20 October 2023

By Maynard Paton

H1 2023 results summary for Bioventix (BVXP):

- A record H1, with revenue up 25% and profit up 26% helped by a post-pandemic recovery and favourable currency movements.

- Product sales were frustratingly conveyed through a broker note, which ‘estimated’ vitamin D income gained 11% and troponin income increased 52%.

- Pipeline efforts and potential continue to rest upon “exciting” Alzheimer’s research, although the work looks set to run to 2026 and associated revenue may occur beyond 2030.

- Repeating the 19% H1 dividend lift for the subsequent H2 would leave room only for a small eighth special payout, a prospect supported by remarks about taxation changes.

- Forecasts for a flat H2, troponin’s finite income and a lack of near-term R&D winners may explain why the £35 shares have not made headway during the last four years. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Product sales and broker note

- Vitamin D

- Troponin, biotin and other antibodies

- Pipeline: Tau

- Pipeline: biomonitoring

- Pipeline: CardiNor and Pre-Diagnostics

- Financials

- Valuation

News links, share data and disclosure

- AGM attendance 08 December 2022

- Interim results and presentation for the six months to 31 December 2022 published 27 March 2023

Share price: £35

Share count: 5,219,656

Market capitalisation: £183m

Disclosure: Maynard owns shares in Bioventix. This blog post contains SharePad affiliate links.

Why I own BVXP

- Develops diagnostic blood-test antibodies, direct competition for which is limited due to the necessary scientific innovation, protracted regulatory testing, onerous switching procedures and ‘captive’ hospital end-customers.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 7%/£13m shareholding and has declared seven special dividends.

- Employs ‘scalable’ royalty/licensing model that requires few employees and leads to terrific margins, generous cash flow and high returns on retained profits.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Revenue, profit and dividend

- This H1 extended the strong performance witnessed during the preceding H2 2022.

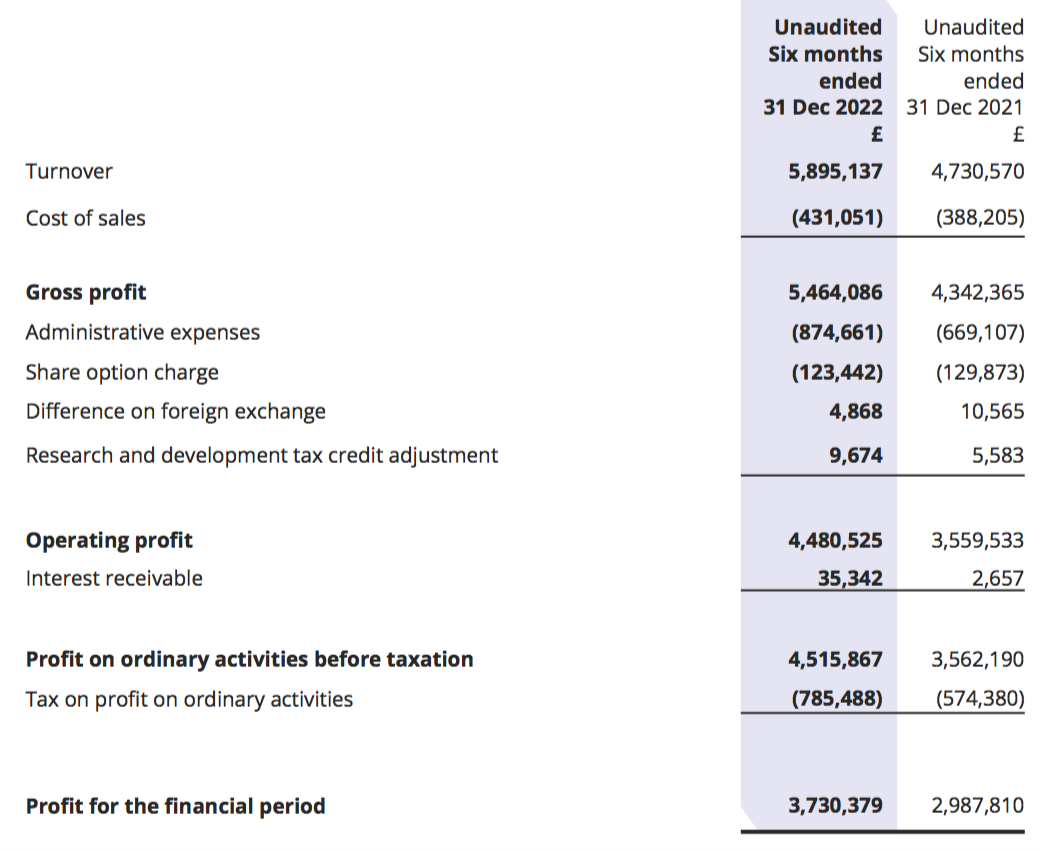

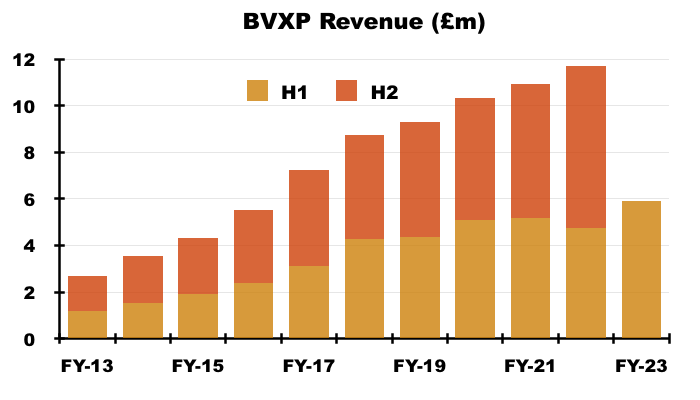

- Revenue advanced 25% to £5.9m to set a new H1 record:

