13 October 2020

By Maynard Paton

Results summary for Andrews Sykes (ASY):

- “Resilient” half-year figures that showed revenue down 4% and profit up 2%.

- No light was shed on how ASY could sustain its performance when 50% of UK employees were furloughed.

- The statement confirmed bumper cash flow of £14m that prompted a special £10m dividend during the summer.

- The books remain healthy with high margins and net cash, although the pension scheme might require extra funds.

- A possible P/E of 17 does not appear completely outrageous for a seemingly pandemic-resistant business. I continue to hold.

Contents

- Event link, share data and disclosure

- Why I own ASY

- Results summary

- Covid-19, furloughed employees and special dividend

- Revenue, profit and dividend

- Financials

- Valuation

Event link, share data and disclosure

Event: Interim results for the six months to 30 June 2020 published 30 September 2020.

Price: 620p

Shares in issue: 42,174,359

Market capitalisation: £261m

Disclosure: Maynard owns shares in Andrews Sykes. This blog post contains SharePad affiliate links.

Why I own ASY

- Supplies air conditioners, portable heaters and industrial pumps for hire, with success based on a prompt 24/7 service, high-quality rental fleet and commercial-only customer base.

- Accounts regularly showcase high margins, generous cash flow, net cash and attractive returns on equity.

- Chairman and family are 90%/£234m shareholders and ensure management focuses on “long-term shareholder value creation” (point 3).

Further reading: My ASY Buy report | All my ASY posts | ASY website

Results summary

Covid-19, furloughed employees and special dividend

- This H1 statement did not shed any light on ASY’s mysterious furlough process.

- To recap, the small-print within May’s annual results stated:

“In the UK, approximately 50% of our employees are furloughed.”

- Those FY 2019 results also claimed:

“In the UK… [t]he impact on the business as of the end of March has been limited with trading levels close to expectation.”

- How the UK business could trade “close to expectation” with 50% of employees sat at home was unclear then and remains unclear now.

- The annual results also admitted many European employees had received state support:

“In France, Italy, Belgium and Luxembourg we are currently working with significantly reduced staff levels, with most of our staff enlisted to the appropriate government employment retention schemes.”

- The final dividend declared within those FY 2019 results therefore seemed questionable given the apparent receipt of overseas government assistance.

- Roll on to July, and ASY announced a special dividend (23.7p per share) that was greater than the entire 2019 full-year payout (22.4p per share).

- And now to this H1 statement, which gave this explanation for the special dividend:

“This [special] dividend was paid out of the group’s substantial brought forward cash reserves accumulated from previous years trading, a proportion of which were surplus to the group’s requirements and were therefore returned to shareholders.”

- ASY paying a special dividend while furloughing staff certainly feels wrong.

- Unless of course any government money received has now all been handed back.

- As mentioned earlier, how 50% of UK staff could have been furloughed and the business still deliver these creditable H1 figures remains unclear.

- However, the furlough/special dividend situation does offer shareholders some positives:

- The lockdown may have inadvertently showed ASY how to operate with fewer employees.

- The special dividend was indeed funded by bumper cash flow (see Financials) and (seemingly) not declared solely to shore up the chairman’s other business interests.

- The ‘going concern’ cash flow projections within the FY 2019 results — which implied very little profit for the nine months to December 2020 — can now be shelved.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue, profit and dividend

- ASY described its lockdown performance as “resilient”.

