14 January 2024

By Maynard Paton

FY 2023 results summary for Tristel (TSTL):

- A positive post-pandemic performance, with strong overseas progress helping FY ‘continuing’ revenue gain 22% and FY profit rebound up to 28% albeit after a bevy of adjustments.

- The FY highlight was a doubling of the final dividend backed by a welcome new policy to increase the ordinary payout by at least 5% a year.

- TSTL revealed ultrasound-probe decontamination supported 33% of group sales and implied a potential 38p royalty per ultrasound disinfection within the United States.

- The accounts showed a record 81% gross margin and net cash recently topping £14m, although restatements continue to occur and audit fees appear unusually steep.

- An estimated 22x P/E for FY 2028 is not an obvious bargain, but a premium rating could be justified by further meaningful growth, lucrative US royalties and the prospect of fresh leadership. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Restatements and audit fees

- Medical-device decontamination

- Surface disinfectants

- UK

- Overseas

- United States

- Patents

- Share options

- Management succession

- Financials: margin and costs

- Financials: balance sheet and cash flow

- Valuation

News links, share data and disclosure

- Annual results, presentation and webinar for the twelve months to 30 June 2023 published/hosted 16 October 2023, and;

- AGM statement published 19 December 2023.

- Share price: 425p

- Share count: 47,419,693

- Market capitalisation: £202m

- Disclosure: Maynard owns shares in Tristel. This blog post contains SharePad affiliate links.

Why I own TSTL

- Develops the “simplest, quickest and most affordable high-performance disinfection” for medical devices, which face limited direct competition due to proprietary chemistry, instrument-manufacturer approvals, scientific testimonies and regulatory hurdles.

- Enjoys a track record of superior growth founded upon a sizeable and resilient UK market position, alongside continuing expansion opportunities abroad including the United States.

- Boasts financials that showcase super gross margins, significant net cash, respectable cash conversion and relatively low operational capital.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary

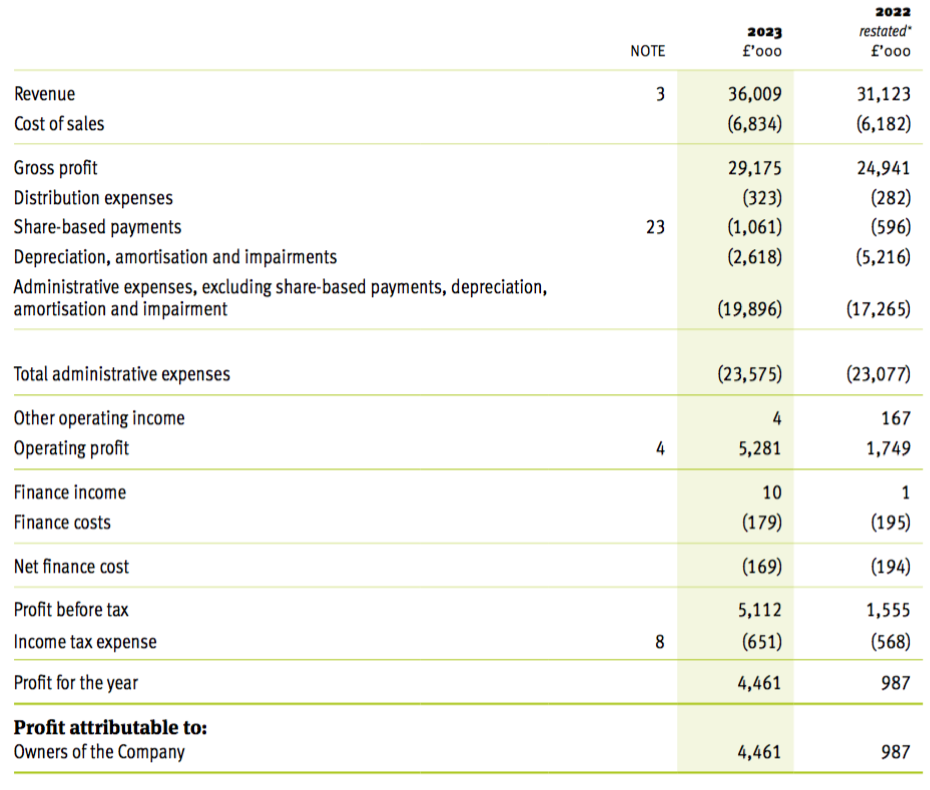

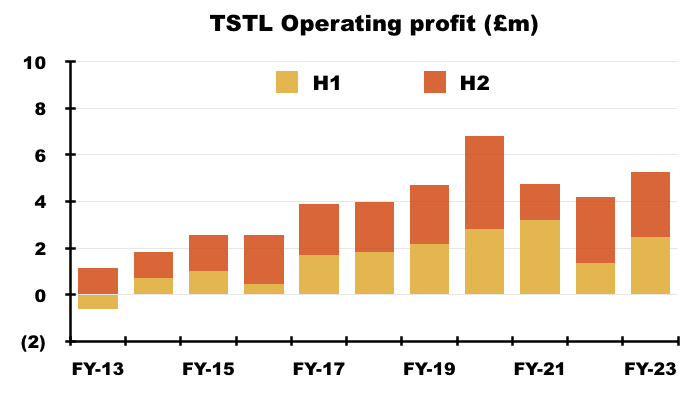

Revenue, profit and dividend

“Demand for Tristel’s infection prevention products for medical device decontamination and for the sporicidal disinfection of surfaces continues to be very robust across all key geographical markets.

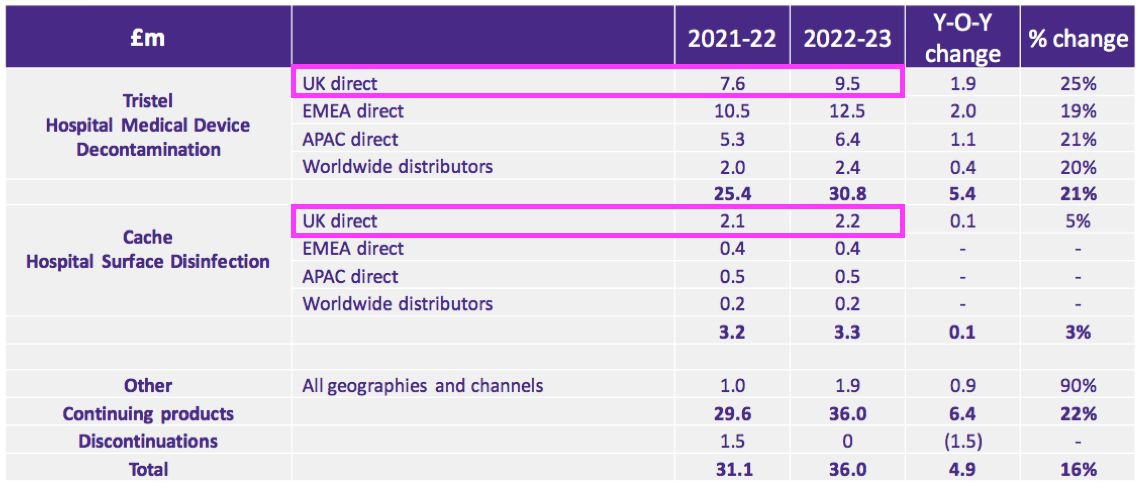

As a result, revenues for the year were up 16% to £36.0m (FY 2022: £31.1m), ahead of consensus forecasts and above the Company’s long-term target for revenue growth. Adjusted profit before tax (adjusted for share-based payments) will be slightly ahead of consensus forecasts of £6m. Tristel continues to be debt free and cash generative. Cash balances on 30 June 2023 were £9.5m (30 June 2022: £8.9m).“

- …had already signalled encouraging FY 2023 progress.

- This FY confirmed the headline figures heralded at July’s open day, with FY revenue at £36.0m, FY adjusted pre-tax profit at £6.2m and the cash balance at £9.5m.

- TSTL’s top-line comparisons were complicated by:

- Brexit stock-piling, which generated extra revenue of £0.9m during H1 2021 that would have otherwise been earned during the comparable FY 2022, and;

- The “discontinuation of several low-growth product lines“, which TSTL said contributed revenue of £1.5m during the comparable FY 2022 but which contributed zero for this FY.

- TSTL said revenue growth excluding the discontinued products was 22%:

- Revenue excluding discontinued products and with the Brexit stock-piling reversed gained 18%.

- Revenue without any adjustments for discontinued products nor Brexit stock-piling gained 16%.

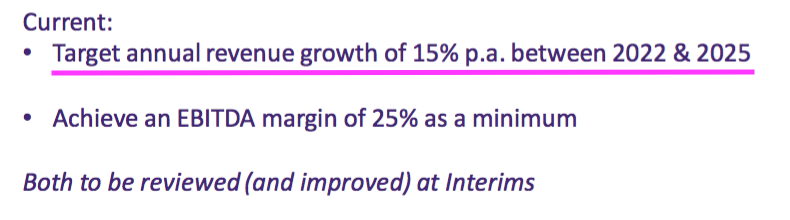

- The 16%, 18% and 22% revenue advances exceeded the 15% target touted during July’s open day:

- TSTL develops wipes and foams that decontaminate diagnostic medical instruments such as nasendoscopes, ultrasound probes and tonometers, and the number of procedures involving such instruments reduced during FYs 2021 and 2022 as hospitals became overwhelmed by Covid-19 matters.

- The pandemic disruption appears to have now passed after this FY referred to a “normalised marketplace“:

“During 2023 the negative impact on our business of both Brexit and COVID-19 receded and we resumed both top and bottom-line growth. We now have a normalised marketplace in all 40 countries in which we operate…”

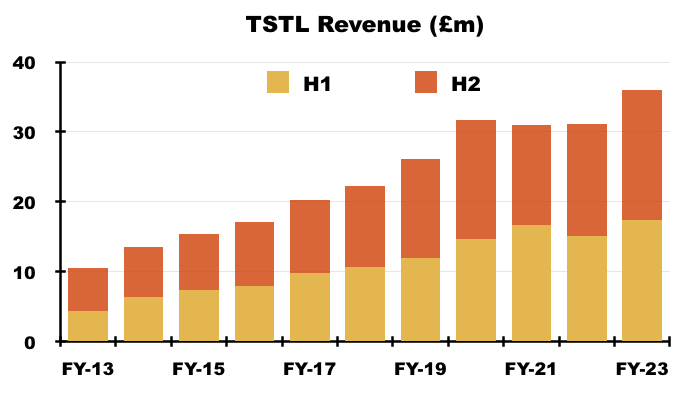

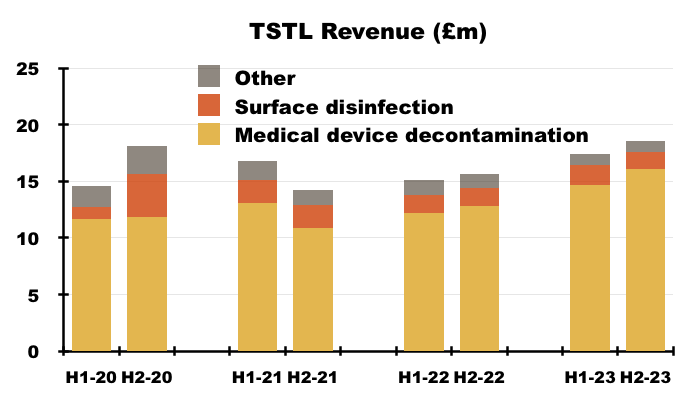

- H2 comparisons were not disturbed by Brexit stock-piling nor discontinued products. H2 revenue advanced 16% to £18.5m to set TSTL’s best ever six-month sales performance:

- TSTL commendably split revenue growth between volume, pricing and currency movements:

“Of the total sales increase of £4.9m, £2.8m can be attributed to growth in the volume of product sold, £1.4m to price increases and £0.7m to favourable currency movements. Volume increases come from international expansion, such as new distributor markets, increased roll-out of product within existing customer sites, and the acquisition of new customers. All of these applied during the year.“

- Higher prices and currency movements had a greater influence on H2 revenue growth than H1.

- The preceding H1 had reported…

“We have increased our prices to hospitals in response to global inflation. Of the increase in revenue of £2.4m, £1.8m relates to additional volume and £0.6m to pricing, which reflects a 4% global price rise. “

- …which implies H2 revenue growth of £2.5m was supported by:

- Additional product volume of £1.0m versus £1.8m for H1;

- Higher product prices of £0.8m versus £0.6m for H1, and;

- Currency movements of £0.7m versus zero for H1.

- TSTL said product prices were increased 4.5%.

- TSTL’s profit progress remains difficult to analyse.

- As well as the Brexit stock-piling and discontinued products, FY profit comparisons were complicated by TSTL’s usual:

- Share-based payments (see Share options), and;

- Costs associated with the US regulatory submission (see United States).

- Discontinued-product write-offs totalling £2.4m and other operating income of £162k (relating to chemical-data fees and formulation transfers) during the comparable FY also influenced the comparison.

- Including every operating credit and charge, the comparable FY £1.7m operating profit was transformed into an FY £5.3m operating profit.

- Excluding the discontinued-product write-offs, FY operating profit went from £4.2m to £5.3m:

- Excluding the discontinued-product write-offs, share-based payments, estimated US costs and other operating income:

- FY operating profit improved 28% from £5.4m to £6.9m;

- H2 operating profit improved 27% from £2.7m to £3.5m, and;

- H2 operating profit improved less than 1% on the preceding H1 operating profit:

- Albeit blighted by adjustments and guesswork, these FY figures do suggest ‘underlying’ profit was TSTL’s highest for any year aside from the pandemic-boosted FY 2020 (£7.1m).

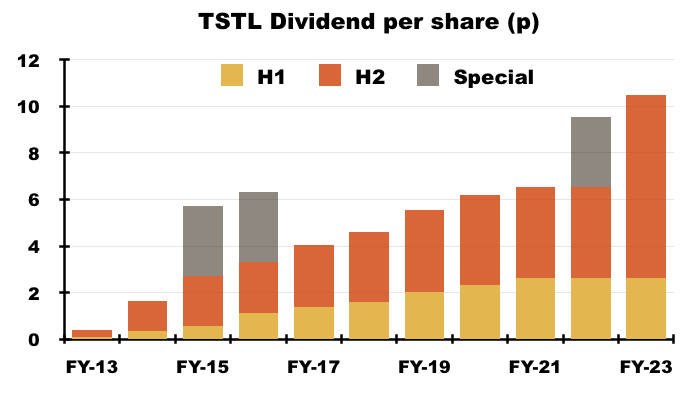

- At least the dividend was not subject to any interpretation. The payout in fact provided the highlight of this FY.

- July’s open-day commentary disclosed the dividend policy was under review:

“The board is currently considering increasing our dividend payout ratio and that is something that we will report back to you when a decision has been made“.

- This FY revealed the ordinary dividend will now advance by at least 5% a year:

“Going forward the Board’s intention is to increase the dividend annually in line with the year’s increase in EPS, committing to minimum dividend growth of 5%.”

- Committing to any level of minimum dividend growth is a bold step for a quoted company. But TSTL has consistently issued three-year revenue and margin targets since FY 2015, and the board therefore ought to be confident about the additional dividend guidance (see Valuation).

- Mind you, the chief executive declaring the new dividend policy has since announced he will retire before the end of this year (see Management succession). I would like to think the new boss will retain the same payout-growth commitment.

- The final dividend was lifted a very welcome 100% to 7.88p per share:

- The total FY dividend of 10.5p per share was covered just 1.02x by TSTL’s 10.7p per share adjusted-earnings calculation.

