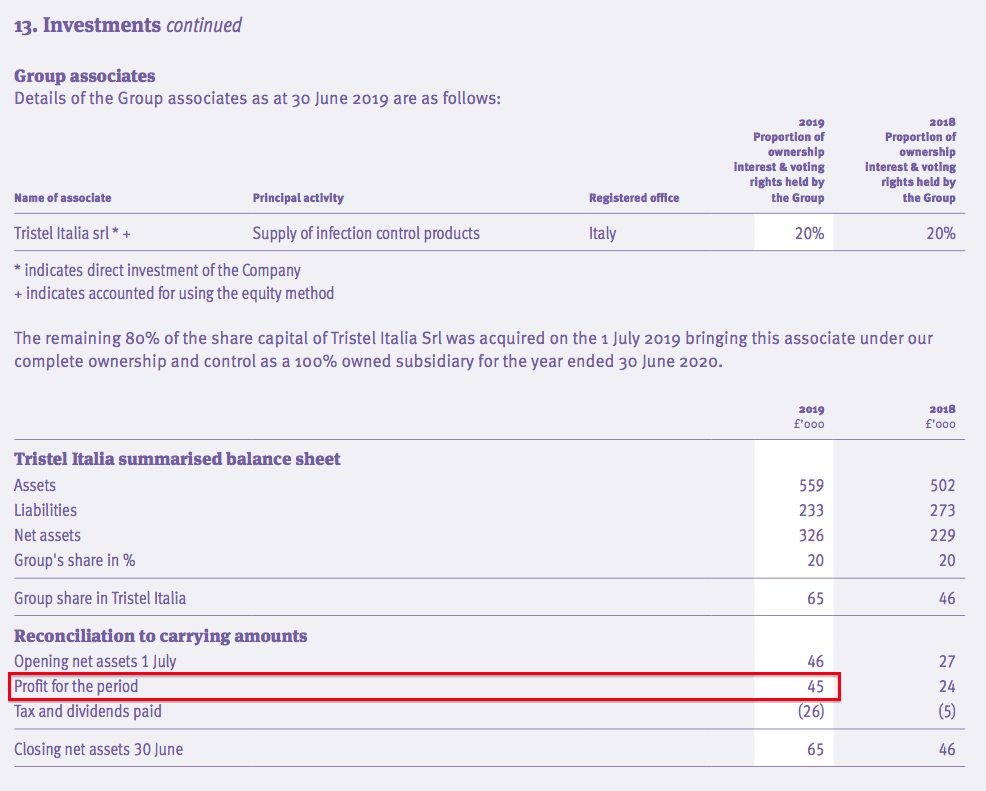

Italy

- TSTL announced the purchase of its Italian distributor during July.

- TSTL previously owned 20% of this distributor, and has paid €661k for the other 80% with a further €150k to be paid if Italian revenue effectively increases by 15% during 2020 and again during 2021.

- The annual report confirmed the distributor generated a profit of £45k for TSTL:

- If 20% of Italian profit came to £45k, then 100% would be £225k.

- The Italian operation has expanded impressively during recent years:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (£k) | 238 | 285 | 385 | 465 | 620* |

| Profit (£k) | 38 | 66 | 96 | 121 | 225 |

(*estimated)

- The acquisition announcement said: “Tristel expects the acquisition to have a neutral impact on earnings in the current financial year ending 30 June 2020 and to be earnings enhancing in future years.”

- The “neutral impact on earnings” — which I take to mean another £45k contribution and not the full £225k — is due to TSTL employing additional sales people to “accelerate growth in this well-established market”.

United States

- The results statement and City presentation did not reveal any notable progress about the group’s US regulatory programme.

- The results reminded investors that this project commenced five years ago (my bold):

“In 2014, we explained to our shareholders that we had embarked upon a United States regulatory approvals programme. To date we have focussed upon our chlorine dioxide foam-based product Duo.”

- TSTL continues to prepare a product submission to the US regulator:

“We are preparing a submission to the FDA for Duo as a high-level disinfectant. The intended use patterns will be for intra-cavity ultrasound probes, nasendoscopes, and lastly certain ophthalmic devices. If successful, this will position us in three of the clinical areas in which we are most successful in other geographical markets.”

