02 January 2024

By Maynard Paton

Happy 2024! I hope your shares prospered last year and you continue to find my blog useful.

A summary of my portfolio’s 2023:

- Total return of +15.3% (Q4: +5.4%)*;

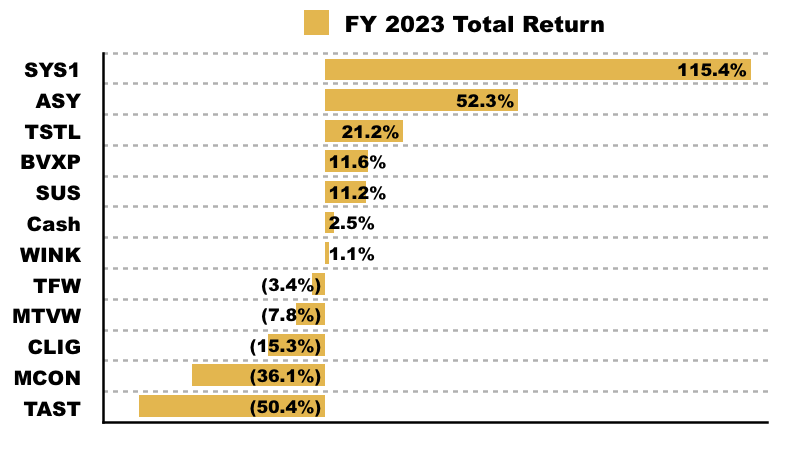

- Individual returns ranged from up 115% for System1 to down 50% for Tasty;

- One share was topped-up: City of London Investment;

- One share was sold: Tasty, and;

- No new shares were purchased and no shares were top-sliced.

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

I publish a portfolio review after every quarter (Q1, Q2 and Q3), and this post recaps my October/November/December activity as well as my 2023 performance.

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tristel and M Winkworth.

Q4 share trades

I increased my City of London Investment position by 20% at 320p including all costs.

The purchase was prompted by a scathing AGM statement from the group’s largest shareholder, George Karpus.

Mr Karpus said “this board should be replaced with a seasoned group of directors that understand the enormous potential of CLIG” and, controlling 36% of the votes, his message should trigger positive management actions during 2024.

The fund manager did not enjoy a great 2023. Annual results published during September revealed lower funds under management causing a 29% profit drop. Rising employee costs combined with reduced fee rates squeezed margins further and left the 33p per share dividend barely covered by CLIG’s own 34p per share earnings projection.

Major new clients meanwhile remain elusive while existing clients have endured low single-digit returns during the last five years. Although CLIG’s investment strategies — centred around buying investment trusts at attractive discounts — are sensible, low-risk approaches, they probably require a commissioned salesforce to assist the in-house marketing.

For now I expect to collect a 10% dividend yield while awaiting intervention from Mr Karpus and/or a wider market rebound to support healthy double-digit returns. Net cash and investments at almost $40m should meanwhile limit any short-term operational trouble.

Q4 portfolio news

As usual I have kept watch on all of my holdings. The Q4 developments are summarised below:

- Ordinary dividends up 21% and R&D work referenced in further academic papers at Bioventix.

- AGM protest votes lodged at City of London Investment.

- Fewer mining customers and vanishing construction contracts at Mincon.

- Half-year figures showing property transactions satisfactory gains at Mountview Estates.

- “Weathering the current economic and political storms” with an unchanged H1 profit and dividend from S & U.

- First-half platform revenue up 44% and some intriguing medium-term growth goals at System1.

- Full-year profit up 16% supporting the 21st consecutive annual dividend lift at FW Thorpe.

- A final dividend up 100% and commitment to lift the payout by at least 5% a year announced by Tristel.

- Nothing of major significance from Andrews Sykes and M Winkworth.

I have written a full review of all the shares I held during 2023 — simply click here for the complete run-down.

Full-year review

I always study my portfolio’s performance at the start of every year.

I am keen to discover where my gains and losses occurred during the previous twelve months, and check whether my portfolio decisions have become consistently good, bad or indifferent.

2023 performance

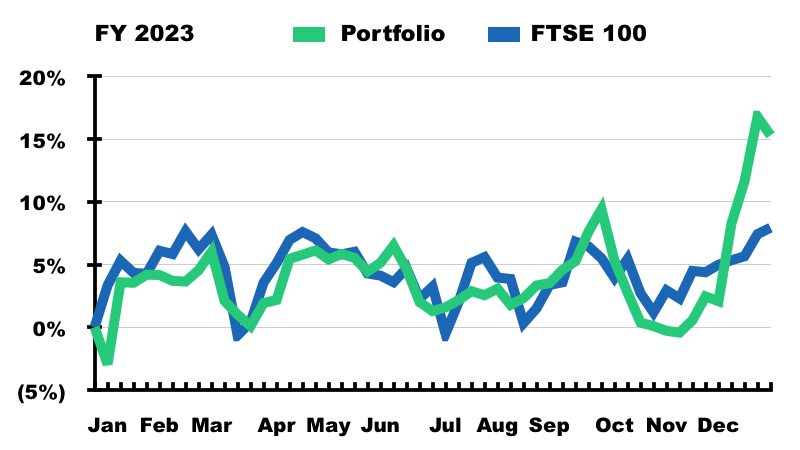

The chart below compares my portfolio’s weekly 2023 progress to that of the FTSE 100 total return index:

I finished up 15.3% versus a 7.9% gain for the UK benchmark. Last year’s positive performance was very welcome given the 23.3% loss I suffered during 2022.

Major factors influencing my 2023 result included:

- One larger holding performing very well: System1 started 2023 at 11% of my portfolio and more than doubled during the year;

- Lower exposure to under-performers: My worst performers, Mincon and Tasty, represented a combined 4% of my portfolio this time last year, and;

- Resilient performances from the rest of my portfolio: My other eight shares all maintained or held their dividends, and their average yearly total return was almost 9%.

2015-2023 performance

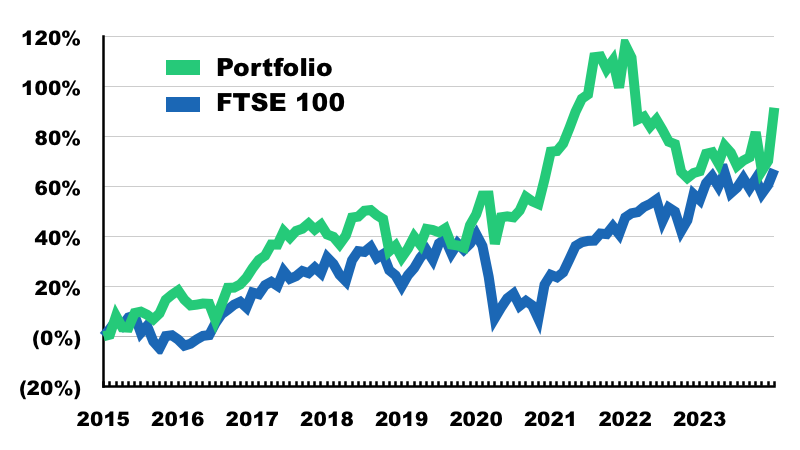

The next chart compares my portfolio’s monthly progress to that of the FTSE 100 total return index. The chart commences from when I became a full-time investor:

I am just about ahead of the FTSE 100 on this nine-year view — up 91% (6.5% per annum) versus up 67% (5.8% per annum).

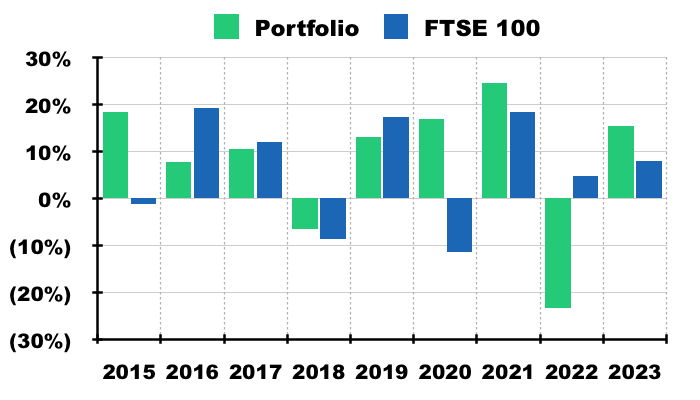

But I have underperformed the UK benchmark during four of those nine years (2016, 2017, 2019 and 2022):

I will let you decide whether my portfolio’s progress makes me a good investor!

Investment returns and attribution analysis

Just to confirm, during 2023:

- I did not buy any new holdings;

- I topped up one holding (City of London Investment (Q4));

- I sold one holding (Tasty (Q3));

- I did not top-slice any holdings, and;

- I left nine holdings untouched (Andrews Sykes, Bioventix, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tristel and M Winkworth).

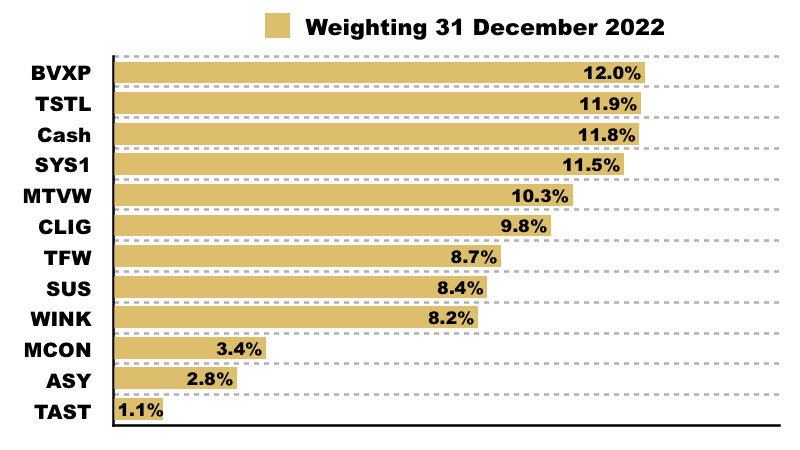

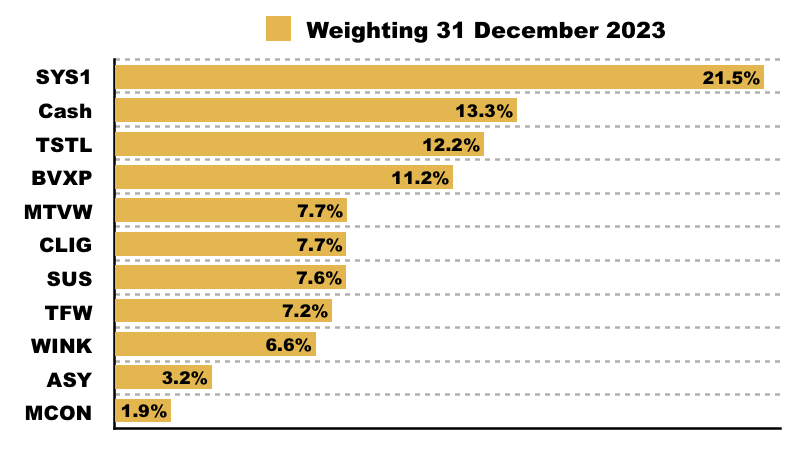

My portfolio started 2023 like this…

…and finished 2023 like this:

This next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding produced for me during the year:

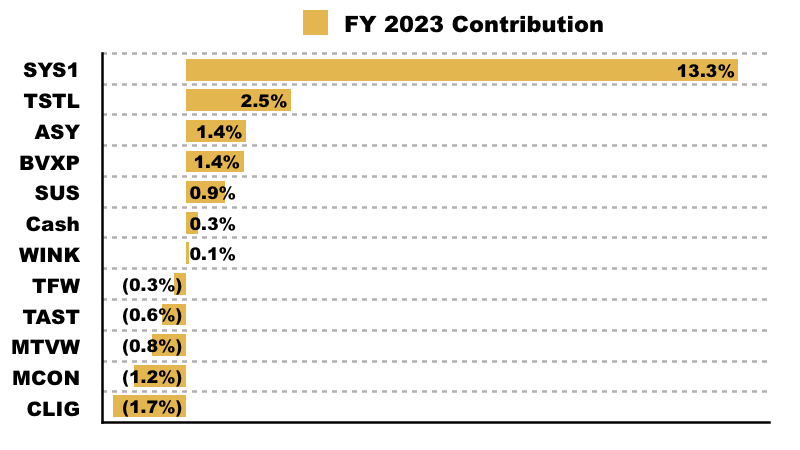

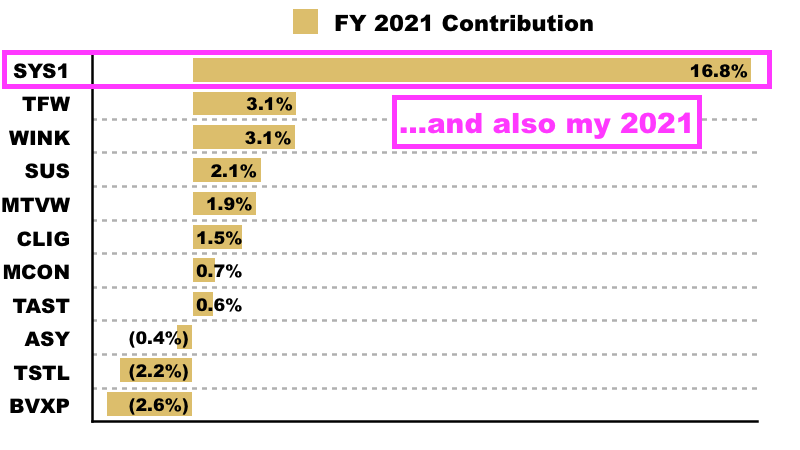

And this chart shows each holding’s contribution towards my overall 15.3% gain:

System1 had an enormous influence on my performance. My portfolio would have gained only 2% had I exited this share at the start of 2023.

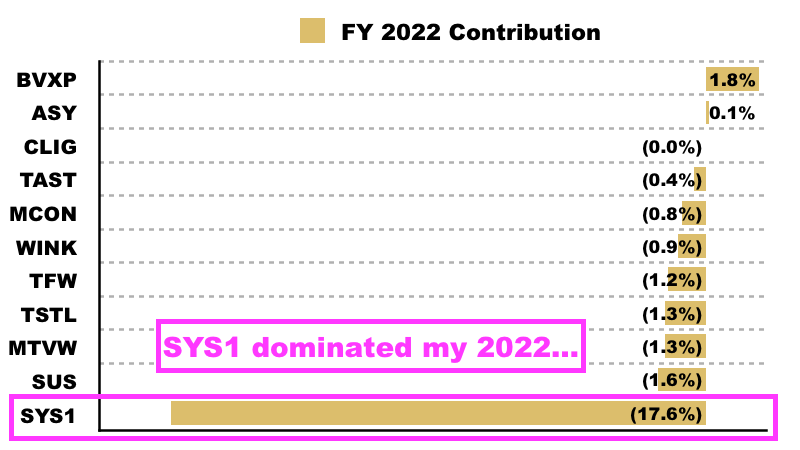

The ups and downs at System1 have dominated my returns during recent years. Some 18 percentage points of my 23% loss during 2022 were due to System1, while some 17 percentage points of my 25% gain during 2021 were also due to System1:

Supported by a bumper special dividend, Andrews Sykes with a 52% total return was my second-best performer of 2023… but sadly its small position size meant the share contributed just 1.4% to my portfolio’s total return.

My performance was helped very slightly by the 13% average cash position held throughout the twelve months. I collected interest at an effective 2.5% after subtracting broker fees and similar.

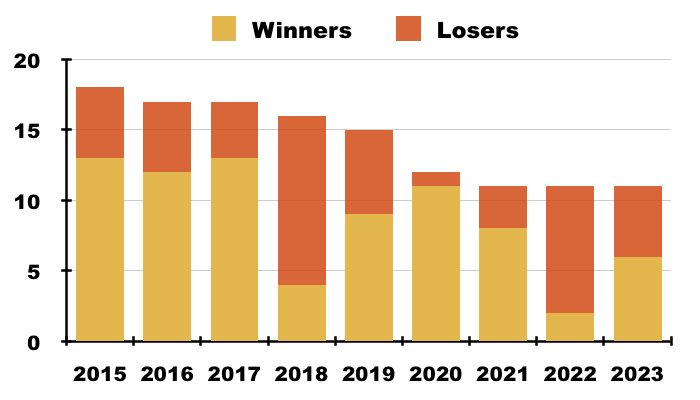

The year saw six of my eleven holdings recording positive total returns:

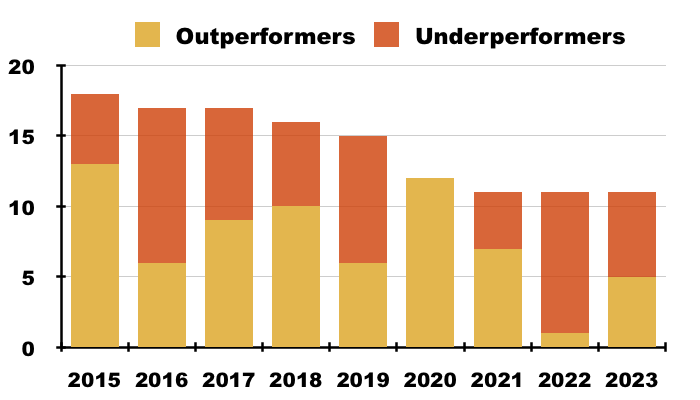

A positive year for the FTSE 100 left only five of my eleven shares beating the index:

Dividends, turnover and costs

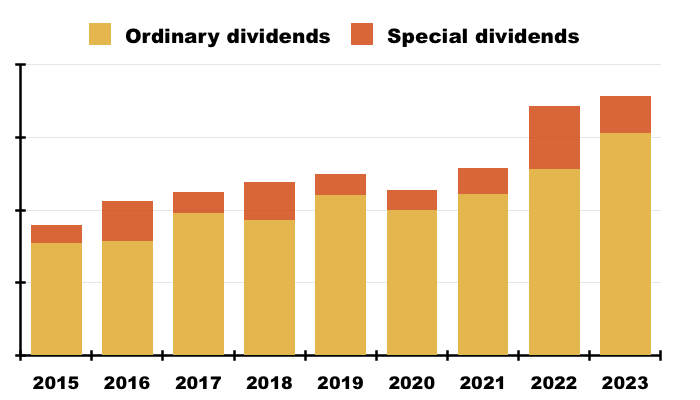

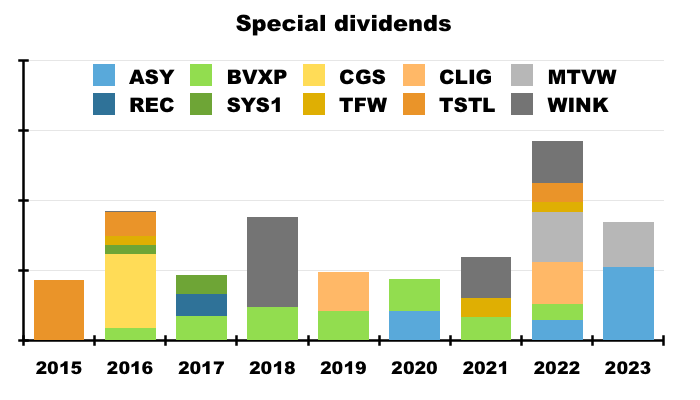

A highlight of 2023 was dividend income. Total payouts advanced 4.1% despite a reduced number of special dividends, and they collectively added 4.1% to my total return:

Last year I received only two special payouts — thank you Andrews Sykes and Mountview Estates — which enhanced my ordinary dividends by 17%. My portfolio has received specials every year since (at least) 2015 and such extra payments have bolstered my ordinaries by 21%:

My ordinary dividends gained 19% last year, which would have been 10% without my top-up of City of London Investment during 2022. I trust the greater dividend income means my portfolio remains in reasonable shape.

Portfolio turnover remained low. I bought and sold shares equivalent to 2.1% of my portfolio’s year-start value.

Trading costs were kept modest. Dealing commissions, stamp duty, foreign-exchange costs and account-management fees represented an aggregate 0.04% of my portfolio’s year-start value.

Summary

So here we go into 2024, with my current investments confirmed below:

Just like 2022, I am starting the year with a significant System1 weighting that will probably dictate proceedings during the next twelve months. Fingers crossed System1 does not repeat its mishaps of 2022!

My next seven shares each represent at least 6% of my portfolio, and all therefore stand a good chance of impacting my 2024 performance.

As usual I have no idea how the market will behave during the next twelve months. But I remain convinced that pinpointing UK small-caps that offer decent accounts, capable managers, respectable prospects and modest valuations remains a sensible long-term approach.

Over time I have noted my portfolio’s encouraging income progress — five of my shares have become ‘dividend baggers‘ — and I now tilt my stock-picking towards healthy payouts. Mind you, total return remains all-important and I still appreciate how multi-baggers can transform a portfolio.

Ambitions for the year ahead are simple:

- Catch up on the huge backlog of results reviews for this blog;

- Find a bargain or two for that 13% cash position, and;

- Attend a few AGMs.

Please click here to read a full review of all the shares I held during 2023.

Until next time, I wish you safe and healthy investing.

Maynard Paton

Excellent summary Maynard. Do you use sharePad for the analytics?

Thanks Michael. I use my own spreadsheet for the charts. I think SharePad can perform some of the analysis, but I was using spreadsheets before SharePad launched and continuing with the same set-up makes things easier for me.

More on SharePad’s portfolio-management facility here:

Hi Maynard

Interesting to note that almost all of the performance came in the last few weeks of the year. I saw something similar in my portfolio and the FTSE 100 and 250, so the Santa rally certainly pulled its weight in 2023.

Even so, I think the UK remains very attractive; we just need some sort of catalyst. I’m tilting towards the idea that it could be buybacks, as these are becoming material at an increasing number of companies and apparently the UK is now the buyback capital of the world.

Anyway, good luck for 2024 and I hope you can sleep well at night with such a huge position in SYS1 !

Happy New Year,

John

Hi John

Yes, I enjoyed an end-of-year spurt — although that was due mostly to SYS1 powering ahead after its December results. I am not entirely convinced UK shares are totally out of the woods yet after interest rates advanced from 1% to 5% in such a short space of time. But valuations are generally pricing in some economic doubt.

I have noticed lots of buybacks appear every morning on the RNS, and I trust the boards are making sensible capital-allocation decisions… there have been plenty of FTSE 100 buybacks that with hindsight were not great for shareholders. I tend to prefer a dividend to a buyback, so I can make my own decision as what to do with the cash!

Best wishes for 2024,

Maynard

(sleeping okay for now)

Hi Maynard,

Entertaining read as always, I’m not sure I could sleep soundly if I had 21.5% invested in a company in which I’d actively campaigned to oust the current management team. From an asset allocation perspective do you still consider SYS1 to be your best idea heading into 2024, its portfolio weighting suggests you do.

I quite like the progress being made and topped up after the trading statement in October which alluded to the company getting fairly close to its FY f/cs in H1 so broker upgrades looked nailed on with the Interims in December.

Still nowhere near 21.5% though ;-)

Hi Patrick

Thanks for the comment. Holding SYS1 in a large way when I voted for the board changes may seem odd, but I get the impression the group’s unhappy investors have sparked some urgency and focus into the business and helped the improved performance. I added heavily during 2020/2021 when Stefan Barden was CEO, and SYS1’s ups and downs since then have dominated my portfolio’s progress. Mr Barden told me, if he became executive chairman, that SYS1 could be sold for £8+/share after three years. That was a bold public statement, and suggests there is some inherent potential in this business. Maybe Mr Barden was being too optimistic, but I am happy to keep the large position and see what occurs. If you view somebody’s largest holding as their ‘best idea’, then yes SYS1 is my best idea!

Maynard

Nice update this morning.

Canaccord upgrade by 50% for FY24 & 58% for FY25 on modest sales increases of 8% & 12% respectively. The operational gearing is very strong here.

We may though start to enter a Stefan Barden overhang situation if he carries out his stated intention of selling down above £4?