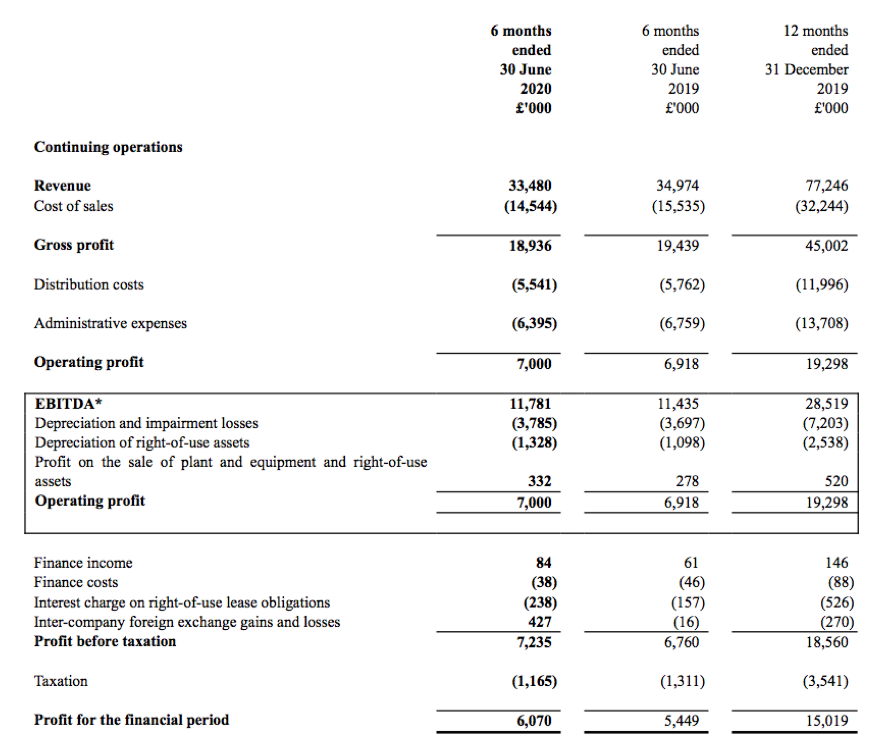

- Revenue fell 4% while profit improved 2%:

| H1 2018 | H2 2018 | H1 2019| H2 2019 | H1 2020

| | |||

| Revenue (£k) | 37,815 | 40,748 | 34,974 | 42,272 | 33,480 | ||

| Operating profit (£k) | 9,280 | 11,401 | 6,918 | 12,380 | 7,000 |

- H1 revenue was the weakest since 2016.

- ASY’s progress is typically bolstered by extreme weather. The H1 2018 performance for example was boosted by a scramble for portable heaters during heavy snow and then for air conditioners during a heatwave.

- H1 UK revenue remained at £21m — a remarkable performance given the aforementioned furlough process.

- ASY’s blog describes various contracts won during the first half, including:

- European sales dropped 14% after being “significantly affected by a combination of the coronavirus pandemic and mild weather”.

- Revenue within the Middle East and Africa fell 4%.

- The geographic revenue split was 62% UK, 21% Europe and 17% Middle East/Africa.

- Up until May’s annual results, ASY had declared 12 consecutive 11.9p per share interim/final dividends.

- The FY 2019 final dividend was then reduced to 10.5p per share.

- However, this H1 declared a return to a 11.9p per share (interim) payout.

Financials

- ASY’s accounts remain in good shape.

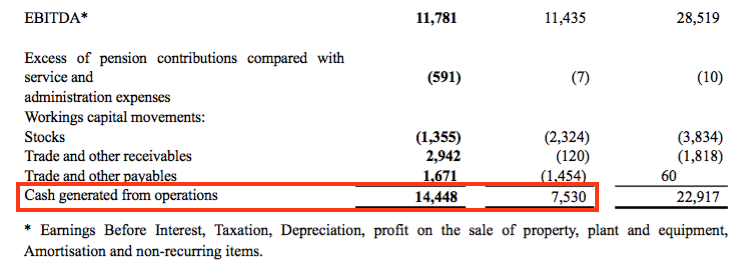

- Cash flow was enhanced by favourable working-capital movements:

| 2015 | 2016 | 2017 | 2018 | 2019 | H1 2020 | |

| Operating profit (£k) | 13,208 | 15,816 | 17,589 | 20,681 | 19,298 | 7,000 |

| Working-capital movements | ||||||

| Stocks (£k) | (1,024) | (2,251) | (1,022) | (2,682) | (3,834) | (1,355) |

| Trade and other receivables (£k) | (2,196) | (1,876) | 563 | (2,139) | (1,818) | 2,942 |

| Trade and other payables (£k) | 139 | 1,970 | (696) | 529 | 60 | 1,671 |

| Total (£k) | (3,081) | (2,157) | (1,155) | (4,292) | (5,592) | 3,258 |

- ASY typically injects cash into working capital each year, so the cash release during this H1 was very unusual.

- Indeed, net cash from operations of £14m during this H1 was nearly double that produced during the comparable period:

- Somewhat oddly, the results RNS did not refer to the bumper cash flow at all.

- The cash flow reported in this H1 contrasted with the warning given within the FY 2019 results:

“Our cash flow forecast assumes that cash collections will reduce over the next nine months as customers take longer to settle their debts.”