- The 25% improvement was way ahead of the “sustainable” 8-10% growth rate cited during the preceding FY:

“We are pleased with our financial results for the year which we believe reflect both the growth in the use of our products and of course some relief from the global pandemic. In particular the continued roll-out of the high sensitivity troponin assays and the royalties associated with them have combined to help replace revenues from NT-proBNP which ceased from August 2021. After stripping out the impact of these 2 significant changes the growth in our underlying business over the year is in the range 8-10% which we believe is sustainable for the immediate future as our sales mix continues to change.“

- The 25% revenue advance was amplified by:

- Pandemic disruption experienced during the comparable H1 2022, and;

- Favourable currency movements experienced during this H1.

- Demand for BVXP’s diagnostic antibodies waned during the pandemic as fewer patients undertook routine blood tests.

- But this H1 confirmed the pandemic problems were now in the past:

“In conclusion, after the difficulties experienced during the pandemic, we are pleased to see a solid performance of our core business and look forward to this continuing over the remainder of the year. “

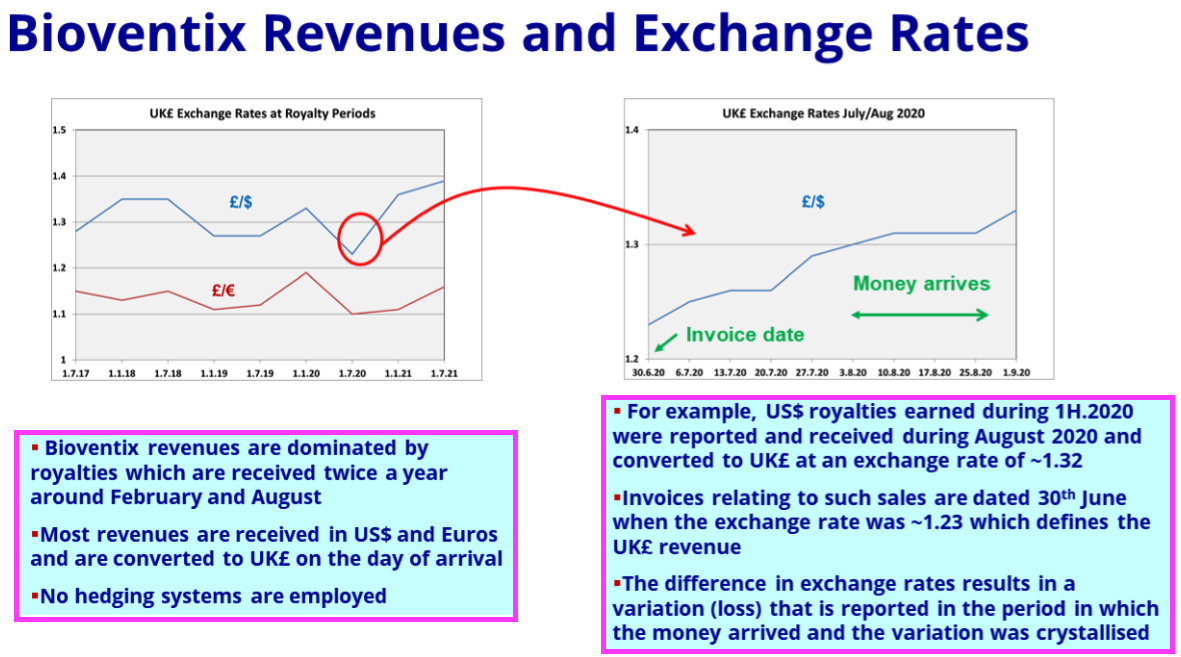

- The preceding FY confirmed the bulk of revenue is earned in USD and EUR:

“The majority of our physical antibody sales are priced in US Dollars. Our royalty revenues from our multinational customers typically arrive in either US Dollars or Euros depending on the location of the global nance centre of the customer… Overall, we estimate that 50–60% of our total sales are directly or indirectly linked to US Dollars.”

- The FY 2021 presentation explained how exchange rates influence revenue:

- Royalty invoices for this H1 were dated 31 December 2022, at which point GBP:USD was 1.209 and GBP:EUR was 1.129.

- Royalty invoices for the comparable H1 were dated 31 December 2021, at which point GBP:USD was 1.352 and GBP:EUR was 1.189.

- As such, USD-invoiced revenue was translated into GBP at a 12% higher rate and EUR-invoiced revenue was translated into GBP at a 5% higher rate during this H1 versus the comparable H1.

- Currency movements may therefore have added 8-9% to H1 revenue, which could mean ‘underlying’ revenue gained 16-17%.

- Unlike the preceding FY, within which BVXP disclosed a £0.4m revenue benefit from currency movements, no mention of favourable exchange rates was made within this H1.