- TSTL withdrew all timetable guidance for its US regulatory programme within February’s interim results.

- The withdrawal followed a series of frustrating and ongoing delays to the product submission.

- The FDA project cost £0.5m during 2019 and management confirmed at the City presentation that a further £0.5m was budgeted for 2020.

- The FDA costs were — and will continue to be — entirely expensed against earnings.

- Management once again commented upon the US presence of Nanosonics, the manufacturer of the high-level disinfection Trophon machine, at the City presentation.

- The Trophon machine disinfects only ultrasound probes and management claimed the US offered “ample space” for both TSTL and Trophon — in part because the Trophon machines “break down”.

- Management also reiterated that TSTL would collect a 17.5% royalty on US sales though its US manufacturing partner, Parker Laboratories.

- I continue to guess/hope that TSTL could submit its FDA application during 2020, perhaps receive approval during 2022 and start collecting US royalties during 2023.

Three-year financial targets

- The most impressive part of these results was the publication of new three-year financial targets.

- Few quoted companies disclose any financial targets, so TSTL’s directors must be applauded for their confidence.

- TSTL’s previous three-year guidance was issued during 2016, and had anticipated lifting revenue by between 10% and 15% a year during 2017, 2018 and 2019, while sustaining a pre-tax margin of 17.5% throughout.

- The guidance previous to that anticipated revenue growing by at least 50% between 2014 and 2017 while maintaining the pre-tax margin at 15%.

- Both sets of previous three-year targets were met — although acquisitions and favourable currency movements did help.

- The latest targets for the three years to 30 June 2022 are to:

- “Grow revenue in the range of 10% to 15% per annum, on average”, and;

- “Continue to achieve an earnings before interest, tax, depreciation and amortisation (Ebitda) margin of at least 25%, also stated before share-based payment charges”.

- Increasing revenue by 10% a year for three years would mean revenue expands by £8.7m to £34.8m by 2022.

- Generating the additional revenue of £8.7m will be helped by a full-year contribution from Ecomed (perhaps giving an extra £1.2m) and the purchase of the Italian distributor (perhaps giving an extra £0.6m).

- Take the extra Ecomed and Italian revenue into account, and only a further £6.9m— equivalent to 7.5% per annum growth — may be required to meet the minimum £34.8m revenue target for 2022.

- TSTL’s revenue ambition could be hindered by ‘legacy’ products that do not use the group’s core chlorine-dioxide chemistry.

- Such products represent £3.7m, or 14%, of total revenue and their sales decreased by 2% during 2019:

- Significantly, management confirmed at the City presentation that:

- No “obvious” distributors were now left to acquire, which implied the new revenue target would be achieved through organic growth, and;

- No potential US revenue was included in the new three-year targets.

- TSTL explained the target profitability measure had changed from a pre-tax margin to an Ebitda margin “so that our profitability target does not deter investment in future revenue and profit generating possibilities, which will impact amortisation.”