Restatements and audit fees

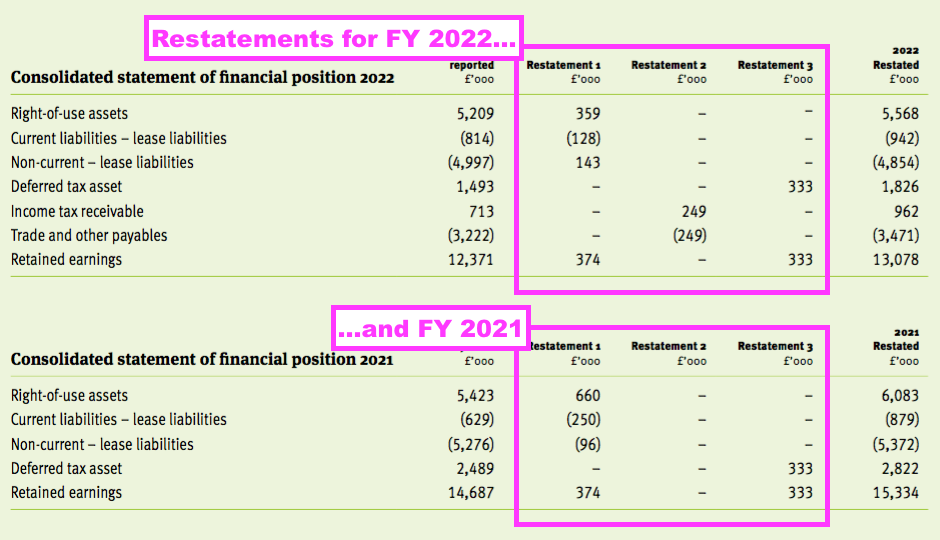

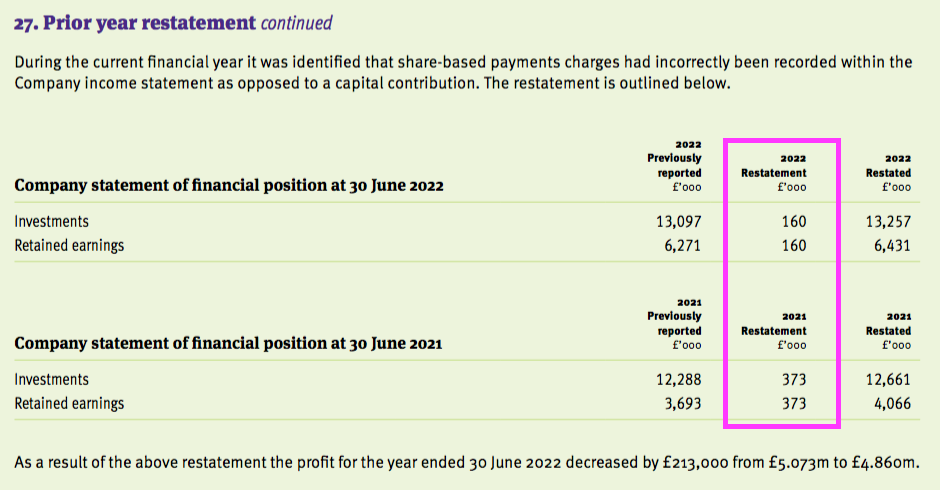

- This FY was the second consecutive FY to reveal a prior-year restatement.

- A handful of minor revisions for the comparable FY 2022 were disclosed:

“Restatement 1

During the current financial year the Group adopted a suite of lease accounting software. The software has outlined the need for a restatement of the financial position of prior years which is detailed below. These differences emerged from varying discount rate applications and omitted leases, which in current year have been supplied by an independent third party due to the lack of borrowing within the Group and rectified respectively…

Restatement 2

During the current financial year it was identified that a corporate tax receivable balance had incorrectly been recorded as a sales tax payable in the prior year…

Restatement 3

During the current financial year it was identified that no adjustment had previously been made for the tax effect of unrealised intra-group profits…“

- The restatements also necessitated minor changes to FY 2021:

- TSTL also incorrectly recorded its share-based payment expense within the last two sets of parent-company accounts:

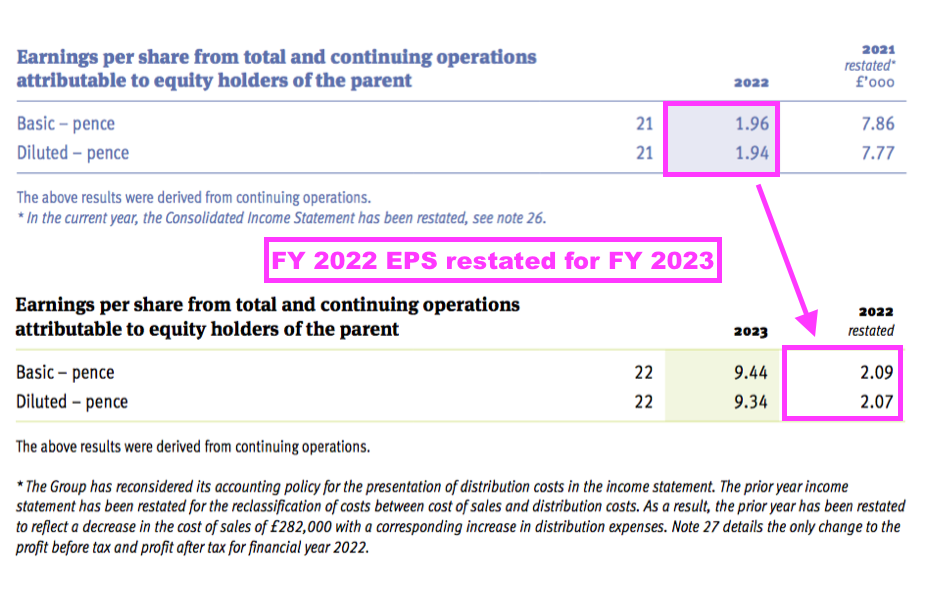

- The restatements meant FY 2022 earnings that were originally declared as 1.96p per share were revised 7% higher to 2.09p per share:

- The comparable FY 2022 had also revealed a prior-year restatement (for FY 2021):

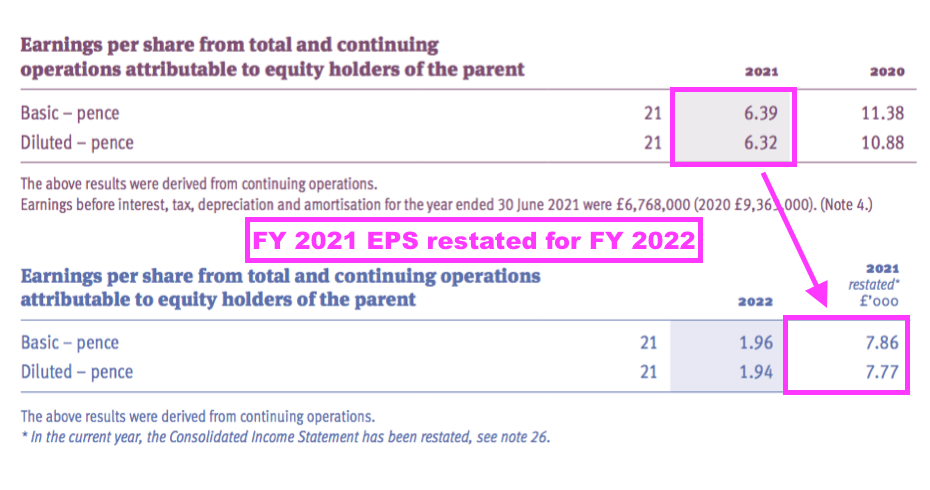

“During the current year, it was identified that deferred tax assets relating to unrecognised taxable losses of £3,600,000 in the UK had not been recognised in the prior year. Based on the circumstances in the prior year, these should have been recorded as a deferred tax asset at 19%, equating to £684,000. The prior year financial statements have been restated for this adjustment. In addition, in the prior year an income tax receivable for £170,000 was inappropriately classified as an income tax liability. The prior year comparatives have been restated to correctly reclassify the balance as an income tax receivable.”

- FY 2021 earnings that were originally declared as 6.39p per share were then revised 23% higher to 7.86p per share because of a much lower tax charge:

- The run of restatements meant net asset value for FY 2021 that was declared initially as £30,083k was restated to £30,767k during FY 2022 and then restated again to £31,414k for this FY.

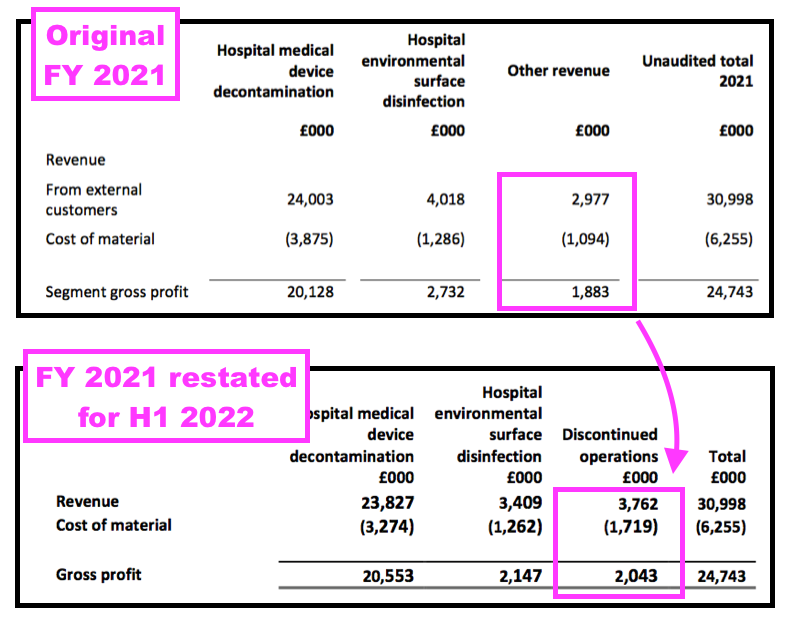

- The run of restatements coincides with TSTL deciding to distinguish between continuing operations and discontinued operations for H1 2022, which prompted the restatement of FY 2021’s divisional performances:

- However, TSTL was subsequently instructed by its auditor, KPMG, to ditch the continuing/discontinued reporting and revert back to the original format for the next set of results. The finance director said at the time:

“We believed in February that we were reporting a discontinued operation and the accounting policy around it we thought we satisfied, which was that… there was a whole division… that we were ceasing. But our auditors have told us they viewed it differently, so it’s not appropriate. It’s a pure accounting decision by KPMG… which I’m actually really disappointed about, because I thought it was really simple and straightforward to restate… It was a huge blow. We were very disappointed not to be able to demonstrate it in that way.“

- None of restatements during the last few years has been individually material. But the revisions continue to rack up and shareholders are right to question whether:

- Earnings per share and other figures within this FY will be revised for FY 2024, and;

- TSTL’s accounting function has struggled to cope with the group’s expansion.

- After being instructed by KPMG to ditch the continuing/discontinued reporting, TSTL appointed Grant Thornton as the group’s auditor for this FY:

Reappointment of auditors:

“Grant Thornton UK LLP is the Company’s auditor having been appointed for the first year on the 6 December 2022. In accordance with section 485 of the Companies Act 2006, a resolution for the re-appointment of auditors of the company is to be proposed at the forthcoming Annual General Meeting.“

- The 2023 annual report claimed TSTL’s audit committee considered the “value for money” provided by KPMG and Grant Thornton:

“During the 2022-23 year the Audit Committee met on two occasions to:

• Discuss findings and hear recommendations arising from the annual audit

• Discuss with the Company’s external auditors matters such as compliance with accounting standards

• Monitor the external auditorsʼ compliance with relevant ethical and professional guidance on the rotation of audit partners, the level of fees paid by the Company and other related requirements

• Consider the performance and value for money of the Company’s external auditors

• Approve the appointment of the Company’s external auditors, including their terms of engagement and fees“

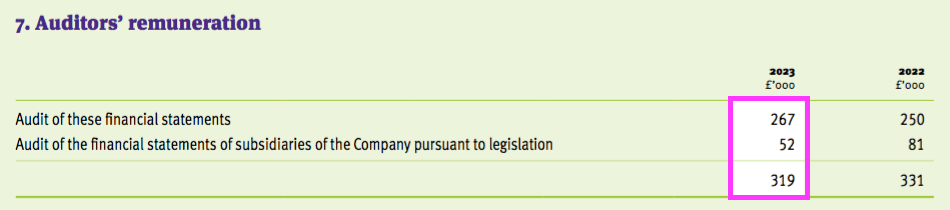

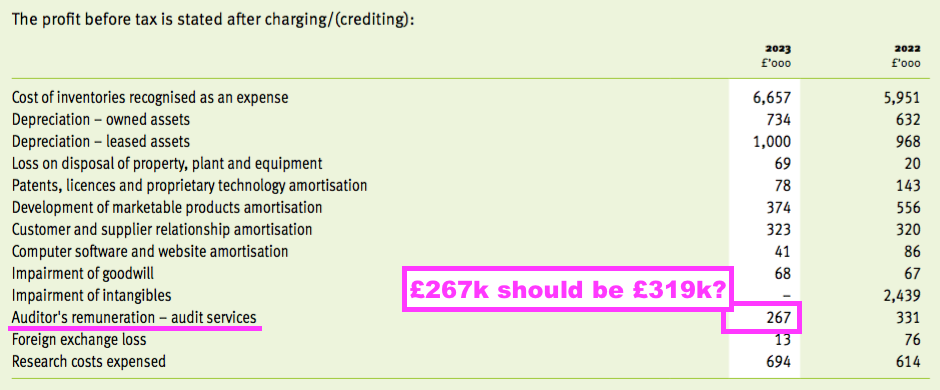

- Total audit fees for this FY 2023 were £319k…

- …although the accounting notes were inconsistent:

- Audit fees of £319k absorbed 0.89% of FY revenue, which is the largest proportion within my portfolio:

| Company | Year to | Revenue (£k) | Auditor | Fees (£k) | Fees/ Revenue |

| ASY | 31-Dec-22 | 83,007 | Mazars | 251 | 0.30% |

| BVXP | 30-Jun-23 | 12,816 | Kreston Reeves | 25 | 0.20% |

| CLIG | 30-Jun-23 | 57,326 | RSM | 193 | 0.34% |

| MCON* | 31-Dec-22 | 170,008 | Grant Thornton | 225 | 0.13% |

| MTVW | 31-Mar-23 | 73,593 | BSG Valentine | 75 | 0.10% |

| SUS | 31-Jan-23 | 102,714 | Mazars | 163 | 0.16% |

| SYS1 | 31-Mar-23 | 23,410 | RSM | 117 | 0.50% |

| TFW | 30-Jun-23 | 176,749 | PwC | 374 | 0.21% |

| TSTL | 30-Jun-23 | 36,009 | Grant Thornton | 319 | 0.89% |

| WINK | 31-Dec-22 | 9,307 | Crowe | 69 | 0.74% |

(*figures in euros)

- I note Mincon employs the Dublin branch of Grant Thornton for its audit, but pays less for auditing than TSTL despite generating four times as much revenue.

- I am therefore not clear how TSTL’s audit committee decided whether the change of auditor delivered “value for money“.

- The chief executive has announced he will retire later this year, and maybe a change of other board members — rather than a change of auditor — is also required given the run of accounting restatements (see Management succession).

Medical-device decontamination

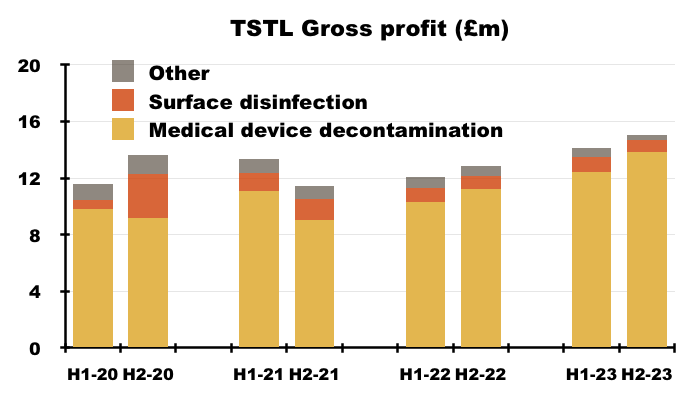

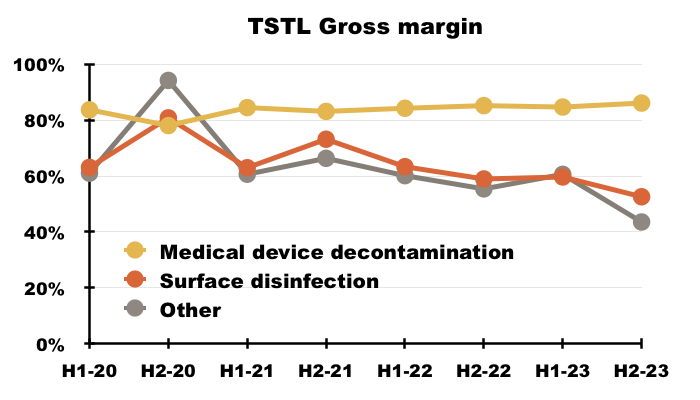

- TSTL’s wipes and foams that decontaminate medical devices remain by far the group’s most successful products:

- During H2, 87% of revenue and 92% of gross profit were generated from the wipes and foams:

- TSTL’s surface disinfectants meanwhile contributed approximately 8% of revenue and 5% of gross profit during H2.