- I estimate H1 revenue gained an extra £0.4m due to the stronger USD and EUR.

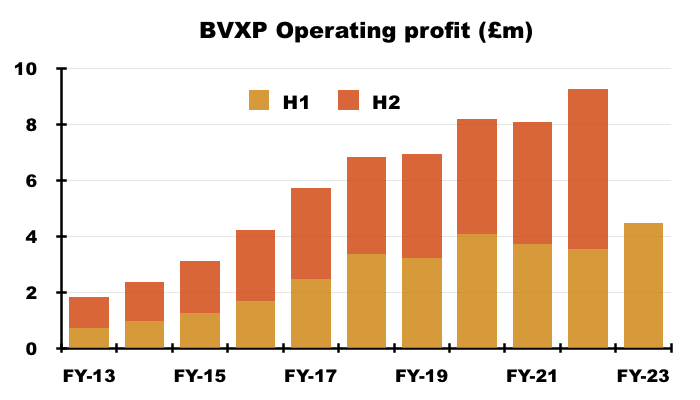

- The greater revenue pushed H1 operating profit up 26% to £4.5m and set a new H1 record:

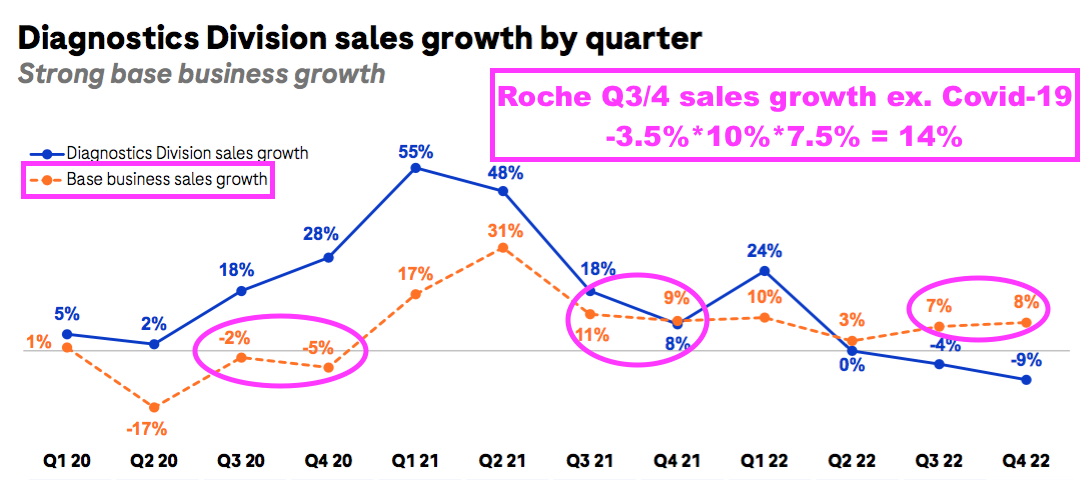

- BVXP appears to have slightly outperformed Roche during the pandemic.

- Roche is the world’s largest in vitro diagnostic (IVD) company and is as good a benchmark as any to judge demand for the type of blood-test antibodies that BVXP develops.

- Between July-December 2019 and July-December 2022, BVXP’s revenue advanced by 16% (£5.1m to £5.9m) while Roche’s routine-diagnostic sales expanded by approximately 14%:

- The profit increase led to the H1 dividend being lifted a very useful 19% to 62p per share:

- Cash finished the half at £5.1m and exceeded BVXP’s desire for a minimum £5m cash balance reiterated within the preceding FY:

“Our current view continues to be that maintaining a cash balance of approximately £5 million is sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future. We have therefore decided to distribute surplus cash that is in excess of anticipated needs and we are pleased to announce a special dividend of 26 pence per share.”

- Cash continuing to top that £5m ‘buffer’ may therefore herald BVXP’s eighth special dividend within the forthcoming FY 2023 (see Financials).

Product sales and broker note

- BVXP’s H1 statements have traditionally provided little commentary about the company’s various antibodies.

- Product progress this time was limited to the following remarks:

“Sales of physical product have performed well and revenues from our vitamin D antibody and other core antibodies have all increased as anticipated.

Sales relating to troponin antibodies grew significantly once again during the period. The continued roll-out of high sensitivity troponin tests provides further encouragement for our future sales in this area.”

- The H1 presentation meanwhile just repeated the sales chart from the preceding FY:

- BVXP very annoyingly tips off its house broker about H1 product sales.

- The house broker’s note said:

“Vitamin D testing antibody sales and royalties increased 11% (+£0.3m) to c.£2.9m, representing c.49% of revenues. Troponin revenues rose 52% to c.£0.8m, albeit only modestly ahead of H2 FY 2022 revenues. The remainder of its portfolio saw revenues increase c.44% (+c.£0.7m) to c.£2.3m, representing 38% of revenues, aided by the ongoing recovery in routine testing post-pandemic as well as increased supply of physical antibodies.“

- The broker note in fact provides detailed revenue ‘estimates’ for each of BVXP’s major antibodies:

- BVXP shareholders being forced to access a broker note to discover half-year product sales is very frustrating, not least because BVXP quite happily reports product sales at each FY! (see Troponin, biotin and other antibodies).