- Cash flow clearly did not suffer as badly as the forecast had projected.

- Cash flow during this H1 funded last year’s £4.4m final dividend and added a further £3.9m to the bank.

- Cash at the half year was £32.1m, with conventional debt at £3.5m to give net cash of £28.6m.

- The aforementioned special dividend was paid in August and cost £10m.

- ASY presumably deems any net cash beyond £18.6m (i.e. the half-year net cash of £28.6m less the £10m special dividend) to be surplus to requirements.

- The £18.6m net cash still on hand but not paid as a special dividend may therefore be essential for the business to operate.

- ASY has carried net cash since 2010.

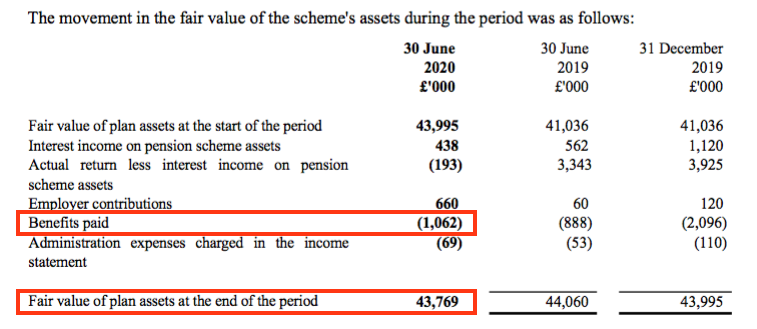

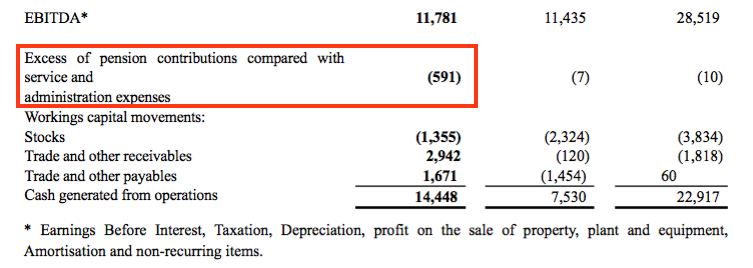

- ASY’s defined-benefit pension scheme continues to enjoy an accounting surplus.

- Despite the surplus of £479k, a £600k one-off contribution was injected into the scheme during this H1:

“The next formal triennial funding valuation is due as at 31 December 2019. This is currently being worked upon and, subject to unforeseen circumstances, should be presented to the board of directors in the Autumn.

A draft funding valuation was presented for discussion in the Summer and the group made a one-off contribution of £600,000 in late May 2020 to largely eliminate the indicative funding deficit as at 31 December 2019.

In addition, the group has continued to make regular monthly contributions of £10,000 per month during 2020 and therefore the group anticipates that total contributions to the defined benefit pension scheme during 2020 will be at least £720,000.”

- To cut a long actuarial story short, pension accounting surpluses and deficits do not always reflect the true-life demands of a final-salary plan.

- Important pension-scheme figures to consider are the benefits being paid and the plan’s asset value:

- For ASY, paying annual benefits of £2.1m from scheme assets of £43.8m requires an investment return of 4.5%.

- I am not convinced ASY’s standard contributions of £120k a year are enough to sustain benefits of £2.1m should a market slump erode the £43.5m scheme assets.

- Note that extra pension contributions bypass the income statement — with the cash flow statement highlighting the expense:

- I expect ASY’s FY 2020 results due in May next year will reveal the outcome of the triennial scheme review and any revised contributions.

- Despite the pandemic, ASY’s H1 operating margin was a healthy 20% that reflected a “favourable business mix”.

- ASY’s business consistently enjoys positive economics. The full-year operating margin has topped 20% since 2002.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- ASY’s blog indicates the company had a busy summer supplying cooling equipment:

- The busy blog and this resilient H1 performance could mean judging H2 profit may not be complete guesswork.

- A repeat of last year’s H2 performance may in fact be very plausible for FY 2020.

- If so, FY 2020 operating profit (less IFRS 16 interest costs) would be £18.8m.

- Applying tax at the UK standard 19% would then give earnings of 36.1p per share.

- ASY remains a tightly held share with a very wide bid-offer spread.

- The 100-year-old chairman and his family own almost 90%, leaving approximately 10% for everybody else.