- Approximately 4% of TSTL’s business is derived from Other revenue, which represents a variety of legacy products that escaped the H1 2022 cull.

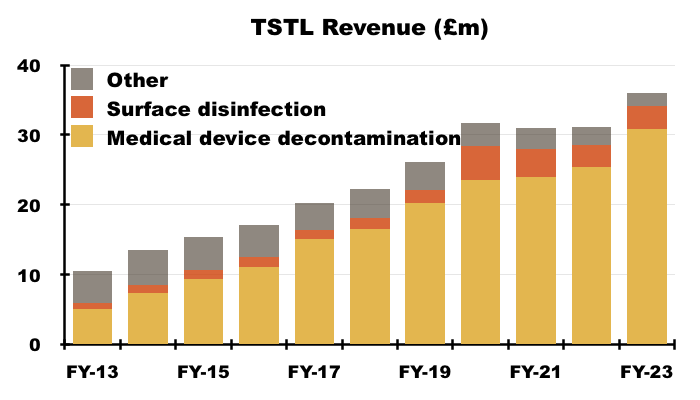

- FY revenue from the medical-device wipes and foams improved 21% to £30.8m, with a 22% advance to £16.1m enjoyed during H2.

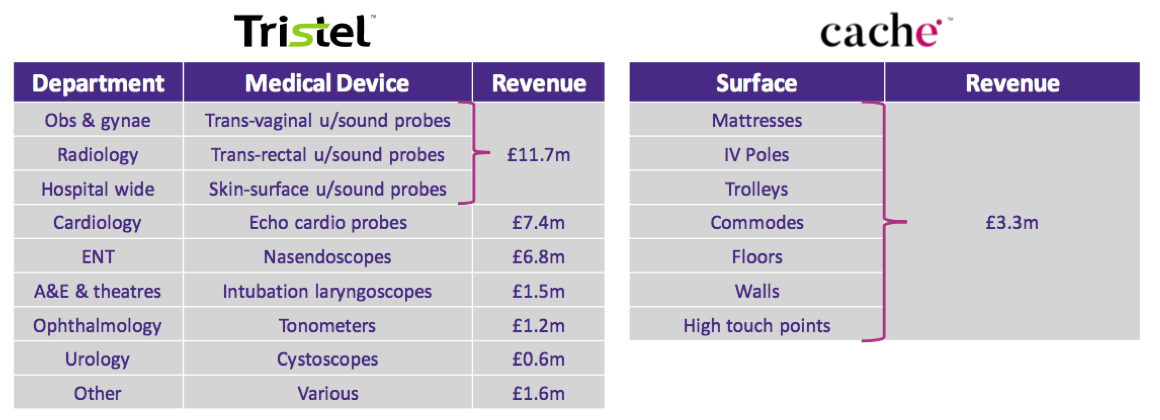

- TSTL helpfully provided a breakdown of revenue generated by various kinds of medical device:

- Decontaminating ultrasound probes represented £11.7m or 38% of medical-device revenue (and 33% of total revenue).

- However, last year’s FDA-approval RNS suggested the figure was closer to 50%:

“Approximately half of Tristel’s global revenue is generated from the ultrasound market.“

- Last year’s FDA-approval slides indicated TSTL products handled 5.8 million ultrasound procedures…

- …implying revenue per ultrasound procedure was £11.7m / 5.8 million = £2.02.

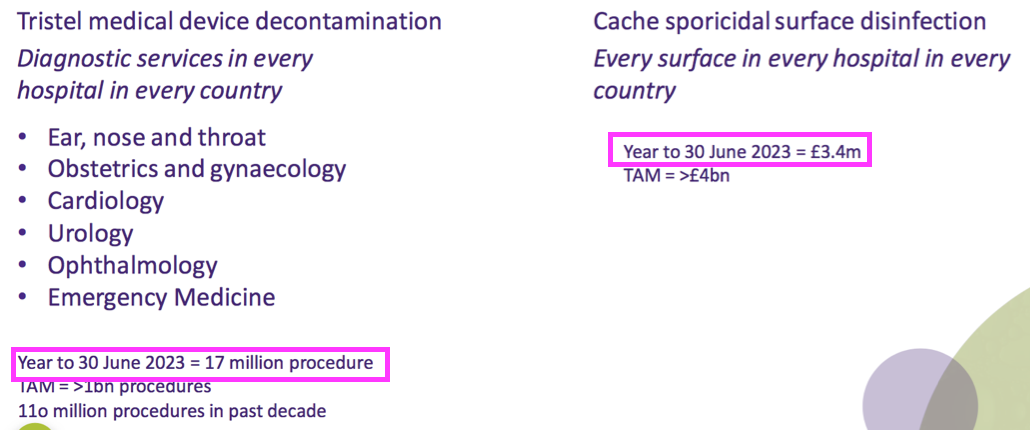

- July’s open day indicated TSTL products handled 17 million medical procedures…

- … implying revenue per medical procedure of £30.8m / 17 million = £1.81.

- Revenue per procedure (and in particular, per ultrasound procedure) can help shareholders gauge the market potential of the United States (see United States).

- Decontaminating 17 million medical devices during this FY compares to 15.7 million disinfections using a TSTL wipe or foam during FY 2022 and 12 million for FY 2019:

- Revenue per disinfection for FY 2022 was therefore £1.62 (£25.4m / 15.7 million) and for FY 2019 was £1.73 (£20.8m / 12 million).

- My online searching shows TSTL’s Trio Wipes System available to buy for £363 (before VAT) and its Duo ULT foam available to buy for £251 (before VAT).

- The Trio Wipes System contains enough wipes to conduct 50 disinfections and therefore costs the purchaser £7.26 per disinfection (£363/50). The Duo ULT foam gives 310 doses — equivalent to 155 disinfection procedures — and therefore costs the purchaser £1.62 per disinfection (£251/155).

- TSTL’s income will be less than £7.26 or £1.62 per disinfection because of the gross margin enjoyed by the retailer selling the wipes and foams.

Surface disinfectants

- FY revenue from TSTL’s surface disinfectants advanced 4%, with the 14% H1 improvement negated by a 6% reversal during H2:

- H2 surface-disinfection revenue of £1.5m was the lowest six-month contribution from the division since H1 2020 (£1.1m).

- TSTL referred to regulatory backlogs for delays to launching new surface products:

“Our second product range, Cache, made much slower progress during the year. Revenue was £3.3m compared to £3.2m in the previous year. Part of the new Cache range is still in the product design and testing stage, and the part of the range which is ready to be actively marketed is waiting for regulatory approvals in key markets.

In Europe, CE marking is required for medical device disinfectants, and while the Cache product range is intended for environmental surfaces, many of the surfaces around the patient are considered medical devices requiring CE marking as well as approval under the European Biocidal Products Regulation. Post Brexit, the UK introduced UKCA Marking Certification for medical devices, and we are waiting to receive UKCA approval for the new Cache products.”

“Our Cache products consist of legacy products, which are a chlorine-dioxides trigger spray that we brand Jet and a chlorine-dioxide burstable sachet [called Fuse], which brings the two pairs of the chemistry together, and can be diluted into five litres of water and can then be used for mopping. They make up the £3.3m of Cache revenue that exist at the moment.”

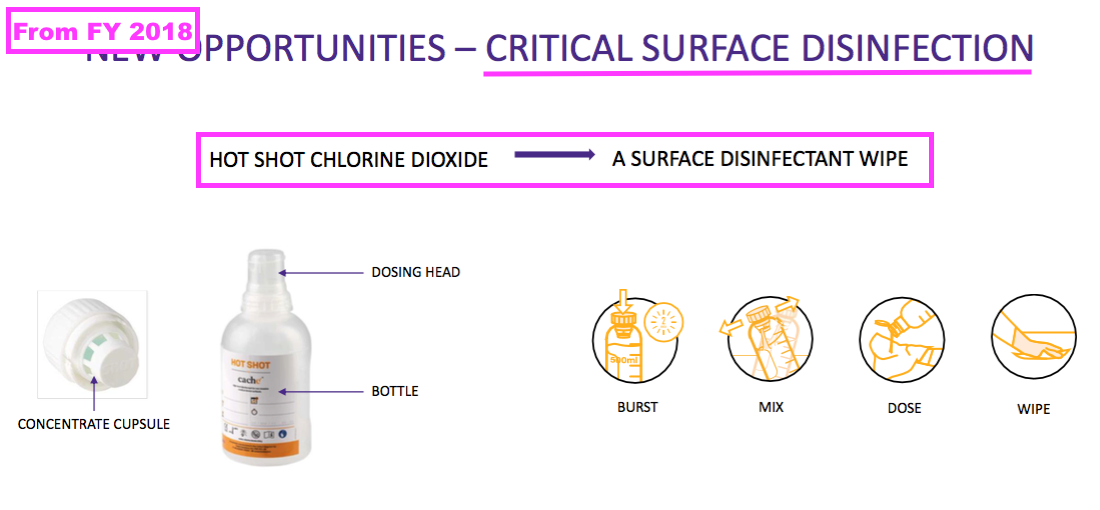

- Management’s FY webinar confirmed the new surface products to be Tank and Shot:

“Our new product range, which is going through UK CA marking at the moment, and also CE marking, is the range of products that we refer to as Tank and Shot“

- Development of the new surface disinfectants has been slow going. Shot for example has been in development since at least H1 2018. From my notes at the time:

“The presentation slides referred to a new product called Shot. Essentially it is a bottle with a clever ‘dosing head’ that allows a TSTL disinfectant capsule to be mixed with exactly 10ml of water.“

- Management’s FY webinar claimed the new surface products could one day generate sales equal to those of the medical-device disinfectants:

“Where do we think this product can take us? The use of a surface disinfectant within a hospital is enormous. Every surface within a hospital will be disinfected, will be mopped or wiped, … so we certainly believe we can equal the revenue we are achieving within our Tristel product range of medical-device decontamination products with our Cache range.”

- Surface-disinfection revenue would have to grow more than nine times to equal the present revenue from medical-device decontamination.

- From what I can tell, TSTL’s surface disinfectants have in the past struggled to take off due to their higher pricing versus less effective alternatives. Management’s FY webinar confirmed the new products would be priced at the same level:

“The performance of the chemistry. It’s an extremely powerful biocide. It kills all pathogens of concern and it kills them very very quickly. And in the process of doing that the chemistry itself is extremely safe. So you can dip your hand in a bucket of solution and it won’t harm you at all… And of course we can deliver the chemistry at a price the incumbent low-level disinfectants are charging within the hospital… We are very hopeful for the Cache range.”

- Management’s FY webinar also indicated regulatory approvals for Tank and Shot ought to be received during the current FY 2024:

“These approvals have taken longer than originally anticipated but we are confident that the majority will be secured in the current financial year, giving us the opportunity to deliver significant growth in sales of this product range going forward.“

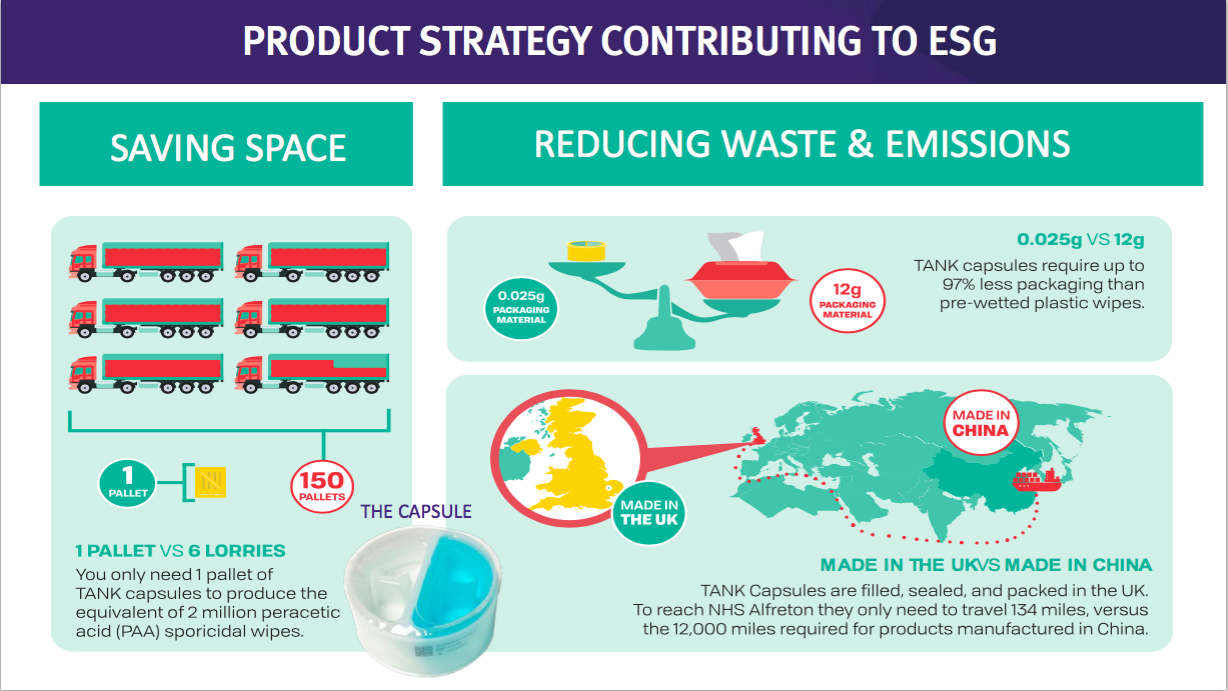

- This TSTL website showcases the surface disinfectants and their environmental credentials versus pre-wetted plastic wipes:

- The drawback to surface disinfectants for shareholders may be their significantly lower price point compared to the medical-device wipes and foams.

- Management’s presentation comments from FY 2018 suggested the NHS was purchasing low-grade surface wipes at 2p a pop.

- Assuming TSTL price-matches that 2p, enormous volumes will be needed for surface disinfectants to represent a notable proportion of TSTL’s business.

- This FY claimed the size of the surface-cleaning market was “far greater” than the medical-device decontamination market:

“The cleaning and disinfection of environmental surfaces in hospitals is ubiquitous and the global expenditure by hospitals on surface disinfection is far greater than the expenditure on decontaminating medical devices.”

- In theory at least, a much more effective surface cleaner that is priced identically to low-grade plastic wipes — as well as being much more environmentally friendly — ought to have a big future:

- Mind you, TSTL promoting the environmental benefits of its surface disinfectants against pre-wetted wipes does raise the question about the environmental impact from the plastic wipes used with the group’s Trio Wipes System.

