20 December 2019

By Maynard Paton

Results summary for System1 (SYS1):

- Another unremarkable performance, with underlying gross profit up 4% and profit (without AdRatings) rebounding 24% due mostly to improved cost control.

- The start-up AdRatings service continues to lose £2m a year and is increasingly dictating the company’s progress, potential and valuation.

- An ITV competition to determine the most “emotionally engaging” advert during Euro 2020 could create extra recognition for System1-type marketing and SYS1’s services.

- The accounts remain cash rich and the business (without AdRatings) exhibited a healthy 21% margin.

- The P/E could be anywhere between 8 and 26 depending on how AdRatings, share-based payments and the cash position are viewed. I continue to hold.

Contents

- Event links and share data

- Why I own SYS1

- Results summary

- Revenue, profit and dividend

- Divisions

- AdRatings

- Industry developments

- ITV Euro 2020 competition

- Financials

- Valuation

Event links and share data

Event: Interim results and presentation for the six months to 30 September 2019 published 07 November 2019

Price: 210p

Shares in issue: 12,576,619

Market capitalisation: £26.4m

Why I own SYS1

- Market-research agency that predicts the long-term effectiveness of client adverts, with success built upon a “difficult-to-replicate” database of advert assessments created over 20 years.

- Boasts founder/entrepreneurial/owner-friendly chief exec who has overseen an acquisition-free growth record, retains a 23%/£6m shareholding and has declared five special dividends.

- Offers cash-rich accounts, high underlying margins and a potentially low valuation — assuming the new AdRatings service can one day break even.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

Revenue, profit and dividend

- Annual results issued during June followed by a trading statement published during October had already heralded these unremarkable first-half numbers.

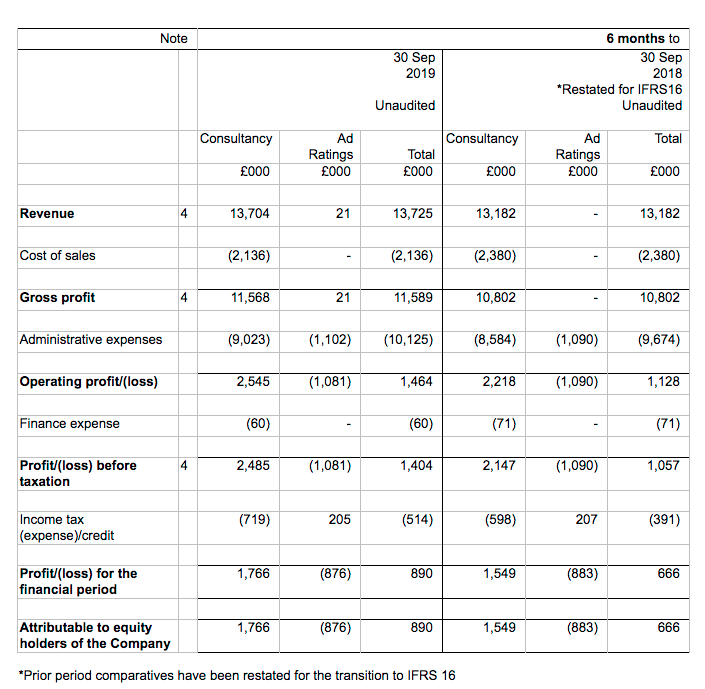

- Gross profit — SYS1’s main top-line performance indicator— was indeed up 7% (to £11.6m) while pre-tax profit (before share-based payments and AdRatings losses) was indeed £2.4m (up 24%).

- Three factors complicated SYS1’s profit progress:

- A £251k exceptional gain recorded during the comparable H1 and accounted for within operating profit;

- The introduction of IFRS 16, whereby operating lease costs are now partly recognised as a finance expense, and;

- Share-based payments, which were credits during this H1 and the preceding H2.

- A £251k exceptional gain recorded during the comparable H1 and accounted for within operating profit;

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Revenue (£k) | 13,822 | 13,117 | 13,182 | 13,714 | 13,704 | ||

| Gross profit (£k) | 11,394 | 10,837 | 10,802 | 11,245 | 11,568 | ||

| Admin costs* (£k) | (10,325) | (9,698) | (8,794) | (9,422) | (9,109) | ||

| Operating profit (£k) | 1,069 | 1,139 | 2,008 | 1,823 | 2,459 | ||

| IFRS 16 finance cost (£k) | - | - | (72) | (65) | (60) | ||

| Operating profit less finance cost (£k) | 1,069 | 1,139 | 1,936 | 1,758 | 2,399 | ||

| Share-based payments (£k) | (229) | 6 | (41) | 173 | 86 | ||

| Exceptional item (£k) | - | - | 251 | - | - |

(*excludes exceptional item and share-based payments)

- Adjusting for the £251k exceptional gain and the share-based payments, but including the IFRS 16 finance cost, ‘underlying’ profit before tax increased 24% from £1.9m to £2.4m.

- The 24% improvement simply reflects gross profit growing by 7% and costs increasing by 4%.

- Bear in mind that the comparable H1 2019 was somewhat lacklustre, with competitive pricing and re-designed products causing a sub-par performance twelve months ago.

- SYS1 admitted gross profit growth for this H1 at constant currency rates was only 4%.

