02 January 2024

By Maynard Paton

Happy New Year!

I trust you enjoyed the festive break and are now ready to battle the market for another twelve months!

This 4,833-word post provides a ‘year in review’ of my current holdings. I recap how each business performed during 2023 as well as provide a few remarks about valuation.

These reviews are very useful to write, not least because they help ensure I am still invested for the right reasons. Any upsets I will suffer during 2024 will most likely be caused by the shares I already own rather than any new shares I will buy.

I undertook the same annual review at the start of 2015, 2016, 2017, 2018, 2019, 2020, 2021, 2022 and 2023.

My portfolio gained 15.3% during 2023. This other post explains that performance in more detail and clarifies how my portfolio begins 2024.

I have covered each of my holdings below in order of size within my portfolio. I have accompanied each write-up with a SharePad chart to show how each company has progressed over the longer term.

Of course my calculations, logic, assumptions and charts may have little bearing on the future… so please do your own research and derive your own conclusions!

Contents

- System1

- Tristel

- Bioventix

- Mountview Estates

- City of London Investment

- S & U

- FW Thorpe

- M Winkworth

- Andrews Sykes

- Mincon

- Tasty

- Summary

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tristel and M Winkworth. This blog post contains SharePad affiliate links.

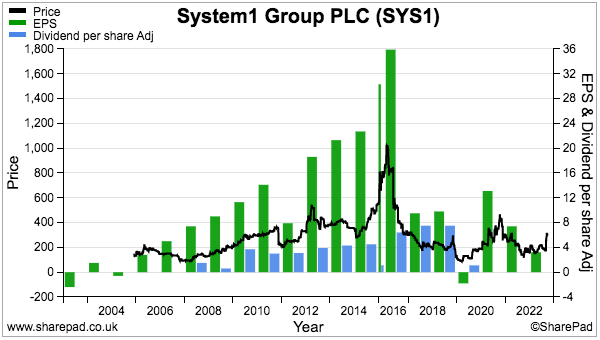

1) System1 (SYS1)

- Bid-price: 280p

- Market cap: £37m

- Portfolio weighting: 21.5%

SYS1 drew my blog into the RNS spotlight last year. Former directors Stefan Barden and James Geddes became frustrated with the ad-testing group’s haphazard progress and requisitioned a general meeting to propose a board revamp… and they referred to my website to help their cause:

“In that regard, you might find the latest System1 Group PLC update from Maynard Paton helpful. Maynard is an investor in the company and also an independent investment commentator and former analyst, who has followed the company closely over a prolonged period. You can find his commentary at https://maynardpaton.com.“

My commentary relayed my conversation with Mr Barden and outlined how, if he were elected as executive chairman, SYS1 would refocus on data services and be sold for at least £8 a share within three years. I backed Mr Barden and Mr Geddes because SYS1’s transition from bespoke consultancy to automated data services had continually faltered under the leadership of founder John Kearon.

Mr Kearon’s 22% shareholding sadly helped veto the board shake-up, but I am convinced the disgruntled 35% of shareholders helped inject some urgency into proceedings. An update just before the board vote funnily enough revealed a bumper Q4 2023, with data/data-led sales growth surging 73% that would herald FY 2023 profit to “slightly exceed previous expectations“.

Those FY 2023 figures were not perfect, with ongoing profit adjustments and inconsistent customer reporting continuing to obscure SYS1’s ‘scalable’ potential.

But the intriguing promise of the group’s ad-testing services does remain: “unmatchable predictiveness” delivered through a “world-class product suite” should lead to larger customers, more predictable revenue, significant economies of scale and very robust financials.

December’s interims disclosed platform income up 44% while the presentation showed “medium term” goals that implied £80m revenue leading to adjusted ebitda of £24m… which compared to the recent £37m market cap may explain why the shares rallied 115% last year.

I bought SYS1 at 325p during 2016, at 238p during 2018, at 183p during 2020 and at 242p during 2021, and have never top-sliced. I remain hopeful the transition to data services can accelerate during 2024, and speculate whether Mr Barden’s plan to sell SYS1 means the group could be valuable to a large industry incumbent.

My SYS1 buy report | All my SYS1 posts

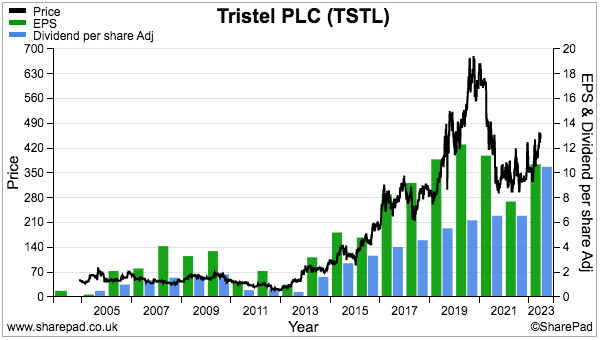

2) Tristel (TSTL)

- Bid-price: 450p

- Market cap: £213m

- Portfolio weighting: 12.2%

This time last year I pondered:

“Could 2023 be the year TSTL finally receives approval to sell a high-level hospital disinfectant in the United States?“

The answer was yes. TSTL announced FDA regulatory approval for an ultrasound-probe disinfectant during the summer after eight years of preparing a submission.