UK

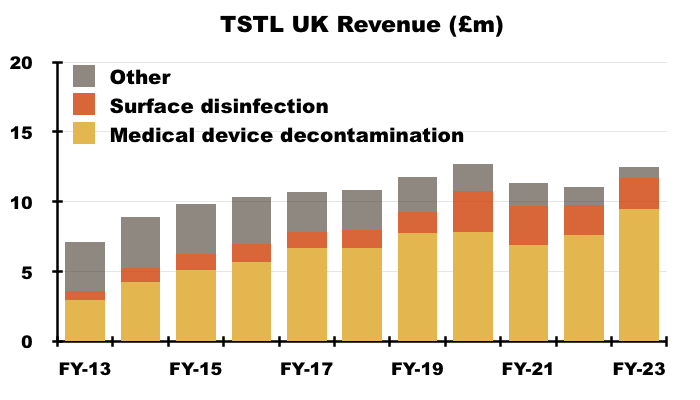

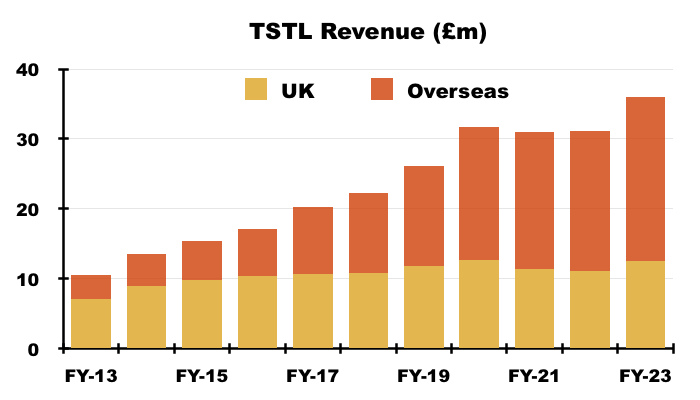

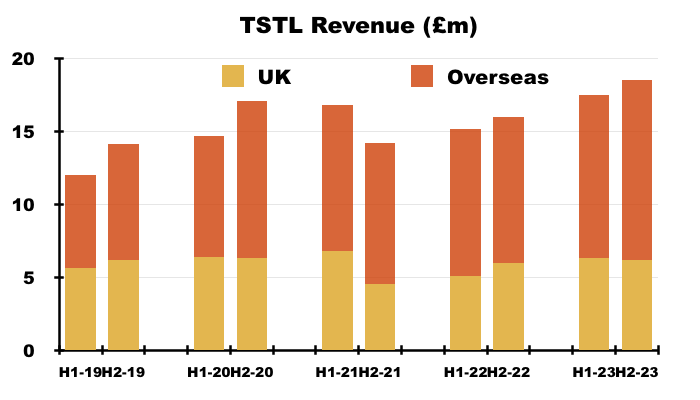

- The UK remains TSTL’s largest individual market, with total FY revenue gaining 13% to £12.5m:

- UK progress has in the past been influenced by sales of now-legacy/now-discontinued ‘Other’ products. The aforementioned Brexit stock-piling also distorted the UK revenue comparison for this FY.

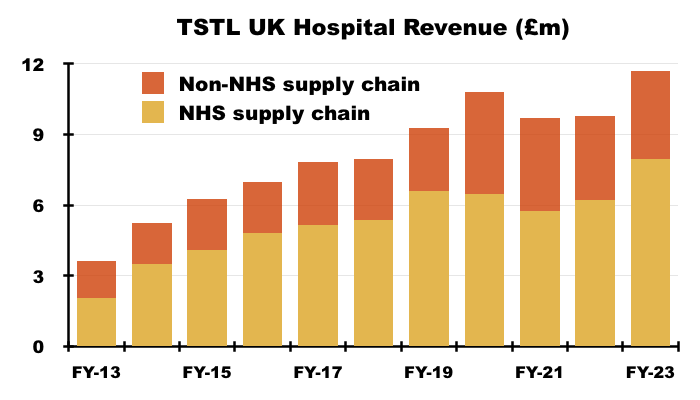

- TSTL’s FY presentation showed UK hospital-disinfection sales gaining 21% from £9.7m to £11.7m:

- Add back the Brexit stock-pile revenue of £0.9m to the comparable £9.7m, and ‘underlying’ UK hospital revenue gained 10% during this FY (£11.7m/£10.6m).

- UK hospital revenue of £11.7m was £1.1m greater than the previous high set during FY 2020.

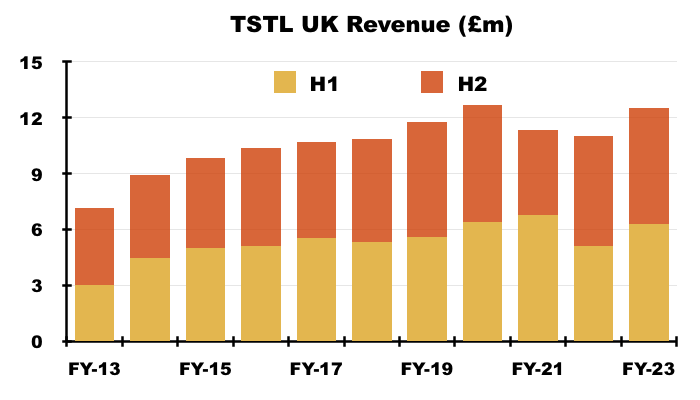

- Total UK sales were split £6.3m during H1 and £6.2m during H2:

- Total UK sales during H2 gained only 4% on the comparable H2, which I think was due to lower sales of surface disinfectants and/or legacy products.

- UK revenue has progressively become a smaller part of TSTL as the group expanded overseas through deft purchases of international distributors (see Overseas):

- UK revenue represented 35% of total revenue during this FY and 34% during H2.

- UK revenue includes sales to the NHS Supply Chain, which has always dominated UK hospital-disinfection income and, alongside Brexit-stock-piling, has in the past led to unpredictable orders and bulk purchases to create some inconsistent UK performances.

- The Supply Chain represented 22% of total revenue during this FY:

“Hospital medical device decontamination revenues were derived from a large number of customers but include £6.133m from a single customer in the UK which makes up 20% of this product category’s revenue (2022: £4.572m, being 18%). Hospital environmental surface disinfection revenues were derived from a number of customers but include £1.82m from a single customer in the UK which makes up 55% of this product category’s revenue (2022: £1.636m, being 51%)… During the year 22% of the Group’s total revenues were earned from a single customer (2022: 20%). “

- Revenue earned from the Supply Chain represented 68% of this FY’s UK hospital-disinfection revenue, which was within the 60%-71% range witnessed during the last ten years:

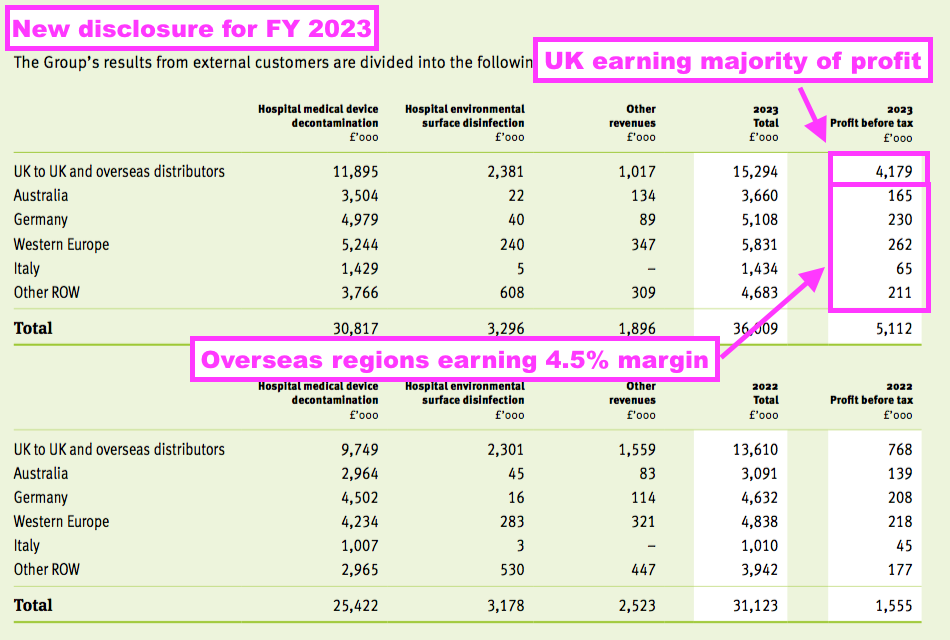

- This FY revealed segmental profit for the UK and other sales regions:

- A UK pre-tax profit of £4.2m represented 82% of group pre-tax profit, despite UK sales representing 35% of total revenue.

- Management’s FY webinar explained the UK profit bias, citing the group’s “transfer pricing policy” and wishing to “achieve the best tax profile“.

- All TSTL’s manufacturing occurs in the UK, and the products are sold to the group’s overseas divisions on an ‘arm’s length’ basis for resale within their respective markets.

- TSTL therefore records all of its ‘manufacturing profit’ within the UK.

- Management’s FY webinar noted all the overseas sales regions have their profit margin set at 4.5%.

- Total UK revenue of £12.5m still provides a good benchmark for the sales potential of other countries…

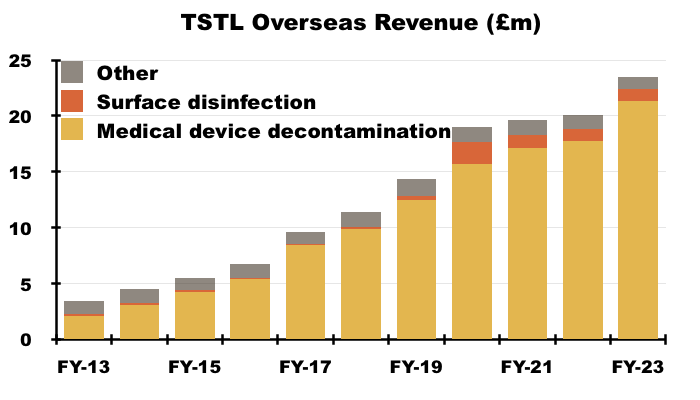

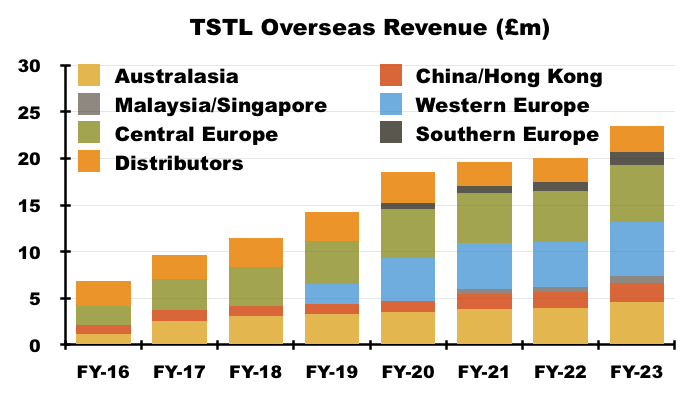

Overseas

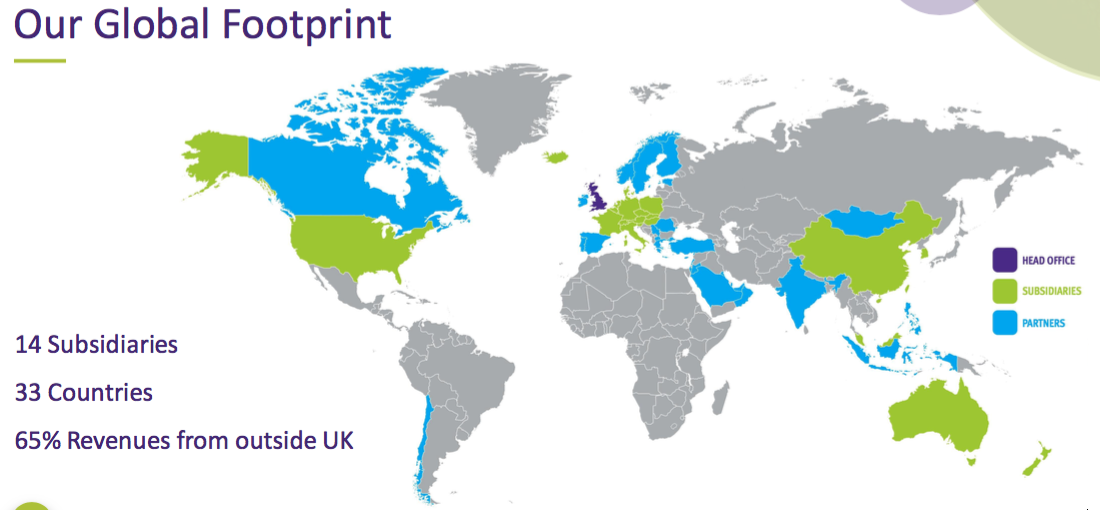

- Overseas revenue is derived from a mix of direct operations and independent distributors that combine to sell within more than 30 countries:

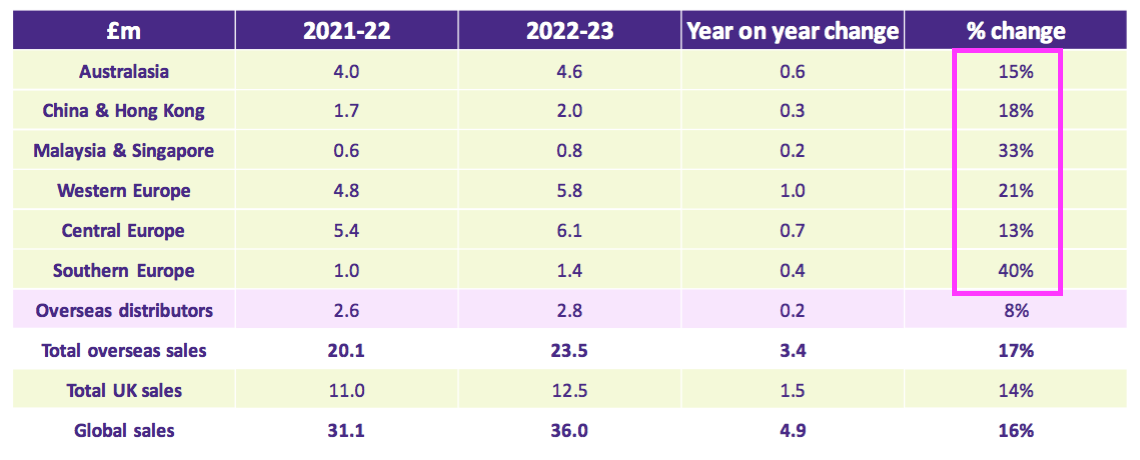

- Overseas revenue climbed 17% to £23.5m during this FY:

- Overseas sales of the ‘core’ hospital-disinfection products climbed 19% to £22.4m.

- H2 was stronger than H1 for the overseas division:

- H2 overseas revenue of £12.3m was up 10% on the preceding H1 and up 22% on the comparable H2.

- TSTL’s overseas subsidiaries all registered double-digit FY revenue progress:

- Overseas distributor revenue advanced only 8%, although TSTL has over time acquired a number of distributors and those that remain independent may not be such attractive operators.

- TSTL acquired:

- I calculate:

- Australasian sales (i.e. Australia and New Zealand) have since climbed 111% from approximately AU$3.9m to approximately AU$8.2m (seven-year CAGR: 11%);

- Western Europe sales (i.e. Belgium, Netherlands and France) have since climbed approximately 123% from €3.1m to approximately €6.8m (five-year CAGR: 17%), and;

- Southern Europe sales (i.e. Italy) have since climbed 136% from €700k to approximately €1.6m (four-year CAGR: 24%):

- Management’s FY webinar named Ireland, Korea and Chile as distributors that performed well during this FY.

- The 2023 annual report disclosed Belgium and the Netherlands did not perform well during this FY:

“[M]anagement has considered the sales decline shown in Belgium and Netherlands in the current year and sensitised the recoverable value calculation to show 2-7% sales growth over the five-year period and an increasing cost base of between 4% and 7%, assuming all other assumptions remain unchanged.“

- France therefore appears to have performed exceptionally well given total Western Europe sales gained 21%.

- Notable Middle Eastern sales may now be one step closer following the purchase of another distributor during this FY:

“In May 2023 the assets of Fal Care FZE, a distributor based in the Middle East and North Africa, were purchased for £339,000.”

- TSTL also established an in-house Spanish subsidiary during this FY:

“We have 14 subsidiaries selling directly into the hospital marketplace in the United Kingdom, Belgium, the Netherlands, France, Italy, Germany, Switzerland, Poland, Hong Kong, China, Malaysia, Singapore, Australia, and New Zealand. We have subsidiaries in the United States, Japan, India, Spain and Ireland which are not yet active in terms of selling.”