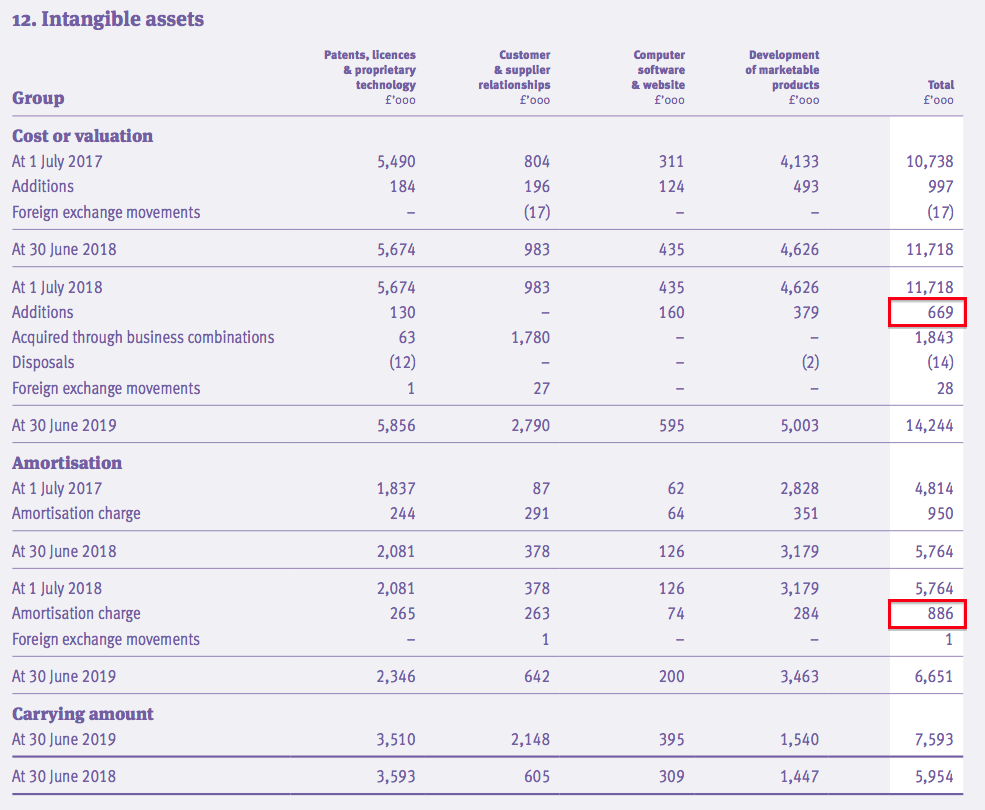

- The reference to amortisation suggests TSTL may increase its spend on new product development and other intangible items (such as patents and software).

- During 2019, TSTL spent £669k on intangible assets and the associated amortisation charge applied was £886k:

- TSTL has historically — and commendably — matched its cash expenditure on intangible items with the amortisation charged against earnings:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 |

| Amortisation (£k) | 447 | 524 | 679 | 950 | 886 |

| Intangible capital expenditure (£k) | (567) | (406) | (419) | (997) | (669) |

- I trust any greater development spend will see a commensurate increase to amortisation and therefore not risk reported earnings becoming flattered.

- Management said at the City presentation that the 25% Ebitda target was a “base line” and that the company “very much expects to exceed 25%” during the next three years.

- During 2019, Ebitda before share-based payments was £7.1m and reflected a 27% margin.

- All told, the new three-year revenue and Ebitda targets should be reasonably straightforward for TSTL to achieve.

- Management did confess at the City presentation that a third target measure — “while progressively increasing earnings every year” — should have been included as well.

Non-core

- Management revealed for the first time at the City presentation that the group’s ‘non-core’ operations could be sold to another manufacturer.

- The ‘non-core’ operations consist of all the non-chlorine-dioxide products as well as all the veterinary and cleanroom disinfectants.

- Such items earned 2019 revenue of £4.2m (16% of total revenue), which was unchanged on the year before.

- Management claimed at the City presentation that the ‘non-core’ operations were “profitable and cash generative.”

- However, management also admitted that converting customers from legacy chemistries to the core chlorine-dioxide products had been “slow”.