- With revenue and profit up 25% or more, the need for precise product-sales figures may not have been pressing for this H1.

- But a time will come when BVXP’s H1 performance will not be so positive, and shareholders will then require greater information to understand the disappointing progress.

- Up until July 2020 the finance director was a part-time non-exec being paid £19k a year. So perhaps extensive disclosures should not have been expected back then.

- But with the replacement FD on £81k a year, up-to-date product sales really ought to be disclosed within every results statement and presentation.

- Enhanced shareholder communication would also save BVXP money by negating the need to commission broker ‘research’ to convey important sales figures.

Vitamin D

- The house broker

was toldestimated vitamin D sales gained 11%:

“Vitamin D testing antibody sales and royalties increased 11% (+£0.3m) to c.£2.9m, representing c.49% of revenues”

- Adjust for currency movements and that 11% may translate into 2-3%.

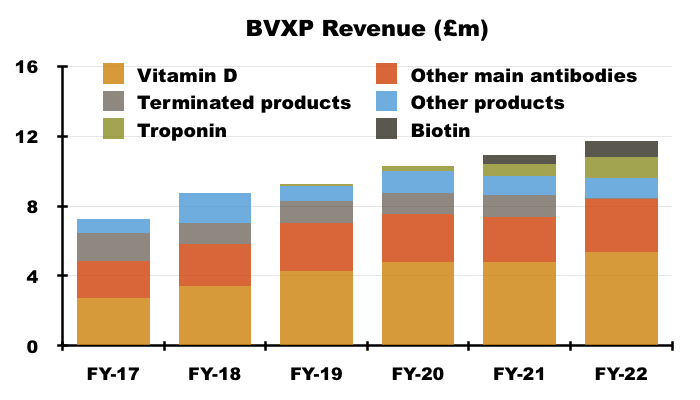

- Vitamin D progress is important for shareholders because the antibody is by far BVXP’s best seller. Vitamin D represented 46% of revenue during FY 2022:

- BVXP’s vitamin D commentary has fluctuated of late.

- The comparable H1 talked of “price erosion in downstream markets“:

“As reported previously, the growth rates for our vitamin D antibody sales were not expected to match those seen in recent financial years and a plateau in the downstream global vitamin D assay market had been anticipated. Sales associated with assay formats using larger quantities of antibody per test suffered more as price erosion in downstream markets puts pressure on costly “antibody-hungry” products“

- But the preceding FY statement claimed an “improved downstream market”:

“Our most significant revenue stream continues to come from the vitamin D antibody called vitD3.5H10. This antibody is used by a number of small, medium and large diagnostic companies around the world for use in vitamin D deficiency testing. Sales of vitD3.5H10 increased by 13% to £5.4 million which we believe reflects an improved downstream market for vitamin D testing following a degree of recovery from coronavirus pandemic effects.“

- Management’s AGM remarks explained vitamin D “price erosion” was caused by new tests entering the market. The AGM remarks also claimed vitamin D still ought to expand at 5-10% a year as per the wider IVD market.

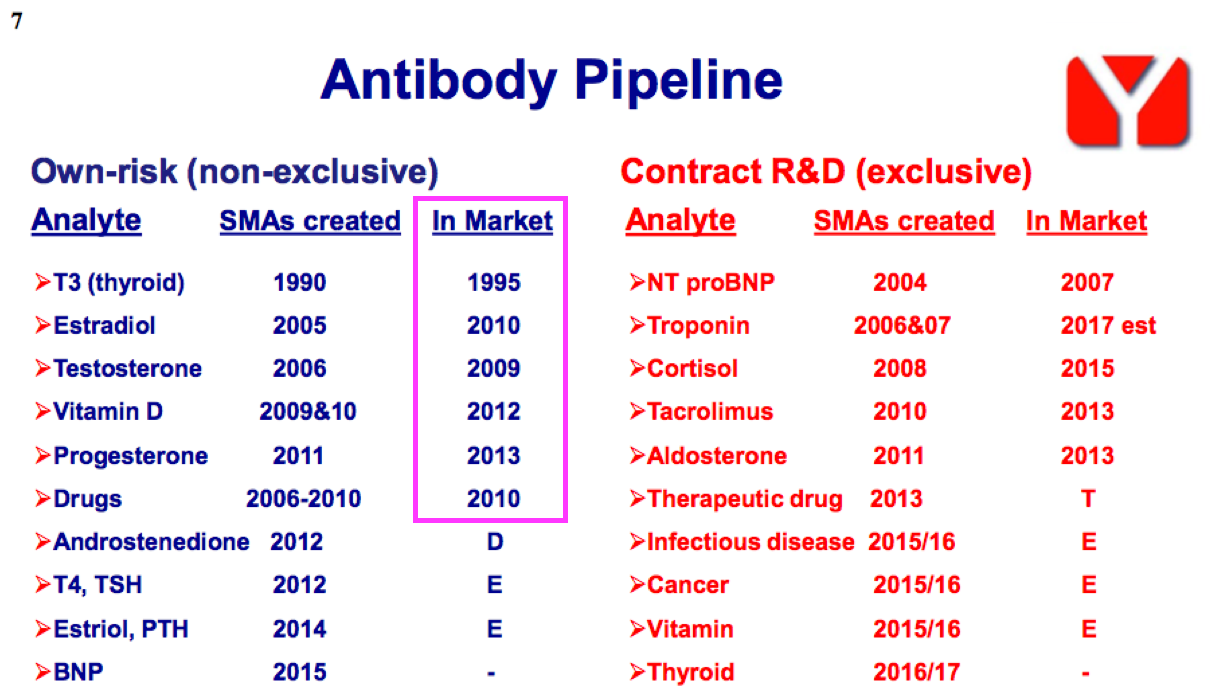

- Development on the vitamin D antibody started during 2008 and revenue was first earned during 2011.