- The major overseas hope of course is the United States…

United States

- The 2023 annual report understandably trumpeted the approval to sell an ultrasound-probe disinfectant in the United States:

- TSTL said the approval had created the group’s strongest-ever outlook:

“The enormous achievement of the year has been to gain FDA approval, thereby gaining access to the largest healthcare market in the world and creating the opportunity to leverage the significance of an FDA approval in countries that look to the USA regulator for their own practice. This includes Central and South America. We now have the opportunity to establish a global footprint for our products and technology. The outlook for the Company is the strongest it has been in its 30-year history.”

- The FY powerpoint confirmed the first US orders had been “shipped and invoiced“:

“Manufacturing:

• Process validation complete • Production underway & inventory available

Sales and marketing:

• First orders shipped & invoiced

• Parker distributors include: Medline Industries / Henry Schein / Owens & Minor / McKesson Corp

• Listing in hospital and distributor procurement systems underway

• FY24 Parker exhibiting at 7 major USA conferences and Innova at 2 major Canadian conferences, supported by Tristel team“

- December’s AGM update revealed early customers were “beta site users“:

“In the United States, Parker Laboratories, our manufacturing and distribution partner, completed its first production run for Tristel ULT in early October, following receipt of our FDA approval in June 2023. This has enabled Parker to stock its national distribution network and provide product to the first beta site users.

We expect to make steady progress in building our customer base throughout the United States during the second half of our financial year. We remain very excited about our prospects as we begin serving the largest healthcare market in the world.“

- “Beta site users” suggest US hospitals have not yet gone ‘all in’ on TSTL’s FDA-approved foam.

- Management’s FY webinar cited the US was “on track with operational timelines” and “should have real traction” by February.

- Management’s FY webinar reiterated the 24% royalty agreement with US manufacturing partner Parker Laboratories announced last year:

- Management’s FY webinar helpfully disclosed the anticipated revenue per ultrasound-disinfection procedure within the US.

- US hospitals are expected to pay between $3 and $3.50 per disinfection procedure for TSTL’s foam, with Parker collecting $2 and its appointed sales distributors capturing between $1 and $1.50.

- TSTL’s 24% royalty therefore equates to 24% of $2 = $0.48 = 38p per disinfection with GBP:USD at 1.25.

- 38p per disinfection is much lower than the aforementioned £2.02 per ultrasound disinfection that I calculate TSTL enjoyed within its established markets during this FY.

- That said, the mooted 38p from the US is 100% royalty income with no associated direct costs. In contrast, the £2.02 earned elsewhere attracts raw material, manufacturing and employee expenses.

- Management’s FY webinar referred to the group’s broker projecting US royalty income of £0.5m for FY 2024 and £1.4m for FY 2025.

- US royalty income of £0.5m translates into Parker sales of almost £2.1m and purchases by US hospitals of approximately £3.4m

- US royalty income of £1.4m translates into Parker sales of £5.8m and purchases by US hospitals of approximately £9.5m.

- Gross distributor sales of £9.5m would make the US TSTL’s second-largest market after the UK.

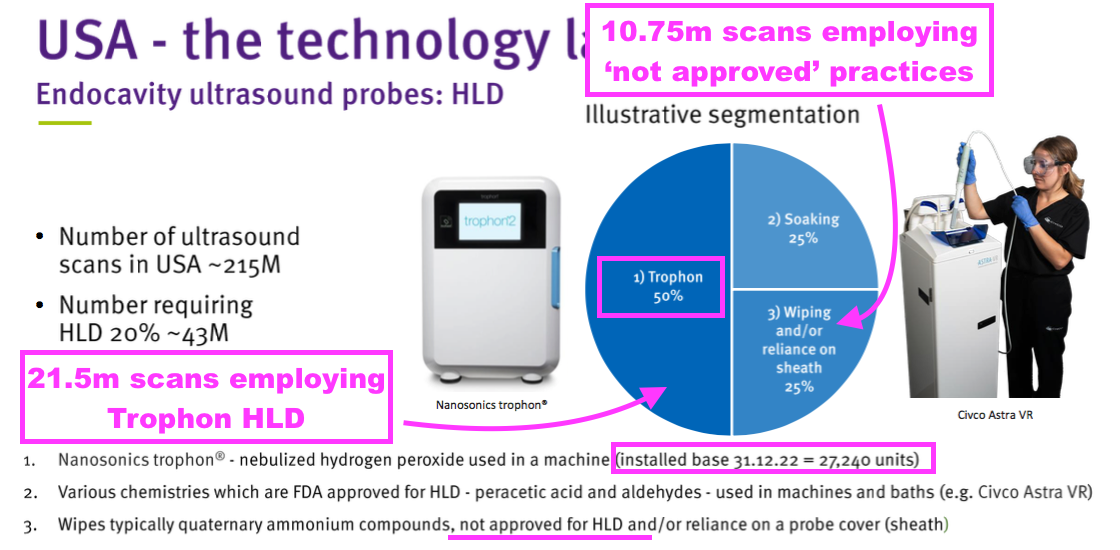

- TSTL has previously indicated US hospitals undertake 43 million ‘high level’ ultrasound-disinfection procedures a year:

- 43 million disinfections that each generate a $0.48 royalty gives a potential $20.6m royalty maximum for TSTL, and implies possible maximum expenditure by US hospitals of $140m on TSTL’s ultrasound foam.

- The US benchmark is set by Nanasonics (NAN), the quoted Australian group that manufactures the Trophon machine. Trophon machines are limited to disinfecting ultrasound probes only.

- That TSTL slide above shows 27,240 Trophon machines in North America undertaking 21.5 million ultrasound-probe disinfections every year:

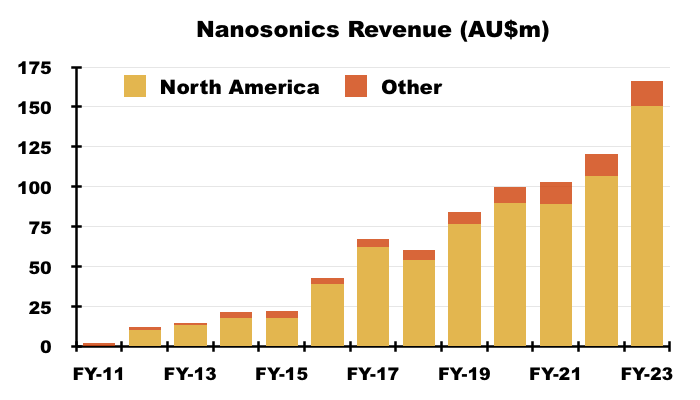

- NAN’s FY 2023 results disclosed revenue of AU$166m, of which AU$150m (approximately $101m) was earned within North America:

- NAN North American revenue of $101m and 21.5 million US Trophon disinfection procedures gives an approximate cost per disinfection of $4.70.

- $4.70 per Trophon disinfection compares to the $3 to $3.50 TSTL reckons US hospitals will pay per disinfection using the group’s foam.

- That $4.70 estimate reduces to $2.76 per procedure if NAN’s North American revenue includes only consumable and spare parts income, and excludes Trophon purchasing and servicing income.

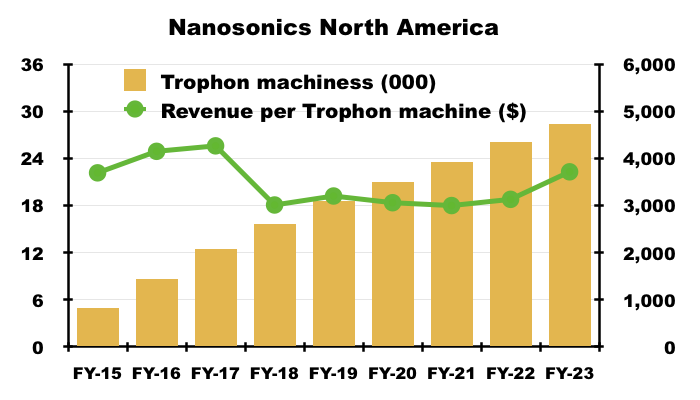

- NAN reckons North America could support 60,000 Trophon machines. Revenue per Trophon machine last year was approximately $3,700:

- NAN’s theoretical market size for North American high-level ultrasound disinfection is therefore $222m (60,000*$3.7k).

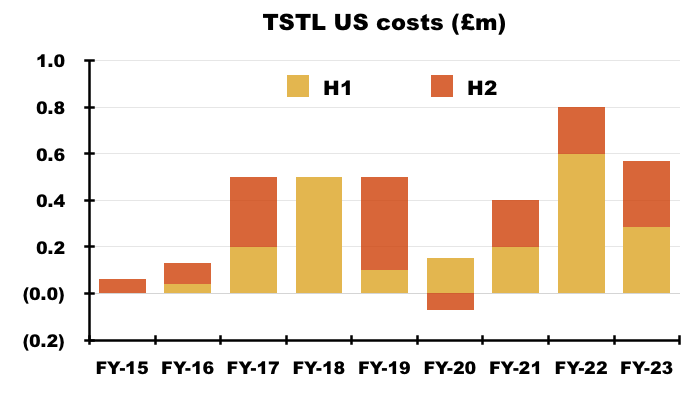

- TSTL did not specify the US regulatory costs incurred during H2.

- I have therefore guessed H2 US regulatory costs matched the £285k cited by management for the preceding H1:

“The USA costs were £285k in the first halfand will likely be the same again or less in the second half. The resources needed in the US going forward will principally be travel of the Company’s staff into the country to help launch the product. Tristel doesn’t anticipate anything more substantial at this time.”

- I calculate the aggregate US regulatory expenditure during the nine-year application programme to be £3.5m:

- TSTL did not refer to possible US operating costs within this FY or during the webinar. The preceding H1 presentation highlighted regional operating costs of £350k:

- I would not be surprised if US-related costs continue at £285k every six months.

Patents

- TSTL’s annual reports have regularly cited patents as part of the group’s competitive advantage:

“INTELLECTUAL PROPERTY PROTECTION

On 30 June 2023, we held 142 patents granted in 32 countries providing legal protection for our products.

In its broadest sense, our intellectual property relates to:

1. Patents, trademarks and registered designs

2. The scientific validation of our chemistry and our products that have entered the public domain, via a number of peer-reviewed and published papers

3. The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 56 medical device manufacturer, with respect to 1,449 of their individual models

- Some of TSTL’s patents are due to expire this year.

- Google Patents shows the anticipated expiry dates of TSTL’s wipe patents to be:

- UK: 7 May 2024 (GB 241 3765)

- EU: 26 July 2024 (EP 174 2672)

- US: 7 September 2024 (US 808 0216)

- Google Patents shows the anticipated expiry dates of TSTL’s foam patents to be:

- UK: 27 January 2026 (GB 242 2545)

- EU: 27 January 2026 (EP 184 3795)

- US: 11 September 2030 (US 884 0847)

- The Q&A during July’s open day prompted extensive management remarks about patents and general intellectual-property protection, which concluded:

“Patents are quite important, but not at the top of the list of the protections we enjoy that help us with our competitive position.”

- Management’s FY webinar repeated the same message, and confirmed the chemistry includes a “trade secret“:

“Patenting is not the only IP protection that we have. The chemistry itself is protected by a trade secret within the formulation, something that only a handful of people have access to, and something that has never been reversed engineered. We have worked with some large organisations and we are happy with the security of the product. We also have thousands of medical-device compatibility statements issued by instrument manufacturers, which provide another layer of protection and a number of published papers and studies that have been performed. All of which provides a significant wall around our IP that keeps us protected.”

- My discussion with Bruce Green, the chemist who devised TSTL’s disinfectant chemistry, at the 2022 open day confirmed competitors were kept at bay through secret chemical ingredients and secret manufacturing processes.

- I would like to think US partner Parker — a long-time US market leader within the ultrasound gel market — would not have become involved with TSTL if TSTL’s expiring patents would quickly allow generic alternatives to disrupt the US market.

- Parker seemingly has very few patents, suggesting other competitive factors may be more important when supplying products to the US ultrasound market.

- Only after the aforementioned patents expire will shareholders really know how important those patents were to TSTL.

- While “not at the top of the list of the protections“, TSTL continues to file patents. This FY witnessed 62 patent applications submitted and six granted.

- According to Google Patents, among the patents granted during 2022 were:

- Patent GB 259 7069, which proposes “to include in one of the components a pH-sensitive indicator which changes colour or becomes clouded when adequate mixing has occurred“, and;

- Patents GB 259 7911, GB 259 7912 and GB 259 7913, which all cover the “validation of procedures in a decontamination process” that involve “capturing a video stream of a work area… in which the… procedure is carried out by a user [and] analysing the video stream…”

- I believe these new patents relate to the R&D that helps verify TSTL’s manual disinfection processes:

- The equivalent new patents for Europe and the US remain pending.

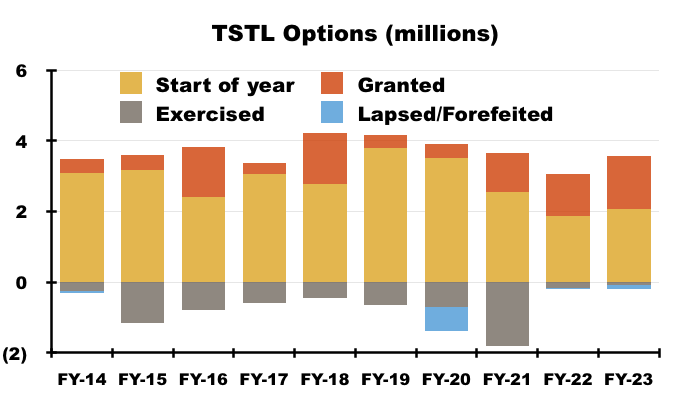

Share options

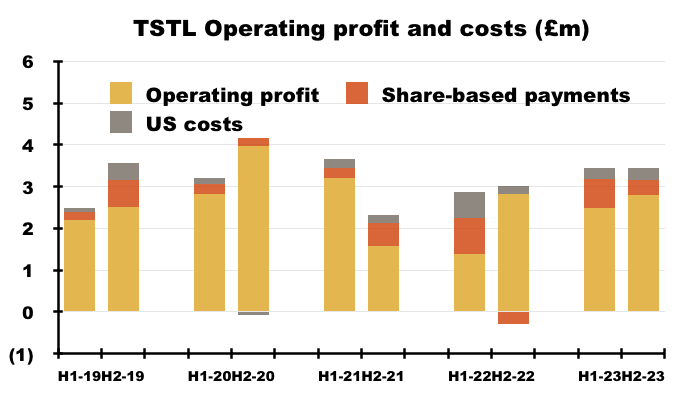

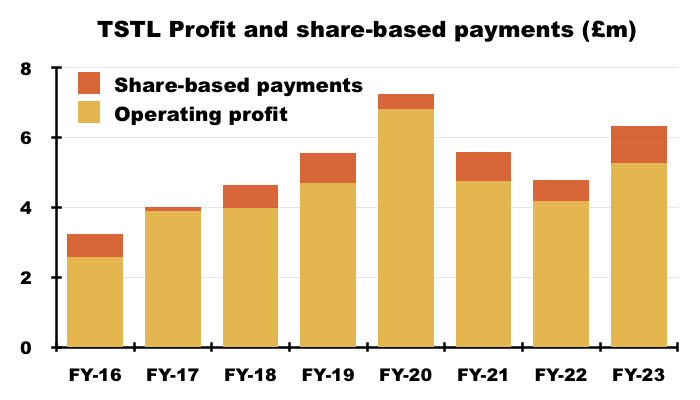

- Significant share-based payments have featured regularly within TSTL’s accounts.

- Between FYs 2016 and 2023, share-based payments reduced the aggregate pre-exceptional operating profit by £5.2m, or 13%:

- This FY witnessed share-based payments reduce operating profit by £1,061k, or 17%.

- TSTL presents an adjusted profit excluding share-based payments:

“Charges associated with share-based payments have been included as adjusting items. Although share-based compensation is an important aspect of the compensation of our employees and executives, management believes it is useful to exclude share-based compensation expenses from adjusted profit measures, to better understand the long-term performance of the underlying business.”

- One reason for adjusting for share-based payments is such charges can occur despite the options possibly becoming worthless.