- A 620p mid-price values ASY at £261m and the free float at £27m.

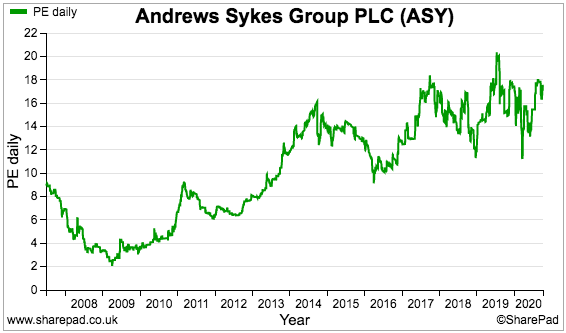

- Making no adjustments for the retained cash or pension contributions, the P/E could be 620p / 36.1p = 17x.

- The multiple does not appear completely outrageous for a high-margin, cash-rich and apparently pandemic-resilient business.

- The trailing 22.4p per share dividend meanwhile supplies a 3.6% income at 620p.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Another excellent analysis Maynard, I always enjoy reading your extensive analysis which is very thorough, well researched and thought through.

I’ve been a holder of Andrew Sykes for 4 years and enjoy the relative resilience of the company and the good yield on my purchase price £3.71. The free float has always been a bit of a concern with regard to liquidity and the spread and makes me hesitant to add to my holding. However as we learn from Lord Lee investing in companies where family members / owners have large stakes can be a good insurance that the company won’t take unnecessary risk. The good cash management here at ASY is testament to that.

Hello Steven,

Thanks for the comment and I am glad you like the article. Yes, the free float can be a concern and quite often readers here have queried the chance of a delisting. I did ask ASY’s management about why the company has a quote, and I was told the chairman and family like the financial reporting/discipline that a listing provides. The chairman/family are all ‘hands-off’ investors. Can be hard to pick up stock, but keen sellers do occasionally drive the price notably lower.

I should add that the furlough ‘mystery’ may well be due to ASY furloughing staff for only a few weeks, and perhaps bumper trade before and after the worst of the lockdown made up the shortfall. I don’t know.

Good point on Lord Lee. ASY, S&U, M Winkworth and FW Thorpe are all blessed with large family managers/owners and have each released resilient statements of late — despite not operating within obviously defensive/pandemic-proof sectors. I am hopeful these businesses will take market share once the dust settles.

Maynard

Steven, you need to calculate yield on the current market price not on your £3.71 purchase price as the opportunity cost of holding the shares is the lost opportunity of reinvesting today’s market value elsewhere. The purchase price is only relevant to capital gains calculated on a CAGR basis.

The other point that I would like to make is that investing in heavily family owned businesses also has its downside. In relation to the 100 year old chairman, his personal holding will at some point in the not too distant future be left in a will to family members and perhaps charities. How many of the beneficiaries may choose to cash in their inheritance? Do you agree that this is a huge risk in terms of market pricing particularly for such an illiquid stock.

Hi James,

The other point that I would like to make is that investing in heavily family owned businesses also has its downside. In relation to the 100 year old chairman, his personal holding will at some point in the not too distant future be left in a will to family members and perhaps charities. How many of the beneficiaries may choose to cash in their inheritance? Do you agree that this is a huge risk in terms of market pricing particularly for such an illiquid stock.

Jumping in ahead of Steven here, and yes nobody knows what the beneficiaries will do. If the beneficiaries all want out, they are far more likely to sell to a trade bidder than sell in one go into the stock market. The beneficiaries may sell parts to institutions, too, which may in turn reduce the bid offer spread :-) The real danger is not so much any selling, but the chairman’s son (or whoever else becomes chairman) implementing an adverse business strategy that results in reduced earnings (and dividends!).

Maynard

I have been watching Andrews Sykes as a target investment. I have identified the company as having favourable fundamentals, however my issue is the bid/ask spread on this stock. Today it is being quoted 500/600 which means that if I go long at 600 I need the stock to appreciate by 20% just to break even. Said differently, I am down 20% on the day I take the position.

This leads me to another issue that I have with the company. They are generating healthy levels of cash year on year which is good. Growing cash balances suggest that either there is no opportunity to invest the cash to grow the business either organically or by way of acquisition which is a shame. So the Board decides to return capital to shareholders. Fair enough. However, returning cash in the form of dividends and special dividends is not, in my opinion, in the best interest of shareholders and I shall explain my reasoning:

(1) A shareholder receiving a dividend is seeing his portion of corporate earnings subjected to double taxation. Dividends are paid out of net income after corporate taxes on earnings have been paid and then the shareholder is required to pay income tax on the dividend! Madness. This is why the likes of Warren Buffett refuses to pay dividends.