- Indeed, gross profit was only 2% higher than the gross profit reported for H1 2018.

- The 2019 annual results reminded shareholders that gross profit has compounded at only c5% per annum since 2012.

- SYS1 confessed that growth during this H1 was “not yet on the trajectory we are aspiring to”.

- A notable development was the maintained 1.1p per share dividend.

- This time last year SYS1 said: “[The] final dividend may be reduced, depending principally on the scale of further investment in AdRatings and on opportunities to repurchase shares at an attractive valuation.”

- The subsequent annual results revealed an unchanged final 6.4p per share payout:

“Given the investment opportunities with AdRatings, and a share price which some consider depressed, the decision to maintain the dividend was considered carefully.

- However, the door was seemingly left ajar for a future dividend cut:

“Whilst the Board is prepared to consider reducing the dividend (as flagged in our [2018] Interim Statement), it views maintenance of the dividend as a useful discipline which it seeks to adhere to unless there is sufficiently clear-cut reason otherwise (which, in the Board’s view, is not the case at this time).

- A dividend cut could still be forthcoming. This results RNS said: “We are keeping this [dividend] policy under review”

- Perhaps sustaining the dividend rather than ploughing even more money into AdRatings (see AdRatings below) and/or repurchasing shares tells us something about the prospects for both AdRatings and the share price.

Divisions

- SYS1 operates three market-research divisions.

- SYS1 has claimed its “main competitive strength” lies within its Communications division, which assesses televisions adverts and has “developed market research techniques which we believe are better able to predict the long-term effectiveness of advertising than anyone else’s.”

- The Brand division tracks ongoing client-brand popularity, while the Innovation division tests new marketing concepts.

- The Communications division should offer the best growth prospects and the widest ‘moat’ to shareholders. Brand is apparently the more reliable of the three income sources, while Innovation is apparently the most unpredictable.

- The table below summaries the gross-profit contributions from each department:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Comms (£k) | 3,582 | 3,412 | 3,059 | 4,313 | 3,608 | ||

| Brand (£k) | 2,102 | 2,409 | 1,726 | 1,973 | 1,628 | ||

| Innovation (£k) | 4,381 | 4,023 | 4,929 | 4,057 | 5,135 | ||

| Other (£k) | 1,168 | 781 | 978 | 589 | 1,068 | ||

| Agency (£k) | 161 | 212 | 110 | 316 | 129 | ||

| AdRatings (£k) | - | - | - | - | 21 | ||

| Total (£k) | 11,394 | 10,837 | 10,802 | 11,248 | 11,589 |

- Communications gross profit gained 18% on the comparable H1 2019 — but this 18% leap appears to be an anomaly.

- Communications gross profit for this H1 was actually equal to that achieved for H1 2018.

- Full-year Communications gross profit improved by 5% during 2019, and was only 3% higher than the level recorded during 2016.

- The numbers do not suggest the more attractive Communications division is growing at a particularly impressive rate.

- Communications gross profit as a proportion of group gross profit has increased from 28% to 33% since 2016.

- SYS1 therefore remains somewhat dependent on progress within the less trail-blazing Brand and Innovation operations.

AdRatings

- The new AdRatings service continues to earn a pitiful income — just £21k during the last six months.

- To recap what AdRatings offers:

“AdRatings is a large database showing ‘ratings’ or ‘scores’, of adverts in the market as a whole. It allows clients to assess the effectiveness of their historical advertising and benchmark it against peer companies, competitor categories and the industry as a whole.”

- This results RNS described AdRatings as “the world’s largest, and most predictive and validated database of short and long-term advertising effectiveness”

- AdRatings is based on the ad-testing performed by the Communications division and — according to SYS1 — no other source of advert ratings “correlates with long-term profitability” the way AdRatings does.

- The AdRatings database now contains more than 42,000 analysed adverts for subscribers to study.

- The AdRatings analysis appears to be accurate:

- And yet paying AdRatings subscribers can be counted on one hand (or even one finger).

- Why are SYS1’s current 246 clients not interested?

- Management comments at the AGM during August revealed:

- Interested clients require “validation” — they want to see market-share changes in their particular advertising category correlate to changes to SYS1’s star ratings for the relevant adverts. SYS1 has correlation evidence for only certain advertising categories. Work is underway to ensure all categories have such validation.

- The low (£2k/month) subscription cost of AdRatings has meant the service has still to reach the attention of chief marketing officers (CMOs) — who can’t justify their time evaluating a £24k a year product.

- Interested clients require “validation” — they want to see market-share changes in their particular advertising category correlate to changes to SYS1’s star ratings for the relevant adverts. SYS1 has correlation evidence for only certain advertising categories. Work is underway to ensure all categories have such validation.

- Attracting the attention of CMOs is important to SYS1.

- Management comments at the AGM claimed CMOs generally accept the benefits of System1-type advertising and are open to experiment.

- Trouble is, a CMO’s team is often risk-averse and wishes to keep using existing suppliers/methods/data rather than throw away years of work and restart using other suppliers/methods/data.

- This results RNS said AdRatings had been “a factor… in our gaining much greater access to marketing leaders in large multinationals”.