- This FY revealed an executive LTIP incurred a £0.3m cost:

“The non-cash IFRS2 charge (share-based payment charge) for the year was £1.1m (2022: £0.6m). £0.329m (2022: £0.094m) of the charge relates to the Executive Management LTIP scheme approved at the Company’s 2020 AGM, the remaining £0.732m (2022: £0.506m) relates to the Company’s All Staff Option scheme.“

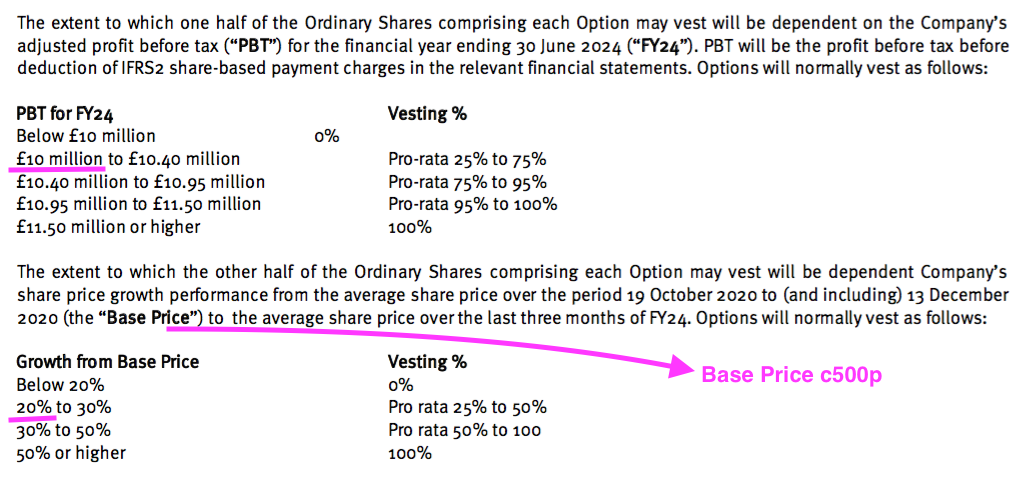

- The LTIP in question relates to 800k options that pay out if profit (before share-based payments!) reaches £10m during FY 2024 (versus £6.2m for this FY) or the share price trades at a c600p average during April/May/June 2024:

- The 2023 annual report admits management has given up on profit reaching £10m for FY 2024:

“The Executive Director Scheme is part of the remuneration package of the Executive Directors of the parent company… Management do not consider the adjusted profit before tax condition is deemed to be achievable and as such no share-option charge relating to that condition has been recognised.”

- The LTIP’s other condition — the share price averaging c600p during the three months to June 2024 — seems highly unlikely as well with the price presently at 425p.

- The true cost of options to ordinary shareholders is through permanent dilution and not accounting charges.

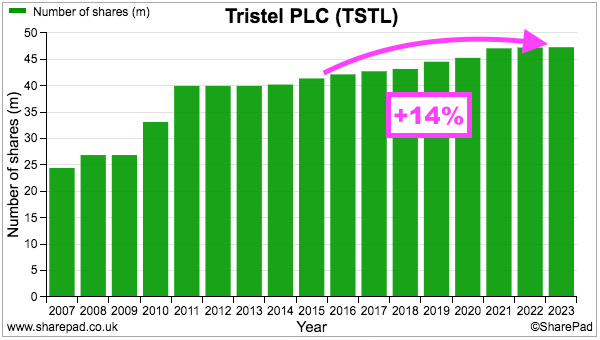

- TSTL’s share count has advanced 14% between the start of FY 2016 and the end of FY 2023, with 12% due to options and 2% due to the purchase of the Belgian/Dutch/French distributor:

- During the same period, the share price has increased from 101p to 425p while the dividend has increased from 2.72p to 10.5p per share. Outside shareholders have therefore still been rewarded despite the dilution.

- July’s open-day commentary disclosed a fascinating option revelation: option grants have been paused due to excessive past grants:

“Everybody within the company would qualify for the issue of share options over the course of their long service. As a board, we had to revisit that because the number of shares under option was exceeding the ABI [Association of British Insurers] rules. It has caused us to have a pause on the scheme and in fact it is a subject for our board discussions over the course of the next three or four months because we all recognise what an incentive it is.

- I believe best practice with options is to limit awards to 10% of the share count over ten years.

- I calculate TSTL has granted 6.9 million options during the ten years to FY 2023:

- The share count at the start of that ten-year period was 40.0 million.

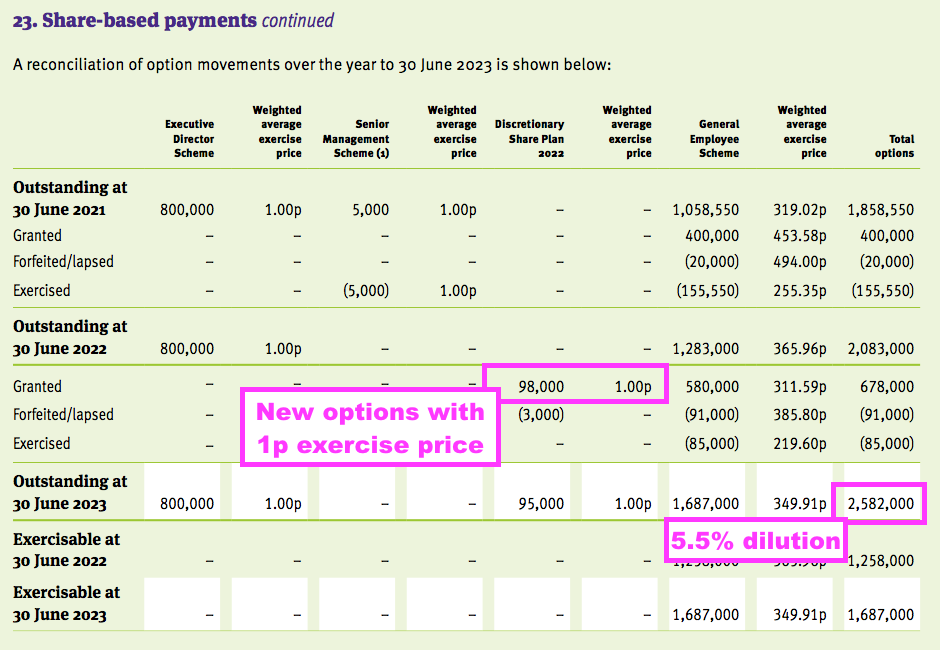

- The 2023 annual report shows TSTL granting 98,000 options within a new “discretionary” scheme with an exercise price of 1p:

- The annual report indicates 2.6 million options outstanding and potential further dilution of 5.5%.

Management succession

- December’s AGM statement announced the forthcoming retirement of TSTL’s chief executive:

“CEO succession planning

In addition, Paul Swinney, co-founder of the business in 1993 and Group CEO for the past thirty years, has informed the Board of his intention to retire within the next twelve months. Paul will continue in his post until a successor is appointed and has committed to remain available thereafter to support and advise the business in executing a successful transition in the leadership of the Group. The Board has, therefore, initiated a formal succession process, supported by the global organisational consulting firm The Coulter Partnership, that will consider both external and internal candidates.

The Group’s new CEO will join a strong executive leadership team with significant functional and market experience, gained from within and outside the business.”

- The chief executive turned 66 last month and the 2022 annual report (point 6i) had already signalled a “CEO succession plan [had been] agreed“.

- The chief executive has led TSTL for 30 years and, during my ten years as a shareholder, has overseen a multi-bagger return for my portfolio.

- I would normally express some concern when a long-time leader of a successful investment decides to retire. After all, the next boss may not be as talented as the old boss.

- With TSTL though, I am much less worried about the forthcoming leadership change.

- I believe TSTL’s management has not been entirely straight with shareholders on a number of occasions.

- In particular, there was the dubious £1m option vesting during 2016:

“To cut to the chase, last week’s statement revealed the group’s previous revenue guidance would now be “unlikely to be met”… and that the senior management team had just earned itself a £1m option windfall.

I wrote at the time that I had my suspicions about management’s behaviour. I have no proof that the board has done anything wrong, and no doubt the executives can point to the AIM Rules and say nothing has been breached.

It’s just that reading TSTL’s past RNS statements has now given me some doubts about the leadership quality of this business.

…

I feel it’s a shame that TSTL’s boardroom now looks to be of much lower quality than the products the firm is trying to sell.

- Then there was the protracted FDA submission, during which management publicly claimed the programme was “progressing as planned” despite having received — two months earlier! — a notification from the FDA to switch to a more demanding application process:

• The FDA’s change of mind to a (more demanding) De Novo application meant TSTL required far more testing and data for its regulatory submission.

• But TSTL remained optimistic despite the FDA’s change of mind.

• Full-year results published on 17 October 2018 — three weeks after the FDA’s revised application guidance was received on 25 September 2018 — revealed TSTL still hoping to submit an application based on the original (and less demanding) 510(K) Predicate process.

…

• An AGM update on 11 December 2018 — more than two months after the FDA’s revised application guidance was received — then stated the FDA project was “progressing as planned“:

- The aforementioned run of accounting restatements does not suggest the finance director would be a viable replacement for the chief executive.

- TSTL’s chief executive and finance director are married (point 5) and collectively own a 1.0% shareholding and 1.5% option holding.

- The AGM statement described the agency searching the for new chief executive as a “global organisational consulting firm”, and I would welcome a “global” appointment to deepen the board’s talent and to exploit the group’s ‘strongest-ever’ outlook.

- For example, multinationals Reckitt Benckiser and Johnson & Johnson both supply consumer disinfectants…

- … and I speculate both groups must harbour scores of divisional managers capable of maximising a provincial small-cap blessed with a prominent disinfection niche, significant worldwide opportunities, gross margins of 80%-plus and approximately £10m net cash.

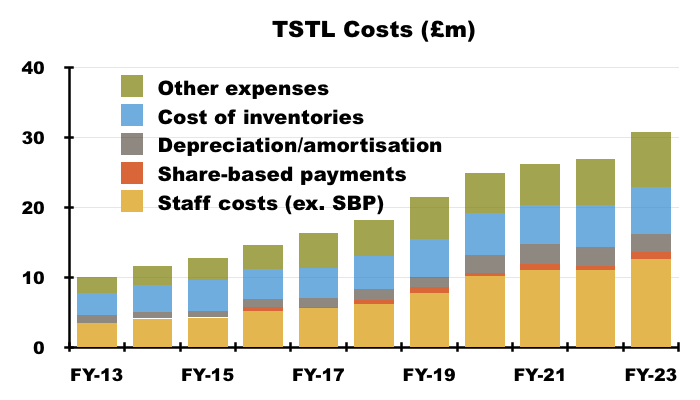

Financials: margin and costs

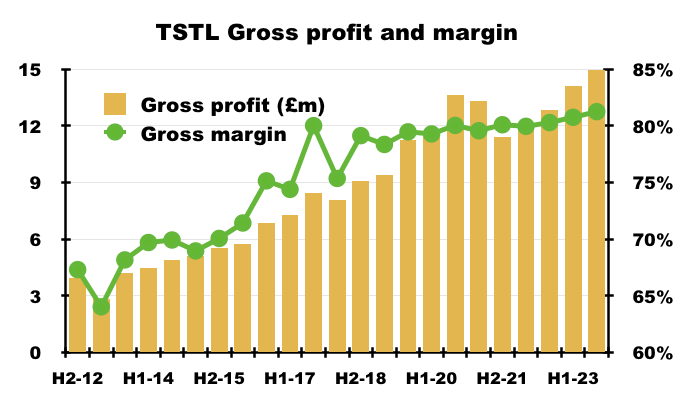

- The preceding H1 disclosed a record 81% gross margin that was maintained for this FY:

- An 81% gross margin is equivalent to buying stock for £19 and selling it for £100, and underlines how TSTL’s customers do value the effectiveness of the group’s chemistry.

- The medical-device wipes and foams boasted an 86% gross margin during H2:

- The gross margin earned from the surface disinfectants continues to decline, and suggests the new Tank and Shot products are needed to shore up that division’s profitability.

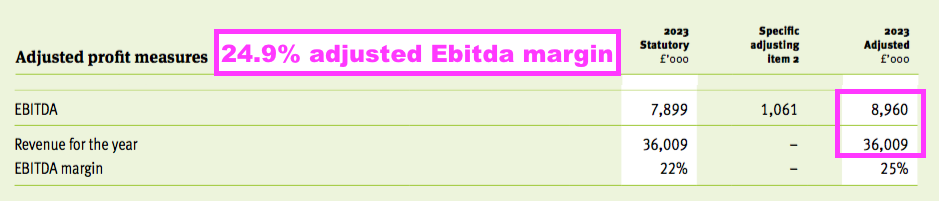

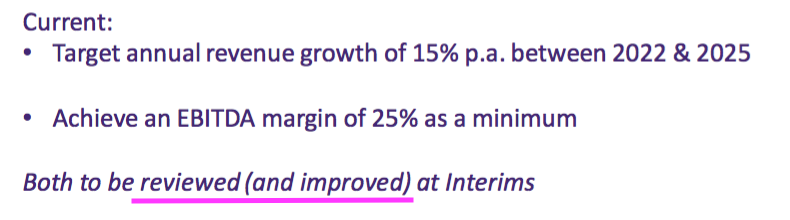

- The 81% gross margin almost helped TSTL meet its Ebitda target, which the comparable FY set to least 25%:

1. Sales growth in the range of 10% to 15% per annum as an annual average over the three years

2. The achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%, and

3. To increase profit before tax (excluding share-based payments) year-on-year, independently of the other two targets

- This FY’s Ebitda margin was 24.9%:

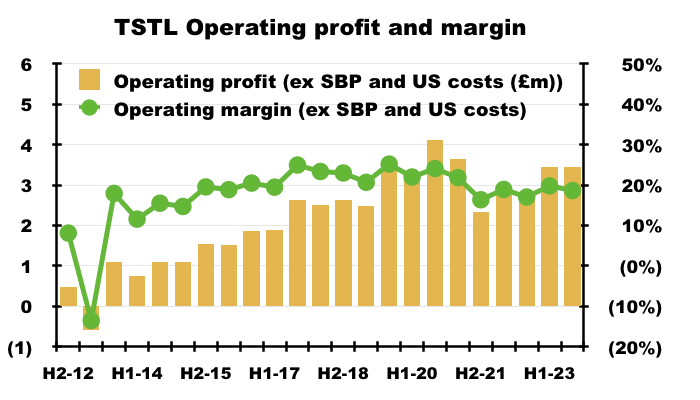

- The FY operating margin excluding share-based payments and US costs was a useful 19%:

- Mind you, the same margin calculation was 20% or more between FYs 2016 and 2020.

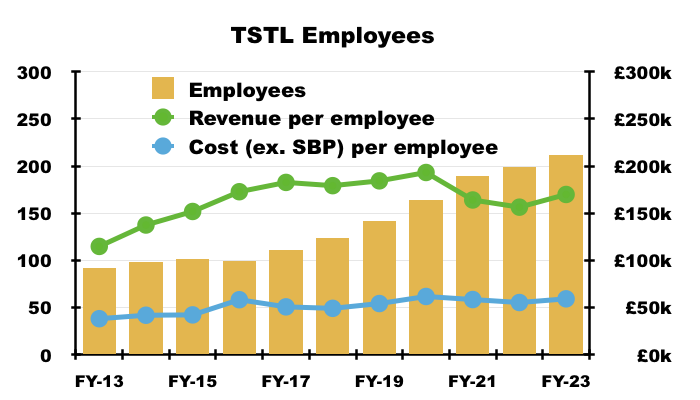

- TSTL has shouldered greater staff costs during recent years, and this FY showed that trend continuing:

“Overheads (excluding share-based payments, depreciation and amortisation) rose by 14% from £17.3m to £19.9m, principally due to the increase in headcount from 204 to 224. The associated increase in wages and salaries was £1.7m (excluding share-based payments).”

- Staff costs are TSTL’s largest expense, representing 35% of revenue during FY 2023 versus 30% or less between FYs 2014 and 2019:

- The average staff salary was £54k during this FY versus £44k for FY 2018 and £34k for 2013.

