23 June 2024

By Maynard Paton

H1 2024 results and Capital Markets Day (CMD) summary for System1 (SYS1):

- A positive H1, with platform revenue up 44%, greater workforce productivity and improved cash generation leading to better-than-expected Q3/Q4 statements and the upcoming reappearance of the dividend.

- H1 progress was not perfect, and drawbacks included questionable adjustments, revenue per client seemingly stagnating and services beyond ad-testing — which offer much larger addressable markets — still losing sales and still requiring product revamps.

- Despite the higher H1 revenue, direct costs declined a remarkable 17% to deliver a record 88% gross margin. But significant bonuses limited the Ebitda margin to 13% — somewhat below the “at scale” target of 30%.

- The subsequent CMD disclosed founder/executive John Kearon is now evaluating “long-term strategic opportunities“, which raises questions about his “relentless execution” of his own platform plan.

- The CMD also provided a £17.5m illustrative Ebitda projection, which supports a possible £15 share price and reinforces my speculation that SYS1 could/should become a bid target.

Contents

- News links, share data and disclosure

- Why I own SYS1

- Results summary

- Revenue and profit

- Strategic review follow-up

- Platform versus non-platform

- Ad testing versus Innovation testing and Brand tracking

- Fame generation versus marketing courses

- John Kearon

- Platform clients

- Employees and bonuses

- Financials

- Q3 and Q4 trading statements

- Valuation

- Shareholder changes

- Potential bid target?

News links, share data and disclosure

- Interim results, presentation and webinar for the six months to 30 September 2023 published/hosted 06/18 December 2023;

- Management Q&A session hosted 11 December 2023;

- Q3 2024 trading update published 24 January 2024;

- Capital Markets Day presentation and webinar hosted 07 February 2024;

- Q4 2024 trading update published 16 April 2024, and;

- Holding(s) in Company (x5: 1,2,3,4,5) published 24/28 May 2024.

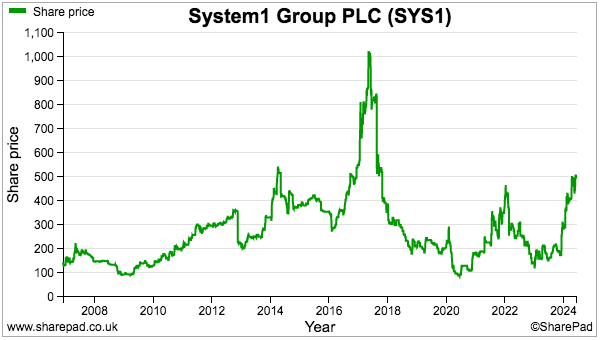

- Share price: 500p

- Share count: 12,689,073

- Market capitalisation: £63m

- Disclosure: Maynard owns shares in System1. This blog post contains SharePad affiliate links.

Why I own SYS1

- Research specialist that forecasts the success of television adverts, with progress resting upon “unmatchable predictiveness” backed by “unique IP” delivered at “market-beating speed and value” through a “world-class product suite“.

- Transition from bespoke consultancy towards automated ‘platform’ services continues apace and is increasingly underpinned by solid revenue growth, improving financials and healthy net cash.

- The company’s own £17.5m illustrative Ebitda projection supports a potential £15 share price and heightens the possibility of an eventual bid — an outcome a former director has previously called for.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

Revenue and profit

- Upbeat comments within September’s AGM statement…

“The Board is encouraged by trading in FY24 H1 and believes that the Group is well set to outperform the current consensus numbers for Revenue and Adjusted Profit Before Taxation for the current financial year.”

- …followed by October’s favourable Q2 update…

“Revenue performance for H1 was slightly ahead of the estimates contained in last month’s AGM trading update, with total revenue expected to be up 27% on H1 FY23 and platform revenue expected to grow by 44%.

Gross profit for the first half year is expected to reach £11.6m at a margin of 87%…The Company expects to report a Statutory Pre-Tax Profit just below £1.0 million for the half-year (H1 FY 23: £0.0m).

Cash inflow during H1 amounted to £0.6m, resulting in a 30 September 2023 net cash balance of £6.3m (31 March 2023: £5.7m)“

- …had already heralded a positive H1 2024.

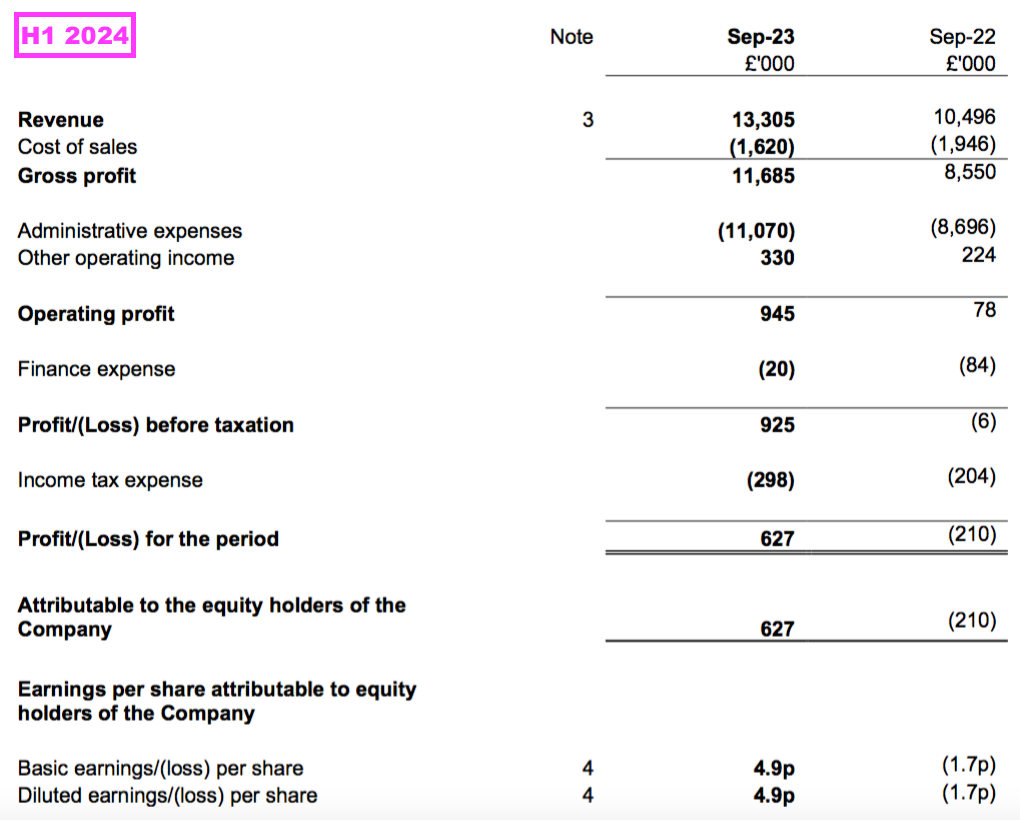

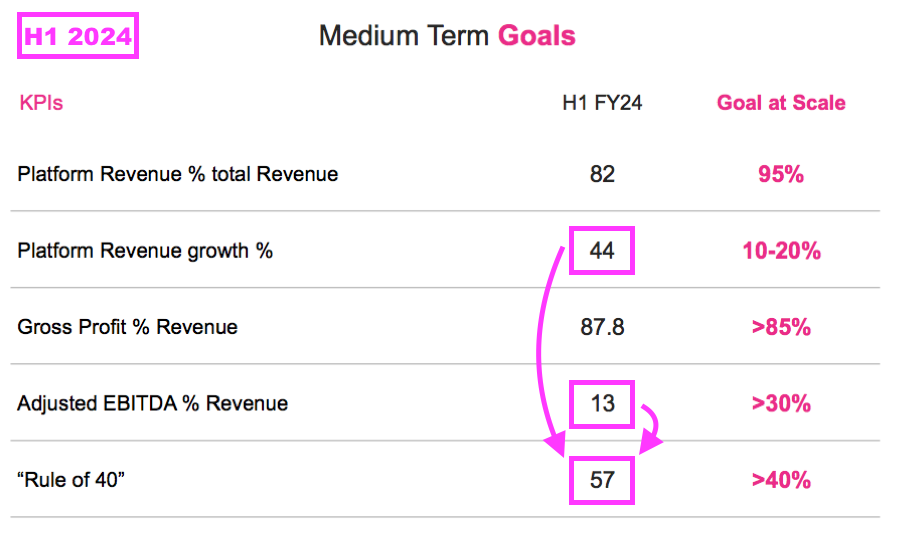

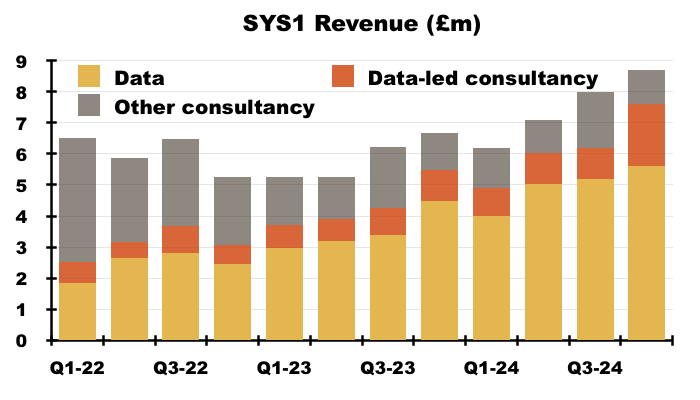

- H1 revenue did indeed increase 27%, to £13.3m, while H1 platform revenue did indeed increase 44%, to £10.9m.

- Both H1 gross profit and the H1 gross margin were a fraction better than October’s projections, at almost £11.7m and almost 88% respectively.

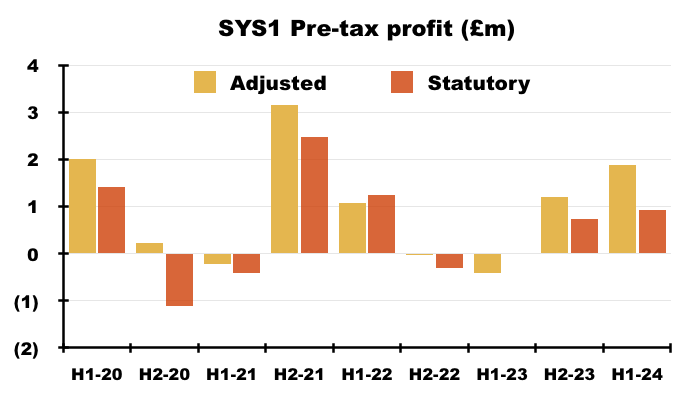

- The H1 statutory pre-tax profit was indeed “just below” £1m at £925k, the H1 cash inflow was indeed £0.6m at £557k and the net cash balance was indeed £6.3m at £6,281k.

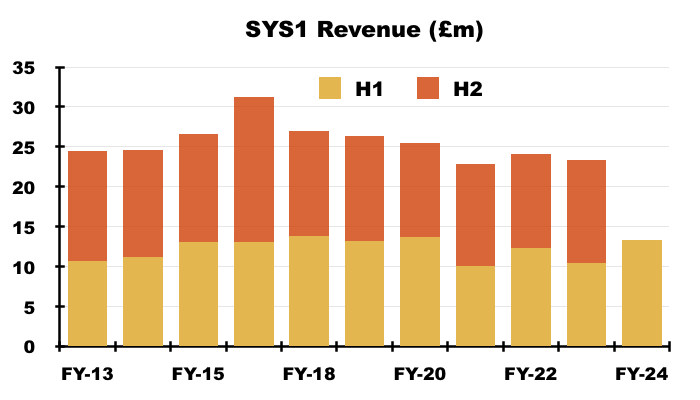

- H1 revenue of £13.3m was the best six-month revenue effort since H1 2020:

- 82% of H1 revenue was supported by platform revenue, due in part to non-platform revenue (i.e. bespoke consultancy income) declining 18% to £2.4m (see Platform versus non-platform):

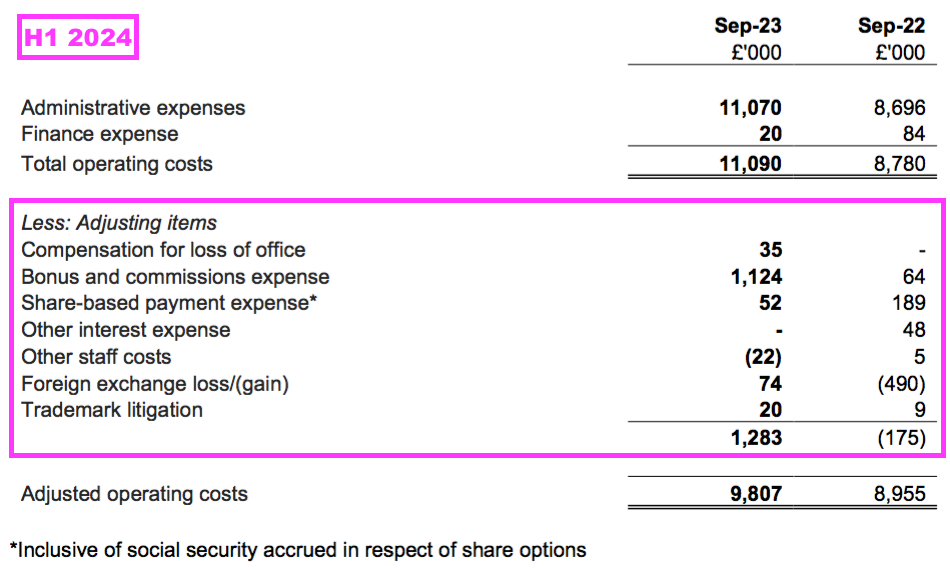

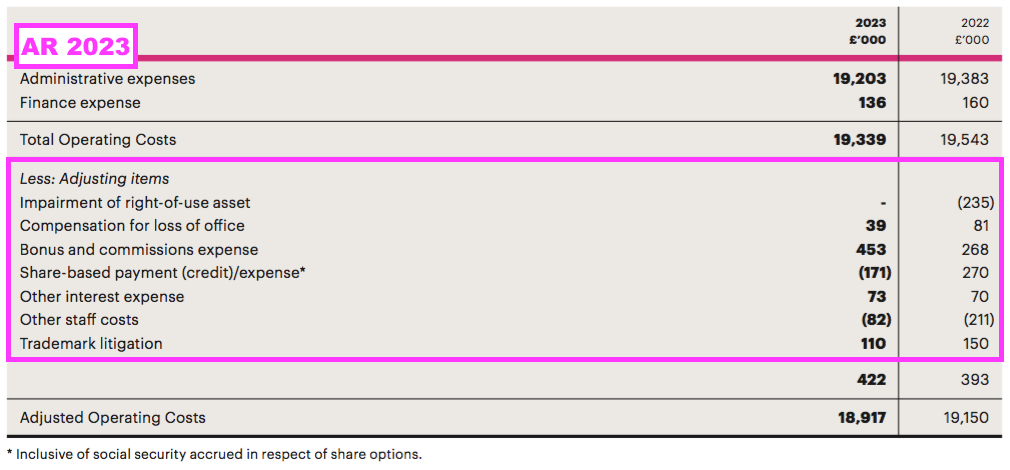

- This H1 included SYS1’s usual array of adjustments:

- SYS1 once again claimed its adjusted figures excluded items that “impede easy understanding of underlying performance” (see Financials).