- Going from zero revenue to beyond £5m within twelve years may give some idea as to the potential for BVXP’s newish troponin antibody.

Troponin, biotin and other antibodies

- The house broker

was toldestimated troponin sales gained 52%:

“Troponin continues to ramp: Revenues in H1 rose c.52% to c.£0.8m, accounting for c.13% of total revenues and 21% of the incremental revenue increase. Although a stronger H2 (c.£1.1m) will be required to meet our current FY 2023 forecasts, we consider troponin to be on track to meet our long-term outlook for c.£3.0-3.5m of revenues, with the potential for use in wider indications (eg. at-risk patients and allow for earlier invasive strategies) driving higher sales in the future.“

- Development work on troponin — an element used to detect potential heart attacks — started during 2006 and the antibody first generated sales during FY 2019.

- Trailing twelve-month troponin sales are, according to the house broker, approximately £1.5m or 12% of total revenue.

- BVXP’s house broker continues to “expect peak revenues of troponin in 2025 to still be in the £3-3.5m range.”

- Income from “biotins and biotin blockers” was divulged for the first time within the preceding FY:

- T3 (tri-iodothyronine): £0.93 million (+25%);

- biotins and biotin blockers: £0.90 million (+67%)

- progesterone: £0.62 million (+14%);

- estradiol: £0.59 million (+34%);

- testosterone: £0.47 million (+7%);

- drug-testing antibodies: £0.38 million (-7%);

- Management confirmed at the AGM that its original biotin antibody was generating all the extra sales while the new biotin-blocker product had experienced “minimal” income.

- Management’s AGM remarks also noted the biotin antibody was developed during 1999 and may now — through “good fortune” — be used as a replacement for streptavidin.

- But management claimed no insight as to what the end customers were buying the streptavidin-like antibody for.

- The sudden demand for the biotin antibody highlights a positive and negative aspect of BVXP’s business:

- On the plus side, an antibody can still earn good money 24 years after its development.

- On the minus side, BVXP seemingly has little knowledge about what exactly drives demand for certain antibodies.

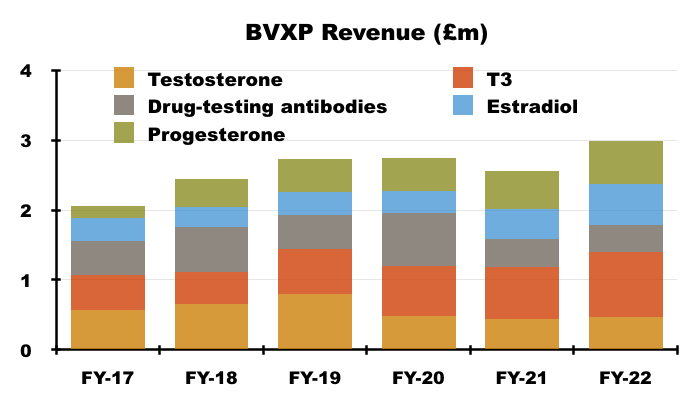

- H1 income from BVXP’s five other leading antibodies — used for testing thyroid function, fertility and drug abuse — climbed from £1.1m to £1.4m, at least according to the house broker.

- Longer-term progress from these five antibodies has been mixed. Between FYs 2017 and 2022 for example, sales of T3 have rallied 88% while sales of testosterone have slid 19%:

- Once developed, BVXP’s antibodies do tend to earn revenue for some time. The FY 2016 presentation suggested many antibodies have now generated royalties and/or sales for more than ten years:

- Antibody longevity is due mainly to the healthcare industry’s reluctance to replace a proven blood-test biomarker, unless the new upgraded antibody offers significant diagnostic improvements over the incumbent.