- Lifting staff costs when revenue per employee has flat-lined is not ideal:

- Reasons why revenue per employee has not advanced may include recruiting employees to:

- Handle the US regulatory submission;

- Administer tasks involving compliance and ESG, and;

- Undertake R&D for products yet to become commercial.

- Expensed R&D was £694k during this FY and has totalled £3.2m since FY 2019, equivalent to 2.0% of revenue during the same five years.

- I must admit I am not sure whether any new products have been launched — and then delivered material revenue — during the last five years.

- TSTL capitalised a further £927k R&D during this FY on to the balance sheet (see Financials: balance sheet and cash flow).

Financials: balance sheet and cash flow

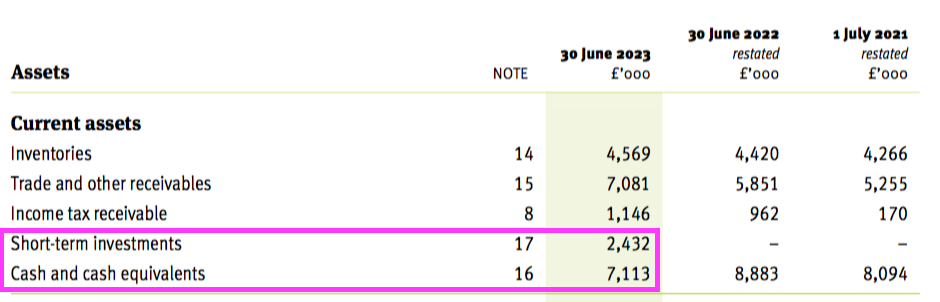

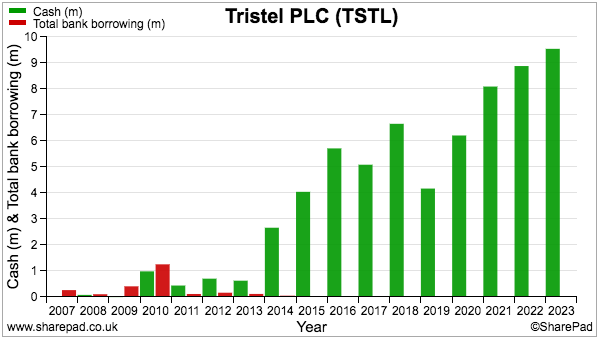

- The aforementioned £9.5m cash position included £2.4m cash deemed as “short-term investments” held within term-deposit accounts:

- The 2023 annual report said the money on deposit had at least a six-month term:

“The increased Bank of England (BOE) interest rate has incentivised prompt cash collection across the group which are subsequently invested on short term deals. At year end £2,432k was invested for a period of greater than 6 months.“

- Management’s FY webinar revealed the deposits had been placed during the final quarter of this FY, and that deposits post-year-end had increased to £6m.

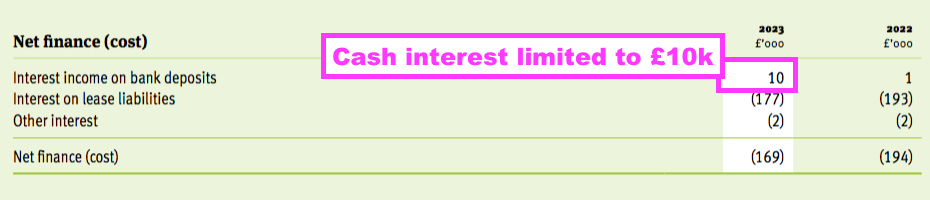

- I trust the deposit interest rate is higher than the 0.01% cited within the 2023 annual report:

“The Group’s financial assets include cash at bank and short-term investments. At 30 June 2023, the average interest rate earned on the temporary closing balances was 0.01% (2022: 0.1%).”

- Interest earned on the £9m or so held throughout this FY was a lowly £10k, all of which was earned during H2 that suggests a c2% interest rate:

- Companies blessed with significant ‘surplus’ cash should now be earning notable interest.

- NatWest for example offers 35- and 95-day notice business accounts paying 3.25% and 4.25% AER (variable) respectively.

- 3.25% on £6m would provide TSTL a useful £195k interest payment.

- The 2023 annual report confirms the group’s overseas subsidiaries hold “only the cash required for their operational activities”, and therefore “excess funds are held in the United Kingdom“.

- December’s AGM statement revealed “forecast cash balances of approximately £10.4m after payment of this year’s final dividend [of £3.7m]“, which implies cash had topped £14m:

- Cash generation remains respectable.

- The year ended with cash up £0.7m after £9.0m was generated by operations, £0.8m spent on tangibles, £1.5m spent on intangibles, £1.3m spent on leases, £0.3m spent on tax, £4.5m spent on dividends and £0.2m raised from options.

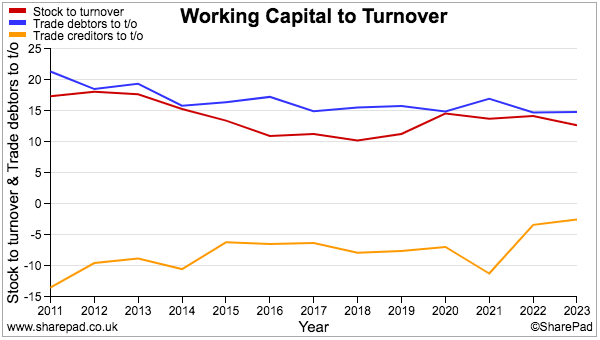

- Working-capital investment continues to be satisfactory:

| Year to 30 June | 2019 | 2020 | 2021 | 2022 | 2023 |

| Operating profit* (£k) | 5,549 | 7,240 | 5,586 | 4,784 | 6,342 |

| Depreciation and amortisation (£k) | 1,470 | 1,799 | 1,974 | 1,737 | 1,550 |

| Net capital expenditure (£k) | (1,347) | (2,380) | (1,767) | (1,203) | (2,423) |

| Working-capital movement (£k) | (780) | (1,453) | 324 | (636) | (49) |

| Net cash (£k) | 4,170 | 6,212 | 8,094 | 8,883 | 9,545 |

(*before share-based payments)

- An aggregate £2.6m has been absorbed into extra stock, debtors and creditors during the last five years — equivalent to an acceptable 9% of the £29.5m total operating profit recorded during the same time.

- SharePad shows stock and debtor levels versus revenue as being reasonably consistent, while decreasing creditor levels presumably reflect TSTL paying suppliers faster and does not feel too worrying:

- The five-year depreciation and amortisation expensed against earnings has meanwhile just about covered the actual net expenditure on tangible and intangible assets.

- The aforementioned £339k spent acquiring a Middle Eastern distributor was capitalised as an intangible “customer relationship” asset and will be amortised over 7-10 years — suggesting the distributor’s customers may place orders for up to another decade.

- A further £927k was capitalised as “development of marketable products” during this FY, with a cumulative carrying value standing at £1.9m that has yet to be expensed against earnings. Amortisation of such development expenditure runs between seven and (an extremely lengthy) 25 years(!).

- TSTL’s balance sheet implies the business remains an inherently capital-light operation.

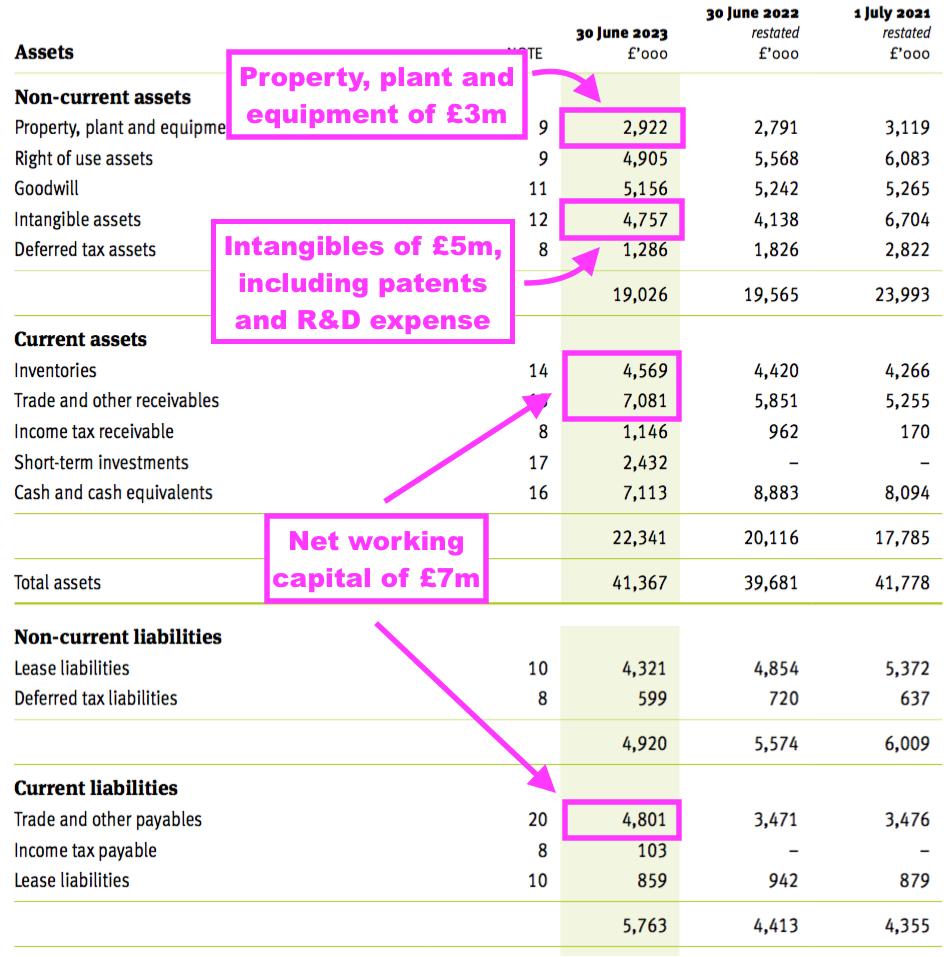

- Net assets of £31m less goodwill (£5m) and cash (£10m) leaves £16m, represented mostly by working capital (£7m), various intangibles (£5m) and property, plant and equipment (£3m):

- That £16m compares to FY operating profit (before share-based payments) of £6.3m, and implies TSTL may not need to reinvest relatively huge amounts to advance profit further.

- TSTL carries no bank debt and no final-salary pension obligations.

Valuation

- December’s AGM revealed H1 2024 sales had improved 18%:

“I am pleased to report that the Company has had a record first half with revenue for the six months ending 31 December 2023 expected to be £20.7m, an increase of 18% compared to £17.5m in the first half of last year. Revenue growth has been delivered across all our geographical markets. Gross margin remains above 80% in line with our expectations.”

- That 18% was not muddied by Brexit stock-piling nor discontinued products, and is ahead of TSTL’s own 15% sales growth target.

- July’s open day revealed TSTL’s financial targets would be “reviewed (and improved)”…

- …and this FY reiterated next month’s H1 2024 statement would reveal the upgraded guidance.

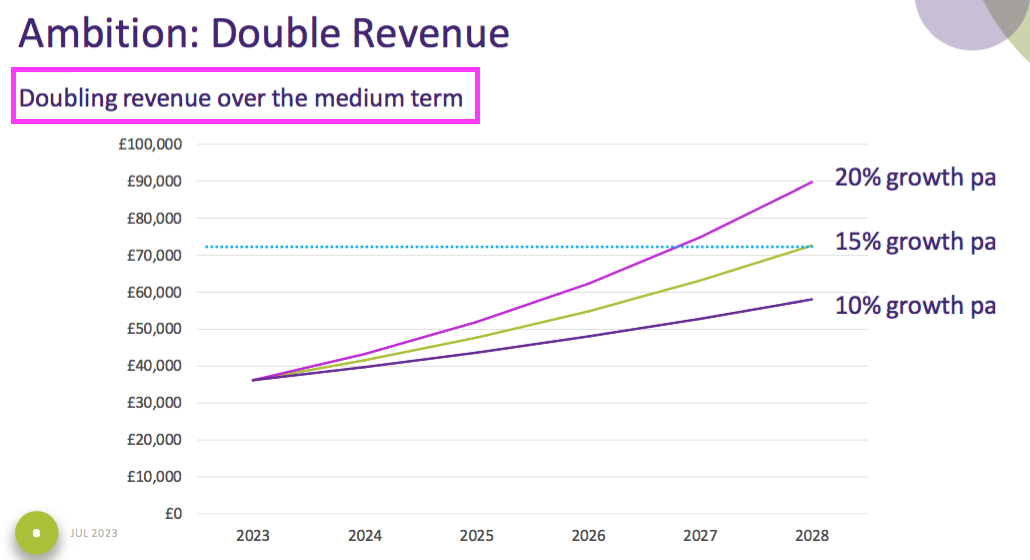

- July’s open day included a tantalising chart suggesting revenue may double “over the medium term“:

- Revenue doubling from this FY over five years would lead to revenue of £72m for FY 2028.

- Then meeting the minimum 25% Ebitda margin (before share-based payments) would give FY 2028 Ebitda of £18m.

- Depreciation and amortisation staying at 8% of revenue would then leave an operating profit of £12m.

- Applying standard 25% UK tax to my £12m projection then leaves possible FY 2028 earnings of £9m or 19p per share.

- My valuation sums could be fine-tuned for margin improvements, lease costs, the cash position, option dilution and tax intricacies, but the 425p share price at 22x my 19p per share estimate — for FY 2028! — does not indicate an obvious bargain.

- I would like to think the new chief executive will also want to see revenue (at least) double “over the medium term“.

- For now the 425p shares trade at a racy 40x trailing adjusted earnings, the basis for which includes TSTL enjoying:

- Very lucrative US royalties and significant progress within other new territories;

- Further meaningful growth from established products within established markets;

- A long-term competitive advantage through patents, manufacturer agreements, regulatory approvals and secret chemistry;

- Greater multinational acumen following the appointment of a new chief executive, and;

- Attractive returns from Tank, Shot and the rest of that R&D spend.

- My decision to purchase TSTL during 2013 and 2014 was made much easier because the 46p shares were then valued at a more modest c12x P/E multiple.

- While shareholders await the upgraded financial targets, details about early US progress and a new chief executive, the trailing 10.5p per share ordinary dividend should become at least 11.0p per share given the new 5%-plus dividend-growth commitment.

- A prospective 11.0p per share payout at 425p supports a 2.6% income.

Maynard Paton

Tristel (TSTL)

Publication of 2023 annual report

Here are the points of interest beyond those noted in the blog post above:

——————————————————————————————————————

1) OUR MARKETPLACE AND TECHNOLOGY

This section carries several paragraphs of identical text to the previous year, until right at the end, when this text from the previous report…

“We expect a legacy of COVID-19 to be that hospitals will be more rigorous in their selection of the best-performing and most scientifically validated disinfectant products, which will benefit Cache.”

…is absent from this year’s report. Maybe hospitals are no longer so “rigorous” with their disinfectant purchases?

2) REVENUE BY CHANNEL

I am pleased the annual report shows the revenue product split between countries:

The previous year’s report contained just ‘EMEA’ and ‘APAC’ within the revenue product split.

3) OUR STRATEGIC ASSETS

The statistics in this section have in the past included the non-core products that TSTL culled the other year. So identifying favourable or adverse trends is difficult.

But for the record…

“Our regulatory programme succeeded in attaining 16 approvals for 11 products in nine countries during the year. This includes FDA grant of the De Novo request for Tristel ULT.”

…compares to 21, 16 and five for the previous year.

TSTL now holds five more patents but in one less country:

“ On 30 June 2023, we held 142 patents granted in 32 countries providing legal protection for our products.”

And no changes to the number of compatible manufactures and their models:

“The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 56 medical device manufacturer, with respect to 1,449 of their individual models”

4) NON-FINANCIAL KEY PERFORMANCE INDICATORS

QMS audits created a few issues a few years ago, but nothing untoward occurred this time:

“During the year, the Group underwent three audits of the Quality Managements System and two desktop reviews of device technical files, and no major non-conformances were reported (2022: none).”