(2) If a shareholder receiving a dividend wishes to reinvest that money in the company then he/she only has the net proceeds to reinvest after the double taxation and, as alluded to earlier, is required to cross a bid/ask spread of 20%. So every £100 of corporate operating earnings become £75 after 25% corporation tax is applied, then become £45 after 40% income tax and then after crossing the 20% spread buys the equivalent of £36 of company equity!

At current stock market valuations the sensible thing for the company to do would be to repurchase its own stock (if there are no other companies to acquire then it is often worth acquiring your own company!) A great deal could be learned from reading about the likes of the great CEO Henry Singleton (Teledyne).

My suggested approach would return capital to shareholders in the form of enhancement of equity valuations; and, if the shareholder wishes to reinvest in the company then that is already achieved in the most efficient manner (having avoided the excessive taxation and, one would imagine, at a more favourable price to the 20% spread available in the market). More particularly, shareholders may choose when to cash in their equity in a manner which is most tax advantageous to the individual rather than, in the alternative, at a time dictated by the company when dividends are paid.

This type of family company has nepotism at its heart: keeping the management in the family means that finding the best man to run the business is a secondary consideration to finding a man with the correct surname.

I welcome your comments.

How do you deal with the 20% bid/ask spread?

http://www.theinvestment.company

Hi James

Thanks very much for the comment.

I have been watching Andrews Sykes as a target investment. I have identified the company as having favourable fundamentals, however my issue is the bid/ask spread on this stock. Today it is being quoted 500/600 which means that if I go long at 600 I need the stock to appreciate by 20% just to break even. Said differently, I am down 20% on the day I take the position.

Yes, the wide spread is a result of the main family shareholders owning 90% of the stock and the company keeping a low profile. You may be able to deal inside the quoted spread and I cannot recall what the quoted spread was when I bought during 2013.

True, you have a 20% paper loss just after purchase, so this is a stock for patient investors only with an optimistic view of the company. I have been patient and optimistic and enjoyed decent capital gains and dividends during the last 7 years. But I recognise today’s buyers may not be as fortunate during the next 7 years.

This leads me to another issue that I have with the company. They are generating healthy levels of cash year on year which is good. Growing cash balances suggest that either there is no opportunity to invest the cash to grow the business either organically or by way of acquisition which is a shame. So the Board decides to return capital to shareholders. Fair enough. However, returning cash in the form of dividends and special dividends is not, in my opinion, in the best interest of shareholders and I shall explain my reasoning:

(1) A shareholder receiving a dividend is seeing his portion of corporate earnings subjected to double taxation. Dividends are paid out of net income after corporate taxes on earnings have been paid and then the shareholder is required to pay income tax on the dividend! Madness. This is why the likes of Warren Buffett refuses to pay dividends.

(2) If a shareholder receiving a dividend wishes to reinvest that money in the company then he/she only has the net proceeds to reinvest after the double taxation and, as alluded to earlier, is required to cross a bid/ask spread of 20%. So every £100 of corporate operating earnings become £75 after 25% corporation tax is applied, then become £45 after 40% income tax and then after crossing the 20% spread buys the equivalent of £36 of company equity!

Double taxation affects all UK quoted companies, not just ASY, and company managements can’t change tax laws. At least for UK private investors, investments are protected from income (and capital gains) tax though ISAs and SIPPs, so no further tax is payable on the dividend received within these shelters.

Long ago the double taxation issue was circumvented by something called ACT (https://en.wikipedia.org/wiki/Advance_corporation_tax) but all that was scrapped.

Mr Buffett may refuse to pay dividends via Berkshire, but his common stocks continue to pay Berkshire dividends and (presumably) Mr Buffett suffers double taxation as a result. I am not sure what he thinks about that.

The alternative is companies keeping all of their retained profits, either to simply hoard or reinvest. Reinvesting just for the sake of reinvesting is probably asking for trouble with most companies. Hoarding cash is not great either, and I suspect governments would fiddle with tax laws if hoarding levels reached unacceptable levels and affected the tax take. Ultimately every company exists to distribute actual cash to the pockets of shareholders.