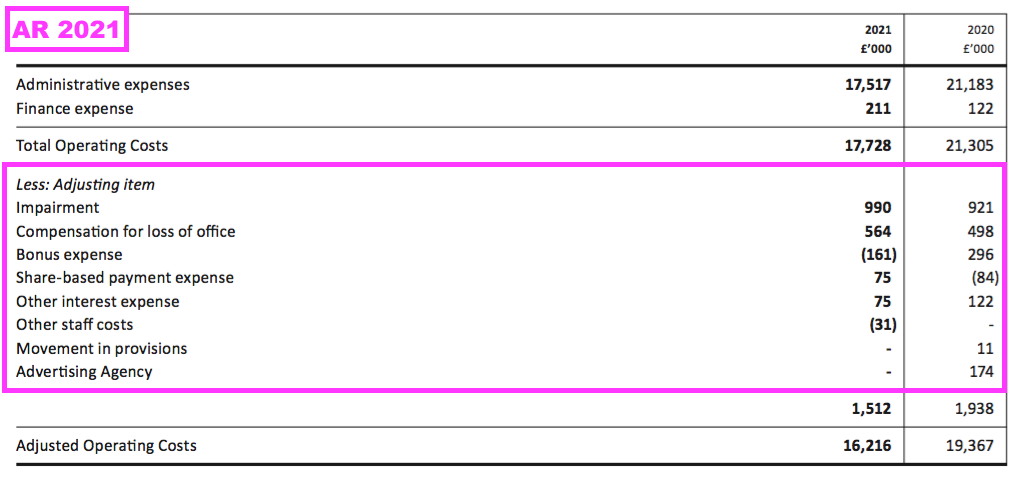

- SYS1’s results have not offered an “easy understanding of underlying performance” for some time. Notable adjusting items featured during FYs 2020, 2021, 2022 and 2023:

- SYS1 indicated this H1’s statutory £925k pre-tax profit was £1,878k excluding the various adjusting items:

- I calculate adjusting items during FYs 2020, 2021, 2022 and 2023 alongside this H1 have totalled £5.5m. Many of the items have a rather questionable ‘adjusting’ status (see Financials).

- In addition to the adjusting items, SYS1 continues to capitalise certain software development expenditure.

- This H1 witnessed a net £0.3m spent on new IT systems that bypassed the income statement. Total software development costs yet to be amortised against earnings now stand at £1.4m (see Financials).

- Other income received during this H1 came to a useful £330k, which included a mix of trademark-settlement payments, office sub-lease receipts and (possibly) AI-research grants.

- The adjustments, capitalisation and other income continue to leave SYS1’s statutory profit history rather difficult to interpret:

Strategic review follow-up

- The comparable H1 announced a strategic review that concluded SYS1 should devote greater attention to:

- The group’s “unique selling proposition [of] ‘predictiveness’“;

- Digital ads;

- The world’s largest advertisers;

- Partnerships with media groups, such as the existing tie-ups with ITV and LinkedIn;

- Partnerships with industry agencies, such as Omnicom/BBDO, and;

- The United States.

- The strategic review was triggered by shareholders frustrated by how SYS1 had struggled to fully exploit its “world class” market-research products and deliver worthwhile, dependable earnings.

- The unhappy shareholders were unconvinced by the strategic review and, during April 2023, requisitioned a General Meeting (GM) that proposed a number of board changes, including:

- The appointment of former SYS1 chief executive Stefan Barden as executive chairman, and;

- The demotion of SYS1 founder/executive John Kearon to a non-exec role.

- Shareholders rejected the proposed board changes by 58% to 42%, which left the strategic review in place.

- Updates to most of the strategic-review initiatives were supplied during this H1 and the subsequent Capital Markets Day (CMD).

- The H1 slides reiterated SYS1’s ‘unique selling proposition of predictiveness’…

- …while the H1 webinar reemphasised SYS1’s “unique” market position and the importance of serving customers very quickly:

“We are unique in being able to translate emotion into predictive results. We deliver a high level of return on marketing investment for our customers, and the way we do this is by being the most predictive player in the market.”

…

“Our customers… tell us our speed is also very, very competitive, so if we could offer the predictiveness without having the speed, they would not be coming to us.”

- February’s CMD webinar underlined the group’s “unique” qualities by referring to years of developing intellectual property and mentioning a “defensive moat“:

“We are predictive through the use of emotion. So when you look into out methodology, it is all about left-brain thinking versus right-brain-thinking, and what most of our competitors are doing is talking about rational thinking. What we do is take emotion and… we turn that into predictiveness. That has been built out over the last 20 years in intellectual property and is not something that someone can copy overnight.

What also have a bit of a defensive moat, where we have also tested every ad in the US and the UK over the last five or six years, so we are able to say for every single person we work with how they are doing and how their competitors are doing. And that… again, alongside our IP, is something other people can’t copy.“

- The H1 slides also recapped recent work on new media-channel partnerships and digital ads:

- February’s CMD reviewed SYS1’s efforts to capture the largest advertisers within the United States:

- Note that the strategic review originally announced Mr Kearon had been given the “priority task of securing new business and partnership opportunities in the US“.

- However, February’s CMD disclosed Mr Kearon was now back in the UK and currently working on undisclosed “strategic opportunities” (see John Kearon).

- The only strategic-review initiative not mentioned during this H1 or the subsequent CMD was partnerships with industry agencies such as Omnicom/BBDO.

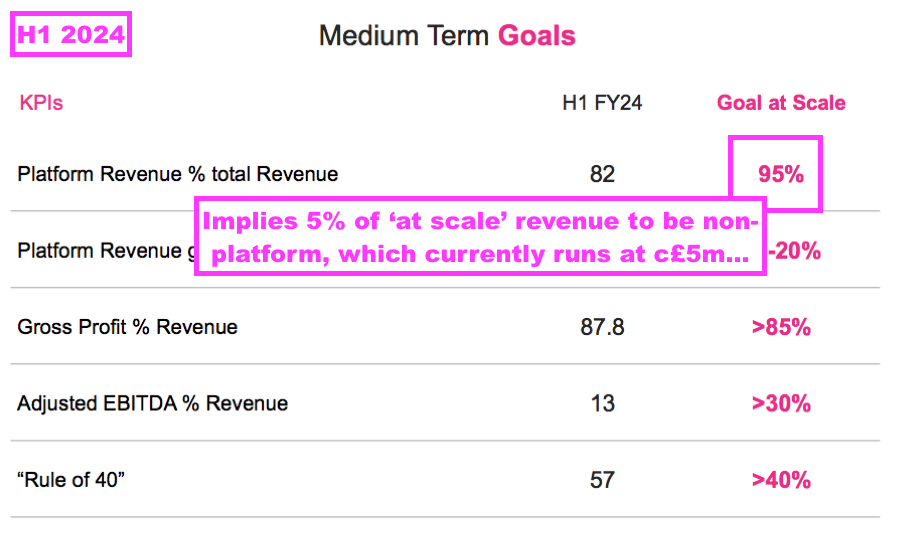

- The ‘Rule of 40’ target introduced by the strategic review was maintained for this H1:

- The Rule of 40 figure is derived by adding platform revenue growth (H1: 44%) to the total adjusted Ebitda margin (H1: 13%)…

- …although that calculation could be flattered by excluding non-platform revenue while including non-platform Ebitda (see Platform versus non-platform).

- The Rule of 40 would have (just) been met if SYS1 added total revenue growth (H1: 27%) to the total adjusted Ebitda margin (H1: 13%).

- All told, SYS1 looks to have adhered to most of its strategic-review initiatives and this improved H1 performance — followed by upbeat statements during January and April (see Q3 and Q4 trading statements) — might on the surface suggest shareholders were right to reject the proposed GM board changes.

- But the GM protest votes do seem to have had some sort of impact on SYS1.

- In particular, Mr Kearon’s new role working in the UK on new “strategic opportunities” implies he is not actively working on the primary (and supposedly solitary) platform strategy (see John Kearon).

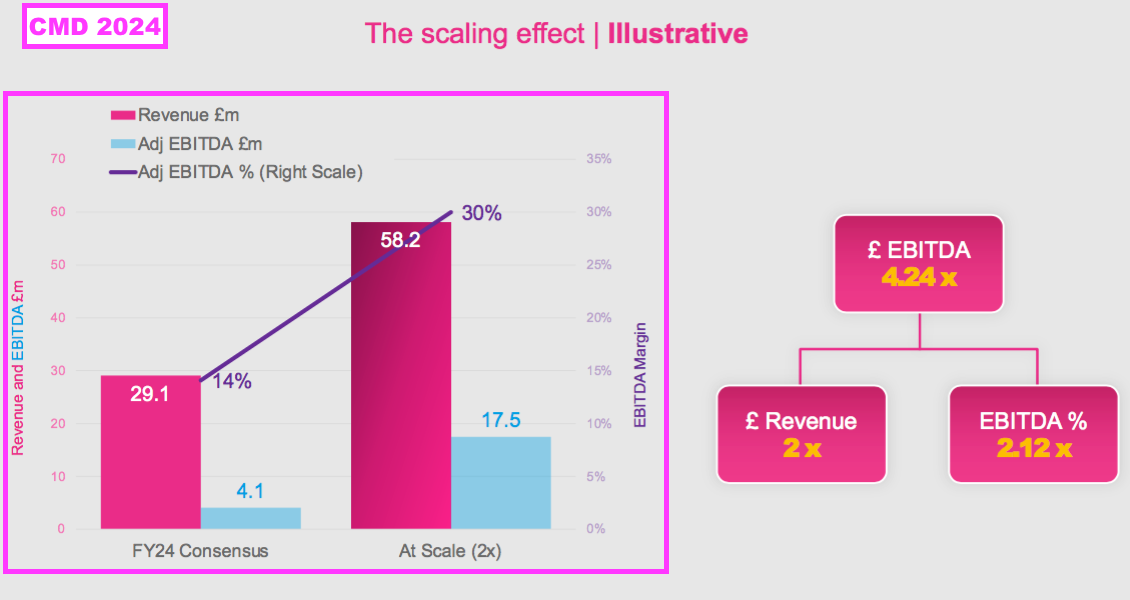

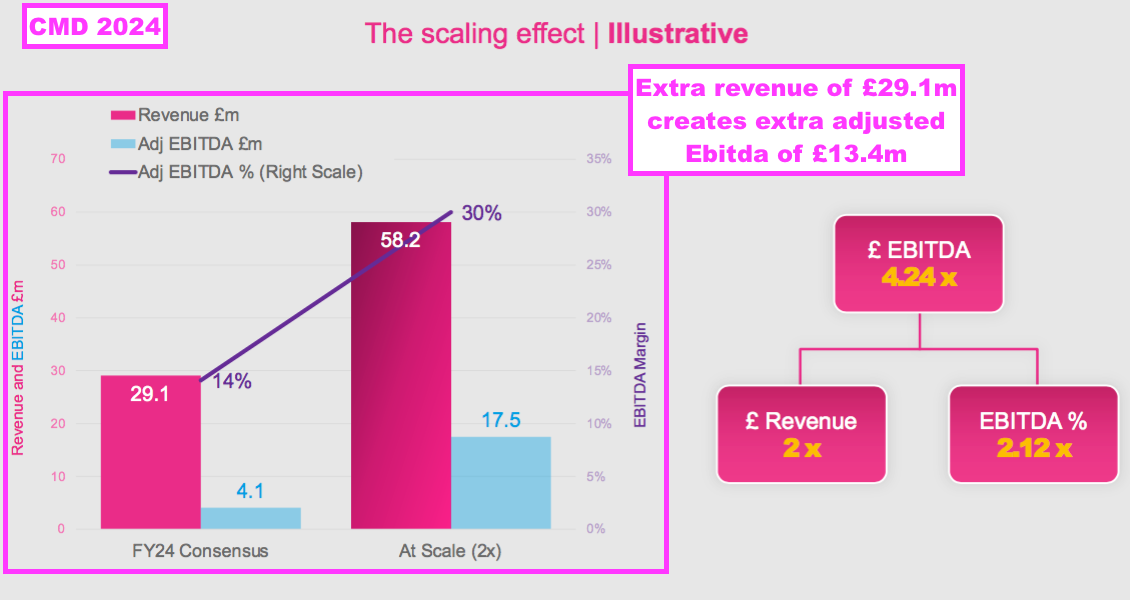

- Furthermore, the CMD presentation disclosed an extremely intriguing Ebitda projection based on an illustrative doubling of revenue (see Valuation):

- The illustrative Ebitda projection seemed a direct answer to a question Mr Barden raised at the April 2023 GM:

“6) Valuation: As a result, and you might want to pass this to Chris, if successful, how much could System1 be worth in say 2 to 3 years time?

a) If you can’t give a valuation what would the shape of the P&L be? For example, your 25% CAGR sales growth aspiration is a doubling in sales every 3 years. What is the associated cost structure?“

- Wishful thinking perhaps, but I speculate a middle ground between Mr Kearon and Mr Barden has been found to move SYS1’s platform strategy forward after the GM (see Shareholder changes).