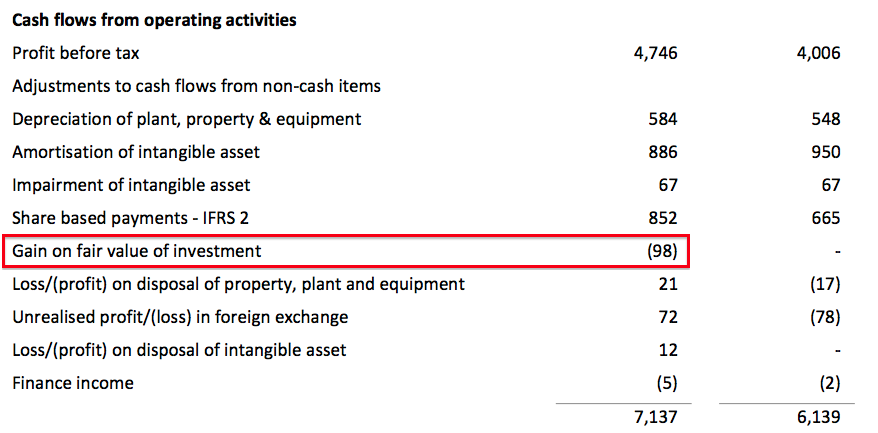

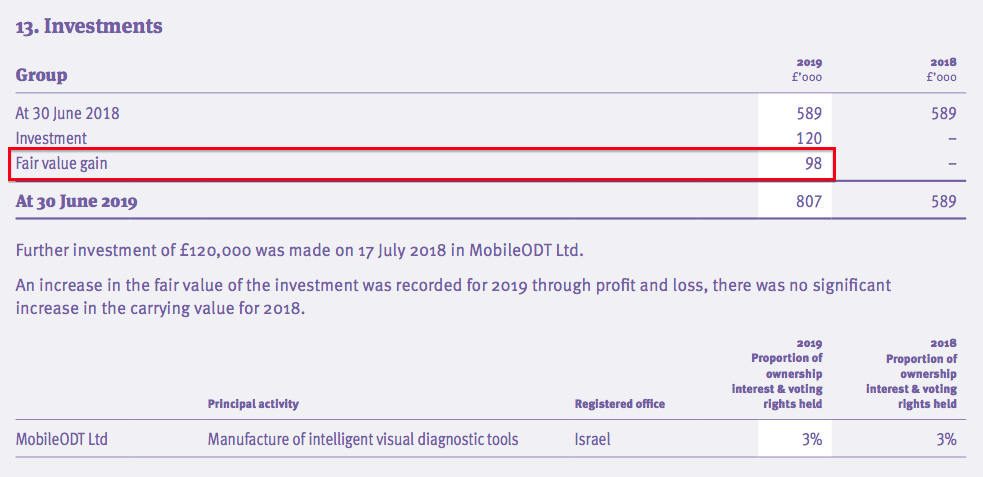

MobileODT

- The cash flow statement revealed a £98k fair-value gain:

- The gain related to TSTL’s stake in MobileODT, a developer of hand-held colposcopes:

- The £98k gain was included within operating profit, although arguably the item could/should have instead been recorded as financial income.

- Following these results, TSTL announced it had not participated in a further, $9.75m round of investment in MobileODT.

- TSTL’s stake in MobileODT therefore reduced from 3.22% to 2.13%, which implies this latest fund-raised increased MobileODT’s share count by 51%.

- If a third of MobileODT is now worth $9.75m, then MobileODT as a whole could be worth $29m.

- MobileODT was not mentioned in this results RNS or the City presentation.

- The decision not to invest further and the lack of management discussion might suggest the MobileODT investment — in the accounts at £807k — is no longer going entirely to plan.

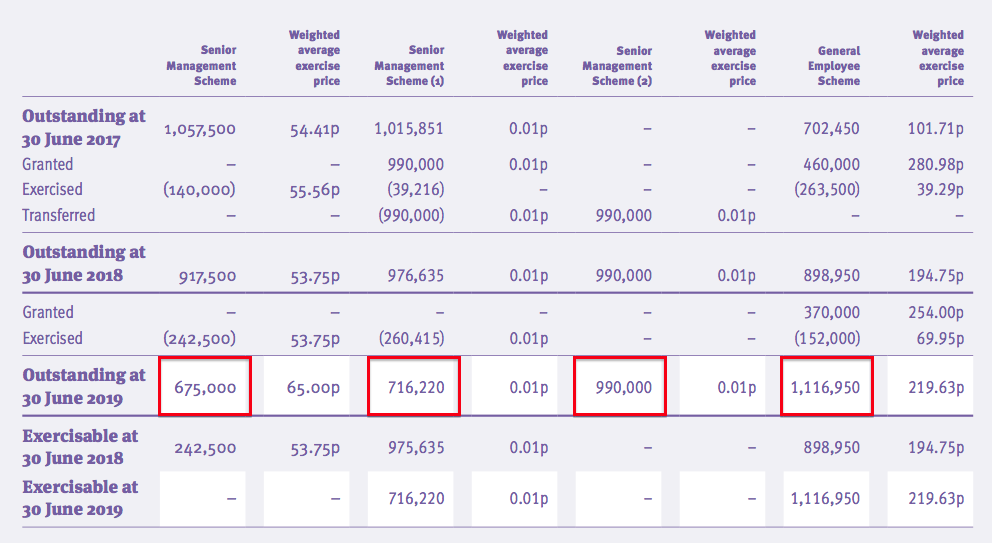

Share options

- Significant share-based payments have blighted TSTL’s operating profit during recent years:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit before SBP (£k) | 2,576 | 3,242 | 4,023 | 4,645 | 5,549 |