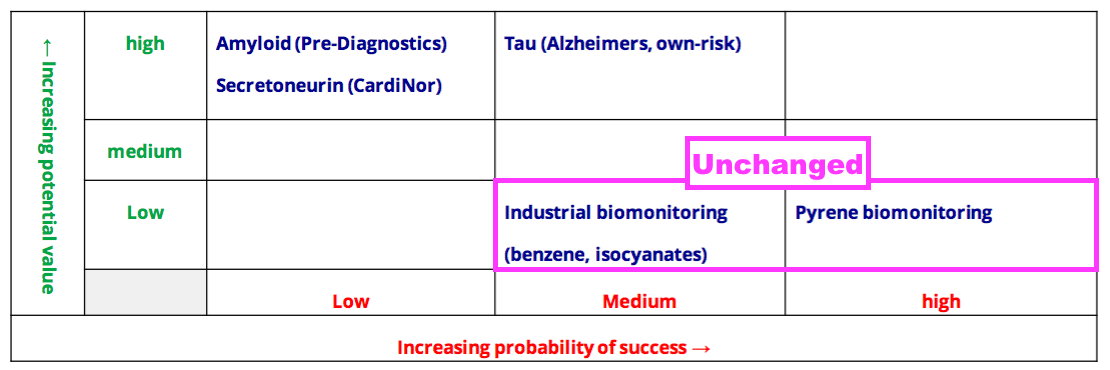

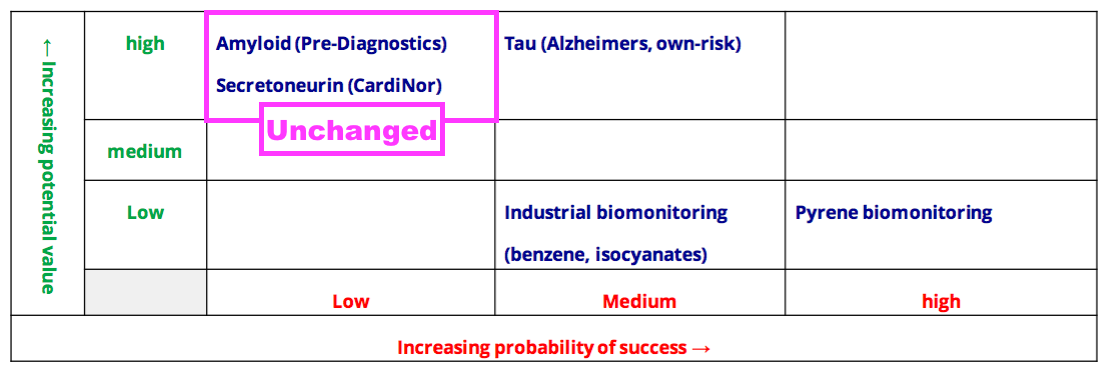

Pipeline: Tau

- A good chunk of the H1 commentary concerned studying Tau proteins for dementia research:

“A considerable amount of our laboratory resource has been focused on the Tau biomarker which shows exciting potential in neurodegenerative diseases including Alzheimer’s disease.

We continue to create new antibodies which will be subjected to assay development and validation using clinical samples at the world-renowned laboratory of Kaj Blennow and Henrik Zetterberg at the University of Gothenburg.

Using a novel Bioventix antibody, our academic collaborators in Gothenburg have recently published data on a novel assay that detects “brain-derived” Tau in blood (Brain 2022: 00; 1-14). Brain-derived Tau levels in blood appear to mimic Tau levels in cerebral spinal fluid and could be a useful blood biomarker for neurodegeneration that occurs later in the Alzheimer’s disease pathway. Currently, the preferred candidate research biomarkers for early Alzheimer’s disease are phosphorylated forms of Tau (pTaus).

We eagerly await more data from Gothenburg on the pTau antibodies developed by us and delivered to Gothenburg in 2022. We will be providing additional antibodies from the Bioventix pipeline for further evaluation in Gothenburg later in 2023. We are delighted with the continuing development of this collaboration and the outlook remains exciting.“

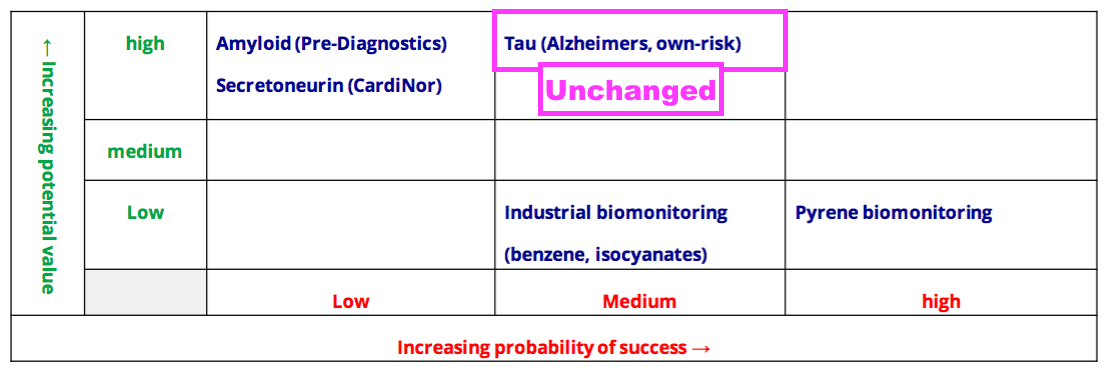

- The Tau project’s probability of success was elevated from Low to Medium during the preceding FY and remained at Medium for this H1:

- The ‘holy grail’ of the Tau project is to develop an antibody for a mass-screening blood test that can detect the very early stages of Alzheimer’s disease (AD).

- AD can develop over 10-20 years and the brain adapts to the condition before obvious signs of dementia emerge, at which point the symptoms can’t be reversed.

- At present, a recognised method of detecting the onset of AD is by locating brain-derived Tau in cerebral spinal fluid.

- However, a spinal-fluid test requires a lumbar puncture — a procedure usually performed with a local anaesthetic and therefore not as straightforward to undertake as a blood test.

- Prior to this H1, management had informed shareholders at the AGM that BVXP’s Tau work would be reviewed in the scientific journal Brain.

- The Brain paper confirmed how a BVXP antibody detected brain-derived Tau on a par with spinal-fluid tests in 609 blood samples — therefore bringing the prospect of a working AD blood test one step closer.

- The Brain paper acknowledged more testing was needed to prove the BVXP antibody works i) on more diverse/larger samples, and; ii) with different stages of AD.

- Management’s AGM remarks described the Gothenburg researchers as “excited” by the Brain paper. Management also admitted BVXP was not the only supplier of antibodies to the Gothenburg lab.

- The H1 presentation slides implied Tau research may continue until 2026:

- Management’s AGM remarks indicated BVXP’s Tau research would continue until either the company — or somebody else — succeeded in developing a suitable AD blood-test biomarker.

- Management also suggested any Tau-related revenue would occur beyond 2030, when “when AD therapies become more commonplace”.

- Management reiterated at the AGM that nothing in the pipeline — including Tau — offered troponin-type potential.

- Management’s AGM remarks also claimed Tau was “looking like a better biomarker” for AD than amyloid beta, which is being studied by BVXP partner Pre-Diagnostics (see Pipeline: CardiNor and Pre-Diagnostics).

- The preceding FY referred to a breakthrough AD treatment:

“The recent success of the Eisai/Biogen lecanemab clinical trial is likely to increase the need for early [Alzheimer’s] diagnostics and we are very fortunate to be working with one of the world’s leading labs focussed on Alzheimer’s biomarkers and tests.“

- Since then Eli Lilly has announced successful Phase 3 trials of donanemab, which was “able to slow clinical decline by 35% in people with early Alzheimer’s…”

- Scientists at the Dementia Research Institute at University College London and KU Leuven in Belgium have meanwhile claimed to have discovered how to prevent neurons from dying due to AD. This research may create new ways of treating the condition.

- Lecanemab, donanemab and other future treatments should in turn spur demand for blood tests that indicate the early development of AD well before the symptoms become obvious.

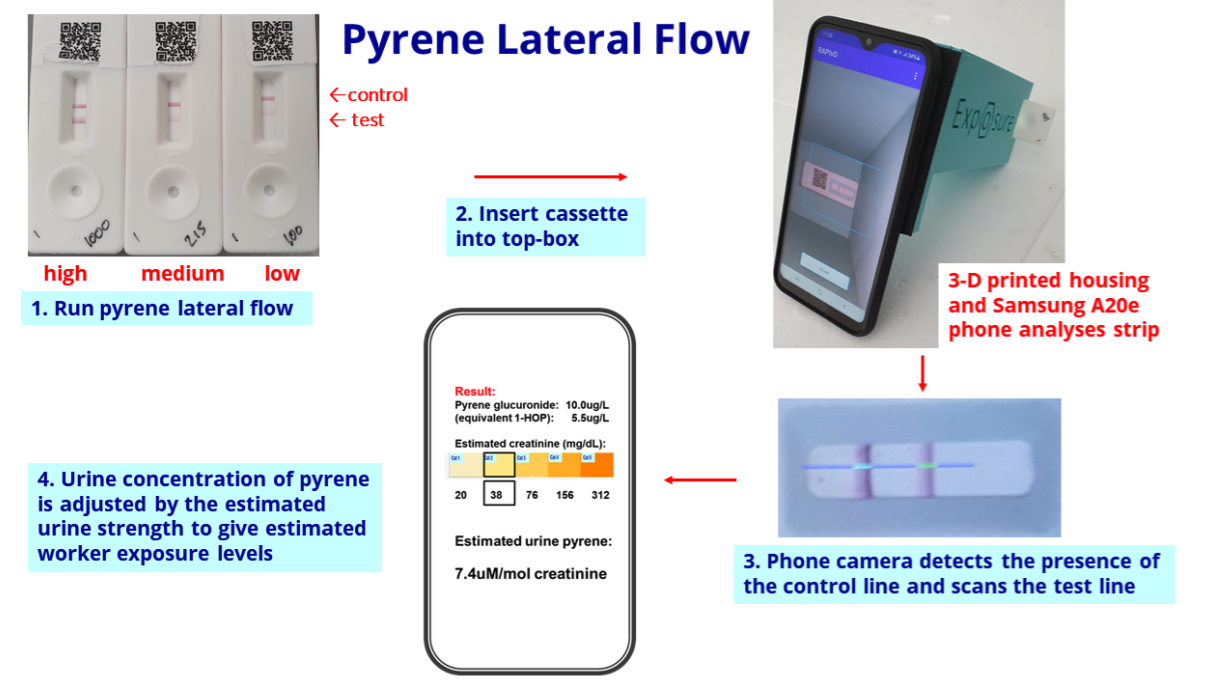

Pipeline: biomonitoring

- BVXP’s pipeline grid continues to rate the group’s two biomonitoring projects as Low potential value:

- Mind you, BVXP still tantalises shareholders by showcasing pyrene biomonitoring on its homepage:

- The biomonitoring tests work by examining a urine sample through a mobile phone:

- The preceding FY indicated tests for industrial-pollution biomonitoring would be conducted throughout 2023:

“Our pyrene lateral flow system for industrial pollution biomonitoring completed a trial at a UK industrial site during quarter 4 of 2021. This went well and we plan to conduct additional site studies during 2023.