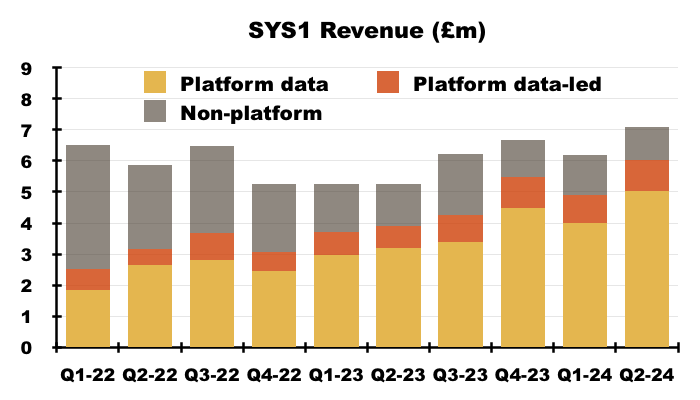

Platform versus non-platform

- SYS1’s strategic review validated the group’s shift from supplying bespoke consultancy work to providing automated data services via a “marketing decision-making platform“.

- Platform products are led by Test Your Ad (TYA)…

- …which was launched during April 2020 and allows customers to upload proposed adverts to SYS1 and receive a report within 24 hours based upon the verdict of an online panel:

- Platform revenue is supported by Test Your Innovation (TYI) and Test Your Brand (TYB), which perform the same online-panel function for product ideas and company brands:

- TYB and TYI were launched during November 2021 and May 2022 respectively.

- Platform ‘data’ revenue is bolstered by ‘data-led’ consultancy revenue, which consists of follow-up improvements and guidance from SYS1’s marketing experts:

- This H1 revealed:

- H1 platform ‘data’ revenue up 46% to £9.0m, and;

- H1 platform ‘data-led’ revenue up 31% to £1.9m.

- Note that platform revenue can vary from quarter to quarter:

- For example, Q4 2023 witnessed platform revenue of £5.5m that reduced to £4.9m for Q1 2024 but rebounded to £6.0m for Q2 2024.

- Management said during my Q&A:

- SYS1 does “not have a massive amount of seasonality quarter to quarter“, and;

- The strong Q4 2023 was possibly due to encompassing some work originally scheduled to complete during the preceding Q3.

- Management noted during the CMD webinar that growth ought to be judged on a six-month or twelve-month view:

“Our ambition is to grow the business mainly on a half-on half or a year-on-year basis. We would love it to be on a quarterly basis and sometimes that is driven by customer demand… It is hard for us to stop customers wanting to use their budgets before the end of their fiscal years.”

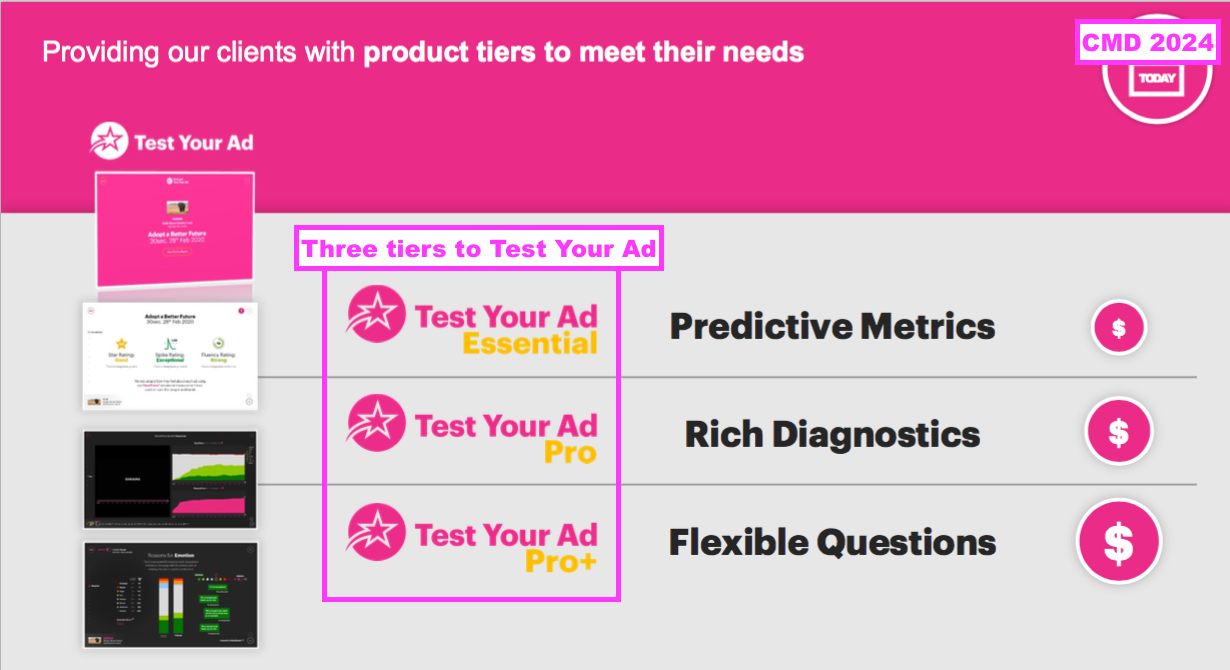

- Management’s CMD commentary disclosed TYA Pro — the mid-tier TYA service that supplies extra data insights — was the group’s best-selling product that represented more than 40% of total group revenue (see Ad testing versus Innovation testing and Brand tracking):

- The CMD commentary also claimed TYA Pro+ — the top-tier TYA service — helped persuade larger clients to join through greater product “flexibility” but, importantly, not at the expense of ‘scalability’:

“TYA Pro+ is really easy for us to manufacture at scale and we retain a really high margin, but most importantly the customer feels they are in the driving seat and have the ability to choose.“

- On the non-platform side, the CMD commentary reiterated how bespoke consultancy was needed to assist some large clients to join SYS1 and could remain approximately 5% of the business “at scale“:

“We have also learnt we need the ability to retain bespoke consultancy, which allows customers to transition from what they are doing to day to what they could and should be doing in the future. We know this is only a very small part of our offering, likely around 5% at scale, and something that we offer to new or very large customers with his revenue potential to help them come on board.“

- H1 non-platform revenue was £2.4m and the H1 webinar revealed £5m for the full year would be a “good outcome” that was still being aimed for.

- Non-platform revenue at £5m possibly representing 5% of total revenue “at scale” leads to a very ambitious revenue estimate (see Valuation).

- The H1 presentation suggested approximately £1.3m of non-platform revenue involved advert testing…

- … leaving approximately £1.0m spread between innovation testing and brand tracking.

- SYS1 has never disclosed the profit contributions from platform revenue versus non-platform revenue.

- Management during my Q&A suggested platform and non-platform revenue enjoyed similar margins:

“They have the same level of margin. Gross margin for both is well above 80% and the difference is not platform or non-platform.It is how tough the client is on price, and sometimes what part of the world the client is in, because prices are just lower in some markets.”

- Management during my Q&A also noted:

- Both platform and non-platform revenue sources attracted similar staffing costs — “expensive IT people” for the former and “highly skilled researchers” for the latter;

- The group now employs “twice the number of IT developers and half the number of researchers” as it used to (see Employees and bonuses), and;

- “The issue is the long-term economics and the scalability of one [service] versus the other”.

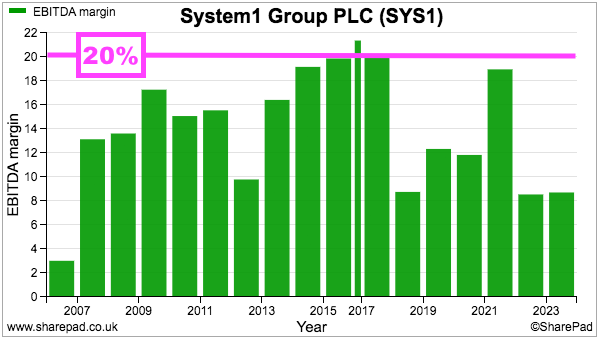

- The H1 presentation indicated a “medium-term goal” of a 30%-plus adjusted Ebitda margin:

- SYS1’s non-platform heyday witnessed Ebitda margins of 20%:

- In theory at least, the ‘scalable’ platform services ought to enjoy much higher margins than the non-platform consultancy work… but the obviously superior economics have yet to emerge at group level.

- April’s Q4 update indicated an FY 2024 adjusted Ebitda margin of 14% that implied a 15% margin for H2 2024 (see Q3 and Q4 trading statements).

Ad testing versus Innovation testing and Brand tracking

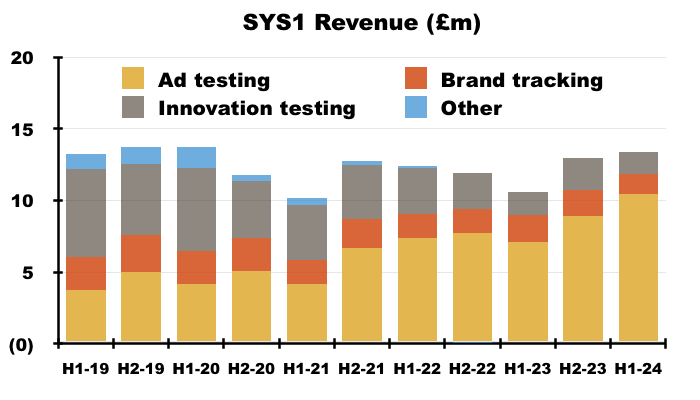

- Ad testing — via the TYA platform service and certain non-platform consultancy work — continues to dominate SYS1’s revenue:

- Ad-testing revenue supported 78% of H1 revenue versus 67% during the comparable H1 and just 27% during H1 2019.

- While H1 ad-testing revenue gained 48% to £10.4m…

- …H1 innovation-testing revenue slipped 6% to £1.5m and H1 brand-tracking revenue dived 24% to £1.4m.

- Combined H1 innovation-testing and brand-tracking revenue of £2.9m compares to £8.4m recorded during H1 2019.

- Using my aforementioned estimate that innovation-testing and brand-tracking revenue included £1.0m earned from non-platform consultancy work…

- …this H1 may have witnessed revenue of £1.9m derived through platform services for innovation testing and brand tracking:

- My chart above (if accurate!) shows platform revenue from innovation testing and brand tracking (c£1.9m) lagging far behind the platform revenue from ad testing (c£9.0m).

- The H1 presentation highlighted a planned relaunch of TYI during calendar 2024:

- Management’s H1 webinar explained:

“TYI was not always meeting what the customer always wanted. So what we identified was the customer process [with] new product development, so from discovering what they might want to focus on, to selecting a few of those ideas, improving the ideas, validating the ideas, and then tracking the ideas.”

- Management said during my Q&A that the relaunch was “not a massive platform rebuild” and was “mainly about how we package it up“.

- The CMD webinar showed the addressable market of TYI to be almost five times the addressable market of TYA:

- TYI could therefore become a much greater money-spinner than TYA.

- But TYI may need heavy promotion to really get off the ground (see Fame generation versus marketing courses).

- This H1 nor the subsequent CMD made any great mention of TYB.

- Management during my Q&A was not overly positive on TYB. Notable comments included:

- “TYB will be the third tier of what we offer — the two prongs for attack will be innovation and advertising“, and;

- “[TYB] is more competitive and lower margin, and the USP is harder to explain.”

Fame generation versus marketing courses

- SYS1’s 2023 annual report (point 1f) reiterated the group’s “relentless execution” towards four goals that included “Generate fame“:

“This year, alongside our shift of culture towards relentless execution, we made significant progress towards delivering the four goals we set out 5 years ago, namely: Build defensible assets; Generate fame; Win new customers; and Generate new revenues.”

- The 2023 report listed a number of ‘fame-generating’ activities:

- Ad of the Week US and UK: “…celebrates the best and most effective creative content“;

- Feeling Seen US: “…how diverse advertising…translates into greater commercial effectiveness“;

- Wise Up: “…how can advertisers portray age more accurately and consistently?“;

- The Short-Cut Guide to Short Term Advertising;

- Addressable Advantage: How Addressable TV Makes Audiences Happy: “…how partnering the right creative content with a targeted audience allows brands to dial up campaign effectiveness“;

- Digital Ad Effectiveness;

- Creativity Goes Omni: “…explores the importance of brand building“;

- How To Create The Perfect Digital Poster;

- Hot Topic Webinars: “…help customers… create winning key moment campaigns“, and;

- The Uncensored CMO: “the global number1 marketing podcast“

- The fame-generating activities all revolved around improving the effectiveness of adverts, which have clearly assisted the growth of TYA…

- …but have not yet helped TYI really take off.

- I would argue the relaunch of TYI later this calendar year ought to be complemented with substantial TYA-like ‘fame generation’.

- After all, TYI enjoys a much greater addressable market than TYA, and SYS1 has enjoyed significant revenue from innovation testing in years gone by.

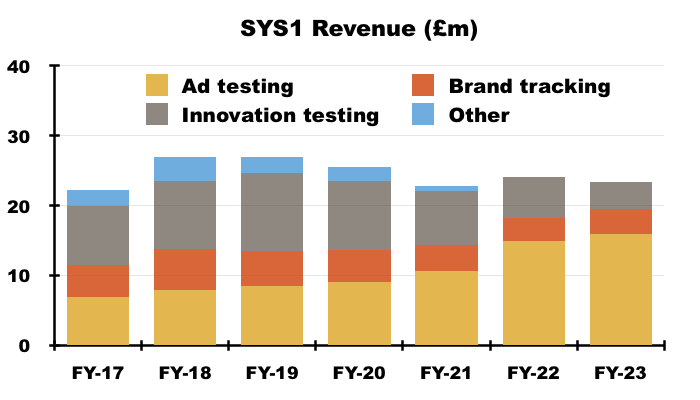

- Innovation-testing revenue in fact topped £11m during FY 2019 versus less than £4m during this H1 and the preceding H2:

- Management’s CMD comments implied huge TYI ‘fame generation’ might not be needed:

“If a customer buys into the SYS1 methodology for their ad testing, we know it won’t be such a big leap for them to go from the ad testing to believing that approach will work on their innovation funnel.”

- Mind you, director comments during the 2023 AGM suggested TYI was in fact a “harder sell“…

“TYI is a harder sell, partly because the cycle is longer. New product cycles tend to be multiple years, so people do not do a new product every year. They might do it in one, three, five or seven year cycles, whereas TYA typically will be annual or bi-annual. Innovation is a longer cycle to get in and start doing stuff with them. But the potential is huge…”

- …while management claimed during my Q&A that the TYI promotional work was in hand:

“We are working on it. It takes longer to do a Lemon or a Look Out for innovation than getting the product repackaged and recreated in the right way.”

- Lemon and Look Out are books written by SYS1’s chief innovation officer, Orlando Wood:

- Both books help the reader understand advertising effectiveness, albeit using lessons drawn from very highbrow sources:

- My FY 2023 review revealed Mr Wood was devising a new marketing course. I wrote at the time:

- “Quite why SYS1’s chief innovation officer is spending time developing a marketing course when Test Your Idea/Brand are without their own books, “thought leadership” and wider promotion has not been made clear.

- This FY talked of SYS1 being “relentlessly focussed on execution against our strategy”, but Mr Wood’s new course suggests he has escaped/ignored/missed that board instruction.”

- Mr Wood’s course has now been launched and is priced at £1,895 per person (group discounts are available!):

- The directors disclosed during the 2023 AGM that Mr Wood was reducing his SYS1 workload to four days a week to manage the course:

“[The course is] a joint thing, it will be co-branded with SYS1, it will raise the [group’s] fame and [Mr Wood] will still be working four days a week, not five, four days a week with us… And he is going down to four days a week in terms of his pay.“

- The directors made these other points about the course at the 2023 AGM:

“The great thing about [the course] is the scalability and that it is modular. It is pre-recorded and essentially can be scaled to multiple people, versus having people in one room with one customer at a time which is much less scalable.”

…

“One of the things that Orlando is brilliant at is making what could be quite a dry topic, fruity, and that is why we think [the course] is going to be incredibly successful.”

…

“Our target market [for the course] is not with professional investors.“

- The AGM discussion indicated the marketing course was a joint venture between Mr Wood and SYS1.

- And Mr Wood looks to have established his own company during February this year (although at least two Orlando Woods are registered at Companies House!).

- A larger addressable market should (in theory) help TYI become a much greater money-spinner than TYA, and I remain convinced SYS1’s most pressing new fame-generation activity right now ought to be developing promotional material for the TYI relaunch…

- … and not commencing marketing courses through senior-manager side projects.

- Given the purported success of Lemon and Look Out with TYA, shareholders can only trust Mr Wood is currently spending his four days a week at SYS1 writing a new “thought leadership” book for TYI.

- I am not too hopeful but look forward to being proved wrong.

John Kearon

- Another senior manager who may not be undertaking “relentless execution” of SYS1’s platform strategy is founder and executive director John Kearon:

- To recap, the aforementioned strategic review said Mr Kearon was going to work on sales in the States:

“John Kearon, currently Founder and CEO, will become Founder & President from 1 December, with the priority task of securing new business and partnership opportunities in the US, where he will spend most of the first half of 2023. John will no longer act as CEO but will remain a director of the Company.”

- SYS1 then announced ahead of the April 2023 GM that Mr Kearon was already capturing new US customers:

“John has recently been working in the US, using his unique position as the Company’s founder to develop new business opportunities and partnerships. This activity is already bearing fruit with several recent customer wins. The Board is delighted that John Kearon has been working in the US where System1 has lower levels of name recognition than in the UK. John is leading the charge to build the fame of our Company and our products alongside the US sales team.“

- Perhaps due to Mr Kearon’s early US customer wins, shareholders voted to maintain Mr Kearon in his executive role at the April 2023 GM.

- The CMD earlier this year disclosed Mr Kearon was no longer leading the US sales charge:

“John Kearon has done an outstanding job over there [in the US]. We had a relatively new sales team and for him to be able to be in the US to bring to life who we are and what we do with that passion as our founder and president was incredible. He was also really able to get the market going by knocking on some doors and being the founder there in person.

What John’s expertise really is, is on that first starting of a business and the entrepreneurial enthusiasm you bring in, and the what you reach after that is the level where you need the big points of scalable growth.

So with that John Kearon has actually just moved back to the UK around Christmas time, and he is going to be helping look at some long-term strategic opportunities in that space for three-to-five years. What we will be doing is then expanding our US sales leadership team to be able to cover and execute that gap of scalable growth.“

- What exactly the “long-term strategic opportunities” Mr Kearon is now working on was not made clear.

- I would argue SYS1’s sole ‘strategic opportunity’ concerns the long-term growth of the current platform service.

- The CMD commentary suggested (at least to me) that Mr Kearon was not deemed the best person to lead the US sales team to “scalable growth“…

- …which does raise the question whether Mr Kearon is in fact suitable to lead the wider group as a board executive to “scalable growth“.

- I am not sure how Mr Kearon’s new “strategic opportunities” role fits in with SYS1’s aforementioned four goals:

“Build defensible assets; Generate fame; Win new customers; and Generate new revenues.”

- I note Mr Kearon did not contribute a lot to the discussion at the April 2023 GM and was the only director not to speak during the 2023 AGM.

- Nor has Mr Kearon appeared on investor webinars for the preceding FY, this H1 and the subsequent CMD.

- I would have thought that, after seeing off the boardroom challenge at the April 2023 GM, Mr Kearon would be taking every opportunity to extol his platform strategy to shareholders.

- Mr Kearon was certainly enthusiastic about SYS1’s future during the 2019 AGM; his presentation to attendees claimed SYS1 was aiming to become the “YouGov of advertising data”.

- I would like to think the forthcoming FY 2024 results will clarify Mr Kearon’s role and whether — as shareholders were led to believe ahead of the April 2023 GM — he is fully behind SYS1’s platform ambition.

- Mr Kearon was paid the highest salary of SYS1’s three executives during the preceding FY (£265k, point 7c).

Platform clients

- Prior to this H1, SYS1 had for some time inconsistently referred to both ‘clients’ and ‘customers’, whereby a multinational ‘client’ could provide the group with multiple regional ‘customers’.

- The inconsistency meant accurately tracking SYS1’s progress through a revenue per client or customer measure was impossible, especially as the group could also refer to ‘data customers’ but then refer later to ‘total clients’.

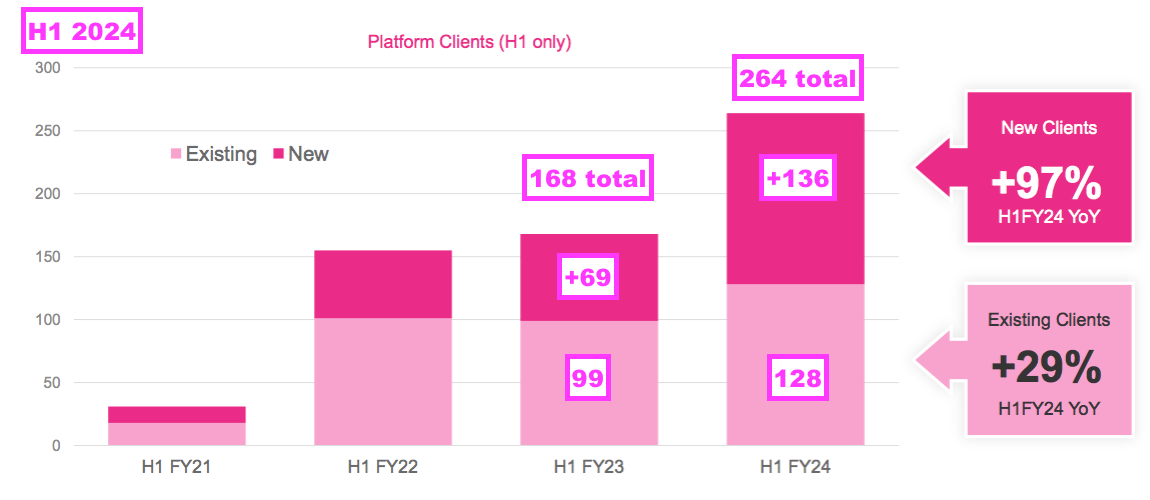

- But this H1 thankfully followed the previous FY and referred to ‘platform clients’ to finally create some reporting consistency.

- The previous FY said:

“FY23 was a record year for new client acquisition, based on our platform automation and increased fame building, amplified through many global partnerships. We recruited 149 new platform clients in the financial year (previous year: 117).“

- And this H1 said:

“Our fame-building, products and partnerships helped the Company to win 136 new platform clients in H1 (H1 FY23: 69). Furthermore, we retained 128 existing H1platform clients in H1 compared with 99 in H1 FY23.“

- I translate the new and retained platform-client numbers to mean total platform clients improved from 168 to 264 between the comparable H1 and this H1:

- SYS1 disappointingly avoids disclosing a formal revenue per platform-client KPI.

- I have estimated SYS1’s platform-client revenue from the chart below:

- Much greater spend per platform client (whether new or retained) during this H1 is not obvious from my sums. I calculate:

- Retained platform clients spent approximately £68k each during this H1 versus approximately £66k during the comparable H1;

- New platform clients spent approximately £16k each during this H1 versus approximately £16k during the comparable H1, and;

- All platform clients spent approximately £41k each during this H1 versus approximately £45k during the comparable H1.

- Perhaps SYS1 does not present a formal revenue per platform-client KPI because the KPI would not reveal fantastic progress.

- A revenue per platform-client KPI showing significant improvements would:

- Underline the growing attraction of SYS1’s platform services to its users, and;

- Help validate the general platform strategy to any unconvinced shareholders.

- Management clarified during my Q&A that a new client is a client that had not purchased a service during the previous financial year. As such, a new client could be an existing client that was simply ‘dormant’ for twelve months.

- Management made the following points about platform clients during my Q&A:

- Few platform clients pay the ‘average’ spend. Larger clients spend many £100,000s, while smaller ones spend low £10,000s;

- Smaller clients are not actively targeted but can be recruited following their inbound enquiries: “It doesn’t cost anything if they come to us. We just pay the gross margin and there are negligible other costs”;

- A “big metric” occurs when a client spends £100k-plus, at which point the client is more likely to have SYS1 “embedded” into its procedures and therefore more likely to become “very sticky“, and;

- Client KPIs are still being worked on, but the best measure could involve just the top 20 clients to avoid distortions with the “long tail” of smaller clients.

- SYS1 did publish the revenue earned from its top 20 customers (not platform clients!) within the preceding FY:

- The top 20 customers (not platform clients!) during the preceding FY spent an average £820k — although that revenue included non-platform income.

- The CMD commentary revealed the top 20 customers (not platform clients!) were each spending more than £250k and many were spending more than £1m a year.

- The CMD commentary also suggested customers (not platform clients!) may one day even spend more than £3m a year:

“Fairly consistently, our top ten customers represent about a third of the company’s revenue. We have had a situation in the past when a single customers was more than 10%, and I think we could have two or three customers that could become close to 10%… in the next couple of years. It is very plausible we can have multiple customers over £1m and have some customers over £2m and maybe some over £3m. That is not at all out of the question.“

- Note that the CMD commentary revealed SYS1 implemented a price rise last year:

“We did last year with our existing customers put in a price rise and they all love our service enough not to have anybody leave us or have any challenges… Obviously increasing prices to people who have bought into long-term contracts can take a long time for it to flow through before it actually hits. What we have is the ability to really hold our market prices and not have to discount significantly…against them.”

- Although nobody leaving the service because of the higher prices is good news…

- …. those higher prices did not really filter through to my earlier estimated revenue per platform-client calculations.

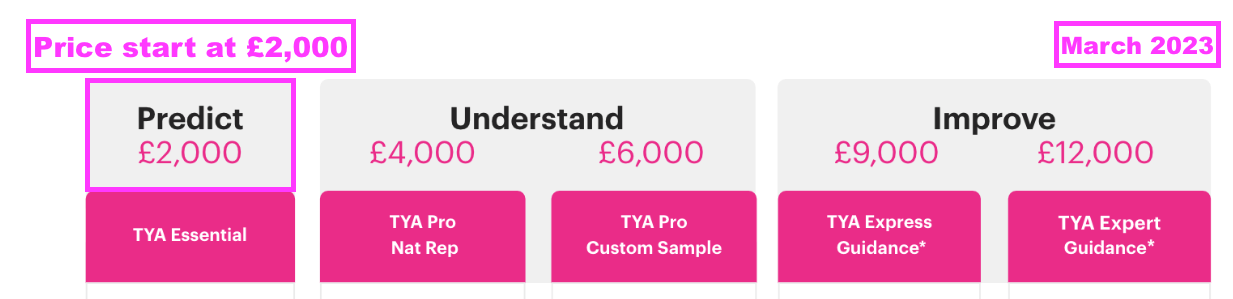

- My H1 2023 review (published March 2023) showed TYA prices starting at £2,000…

- …while SYS1’s TYA prices currently start at £2,500:

- The CMD commentary implied further price increases could be implemented:

“We are also aware we have been strongly focused on price, but actually over the last year we have seen some price increases go through and we are aware there is some more headroom for us to focus on in the future.“

- I maintain SYS1 must continue to provide consistent platform-client numbers — and begin publishing revenue per platform-client figures — for shareholders to accurately assess the group’s platform economics.

- My FY 2023 review said OnTheMarket (OTMP) provided a useful comparison for investor-platform disclosure.

- Similar to SYS1, OTMP is a small company with a mixed financial record that operates a fledgling platform trying to disrupt much larger incumbents.

- OTMP spotlighted its different ARPA (average revenue per property advertiser) measures clearly within its investor presentations:

- OMTP was acquired during October 2023 at a 56% premium to its prevailing share price.

- SYS1 shareholders may well ask whether the absence of platform-client KPIs is obscuring the group’s platform economics from would-be acquirers (see Potential bid target?).

Employees and bonuses

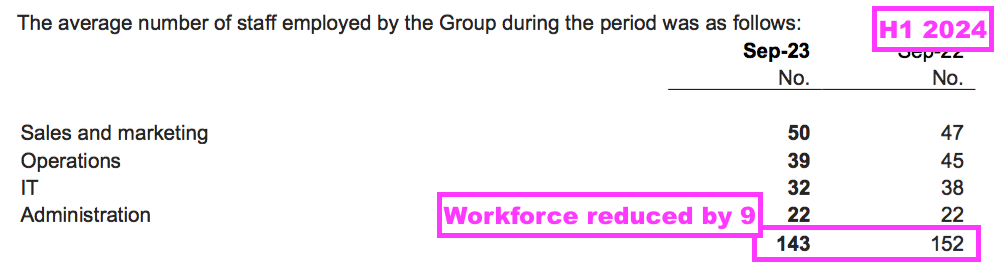

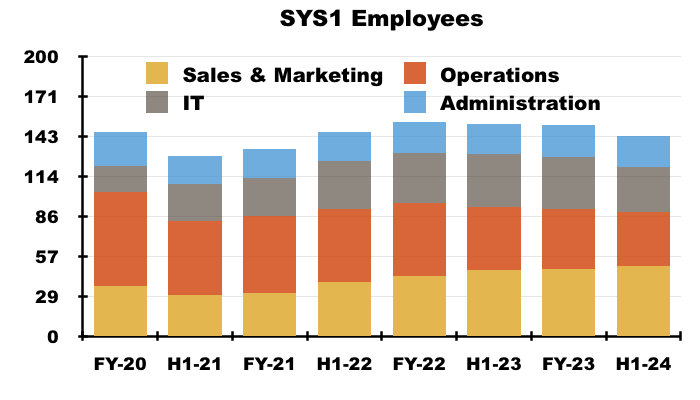

- One of the most encouraging developments within this H1 was lifting revenue by 27% with nine fewer employees:

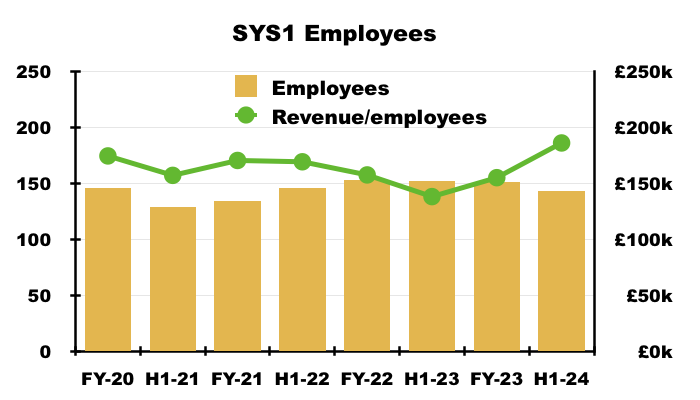

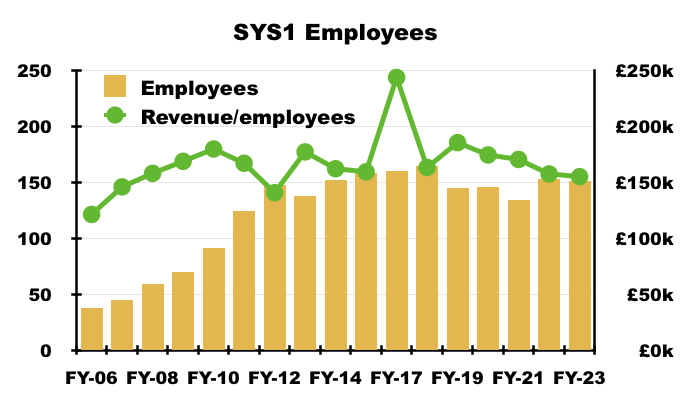

- H1 revenue of £13.3m and the 143 headcount gives revenue per employee of £186k, the highest level during recent H1s and FYs…

- ….and second only to the £244k per employee recorded during the bumper FY 2017:

- Between FY 2020 and this H1, the workforce proportions have changed as follows:

- Sales and marketing: from 25% to 35%;

- Operations: from 46% to 27%;

- IT: from 13% to 22%, and;

- Administration: from 16% to 15%:

- The shift away from ‘consultancy’ operations staff towards sales and IT employees clearly reflects the group’s platform strategy and — quite possibly — “scalable growth” beginning to emerge on a per-employee basis.

- Management said during my Q&A:

- Any extra employees would be sales and marketing, and;

- Revenue could “probably get well past £30m” with the current workforce “give or take a couple of heads“.

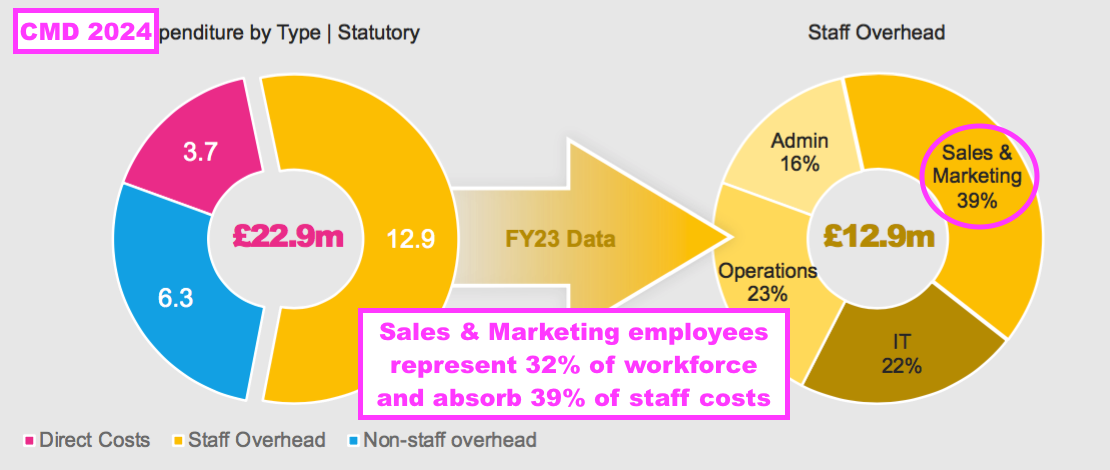

- The subsequent CMD anticipated a “low impact on overhead costs” with extra sales and marketing employees being the most likely new hires:

- Note that, during the preceding FY, sales and marketing employees represented 32% of the workforce but also represented 39% of the staff overhead:

- This H1 reported staff bonus and commission payments had jumped to a significant £1.1m:

- Management explained during my Q&A:

- The £1.1m bonus and commissions were split £400k from a one-off H1 bonus scheme and £700k from the FY 2024 bonus scheme;

- If SYS1 were to continue its “current trajectory“, another £700k could be expected to be charged during H2 from the FY 2024 bonus scheme;

- The £400k one-off H1 bonus scheme was implemented in lieu of H1 pay rises;

- Pay rises were implemented at the start of H2 2024;

- The H1 staff bonus was measured on gross profit;

- Sales commissions accounted for approximately £0.1m of the £1.1m;

- Commissions are based on gross sales from new customers and are typically paid for the first year only;

- Larger percentage commissions are earned from larger new customers, and;

- Commissions are paid only to a handful of employees.

- SYS1 declared the staff bonus and commission payments as an adjusting item, but management during my Q&A disclosed such payments would become a “normal cost” within the upcoming FY (see Financials).

- Management during my Q&A refused to disclose how much of the £700k reflected the short-term bonus scheme for the group’s senior managers.

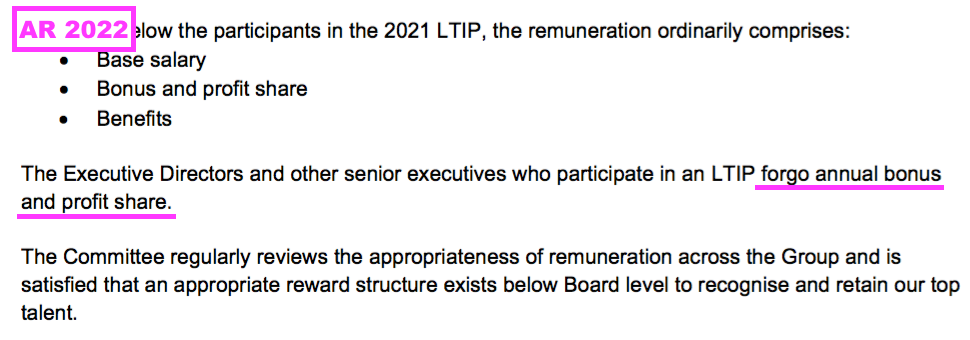

- The short-term bonus scheme for senior managers was revealed within the 2023 annual report… and was introduced despite shareholders previously approving an LTIP on the understanding the senior managers would forgo a short-term bonus! (point 7a):

- The directors described the new senior-manager bonus scheme as “extraordinarily effective” during the 2023 AGM.

- Indeed, SYS1’s revenue progress since the AGM (i.e. during Q3 and Q4) may well have justified all of the bonus schemes employed during this H1 and the subsequent H2 (see Q3 and Q4 trading statements).

- Mind you, SYS1 must be careful its greater revenue is not counterbalanced by far greater employee pay, bonuses and commissions…

- …which restrict the platform’s economies of scale and in turn limit profit growth for shareholders.

Financials

- The most promising financial measure of this H1 was gross margin, which set a new record at almost 88%:

- An 88% gross margin implies SYS1 can buy online-panel responses for £12 and repackage that data for sale at £100.

- This H1 said the improved gross margin followed “platform and supply chain efficiencies, price increases and favourable product and geographic mix.”

- Somewhat remarkably, direct costs declined 17% despite revenue increasing 27%:

- Management explained during my Q&A:

- More than 80% of direct costs relate to outsourced panels;

- A significant part of the gross-margin improvement was due to greater API use with panel suppliers, which gave SYS1 more control over costs;

- Panel operators are “incentivised” to supply good data, and checks are in place to “protect against low-quality data“, and;

- “It is not a race to the bottom on costs… data quality is the number one metric we rely on.”

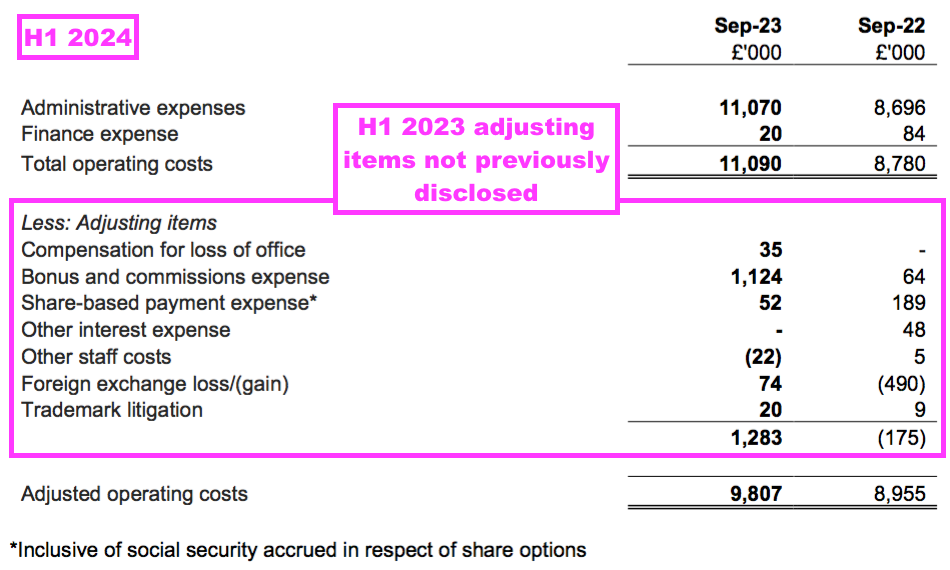

- This H1 included the usual array of adjusting items:

- I think only ‘Trademark litigation’ could be deemed a genuine one-off charge.

- ‘Compensation for loss of office’ for example has been reported every year since FY 2012 (total £1.8m).

- Management confirmed during my Q&A that ‘bonus and commissions expense’ would be reclassified as a “normal cost” for FY 2024 (see Employees and bonuses).

- I have never really understood what ‘Other interest expense’ and ‘Other staff costs’ represent.

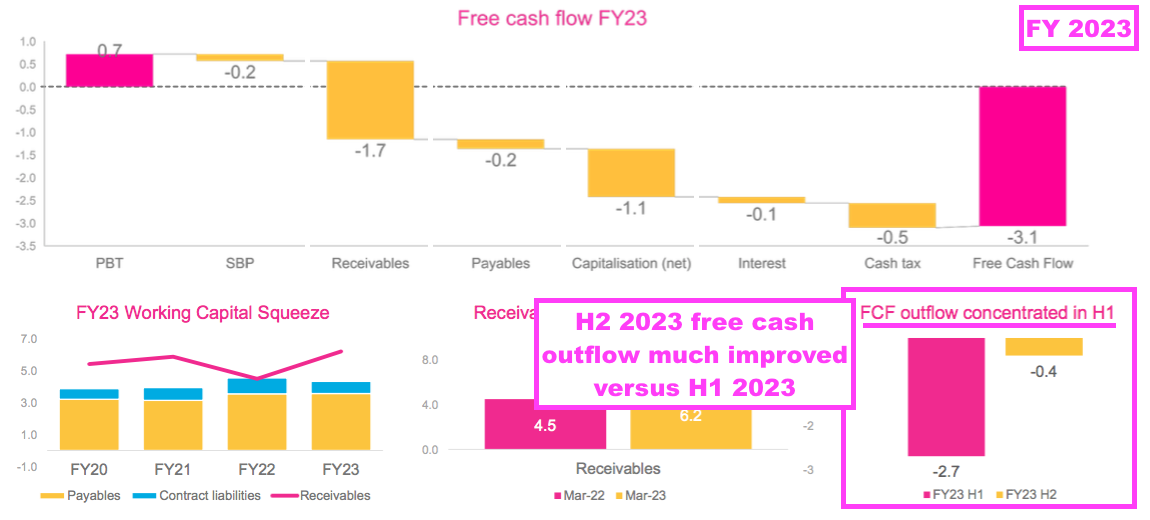

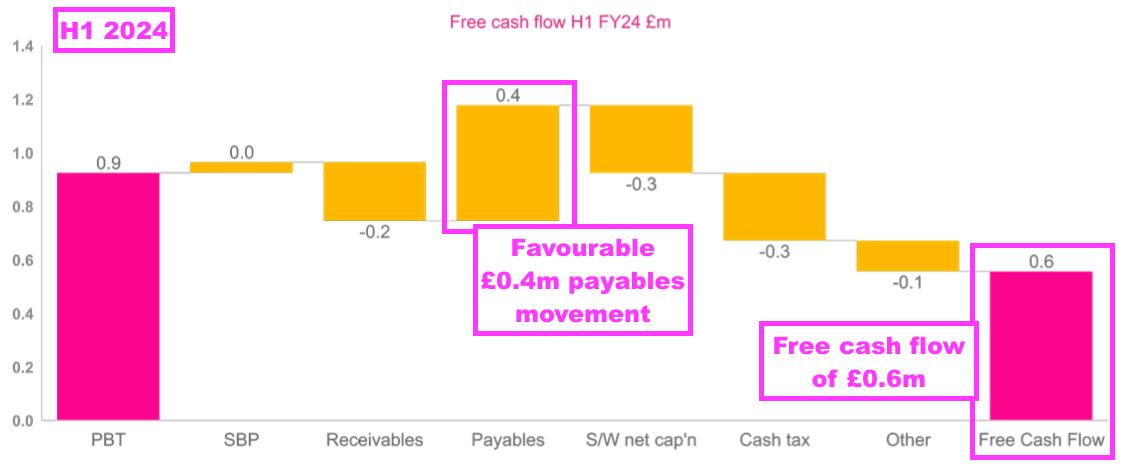

- The preceding FY had seen the group’s free cash outflow reduce from £2.7m to £0.4m from H1 to H2:

- SYS1’s free cash generation improved further during this H1 to record an inflow of £0.6m:

- Mind you, the free cash performance was supported significantly by a favourable £0.4m payables movement — which I suspect reflects H1 bonuses owed at the half year.

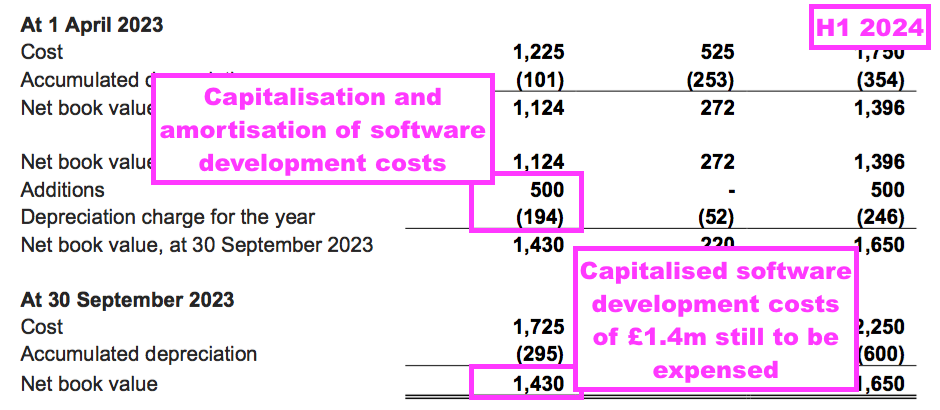

- Note that SYS1 continues to capitalise certain software development costs. During this H1, £500k was redirected onto the balance sheet with an associated amortisation charge to earnings of only £194k:

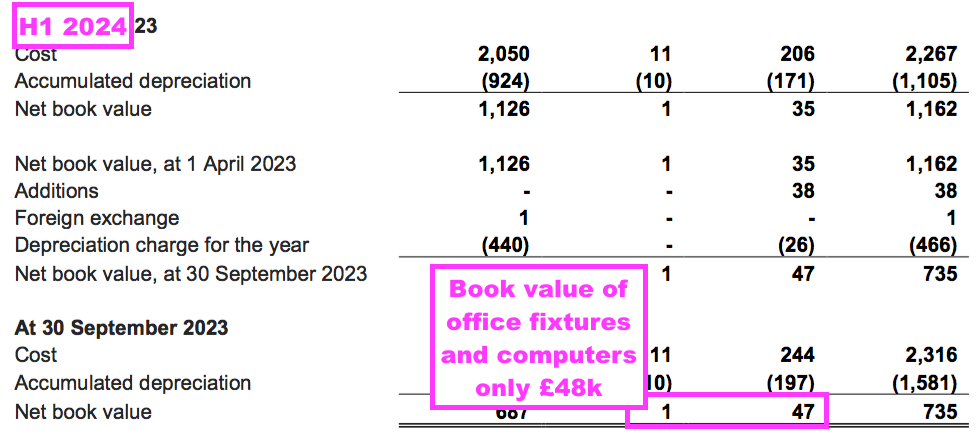

- SYS1 commendably operates with few conventional tangible assets. The book value of office fixtures and computers is only £48k after £38k was spent during this H1:

- The £0.6m free cash inflow took the cash position to £6.3m, equivalent to almost 50p per share. SYS1 continues to carry no bank debt nor pension complications.

- Despite the significant cash position, this H1 disclosed zero financial income.

- Management said during my Q&A that SYS1:

- Did keep its cash in banks (points 4a and 11), and;

- Was earning interest during H2.

- A cursory analysis of my portfolio shows other companies were able to earn at least 2% on surplus cash during this H1.

- Collecting 2% on £6m would earn SYS1 an extra £120k a year to help mitigate higher staff costs (see Employees and bonuses).

- Cash generation reassuringly improved during the subsequent H2, with the Q4 2024 statement announcing net cash of £9.6m (up a further £3.3m) and the encouraging reintroduction of dividend payments (see Q3 and Q4 trading statements).

Q3 and Q4 trading statements

- SYS1’s Q3 and Q4 trading statements were both very positive.

- The Q3 statement published during January revealed:

- Q3 platform revenue up 46% to £6.2m;

- Q3 non-platform revenue down 6% to £1.8m;

- Q3 total revenue up 29% to £8.0m;

- A YTD gross margin of 87%, and;

- Q3 net cash of £6.4m.

- The Q3 performance appeared better than SYS1 had expected:

“The Group enters the final quarter of the year with good trading momentum following a consistently strong December quarter. As a consequence, the Board believes that the Group is now well placed to deliver results ahead of previous expectations. Revenue for the current financial year is expected to be at least £29 million (FY23: £23.4 m) and statutory profit before tax to be comfortably above £2 million and materially ahead of current consensus (FY23: £0.7m).”

- The Q4 statement published during April revealed:

- Q4 platform revenue up 37% to £7.6m;

- Q4 non-platform revenue down 6% to £1.1m;

- Q4 total revenue up 30% to £8.7m;

- An FY gross margin of 87%, and;

- Q4 net cash of £9.6m.

- The Q4 performance also appeared better than SYS1 had expected:

“Based on the unaudited management accounts, Profit before Taxation for the year ended 31 March 2024 is expected to amount to £2.8m, up £2.1m on FY23 and ahead of market expectations (revenue: £29.1m, profit before tax : £2.4m). This Profit before Taxation figure includes the release of £0.4m of provisions related to a now-closed sabbatical scheme.“

- The Q4 statement supplied a number of reassuring snippets.

- “All geographic regions achieved substantial double-digit Revenue growth for the year.”

- The H1 performance had shown revenue from the Americas (£4.7m) down on the preceding H2 (£5.4m), with all other regions showing their revenue up.

- “The Communications product group (Test Your Ad) delivered the majority of the Revenue growth in FY24, with gains in Innovation offsetting a reduction in Brand following the end of a non-platform multi-year contract.”

- The performance of TYI may have improved following its disappointing H1.

- “Marking its confidence in the Group’s cash generation and continuing profitable growth, the Board intends to resume paying dividends, starting with a final dividend for FY24 which will be detailed in the annual results and formally proposed to shareholders at September’s AGM.”

- A dividend payment suggests the business has reached a foundation level of profit.

- “All geographic regions achieved substantial double-digit Revenue growth for the year.”

- The Q4 statement also gave this client update:

“New business performance was strong throughout the year, with over 250 new clients providing just over a quarter of total Revenue.”

- 250 new clients supplying 25% of FY 2024’s revenue of £30m = £30k per new client… which does not suggest a huge improvement from the £16k (or £32k annualised) per new (platform!) client during this H1.

- The Q4 statement provided an Ebitda update, too:

“The adjusted EBITDA margin for the year is expected to exceed 14% (FY23: 8%), representing good progress towards the Group’s at-scale goal of 30%.”

- I calculate H2 total revenue was £16.7m and, if the FY 2024 adjusted Ebitda margin was 14%, H2 adjusted Ebitda was therefore £2.5m and the H2 adjusted Ebitda margin was therefore 15%.

- An H2 adjusted Ebidta margin of 15% improves on the 13% registered for this H1.

- I also calculate FY 2024 delivered adjusted Ebitda of £4.2m, which means:

- FY 2024 witnessed extra revenue of £6.6m and extra adjusted Ebitda of £2.3m versus FY 2023, and;.

- The extra revenue for FY 2024 enjoyed an adjusted Ebitda margin of 35% (£2.3m/£6.6m).

- SYS1’s platform economics may well be emerging if revenue beyond FY 2024 can achieve a 35% adjusted Ebitda margin as well.

- The CMD presentation suggested additional revenue may even achieve an adjusted Ebitda margin beyond 35%…

Valuation

- The CMD presentation commendably included an illustrative projection of revenue doubling and the resultant illustrative projection of adjusted Ebitda:

- The illustrative CMD projections imply extra revenue of £29.1m would earn extra adjusted Ebitda of £13.4m through an adjusted Ebitda margin of 46% (£13.4m/£29.1m).

- As mentioned earlier, the £17.5m illustrative Ebitda projection seemed a direct answer to a question Mr Barden raised at the April 2023 GM:

“6) Valuation: As a result, and you might want to pass this to Chris, if successful, how much could System1 be worth in say 2 to 3 years time?

a) If you can’t give a valuation what would the shape of the P&L be? For example, your 25% CAGR sales growth aspiration is a doubling in sales every 3 years. What is the associated cost structure?“

- Mr Barden’s reference to “25% CAGR sales growth” reflected SYS1’s commentary ahead of the April 2023 GM:

“We have stated our ambition to become a Rule of 40 company. To do this, we will need to deliver revenue growth of the ‘Predict Your’ and ‘Improve Your’ products, plus EBITDA margin, to total 40. While we are in growth mode, we expect the majority of this to come from revenue, so the Company will need to be growing revenue at a minimum of 25% over the coming years.“

- If SYS1 expands its revenue at a 25% annual compound rate, then the illustrative CMD revenue projection would be achieved after three years (i.e. during FY 2027).

- If both SYS1’s illustrative revenue and adjusted Ebitda projections are achieved during FY 2027, I would argue a small-cap growing revenue at a 25% CAGR and enjoying an 30% adjusted Ebitda margin would trade on a premium multiple….

- …and today’s £63m market cap would in turn offer compelling upside.

- Assuming:

- Depreciation and amortisation continue to absorb 5% of revenue, and;

- Tax is charged at the standard 25% UK rate…

- …the £17.5m illustrative Ebitda projection could translate into earnings of approximately £10m, which at, say, a 20x P/E would support a £200m market cap or a £15 share price.

- The illustrative projections can of course be viewed in two ways.

- On the one hand, very few quoted small-caps are confident enough to provide tantalising illustrative projections of revenue and Ebitda… and no sensible board would publish such illustrative projections unless they were reasonably plausible.

- On the other hand, SYS1:

- Has not yet entirely proven its platform economics;

- Has issued very bold ambitions before (for example, the £1 billion market-cap aspiration), and;

- May have presented some fanciful numbers simply to quell further unrest from Mr Barden.

- Note that SYS1’s adjusted Ebitda figures exclude share-based payments but do include staff bonuses/commissions and do include those other adjusting items.

- SYS1 did not put a timescale on its illustrative CMD projections, although the longer revenue takes to double, the less likely the £17.5m illustrative adjusted Ebitda will be achieved due to cost inflation.

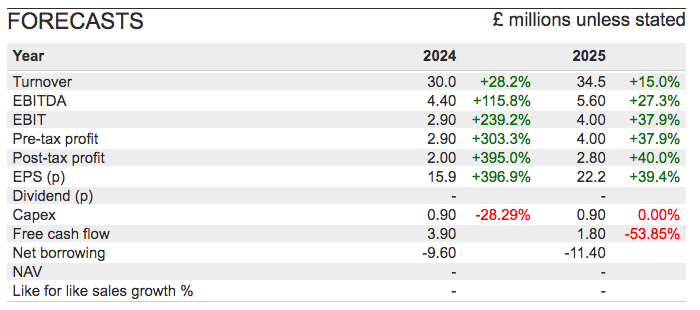

- SharePad shows the following broker forecasts:

- Revenue forecast to advance by 15% to £34.5m for FY 2025 could mean doubling revenue by FY 2027 is a tall order.

- Mind you, annualising Q4 2024 revenue of £8.7m gives £34.8m and equates to more than that FY 2025 forecast of £34.5m. I therefore get the impression the FY 2025 broker forecasts may be somewhat conservative.

- For perspective, annualising Q4 2023 revenue of £6.7m gave £26.8m and yet FY 2024 revenue eventually came to £30.0m.

- The FY 2025 forecasts do not seem to meet SYS1’s Rule of 40 either (i.e 15% revenue growth plus an implied 16% Ebitda margin = 31).

- And I note the broker forecasts within SharePad do not show a dividend despite the Q4 statement announcing a final payout for FY 2024.

- The broker forecasts within SharePad support a 22x P/E for FY 2025 and suggest the 500p shares are anticipating significant growth for FY 2026 and beyond:

- As well as the illustrative projection of revenue doubling, the H1 presentation included another hint of optimistic progress:

- Platform revenue predicted to represent 95% of total revenue “at scale” means non-platform revenue “at scale” would represent 5%…

- …and with near-term non-platform revenue expected to be approximately £5m (see Platform versus non-platform), could total revenue “at scale” actually reach £100m?!

- Management explained during my Q&A:

- The 95% ‘at scale’ proportion could be between 90% and 99% depending on how larger customers decide to spend on non-platform services;

- ‘At scale’ is “essentially quadruple” this H1, “so we are talking a £50m [revenue] business”, and;

- Revenue of £50m “could be very achievable in the next couple of years… given the growth we are looking at.“

- Whether revenue reaches an ‘at scale’ £50m or the illustrative £58m, the recent £63m market cap should still be very undervalued if the adjusted Ebitda margin heads towards the group’s 30% target.

- I am now more convinced Mr Barden was right when he told me ahead of the April 2023 GM that SYS1 could be worth “£100m at least… if not £125m“:

“I think this business is worth £100m at least, £8 a share, if not £125m, £10 a share.“

- I even believe Mr Barden could be on the low side with his valuation estimates of last year.

- My optimistic £200m market-cap/£15 a share calculations must be countered by numerous possible drawbacks, including:

- Revenue growth may plateaus as:

- Winning larger customers in the States takes much longer than expected, and/or;

- TYI and TYB struggle to re-establish themselves due to insufficient ‘fame generation’;

- Adjusted Ebitda margins fail to reach the 30% ‘at scale’ goal as salaries, bonuses and other expenses advance too quickly, and;

- Senior managers not involved with the “relentless execution” of the platform strategy start meddling with the group’s operations.

- Revenue growth may plateaus as:

- On that final point, I am hopeful SYS1’s board and larger shareholders will prevent any untoward senior-manager interference…

Shareholder changes

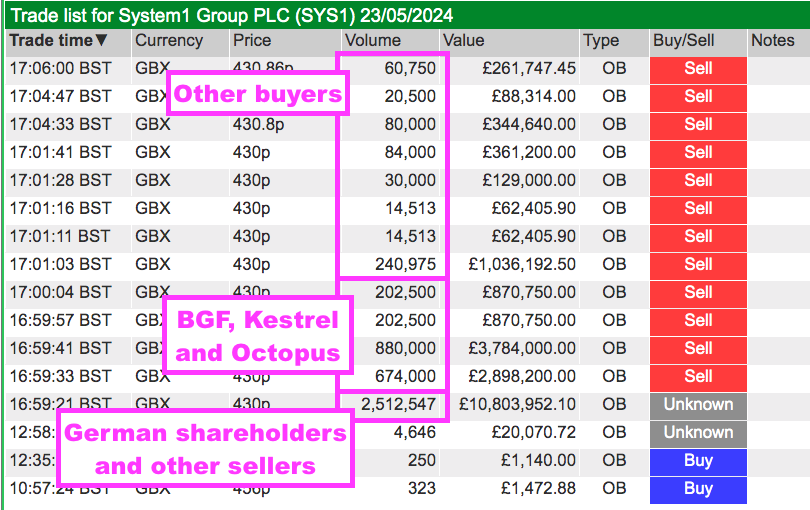

- Significant changes to SYS1’s shareholder register occurred during May.

- The FY 2023 annual report listed the following major shareholders (point 4e):

- Reported changes during May were:

- Investmentaktiengesellschaft für Langfristige Investoren TGV reducing from 10.4% to 0%;

- Chapters Group (formerly Mediqon) reducing from 5.5% to 0%;

- BGF increasing from 0% to 6.9%;

- Kestrel Partners increasing from 0% to 5.3%, and;

- Octopus Investments increasing from 0% to 3.2%.

- The buys and sells were all conducted at 430p.

- Note that trade data from SharePad implies a further:

- 500,000 shares (3.9%) were sold alongside the German (Langfristige and Chapters) disposals, and;

- 545,251 shares (4.3%) were bought alongside the BGF, Kestrel and Octopus purchases:

- The sellers of the 500,000 shares and the buyers of the 545,251 shares have not identified themselves through the RNS.

- The exit of the two German investors is not ideal. After all, during the summer of 2022 the Germans agitated for the strategic review and installed their own non-exec on the board.

- The German investors also voted for the proposed board changes at the April 2023 GM.

- The German investors appear to have made reasonable money on SYS1, with their initial RNS disclosures published when the shares were approximately 300p (July 2018 and June 2022) and subsequent purchases performed when the shares were much closer to 200p.

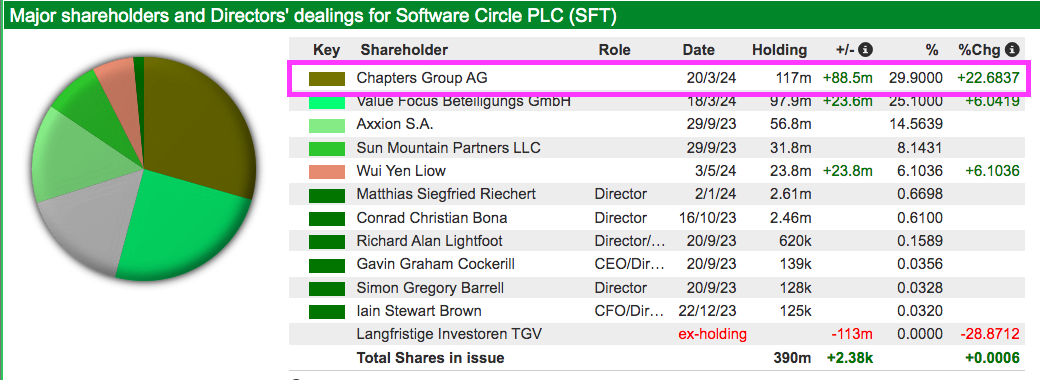

- I speculate the Germans now have investment ambitions elsewhere. Chapters in particular is a €460m software conglomerate and has become the driving force behind serial SaaS acquirer Software Circle:

- At least SYS1’s RNSs have not revealed Mr Barden selling out.

- Ahead of the April 2023 GM, Mr Barden told me he would “likely exit” at 440p:

“If at the GM the board and its supporting shareholders carry the vote against our resolutions and continue to support current management, then I will likely exit at £4.40, the share price at the time I stepped back, such is my lack of confidence in the current board to obtain £8/£10 per share.

…

If I do not become chairman, I’m therefore inclined to wait for the £4.40, and hold management to account accordingly. The ‘global #1 platform’ shareholders will increase board pressure until either the share price rises or ever-growing shareholder frustration will lead to patience eventually running out and board changes.”

- If Mr Barden remains a shareholder at the recent 500p, then perhaps he:

- Is satisfied by SYS1’s recent progress;

- Welcomes the illustrative CMD projections, and;

- Reckons the £17.5m illustrative adjusted Ebitda could actually be very plausible.

- Mr Barden may even believe SYS1’s present board could match his own ambition to advance the market cap to “£100m at least… if not £150m“.

- Of the three incoming major shareholders, Kestrel appears the most interesting.

- Kestrel invests in software companies with “attractive financial characteristics”…

“The attractive financial characteristics of software companies are well understood and include:

• High levels of recurring revenues from B2B or B2B2C customers

• Well invested and IP-rich assets

• High and sustainable gross margins

• Substantial and growing international revenues

• High levels of cashflow conversion

• Negative working capital“

- …and often takes an ‘active’ role:

“We’re challenging, supportive and above all ambitious for our portfolio companies, partnering with management teams to identify key issues and uncover fundamental strengths.

By uncovering fundamental strengths and working closely with management teams, often over several years, we unlock significant equity upside for our investors. When required, we actively engage and take board seats in our portfolio companies, assisting with governance and strategic issues to accelerate change and drive value.“

- Kestrel is not afraid of taking large stakes and encouraging takeovers.

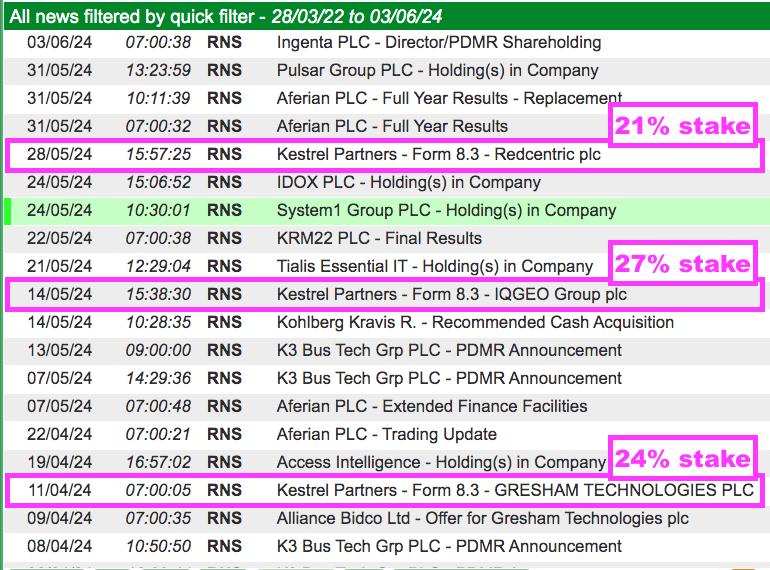

- SharePad reveals Kestrel holding 20%-plus stakes in Redcentric, IQGEO and Gresham Technologies after the trio each received a bid earlier this year:

- I would like to think Kestrel would become somewhat ‘active’ with SYS1 should SYS1’s board deviate from its platform strategy.

- Kestrel has taken non-exec appointments at Gresham Technologies, Redcentric, Team Internet, Pebble Beach Systems, K3 Business Technology, Smoove, IQGEO and Idox.

- I would also like to think Kestrel (as well as BGF and Octopus) has identified significant potential upside to SYS1’s £63m market cap.

- You never know, perhaps Kestrel, BGF, Octopus and Mr Barden have arrived at the same conclusion I have — that the shares could be worth £15 were the illustrative CMD projections to materialise within the next few years.

Potential bid target?

- Ahead of the April 2023 GM, Mr Barden told me he planned to refocus SYS1 before selling the group for at least £100m were the GM vote to go his way:

“It is Focus, Prove and Sell. System1’s products can be global leaders, but only if sold through an existing global salesforce with existing global sales relationships. It is hubris to think System1 can build this capability organically itself. But global buyers will want proof before they pay a premium. Over the next few years we prove the System1 business really works, and then sell it. Shareholders will get a percentage share of the synergies that the new owners get. The crux is there is a big chunk of synergy there that shareholders would receive. Shareholders would also be able to realise this gain without selling at a discount.“

…

“I think this business is worth £100m at least, £8 a share, if not £125m, £10 a share.”

- At the time Mr Barden gave the example of Sumero Equity spending $170m to acquire Zappi.io, a marketing-platform business that offers a TYI-type service to multinationals.

- Zappi was established in 2012 and Companies House shows revenue surging from £6m to £45m between 2015 and 2022:

- I am convinced SYS1 should now be of interest to similar private-equity buyers, given SYS1 has recently demonstrated:

- Superior top-line growth, with Q4 2024 platform revenue up 37%;

- A higher gross margin (FY 2024: 87%) than Zappi (FY 2022: 69%);

- Greater revenue per employee (H1 2024: £186k) than Zappi (FY 2022: £149k), and;

- Profitability and surplus cash generation, unlike Zappi.

- Mr Barden should possess good knowledge of the likely bid chances for SYS1 and similar market-research businesses. His statement at the April 2023 GM referred to his chairmanship of Behaviorally:

“The Market Research industry is a laggard in Platform development. It remains highly ad-hoc, relationship and agency/talent focused, for a variety of well understood reasons. But the first Platforms are emerging. For example, I chair Behaviorally LLC, a non-competing, USA-based research firm, where I support the team led by Alex Hunt who is creating much value by leaning into this Platform opportunity. As Behaviorally is owned by a single Private Investor, I suspect its progress will become public at some time in the future, and if so then at that time it will become a good comparison for System1.”

- Behaviorally is a US market-research specialist that uses AI, surveys and data analysis to predict the sales success of product packaging. Clients include Colgate, Ferrero and Kraft Heinz.

- Mr Barden’s reference last year to Behaviorally “creating much value“ suggests the US firm has been performing well.

- Available financial information about Behaviorally is presently limited to disclosing 137 employees, a number similar to SYS1’s 143. But Mr Barden suspecting Behaviorally’s progress “will become public at some time in the future” sounds very intriguing…

- …especially as Mr Barden’s statement at the April 2023 GM also noted his work with “investment advisors“:

“I also work with investment advisors and, being a good pupil, believe that I understand today’s Market Research industry layout relatively well.”

- As well as investment advisors, Mr Barden works alongside two representatives of Alcentra, a private-credit investment manager, as part of Behaviourally’s board:

- I presume Alcentra is no stranger to M&A deals, which I like to think adds weight to Mr Barden’s conviction about eventually selling SYS1 had the GM vote gone his way.

- Incidentally, the Behaviorally chief exec that has been “creating much value” is former SYS1 director Alex Hunt, who seems very capable of spearheading market-research businesses in the States:

- Mr Hunt became co-head of SYS1’s US division during 2012, led the US division outright from 2015, was appointed to the board during 2017 and left SYS1 to join Behaviorally during 2018.

- Between FYs 2012 and 2018, SYS1’s US revenue surged 72% to £10.3m. Without Mr Hunt, SYS1’s latest 12-month ‘Americas’ revenue — which includes both US and non-US sales — was only £10.1m .

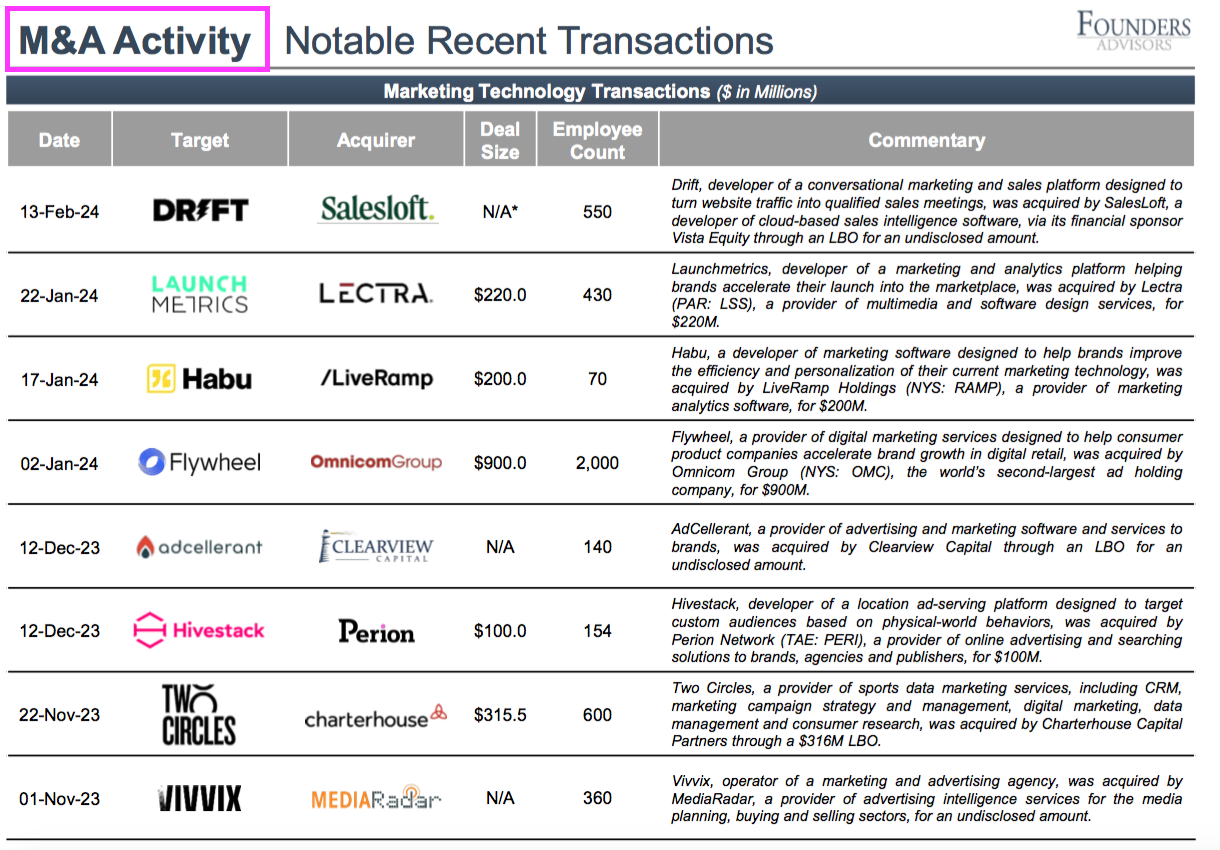

- M&A activity within the wider marketing-technology sector is spotlighted by Founders Advisors, a US ‘transaction advisory firm’, through a very useful February 2024 presentation:

- The presentation implies sector M&A deals continue apace as lots of interested parties remain prepared to pay decent sales multiples to land the right ‘MarTech’ business.

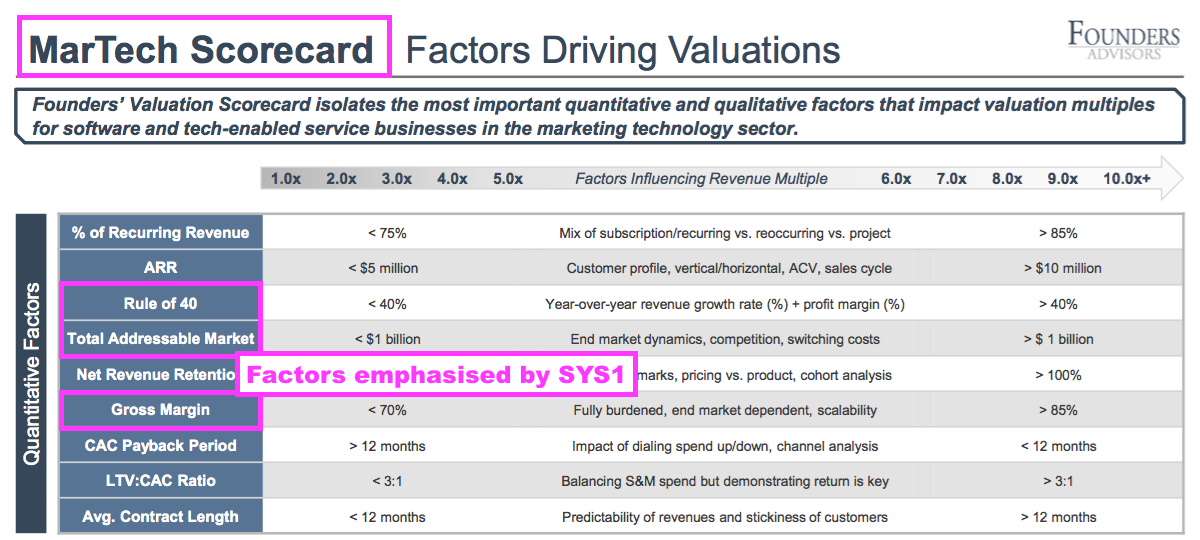

- SYS1 also ticks a few boxes with Founders Advisors’ ‘MarTech Scorecard’:

- No wonder Mr Barden was so confident last year about selling SYS1 for at least £100m.

- Alongside private equity, industry multinationals such as Ipsos, Kantar and Nielsen — all of which undertake regular M&A — could also be suitors for SYS1:

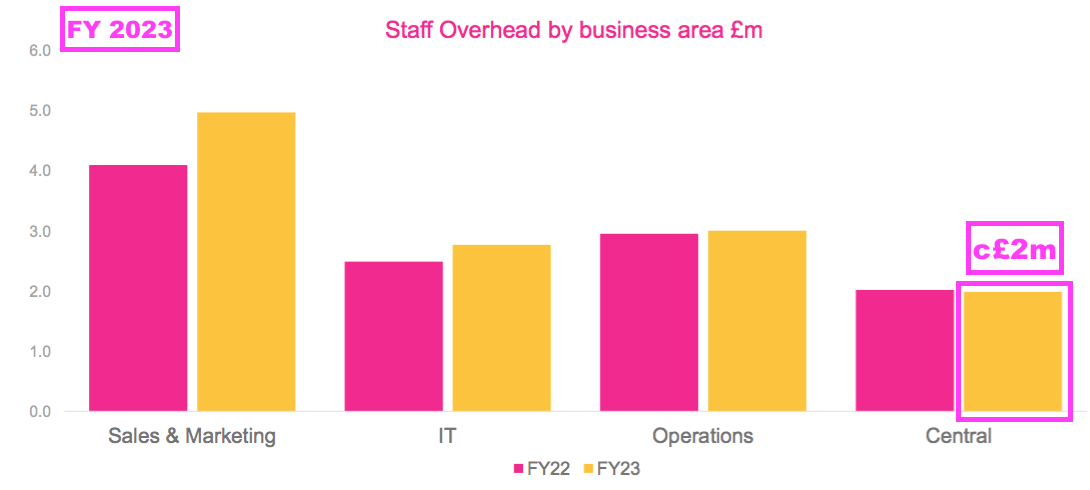

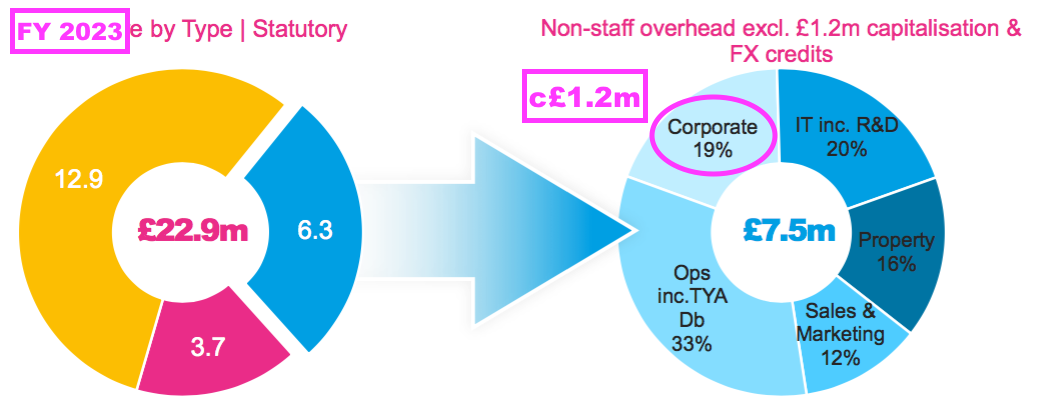

- I note SYS1’s preceding FY presentation gave possible bidders helpful details of potential cost cutting, including central staff salaries of approximately £2m…

- …and corporate expenses of approximately £1.2m:

- Assuming the illustrative CMD projections are plausible and can be achieved within the next few years, would-be bidders can now acquire SYS1 before the group’s full ‘at-scale’ potential is realised.

- Endorsed perhaps by Mr Barden and/or Kestrel, private equity or a trade buyer could today pitch a knockout offer at, say, £8 a share…

- …and then accrue for themselves SYS1’s potential platform growth to my £15 a share estimate and beyond.

Maynard Paton

Thanks for your very detailed and insightful writeup on System1.

I have been following your writing on System1 for a few years now, and been a holder twice in that time (currently holding).

Like the Germans, I sold last month from The Boon Fund, but only top-slicing, as I too believe this should head north. My sell target is less ambitious than either yours or Mr Barden’s, at only 620p.

I have concerns whether existing management have the experience for the next stage of growth, especially USA and internationally, and also think that trying to scale up the in-house sales team will prove painful and throw some spanners into the growth momentum. At least for a quarter or two.

I would most welcome a bid, but with the Germans selling out it looks like possibly no offers, even preliminary discussions, were on the table (otherwise why sell out). But potentially, bidders might be waiting for the FY results and Q1-25 trading update, to get the full picture.

Hi Boon,

Glad you thought the writeup was useful. Good point on international expansion. USA has not gone entirely to plan over time, and I can see with the benefit of hindsight the departure of Alex Hunt in 2018 has had some impact. USA was once a very large innovation-testing market for SYS1, but whether USA ad-testing can reach similar heights — of even the heights of UK ad-testing — remains to be seen. SYS1 is enjoying a lot more ‘fame’ in the UK now, but I recall management saying in a webinar USA may be a 3-year journey to get to similar recognition. SYS1 has also gone very quiet on the USA ‘advisory team’ established last year.

Talk of bidders is just speculation on my part, fuelled by Mr Barden saying last year that he was confident SYS1 could be sold after three years if he were to become executive chairman.

I am not quite sure why the Germans have sold. They did the hard work by effectively instigating the strategic review and the business has turned around and will even resume dividends. I would have thought they would be holding on for more of the recovery. So either they know something sinister, or they have other investing ideas.

Maynard

Sparkling results and a very bullish outlook. I followed you in on this one Maynard with a position that in hindsight was far too small. My numbers suggest that coming years figures should get close to £40m revenue, we should start getting some operational gearing with that figure. Assuming that plays out, the current valuation doesn’t seem that expensive to me. My position is still small so I will resist the urge to take some profits.

A sale at a higher price at some future date has only gotten more likely.

Thanks Patrick. I don’t recommend anybody follow what I do, but happy things have worked out so far!

Maynard

Hi Patrick,

Just replying to your comment as I have held SYS1 for a number of years and exchanged views with Maynard on this blog and elsewhere over that time and I thought there may be confusion as we share the same forename and I didn’t want anyone to attribute our comments incorrectly :-).

……….And I certainly didn’t follow Maynard into SYS1 :-)

Great analysis, very much appreciated.

Thanks David, glad you found it useful

Maynard

The Investmentaktiengesellschaft für langfristige Investoren commented on their exit in their HY letter, without saying much though:

“System1 shares had been a longstanding holding in the TGV Partners Fund until May of this year when the fund sold its whole position amid a larger reallocation of shares among various stakeholders.”

And then they go on describing the volatility of the investment:

https://valueandopportunity.com/wp-content/uploads/2024/07/bericht-des-sub-advisors-fuer-das-teilgesellschaftsvermoegen-partners-fund-ueber-das-erste-halbjahr-2024-englisch.pdf

My personal impression from reading it is that they saw better opportunities rather than having made an unsettling discovery in System1.

Many thanks Simon. A useful link (that I have inserted for you!)

TGV enjoyed a 24%pa IRR on SYS1 having first bought in 2018 at c200p, and as the report says, then purchased more at the lows. They probably want a less volatile investment!

Maynard