| Share-based payment (£k) | (35) | (674) | (121) | (665) | (852) |

| Operating profit (£k) | 2,541 | 2,568 | 3,902 | 3,980 | 4,697 |

- Share-based payments have reduced total operating profit by £2.3m, or 12%, since 2015.

- For 2019, share-based payments reduced operating profit by £852k, or 15%.

- TSTL has some form with share options. During 2016, the executives and senior managers collected a £1m options windfall following — in my view — the dubious disclosure of trading information and of the option plan itself.

- The directors have since told me they “strongly rebut” the allegations of a lack of disclosure and of them “dipping their fingers into the till”.

- The directors decided to award themselves more options during 2017.

- This time the terms of the award were announced very clearly and the new scheme was in fact put to a vote at an AGM.

- This latest option batch is divided into three tranches and will come good only if:

- The share price trades at an average of 350p (tranche 1), 425p (tranche 2) and 500p (tranche 3) for at least three months before 30 June 2021, or;

- The company is acquired (which is standard for option schemes).

- I like option plans that are based on share prices. Everyone knows exactly when the options have vested and shareholders can always take advantage of the higher share price and sell.

- Of course, a share price may not always reflect the long-term value of a business.

- But then again, alternative measures such as earnings per share, return on equity, and so on, can all be fudged to trigger option payouts — and subside thereafter, too.

- The drawback to TSTL’s latest option batch is the 1p exercise price. If the company is acquired for peanuts, the options will vest and management will receive some extra money — yet shareholders will be mugged.

- Accounting rules require TSTL to record a share-based payment charge even if these latest options turn out to be worthless (i.e. the share price never trades at a 350p average (or more) for at least three months before 30 June 2021).

- The share price has to date never traded at 350p — let alone at a 350p average (or more) for at least three months.

- Rather than adjust reported earnings for a theoretical share-based payment charge, one alternative is to ignore the charge and instead assume every granted option is exercised.

- The annual report shows 3,498k outstanding options:

- The share count would increase by almost 8% to 48,061k if all outstanding options were exercised

- Those 3,498k outstanding options have exercise prices ranging from 1p to 320p and would raise approximately £2.9m for TSTL if they were all exercised.

- Any earnings guess would then use the 48,061k share count to determine a per share figure, while the cash position would be increased by £2.9m.

- Whether the directors and employees deserve 3,498k options — and the potential to convert them into shares worth £10m or more (at the recent share price) — is debatable.

- I will nevertheless be very happy if the latest option batch vests entirely — that outcome requires the share price to trade at an average of 500p (or more) for at least three months before 30 June 2021.

Financials

- TSTL’s accounts remain straightforward and in good shape.

- Cash generation appears fine:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit (£k) | 2,541 | 2,568 | 3,902 | 3,980 | 4,697 |

| Depreciation and amortisation (£k) | 844 | 966 | 1,243 | 1,498 | 1,470 |

| Net capital expenditure (£k) | (1,045) | (889) | (959) | (1,450) | (1,347) |

| Working-capital movement (£k) | (606) | 467 | (530) | (520) | (780) |

| Net cash (£k) | 4,045 | 5,715 | 5,088 | 6,661 | 4,170 |

- During the last five years, total expenditure on tangible and intangible assets has been more than matched by the combined depreciation and amortisation expensed against earnings.

- The five-year aggregate working-capital investment of £2m looks modest given operating profit has totalled £18m during the same time.

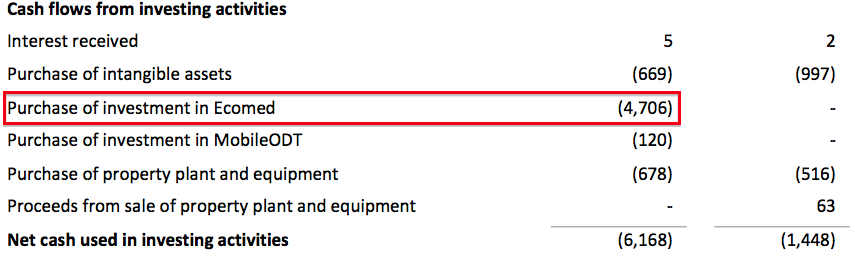

- After £4.7m was spent purchasing Ecomed and £2.2m spent on dividends, the year-end cash position decreased by £2.5m to £4.2m.

- Management revealed the latest cash position to be £4.3m (equivalent to 9.6p per share) at the City presentation.

- TSTL carries no debt and no pension obligations.

- TSTL’s operating margin remains at a level that underlines the competitive strength of the group’s packaging patents, secret ingredients, proprietary know-how, device-manufacturer approvals and independent scientific testimonies:

| Year to 30 June | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating margin* (%) | 17.0 | 15.8 | 21.7 | 20.2 | 19.9 |

| Return on average equity** (%) | 22.6 | 21.7 | 33.8 | 28.8 | 26.0 |

(*before US regulatory costs **adjusted for net cash)

- Returns on equity remain at very acceptable levels.

Valuation

- TSTL’s reported operating profit was £4.7m for 2019.

- The following adjustments give an ‘underlying’ operating profit of £6.4m:

- Adding £500k for US regulatory costs;

- Subtracting £98k to eliminate the fair-value gain;

- Adding an estimated £450k to reflect a full-year Ecomed contribution before “acquisition related costs”;

- Adding £852k to ignore share-based payments, and;

- Adding £45k for Italy.

- Applying the standard 19% UK tax rate then gives earnings of £5.2m.

- Assuming every outstanding option is exercised:

- Earnings of £5.2m convert into 10.9p per share, and;

- The £4.2m cash position would increase by £2.9m to £7.1m — equivalent to approximately 15p per share.

- Subtract that 15p per share from the 340p share price, and the ‘underlying’ cash- and option-adjusted P/E could be 325p/10.9p = 30.

- A premium rating remains understandable given:

- Management has essentially signalled organic revenue growth of at least 10% per annum during the next three years;

- The accounts clearly show TSTL’s disinfectants delivering attractive economics;

- A disposal of the ‘non-core’ operations would almost certainly showcase the greater profitability and faster growth rate of the ‘core’ products, and;

- The possibility one day of a successful FDA application and the start of US sales.

- The full-year 5.54p per share dividend meanwhile supplies a modest 1.6% yield.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Tristel.

Maynard,

I went to the TSTL AGM last week and the decision not to participate in the Mobile ODT fund raise was one of the things that I raised. Management confirmed my assumption that no further investment was made because the investment is non-core and that the level of investment that they have and their role as a distributor for Mobile ODT in certain regions gives them sufficient exposure and visibility. I gather that some new VC investors joined in the fund raise, which went well. Whilst TSTL’s percentage shareholding was obviously diluted, I was told that the actual value of their investment slightly increased.

Regards.

Hi Andrew

Thanks for the comment. The initial MobileODT investment was made in July 2017 and two years on is now deemed ‘non core’. Oh well. I suspect the investment has not entirely gone to plan, and — you raise a good point here — the role of distributor gives the company an ‘insider’s view’ when MobileODT asks for more money. Feel free to comment on any other AGM snippets :-)

Maynard

Tristel (TSTL)

AGM statement

Here is the full text from December’s update:

—————————————————————————————————————-

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, will hold its Annual General Meeting today at 10am at Lynx Business Park, Fordham Road, Snailwell, Newmarket, Cambridgeshire CB8 7NY.

At the meeting Paul Swinney, Chief Executive Officer, will provide shareholders with the following update:

“We expect unaudited pre-tax profit (before share-based payments) for the first half to be no less than £2.8 million, compared to £2.4 million for the same period last year. The expected pre-tax profit includes a positive contribution from our operations in Belgium, the Netherlands, France and Italy which were all acquired during the past year. The Company is performing in line with management’s expectations and our United States regulatory approvals project is progressing well.”

Paul Barnes, Chairman, will add:

“On behalf of my Board colleagues I would like to welcome Dr Bruno Holthof to the Chair. Our Company will undoubtedly benefit from his very broad experience of global healthcare.”

—————————————————————————————————————-

Difficult to read too much into the quoted profit figures — TSTL’s profit is affected by US regulatory costs (£100k in the comparable H1 2019) and the purchase of Ecomed (a net £125k contribution in the comparable H1 2019). I will await February’s results to evaluate the group’s progress.

The comment “our United States regulatory approvals project is progressing well” is encouraging after TSTL scrapped giving any guidance for the project in February.

The latest (full-year) results said: “We are advancing our De Novo submission for Duo to the USA Food and Drug Administration and are awaiting feedback to our most recent pre-submission request to the agency. We expect to receive this before the end of 2019.”

So maybe the pre-submission feedback has been received and is positive?

Maynard

Tristel (TSTL)

Publication of 2019 annual report

The annual report was published during October 2019 at the time of the full-year results (reviewed in the blog post above). Some parts of the report were highlighted in the blog post, but some were not. Here are those extra snippets:

1) Management commentary:

The annual report did not contain any extra management commentary beyond what was stated in the results RNS.

2) Principal risks and uncertainties:

This note has changed:

For 2018, the note warned that “a significant reduction in the supply of funds to the National Health Service could negatively affect the Group’s revenues“:

The omission for 2019 suggests NHS funding is no longer a risk.

This note claims trade receivables are not concentrated:

Mind you, TSTL still services one large customers, the NHS supply chain, which represented revenue of £6.6m (25%) during 2019:

Revenue earned from the NHS supply chain climbed a very impressive 23% during 2019.

Total UK human healthcare revenue gained 12%, and all that gain (and a bit more) was represented by the additional spend by the NHS supply chain.

I am pleased no major product-quality mishaps were detected:

3) Director biography

The 2019 report includes the bio for the new non-exec — and now chairman:

A smart appointment — Dr Holthof has hands-on experience of running hospitals in the UK and the Netherlands.

4a) Director remuneration

Here is the director pay:

The chief exec and the FD did not receive pay rises last year.

The note below is interesting. The execs can collect only 3% of gross profit through their aggregate base salaries:

3% of £20,665k = £620k.

Base salaries for 2020 are £180k (B Leemans), £250k (P Swinney, up 8.6%) and £185k (E Dixon, up 2.8%) = £615k:

So for salaries to advance further for 2021, gross profit has to advance — which seems fair enough. Salaries do not appear obviously outrageous given the level of group profitability and the group’s recent progress.

Note that bonuses for 2019 represented 24% of salary — not extravagant when revenue (and perhaps profit) before acquisitions gained 10%.

The small-print now includes the word “normally” as to when salary reviews take place:

The small-print no longer refers to “that of the wider workforce of the Company” when looking at director salary levels — just “comparable organisations”.

Additional small-print confirms up to 15% pension contributions, further shareholder consultation on LTIPs and the cessation of granting options to non-execs:

I like how ordinary staff can be awarded 40,000 options if they complete 10 years of service:

The FD has exchanged her peculiar “change of control” options for a greater pay-off should TSTL be acquired:

A 185% “change of control bonus” equates to a £342k pay-off at the FD’s 2020 £185k salary.

87,500 options with a 65p exercise price would raise the same (net) £342k with the share price at 456p.

The shares were 294p when the 2019 results (and annual report) were published during October 2019. So perhaps the board felt at the time a 456p per share offer would be acceptable. The share price has recently traded at the 450p mark, and presumably the board would no longer consider 456p acceptable.

4b) Corporate governance

The corporate governance review brought three new key changes:

The third point is interesting. Succession planning has never been an obvious concern/risk.