At current stock market valuations the sensible thing for the company to do would be to repurchase its own stock (if there are no other companies to acquire then it is often worth acquiring your own company!) A great deal could be learned from reading about the likes of the great CEO Henry Singleton (Teledyne).

ASY can’t really buy back stock because the family shareholders already own 90%. The firm might as well delist instead of buying back shares. But management has told me the family like the listing because the family are hands-off investors and like the financial reporting/discipline that a listing requires. So I doubt we will see a buyback.

Buybacks generally are not really proven to generate great returns, at least for UK companies. Most buybacks are performed when prices are high and are suspended when prices are low. For every Henry Singleton there are hundreds of managers who have overseen buyback blunders. The history of BP’s buybacks for example are shocking.

That said, I would have no problem investing alongside the ‘next Henry Singleton’, assuming I can find him/her.

My suggested approach would return capital to shareholders in the form of enhancement of equity valuations; and, if the shareholder wishes to reinvest in the company then that is already achieved in the most efficient manner (having avoided the excessive taxation and, one would imagine, at a more favourable price to the 20% spread available in the market). More particularly, shareholders may choose when to cash in their equity in a manner which is most tax advantageous to the individual rather than, in the alternative, at a time dictated by the company when dividends are paid.

That is fair enough. You just have to ensure the dividend cash that builds up inside the company is generally reflected in the share price.

On this wider subject, I am reminded of the old adage that the tax tail should not wag the investment dog!

This type of family company has nepotism at its heart: keeping the management in the family means that finding the best man to run the business is a secondary consideration to finding a man with the correct surname.

ASY’s family management are directors, but are hands-off directors. The day-to-day running of the business is done by ‘professional’ managers and the MD’s surname is Wood while the chairman’s surname is Murray :-)

Thanks

Maynard

I did not realise ASY’s chairman had handed his shareholding over to his children in 2008:

https://maynardpaton.com/2021/01/01/my-portfolio-year-in-review-2020/#comment-12862

So the inheritance worry has already been resolved.

Maynard

Andrews Sykes (ASY)

Paul Wood published 28 January 2021 and Senior Management Appointment published 17 December 2020

Sad news about ASY’s managing director:

———————————————————————————————————–

The board of Andrews Sykes (the “Board”) is deeply saddened to announce the death of its long-serving Managing Director, Paul Wood, aged 58, who has passed away after a short illness. Our thoughts and prayers are with Paul’s family and all his colleagues across the Group, many of whom have worked with Paul for many years.

Paul himself worked for the Group for the whole of his working life, joining from school in 1978. Having risen to the top of the business, his leadership has been exemplary, and he has delivered excellent and consistent returns for shareholders.

Equally, he has built a strong management team around him and in Carl Webb we have a fine leader who has been the Group’s acting Managing Director since Paul’s illness was announced.

———————————————————————————————————–

The news about Mr Wood follows the appointment of a new finance director. The previous FD left during January 2020, and as far as I can tell ASY had been without a proper FD since. The FD vacuum did not seem to affect ASY’s performance during the pandemic.

Here is the full text:

———————————————————————————————————–

The board of Andrews Sykes (the “Board”) is pleased to announce the appointment of Ian Poole as Finance Director. He will join the Company with effect from 22 February 2021 and his responsibilities will encompass all of the financial affairs of the Andrews Sykes group companies, reporting directly to the Board, although he will not himself be a statutory director of the Company.

Ian Stuart Poole (aged 37) has over 16 years’ experience as a finance professional. He joins Andrews Sykes from Incorporatewear Ltd, the UK subsidiary of Australian uniforms solutions business, The Workwear Group, where he was responsible for all financial analysis, controls and reporting as well as IT matters. Prior to this he spent seven years at Chamberlin Plc, the AIM listed foundry and light engineering business, initially as Group Financial Controller and including a period as acting Group Finance Director.

Ian Poole is a qualified chartered accountant having started his career at BDO LLP after graduating with a BSc in Accounting & Finance from the University of Birmingham.

Commenting on the appointment, Paul Wood, Managing Director of Andrews Sykes, said:

“We are pleased to announce that Ian Poole will be joining our senior management team, he brings with him a strong track record in financial management and we look forward to welcoming him to Andrews Sykes.”

———————————————————————————————————–

We can only wait and see how these leadership changes impact ASY.

Maynard