04 December 2020

By Maynard Paton

Results summary for Mountview Estates (MTVW):

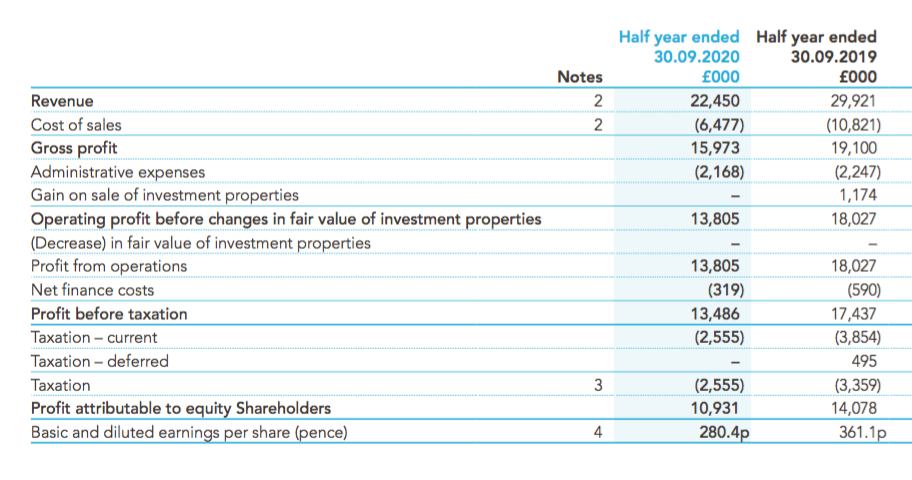

- A pandemic-affected H1 that showed revenue down 23% and profit down 18% following procedural delays to property sales.

- A maintained dividend, a lack for furloughed staff and rents up 1% did not signal inherent lockdown trouble.

- Significant gross-margin enhancements may reflect an underlying step-change in performance and have favourable implications for valuation.

- Expenditure on property purchases has picked up, with management hopeful of acquiring “exceptional opportunities”. Debt levels remain modest.

- Book value inched to a record £98 per share, although new profit assumptions now point to a balance sheet possibly worth up to £225 per share. I continue to hold.

Contents

- Event link, share data and disclosure

- Why I own MTVW

- Results summary

- Coping with Covid-19

- Revenue, profit, dividend and net asset value

- Gross margins

- Allsop valuation

- Financials

- Corporate governance and protest votes

- Valuation

Event link, share data and disclosure

Event: Interim results for the six months to 30 September 2020 published 26 November 2020

Price: £110

Shares in issue: 3,899,014

Market capitalisation: £429m

Disclosure: Maynard owns shares in Mountview Estates. This blog post contains SharePad affiliate links.

Why I own MTVW

- Buys, holds and sells regulated-tenancy properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to control an aggregate 50%/£215m shareholding.

- Simple accounts carry properties at cost, which if sold at their current ‘reversionary’ values may be worth significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

Coping with Covid-19

- Annual results published during June did not suggest MTVW would face major lockdown problems.

- MTVW said at the time:

“We have not had to furlough any staff or reduce staff numbers in any other way and I remain confident that our years of financial prudence will enable us to continue to conduct the business successfully and to maintain our dividend payments.”

- These H1 results reiterated the lack of furloughing and declared a maintained dividend.

- June’s statement also claimed the company was “active in auctions” during the half:

“This keen eye on purchasing has continued into the new financial year, despite Covid-19, and we have been active in auctions, both buying and selling properties at prices that we would have been pleased with at any time in recent years.”

- But this H1 revealed MTVW was not as active in auctions as would have normally been the case:

“The first lockdown started shortly before the beginning of our financial year and had the effect of delaying the procedures that are necessary to bring a vacant property to market. This delay was about a month or six weeks and is commensurate with our fall in turnover.”

- A six-week delay during a 26-week period implies turnover should have fallen 23%.

- Total revenue actually fell 25%, but income from property sales reduced by 37%.

- On rents, MTVW said in June:

“Over 80% of our rents are paid directly into the bank and regulated rents are set at a modest level. Provided tenants pay their rent they have absolute security of tenure and a significant number have help from social services.”

- Sure enough, income from rents climbed 1% during this H1 — progress that matched the five-year compound average.

Revenue, profit, dividend and net asset value

- MTVW’s revenue is dependent largely on sales of regulated-tenancy properties.

- Such properties typically become available for sale only when the tenant dies.

- As such, the total proceeds MTVW collects from one set of results to the next can be unpredictable.

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 | |||

| Property sales revenue (£k) | 20,656 | 25,774 | 20,199 | 25,452 | 12,606 | ||

| Properties sold | 73 | 81 | 75 | 92 | 50 | ||

| Average selling price (£k) | 283 | 318 | 269 | 277 | 252 |

- The pandemic presumably led to 20 or so properties not making it to auction.

- Whether the pandemic influenced the lower average sale price is hard to say.

- Although total revenue fell 25%, operating profit before investment gains dropped ‘only’ 18%.

- Profit not falling as much as revenue was a significant development, with MTVW reducing costs and lifting margins during the lockdown.

- Administrative expenses were trimmed 3% during the half.

- But a huge 40% reduction to cost of sales reflected a potential step-change in performance (see Gross margins and Allsop valuation below).

- A 200p per share interim dividend was declared for the sixth successive year.

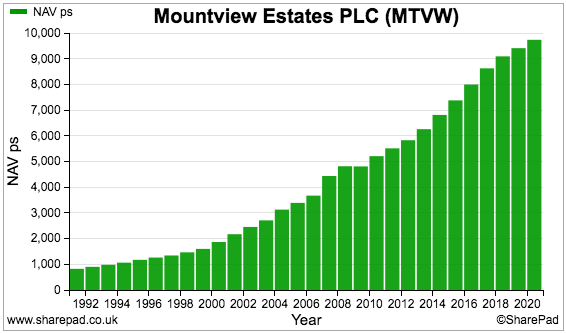

- MTVW’s property activities mean net asset value (NAV) is an important performance measure.

- NAV inched £3m higher to £383m — equivalent to £98.15 per share and a fresh NAV record.

- NAV was £302m five years ago and has since grown at approximately 5% per annum:

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Gross margins

- These H1 figures revealed dramatic enhancements to the margins enjoyed from property sales and collected rent.

- The 379-word management narrative did not mention the margin improvement, which meant shareholders could only speculate on what had occurred.

- The gross margin generated through property sales is calculated using the original cost of the properties.

- The longer MTVW has owned a property, the higher the property-sale gross margin should be.

- The overall property-sale gross margin within any set of results will naturally vary depending on the mix of properties sold.

- The gross margin achieved from property sales suddenly improved to 65.1% during this H1:

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 | |||

| Property sales revenue (£k) | 20,656 | 25,774 | 20,199 | 25,452 | 12,606 | ||

| Property sales gross profit (£k) | 11,706 | 15,751 | 12,271 | 15,694 | 8,203 | ||

| Property sales gross margin (%) | 56.7 | 61.1 | 60.8 | 61.7 | 65.1 |

- A 65.1% gross margin is equivalent to buying a property for £100k and selling it for £287k.

- MTVW selling properties at 65% gross margins is not unheard of but not common either.

- MTVW has recorded property-sale gross margins of 65% or more during eight of the last 20 years — most recently during FYs 2015, 2016 and 2017.

- This H1’s elevated gross margin may simply be due to an unusual collection of properties becoming available for sale.

- Or perhaps the lockdown was the cause…

- …because MTVW’s rental income has suddenly become more profitable, too.

- The gross margin achieved from rental income suddenly improved to 78.9%:

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 |

|||

| Rental revenue (£k) | 9,510 | 9,488 | 9,722 | 9,500 | 9,844 | ||

| Rental gross profit (£k) | 6,868 | 6,476 | 6,829 | 6,560 | 7,770 | ||

| Rental gross margin (%) | 72.2 | 68.3 | 70.2 | 69.1 | 78.9 |

- The gross margin from rental income has bobbed around the 70% level for years and has never topped 73% since at least 2000.

- And yet this H1 witnessed the rental gross margin jump to 79%.

- I can only presume less property maintenance was performed during the half due to the pandemic, which lowered MTVW’s expenses.

- Wishful thinking perhaps, but maybe some of that rental-margin improvement can be maintained as staff and tenants adapt to new ways of working.

- All told, something unusual has supported both property-sale and rental-income profits during this H1 — possibly pandemic-related, possibly something else.

- But whether the gross-margin improvements are one-offs, or have become permanent — or end up somewhere in between — is sadly impossible to say at present.

Allsop valuation

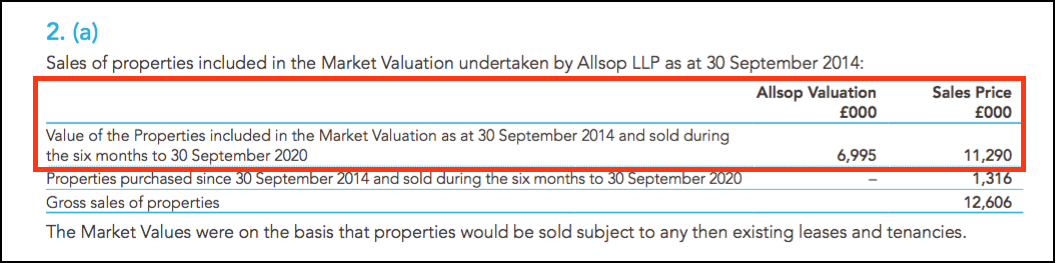

- Adding to the gross-margin puzzle is the sudden improvement to the proceeds from sold properties compared to their Allsop valuations.

- To recap, MTVW commissioned property agent Allsop during September 2014 to assess the group’s estate.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties carried at the time.

- The Allsop calculation was based on MTVW’s properties remaining in their regulated-tenancy state and therefore excluded any ‘reversion’ premium (i.e. the value uplift that occurs when a regulated tenancy finishes and the rent reverts to a proper market level).

- The Allsop valuation was not formally applied to the accounts. MTVW’s properties remain on the balance sheet at their original cost.

- Following the Allsop valuation, MTVW reveals the proceeds from sold properties versus their stated Allsop value:

- Sale proceeds during the last five years have averaged 1.45x the associated Allsop valuation.

- However, these H1 results showed the ‘sold-premium-to-Allsop’ multiple at 1.61x:

| FY 2016 | FY 2017 | FY 2018 | FY 2019 | FY 2020 | H1 2021 | ||

| Property sales revenue (£k) | 61,442 | 57,174 | 45,156 | 41,273 | 41,819 | 11,290 | |

| Allsop valuation (£k) | 42,600 | 38,505 | 30,594 | 28,727 | 29,221 | 6,995 | |

| Sold-premium-to-Allsop (x) | 1.44 | 1.48 | 1.48 | 1.44 | 1.43 | 1.61 |

- The ‘sold-premium-to-Allsop’ multiple jumping higher during this H1 is another mystery not explained by the management narrative.

- The higher multiple may of course be due to the random mix of properties involved.

- Or the higher multiple may have been supported by significantly greater sale prices being achieved in a rebounding housing market.

- Similar to the gross-margin improvements, arriving at a firm conclusion as to what has actually occurred is difficult given the pandemic disruption.

- That said, a 1.61x ‘sold-premium-to-Allsop’ multiple is unusual and has notable implications for assessing MTVW’s valuation (see Valuation below).

- Let’s not forget the Allsop valuation is now six years old and has probably become rather stale.

- MTVW has sold properties with a book value of £113m during the six years following the Allsop review.

- Assuming the same rate of sales, MTVW could take a further 11 years to sell the remaining properties that were valued by Allsop.

- My sums suggest MTVW’s property stock is presently split approximately 50:50 between property valued by Allsop and properties acquired since the Allsop valuation.

- As more Allsop-valued properties are sold and other properties are purchased, the less relevant the Allsop valuation becomes.

- MTVW is not keen to undertake another formal valuation. This year’s AGM Q&A update said:

“The cost of carrying out a valuation is such that your Board are reluctant to inflict such an expense on the shareholders when the information so acquired is not a useful management tool. The uncertainties created by Brexit and Covid are such that any current valuation is unlikely to have any long term reliability. Nevertheless your Board always review any representations made by shareholders in respect of a potential valuation.”

- I still maintain MTVW ought to implement regular valuations to provide greater insight into the inherent value of the group’s property estate.

- Regular valuations would also outline the prudence (or not) of MTVW’s more recent purchases.

- All shareholders have to go on at present is the six-year-old Allsop valuation that excludes ‘reversionary’ uplifts.

- MTVW continues to buy and sell properties, which implies their fair value can still be judged by management despite the “uncertainties created by Brexit and Covid”.

- And if MTVW’s management can still judge the fair value of a property, Allsop can as well — and conduct another valuation!

Financials

- MTVW’s accounts remain very straightforward.

- Some £20m was spent during the six months acquiring 77 additional properties at an average cost of £266k.

- MTVW described the purchases as “substantial”.

- For perspective, MTVW has on average spent £30m acquiring 98 properties a year since FY 2016:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Number of properties purchased | 90 | 118 | 119 | 105 | 57 |

| Cost of properties purchased (£k) | 28,330 | 29,800 | 47,130 | 30,731 | 15,420 |

| Average cost (£k) | 315 | 253 | 396 | 293 | 271 |

- This H1 statement did not contain any further write-downs to MTVW’s portfolio of standard investment properties.

- This portfolio suffered a £1m write-down within the FY 2020 results due to the pandemic, and remains in the books at £24m.

- MTVW took on additional loans of £13m to help fund the aforementioned purchases, which lifted net debt to £47m — equivalent to 12% of the group’s £409m property stock.

- The 12% level is not out of line with recent history:

| Year to 31 March | 2016 | 2017 | 2018 | 2019 | 2020 |

| Trading properties (£k) | 334,108 | 347,380 | 376,879 | 392,384 | 392,069 |

| Net debt (£k) | (41,619) | (31,217) | (44,995) | (46,519) | (29,607) |

| Net debt/Trading properties (%) | 12.5 | 9.0 | 11.9 | 11.9 | 7.6 |

- MTVW said its balance sheet reflected “years of financial prudence”, which would give the group the “ability to take advantage of exceptional opportunities that may arise”.

- The 2020 annual report (point 12) showed banking facilities of up to £90m — equivalent to 22% of the property estate.

- MTVW’s gearing has been higher. During 2012 and 2013 for example, net debt represented 30% of the property stock.

- Net finance costs of just £319k for this H1 imply a welcome sub-2% interest rate on the period’s £38m average net debt.

- MTVW’s accounts are free of pension obligations.

Corporate governance and protest votes

- Not every shareholder is happy with the way MTVW is managed.

- The last four AGMs have witnessed c30% protest votes against re-electing independent non-execs, approving the board’s pay and re-appointing the auditors.

- MTVW shareholders can be divided into three camps:

- The Sinclair family concert party, which is led by chief executive Duncan Sinclair and represents just over 50% of the share count;

- The Murphy family and connected parties, who claim to own 24% of the share count and whose largest shareholder is the chief executive’s sister, and;

- Everybody else, who are left with 25% of the share count.

- The protest votes come from the second camp.

- This time last year I recapped the grievances of the Murphy family and how the dissident shareholders have prevented the re-election of certain non-execs at the 2017, 2018 and 2019 AGMs.

- The dissidents prevented the re-election of certain non-execs at the 2020 AGM as well.

- When announcing this year’s AGM voting result, MTVW said:

“The Directors will engage with shareholders to obtain feedback on their concerns and will publish an update on that engagement within six months of the date of the Annual General Meeting.“

- A statement should therefore be published on or before 12 February 2021.

- I am not hopeful of any material feedback.

- Talks with the Murphy family appear to have collapsed completely. MTVW said during June:

“[T]he Company had identified, as far as possible, those shareholders who did not support the resolutions and attempted to engage with them to seek their views. The offer was declined and they indicated they did not wish to engage further.“

- How the Murphys intend to change the way MTVW is managed therefore remains unclear.

- Support for the Murphys may be increasing, albeit slowly. Approximately 30k extra votes were cast against the contentious resolutions at this year’s AGM and subsequent general meeting:

| 2017 | 2018 | 2019 | 2020 | |

| AGM | ||||

| Votes FOR | 126k (13%) | 223k (19%) | 180k (16%) | 236k (20%) |

| Votes AGAINST | 827k (87%) | 927k (81%) | 938k (84%) | 971k (80%) |

| Subsequent GM | ||||

| Votes FOR | 2,361k (74%) | 1,504k (62%) | 2,095k (69%) | 2,048k (68%) |

| Votes AGAINST | 826k (26%) | 941k (38%) | 939k (31%) | 971k (32%) |

- The 2020 annual report invited shareholders to submit questions in advance of the AGM (point 18), but I understand not every question received a public response.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- MTVW’s shares could be worth more than £200 — assuming all of the group’s regulated tenancies end immediately and the properties then fetch a fair market value.

- Just how much in excess of £200 depends on your view of the aforementioned ‘sold-premium-to-Allsop’ multiple.

- Assuming:

- The 1.61x ‘sold-premium-to-Allsop’ multiple recorded during this H1 is a freak result, and;

- The preceding 1.43x multiple is more representative…

- … I arrive at a possible £201 per share valuation.

- The following table outlines the sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less property stock sold since Sept 2014 (£k) | (113,259) |

| 204,392 | |

| Allsop-premium-to-book | 2.10x |

| Sold-premium-to-Allsop | 1.43x |

| 612,684 | |

| Stock purchased since Sept 2014 | 204,904 |

| Sold-premium-to-Allsop | 1.43x |

| 293,011 | |

| Possible property stock value (£k) | 905,696 |

- I have taken the original September 2014 portfolio value of £318m and subtracted the £113m book value of properties sold since that date.

- I have then multiplied the £219m remainder by the 2.1x ‘Allsop-premium-to-book’ multiple and then by the 1.43x ‘sold-premium-to-Allsop’ multiple.

- I arrived at a £613m estimate for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has acquired additional properties with a net £205m book value.

- I have assumed all of these can be sold one day for £293m based on my 1.43x ‘sold-premium-to-Allsop’ multiple.

- Adding the £613m and the £293m together gives £906m.

- This next table adjusts that £906m for 19% taxation, other investments, net debt and other liabilities to give a possible book value of £785m or £201 per share: (EDIT 14 July 2021: Sorry, but the table below has been inadvertently updated with incorrect figures).

| Possible property stock value (£k) | 941,672 |

| Less tax at 19% (£k) | (103,266) |

| Plus other investments (£k) | 25,574 |

| Less net debt (£k) | (21,283) |

| Less other liabilities (£k) | (7,586) |

| Possible NAV (£k) | 835,111 |

| Possible NAV per share (£) | 214.19 |

- These sums are not perfect, and the major question remains how long MTVW will take to sell all of its properties.

- Apply this H1’s 1.61x ‘sold-premium-to-Allsop’ multiple to the calculations instead, and I arrive at a £1,020m potential value for the current estate.

- Adjust for taxation, other investments, net debt and other liabilities then gives a possible book value of £877m or £225 per share:

| Possible property stock value (£k) | 1,019,699 |

| Less tax at 19% (£k) | (115,977) |

| Plus other investments (£k) | 24,122 |

| Less net debt (£k) | (47,103) |

| Less other liabilities (£k) | (3,607) |

| Possible NAV (£k) | 877,134 |

| Possible NAV per share (£) | 224.96 |

- Either way, the possible market value of MTVW’s balance sheet is significantly in excess of the present £429m market cap.

- The actual £383m balance-sheet value is meanwhile not far below the present £429m market cap.

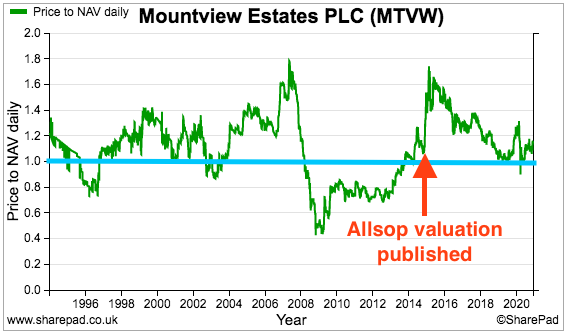

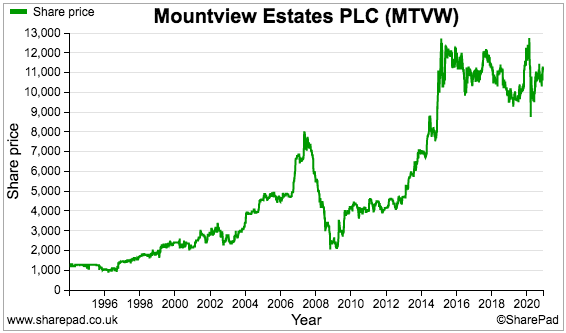

- Following the Allsop valuation, MTVW’s shares have generally traded ahead of NAV (blue line below):

- The premium to NAV with the shares at £110 is 12%, which does not seem excessive post-Allsop.

- Remember, NAV is calculated with properties of £409m — or £105 per share — accounted for at cost.

- The trailing 400p per share annual dividend supplies a 3.6% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Another very interesting and helpful analysis. There is much other information that would be nice to know, but that we probably never will. Such is often the case with family-run PLCs. The average property price changes issued by the Land Registry, Halifax and Nationwide are probably the best guides to future performance over the long term. As long as the dividend is maintained and occasionally increased I will retain.

Hi Ian,

Thanks for the comment. Yes, MTVW could disclose a lot more information but sadly chooses not to. Questions at the AGM have not revealed much either. The stats published by Grainger in contrast are very informative. For now we just have to hope MTVW can pick up some bargains in the auctions.

Maynard

Maynard, thanks for another one of your very helpful insights into this button-lipped organisation. There are good reasons to be wary of these shares – only a low volume of trades takes place each day (only a quarter of the shares are not held by the concert parties), and the directors are uber-economical with the information that they make public. Like you, I hold for the income and the potential uptick when the apparent underlying asset values are realised. In the meantime, we’re shooting in the dark and watching the Sinclair Murphy feud with interest – I’m just glad that you are able to shine your torch into some of the dark corners.

Hi Paul, glad you found the article useful. Maybe one day another stock valuation will help illuminate proceedings!

Maynard

Hi Maynard,

Many Thanks once again for your time in producing this extremely interesting report.I believe that Sinclair is quite conservative in his general persona & the figures he reveals .Consequently I believe that there may well be an element of “hidden value” lurking within the co. I hold with much interest to see what the future holds on this stock,

All the best,Giles.

Hi Giles,

Glad you found the article useful. I have attended two MTVW AGMs and Mr Sinclair’s persona could also be interpreted as lacking enthusiasm — at least when it comes to engaging with shareholders! Still, the business chugs along while we all await the day something happens to clarify the scale of that ‘hidden value’!

Maynard

Mountview Estates (MTVW)

Update on 2020 Annual General Meeting outcome published 12 February 2021

Some shareholders have apparently engaged with management for change. The identity of the shareholders, though, is a mystery.

Here is the full text:

———————————————————————————————————–

In accordance with provision 4 of the UK Corporate Governance Code, the Company is providing the following update to the 2020 Annual General Meeting (“AGM”) voting results announced on 12 August 2020 regarding the significant vote against a number of resolutions:

Resolution 5: re-election of Ms M.L. Archibald as a director of the Company

Resolution 6: re-election of Mr A.W. Powell as a director of the Company

Resolution 8: to approve the Directors’ Remuneration Report

Resolution 9: to approve the Directors’ Remuneration Policy

Resolution 10: re-appointment of Messrs BSG Valentine as auditors of the Company

In addition, Resolutions 12 and 13, to re-elect Ms M.L. Archibald and Mr A.W. Powell as directors of the Company, were not approved by a majority of the Company’s independent shareholders. At a subsequent general meeting held on 23 November 2020, as the Company was entitled to convene in accordance with the Financial Conduct Authority’s Listing Rules, both Ms M.L. Archibald and Mr A.W. Powell were re-elected as directors of the Company.

Following the 2020 AGM, and as it has done previously, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage. The Company remains committed to shareholder engagement and we will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.

———————————————————————————————————–

A slight change in the text from the Update on 2019 AGM outcome statement.

Last year the text said:

“Following the 2019 AGM in August and prior to the general meeting held on 18 November 2019, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. They declined to meet or engage. The Company remains committed to shareholder engagement and we will continue to offer to meet with shareholders to take into account their concerns and considerations in the future.”

This year the text said:

“Some shareholders did not wish to engage”

I can only presume dissident shareholders not related to the Murphys this time did speak to management. The Murphys have in the past claimed to control 24% of the shares, and the protest votes amounted to 25% at the AGM. So perhaps the talks involved a 1% shareholder.

This TR1 from November may have had some bearing on the situation.

Craig Murphy reduced his shareholding to below 3% and maybe the buyer fancies his/her chances of engaging with the board.

Elsewhere, fellow regulated-tenancy landlord Grainger has stated: “Our sales performance of ex-regulated tenancy properties has been notably strong, with high volumes ahead of valuations.” That sounds promising.

Maynard

Maynard, the £200 value you estimate accrues over (a long ) time, it cannot be realised until the tenant dies and meanwhile they pay a low rent. So if you discount the value back over the time it will take to realise it to today, how cheap is it really?

Cheers

Steve

Hi Steve,

The £200 per share value is based on “assuming all of the group’s regulated tenancies end immediately and the properties then fetch a fair market value” — so it is based on today’s money. So no discounting is involved.

Over time house prices should rise and so should the ‘sold-premium-to-Allsop’ multiple used to construct that £200, which ought to mean the £200 figure ought to rise as well. But you are right to question the assumption that the share is ‘cheap’ as my sums have pointed to a c£200 for some years now as the ‘sold-premium-to-Allsop’ multiple has stayed around 1.4x. And the share price has not really performed either.

Maynard

Mountview Estates (MTVW)

PI World video: Andy Brough’s 3-minute Stock Slam and other gems published 30 April 2021

A very informative interview with Andy Brough of Schroders.

He mentions he owns MTVW for his own account at 5m05s. Mr Brough attended MTVW’s AGM in (I think) 2010 and he is the only fund manager I have ever seen at an AGM (although he spent most of his time looking at his phone). He asked how old MTVW’s tenants were, and received a ‘don’t know’ reply. Useful to know he still holds.

Maynard

Mountview Estates (MTVW)

Update on General Meeting voting outcome published 24 May 2021

Any company meeting that creates a significant protest vote requires a formal update six months later. MTVW’s AGM, where certain non-execs are voted off the board, and the subsequent general meeting, where those same non-execs are voted back on, gives MTVW two opportunities every year to engage with the dissident investors.

Some of the dissidents still do not wish to engage with MTVW, but some still do. MTVW sadly does not disclose the subject of the discussions that take place.

Here is the full text:

——————————————————————————————————————

In accordance with provision 4 of the UK Corporate Governance Code, the Company is providing the following update to the General Meeting voting results announced on 23 November 2020 regarding the significant vote against both resolutions which were put to shareholders at the General Meeting, namely:

Resolution 1: to re-elect Mr. A. W. Powell as a director of the Company; and

Resolution 2: to re-elect Ms. M.L. Archibald as a director of the Company.

At the General Meeting, both Mr. A.W. Powell and Ms. M.L. Archibald were re-elected as directors of the Company.

Following the meeting, the Company identified, as far as possible, those shareholders who did not support the resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage. The Company remains committed to shareholder engagement and will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.

——————————————————————————————————————

Maynard