I am not not sure whether this blog is counted as “popular“:

+++++++++++++++++++++++++++++++++

EDIT 23 OCT 2020

Annoyed I missed this at the time. The chief exec and finance director have got married:

+++++++++++++++++++++++++++++++++

I like “no-nonsense” companies:

I trust the “no-nonsense” culture will always be reflected in TSTL’s future financial reporting and disclosures.

The (now former) chairman claimed the board operated “effectively”:

I am not quite sure why the strategic goals include a share-price measure if that measure is ignored when the share price does down.

TSTL still likes to keep at least £3m in the bank:

TSTL continues to use the Buffett term “protective moat”:

5) Auditors

KPMG has replaced Grant Thornton of Patisserie Holdings fame:

Brexit became a key audit matter:

October 2019 was a bit late for the auditor to become more concerned about Brexit. TSTL had commendably outlined its Brexit plans 12 months beforehand.

Revenue recognition remained a key audit matter, but this time the matter concerned the possibility of revenue being misstated due to share-option incentives issued to management:

I can’t recall ever seeing such a key audit matter before.

Last year the revenue-recognition matter concerned “the high volume of transactions across various product categories and geographic regions gives rise to a risk that revenue may not have occurred.”

Audit materiality is the standard 5% of pre-tax profit while the full-audit scope was an acceptable c90% of revenue and profit:

6) IFRS 9 adoption

No impact:

7) Geographical segments

A bit sloppy to change the geographical revenue segment from Germany to Europe for 2019, but not restate the segment for 2018…:

…and then also leave the 2019 geographical asset segment as Germany:

8) Employees

Here are the details:

Productivity has improved to a new high. Revenue per employee is now £184k, versus £179k for 2018 and £137k for 2014.

Employee costs as a proportion of revenue is almost 33%, up from 30% for 2018 and matching levels seen in 2016 and 2013. The ratio has bobbed between 28% and 33% since 2011.

Exclude the directors’ emoluments from the sums, and rank-and-file employee costs are 27% of revenue, and have bobbed between 24% and 27% since 2015.

Rank-and-file employee costs have increased from £3.7m to £7.0m since 2015, and the average employee (excluding directors) now costs £51k, versus £48k-50k for 2016-2018 and £38k for 2015.

8) Operating expenses

Cost of inventories recognised as an expense is notable:

Cost of inventories recognised as an expense as a proportion of revenue was 20% for 2019 and 21% for 2018 and 2017. Very consistent.

Average stock levels last year were £2.7m — or 50% of the cost of inventories recognised as an expense of £5.4m. Stock therefore in theory sits in the warehouse for six months before being sold. Seems a long time, but past accounts have shown similar timescales and never signalled obvious problems with stock build-ups resulting in adverse cash conversion.

The operating expenses also disclose research costs down almost £250k on 2018. The £981k for 2018 may be an aberration, though, as the amount expensed for 2017 was £665k. Before that the expense was £251k or less.

9) Tax

TSTL enjoys some tax relief through patents and R&D:

Some companies benefit from share options with their tax charge.

TSTL has sizeable share-payment charges, yet does not recognise any accompanying tax benefit in the P&L. I am not sure why some companies (such as CLIG (point 10)) can enjoy a share-payment tax benefit, and some do not.

10) Trade receivables

Trade receivables show very welcome consistency:

Trade receivables as a proportion of revenue were 16% for 2019, versus 16%, 15%, 17%, 16% and 16% for the previous 5 years.

Provisions relating to trade receivables are minor and suggest little in the way of bad trade debts:

Past due figures include all other receivables as well as trade receivables, but the proportion past due, at 29% for 2019, is half-way within the wide 17% to 40% range seen since 2013:

11) Leases

The 1-year lease obligation suggests TSTL’s total leases have 6.5 years on average to run:

12) Trade and other payables

No concerns here:

Trade payables as a proportion of cost of goods sold = £1,989k / £5,504 = 36%. Suggests TSTL takes 3-4 months to pay its stock suppliers — although trade payables may include money owed for services recognised as admin expenses. Total payables at 36% of revenue is the highest since 2011 (37%) and suggests TSTL operates without undue pressure to pay its bills.

Maynard