This text is new for 2023:

“The Board [is] regularly updated on employee turnover, gender split and pay gap, age statistics and Company tenure. Operational performance and customer satisfaction are assessed by purchasing compliance and delivery OTIF (On-Time-In-Full) percentages and customer complaints are monitored and target above 98% effectiveness, which is measured as complete orders delivered free from defect.”

5) GOING CONCERN

A reverse stress test is now included within the going-concern assessment:

“The Directors have prepared cash flow forecasts in order to assess going concern. The forecasts take account of potential and realistic changes in trading performance, and also include severe yet plausible downside scenarios. These scenarios include modelling reductions in revenue and margins and increasing costs and considering the consequent cash outflow that could result. A reverse stress test was also conducted.”

6) KEY BUSINESS RISKS

Remain the same:

• Operations

• Regulatory and Legal Approval

• Pandemic — Supply chain, Health and safety, and IT

…with only minor text amendments for this year.

7) EXTERNAL RISKS

The “credit and liquidity risks” from the previous report…

“The Group’s principal financial assets are cash and receivables. Credit risk is primarily attributable to its trade receivables, which are diversified across a large number of low-value customer accounts. In addition, operations in new markets may have a higher than average risk of political or economic instability, and may carry increased credit risk. In each case the risk to the Group is its ability to collect its debts.

Credit risk on liquid funds is limited because the counterparties are banks with high credit ratings assigned by international credit rating agencies. The credit risk on trade and other receivables is managed by agreeing appropriate payment terms with customers, obtaining credit agency ratings of all potential customers; by requiring wherever possible payment for goods in advance or upon delivery; and by closely monitoring customer balances due, to ensure they do not become overdue. In addition, careful consideration is given to operations in new markets before the Group enters that market.

Rising inflation impacts the business’s ability to maintain profitability levels and stakeholder goodwill. Where cost increases cannot be absorbed via efficiencies and adaptations, customer price increases will be considered.

The Group policy is to maintain a strong capital base to enhance investor, creditor and market confidence. Surplus funds are placed on time deposits, with cash balances available for immediate withdrawal if required. The Group has significant cash reserves at the date of signing, no external debt and no covenants.”

…were absent from this 2023 report. But the first two paragraphs are included within accounting footnote 26, so the credit risk has not been overlooked entirely.

But the term “rising inflation” does not appear in this 2023 report, nor does “a strong capital base to enhance investor, creditor and market confidence“. Even though TSTL remains cash rich, would be nice to read “a strong capital base” is a deliberate policy.

The cash flow risk and the exchange-rate risk remain the other external risks with no text changes.

8) SECTION 172

Includes additional text this year.

This is an additional introduction:

“The Board recognises that a director of a company must act in the way they consider, in good faith, would be most likely to promote the success of the company for the benefit of its members as a whole, and in doing so have regard (amongst other matters) to:

• The likely consequences of any decision in the long term

• The interests of the Company’s employees

• The need to foster the Company’s business relationships with suppliers, customers and others

• The impact of the Company’s operations on the community and the environment

• The desirability of the Company maintaining a reputation for high standards of business conduct, and

• The need to act fairly as between members of the Company”

And additional text about ESG matters:

“Significant Board time and focus is given to Environmental, Social and Governance (ESG) matters, ensuring that the Company is operating in an ethical, thoughtful and inclusive manner. The Board’s objective is to ensure that the Company’s societal impact is positive, and that any harm its activities cause to the environment are understood, with steps taken to minimise and eliminate them.”

One s172 line that has not changed confirms TSTL’s “primary asset” is not the product patents nor the chemical formulae nor the manufacturer-compatibility statements… but is the workforce:

“The Company’s primary asset is its workforce and so the safety, motivation, reward, retention, and happiness of staff is of the utmost concern to the Board in its decision making.”

9) DIRECTORS’ BIOGRAPHIES

A few minor text changes.

The bio of executive Bart Leemans now has all references to his pre-TSTL IT and e-commerce ventures removed.

The bio of non-exec Tom Jenkins confirms he moved to Sigmaroc during the year to head that company’s Investor Relations team.

Before joining Sigmaroc, Mr Jenkins had created the quoted investment team for investors BGF, which this 2023 report indicates owns 3.9% of TSTL. I had assumed his non-exec position was related to that 3.9% and allowed him to keep an eye on TSTL’s progress for BGF from the inside.

A bit of a shame Mr Jenkins no longer has a ‘professional shareholder’ interest with TSTL. He was appointed a non-exec in 2017, so perhaps has 2 years left to serve before reaching the 9-year guideline for a maximum non-exec stint.

Non-exec David Orr was appointed in 2015, so he will soon be straying beyond the 9-year maximum guideline. I would not be surprised if the recent appointment of a new chief executive heralds further board changes, and perhaps Mr Orr — a packaging executive — decides to leave. The aforementioned Mr Leemans has already stepped down from the main board but remains an executive.

Non-exec Isabel Napper is keeping busy, with her bio now referring to non-exec positions at Skillcast Group and Keystone Law.

Non-exec Caroline Stephens no longer cites a “Deep understanding and in-depth experience of an end-to-end digital agenda” among her skills.

I should add TSTL’s non-execs are commendably very relevant to this business. Napper worked on IP legal matters for 35+ years, Stephens worked at a senior level at Johnson & Johnson for 25+ years while the chairman Bruno Holthof was chief executive of hospital trusts in Antwerp and Oxford for c20 years.

10) DIRECTORS’ REMUNERATION REPORT

a) Introduction

These lines are new for 2023 and imply the information may not entirely meet tip-top reporting standards:

“This Directorsʼ Remuneration Report, which is approved by the Board, is voluntarily prepared and is not intended to meet the requirements of SI 2008/410 Sch 8.

“On behalf of the Board, I am pleased to present our Remuneration Report for 2023. While not a statutory requirement, the Group has produced this statement, to be read in conjunction with the Report of the Remuneration Committee, to comply with AIM rule 19 and also meet the requirements of the QCA code.”

b) Remuneration policy

This is text from last year:

“The Group’s remuneration policy for Executive Directors seeks to:

1. Consider an individual’s experience and the nature and complexity of their work to set a competitive base salary that attracts and retains individuals of the highest quality, whilst avoiding remunerating more than is necessary.”

But the line “whilst avoiding remunerating more than is necessary” has been removed from this year’s report!

That text removal gives the impression TSTL is now happy to remunerate more than is necessary, which is not ideal.

c) Directors’ remuneration

Pay rises all round for 2023:

The (now ex-) chief executive enjoyed a 20% salary increase while the other two execs enjoyed 19% increases. The chairman is now paid an extra £10k (to £80k) with the other non-execs collecting another £5k (to 40k).

The chief exec’s 20% increase seems generous, but the text explains:

“As explained in the Group’s Annual Report for 2022, the CEO and CFO volunteered to defer the implementation of their salary increase until the second half of the financial year. Their 2023 increase was not paid out until 1st January 2023, after it was confirmed that the Group was performing in line with its agreed internal budget.”

Note also that, since FY 2019, the chief exec’s pay has increased 30% (from £230k to £300k) while the dividend has advanced by 90%. So shareholders have seen their own income improve significantly.

And bonuses have been modest. The chief exec’s £82k bonus for 2023 means his aggregate bonuses during the last ten years (£661k) have equated to just 30% of his aggregate salary (£2,187k).

A modest pay rise for the executives is expected for 2024:

“The Committee therefore recommended an increase for the financial year 2024 in line with the general increase offered to the Group’s staff. However, the Committee also recognised two additional elements: first, that tremendous efforts had made by the Executive Directors during the COVID-19 pandemic, and second, that the recommended increase was significantly below prevailing inflation rates. With those two factors in mind the Committee recommended an extra performance bonus, payable in addition to the standard annual bonus but only if certain profit targets are hit.”

But there may be an “extra performance bonus“.

Remuneration details for the replacement chief executive may be disclosed in the forthcoming 2024 annual report, although we could have to wait for the 2025 annual report instead as the new boss started his TSTL employment in the 2025 financial year.

d) Bonuses

This is commendable; the executives voluntarily agreed to higher bonus targets and then missed out on £107k:

“Annual bonuses were awarded to the Executive Directors during the year to 30 June 2023. By agreement £107,000 of the available bonuses were forsaken by Executive Directors during the year, having volunteered an upward adjustment to the incentive target.”

e) Share options and shareholdings

The executives still have 800k options between them, although I believe these have all since expired worthless (more here).

Bart Leemans has commendably never sold a share since he sold Ecomed to TSTL in 2018 and took c950k TSTL shares as part payment:

The (now ex-) chief exec and finance director, however, have been keen sellers of late — no doubt due to the chief exec retiring and the two of them being a married couple and both perhaps thinking of life beyond TSTL.

The chief exec was last said to have owned 154,501 shares on 11 June 2024, and no longer being a director means he can now sell further shares without notifying the market. The FD was last said to have 150k shares earlier this month.

11) ESG REPORT

An all-new section for 2023, spanning nine pages. TSTL claims stakeholders (including shareholders) have “accepted” the associated ESG costs:

“As we look to the future and strive towards achieving our sustainability goals, we must acknowledge and address obstacles that may lay ahead. We have identified some of the challenges over the coming years to be:

• The availability of materials and technologies that will enable a continual reduction in Tristel’s carbon emissions

• In some markets in which we operate there is less appetite for sustainable products, where convenience and low cost are

the priority

• The acceptance by our stakeholders that an improvement to our ESG profile will come at a financial cost

We will address these challenges by setting unambiguous and tough goals; by ensuring that the Board is at the front and centre of the drive to success; by partnering with third parties who have like-minded and innovative approaches to sustainability and ESG; and by reporting transparently on our ESG activities regardless of whether they might be viewed as successful or otherwise.”

The ESG strategy has three “strategic pillars“, of which each has two or three “priority topics“:

The text explaining each pillar and priority contains nothing radical, although the language used is very ‘corporate’:

For example: “At the heart of our operations lies a profound commitment to fair and decent work. Fair and decent work resonates far beyond the confines of our office walls, reaching into the fabric of our employees’ lives. As we navigate the dynamic landscape of our industry, fair and decent work are not merely abstract concepts we endorse; they are the foundations upon which our success is built. In a time marked by a pressing cost-of-living crisis, our dedication to prioritising fair and decent work takes on an even greater significance, reflecting our commitment to the holistic welfare of all those who contribute to our mission.”

Possibly the most relevant ESG topic for shareholders is ‘innovation’, which includes two R&D KPIs:

The ‘innovation’ text mentioned “investigations into low carbon emission wipe alternatives working with substrate manufacturers“, which might imply work is being done to enhance the group’s wipe-based products.

But not all KPIs for ESG matters have been set. For example:

And TSTL has decided not to bother with standard SECR disclosures:

“Tristel, as a low energy user, is not required to make the detailed disclosures of energy and carbon information but is required to state, in its relevant report, that its energy and carbon information is not disclosed for that reason. Tristel’s annual energy use and greenhouse gas emissions, and related information has not been disclosed in this annual report as it is a low energy user.”

Emission data contained within this report related to 2022:

“Our 2022 carbon footprint totalled 3,337 tonnes of carbon dioxide equivalent (tCO2e).”

“Refrigerants” are fluids that can be used in air-conditioning systems, and I recall TSTL’s head office had a very powerful air-con system when I attended the 2022 open day — hosted during a near-40C heatwave!

12) CHAIRMAN’S CORPORATE GOVERNANCE REPORT

Lots of text changes to this section versus 2022.

a) Introduction

Revised text now says TSTL’s corporate governance meets the QCA code:

“This Corporate Governance Report is in compliance with the Quoted Companies Alliance (QCA) Corporate Governance Code.”

b) Corporate governance review

New text that mentions a “strategic review“:

“• Completion of a strategic review, in conjunction with the Company’s North American product launch, resulting in redefined strategic objectives and financial goals”

From what I can recall, TSTL has never mentioned a “strategic review” within its results, but understandably the FDA approval has prompted additional or revised ambitions.

New text confirming the ESG work:

“• Formulation of an ESG strategy and setting of targets”

c) Principle 1 – Establish a strategy and business model which creates long-term value for shareholders

No changes to this text that claims TSTL’s wipe system is the sector’s “gold standard“:

“Through technological innovation, maintain our position as the gold standard manual process for High-Level Decontamination of medical devices.“

TSTL’s ambition for its surface disinfectants remains to become the “global market leader“:

“To become the global market leader in sporicidal surface disinfection.”

Lots of new text about ESG matters as well:

“We have set ourselves the following carbon emission targets:

• To achieve net zero emissions for scopes 1 and 2 by 2030, and

• To achieve net zero emissions for scopes 1, 2 and 3 by 2045 in line with the NHS’s net zero target, in so far as we can exercise control over our emissions impact

We have also set targets pertaining to health, safety and wellbeing; diversity, equality and inclusion; fair and decent work, which are detailed later within this report. We will be setting waste management targets during FY24.”

This new text about risks is useful:

“The key risks to the Company delivering upon its strategic objectives are:

• Competing technologies

• Divergence by regulators away from chemical disinfectant products

• A shift in market acceptance of manual decontamination systems

The risks are addressed through product development, enabling the benefits of alternative systems to be incorporated into our offering while maintaining its existing unique and very high performance qualities.“.

Nothing mentioned about the workforce risks, though, despite the staff being the company’s “primary asset“. Nor anything mentioned about risks from patent expiries or other IP being breached.

d) Principle 2 – Seek to understand and meet shareholder needs and expectations

Not sure whether this blog counts as the “financial press“. Text for 2023 now includes a new line about AGM voting:

“The Board sees all write-ups on the Company by the financial press, monitors popular online bulletin boards and has a series of online facilities in place that provide a conduit between the Company and its shareholders. AGM voting recommendations and trends are reviewed by the Board and actions taken when there is evidence that shareholdersʼ expectations are not being met.”

e) Principle 3 – Take into account wider stakeholder and social responsibilities and their implications for long-term success

New culture adjectives for 2023. Out go “positive” and “engaged” and in come “candid” and “considerate“:

“The Board’s assessment is that the Company’s culture is energetic, candid and considerate, which is reflected in the achievement of its strategic goals.”

Additional text this year explaining the company’s “strong barriers to competition“:

“The management team works closely with regulators, key opinion leaders and authors of clinical guidelines in all countries, seeking counsel and working in cohort when appropriate. Effective connections and relationships are key to the success of the business and via these networks the Company has built strong barriers to competition, consisting of the inclusion in guidelines, studies, published papers, and medical device manufacturer care-cards. These relationships and their outcomes, combined with the Company’s proprietary formulation of chlorine dioxide and extensive patent protection, give the Board confidence that long-term success can be achieved by the Company in accordance with its strategic plan.”

Lots of additional ESG text as well, including this line…

“• Enhance the Annual report and Company website to provide clear updates to readers on the Company’s ESG activities”

…which implies the 2024 annual report may have a lot more than 9 pages devoted to the ESG section!

f) Principle 5 – Maintain the Board as a well-functioning, balanced team led by the Chair

Board now complies with the QCA code that requires at least half of the directors are deemed independent. Tom Jenkins became independent after leaving BGF, and David Orr will indeed retire after his nine-year stint:

“The Board believes that there is an appropriate balance between Executive and Non-Executive Directors on the Board. Isabel Napper is the Senior Independent Non-Executive Director, Bruno Holthof who is the Non-Executive Chair of the Board is also independent. Tom Jenkins and Caroline Stephens are Independent Non-Executive Directors, Tom becoming independent in the final quarter of the financial year. David Orr is not considered to be independent by virtue of his directorship and shareholding in Manor packaging, a supplier of cardboard to the Company. David will step down from the Board at the end of his nine-year tenure, during 2024.”

This sub-section is where TSTL discloses the chief executive and finance director are married:

“The Executive team consists of Tristel’s Chief Executive Paul Swinney and Chief Financial Officer Elizabeth Dixon, who are married, and Bart Leemans. Bart is an Executive Director, alongside his role managing the Group’s French and Belgian operations.”

g) Principle 7 – Evaluate Board performance based on clear and relevant objectives, seeking continuous improvement

An “external consultancy” was recruited this year to assess the board: