11 February 2024

By Maynard Paton

FY 2023 results summary for FW Thorpe (TFW):

- A record FY performance bolstered by acquisitions that showed total revenue up 23%, adjusted profit up 16% and the ordinary dividend lifted for the 21st consecutive year.

- Largest division Thorlux continued to fare well, expanding by almost 30% helped by SchahlLED acquired at a possible 5x Ebitda.

- Mixed progress was experienced elsewhere, with Dutch profit down 8%, Zemper yet to show its full potential and the EV-charging joint venture going from profit to loss.

- Despite acquisition payments of £19m, very respectable cash conversion left cash only £6m lower at a very useful £35m — a figure that required justification to ‘some shareholders’.

- A possible 20x P/E seemingly reflects TFW’s distinguished operating history and the persistent demand for energy-saving lighting rather than doubts about the significant acquisition expense and near-term prospect of subdued trading. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Thorlux and SchahlLED

- Netherlands

- Zemper

- Ratio Electric

- Other companies

- Financials: balance sheet and cash flow

- Financials: pension scheme and employees

- Valuation

News links, share data and disclosure

- Annual results for the twelve months to 30 June 2023 published 12 October 2023;

- AGM statement published 16 November 2023;

- Directorate changes published 04 July 2023, and;

- Directorate change published 16 Jan 2024.

- Share price: 375p

- Share count: 118,935,590

- Market capitalisation: £446m

- Disclosure: Maynard owns shares in FW Thorpe. This blog post contains SharePad affiliate links.

Why I own TFW

- Develops professional lighting systems with a long-established reputation for high product quality, leading technical innovation, first-class service and sustainable manufacturing processes.

- Board led by a veteran executive and assisted by family non-execs who steward a 43%/£191m shareholding and favour special payouts.

- Conservative accounts typically display useful operating margins, substantial cash reserves, consistent working-capital management and illustrious rising dividend.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary

Revenue, profit and dividend

- A record H1 performance that anticipated a “quite positive” H2…

“High energy costs and the imminent ban on the sale of fluorescent lamps in the UK and EU are both stimulating activity in the Group’s key market sectors. The outlook for the second half remains quite positive, although the revenue growth percentage is unlikely to be maintained at such a high level due to the good performance in the second half of last year.”

- …had already heralded a satisfactory FY 2023.

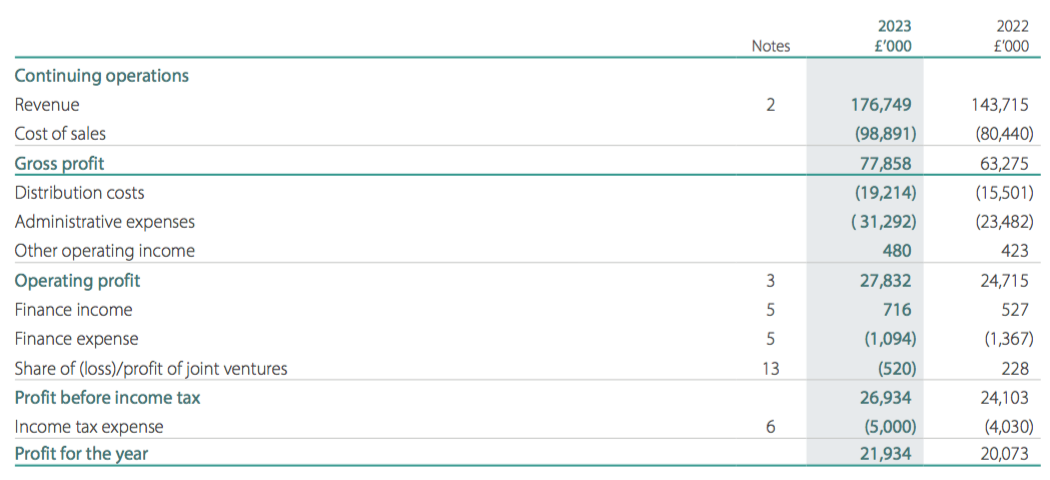

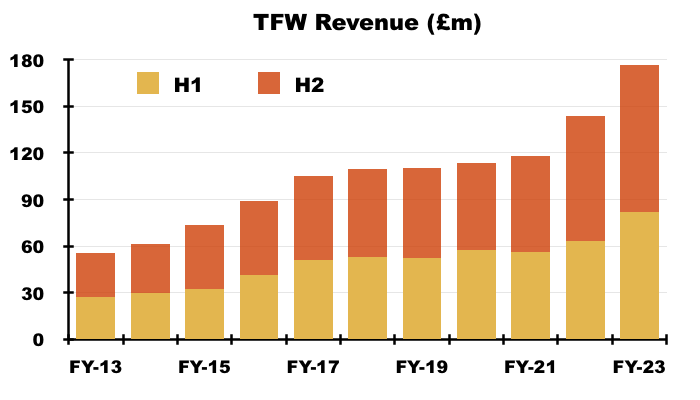

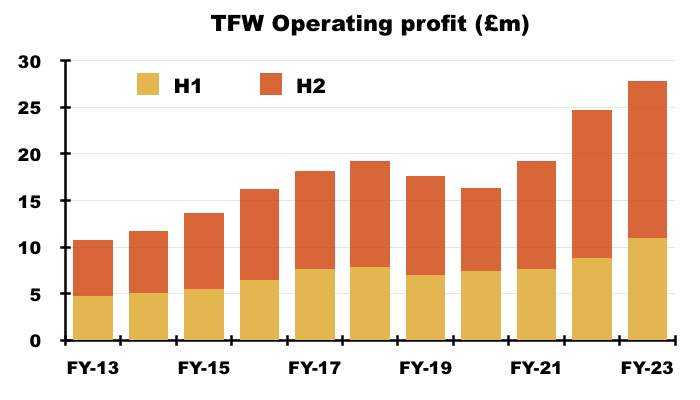

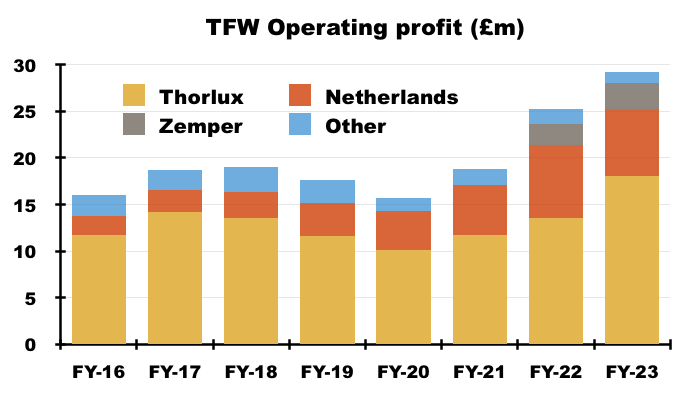

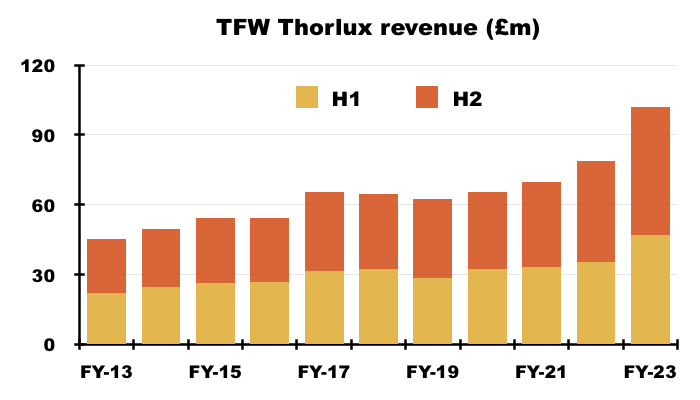

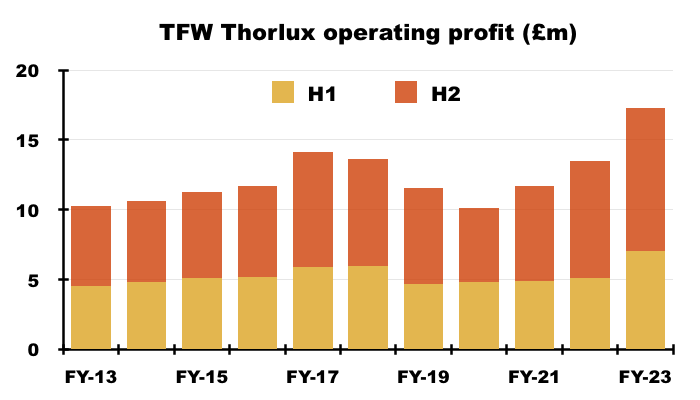

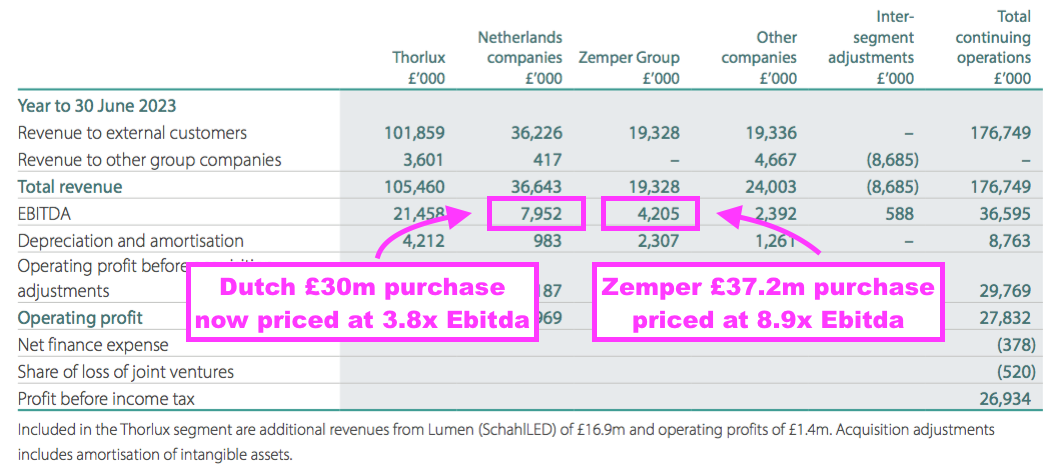

- This FY set new highs for both revenue, up 23% to £177m, and operating profit, up 13% to £28m:

- Progress was boosted by two acquisitions:

- Zemper, which was purchased during October 2021 and contributed for nine months during the comparable FY and twelve months during this FY, and;

- SchahlLED, which was purchased during September 2022 and contributed for nine months during this FY.

- TFW reckoned growth adjusted for the two acquisitions was 9%-11%:

“Excluding Zemper and SchahlLED acquisition effects, for comparison’s sake, like-for-like revenue increased by 11% to £159.1m and operating profit by 9% to £26.9m.“

- TFW described this FY as “less turbulent“, with a greater supply of components — notably microchips — allowing an order backlog to be fulfilled:

“Financial performance overall was strong, with significant organic revenue increases for most companies, primarily due to much improved material availability and the consequential fulfilment of the previous year’s order backlog“

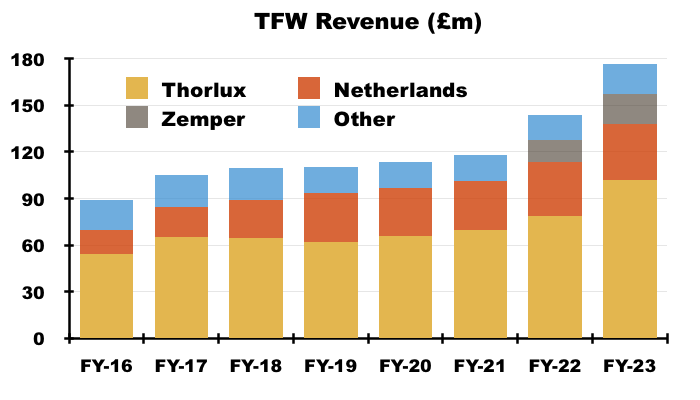

- Divisional results were mixed. Thorlux, which now encompasses SchahlLED, was the best performer. Zemper, the Dutch operations and various Other subsidiaries meanwhile did not fare quite so well:

- The ability to pass on cost increases to customers seemed to dictate the differing divisional efforts:

“All companies wrestled with inflationary effects on material and labour costs, and some were better able than others to adjust selling prices to maintain margins.“

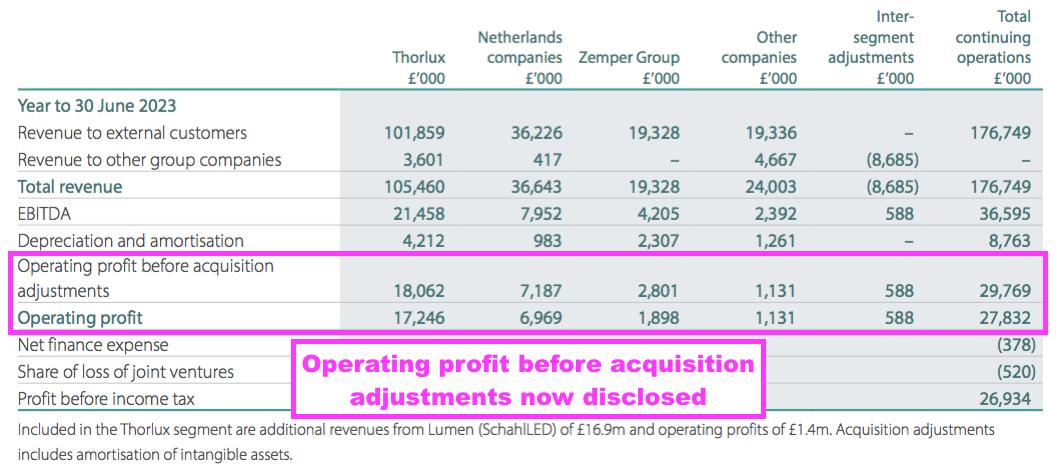

- TFW reiterated its reported operating profit was hindered by acquisition adjustments:

“Given the Group has committed to acquiring the remaining shares over the next few years, we account for 100% of the revenue derived by these companies but adjust the operating profit for intangibles valued at acquisition and profit before tax to reflect the minority shareholding. For added complexity, SchahlLED predominantly distribute Thorlux products, so there are further adjustments at a revenue and operating profit level.“

- The adjustments involve the amortisation of acquired intangibles as well as (I believe) changes to earn-out provisions. TFW helpfully disclosed operating profit before and after such adjustments:

- FY operating profit before the acquisition adjustments in fact gained 16% to £29.8m.

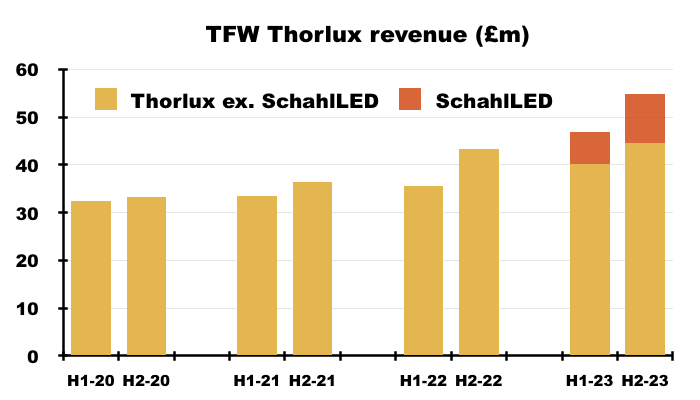

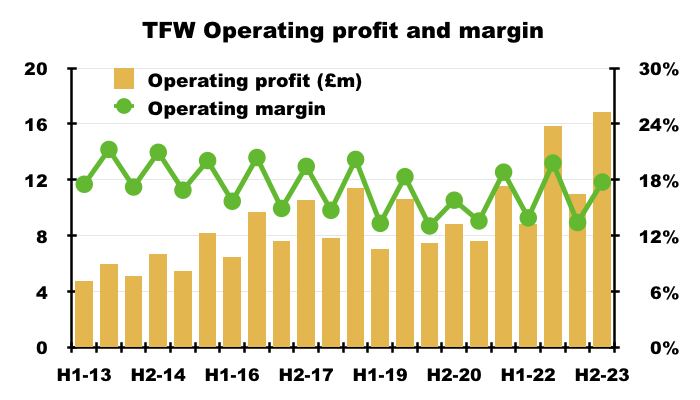

- H2 set new six-month records for both revenue, up 18% to £95m, and operating profit, up 5% to £17.2m before acquisition adjustments.

- Excluding SchahlLED, H2 revenue would have gained approximately 6% to almost £85m.

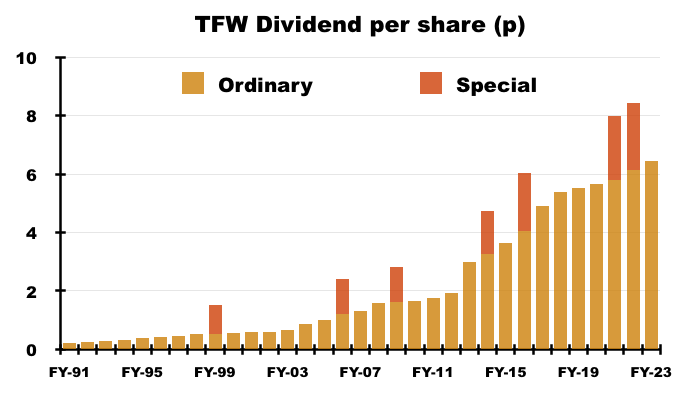

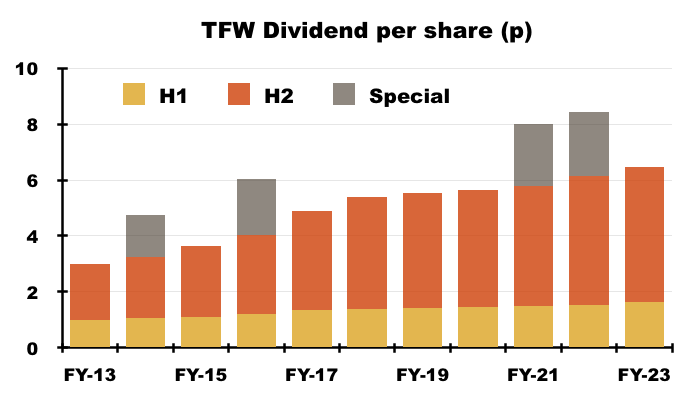

- The final dividend was raised 5% to match the 5% H1 dividend lift and ensured TFW registered its 21st consecutive annual dividend increase:

- The payout has not been cut since at least 1991.

- The ordinary dividend has expanded at an 8% CAGR during the last 10 years:

- Special payouts were declared during FYs 2021 and 2022, but understandably ceased following significant expenditure on SchahlLED, Zemper and joint-venture Ratio Electric (see Financials: balance sheet and cash flow).

Thorlux and SchahlLED

- Thorlux manufactures a wide range of professional lighting equipment — most notably the SmartScan system — and represents approximately 60% of the group:

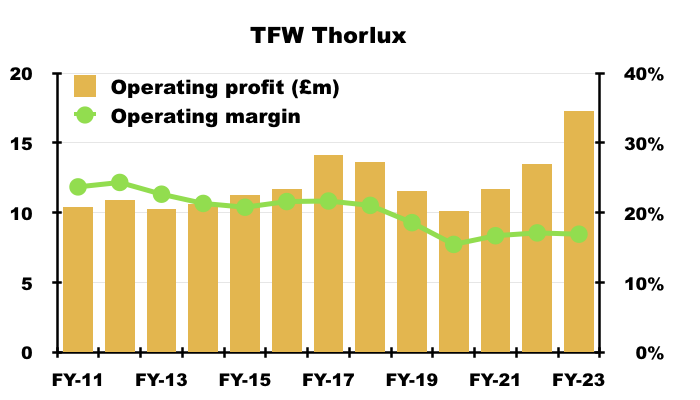

- Thorlux reported a record divisional effort, with FY revenue up 29% to £102m and FY operating profit up 28% to £17m:

- Thorlux started working with SchahlLED during 2019, after which the German lighting installer quickly became TFW’s largest customer before being acquired by TFW:

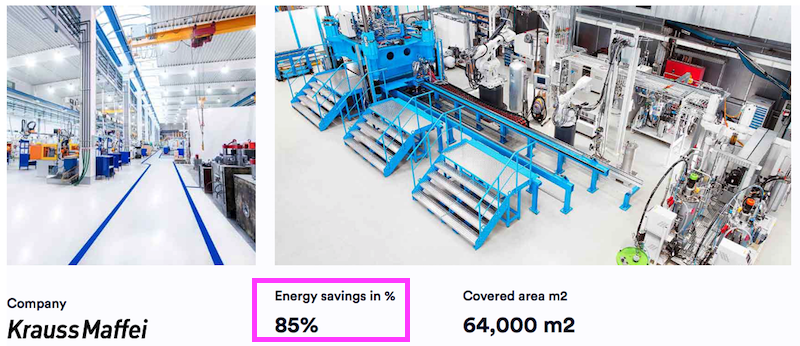

- A SchahlLED case study involving KraussMaffei reported an 85% reduction to energy costs through installing Thorlux lighting. The customer apparently enjoyed a “high return on investment with a payback period of less than 3 years“:

- SchahlLED was amalgamated into Thorlux and delivered the following nine-month contribution:

“In the year, SchahlLED added nine months of revenue to the consolidated figures of £16.9m and operating profit of £2.3m before acquisition adjustments.”

- SchahlLED’s twelve-month revenue was €23.9m/£20.8m:

“If the acquisition had occurred on 1 July 2022 the consolidated pro-forma revenue and profit before tax for the year ended 30 June 2023 would have been €23.9m (£20.8m) and €1.3m (£1.1m) respectively.”

- €23.9m compares well with the €15.9m recorded during calendar 2021 that was stated at the time of acquisition:

“During the last financial year ending 31 December 2021, SchahlLED achieved revenues of €15.9m with EBITDA of €2.8m.“

- TFW looks set to pay €7.5m/£6.6m for the outstanding 20% of SchahlLED to take the total payment to €22.1m/£19.5m:

“On 23 September 2022, the Group acquired 80% of the share capital and hence control of Lumen Intelligence Holding GmbH, a company that holds 100% equity interest in SchahlLED Lighting GmbH, a turnkey provider of intelligent energy saving lighting products for the industrial and logistics sectors.

The company was acquired for an initial consideration of €14.6m(£12.9m). There is a fixed commitment to acquire the remaining shares, based on current best estimates, a further €7.5m (£6.6m) could be payable, which is subject to future performance conditions.”

- The €7.5m/£6.6m earn-out for SchahlLED was calculated at eight times Ebitda:

“A multiple based on a six times EBITDA, that we consider a reasonable multiple for the sector, is used in these computations, except for Zemper CGUs and Lumen CGUs where an EBITDA multiple of ten and eight, respectively, have been used in accordance with the agreement upon which the contingent consideration is based.”

- The acquisition announcement said the SchahlLED earn-out would be based upon Ebitda generated during this FY:

“FW Thorpe has paid an initial consideration of €14.6m (circa £12.8m) and could pay an additional amount to be determined by SchahlLED’s EBITDA performance in the year ending 30 June 2023.”

- Paying €7.5m/£6.6m for 20% of SchahlLED based upon eight times Ebitda implies 100% of SchahlLED’s Ebitda for this FY was €4.7m/£4.1m ((€7.5/£6.6m)*5/8)).

- €4.7m compares well with the €2.8m recorded during calendar 2021 that was stated at the time of acquisition:

“During the last financial year ending 31 December 2021, SchahlLED achieved revenues of €15.9m with EBITDA of €2.8m.“

- Paying a total €22.1/£19.5m for SchahlLED Ebitda of €4.7m/£4.1m equates to an Ebitda multiple of less than 5.

- TFW’s return on its SchahlLED investment could be fine-tuned for the subsidiary’s depreciation, amortisation and taxation, its loans of €2.6m (now repaid) and the gross margin now captured by Thorlux, but my single-digit Ebitda multiple already suggests the deal was not extravagant.

- Thorlux’s FY revenue without SchahlLED gained 8% to £85m, although the division’s H2 revenue without SchahlLED advanced only 3% to £45m:

- Thorlux’s FY operating profit (before acquisition adjustments) without SchahlLED gained 17% to £16m.

- Thorlux’s FY operating margin (before acquisition adjustments) without SchahlLED was therefore 18.6% (£16m/£85m).

- Thorlux’s FY operating margin (before acquisition adjustments) with SchahlLED was 17.7% (£18m/£102m).

- The 17.7% divisional margin for this FY was the highest since FY 2019 (18.6%)…

- …but was a few percentage points below the 21%-plus scored regularly up to FY 2018.

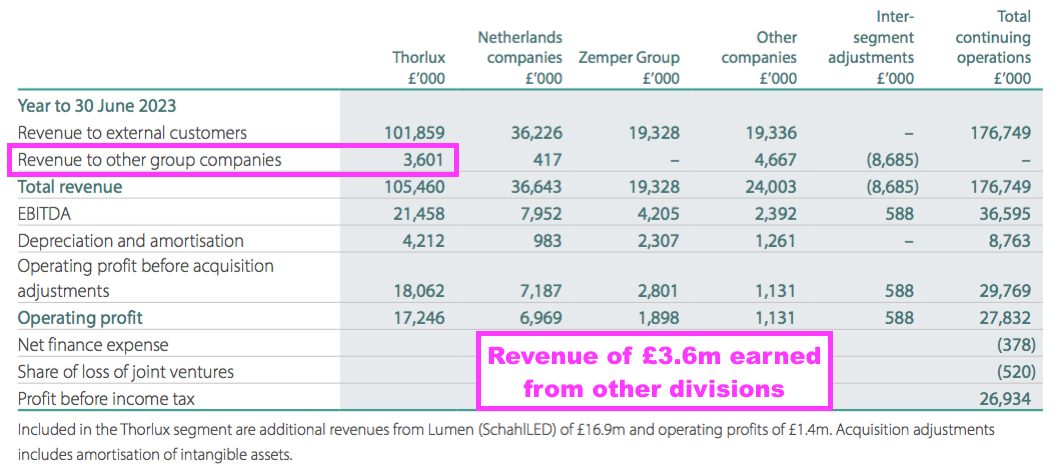

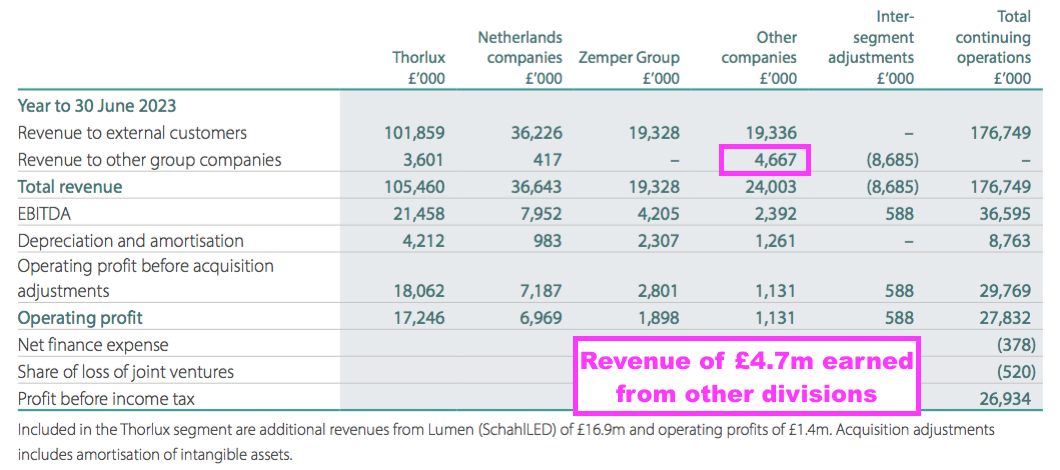

- Note that Thorlux also supplies products to different group subsidiaries, and the profit generated when those products are sold to the final customer may accrue to those different subsidiaries and not to Thorlux:

- Products worth £3.6m were sold to other subsidiaries during this FY, and the yearly figure has typically bobbed between £3m and £4m since FY 2017.

- Thorlux’s margin may have been assisted by fewer supply and redesign headaches:

“With the improvement in component availability, Thorlux’s engineering resource has been able to move the focus away from sourcing and redesigns, to more forward-looking activities supporting product innovation.”

- Wider Thorlux progress appeared supported by SmartScan…

“The SmartScan platform has delivered strong revenue growth again this year, with new features added as part of the generation 2 launch. New products include a commercial luminaire range with reduced material usage and energy consumption, underpinning Thorlux’s sustainability credentials.”

- …alongside favourable environmental/regulatory trends.

“Whilst energy costs are slowly reducing, there is still a push for both carbon reduction and data reporting – areas where the SmartScan system excels and has a proven track record. Along with the impending ban on fluorescent lamps across the UK and the EU, these factors should counteract any slowdown in general capital investment commitments.”

- This FY unveiled a top-secret Thorlux lighting project at the Houses of Parliament:

“Thorlux developed special products between 2016 and 2022 which provide colour-tuneable illumination of all four clock faces and the balconies above, a new Ayrton Light (a special lighthouse style lamp used to indicate when Parliament is sitting), illumination of the clock mechanism, the bells, including floodlighting the Big Ben bell itself, all internal rooms, and the 340 steps, and all emergency lighting. SmartScan features heavily in the controls for ancillary areas.

The project has been kept secret until now, even during the 2023 New Year celebrations.”

- More day-to-day Thorlux projects involved a factory, some healthcare offices, a warehouse and a cricket school:

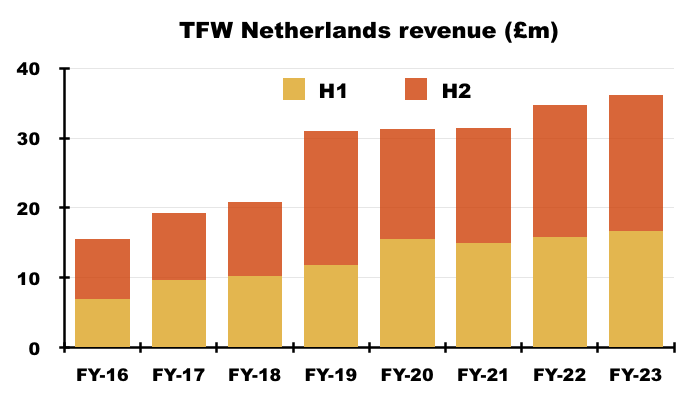

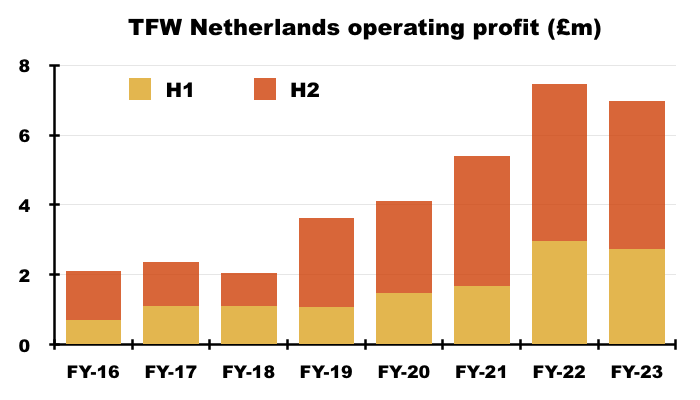

Netherlands

- TFW’s Dutch businesses — Lightronics and Famostar — represent a quarter of group profit.

- Lightronics manufactures mostly street lighting and was acquired during FY 2015 for an initial £8.3m that included a £1.9m debt repayment.

- Famostar manufactures mostly emergency lighting and was acquired during FY 2018 for an initial £6.3m:

- A £15m earn-out payment during FY 2022 took the total Dutch acquisition cost to £30m.

- Both Lightronics and Famostar appear to have performed well within TFW.

- Aggregate Lightronics/Famostar revenue for this FY was £36m versus less than a combined £18m at the time of their purchases.

- Aggregate Lightronics/Famostar operating profit for this FY was £7.2m versus a combined £2.3m at the time of their purchases.

- The Dutch businesses sadly did not deliver a fantastic FY.

- FY Dutch revenue increased 4% to £36m, but FY Dutch profit (before acquisition adjustments) fell 8% to £7.2m:

(Famostar acquired during H1 2018 but reported within Netherlands from H1 2020)

- Mind you, Dutch profit of £7.2m from a total £30m Dutch investment still generated TFW a very satisfactory 24% (or possibly more) pre-tax return.

- Higher supply costs at Lightronics were blamed for this FY’s Dutch profit shortfall, although actions have been taken:

“The main challenge during the year has been managing increases to supply chain costs. Some progress was made both in improving selling prices and reducing costs, but there is work to do. The commercial organisation continues to develop under the leadership of Lightronics’ new commercial director.

Margins improved in the second half of the year; Lightronics expects this to continue into the new financial year, following some positive results on purchase price negotiations in the supply chain. The business starts the new year with a solid order book, with a clear target of improving operating returns in 2023/24.”

- The Dutch operating margin (before acquisition adjustments) was still an appealing 20% for this FY, albeit lower than the 23% enjoyed during the comparable FY and the 22% for FY 2021.

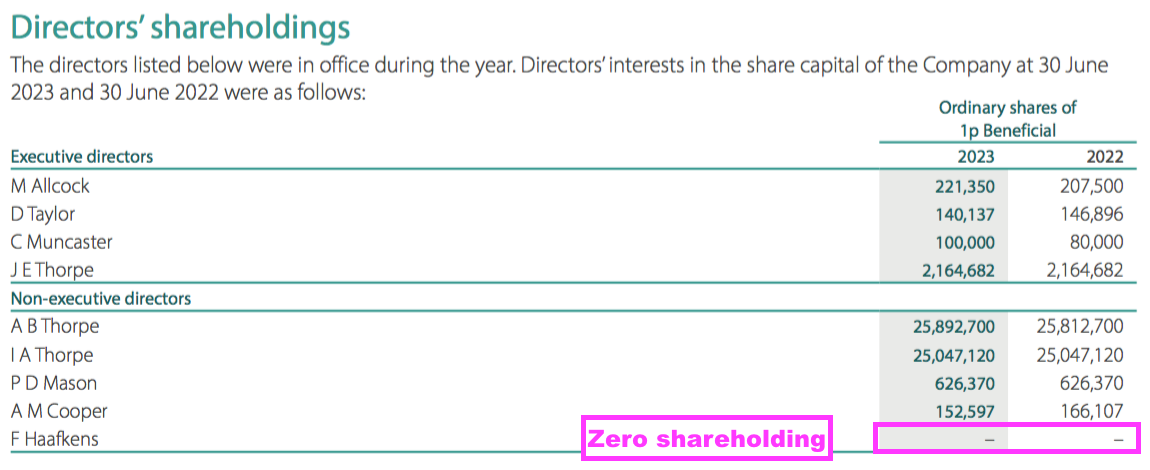

- TFW commendably widened its boardroom talent during October 2022 after appointing Frans Haafkens as the group’s “first recognised independent” non-executive:

- Mr Haafkens has worked with TFW since TFW bought Lightronics from his private-equity group during FY 2015.

- Mr Haafkens’ investment firm co-purchased Famostar with TFW during FY 2018, and bought a majority stake in Ratio Electric a year before TFW bought a 50% stake during December 2021 (see Ratio Electric).

- I trust Mr Haafkens’ “hands-on” private-equity approach can assist TFW with further acquisitions… although he has yet to buy any TFW shares:

- TFW’s board may now have room for extra non-execs. Two non-execs have retired so far during FY 2024, leaving only Mr Haafkens and two Thorpe family members as non-execs at present.

- A second “recognised independent” non-exec with European lighting experience could be the ideal appointment to complement a board dominated by Thorpe family members and veteran UK employees.

Zemper

- Encouraged perhaps by the success of the Lightronics and Famostar acquisitions, TFW purchased Spanish emergency-lighting group Zemper during October 2021:

- TFW spent an initial £19.9m to buy a 63% share that included cash of £5.3m. A further £5.3m was spent during September 2022 to purchase another 13.5%.

- This FY forecast the remaining 23.5% would be acquired for €12.6m/£10.9m:

“Included within other payables are commitment to purchase the remaining outstanding shares (redemption liability and contingent consideration) in Electrozemper S.A. of €12,623,000 (£10,853,000) and Lumen Intelligence Holding GmbH of €7,508,000 (£6,455,000).“

- But the comparable FY anticipated the remaining 23.5% would be acquired for €13.9m/£12.0m:

“Included within other payables is a commitment to purchase the outstanding shares (redemption liability and contingent consideration) in Electrozemper S.A. of €20,046,000 (£17,248,000). Of this amount €6,123,000 (£5,268,000) is included in current liabilities and €13,923,000 (£11,980,000) in non-current liabilities.”

- I believe the €1.3m/£1.1m difference reflects an extra payment for Zemper during H2 to take this FY’s follow-up payment to £6.4m:

- TFW said Zemper recorded a flat FY performance:

“Zemper’s profit contribution to the Group in 2022/23 was marginally lower than forecast, with orders down in the first half year; however, various new products and marketing supported growth in the second half to recover the full year’s numbers to be in line with the prior year’s numbers.“

- TFW added Zemper “synergies” ought to emerge during FY 2024:

“Projects include in-sourcing of troublesome plastic components, standardisation of product offerings across multiple territories, and continual development of shared product ideas. These synergies take time to implement, but the Group expects to see some benefit later in the new financial year.”

- The initial £19.9m payment plus the follow-up £6.4m payment plus the forecast £10.9m payment gives a £37.2m total anticipated payment for Zemper.

- A £37.2m total purchase price versus this FY’s £29.8m group operating profit (before acquisition adjustments) makes Zemper a very significant purchase.

- Zemper produced a £4.2m Ebitda for this FY, which values Zemper at nearly 9 times Ebitda based upon a £37.2m total purchase price:

- Nearly 9 times Ebitda is higher than my estimated sub-5 times multiple paid for SchahlLED and what is now sub-4 times paid for Lightronics/Famostar.

- Zemper’s higher valuation may reflect the subsidiary’s high-spec factory…

“Zemper’s facility in Spain is a credit to its founding family’s professionalism. The company is very self-sufficient, with ownership of all its intellectual property, and with its own laboratory test facilities and state-of-the-art manufacturing equipment.”

- …and/or the lengthy 15-year longevity of acquired ‘customer relationships’ (point 31), which suggests loyal clientele and reliable orders.

- For comparison, SchahlLED’s ‘customer relationships’ have a useful life of six years.

- Zemper’s higher valuation could also reflect intriguing commentary about future “premium connected technology“:

“[S]ome significant technological projects are underway to harness Zemper’s design, technical and manufacturing know- how. These projects will support the Group’s electronic operations and its aspirations for premium connected technology in the emergency lighting sector.”

- Zemper may well be involved with a SmartScan equivalent for emergency lighting.

- I would like to think the aforementioned “synergies” will soon improve Zemper’s 14% operating margin (before acquisition adjustments), and enlarge the subsidiary to represent more than the present c10% of the wider TFW group.

Ratio Electric

- TFW acquired 50% of Ratio Electric during December 2021 for £5.8m, with a loan note issued for £0.9m “to help fund the development of [the] business”.

- Ratio is headquartered within the Netherlands and develops electric-vehicle charging systems:

- This FY revealed the loan note had increased to £1.3m, with a further £1.3m loan note issued to Ratio Electric’s UK operation:

“Pursuant to the investment in Ratio Holding B.V., the Group has issued loan notes of €1,500,000 (£1,290,000) (2022: €1,000,000 (£860,000)) to help fund the development of this business. With accrued interest, the balance at 30 June 2023 is €1,566,000 (£1,347,000) (2022: €1,012,000 (£872,000)). During the current year, the Group has issued loan notes of £1,250,000 to Ratio EV Limited, a wholly-owned subsidiary of Ratio Holding B.V., to help fund the development of its business. With accrued interest, the balance at 30 June 2023 is £1,266,000. “

- Issuing extra loan notes does not sound promising, and sure enough Ratio recorded a £1m loss for this FY:

“In the year to 30 June 2023, the joint venture, Ratio Holdings B.V. generated a loss after tax of €1,199,000 (£1,041,000) (2022: profit after tax of €683,000 (£588,000)).

The Group has recognised its 50% share of loss of €599,000 (£520,000) (2022: profit of €342,000 (£290,000)) in the Income Statement, less costs in the parent company of £nil (2022: £62,000).”

- This line was somewhat concerning:

“No further analysis of the joint ventures has been provided as the activities are not considered material to the Group.”

- The comparable FY had presented a simple income statement for Ratio…

- …despite the joint venture’s £683k profit for that FY also not being material to the group.

- Electric-vehicle charging is a departure from TFW’s lighting speciality. At the time of the Ratio investment, TFW said:

“This is an exciting opportunity for the Group. FW Thorpe’s know-how in electrical engineering, manufacturing and lighting, combined with Ratio’s experience in electrical vehicle charging will allow the introduction of new products into the UK market as well as supporting growth in Ratio’s existing markets.

We see similarities in technology and engineering skills, giving the Group the opportunity to diversify into new areas of engineering with high growth potential.”

- Ratio’s “high growth potential” may have come with high cost potential to remain competitive. This FY suggested Ratio required greater innovation:

“In the Netherlands, at the Ratio HQ, operations have been adjusting to the fast moving EV marketplace, and investments in smart charging technology and connectivity have dented returns.”

- This FY witnessed Ratio’s UK progress restricted by capacity issues:

“Availability of the new EV charging pillar has been limited due to production capacity restraints, but Ratio hopes to be able to better satisfy the Group’s sales teams in coming months, who are chomping at the bit to get going.“

- The Ratio equity investment is carried presently at £5.6m with the loan notes carried at £2.6m.

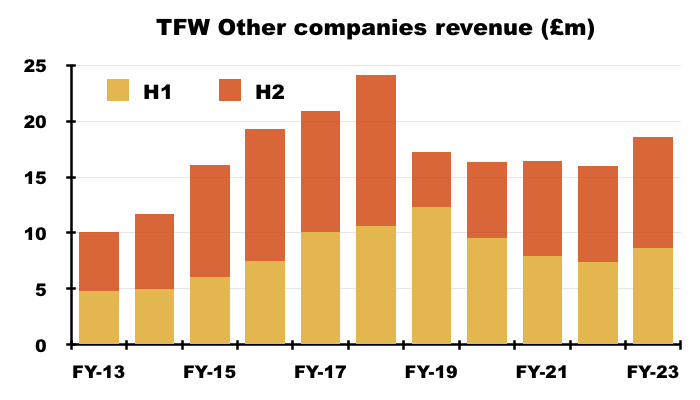

Other companies

- TFW’s Other companies consist of:

- TRT Lighting, which supplies lighting for roads and tunnels, and earns revenue of approximately £10m;

- Philip Payne, Solite and Portland, which between them supply emergency lighting, cleanroom lighting and shop lighting to earn combined revenue of approximately £11m, and;

- A handful of overseas Thorlux offices.

- The best long-term performing Other subsidiary is TRT Lighting, which was established during FY 2012 and by FY 2016 had already become the largest Other subsidiary by revenue.

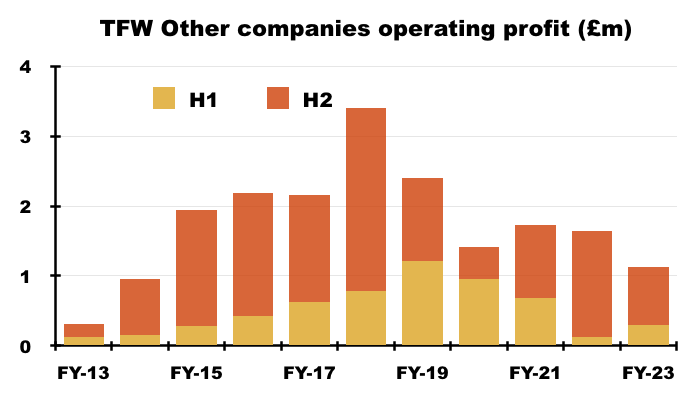

- But TRT’s recent progress has not been spectacular. The comparable FY admitted to a “marginally above break-even” performance and this FY acknowledged a thin 3% margin following personnel changes:

“TRT Lighting increased its profit but, at only a 3% profit-to-sales ratio, profit remains significantly below Group expectations and must improve. In recent months the TRT Board structure has been altered and strengthened, with a new operations director and new sales director, and the sales team has been refreshed”

- TRT’s low margin has been due to an absence of larger projects, which are expected to return for FY 2024:

“Street lighting projects contributed most of the revenues for this year. Tunnel projects were at lower levels, with only some smaller scale projects in the UK and Australia. Some larger projects have been secured and ordered for delivery in 2023/24; these higher margin projects will make a strong contribution to results for 2023/24.”

- Philip Payne and Solite put in positive revenue performances, while Portland lost ground as customers for Belisha beacons proved elusive.

- Other-subsidiary profit of only £1.1m on net revenue of £19.3m suggest the Other subsidiaries have struggled collectively with demand, costs and/or competition:

- I speculate Philip Payne, Solite, Portland and possibly TRT are kept on by TFW primarily because they supply products and services to the group’s larger operations:

Financials: balance sheet and cash flow

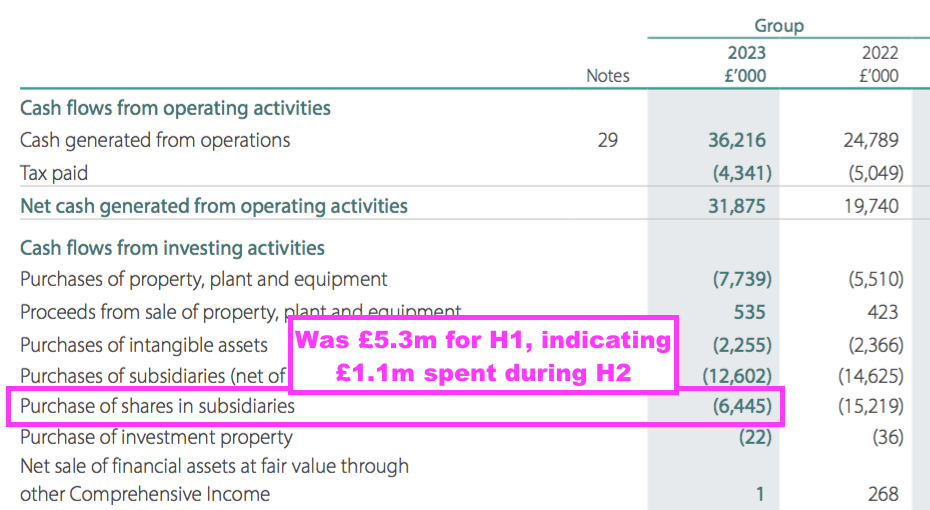

- TFW’s balance sheet remains flush with cash despite the payments for SchahlLED (£13m net of cash acquired) and Zemper (£6m).

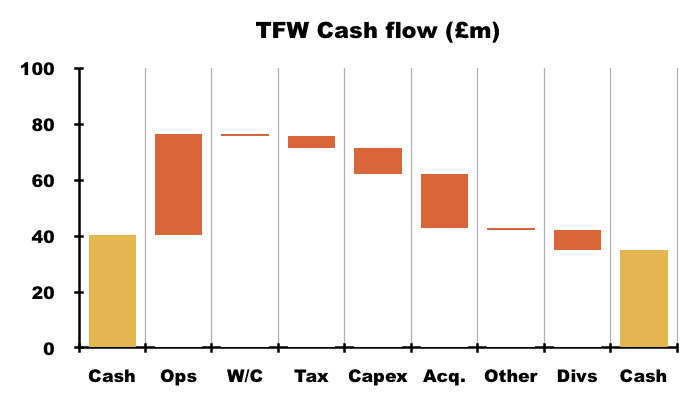

- Cash and short-term deposits ended this FY £6m lower at £35m after cash from operations of £36m invested only £1m into working capital, paid tax of £4m, funded net capex of £9m, spent £19m on acquisitions and distributed £7m as dividends:

- The £35m cash position is not troubled by significant borrowings. ‘Financial liabilities’ (mostly bank debt, factoring liabilities and government loans associated with SchahlLED and Zemper) were £3m.

- This FY answered a common question from “some shareholders” about the substantial net cash position:

“For many years some shareholders have questioned the rationale behind the Group holding large cash reserves. The Board chooses to maintain a large reserve as one never knows what is around the corner, as proven recently by the COVID lockdown. The Board remains prudent, with no plans to move away from this philosophy, and will not fund further growth unless it can do so from cash reserves.

- Amen.

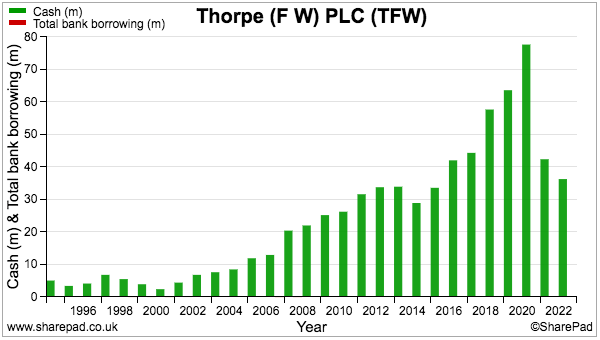

- TFW in fact has operated with net cash for at least the last 30 years:

- I dare say the conservative approach to cash reserves (and that illustrious dividend record) may be connected to the board’s 45%/£201m shareholding.

- TFW added:

“Although reserves have reduced with recent acquisitions activity and with stock control complexities, even with future earn-out provisions and commitments the Board remains confident that the current £35.0m at the year end, which remains well above its desirable minimum target, will more than suffice.”

- £35m will indeed suffice to cover the aforementioned £11m to clear the Zemper purchase and £6m to clear the SchahlLED purchase.

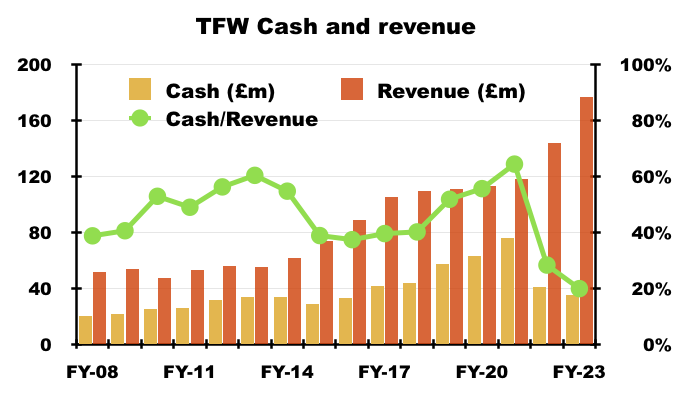

- Mind you, cash at £35m is equivalent to ‘only’ 20% of annual revenue — the lowest proportion since FY 2002 (15%):

- Bank interest amounted to only £236k or 0.6% on this FY’s average £38m cash position.

- However, £236k/0.6% did advance on the comparable FY’s £49k/0.1% and TFW did suggest a further improvement for FY 2024:

“[T]he recent upturn in interest rates have seen returns on our significant cash holding improve in the last quarter of the year.“

- Companies blessed with significant ‘surplus’ cash should now be earning notable interest.

- As a minimum, NatWest for example offers an instant-access business account paying between 1.46% and 1.92% AER (variable), which would pay a useful £650k interest on this FY’s £35m.

- TFW’s ability to fund material acquisition payments while maintaining a significant cash surplus reflects the group’s very respectable cash generation.

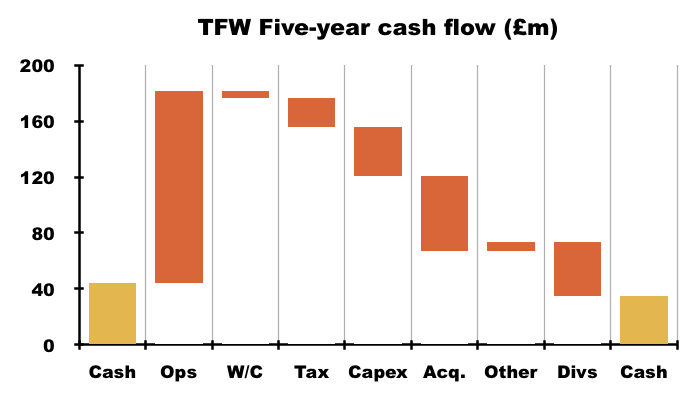

- For example, during the five years to this FY, cash and short-term deposits declined just £9m to £35m after cash from operations of £138m invested only £5m into working capital, paid tax of £21m, funded net capex of £35m, spent £54m on acquisitions and distributed £39m as dividends:

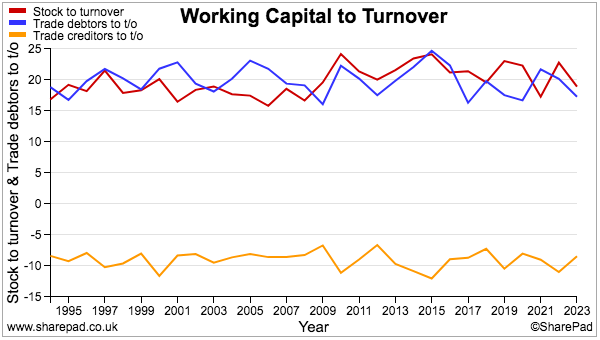

- TFW’s working-capital management has been particularly impressive.

- Despite the group growing eight-fold during the last three decades, stock, trade debtors and trade creditors as a proportion of revenue have been remarkably consistent:

- This FY confirmed stock levels were being “actively managed“:

“There are targets around the Group to reduce stock – of components, in particular. The easing of the recent supply shortage situation has now inevitably created an overstock in most Group companies and elsewhere throughout the extensive supply chain. Stock levels are being actively managed, in particular to ensure agility in Group businesses and to reduce possible obsolescence. Whilst stock increased last year from £32.8m to £33.4m, the number reduced from an interim high of £37.9m and will fall further.”

- TFW does carry the risk of stock becoming obsolete. This FY noted:

“The value of the inventory provision is £5,122,000 (2022: £4,449,000) for the Group and £2,785,000 (2022: £2,477,000) for the Company.”

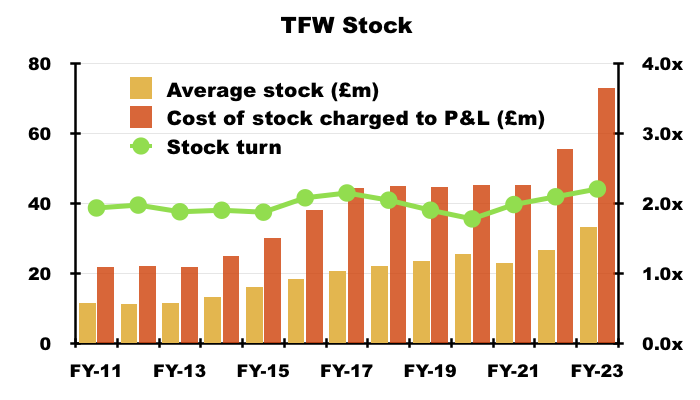

- A £5m inventory provision equates to 13% of this FY’s stock value of £33m. The 13% is commensurate to previous FYs, but the figures imply £5 of every £38 invested in stock is written off.

- The cost of inventories expensed against profit for this FY was £73m, which versus average stock held during the year of £33m implied stock was kept in the warehouse for almost six months before sale.

- Such stock turn at 2.2x (£73m/£33m) matches TFW’s longer-term pattern:

- Capital expenditure seems adequately expensed through the income statement:

| Year to 30 June | 2019 | 2020 | 2021 | 2022 | 2023 |

| Depreciation and amortisation (£k) | 4,399 | 5,037 | 4,985 | 5,481 | 6,194 |

| Cash capital expenditure (£k) | (5,473) | (8,495) | (4,398) | (7,453) | (9,459) |

(Depreciation and amortisation for property/plant/equipment, capitalised development and software only)

- The £9m difference between five-year net capital expenditure of £35m and five-year depreciation and amortisation of £26m can be explained by £11m spent on freehold properties. Total freeholds are carried at a net £22m.

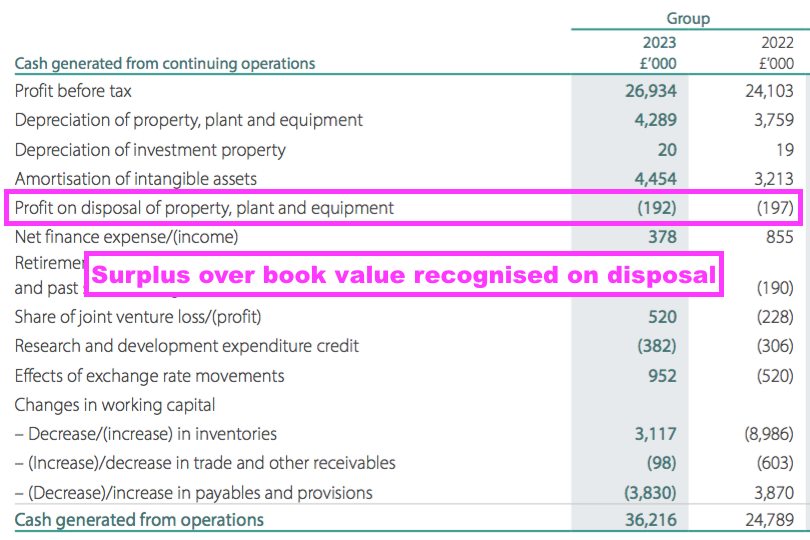

- TFW’s cash flow includes consistent ‘profit on disposal of property, plant and equipment’ entries:

- These entries suggest a conservative depreciation policy, whereby equipment is written down on the balance sheet to valuations below the eventual disposal proceeds.

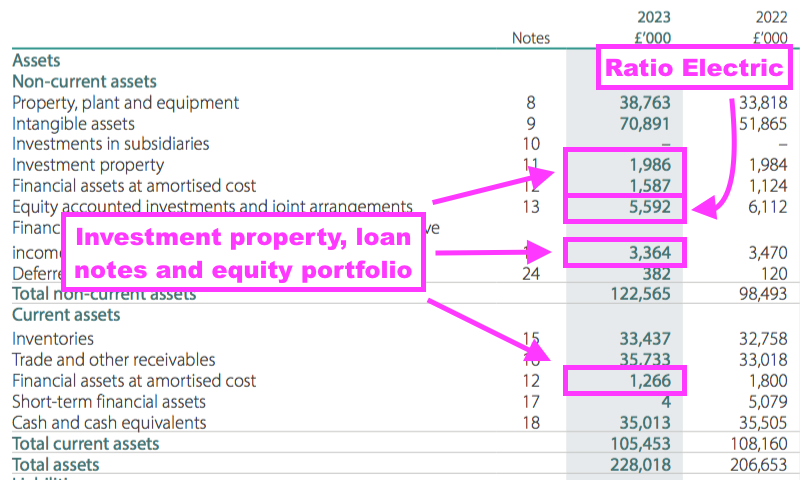

- The accounts also include investment property of £2m, loan notes of £3m, an equity portfolio of £3m as well as the £6m Ratio Electric investment:

- Calculating TFW’s return on capital (and similar ratios) is fraught with nuances given the significant (and low-earning) cash position, the amortisation of acquired intangibles, the array of non-operational investments and the forecast payments to acquire the rest of SchahlLED and Zemper.

- My best guess at total invested capital is

- Property, plant and equipment of £38m, plus;

- Intangibles of £71m, plus;

- Cumulative acquisition adjustments of £3m, plus;

- Working capital of £20m, plus;

- Forecast SchahlLED and Zemper payments of £17m…

- …giving approximately £150m.

- This FY’s operating profit before acquisition adjustments of almost £30m gives an encouraging pre-tax return on invested capital of 20%.

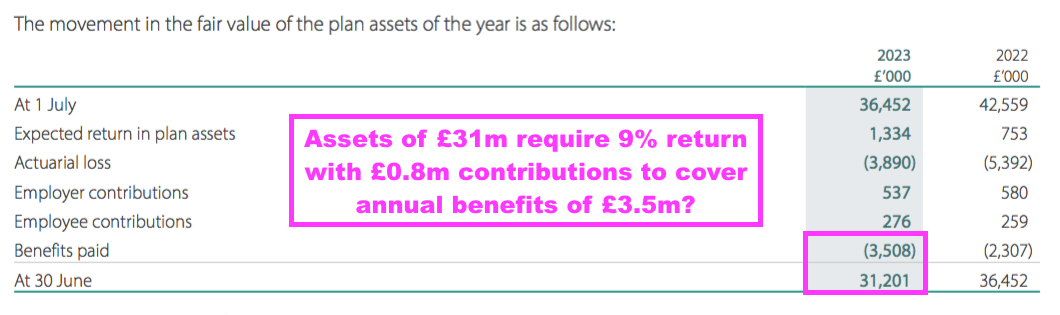

Financials: pension scheme and employees

- TFW operates a “hybrid” defined-benefit/defined-contribution pension scheme:

“The Group operates a funded hybrid pension scheme for employees in the UK….

…

The contributions of the pure defined contribution, the defined benefit underpin and pure defined benefit elements are paid into one pension scheme, where the contributions and assets are segregated and ring-fenced from each other.”

- The scheme’s hybrid set-up means shareholders can’t really be sure about the funding risks of the defined-benefit element.

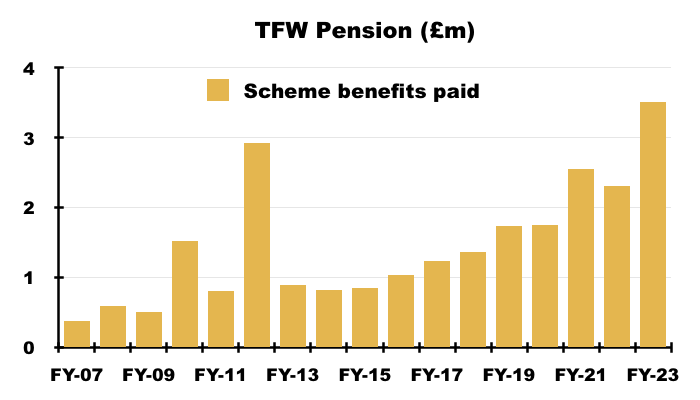

- Scheme benefits paid during this FY jumped by £1.2m to £3.5m:

- Versus scheme assets of £31m, paying benefits of £3.5m a year might normally risk permanent asset erosion for a defined-benefit scheme.

- But the scheme’s assets and benefits include defined-contribution pensions, for which the scheme member — not TFW — takes the investment risk.

- As such, shareholders are left to guess whether the scheme’s assets of £31m remain sufficient to fund the obligations for the defined-benefit members.

- TFW’s pension commentary was very limited:

“The latest triennial actuarial valuation was completed as at 30 June 2021. This valuation showed that the pension scheme position remains in surplus and a funding level for the future has been agreed between the trustees of the scheme and the directors of the Company. The directors consider it unlikely that any changes to the present funding levels will have any significant effect on the strength of the Company’s statement of financial position.”

- Although the scheme’s benefit payments can fluctuate from year to year, the general trend is up:

- This FY suggested the group’s scheme contributions would not be increased for FY 2024:

“As a result of the most recent valuation, and in light of the non-recognition of the pension scheme surplus, the recovery plan liability of £189,000 (2022: £189,000) is included in other payables.

…

The Group expects to pay £364,000 contributions (2022: £361,000) into the pension scheme during the forthcoming year.“

- The scheme’s next triennial funding review will be calculated as at 30 June 2024. The resultant contribution recommendation will provide shareholders the best insight into the scheme’s financial requirements.

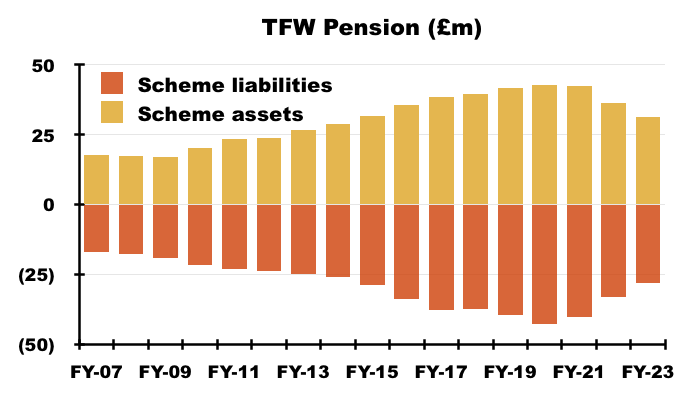

- For some perspective, TFW and its employees have contributed an aggregate £21m into their hybrid scheme since FY 2007… yet the scheme’s assets have advanced by £17m during the same time while the (defined-benefit) liabilities just seem to mirror the progress of the assets:

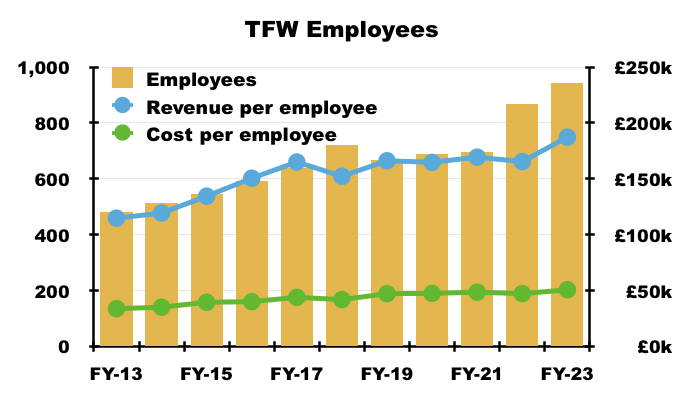

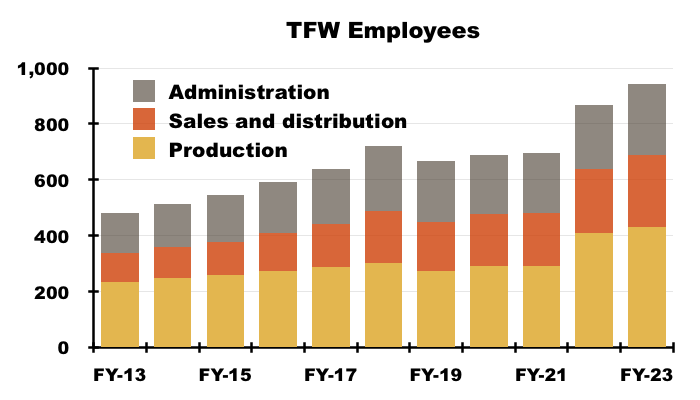

- TFW’s employee productivity continues to improve.

- Revenue per employee for this FY reached a new £187k high:

- The cost per employee advanced by £4k to £51k, but employee costs were commendably kept to 27.1% of revenue — the lowest since FY 2016 (26.7%).

- TFW’s improving productivity may be due to employing a greater proportion of revenue-earning workers.

- Since FY 2013, the headcount undertaking a sales and distribution role has increased from 22% to 27% of the workforce, while the headcount undertaking an administration role has declined from 30% to 27%:

- Keeping employee costs at 27% of revenue did not help TFW’s overall margin improve.

- H2 operating profit as a proportion of revenue was 18% to give an FY margin of 16%, or 17% before acquisition adjustments. The comparable FY margin before acquisition adjustments was 18%:

- Although a 17% group margin remains healthy, TFW did enjoy an 18%-plus group margin for many years up to FY 2016. A degree of competitive abrasion may have since occurred.

Valuation

- Outlook comments within this FY statement were muted:

“As a whole, the outlook from the sales teams is positive. At the start of this new financial year, orders are slightly lower than in the same time period last year, and there is some evidence of projects slowing. Costs are under control and some margin improvements have been made, which will provide an improved return on sales. Revenues, however, are expected to see slower growth than in the recent few years. “

- November’s AGM statement reiterated the subdued prospects:

“Since the beginning of the new financial year, orders and revenue are marginally ahead of the same period last year ‐ there being some ups and downs across the Group. We expect half‐year results to be similar to last year.

The sales teams remain positive, the pipeline is good but projects seem a little slower to materialise than in past years.

New product development remains a high priority and various exciting product innovations are under development.

The long‐term picture is always more challenging to determine, however, our geographical and sector diversity combined with our energy saving solutions present opportunities to target profitable growth.”

- A twelve-month contribution from SchahLED would have delivered FY revenue of £181m and an FY operating profit before acquisition adjustments of at least £30m.

- Applying the 25% UK tax rate to £30m gives earnings of £22.5m or approximately 19p per share.

- My calculations could be fine-tuned further for the:

- Net cash (£32m);

- Forecast earn-outs (£17m);

- The Ratio Electric investment, loan notes, investment property and equity portfolio (£14m), and;

- Potential operating improvements at Zemper, TRT Lighting and the other Other subsidiaries…

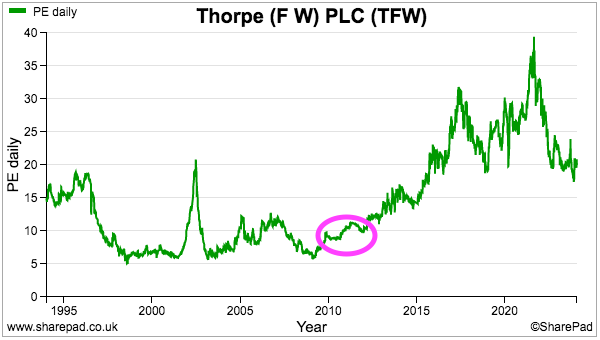

- …but such adjustments will not make a huge difference to the £446m market cap that my guesswork says is supported by a 20x multiple.

- My decision to purchase TFW between 2010 and 2012 was made much easier because the shares were then valued at a more modest c10x P/E multiple:

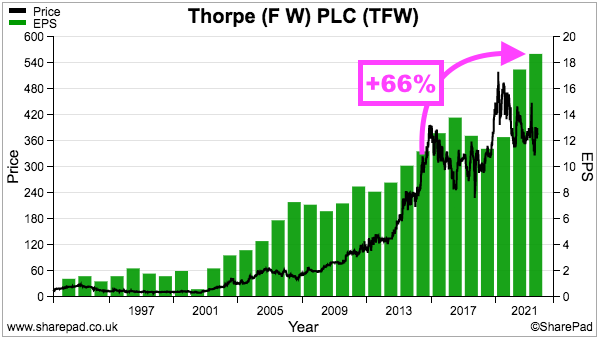

- Despite reported earnings advancing 66% between FY 2016 and this FY, the shares at 375p have traded sideways throughout the same period:

- Perhaps today’s buyers are (still) willing to pay a healthy 20x multiple because of TFW’s:

- Long-time operational resilience as demonstrated by 21 years of consecutive dividend increases;

- Appealing returns on invested capital, driven in part by acquisitions purchased on low multiples (e.g. Lightronics and Famostar);

- Ongoing growth opportunities through product innovation (e.g. an emergency-lighting SmartScan equivalent) and cross-selling into new territories (e.g. Europe through overseas subsidiaries);

- Prestigious contracts such as Elizabeth Tower showcasing first-class business/product credibility;

- Tip-top environmental credentials, as evidenced by more than 20 pages within the 2023 annual report devoted to ‘sustainability’, and;

- Order books supported by customer concerns about elevated energy costs.

- On that last point, a SharePad search through the RNS for ‘LED lighting’ continues to show plenty of FTSE 350 companies that may well be (or become) TFW customers:

- The bear case beyond general economic challenges include:

- Zemper, SchahlLED, Ratio Electric and potential future acquisitions not performing as expected following significant purchase expenditure;

- Greater competition leading to higher stock obsolescence and a lid being kept on the group margin;

- The UK-centric boardroom becoming tested by overseas operations now representing almost 50% of revenue, and;

- Further share-price stagnation as near-term growth moderates to a pedestrian pace.

- For now at least, shareholders may have to be patient for Zemper and Ratio Electric to prove themselves as wonderful investments.

- I would also hope TFW allows Zemper and SchahLED to properly bed in before embarking on another substantial acquisition.

- As shareholders await what might be a quiet FY 2024, the 6.46p per share ordinary dividend supplies a modest 1.7% income at 375p.

Maynard Paton

Thanks very much for your latest analysis on F W Thorpe. I certainly agree with your comments that businesses with substantial cash should now be earning notable interest. With my comparatively minor sums of cash I can currently get 4.66% interest in an instant access account via the Hargreaves Lansdown Active Savings platform, if Thorpe could get anywhere near this figure for their cash it would make a worthwhile difference. I wonder if their banking arrangements restrict their ability to invest their cash elsewhere as the interest rates they report appear derisory.

Thanks John. My experience with HL Active Savings is the money takes c2 days from withdrawal request to land in my current account, so not quite true instant access but the spread of rates are good. I am not entirely sure how exactly quoted companies go about their banking and I dare say there is more to consider than for personal banking, but the NatWest account I highlighted in the blog post above seems quite straightforward and pays close to 2% on more than £10m. Aldermore for example pays 3.25% easy access but the account limit is £1m. My conversation with CLIG shareholder George Karpus touched upon how inadequate UK companies are managing their cash reserves for interest, and that is becoming apparent now rates have increased to normal levels.

Maynard

FW Thorpe (TFW)

Publication of 2023 annual report

Here are the points of interest beyond those noted in the blog post above:

——————————————————————————————————————

1) WHO WE ARE

The same text as last year, but the phrase “each company works autonomously“…

“We specialise in designing and manufacturing professional lighting systems. We currently employ over 900 people and although each company works autonomously, our skills and markets are complementary.”

…does suggest a degree of decentralisation within the group. I wonder if TFW has ambitions to become the Halma of the commercial-lighting industry. This great speech from former Halma boss David Barber explains how Halma’s acquisition strategy — and allowing the subsidiaries to operate independently with a minimal head office — worked wonders for shareholders.

2) OUR INVESTMENT CASE

The same text as last year, except for additional CAGR information:

“• Consistent revenue growth – Compound Annual Growth Rate (CAGR) across the last five years of 10.0%, ten years 12.3%, 15 years 8.5%.”

The investment case remains

• ‘Product innovation’;

• ‘Our focus on sustainability’;

• ‘Means we are positioned for sustainable long-term growth’, and;

• ‘Financial performance’

3) OUR APPROACH TO SUSTAINABILITY

TFW’s timeline within this section reiterates the group introduced its first energy-saving product 30 years ago:

“1994: First energy saving products introduced, controlling lighting and reducing energy consumption“.

The commentary is tweaked this year to confirm TFW is “independently verified” as carbon neutral. The group’s net-zero target was previously “by 2050” but this report now confirms an “aim to achieve [net zero] by 2040“.

4) WHAT WE DO

The same text as last year, and still with an emphasis on “high-quality” and “excellence“:

“Focus on high-quality products and good leadership in technology ”

“Continue to grow the customer base for Group companies”

“Focus on manufacturing excellence”

”Continue to develop high-quality people”

5) OUR BUSINESS

This year’s report includes an introduction to SchahlLED:

“SchahlLED Lighting is a turnkey provider of intelligent LED solutions for the industrial and logistics sectors with more than 50 years of lighting and 20 years of LED experience.The company is based in Unterschleißheim near Munich and has sales offices in Cologne and Weyhe close to Bremen. As both manufacturer and full-service provider, SchahlLED plans lighting concepts and supplies intelligent LED lighting systems.”

SchahlLED’s key products are:

“• Recessed, surface and suspended luminaires

• Emergency lighting systems

• Hazardous area lighting

• High and low bay luminaires

• Lighting controls

• Exterior lighting”

SchahlLED’s market sectors are: Industrial, Logistics and Manufacturing.

6) MARKETPLACE

This year’s report replaces the Q&A from last year with standard commentary. Snippets include fewer product redesigns…

“There has been less focus on redesign this year, allowing our engineering teams to focus on product development. We continue to differentiate ourselves with product and system innovation, combined with our ability to service our markets through the life cycle of a project.”

…and competitors being able to raise prices:

“Across our domestic and international markets we face competition from listed multinationals as well as solid private businesses. Where information is available, we have seen improved financial performance of our main competitors perhaps buoyed by the ability to increase sales prices in the current economic climate.”

7) BUSINESS MODEL

A reminder of TFW’s “peace of mind” business model:

“Customers come to us for peace of mind. They want the correct technical solution, professional service, sustainability of products/services and the ability to provide support during a product’s warrantable life and beyond.

Our business model is focused on the needs of customers and the marketplace, with a robust capital structure that underpins our ability to deliver sustainable growth, innovative products and excellent customer service.”

No text changes for this year, but worth repeating TFW receives its orders through the following specifications: “renovations, new build, energy saving, compliance, technology adoption“.

Note also TFW’s general product features:

“• Energy efficiency

• Low maintenance

• Rapid installation

• Longevity of product

• Low total cost of ownership”

I always translate “Low total cost of ownership” to mean a higher up-front cost but low/no ongoing service expenses. Little ongoing service revenue could make revenue more unpredictable for shareholders, but TFW’s long-term record suggests customers are happy, which in turn makes it hard to argue against the model. Text elsewhere in the report says product warranties last between 5 and 10 years.

8) STRATEGY

No changes to the overview text, and I still like how TFW places shareholders ahead of employees and customers (not every quoted company lists the three in the same order!):

“The Group management team is passionate about developing the business for the benefit of the shareholders, employees and customers.”