- I am hopeful this “greater access” can lead to extra revenue in time.

- SYS1 claimed AdRatings offers “in the longer term… high upside potential”.

- £1.2m was spent on AdRatings during the last six months, and the total cost to date has been £4.2m.

- Total AdRatings revenue to date has been £24k.

- The 2019 results had revealed a £2.5m AdRatings budget for the current year.

- These H1 results implied the full-year cost could be less than £2.4m (before tax).

- Management comments at the AGM indicated AdRatings was becoming an integral part of the business —rather than a standalone operation that could (in theory) be scrapped.

- The AdRatings costs should therefore not be ignored for valuation purposes.

- The 2019 results disclosed AdRatings expenditure consisted of £1.08m for data collection, £1.55m for IT development work and £0.4m for running/other expenses.

- AdRatings costs would therefore reduce to £1.5m per annum were the IT development work to cease completely.

- The AdRatings costs could of course be offset by additional subscribers and/or extra revenue from SYS1’s other services.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Industry developments

- These H1 results referred to a new SYS1 book called Lemon:

- SYS1 said: “Lemon sets out why advertising effectiveness has been in decline over the last few decades and what it will take to reverse the decline at a profound level — and it has received wide industry endorsement.”

- The book was published by the Institute of Practitioners in Advertising (IPA) and costs £53 (or £28 for IPA members).

- I suppose the “wide industry endorsement” for Lemon could help sales of the book exceed the £24k income from AdRatings.

- A free PDF summary of Lemon is available here. The gist is that adverting has become “flat, abstract, dislocated and devitalised” and ought to become more creative and to produce greater emotional reactions.

- Whether Lemon will lead to major changes to multinational advertising campaigns remains to be seen.

- IPA experts Les Binet and Peter Field published a book with a same broad conclusion back in 2012 (PDF here):

“Emotional campaigns, and in particular those that are highly creative and generate powerful fame/buzz effects, produce considerably more powerful long-term business effects than rational persuasion campaigns.”

- Judging by SYS1’s recent progress, few in the industry appear to have read either book.

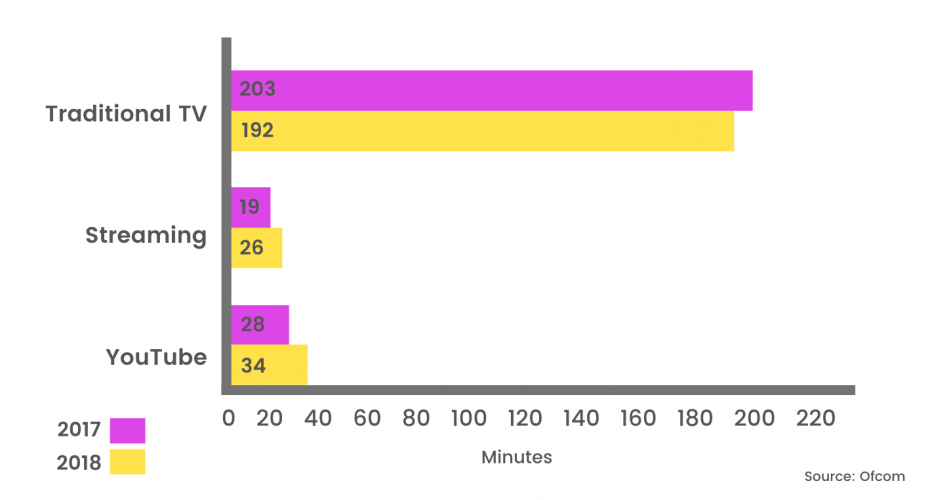

- Perhaps television advertising is shrinking and adverts work differently online.

- According to SYS1 rival Nielsen, UK television advertising revenue was £5.1b during 2018 — the same as for 2017.

- Funnily enough, online businesses remain the largest spenders on UK television adverts.

- For instance, Amazon spent £60m (up 21%) to broadcast UK television adverts during 2018.

- Meanwhile, websites such as Monzo and Sosander have enjoyed bumper demand following their initial television ventures.

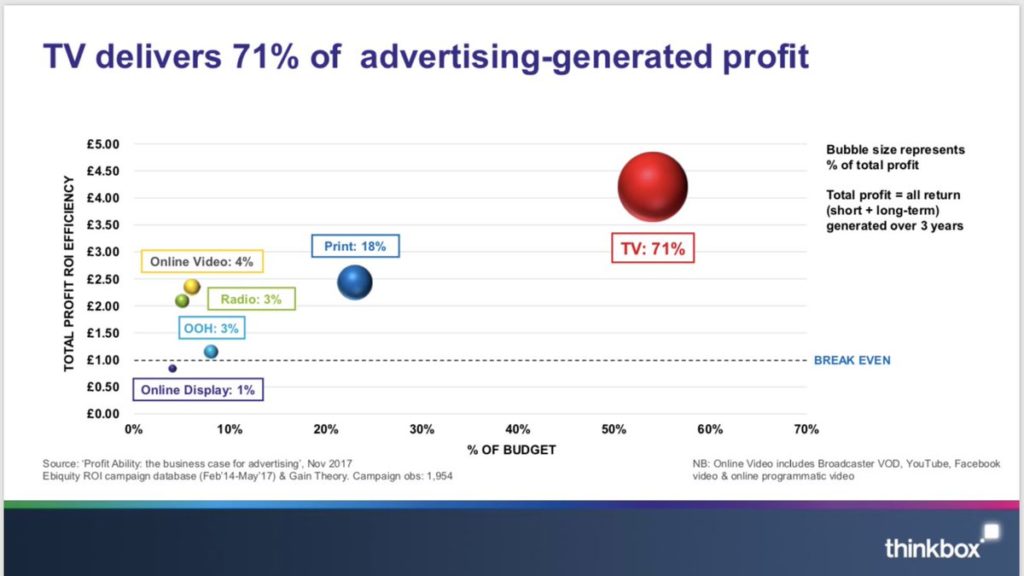

- Advert consultancy Thinkbox claims television remains the most profitable medium for advertisers:

- Marketing expert Mark Ritson reckons “TV’s death dive continues to be overstated and misinformed”.

- Mr Ritson writes: “I have nothing really to say in my column this week other than a) look at the bar chart and b) no, really LOOK at it…”

- As far as I can tell, the purported health of television advertising can’t really explain SYS1’s stalled performance since the name change from BrainJuicer during 2017.

ITV Euro 2020 competition

A potentially significant industry development comes from ITV:

“ITV is the latest media owner to launch a Channel 4-style competition to win free ad space, this time for a prime slot during the Euro 2020 final to the advertiser with the “most emotionally engaging campaign”.

“The broadcaster hopes a competition for free ad space will also improve the quality of the campaigns that run during the major football tournament. Commercial director Simon Daglish said it will work with an “independent research company” to judge the most “emotionally engaging” campaigns from a brand or agency.”

- ITV encouraging multinationals to develop “emotionally engaging” adverts ought to be of enormous assistance to SYS1.

- SYS1 may even be the mystery “independent research company” that performs the judging.

- ITV’s competition could have been encouraged by SYS1’s verdict on the adverts shown during the England-Croatia World Cup semi-final:

- “The biggest night for commercial TV ever” was apparently fairly typical for adverts.

“Humble 20-second ads [including Alpecin Shampoo’s bizarre “Fight For Your Hair!”] shared space with expensive-looking marquee campaigns from BT Plus and Samsung.”

“A third of the ads tested… ended up with 1-Star, suggesting that — from a brand-building perspective — the money was largely wasted.”

- I am hopeful this ITV competition — and the influence the competing adverts will have on their respective product sales — will prompt more companies to consider SYS1’s services.

Financials

- SYS1’s accounts remain reasonably straightforward.

- Cost cuts and product changes during recent years allowed pre-tax profit — before AdRatings and share-based payments — to represent a healthy 21% of gross profit for this H1 (versus 17% for full-year 2019).

- Cash conversion was not great during the six months.

- Total earnings of £860k had to fund additional working capital of £616k and dividends of £804k. A very low tax payment kept the cash outflow to £306k.

- Cash ended the half at £4.1m.

- Total AdRatings expenditure was £1,274k, of which £232k was capitalised on to the balance sheet and avoided the income statement.

- This capitalised expenditure will be amortised through the income statement during the next three years.

- The carrying value of the capitalised AdRatings costs is now £885k.

- SYS1’s books remain free of bank debt and free of pension obligations.

Valuation

- Assessing SYS1’s valuation requires a view on share-based payments and the prospects for AdRatings.

- The vagaries of IFRS 2 have meant SYS1 has recorded share-based payment credits for the last twelve months.

- The credits reverse earlier share-based payment charges, after the likelihood of options becoming exercisable reduced considerably.

- The 2019 annual report indicates 355,823 options have vested, which if exercised would increase the share count by 3% to 12,932k (and raise £61k for SYS1).

- Calculating earnings per share using this enlarged share count seems a better way of accounting for options than the fluctuating IFRS 2 charge.

- SYS1’s other options all require the share price to reach 500p (or more) before potential vesting.

- I will be delighted to revisit my option sums when the share price reaches 500p.

- Pre-tax profit excluding share-based payments were almost £4.2m for the twelve months to September 2019.

- Earnings come to £3.0m, or 23.1p per share, after applying the 29% tax used in these results and the 12,932k option-adjusted share count.

- Assume the net present value of AdRatings is zero, SYS1’s 210p share price is 9 times the 22.9p per share earned by the rest of the group.

- Assume SYS1 will soldier on with AdRatings losing £2.0m a year after tax for ever, and ongoing earnings could be 7.9p per share to support a 26x rating.

- Assume the cash position of £4.1m, or 31.7p per share, is surplus to requirements, and the cash-adjusted multiples range from 8x to 23x.

- The likely earnings outcome — at least for the next few years — could be mid-way between 22.9p and 7.9p per share, which points to a 15x cash-adjusted multiple.

- SYS1’s outlook comments did not hint at an immediate return to superior growth:

“We continue to have limited short-term revenue visibility, so, as always, it is difficult to predict how the year will unfold. Nevertheless, we continue to believe that the business is making progress and in the longer term has high upside potential driven by its AdRatings asset and the more general digitisation of the business.”

- The trailing 7.5p per share dividend supplies a 3.6% income at 210p, and is just about covered by the above 7.9p per share earnings estimate.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in System1.

System1 (SYS1)

New Employees

Forgot to mention this from the results statement:

“Across the business as a whole, we are investing ever more in Talent. During H1 we recruited 2 new members to our management team: Karen Wolfe (formerly Vice President Customer Success at Nielsen), as Chief Commercial Officer, and Jon Evans, (formerly UK Marketing Director at Lucozade Ribena Suntory) as Chief Marketing Officer. They follow Stefan Barden (Board Adviser – previously CEO of Wiggle) and Mark Beard (Chief Information Officer – formerly Group Head of IT at Wiggle) who joined during the course of last year.”

The appoints of the former Vice President Customer Success at Nielsen and the former UK Marketing Director at Lucozade Ribena Suntory appear encouraging.

Nielsen is one of SYS1’s major rivals and its services are apparently entrenched within many marketing departments — something SYS1 has to combat.

SYS1’s appointment of a chief marketing officer is overdue. I am sure Mr Evans was already known to SYS1’s chief exec prior to the appointment as his name has come up in casual conversation at AGMs.

Fascinating interview with Mr Evans here:

“Rather than spending hundreds of thousands of pounds on a new ad, we decided as a team to repeat the same campaign for the second year because our market share went up, we know it works. But we could spend more money on media because we weren’t spending it on agency fees and production,” Evans explains.

“For me that’s a no-brainer but you’d be amazed at how hard it is to get people to do that because everybody wants to make their own thing, they want to learn, to prove themselves. Some people would rather make a worse ad but say they’ve made an ad and it be new than repeat something someone else has done very effectively.”

Maynard

System1 (SYS1)

Trading Update and Planned Share Buyback

Oh dear — a profit warning. Bad news for me as I had bought more SYS1 shares before this statement. More on that purchase in a minute. I have interspersed the text with my comments.

—————————————————————————————————————————–

System1 Group PLC (AIM: SYS1) (the international online market research agency), announces today the following trading update for its financial year to the end of March 2020.

After H1 single-digit growth, followed by modest further progress in Q3, trading in Q4 to date has been disappointing, due in the main to the ongoing transition of sales talent, and subsequent disruption and decline in adhoc revenue from smaller clients. Given the limited visibility in some areas, it is difficult to predict the full year outturn, but the Board believes Gross Profit will be slightly down compared to the prior year.

The Company continues to invest heavily in its AdRatings database, sales talent, digitisation and automation, in support of its increasing emphasis on Advertising Effectiveness. Underlying Overhead Costs (excluding Share Based Payments and AdRatings) are expected to increase 4-6% over the 2019/20 financial year.

The lower than expected Gross Profit and increased costs are expected to result in a normalised 2019/20 Profit Before Tax (i.e. excluding Share Based Payments and AdRatings) materially below the current market expectation.

—————————————————————————————————————————–

The phrase “ongoing transition of sales talent” suggests key employees have been leaving, and continue to leave. Fellow blogger Paul Scott made a good point about Glassdoor reviews.

The latest review says: “ I should have listened to the reviews prior to joining and ruining my career. The company is being run into the ground by a consultant and has perpetual global turnover.” That sounds ominous.

I wonder if the ‘consultant’ is Stefan Barden (point 4), a ‘board adviser’ who is leading SYS1’s tech strategy and ‘digitising’ the business. His way of working may not quite fit in with marketing ‘creative’ types.

I suspect the investment in AdRatings (see below) and the shift to becoming an advert ‘data’ business has meant management’s focus has changed and employees within the ‘legacy’ brand-tracking and innovation-testing departments have perhaps felt neglected.

Anyway, the RNS said gross profit would be “slightly down” on 2019 while underlying overhead costs would increase between 4% and 6%.

Assuming gross profit is unchanged and underlying overheads increase 5%, then 2020 operating profit (excluding AdRatings) might be £22.05m less (£18.35m*1.05) = £2.78m. The first half reported a c£2.5m operating profit, so profitability during the second half has collapsed to just c£0.3m.

Costs up with stagnant (at best) sales is not great. Rising costs will in part be due to appointing new senior employees.

—————————————————————————————————————————–

At the same time AdRatings, now rebranded “Test Your Ad”, is starting to show its commercial promise. As part of ITV Media’s objective to ‘Get people to fall back in love with advertising’, they have chosen System1 as their partner in rating the ‘Nation’s favourite Ads’ and helping advertisers to create more of them – starting with a UEFA Euro 2020 Competition to select the best sporting Ad, with the winner awarded a free advertising slot in the half-time break of the final match.

—————————————————————————————————————————–

So my hunch in the blog post above — “SYS1 may even be the mystery “independent research company” that performs the judging” — proved correct.

Anyone on SYS1’s mailing list could have known about the ITV partnership in advance of this RNS. The formal announcement was made on 29th January and the (free) tickets to the event had already heralded the deal:

I attended the event, hosted in a cinema in central London.

Perhaps the most disappointing — but not surprising — part of the event was the audience’s response to being asked who had read Peter Field’s “Crisis in Creative Effectiveness”. Very few hands were raised, which probably explains why SYS1 has struggled to sell its services of late — marketers just don’t want to know about their adverts becoming less effective.

During the presentation, SYS1 gave lots of tips to creating an advert winner. Here are the best ads of 2019, at least according to SYS1.

Kate Waters, ITV’s director of client strategy and planning, revealed the SYS1 deal had been prompted by surveys showing the public’s increasingly unfavourable attitude towards adverts.

Since the early 90s, the number of people that look favourably towards television adverts has halved, while those who look unfavourably has doubled.

Ms Waters admitted ITV had in the past been like the motel owner below, and effectively turned a blind eye to what its customers were up to:

Now ITV wants to “get people to fall back in love with advertising” — presumably so advertisers can make more effective adverts, sell more stuff, and then have more money to spend on more adverts (on ITV).

ITV spoke to about 20 industry experts, including Orlando Wood, the chief innovation officer at SYS1.

From what I could tell from the presentation and post-presentation chit-chat, SYS1 was the only firm able to offer what ITV was looking for. Could that mean SYS1 really does have unique data that might possess a ‘moat’? Partnership talks with SYS1 began about three to fours months ago.

I think ITV actually expected the data and effectiveness testing would have to be created in-house.

All told, the ITV deal appears to validate the value of SYS1’s data and the AdRatings project. Perhaps other commercial broadcasters may one day feel SYS1’s data is useful. ITV has further details of the advert competition here.

—————————————————————————————————————————–

The Company has £4.2m cash, and no debt, and in line with the Company’s approach to capital allocation, the Board intends to conduct a share buyback program of up to £1.5m of the Company’s shares, following its normal post year-end Trading Update in April, subject to the Company’s share price and cash balance at the time. This would be by way of market purchases. The Company will provide a further update nearer the time. Any share buybacks will be made under the existing authority the Company has in place to make market purchases, and also in accordance with the Market Abuse Regulation (EU) No. 596/2014 and Commission Delegated Regulation (EU) No. 2016/1052 where practicable.

—————————————————————————————————————————–

I am not quite sure why SYS1 wants to wait until after April’s statement before undertaking a buyback. Perhaps the company wants to know exactly how bad Q4 has been before buying — well, that is how I feel at the moment. Obscure stock-market regulations may be preventing the buyback of course.

Cash was £4.1m at the half year, so has increased by £0.1m during Q3.

Assuming AdRatings costs a further £1.2m during H2, then the H2 operating cash loss could be £0.9m (including capitalised AdRatings costs).

I’m not so sure instigating a buyback and sustaining the dividend (£0.9m/year) is wise when the overall business is losing money. As SYS1 has hinted, I think the dividend will have to go to leave room for error with any buyback.

I increased my shareholding by 75% by buying SYS1 shares both before and after the 29th January event. The average price I paid was 251p including all costs, and those purchases will teach me about trying to be too clever with industry announcements.

Using my sums in the blog post above, I reckon a 251p share price had valued the business (excluding AdRatings) at 10x my earnings guess adjusted for the £4m cash position. I had felt the ITV deal would give AdRatings a net present value of at least zero.

I still think ITV’s involvement is positive for SYS1 and AdRatings, and the NPV of the latter is now much more likely to be greater than zero post-ITV.

However, SYS1 appears to be going ‘all in’ with its Advertising Effectiveness and AdRatings departments, which perhaps has led to the other departments losing employees and momentum.

SYS1 will become a higher quality business if it succeeds in transforming into a full ‘data’ operation with ongoing subscription revenues etc, but the path will not be straightforward and the group’s financial performance will be unpredictable in the meantime.

Maynard

PS Thanks to Emma for recommending my blog :-)

System1 (SYS1)

CFO resignation and Trading update

Two statements — neither of which delivered great news.

First, the resignation of the CFO announced 03 April. Here is the text:

——————————————————————————————————

System1 Group PLC (AIM: SYS1) (the international online market research agency), announces today that, after 17 years as Chief Financial Officer, James Geddes is stepping down with effect from April 20th 2020.

The Company has appointed Chris Willford as James’ successor and James will be working with Chris to ensure an orderly handover of responsibilities. It is expected that Chris will join the board of the Company, subject to the satisfactory completion of usual due diligence checks, and a further announcement will be made in due course.

John Kearon, CEO, commented:

“On behalf of the Board, Staff, Investors and Suppliers, past and present, I would like to thank James for 17 years of remarkable service to the Company. James and I have worked shoulder-to-shoulder to build the Company over many years and, on behalf of everyone involved, I am extremely grateful for James’ many years of hard work and enormous contribution.

Change is never easy but someone of the calibre and experience of Chris is a worthy and able successor to help the Company achieve its ambitions. Chris is eminently well qualified for the job, having spent his career with blue chip consumer businesses including Unilever, British Airways (Group Treasurer), Barclays (FD of Corporate Bank and UK Retail Bank) and Bradford & Bingley (Group FD). In the past decade, Chris has worked as a consultant with a portfolio of scale up businesses facing similar challenges to those of System1. I’d like to take the opportunity to welcome Chris to the Company.”

——————————————————————————————————

I had always viewed Mr Geddes as a safe paid of hands and a counterbalance to the somewhat enthusiastic chief exec. Mr Geddes had been SYS1’s CFO since 2003, so his departure was probably not an overnight decision. That makes me worry he has foreseen major trouble ahead.

Not sure what to make of Chris Willford. Any CV that includes Bradford & Bingley requires an online search and sure enough Mr Willford was B&B’s finance director during 2008… and was fined by the FCA and the FRC for not informing the board quickly enough about the bank’s problems. These Guardian articles (here and here) have more.

On the one hand Mr Willford will know all about financial management in a crisis, and has experience at much larger firms so SYS1’s accounts ought to be very manageable. On the other hand he has a blotted copybook.

Given the state of SYS1’s recent trading (see below), the primary abilities of CFO — be it Mr Geddes, Mr Willford or somebody else — is now simply to save costs and hoard cash.

On to the trading update. These first paragraphs cover the FY performance:

——————————————————————————————————

In our Trading Update released on February 6, 2020, we reported that trading in Q4 to date had slowed. This remained the case through the final weeks of Q4. We therefore expect Sales Revenue and Gross Profit for Q4 to be approximately 25 % below that of the prior year and for the financial year as a whole to be down by approximately 2%, much as we anticipated in February.

The modestly reduced sales for the full year, together with a 1% increase in overhead expenditure, is expected to result in a 2019/20 Profit Before Tax figure (excluding AdRatings and share-based payments) of approximately £2.9m, compared with £3.6m in the prior year. Whilst we acknowledge this was a disappointing result, it does exceed our previous expectations.

Investment in AdRatings continued during the year, with expenditure of £1.8m recognised in the income statement, compared with £2.2m in 2018/19. In addition, an impairment charge of £0.9m has been taken in relation to AdRatings development costs in light of the continuing modest AdRatings revenues in the year (£0.05m). On the strength of the industry attention received by AdRatings, we have announced a strategic commercial partnership with ITV, the UK’s largest seller of advertising space, to support its customers in creating ever more innovative and effective advertising. We expect to enjoy revenues from these arrangements although it is hard to quantify this while the Covid-19 pandemic continues.

——————————————————————————————————

The 06 February statement said:

* 2020 gross profit would be “slightly down” on 2019. Now confirmed as down 2%.

* 2020 overheads (before share payments and AdRatings) would be up 4-6% on 2019. Now confirmed as up 1%.

My sums now indicate H2 2020 gross profit could be £10.0m (down 11%) and H2 operating profit could be £0.7m (down 63%). The H2 profit is a little better than the £0.3m I had calculated following the February update. The improvement is due to further cost cutting. SYS1’s prediction of a £2.9m pre-tax result before share-based payments looks about right to me.

AdRatings — oh dear.

£50k revenue for 2020 = £29k during H2 = still no interest from customers.

£1.8m expenses for 2020 = £0.9m during H2 and in line with the expenditure guidance from the H1 results.

No word on how much AdRatings expenditure was capitalised. £232k was capitalised during H1. Possibly nothing was capitalised, because SYS1 recorded a £0.9m AdRatings impairment charge.

Capitalised AdRatings costs up to H1 2020 were £885k, so it appears the whole project has been written to zero. At least the new finance director has grasped that nettle quickly.

So, if AdRatings costs continue at £1.8m a year and my H2 2020 profit guess is doubled to c£1.4m, SYS1 loses money. Not great. And that is before considering the effect of Covid-19.

At least ITV remains on the scene. ITV and SYS1 hosted a joint webinar on 08 April (I have yet to watch it). SYS1’s vague talk of “expect to enjoy revenues” implies the broadcaster is not sending cheques just yet.

On to Covid-19:

——————————————————————————————————

In response to the Covid-19 pandemic, governments across the world have taken unprecedented actions in recent weeks to limit the spread of the virus. These actions vary considerably by country, and their impact varies considerably by business sector. Since the end of the 2019/20 financial year, System1’s trading has inevitably been adversely affected by the global economic situation. The Board has concluded that it is difficult at this stage to provide guidance on the financial performance for the current year until a clearer outlook emerges. The Board will keep investors updated as the impact on the Group’s performance becomes clearer.

System1’s priority, as we face up to the challenge presented by the pandemic, is to maintain a strong financial position while safeguarding the human and intellectual capital needed to take advantage of the what the Board believes will be substantial growth opportunities when the global economy recovers. In accordance with this priority, we are monitoring the trends in forward sales, evaluating a variety of plausible revenue scenarios, and taking decisions on our cost base when agreed trigger points are reached. Mitigating actions to date include deferring employment costs, reducing the number of hours paid for where the volume of work has fallen, and taking advantage of government-backed business support and furloughing schemes in the countries where we operate. The Board and other senior executives of System1 have agreed to defer 20% of their salaries until further notice.

Given the emphasis on retaining cash in the current circumstances, the Board has decided to suspend both the proposed buyback programme of up to £1.5m of System1 shares as well as the payment of a final dividend for the 2019/20 financial year. Future returns of capital will be kept under review as the economic situation develops. In addition, the Company arranged and drew down a £2.5m revolving credit facility in March 2020, ending the year with a gross cash balance of £6.6m (2019: £4.3m) and debt of £2.5m.

At this difficult time we are working as closely as possible with our clients, sharing the latest insights on how Covid-19 has impacted consumer feelings and behaviour around the world and strengthening our relationships with them. We believe this will stand us in good stead and benefit our business when conditions improve.

——————————————————————————————————

Not great. Furloughed staff tells you times are tough. Net cash was £4.1m at H1 (September) and £4.3m at H2 (March), so cash generation of just £0.3m during H2 if you account for the c£0.1m interim dividend. No surprise that the mooted buyback and further payouts have been scrapped.

SYS1 is soldiering on with its Coronavirus tracker and webinars. But are advertisers taking any notice? The tone of the RNS suggests not.

The next results will be fascinating — what will happen to AdRatings? I wrote in February that SYS1 appeared to have gone ‘all in’ with its Advertising Effectiveness and AdRatings departments. I am not sure whether there is now any way back.

AdRatings (https://testyourad.com/) currently has data on 40,397 ads. SYS1’s market cap at 100p/share is £12.6m. Therefore data for each tested advert can be yours to keep for £312. The cost of generating the ad data — involving an online panel of 150 people — must surely be more than £312 even before you consider the IT and staff costs.

Wishful thinking perhaps, but I do wonder whether SYS1 would better suited becoming part of ITV.

Maynard

System1 (SYS1)

Director appointments (Chris Willford and Stefan Barden) published 26 June 2020

Two new director appointments.

1) Chris Willford:

Mr Willford was appointed CFO-elect during early April and is now confirmed as a board member.

The statement reveals Mr Willford’s past:

On 11 December 2013, the Financial Conduct Authority (“FCA”) published a final notice in relation to an investigation into Chris Willford whilst he was finance director at Bradford & Bingley plc (“BBG”) in 2008. Mr Willford was fined £30,000 by the FCA for breaching Principle 6 of the FCA’s Statements of Principle for Approved Persons as a result of Mr Willford’s conduct in his performance of the CF1 Director function as Group Finance Director at BBG during the period between 16 May 2008 and 19 May 2008.

https://www.fca.org.uk/publication/final-notices/christopher-willford.pdf

On 10 July 2014, the Financial Reporting Council (“FRC”) published the outcome of its disciplinary case against Mr Willford in respect of adverse findings made in the FCA Final Notice published on 11 December 2013. The FRC found that the adverse findings were conclusive evidence of misconduct and Mr Willford was reprimanded and fined £13,000.

https://www.frc.org.uk/news/july-2014/outcome-of-disciplinary-case-against-christopher-w

Not the most encouraging appointment. But as I mentioned at the time Mr Willford was recruited, the primary abilities of SYS1’s CFO now are simply to reduce costs and hoard cash.

2) Stefan Barden:

Mr Barden’s appointment is more interesting:

“System1 Group plc (AIM: SYS1) today announces that it has appointed Stefan Barden to the board of directors of the Company as an executive director with immediate effect. From November 2018, Stefan has been an adviser to the board of directors on strategy and technology, and has recently taken on the executive role of chief operating officer to assist the Company through its next phase of development. He will return to the advisory role when this is complete, expected to be in around a year.

Stefan has over 20 years of General Manager, Managing Director and CEO experience after graduating from McKinsey Management Consultancy and Unilever’s fast track management development programme. These include CEO of Northern Foods, CEO Heinz UK and Ireland, as well more latterly CEO of the internet business Wiggle which he took from £140m to £360m in sales in 3 years. Semi-retired, he also supports several CEOs, often founders, in developing high growth businesses. System1 is one of these companies.”

I presume Mr Barden’s COO role will be full time. Note that the appointment is expected to last just one year — the duration of the company’s “next phase of development“. I think that timescale implies the company will undergo some intermediate restructuring.

Mr Barden owns 5.7% of SYS1, shares he bought at c200p — so £1.4m of his own money spent. His options come good only if the shares hit at least 500p. So unlike many executives, at least Mr Barden has some financial alignment to us ordinary investors.

I wrote the following after attending SYS1’s AGM last year:

“The appointment of Stefan Barden (SB) has helped. SB works only two days a week but JK (SYS1 boss John Kearon) said SB is a “machine” (SB is an accomplished triathlete) and is “brilliant”. SB works on the company’s “process, structure and rhythm” — making sure everything works like clockwork. I had no time to ask about SB’s LTIP.”

Mr Barden does not sound like the typical marketing-type person to me, which is perhaps what SYS1 needs in an COO to get things done.

I wrote the following after SYS1’s profit warning in February:

“The phrase “ongoing transition of sales talent” suggests key employees have been leaving, and continue to leave. Fellow blogger Paul Scott made a good point about Glassdoor reviews.

The latest review says: “ I should have listened to the reviews prior to joining and ruining my career. The company is being run into the ground by a consultant and has perpetual global turnover.” That sounds ominous.

I wonder if the ‘consultant’ is Stefan Barden (point 4), a ‘board adviser’ who is leading SYS1’s tech strategy and ‘digitising’ the business. His way of working may not quite fit in with marketing ‘creative’ types.”

Seems like SYS1 boss John Kearon is going ‘all in’ with developing AdRatings (the loss-making start-up subsidiary) and Stefan Barden. I always welcome management attempting radical action, although so far there has been no evidence that SYS1’s clients actually want the AdRatings service.

Maynard