The group described the approval as a “significant inflection point” that would “add a new dimension” to its prospects. The extra USA potential is set to lead to improved guidance — currently 10-15% per annum sales growth and 25%-plus Ebitda margins — at next month’s interims.

Progress last year confirmed the pandemic disruption — hospitals postponed procedures and reduced orders for disinfectants — had now receded. February’s first-half statement showed underlying sales up 21% that were sustained during the second half to support FY 2023 revenue up 22%.

Two-thirds of sales are now earned overseas, while UK revenue of medical-device disinfectants gaining 25% implied no major problems within the group’s largest market. An 85% gross margin meanwhile suggested the group’s main disinfectants still enjoy a competitive edge backed in part through ‘secret’ chemical ingredients and official compatibility with 1,449 medical devices.

True, operating-profit evaluations remain very convoluted due to hefty option costs and US regulatory expenses. But the doubled final dividend, a commitment to 5%-plus yearly payout growth and the £10m net cash position do indicate the accounts are in good order.

The shares rallying 18% during 2023 values TSTL at more than 40x trailing adjusted earnings, and clearly the market is projecting substantial progress for some years to come. As well as revealing sales rising 20%, December’s AGM also announced TSTL’s long-time chief exec is to retire this year.

Deciding to retire when the exciting US potential all lies ahead may seem odd, but I believe TSTL’s ambition to become a “global market leader” demands skills beyond the present board given the protracted FDA saga. I would not be surprised if the finance director, who is married to the chief exec, decides to leave as well. A pair of US healthcare executives could be welcome replacements.

I bought TSTL at a 46p average during 2013 and 2014, and I sold 75% of my shares throughout 2014, 2015, 2016 and 2017 at 79p, 100p, 123p and 289p.

My TSTL buy report | All my TSTL posts

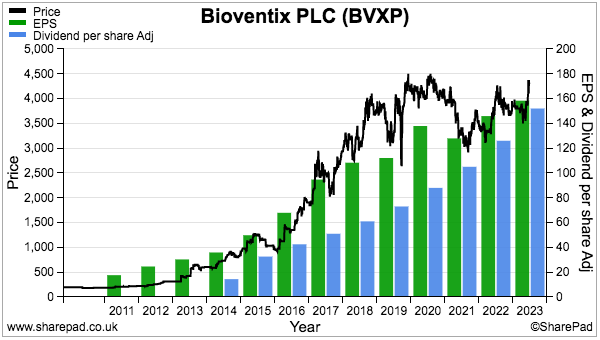

3) Bioventix (BVXP)

- Bid-price: £42

- Market cap: £219m

- Portfolio weighting: 11.2%

BVXP was another company that said farewell to pandemic disruption during 2023. The company’s diagnostic antibodies are utilised within clinical blood tests and had suffered weaker sales when Covid-19 matters overwhelmed hospitals.

Record half-year results delivered during March showed a strong return to normality; revenue recovered 25%, profit rebounded 26% while the interim dividend was lifted 19%.

But October’s annual figures acknowledged a flat second half to re-emphasise the growing maturity of BVXP’s portfolio. Only the newish troponin product is expected to deliver significant revenue growth during the next few years, as income from the other antibodies collectively expands at the industry’s single-digit pace.

Given troponin sales expire during 2032, BVXP’s pipeline R&D has taken on much greater importance. The major potential money-spinner remains an antibody that hopes to detect the very early stages of Alzheimer’s Disease. Increased references to academic papers suggest the lab work is progressing well, but management said at the 2022 AGM any associated revenue would occur beyond 2030.

As investors await R&D excitement, BVXP may transition into an income stock. The final payout was lifted 22% and ensured all earnings since FY 2016 have been distributed as an ordinary or special payout. Yet despite the lack of retained profit, earnings during the same time have doubled.

The wonderful economics of antibody development — customers undertake a lot of the manufacturing and pay BVXP usage royalties — leads to super cash flow and incredible margins. Some 78% of revenue converted into profit last year, with costs kept low because BVXP employs only 16 people in a small lab. Net cash is almost £6m, too.

I bought BVXP during 2016 at £11 and have never top sliced. I patiently await a suitable top-up opportunity, although the recent 26x trailing P/E and 3.6% yield could mean I will be waiting beyond 2024.

BVXP should offer some predictability in today’s uncertain economy; diagnostic antibodies tend not to be toppled unless a significantly enhanced test becomes available. The chief exec founded BVXP, still owns 7% and seems very excited by the dementia research, but I wish he would disclose product sales direct to shareholders and not through the company’s broker!

My BVXP buy report | All my BVXP posts

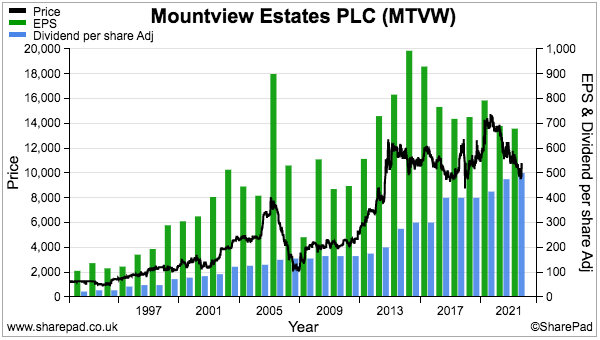

4) Mountview Estates (MTVW)

- Bid-price: £98.50

- Market cap: £384m

- Portfolio weighting: 7.7%

Could 2024 witness activist action at MTVW?

The regulated-tenancy landlord has for years suffered protest votes from the chief executive’s sister and her wider family (24% ownership) about excessive board pay and poor corporate governance.

But last year the protest votes increased by a fifth to 37%. I speculate the AGM appearance of property tycoon David Pears (7% ownership) is connected to the greater objections. Judging by his AGM questions, Mr Pears is an unhappy shareholder.

On the surface at least, MTVW’s reliable financial history does not make the firm an obvious magnet for dissident investors. Since the current chief exec (representing 50% ownership) took charge during 1990, net asset value has rallied 14-fold (+8% per annum average) while the dividend has jumped 43-fold (+12% per annum average).

But progress during recent years has become more debatable. In particular, my calculations suggest properties bought and then sold since 2014 have realised proceeds of only £58m versus an initial cost of £54m. The chief exec has repeatedly confirmed MTVW aims to buy regulated tenancies at 75% of vacant possession value, which should in theory lead to 33% gains on disposal.

Only time will tell what level of gains will be derived from MTVW’s recent purchasing spree. Some £56m was spent acquiring new properties during FY 2023 — the largest amount since FY 2008 — with a further £31m used during the subsequent H1.

MTVW described the acquisitions as “good purchasing opportunities“, which might seem odd when at the same time proceeds from property sales reached a record £395k average. Management talk of “economic difficulties being suffered throughout the country” could in fact signal those “good purchasing opportunities” may not be as good as first imagined.

MTVW’s properties are all carried at cost and I estimate the £102 per share NAV could eventually realise approximately £186 per share versus a mid-price of £103. Exactly what the group’s balance sheet is worth today remains guesswork because management refuses to undertake a repeat of the 2014 independent valuation. That refusal does hint of capital gains since that time being quite limited.

I first bought MTVW during 2011 at £42. I then topped-up at £98 during 2018 and 2019, and have never sold. The very best upside potential seems to occur when the shares trade well below NAV. The resilient dividend meanwhile supplies a worthwhile 5% income.

My MTVW buy report | All my MTVW posts

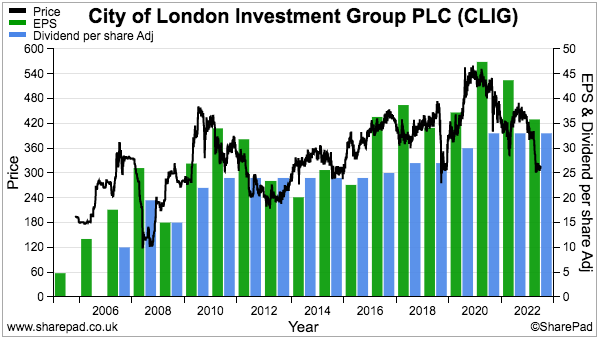

5) City of London Investment (CLIG)

- Bid-price: 314p

- Market cap: £159m

- Portfolio weighting: 7.7%

CLIG was my sole purchase during 2023. I increased my holding by 20% at 320p during Q4 following a scathing AGM statement from George Karpus. The fund manager’s largest shareholder reckoned the board “should be replaced with a seasoned group of directors that understand the enormous potential of CLIG“.

I contacted Mr Karpus to learn more about his statement, and was informed of a somewhat alarming lack of board action following reduced funds under management (FuM), dwindling fee rates and a dividend he believes may become “questionable“.