Important parts of the strategy include:

“ • FW Thorpe has been built on product innovation – design and product development is fundamental”

“ • The Group is product led. This enables us to maintain competitive advantage with market-leading products,”

“ • Control of the manufacturing processes is of utmost importance – key processes are kept in-house with targeted investment in new machinery as required.”

“ • Family principles and how we treat our people is fundamental to our success.”

Within the supplementary strategy text, a few tweaks.

a) A new line about EVs:

“Electric vehicle charging and road safety products now to be marketed by a number of Group companies”

b) Now aiming to sell Thorlux products into France (via Zemper):

“Targeted approach in the Netherlands and France with Thorlux industrial product and controls portfolio”

c) Updates on completed projects and a new Zemper facility:

“• Famostar facility extension project successfully completed

• Completed solar investment at Thorlux

• Expanded injection moulding facility at Zemper Spain to support the manufacture of select components for the Group“

d) Re-emphasising the importance of employing “high-quality people“:

“One of our main sources of competitive advantage, it is imperative we continually develop and retain talent within the business.”

On the people front, new bullet points include “Training and development” and “Inter-company collaboration teams to develop a broader understanding of the whole business.”

9) STRATEGY IN ACTION

a) An impressive case study of illuminating the Big Ben clock faces.

Text says TFW was approached about the work during 2016 for what was a five-year refurbishment programme… which just goes to show some project work can take a long time to complete. I note usage of the SmartScan system resulted in “less cabling and therefore less damage to the historic building fabric“.

b) Some introductory text about SchahlLED, including “In 2019, financial investor Active Capital Company acquired a majority stake in SchahlLED to support the company in its strategic growth plan.“.

I am always a little nervous when quoted companies buy from investors (the latter may ‘plump up’ their businesses specifically for sale). But TFW did purchase its Dutch businesses from private equity and they have worked out well with the private-equity seller actually now represented on the main board.

The SchahlLED investor was invested for less than four years, oversaw two smaller acquisitions by SchahlLED, and announced its disposal to TFW here.

This annual report says “SchahlLED and Thorlux have worked together since 2019, distributing SmartScan products primarily into the German market.“, so presumably TFW knew SchahlLED well before the purchase.

TFW’s original SchahlLED purchase announcement did not mention the identities of the owners.

c) I do like this — TFW encounters a supply problem and casually decides to build a new factory to resolve the issue:

“To address the challenges faced by several Group companies in sourcing plastic moulded components externally, a strategic decision was taken to leverage the expertise and production facilities of Zemper. However, Zemper’s plant in Almagro had insufficient production capacity and space to meet the increased demand. The most viable solution was to construct a new factory adjacent to Zemper’s main facility in Ciudad Real, to produce all Zemper’s plastic components.”

A new warehouse has been built for Dutch subsidiary Famostar, too.

10) KEY PERFORMANCE INDICATORS

The same six KPIs as last year, with C02 emissions (down 13% on a revised calculation) and renewable energy usage (up a surprisingly low 1%) being notable ‘green’ measures.

11) OPERATIONAL PERFORMANCE

A few snippets here:

a) Zemper profits were slightly below those of the comparable year, but this text nonetheless claimed the subsidiary “performed well“:

“Zemper performed well in its first full financial year as part of the Group; with strong performance in France and an improved second half performance in Spain, the company delivered results in line with expectations.”

I hope the better H2 Spanish performance can be maintained to justify what could be a significant £37m total eventual payment for Zemper. I note Zemper traded strongly in France, which may prioritise that particular market for TFW’s next acquisition.

b) An extra cost-of-living payment for staff:

“Employee costs continued to increase, driven by wage increases; this will continue for the coming months until headline inflation rates come under control. Within the Group, companies take pride in paying above minimum wage levels. This year, an additional special cost-of-living payment was also made in December across the Group, targeted at those suffering hardship from increased domestic bills.”

c) TFW has lifted its prices in a kind manner, but some clients remain conscious of costs despite the high-quality products:

“Selling prices have been increased where possible, in a fair and responsible manner, to combat inflationary pressures, but negotiating these increases through to the order book has been more successful with some companies than others”

d) TFW confirms a trio of new recruits among its smaller UK ‘Other’ businesses:

Philip Payne: “New Philip Payne managing director Nick Revell is welcomed to the Group. Nick is charged with continuing the many years of stability and profitable growth delivered under the stewardship of David Taylor, who retired at the end of the 2022/23 financial year. The Group looks forward to Nick moving the business forward from solid foundations built by David and the team over many years”

Portland Lighting: “Traditional outdoor sign lighting sales were down, and the development of a new selection of products to target the road and traffic sign market has yet to deliver the growth planned. However, with a new dedicated person now leading the road safety division, there were some promising signs as the Group closed the financial year and started 2023/24.”

TRT Lighting” “The new operational leader at TRT has made a positive impact. Service levels are good, and the business continues to improve its ability to respond to peaks in customer demand.”

Collectively, these smaller UK ‘Other’ businesses have experienced very mixed fortunes over time and are gradually making less and less impact on the group. I hope the new recruits can enhance their respective businesses, otherwise these businesses may prove a distraction to the main board that has obvious ambitions to expand overseas.

e) Confirmation that Zemper has greater facilities that should benefit other group subsidiaries:

“The [Zemper] business is deeper into the value chain than most Group companies: with its ability to injection mould its own plastic components and populate finished printed circuit boards; it also has its own robotic final assembly and testing process.There has been further investment in these facilities during the year, with the addition of injection moulding capacity that will support the Group as well as additional investment in surface mount machinery that will also facilitate synergy projects for the wider group. ”

12) PRODUCT SPOTLIGHT

I did not know TFW lights could last for more than 11 years of constant use:

“The principles of circularity aim to eliminate waste by keeping as much of the original product material in use for as long as possible, which is why the SkyCore family has been designed to provide a long and reliable life of at least 100,000 hours.”

For perspective, a Philips LED light I bought recently for domestic use has a usage lifetime of up to 15,000 hours.

13) SECTION 172

This text is unchanged from last year, but under ‘shareholders’ I see the bullet point “Trading updates at appropriate times” — I can’t recall TFW publishing a standalone trading update beyond its usual AGM statement!

The bullet point “Investor meetings and presentations, including company visits” sounds as if TFW undertakes conventional City roadshows (although presentation slides are not published on the website):

Pretty sure TFW is the only holding in my portfolio that engages with local politicians: “Engagement with local MPs and Chambers of Commerce”

14) SUSTAINABILITY

This report witnessed a step-change to TFW’s Sustainability section.

The prior year’s Sustainability section consisted of 11 pages, but this year’s Sustainability section ran to 24 pages that included a mammoth 14-page Task-Force on Climate-Related Financial Disclosures (TCFD) report.

This section is important to TFW; the group markets its products on their energy efficiency, and TFW’s operations ought to boast superb ‘green credentials’ to help champion environmental matters to customers.

a) Sustainability in action

Contains the same four areas of focus as the previous year (Products, Operations, Business Model and People), with the accompanying bullet points enhanced for this year.

This year TFW confirms its sustainability drive will spread to suppliers:

“Group companies are working with key suppliers to embed sustainable practices and remove single-use plastic from the supply chain”

But I note last year’s Operations bullet points “Ability for certain staff to work at home – reduced travel” and “Flexible working” have been removed. Everyone is seemingly back in the office.

Within the Business Model bullet points, I have noticed TFW’s customer-financing offer before: “Several Group companies offer financing models for customer projects.” This link reveals a third party takes on the funding risk.

I quite like the People bullet point indicating most of the workforce can achieve a bonus: “All employees are paid above the minimum wage rates and the majority are enrolled in some form of bonus scheme.”

b) Products

No major changes within the main People text, although the number of “mainline” suppliers (100) and “non-product” suppliers (500) are omitted this year.

c) Operations

A few changes to the Operations text:

Electricity is now almost all derived either from TFW’s solar panels or renewable sources:

“The Group has installed solar PV units on the roofs of most of its UK manufacturing facilities, as well as at Lightronics and Famostar in the Netherlands and Zemper in Spain. The units have the capability to deliver over 2 million kWh per annum, reducing the Group’s consumption from traditional electricity sources. All remaining significant electricity consumption is now derived from renewable sources.”

The sustainability drive reads as if money could be saved:

“With improved planning, the Group has been able to manage inventory, reduce excess, consolidate deliveries, and eliminate the purchase of unnecessary items – all of which will reduce the amount of supplier delivered waste.”

The proportion of ‘green’ company vehicles is now over 50% (was 47%)…

“To date, over 50% of company vehicles are either electric or hybrid.”

…although given TFW’s Ratio joint venture develops EV charging points, the proportion should really be moving faster to 100%.

15) TCFD

A whole new revamped TCFD section spanning 14 pages! A few snippets:

a) Overview

TFW introduces the ‘green’ measures as necessary to keep the group competitive:

“The Group commenced its sustainability programme in 2009 and recognises the need to continually invest in greener solutions for its factories, enhance component sourcing and management, foster circular design practices, and develop energy-efficient product offerings to maintain a leading position in the market.”

A warning that environmental-reporting matters are likely to become complicated:

“The Group will be modelling the likelihood and severity of potential impacts on its operations from flooding, storm patterns, precipitation, mean temperatures and sea level rise, to fully understand the threats and establish a mitigation strategy to safeguard the future of the business against climate change.”

b) Governance

Climate change will become a formal management matter:

“Sustainability is a standing agenda item at Board level and is discussed in every Board meeting. From the next reporting year, climate change will become a separate additional agenda item at the quarterly board meetings at each Group company.”

A group ESG committee might be formed:

“Next financial year the Group will consider establishing a formal ESG committee that will include representatives from the Board and key roles relevant to the topic.”

Options and bonuses might soon be linked to TCFD progress:

“The Group’s Board remuneration is currently not directly linked to climate/ sustainability, but any future share options granted will contain a specific performance condition around carbon reduction. FW Thorpe is currently reviewing incentives across the Group to consider a potential link to sustainability targets in 2023/24.”

And options are now linked to ESG matters (point 19)

c) Risk

I am not surprised a TCFD consultant has been hired:

“For a wider assessment of climate-related risks, FW Thorpe has procured an external consultant, to help it understand the risks and opportunities. The consultant will conduct a climate scenario analysis in the next reporting year, and provide the Group with a comprehensive, long-term picture of the potential impacts.”

The consultant will no doubt help TFW prepare the following:

“In the next financial year, the Group will conduct a climate scenario analysis. Three-time horizons will be used to provide the analysis with a suitable level of granularity and coverage. Best, worst and moderate case scenarios will be used to consider a broad range of eventualities.”

The following climate-related risks have been identified:

• Policy & Legal: Mandates on and regulation of products and services

• Markets: Increased cost of energy and materials

• Technology: Cost to transition to lower emissions technologies

• Reputation: Increased stakeholder concern

Also noted are Physical Risks. TFW says its HQ is not in great weather danger: ”A high-level assessment of the primary site in Redditch indicates that the likelihood of extreme weather events at the Redditch site is low.”

Interesting that high temperatures are already causing additional “business disruptions“:

“As a result of rising mean temperatures, the Group has experienced an increase in business disruptions. Rising mean temperatures will increase energy usage, leading to increased operating costs for the business and associated operational emissions.“

d) Opportunities

Climate opportunities will be assessed formally during FY 2024, but for now here is a useful snippet:

“Lighting accounts for 5% (2.5 billion tonnes) of global CO2 emissions. A global switch to energy efficient light emitting diode (LED) technology could save over 1,400 million tonnes of CO2 and avoid the construction of 1,250 power stations.”

e) Metrics and targets

Some bold targets:

“• Reduce absolute Scope 1 and 2 emissions by 42% by 2030, from a 2021 base year on a market- based approach.

• Reduce Scope 3 emissions per £m revenue 51.6% by 2030, from a 2021 base year.

• Reduce Scope 1, 2 and 3 emissions by 90% by 2040 from a 2021 base year, in line with reaching net-zero with a maximum of 10% of emissions being offset by this date.”

The emission charts are heading in the right direction:

TFW claims it is three years ahead of schedule with its 2040 net-zero target:

A very comprehensive “Carbon Balance Sheet“:

The major decline to ‘use of sold products’ is due to TFW customers using greater renewable energy for their lights. Scope 2 emissions are created through electricity purchased by TFW and have significantly reduced due in part through TFW’s solar panels.

16) PRINCIPAL RISKS AND UNCERTAINTIES

As befits the TCFD text, an extra ‘Sustainability & climate-related’ risk has been introduced this year to take the principal risks to 11.

The description of the new risk is:

“The Group has potential exposure to climate-related risk that could impact both its operations and the products it promotes.”

The mitigation of the new risk is as follows:

”• Sustainability targets are set each year for Group companies.

• Education of employees to further develop sustainability and climate-related understanding, evolving knowledge of the related risks.

• Targeted reduction of total GHG emissions, reducing the impact of its operations. ”

The possible impact of the new risk is deemed ‘Medium’.

Among the other 10 risks, ‘Price changes’ and ‘Cyber security’ have been increased from ‘Medium’ to ‘High’.

On ‘Cyber security’, two new bullet points state:

“ • Third party specialists engaged to provide enhanced support and advice

• Critical applications protected by multi-factor authentication and all connectivity is through the Virtual Private Network (VPN)”

The only other risks deemed ‘High’ are ‘Adverse economic conditions’ and ‘Business continuity’ (a significant level of revenue is generated from one site).

New mitigation points among the existing risks include:

“• Energy efficient products with shorter payback periods, and;

• Leveraging increasing footprint in Europe ”

The other principal risks remain legislation, competition, bad debts, currency movements, Brexit and Ukraine.

17) BOARD OF DIRECTORS

This report carries the bio of new non-exec Frans Haafkens:

“Frans holds a Master’s degree in Mechanical & Control Engineering and an MBA. He is Managing Partner at Dutch investment firm i4hi, a company having direct investments in manufacturing and technology businesses. He spent his formative years with McKinsey & Co. as well as working for a short period in the UK lighting industry.

Frans is a Dutch national who has worked with the Group in recent years supporting the continued success of its Dutch entities, Lightronics and Famostar, both as a consultant and an investor.”

Mr Haafkens is a welcome appointment, being the first person from outside the UK, outside the Thorpe family and outside the ranks of TFW employees to join TFW’s main board.

The board has now been slimmed down to six people. Mr Haafkens sits with three Thorpe family members (1 exec, 2 non-exec), the non-exec chairman and the chief exec/finance director. The recent amalgamation of the chief exec/finance director role is very odd and a matter I plan to investigate further.

18) CORPORATE GOVERNANCE

No changes to TFW’s compliance to the QCA’s 10 principles.

TFW is partially compliant on two principles.

This is the first:

”Maintain the Board as a well-functioning, balanced team led by the Chair:

• Total of eight directors, four executive directors and four non-executive directors.

• The non-executives are not considered fully independent. The Board considers that the non-executive directors are appropriate as they bring significant experience and expertise in the sector. In addition, as the directors retire on a three-year rotation, shareholders have a regular opportunity to ensure that the composition of the Board is in line with their interests.

• There is a Remuneration Committee but no Audit Committee, with matters that would normally be tabled at an Audit Committee put to the full Board.”

And this is the second:

“Evaluate Board performance based on clear and relevant objectives, seeking continuous improvement:

• There is no formal evaluation process; however, the Chairman is responsible for Board performance and accordingly actively encourages feedback on the content and function of board meetings.

• The composition and succession of the Board are subject to constant review, considering the ever-changing needs of the Group. In addition, the directors retire by rotation every three years giving shareholders the opportunity to ensure that the Board is aligned with their interests.”

I am not quite sure why TFW implies Mr Haafkens is not an independent non-exec. My blog post refers to TFW describing Mr Haafkens as the group’s “first recognised independent” non-exec. Maybe TFW has since reconsidered Mr Haafkens’ status given his business relation with TFW through Ratio Electric.

Directors seeking re-election every three years is very old-school and best practice today is to seek re-election every year. The lack of an audit committee has not hindered TFW delivering some fundamentally appealing accounts over time.

The absence of a formal board evaluation process has not really hindered TFW’s progress either, and I would like to think the appointment of Mr Haafkens shows some fresh thinking from what has seemed in the past somewhat of an insular board.

Among the other QCA bullet points, shareholder visits appear to be welcomed:

“Meetings are held with shareholders as required; this includes visits to our various company locations being organised and encouraged where possible”

19) REMUNERATION REPORT

No commentary changes to what remains a very terse remuneration report.

Basic pay for executives M Allcock (then exec chairman and joint-CEO), C Muncaster (then FD and joint-CEO) and JE Thorpe (Thorlux business development) increased a substantial 17%:

Interesting that Messrs Allcock and Muncaster enjoyed the same £235k basic pay during FY 2019, but Mr Muncaster’s pay has since advanced to £305k while Mr Allcock’s pay (despite being executive chairman and therefore the senior executive of the two) has advanced to only £274k.

Maybe the pay differential was a signal that Mr Muncaster was taking on more of the joint-CEO workload than Mr Allcock, and why Mr Muncaster has since become sole CEO as well as FD.

Pension “compensation” (which is excluded from the table above) may also explain the differential between Messrs Allcock and Muncaster:

“During the financial year the Company paid pension compensation to M Allcock of £180,953 (2022: £170,358), C Muncaster £51,770 (2022: £44,439), D Taylor £17,266 (2022: £19,546) and to J E Thorpe £23,150 (2022: £12,016).

Bonuses were chunky and exceeded the basic pay of all three executives. But I can live with such bonuses as the price to pay for TFW growing at an underlying c10% (as it did during the year). The bonus calculation remains suitably vague:

“The bonus is made up of two elements. The first element relates to the operating profit of the business unit for which the director has specific performance responsibilities. The second element relates to the operating profit of the Group as a whole.”

Note the bonuses can (unusually) be included in the calculation to determine a director’s pension:

“The defined benefit section aims to provide a maximum pension of two-thirds of pensionable salary at normal retirement date. M Allcock’s and D Taylor’s pensionable salary includes an average of the previous three years’ profit bonus. Defined contribution members contribute up to 5% of basic salary and the Company contributes up to 17%.”

That policy will help Mr Allcock following his retirement from July this year. Pension contributions can be steep at up to 17% of salary, a contribution level that Mr Muncaster enjoyed this year.

Don’t often see the type of table below with my shares:

Seems as if the higher earners within the group are having their pay lifted in line with the top executives, with the lower and middle earners slipping behind. The higher earners also seem to collect relatively higher bonuses, given their total remuneration (£93k) is much higher than their base salaries (£52k).

Director options amounted to 80,000, but these have all since been exercised.

Authority was granted during April 2024 to issue up to 2.1m options to the group’s workforce, and 1.925m options were awarded during May 2024. The executives were issued 400,000 options.

The main vesting target is to increase EPS by CPI +2%, which does not appear outrageously ambitious. Minor vesting targets are based on total shareholder return and ESG progress. Dilution is 1.6%, with almost 1.6m shares already held in treasury to be used to satisfy the option vesting. Options awarded by the previous scheme are now minimal and were based on pre-tax EPS growing at RPI +3% (point 37).

20) INDEPENDENT AUDITORS’ REPORT

a) Scope and materiality

Auditor PwC did less digging this year than last. Famostar was given a full-scope audit last year but had only “specified procedures performed” this year:

“An audit was conducted of the complete financial information of the three reporting units: Thorlux Lighting (the Company, located in the UK), Lightronics Participaties B.V. (located in the Netherlands), and TRT Lighting Limited (located in the UK).

• The audit work performed at these three reporting units (2022: four reporting units), together with specified procedures performed on Electrozemper S.A. (located in Spain), Famostar BV (located in Netherlands) and SchahlLED Lighting GmbH (located in Germany) and additional procedures performed on centralised functions at the Group level, including audit procedures over the consolidation, gave us the audit evidence we needed for our opinion on the Group financial statements as a whole.

• This provided coverage of 70% (2022: 91%) of profit before tax from the full scope audits.”

At least overall materiality was kept at the standard 5% of pre-tax profit (£1.375m).

b) Key audit matters

All changed for this report. Out go the matters from the previous year as the risk of them causing problems is now deemed “low“:

“Valuation of warranty provisions, Capitalisation of internal development costs, Impairment considerations over intercompany receivables and the accounting related to acquisitions of a subsidiary and a joint venture, which were key audit matters last year, are no longer included because of no issues being identified in prior years and the risk of material misstatement in these balances are low. As such, they are not considered to be of most significance in the current year.”

Key audit matters for this year are the pension scheme, SchahlLED intangibles and the Zemper earn-out:

“• Defined Benefit Pension Obligation valuation – Liability assumptions (group and parent)

• Valuation of intangible assets acquired in the acquisition of Lumen Intelligence Holding GmbH (group)

• Valuation of the future consideration payable for Electrozemper S.A. and Lumen Intelligence Holding GmbH (group and parent)”

All three entries in the accounts were deemed appropriate by PwC.

21) ACCOUNTING POLICIES

A few minor additions and changes.

a) New text: TFW discloses the profits attributable to the minority shareholders of Zemper, SchahlLED and other acquisitions as finance expenses (point 25) prior to becoming 100% TFW owned:

“The group does not recognise non-controlling interests in an acquired entity when there is a commitment and obligation to acquire the non-controlling interests of the acquired entity. The acquired entity is consolidated as if it is wholly owned by the Group since acquisition. Any profits attributable to non-controlling interests, if any, are treated as finance expense of the Group.”

Profits earned by minorities are typically identified at the earnings line.

b) Amended text: the amortisation rate for ‘Customer Relationships’ is now 7%-17% rather than simply 7%. Pretty sure the addition of 17% reflects the SchahlLED purchase.

c) New text: raw materials can be used to produce other raw materials:

“Raw materials include items that are both used in the production of finished goods and items used in the production of other raw material items”

d) New text: This may help calculate the SchahlLED earn-out (point 34):

“The Group has the obligation to purchase the remaining shares of the Lumen business in tranches over the next 2 years. To calculate the expected repurchase value the Group has considered the recent and budgeted future performance of the Lumen business analysing forecasted EBITDA, revenue and costs upon which the obligation is based. This analysis is reviewed and updated each year and, if necessary, adjustments are made to ensure that the provision value reflects the best current estimate of settlement with movements recognised as a share-based payment charge. If the forecast EBITDA assumption were to increase by 5%, the resulting contingent consideration would increase by £330,000.”

22) SEGMENTAL ANALYSIS

a) Geography

The SchahlLED purchase has led to ‘Germany’ now being separated from ‘Rest of Europe’:

UK revenue represented 51% of total revenue, the lowest proportion ever. With a full 12-month contribution from SchahlLED, FY 2024 looks set to see overseas revenue exceed UK revenue for the first time.

b) Revenue

SchahlLED looks to have brought with it service revenue of nearly £4m:

Service revenue comprises “surveying, project management, installation and commissioning” and TFW has often said such work is very low margin compared to manufacturing lights. SchahlLED is a (Thorlux) lighting installer, not a lighting manufacturer, which explains its greater service income versus the rest of the group (c£4m versus total SchahlLED revenue of £16.9m).

23) OPERATING EXPENSES

a) Cost of inventories

Most interesting figure here is the cost of inventories at £73m:

The cost of inventories absorbed 41.3% of revenue, the highest since FY 2017 (42.2%). But TFW has commendably ensured its inventory costs have been reasonably tight versus revenue, with a range of 38.4% to 42.8% witnessed since FY 2010.

Assuming cost of inventories are expensed entirely within cost of sales, other cost of sales items have typically offset any greater cost of inventories. For example, this FY’s gross margin is 44.1% versus 44.0% for the prior FY, despite the higher cost of inventories. TFW’s gross margin has ranged between 43.8% and 47.0% since 2010, which seems reasonably consistent and tight to me for a multinational manufacturer.

b) Audit expenses

Despite undertaking one less full-scope subsidiary audit (point 20), PwC lifted its total audit fee by 29% to £374k:

I suppose the extra fees were charged due to SchahlLED becoming part of the group. For perspective, total audit fees were £195k for FY 2018 and have advanced 92% since. At least the £374k audit fees represent only 0.2% of revenue.

24) EMPLOYEES

As per the blog post above, revenue per employee reached a new £187k high.

As also noted in the blog post above, the headcount since FY 2013 undertaking a sales and distribution role has increased from 22% to 27% of the workforce, while the headcount undertaking an administration role has declined from 30% to 27%:

I calculate since FY 2013, the number of production employees is up 85%, the number of sales and distribution employees is up 147% and the number of admin employees is up 77%.

All told, the total number of employees is up 96% since FY 2013, but their total expense is up 194% — with wages up 187% and social security costs and other pension costs up 239% and 229% respectively.

I am therefore pleased TFW is ensuring the extra headcount and their associated extra costs are being counterbalanced by extra revenue — total employee costs at 27.1% of revenue was the lowest since FY 2016 (26.6%).

25) FINANCE INCOME AND EXPENSE

This note lists the income from TFW’s range of assets:

As noted in the blog post above, interest of £236k was equivalent to only 0.6% interest on the £38m average year-end cash position. I expect a company such as TFW to be earning a greater rate during FY 2024.

Dividend income of £209k is generated from financial assets of c£3.4m (point 31), which implies a 6% yield from what I believe are mostly listed UK equities. The dividend income was lower this year versus the previous year, but in line with the 10-year average (£195k).

Net rental income is generated by an investment property (point 28) and it seems by also sub-letting surplus space within operational properties. The investment property generated net rent of £84k, leaving £19k from another property.

Loan interest income arises from various loan notes (point 29). I suspect the bulk of this £168k relates to a £1.8m loan note issued at 4% plus the BOE bank rate. This £1.8m loan note was repaid to TFW during the year, perhaps not surprisingly given the trajectory of base rates. Other loans are to Ratio Electric and a very small and troublesome Spanish investment, the income from which will become identifiable during FY 2024.