31 December 2019

By Maynard Paton

Results summary for Daejan (DJAN):

- The statement revealed fresh first-half records for revenue, up 12%, underlying operating profit, up 7%, and net asset value, up 4%.

- New rent laws in New York led to a £46m devaluation and put DJAN on course to register its first annual valuation loss since 2009.

- A 6% strengthening of the USD counterbalanced the New York devaluation and helped support net asset value.

- The accounts remain conservatively financed, with capital expenditure reduced significantly following earlier cautious remarks from management.

- The share price represents only 46% of net asset value — despite net asset value advancing 75% during the last five years. I continue to hold.

Contents

- Event link and share data

- Why I own DJAN

- Results summary

- Revenue, profit, dividend and net asset value

- New York property devaluation

- Investment properties and borrowings

- Valuation

Event link and share data

Event: Interim results for the six months to 30 September 2019 published 27 November 2019.

Price: £55

Shares in issue: 16,295,357

Market capitalisation: £896m

Why I own DJAN

- Commercial and residential property landlord that boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to control an aggregate 80%/£717m shareholding.

- Net asset value of £120 per share is more than double the recent share price.

Further reading: My DJAN Buy report | All my DJAN posts | DJAN website

Results summary

Revenue, profit, dividend and net asset value

- DJAN’s first-half figures were not quite as bad as the gloomy outlook remarks within the 2019 annual results had suggested.

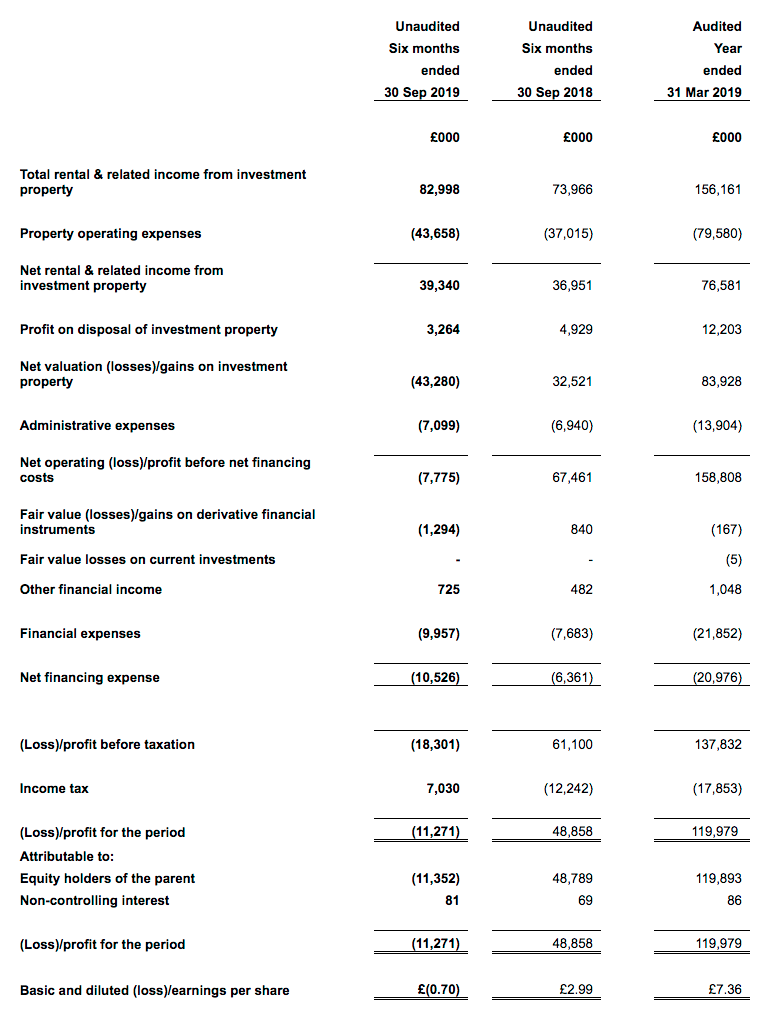

- Revenue gained 12%, operating profit (before disposal gains and valuation losses) advanced 7% while net asset value (NAV) climbed 4%. All three measures set new H1 records.

- DJAN said the revenue improvement was due to “the letting of completed development projects in the UK and property acquisitions in the USA”.

- However, revenue for this first half was only 1% higher than that recorded during the preceding second half:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| UK revenue (£k) | 45,602 | 46,793 | 47,822 | 52,542 | 50,986 | ||

| US revenue (£k) | 25,668 | 24,822 | 26,144 | 29,653 | 32,012 | ||

| Total revenue (£k) | 71,270 | 71,615 | 73,966 | 82,195 | 82,998 | ||

| Operating profit before valuation/disposal gains (£k) | 25,952 | 27,263 | 30,011 | 32,666 | 32,241 | ||

| Valuation gain (£k) | 29,536 | 116,902 | 32,521 | 51,407 | (43,280) | ||

| Disposal gain (£k) | 6,720 | 5,173 | 4,929 | 7,274 | 3,264 | ||

| Net operating profit (£k) | 62,208 | 149,338 | 67,461 | 91,347 | (7,775) |

- UK revenue during this H1 was actually 3% lower than that recorded during the preceding H2.

- UK revenue declining after H2 into the subsequent H1 is not unusual. Such reductions have occurred during the 2011, 2013, 2014 and 2017 financial years.

- DJAN’s revenue includes service-charge income as well as rental payments. Service charges represent additional tenant payments for repairs and maintenance, which can vary from year to year and cause total revenue to fluctuate.

- Operating profit before disposal gains and valuation losses, at £32m, represented 39% of revenue — a tad higher than the 38% average margin witnessed during the previous five years.

- DJAN’s US properties suffered a £46m devaluation (see New York property devaluation).

- The devaluation is likely to mean the current year will witness DJAN’s first property revaluation loss since 2009.

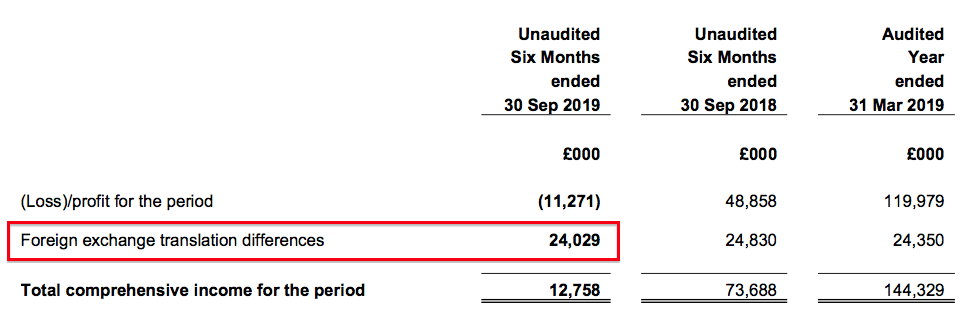

- Only a 6% strengthening of the USD — from 1.304 to 1.230 of GBP — ensured NAV inched to £120 per share from the £119 per share level declared at the full year.

- The 2019 annual report showed DJAN owning net US property assets of £398m, which after translating at the stronger USD rate added £24m to their value and bolstered NAV by a net £13m:

- An interim 35p per share dividend was declared for the seventh consecutive year.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

New York property devaluation

- The 2019 annual statement mentioned: “New rent regulation laws in New York state that came into effect on 1 July 2019 are expected to depress New York residential values in the coming year”.

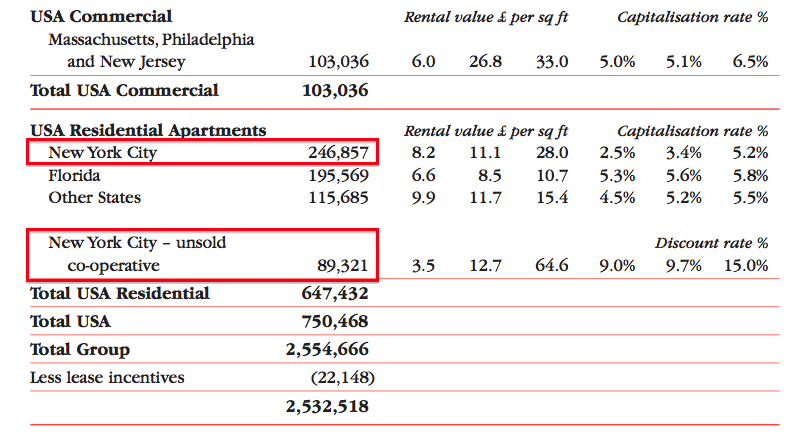

- This H1 RNS revealed DJAN’s American properties had been revalued downwards by £46m.

- The 2019 annual report showed New York properties with a £336m book value and representing 13% of the entire property estate:

- Assuming the value of DJAN’s US properties outside of New York were unchanged, the New York properties lost 14% (£46m/£336m) of their value.

- New York’s new rent regulations have received a mixed welcome and could create unintended consequences (at least according to blogs such as this, this and this).

- US properties continue to carry a c£750m book value and represent approximately 29% of the DJAN’s total estate.

- Including DJAN’s other US assets and the associated borrowings, US net assets represent 20% of the group’s shareholder equity.

Investment properties and borrowings

- UK properties enjoyed a tiny £3m/0.1% valuation uplift during the six months.

- The 2019 annual results had already suggested the benefits of ‘yield compression’ — whereby property valuations are marked higher as investors decide to pay more for rental incomes — may now have stalled.

- Last year DJAN spent an enormous £108m buying new sites and developing old properties.

- The £108m was the largest annual sum spent for at least two decades.

- However, management did say at the time: “[W]e believe that by the pursuit of our well proven strategy of prudence and risk minimisation coupled with the conservation of cash and bank resources we will be well placed to ride out any storms which may lie ahead.”

- The “conservation of cash and bank resources” led to just £10m being spent on new and old sites during this H1.

- Double that £10m to £20m, and 2020 would see the lowest annual level of capital expenditure since 2010.

- DJAN did not explain why extra debt (less debt repayments) of £46m was taken on to fund only £10m of capital expenditure.

- The extra loans alongside the GBP:USD movement meant gross borrowings increased by £64m to £495m, although net borrowings increased by just £4m to £339m.

- Net debt remains equivalent to 13% of the full £2.5b property estate — a very conservative level of gearing for the property sector.

- Annualised bank interest of £17m represented a reasonable 3.8% of the average £463m debt level during the six months.

- Net debt could be reduced during the second half after DJAN confirmed the sale of a £71m London property that was previously “held for sale” on the balance sheet.

- The £71m proceeds will be counterbalanced by a final settlement with HMRC, which this RNS said was paid in November and the 2019 annual report (point 10) said would cost DJAN approximately £43m.

Valuation

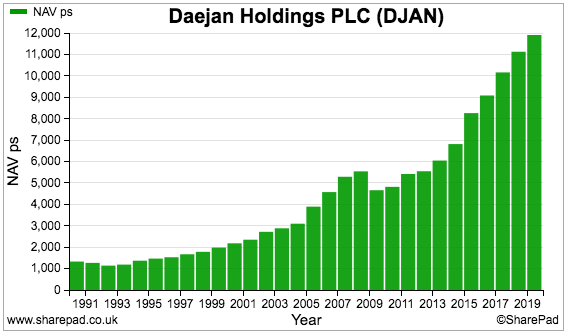

- DJAN’s 2019 annual results declared: “In the immediate future we are unlikely to experience the rate of growth in net asset value that we have enjoyed in recent years.”

- NAV surged from £68 to £119 per share between 2014 and 2019 — a compound average growth rate of almost 12%:

- NAV growth during these six months was just 0.6% .

- Given the low UK gains and the US devaluation, NAV growth for the full year seems unlikely to beat the 7% growth registered during 2019.

- DJAN noted: “Until there is greater clarity on the timing and terms of the UK’s departure from the EU and the outcome of the UK general election in December, the high levels of political and economic uncertainty in the UK are expected to continue. The economic outlook for the USA remains more promising.“

- Maybe the outcome of the recent general election can now lead to lower levels of “political and economic uncertainty”.

- The prospect of low/no NAV growth may explain why the share price has effectively gone nowhere during the last five years — and trades at only 46% of the group’s NAV.

- Other long-standing reasons for the hefty NAV discount include:

- The board’s 80% family shareholding;

- The absence of any takeover possibilities;

- Management’s unconventional corporate governance, and;

- A lack of City engagement.

- Director comments at the AGM in September scuppered any chance of a buyback or REIT conversion to trigger a share-price re-rating.

- Adverse headlines concerning executive diversity did not help matters earlier this year.

- Mind you, the 2019 annual report (point 5) did reveal the board would now consider appointing female directors.

- I remain hopeful that, one day, the discount to book will permanently narrow as the group’s steady performance and growing size become too difficult for the wider stock market to ignore.

- For some perspective, rents have jumped 45%, operating profit before valuation/disposal gains has advanced 90%, NAV has climbed 75% while the dividend has increased 29% between 2014 and 2019.

- And yet during the same five years, the share price has bobbed around the present £55 mark.

- Although near-term rental and NAV progress could be limited, various projects — including a sizeable development in Oxford Street, London (point 3) — will eventually complete and should bolster the full estate’s income and value.

- A £55 share price represents 46% of the latest £120 per share NAV.

- Only during market extremes — the ‘old-economy’ sell off of 2000 and the banking-crash lows of 2009 — has the price to book ever dropped below 40% within the last 20 years.

- Another way of looking at DJAN’s value is from a return on equity standpoint.

- During recent ten-year periods, DJAN has earned at least 7.6% a year from its asset base:

| 10yrs to 2015 | 10yrs to 2016 | 10yrs to 2017 | 10yrs to 2018 | 10yrs to 2019 | |

| Start NAV (£) | 38.94 | 45.74 | 52.88 | 55.40 | 46.60 |

| End NAV (£) | 82.59 | 90.82 | 101.61 | 111.25 | 109.07 |

| Dividends accumulated (£) | 7.55 | 7.83 | 8.11 | 8.41 | 8.74 |

| Total return (£) | 51.20 | 52.91 | 56.84 | 64.26 | 81.22 |

| Total return/Start NAV (CAGR %) | 8.8 | 8.0 | 7.6 | 8.0 | 10.6 |

- Assuming DJAN can earn an average of, say, 7.5% a year from its £120 per share asset base, typical annual earnings could be £8.99 per share — represented by a mix of rental profit and valuation gains.

- In theory at least, enjoying £8.99 per share a year from a £55 entry price is equivalent to a very worthwhile 16% annual return.

- However, perhaps a business that earns a return on equity of only 7.5% deserves a modest rating and should be valued at a discount.

- The trailing 106p per share dividend meanwhile supports a modest 1.9% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Daejan.

Daejan (DJAN)

Recommended final cash offer

Certainly an RNS I did not expect to read this morning — or indeed ever.

The controlling Freshwater family is offering £80.50 per share for the c20% free float. The Freshwaters have held the majority of DJAN’s shares since 1959 and I had thought the business would retain a quote for ever. Certainly cheaper opportunities (e.g. 2008) have presented themselves for a buyout.

The post-meeting chit-chat at last year’s AGM did not suggest anything was planned: “Going private has been discussed, but the Freshwater family “don’t have the appetite” to pay a premium to buy out other shareholders.”

I have mixed feelings about the buyout. Yes, a 50%-plus price jump will bolster my returns this year. However, DJAN was a reliable, lower-risk, no-aggravation, almost hands-off holding — characteristics that will be hard to find within a replacement share.

Here are a few extracts from the announcement, interspersed with my comments:

————————————————————————————————————————

Towards the end of 2019, the Daejan Independent Director received an approach from the Freshwater Group expressing its wish to acquire the Daejan Shares which it did not already own and to take Daejan private. After a period of negotiation involving a material increase in the Offer Price from that first proposed by BidCo, both parties agreed that the Offer should be presented to Relevant Daejan Shareholders because, as explained below, it represents an opportunity for them to realise their investment in Daejan at a price that is unlikely to be reflected in the market in the foreseeable future in the absence of the Offer.

————————————————————————————————————————

DJAN delisting with a low-ball offer was always a risk. Thankfully the sole independent director negotiated a higher price.

The £80.50 offer price compares to the latest £119 NAV per share — so the offer is priced at a 33% discount. Not great, but at least all free-float shareholders will register a profit given the offer represents “a premium of approximately 15 per cent. to the all-time high price of £70.05 per Daejan Share on 18 May 2017.

————————————————————————————————————————

In the five-year period between 20 February 2015 and 20 February 2020, there was a marked divergence between the growth in Daejan’s Reported NAV per Daejan Share and the performance of the Daejan Share price. Over that time, the Reported NAV per Daejan Share increased by approximately 59 per cent. from £75.54 to £119.85, while the Daejan Share price decreased by approximately 12.3 per cent.

————————————————————————————————————————

DJAN’s financial performance diverging from the share price had not gone unnoticed. I wrote in the blog post above:

“For some perspective, rents have jumped 45%, operating profit before valuation/disposal gains has advanced 90%, NAV has climbed 75% while the dividend has increased 29% between 2014 and 2019.

And yet during the same five years, the share price has bobbed around the present £55 mark.”

————————————————————————————————————————

The Freshwater Group has made it clear to the Daejan Independent Director that the Offer is being made entirely at its discretion and if Relevant Daejan Shareholders do not vote in favour of the resolutions to be proposed at the Court Meeting and the General Meeting there may not be another similar opportunity in the foreseeable future.

Furthermore, the Freshwater Group has indicated that it has no intention of selling any of its Daejan Shares, which rules out the possibility of a competing offer from a third party. It has also indicated that, if the Offer is unsuccessful, it has no intention of changing Daejan’s capital allocation or dividend policy and may explore other proposals for achieving a delisting of Daejan without Relevant Daejan Shareholders achieving such an attractive price for the Daejan Shares.

————————————————————————————————————————

DJAN has made clear free-float shareholders ought to accept the offer.

————————————————————————————————————————

BidCo believes that Daejan is better suited to a private company environment. Daejan will also be free from the requirement to meet the public equity market’s reporting requirements, expectations, and the costs, constraints and distractions associated with being a listed company.

————————————————————————————————————————

Not entirely surprising.

DJAN came under fire from diversity campaigners last year. I wrote in August:

“The emerging debate about executive diversity has not helped market sentiment either.

DJAN has never employed a female director — and the board’s “strictly Orthodox background and beliefs” are unlikely to prompt a change any time soon. Diversity campaigners are not impressed.

The board’s old-fashioned ways — which include not moving the previous chairman’s armchair for 40 years — have nonetheless served long-haul investors very well”.

Revised stock-exchange rules for controlling parties of quoted companies may have also added to the red-tape burden and contributed to the exit.

————————————————————————————————————————

It is intended that the Offer will be implemented by means of a Court-sanctioned scheme of arrangement between Daejan and the Relevant Daejan Shareholders under Part 26 of the Companies Act.

In order to be Effective, the Scheme requires:

* the approval of a majority in number representing not less than 75 per cent. in value of the Relevant Daejan Shareholders present and voting in person or by proxy at the Court Meeting; and the sanction of the Court.

…

BidCo reserves the right, subject to the prior consent of the Panel, to elect to implement the acquisition of the Daejan Shares by way of a Takeover Offer. In such event, such takeover offer will be implemented on the same terms (subject to appropriate amendments as described in Part 2 of Appendix I), so far as applicable, as those which would apply to the Scheme. Furthermore, if such offer is made and sufficient acceptances of such offer are received, when aggregated with Daejan Shares otherwise acquired by BidCo, it is the intention of BidCo to apply the provisions of section 979 of the Companies Act to acquire compulsorily any outstanding Daejan Shares to which such offer relates..

————————————————————————————————————————

75% of the 20% free-float shareholders have to agree to the scheme.

If the 75% mark is not reached, then DJAN has left the door open for a Takeover Offer, which I assume will force the (same) deal through whether free-float shareholders accept the offer or not. Looks to me as if this £80.50 proposal will not fall apart.

————————————————————————————————————————

Subject to satisfaction or waiver of the relevant Conditions as set out in Appendix I to this Announcement, the Scheme is expected to become Effective in the second quarter of 2020.

————————————————————————————————————————

Offer should be approved in April and perhaps the proceeds will be received in May.

For now I will hold on to my DJAN shares and await the cash.

That said, if a compelling buying opportunity arises elsewhere, I could sell into the market and take a small discount to the £80.50 offer price and incur selling costs, too.

Maynard

P.S. Thanks to everyone who has sent messages of congratulations about the offer. Always good to know people like to read the blog!

P.P.S. The official documents published so far are located here.

I’ll add to the congratulations, but also offer my thanks having bought into Daejan during your Fool days and added several times since. Thanks also for Tristel, a company I had never even considered before following this blog. Yes there have been some dogs too but in all cases your analysis and updates are insightful, educational and just thoroughly interesting.

Thank you and keep it up!

Tricky.

Hi Tricky

Thanks for the comment and I glad you like the blog. I did think about DJAN in my Fool days after the offer announcement. My records show I tipped the share for Champion Shares PRO at £26 and £22 during Dec 2009 and May 2010 respectively. Let’s say a £24 average, and a sell at £80.50 after ten years. I reckon dividends received come to £8, so a total return of c269% — equivalent to 14% per annum. Not bad for a lower-risk business. Tristel — will publish a write-up on that soon-ish. Hopefully the dog-count will now reduce in number!

Maynard

I have now sold all my DJAN shares.

From my Q1 2020 portfolio review:

“My single Q1 sale was Daejan. The commercial property landlord received an £80.50 per share takeover offer from the controlling Freshwater family during February… and I sold into the market because I became increasingly unsure as to whether the bid would actually go ahead.

Enough small-print was included within the offer RNS to suggest the deal could be called off or re-priced. I suppose a pandemic may well prompt an “adverse change in the business, assets, financial or trading position or profits or prospects” of the property group. A two-week delay to publishing the formal offer document was not encouraging.

The bid may still of course go through unchanged. The Freshwaters appear keen to take Daejan private because the family members want a quiet life — and re-pricing the bid could leave the executives with heightened investor aggravation. Keeping the quote would also mean the group suffering the Covid-19 hit to rents and property valuations in the public eye.

I first bought Daejan in 2015 at £60, then during 2016 at £53, again during 2018 at £57 and again last year at £53 to give an average purchase price of £54. I collected dividends of £3 a share along the way and sold at £77 including all costs.

A 47% gain over a weighted-average holding period of approximately three years is not the greatest result I have ever enjoyed — but not a disaster either in the current market.

Maynard