February’s interims had already admitted profit had fallen 26% after FuM slid 18% and a few more points were chipped off fee rates. September’s annual figures showed no improvement, with rising staff costs looking very awkward given certain FuM strategies showed five-year CAGRs of just 1%.

Mr Karpus founded Karpus Investment Management during the 1980s and knows how to run a lucrative money manager. His firm attracted client money of $3b that paid him a $15m salary before merging with CLIG during FY 2021. Mr Karpus now heads a 36.3% (£59m) concert-party stake.

CLIG retains some attractive financials. Net cash and investments are almost $40m while margins — although not as high as they once were — were a useful 37% during H2. The group’s investment approach for clients, which is based largely on buying investment trusts at attractive discounts, seems eminently sensible as well. But significant new mandates remain frustratingly elusive.

The 10% yield reflects worries that CLIG’s near-term 34p per share earnings projection may not be enough to service the 33p per share dividend should FuM and/or fees rates decline further. I am trusting CLIG’s board will act quickly and appropriately to appease Mr Karpus and avert any chance of a payout cut. The directors collectively own only 1% of the stock and might be hard pushed to shore up support in any SYS1-like activist-vote showdown.

I invested at a 281p average between 2011 and 2013, although I did sell 42% of those shares during 2015 at 335p. CLIG was also my sole purchase during 2022 at 350p. Last year’s trade takes my average buy price to 301p.

My CLIG buy report | All my CLIG posts

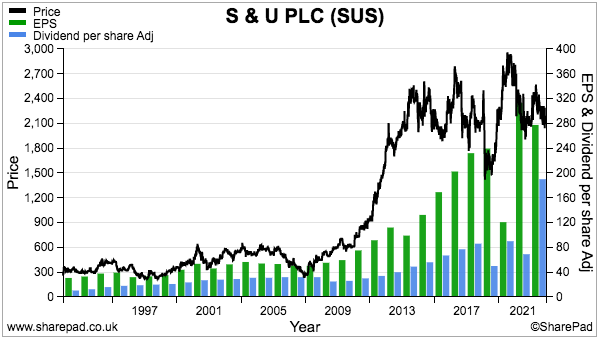

6) S & U (SUS)

- Bid-price: £21.80

- Market cap: £265m

- Portfolio weighting: 7.6%

Commentary from the motor-finance specialist became increasingly frustrated during 2023.

December’s trading update in particular cited the “significant influx of consumer regulation from the Financial Conduct Authority as set out in its Principles for Business, Consumer Credit Source Book, its “Dear CEO” letters, the Borrowers in Financial Difficulty review, its Tailored Support Guidance……….and now by the Consumer Duty” that combined have become “a major [and] often subjective and expensive process“.

Just how the ballooning regulatory burden will impact the economics of hire-purchase on used cars remains to be seen.

But the timing of the additional red tape is not ideal given higher interest rates, cost-of-living woes and transactions within the second-hand car market subsiding by 5%.

And vehicle-loan repayments presently running at 91% of due versus 94% twelve months earlier year may be an early sign of faltering progress — especially as SUS’s borrowers have imperfect credit histories.

That said, I would view any trading setback as a potential buying opportunity, not least because the group’s veteran family executives boast a 42%-plus shareholding, enjoy 40-year tenures and have successfully navigated previous downturns by always ensuring careful underwriting and prudent borrowing.

A hallmark of the family’s success is the dividend expanding 53-fold since 1987 with only one cut (during the pandemic).

Annual results during March showed NAV up 9% and the dividend up 6%, although October’s interims admitted higher tax rates and debt costs had limited NAV growth to 2% and kept the half-year payout unchanged.

NAV is almost £19 per share and the £22 price hardly seems overrated given SUS’s illustrious track record. NAV has grown by 170% since SUS disposed of its home-credit division during FY 2015, and some very appealing returns from the motor-finance subsidiary are obscured by SUS’s smaller property-bridging operation. SUS’s property loans have historically led to minimal write-offs and, importantly in the current climate, are not regulated.

I first bought SUS during 2017 at £21 and bought more during 2019 at £19 and again during 2020 at £17. I have never top-sliced. I am hopeful 2024 sees resilient trading and an opportunity to invest very close to (or even below) NAV. The yield while I wait is 6%.

My SUS buy report | All my SUS posts

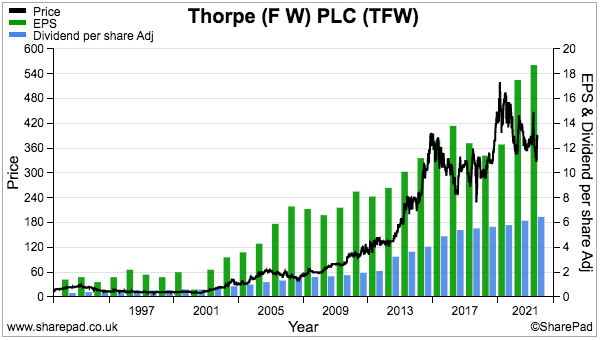

7) FW Thorpe (TFW)

- Bid-price: 380p

- Market cap: £452m

- Portfolio weighting: 7.2%

“I think it is fair to say that Thorlux has provided a fantastic service”

So said the project manager responsible for refurbishing Parliament’s Elizabeth Tower and Big Ben, the clock faces of which are now illuminated by 228 ‘luminaires’ designed and manufactured by TFW’s largest subsidiary.

The clock tower’s new lights have yielded a 60% energy saving, and reducing energy costs through LED systems continues to attract customers to TFW. September’s record annual numbers showed sales up 11% and operating profit up 9% excluding the contribution from recent acquisitions. The dividend was lifted 5% to mark the 21st consecutive annual increase, and has not been cut since 1991. TFW began manufacturing energy-saving lights during 1994.

Acquisitions have been significant influences on shareholder returns during recent years. Two Dutch businesses bought in stages between FYs 2016 and 2022 for an eventual £30m produced a useful £7m profit last year. TFW’s largest customer — a German lighting installer — was meanwhile acquired during FY 2023 for what could be £19m and supplied a useful £2m profit during its first nine months of ownership.

But the FY 2022 purchase of a Spanish lighting firm for what could total approximately £37m is not looking as promising; its FY 2023 profit was less than £3m. And a £6m investment in an EV charging joint-venture lost money last year.

TFW’s quest for greater geographical and product diversity has thankfully not influenced its capital structure. The latest statement commendably noted the group “chooses to maintain a large reserve as one never knows what is around the corner, as proven recently by the COVID lockdown.” Year-end cash was £35m versus financial liabilities of only £3m.

The hefty cash position reflects the long-term thinking of the Thorpe family, which retains a reassuring 45% board shareholding through two former executives and an executive in his 40s.

TFW’s immediate outlook is not incredible, with November’s AGM indicating modest progress during 2024. Management also wants to improve margins; ten years have passed since the group last converted more than 20% of revenue into profit.

Demand for energy-efficient lighting plus prime ESG attractions help justify the c20x rating. I first bought during 2010 at 69p and bought more during 2011 at 80p and during 2012 at 89p. I sold 25% at 234p during 2016.

My TFW buy report | All my TFW posts

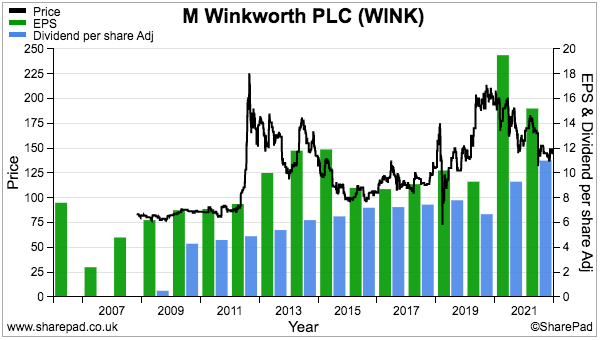

8) M Winkworth (WINK)

- Bid-price: 140p

- Market cap: £18m

- Portfolio weighting: 6.6%

WINK unsurprisingly succumbed to higher mortgage rates last year.

Fewer property transactions caused sales commissions to drop 18% and left September’s half-year results revealing a 26% profit decline. The estate-agency franchisor also admitted its near-term progress had effectively become dependent on Threadneedle Street:

“The outlook for the rest of the year depends to a large extent on the perceived and actual end of the tightening cycle and the Bank of England’s success in managing inflation down towards its target.”

Forthcoming full-year figures are therefore likely to show a subdued outcome.

Still, WINK might be able to manage a faltering housing market better than most.

In particular, the firm’s franchising structure — 101 of the group’s 103 branches are operated by franchisees — provides greater flexibility to chop and change personnel “to maintain… high standards” if “business conditions are not met“. Re-franchising marginal London offices to “new blood” can apparently lead to branch revenue tripling or more.

Conducting business with self-employed, self-motivated franchisees should inherently help matters, too. Productivity remains impressive, with the number of sold-subject-to-contracts, exchanges, withdrawal rates and listing-to-offer timescales all beating local competition throughout 2023.

Additional company-owned branches — returns from the group’s two offices have been impressive — plus WINK’s fledgling commercial-property venture might assist 2024 as well. And the group is still very profitable, despite the 19% H1 margin being the lowest since FY 2009 (pandemic aside).

WINK’s balance sheet remains healthy, with the 81-year-old chairman ear-marking the net cash of £4m to “prioritise” dividends. WINK’s seasoned family directors retain a 47% combined shareholding and do like their quarterly payouts. The dividend has more than doubled during the last ten years, and the cut during the pandemic was more than made up through three specials the year after.

Dividend cover is hovering close to 1x and has left the shares yielding more than 7%. I am hopeful of a buying opportunity during 2024, although liquidity can be minimal.

My initial WINK buy occurred at 90p during 2011 and I sold 70% of my holding during 2013 and 2014 at 173p. I rebuilt my stake at an average 116p during 2016 and 2017, with a 178p top-up made during 2021.

My WINK buy report | All my WINK posts

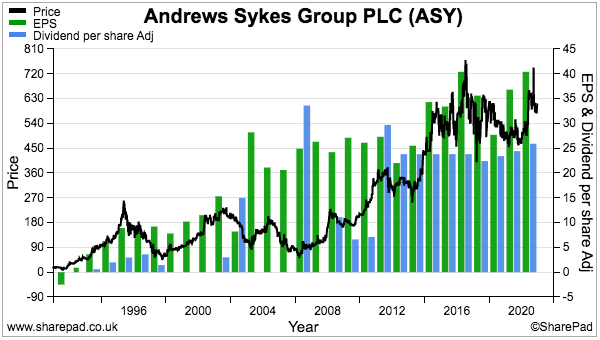

9) Andrews Sykes (ASY)

- Bid-price: 600p

- Market cap: £251m

- Portfolio weighting: 3.2%

ASY’s bumper 59.4p per share special dividend was a particular portfolio highlight of 2023.

The equipment-hire specialist had previously declared special payouts during 2020 and 2022 when net cash had reached approximately £30m, and this time last year I pondered whether “further extra payments may perhaps now be distributed whenever the cash position exceeds that level”.

Net cash in fact reached £39m within September’s interims, and the £25m extra payment reflected “surplus” reserves following the group’s “robust cash generation and de-risking of the defined benefit pension scheme“. ASY did not reveal the initial cost of pension scheme’s “buy-in deal“, but contributions that were running at £1.3m a year should no longer be necessary.

The huge special payout and settling the retirement obligations were announced just a few months after the death of ASY chairman Jacques-Gaston Murray. Mr Murray was probably the oldest director among quoted UK companies — he died aged 103 — and his family are left controlling 91% of the shares.

Wishful thinking perhaps, but the recent dividend and pension actions could be interpreted as optimising the balance sheet for a potential suitor. But I would be happy if ASY remains stewarded by the Murrays; since my initial purchase at 233p during 2013 I have received total dividends of 356p.

ASY’s progress is influenced by extreme weather, such as cold snaps, heatwaves and extensive rain, which create sudden demand for the group’s heaters, air conditioners and water pumps. But I must confess the scorching summer of 2022 did not have the bonanza-like impact I had expected on the annual results published during May.

Those full-year figures showed revenue and profit up 10% and 8% respectively, with UK air-conditioning turnover up 36% suggesting the major money spinners are the heaters and pumps.

Still, May’s results set fresh sales and profit records, as did September’s interims that delivered an appealing 25% margin — the highest H1 margin since FY 2008. But ASY did admit trading during recent months had been “more mixed” and the climate references were economy- rather than weather-related.

European depots support approximately 40% of revenue and future overseas expansion offers longer-term potential, although such progress has been slow going. The 14x trailing P/E and yield of 4.2% do not suggest an obvious bargain.

My ASY buy report | All my ASY posts

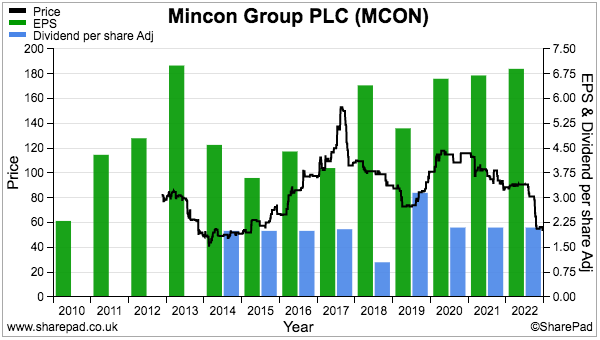

10) Mincon (MCON)

- Bid-price: 53p

- Market cap: £114m

- Portfolio weighting: 1.9%

Twelve months ago I pondered whether 2023 might witness a turning point for MCON. The industrial-drill manufacturer had just announced its first commercial contract for Greenhammer, a new drilling system that management claimed offered “transformational potential for Mincon and the hard-rock surface mining industry“…

…but MCON’s progress unfortunately turned down rather than up.

Rather than splash out on Greenhammers, mining customers in fact reduced their exploration plans and equipment stockpiles. H1 figures published during August showed sales down 5%, with mining-related revenue sliding 15% and mining revenue within Europe and the Middle East collapsing 72%.

Trading appears to have deteriorated further; October’s Q3 admitted nine-month sales down 7% and noted Q4 would suffer from a large construction contract being deferred into 2024 and another seemingly scrapped entirely.

The shares fell 38% last year to a 53p bid price versus the 45p I paid for the shares during 2015.

During my time as a shareholder, the substantial sums spent on new facilities and bolt-on acquisitions have yet to convert the group’s first-class engineering into super accounts. Significant financial differences include lower margins (19% during 2015 versus c12% now) and balance-sheet gearing (€42m net cash during 2015 versus €15m net debt now).

Working-capital certainly needs attention; some €76m of stock is equivalent to an enormous c45% of annual revenue and has diminished returns on capital to single digits. Perhaps it’s no surprise the share price has dropped closer to the 46p per share tangible NAV.

October’s update predicted an Ebitda of €20m for 2023 — which admittedly points to H2 Ebitda down 45% to €8.2m — but does not indicate the business is completely broken. Alongside Greenhammer, projects involving large-diameter drills and subsea micropiles may one day provide a healthy return on their R&D.

I believe MCON has essentially become a bet on the founder family management, which owns 56% of the business and did not sell any shares at the 2013 float and has not sold any since.

I have not sold any MCON shares either, and I trust a veteran family executive becoming chief operating officer (to assist his brother as chief exec) will eventually help improve the group’s economics.

The 2.1 eurocents per share dividend meanwhile supplies a 3% income as a recovery is awaited.

My MCON buy report | All my MCON posts

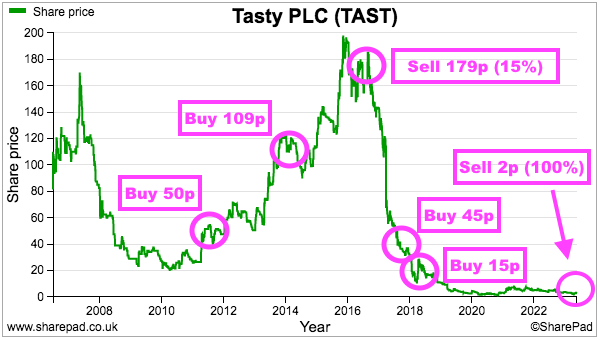

SOLD) Tasty (TAST)

I finally faced up to reality last year and exited TAST. The disposal was my 22nd complete sale since 2004 and the eighth to score a loss… and what a loss it was.

Selling at 2p locked in losing 85% of my total investment.

I first bought TAST at 50p in 2011 and again at 98p in 2014. I sold 15% during 2016 at 179p — and of course regret not selling the rest. Instead I bought more at 45p during 2017 and even more during 2018 at 15p:

I had hoped the hapless restaurant chain could one day instigate a turnaround and prompt the bombed-out share price to stage a dramatic recovery. But some further reflection eventually persuaded me to abandon this disaster.

I belatedly recognised TAST’s menu format and cost structure was inherently flawed, and concluded only an extensive business overhaul could rescue the business.

TAST sadly did not undertake the “radical management thinking” I had encouraged during the early pandemic lockdowns. The chain instead re-opened after the pandemic with the same pizza/pasta/burger menu and the same way of working at the very same locations — and suffered the same losses as before the pandemic!

Lots of lessons to recognise here, not least how businesses employing large numbers of lower-paid staff can suffer when the minimum wage continues to ratchet higher.

During my twelve years owning TAST, employee costs increased from 36% to 44% of revenue to leave no profit for shareholders. TAST’s staff simply did not serve more diners to cover their extra wages.

I guess TAST’s story proves how family management cannot always guarantee success when the economics of an industry change permanently for the worse.

TAST directors Adam and Sam Kaye with their cousin Jonathan Kaye had flourished previously with multi-bagger chains ASK Central in the 1990s and Prezzo in the 2000s. But the hospitality sector moved on during the 2010s, and the Kayes had not kept up.

Looking back, being asked not to write down any notes when attending a one-to-one meeting with media-shy Sam Kaye during 2017 was probably a signal all was not well!

Summary

Last year I stuck with ten of my eleven shares and my holdings mostly exhibit the traits outlined in How I Invest:

- Capable, owner-aligned management;

- Decent accounts;

- Respectable track records, and;

- Reasonable prospects.

The plan for 2024? I am hopeful my returns can remain positive as a mix of savvy management and conservative balance sheets help my shares navigate an uncertain economy. But I am mindful that interest rates rising from less than 1% to more than 5% over 14 consecutive months could easily expose further weaknesses throughout the market. I believe today’s rates are here to stay and will invest accordingly.

My portfolio presently has a 13% cash position to deploy, and leading top-up candidates are CLIG, MTVW, SUS and WINK. My SharePad articles could of course identify some suitable alternatives. I would ideally like to buy at bargain-basement prices, but I recognise the downside of holding too much cash if the market surges from here.

I trust you found this annual review informative. I certainly found it useful to write.

Please click here to examine my portfolio’s 2023 performance in more detail.

Until next time, I wish you safe and healthy investing!

Maynard Paton

Happy New Year, Maynard. This is an absolutely excellent review and of particular interest to me as TSTL, CLIG and BVXP are three of my larger holdings. We exchanged comments on CLIG after the AGM (I also added – on the day of the AGM) and I continue to hope that the Board address the concerns raised by Mr Karpus asap.

I noted your comments about TSTL (my largest individual shareholding by some way in various personal and family accounts). I went to the December AGM, having been slightly surprised by the announcement that morning that Paul Swinney is stepping down, although he has committed to provide support to the new CEO, once selected. In the last few months, Paul is the third CEO of an AIM company in which I am invested (the others are Treatt and Zotefoams), to announce that they intend to step down. As I said at the AGM, I am starting to take it personally.

I do not believe that any of these CEOs were forced out, as all those companies are successful. Being a CEO is very stressful and Paul has been at the helm for 30 years, so I understand why he would wish to step down, having achieved the key FDA approval back in June. Never say never, but I am much less convinced that Liz Dixon will also step down. Indeed, I would not be at all surprised if she throws her hat into the ring as the CEO successor. I very much hope that she does, although I also think that the management team needs to be supplemented in any event as the company grows. I spent some time in the Q&A following the formal AGM and in discussions with various board members afterwards discussing what happens next. The AGM RNS mentions the appointment of The Coulter Partnership to assist in the succession process. I understand that they were up against the much better known (in my view) Heidrick & Struggles – and won very convincingly. The CEO of The Coulter Partnership is apparently heading the team. I think that now is the right time for TSTL to consider what management team it needs for the group over the next development stage – including M&A experience if it receives takeover approaches (which I expect).

My other observation is that whilst the US market is key, there are large parts of the world where it should be relatively easy for TSTL to grow – or initiate – sales. I talked about that quite a lot at and immediately after the AGM. I have encouraged TSTL a number of times to update and share their global strategy (other than for the US) with shareholders. One easy way would be to provide a one page slide of where new applications are in progress, have been consented recently or are planned. That slide used to be part of shareholder briefings.

Best Regards and thanks for the first rate information that you provide,

Andrew

Hi Andrew

Many thanks for the comment and I am glad you found the blog post useful.

I think among TSTL’s executives, I would venture Bart Leemans as my favoured CEO. He founded Ecomed, TSTL’s BEL/NED/FRA distributor that was acquired by TSTL about 5 years ago. I get the impression he is more of a ‘hands on’ entrepreneur rather than a ‘desk bound’ manager. He also owns c2% of TSTL and has (I think) never sold a TSTL share since he sold Ecomed to TSTL, which I like. Not sure he would like trawling around the City meeting with shareholders though. He has not attended many of the summer open days.

The re-restatement of the recent accounts because the auditor disagreed with TSTL’s earlier interpretation of ‘discontinued activities’ does not put the FD’s skills in a good light, at least in my view. If a new CEO is appointed, might be difficult for the FD to then accept a new way of working when her (ex-CEO) husband is at home saying ‘that’s not what I would have done’ :-) There must be loads of senior divisional managers at multinationals such as Reckitt, JnJ etc who would jump at the chance to run a sub-£40m revenue quoted business blessed with 80% gross margins, net cash in the bank, ample growth opportunities overseas and a history of granting hefty options. The CEO appointment could genuinely become pivotal for shareholders if the new boss can exploit the overseas markets to their full. Agree with your view that TSTL could do more to highlight its non-US overseas potential.

Maynard

Hello Maynard.

Whilst I agree that the management team at TSTL needs to be refreshed, I worry about too much change, too soon. The team culture that exists at TSTL is very important, in my view, which is why I favour internal promotions, coupled with the injection of new blood. It is critical that they get this right. I admire Bart Leemans, but I am not convinced that he would be the right CEO, as distinct from running Europe. Mr and Mrs Swinney will continue to hold a large chunk of TSTL and so I think will want to steer that at board level, pending what I see as an inevitable exit through a takeover. For me, that counter-balances concerns about backseat driving. I certainly hope that they hang on to most of that stake. Anyway, we will know more in the next year.

Regards,

Andrew

Thanks Andrew. Will be fascinating to see who eventually is appointed.

Maynard