- This H1 revealed industrial-pollution biomonitoring “field trials” would now continue during 2023 and 2024:

“We are also pleased with our progress on the continued development of our industrial pollution exposure assay. Our prototype lateral flow test for pyrene in industrial worker’s urine is due to feature in a new field trial at a UK industrial site during Q2.2023. The results from the device and phone-app will again be correlated with parallel samples analysed by a central health and safety laboratory. Important feedback from the trial will be gained and is likely to prompt additional modifications to the phone-app camera reader system before more field trials are carried out in 2023 and 2024.”

- Management’s AGM remarks about biomonitoring were not enthusiastic:

“[Biomonitoring is] going to be small I think. I would not bother putting that on the spreadsheet.”

- Management also implied organisations seemed happy with air-monitoring devices for pollution tests.

- The AGM talk included comments of BVXP’s pollution tests creating false alarms; barbecued sausages for example can apparently create high levels of the elements being tested for.

- Even if the pyrene tests work and go on sale, the kit is unlikely to enjoy the same wonderful economics of receiving royalties from antibodies developed a decade (or more) ago with manufacturing generally undertaken by the customers.

Pipeline: CardiNor and Pre-Diagnostics

- Collaborations with Norwegian research houses CardiNor and Pre-Diagnostics remain firmly within the top-left corner of BVXP’s pipeline grid:

- BVXP has invested an aggregate £610k into CardiNor and Pre-Diagnostics since FY 2016.

- This H1 indicated the Norwegian projects showed no sign of imminent revenue:

“We continue to await news and critical data from both of our partners in Oslo; on our secretoneurin project with CardiNor for enhancing cardiac diagnostics and on our amyloid beta project with Pre-Diagnostics in Alzheimer’s diagnostics. We hope to have more news on these two projects during 2023.”

- CardiNor’s secretoneurin biomarker tests for a particular type of heart failure and perhaps complements BVXP’s troponin product.

- Intuitive Investments (IIG) paid £125k for 1.8% of CardiNor during March 2021, which implies CardiNor was then worth almost £7m. IIG continues to hold its Cardinor stake at cost.

- IIG’s latest CardiNor commentary was upbeat, although the news the investment group cited occurred during 2022:

“CardiNor has made excellent progress particularly with the amount of money raised, which includes:

• Elisa test CE marked with clear route to market in the Europe and next generation magnetic test being developed.

• Research Use Only in the US, but distribution deal done with IBL and talking to Labcorp. Going for full FDA approval.“

- This 2018 document from CardiNor’s website indicates BVXP was then a 21.5% Cardinor shareholder, and suggests BVXP’s investment could be worth up to £1.5m based on IIG’s purchase.

- Pre-Diagnostics is developing an early-stage AD test similar to BVXP’s Tau project. Pre-Diagnostics’ work studies amyloid beta peptides, and includes testing saliva as well as blood.

- Other Pre-Diagnostic projects involve tests to indicate i) the likelihood of suffering side effects from new AD treatments and; ii) the likelihood of developing Parkinson’s Disease.

- Pre-Diagnostics seems likely to become commercially viable before CardiNor. Snippets from this Pre-Diagnostics investment summary include remarks about a “licensing agreement by 2025, which also could create a basis for stock-listing or trade sale of shares“:

• In August 2023 a CDA was signed with a global pharma company (intention of entering into an R&D collaboration).

• Validation of fluid biomarkers ongoing, industrial validation expected by end of 2023

• Substantial amount raised in form of non- dilutive grants (MNOK 70), of which MNOK 25 of the grants still remains to be received from the RCN during 2023-25

• In 2022 Pre Diagnostics was selected as a client by a top-tier global financial services firm, highly specialised in Diagnostics and Device. The management team is aiming at a licensing agreement by 2025, which also could create a basis for stock-listing or trade sale of shares.“

- This 25-page Pre-Diagnostics investor presentation supplies further information, but the absence of any monetary values within the document is notable.

- Perhaps coincidentally, the research and technology used by Pre-Diagnostics was established initially by one of the Gothenburg researchers currently testing BVXP’s Tau antibodies.

- This 2020 document from Pre-Diagnostics’ website indicates BVXP was at the time a 7.5% Pre-Diagnostics shareholder.

Financials

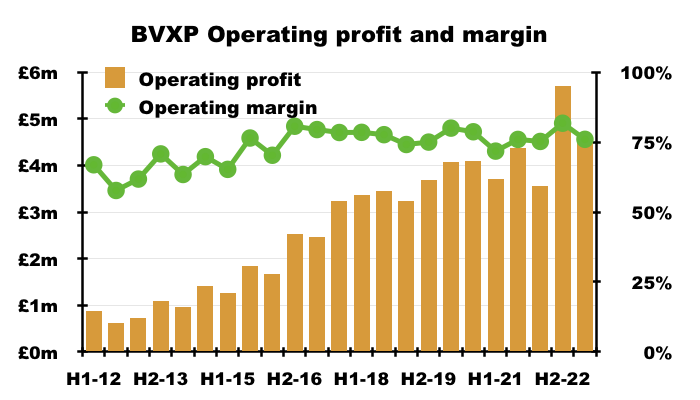

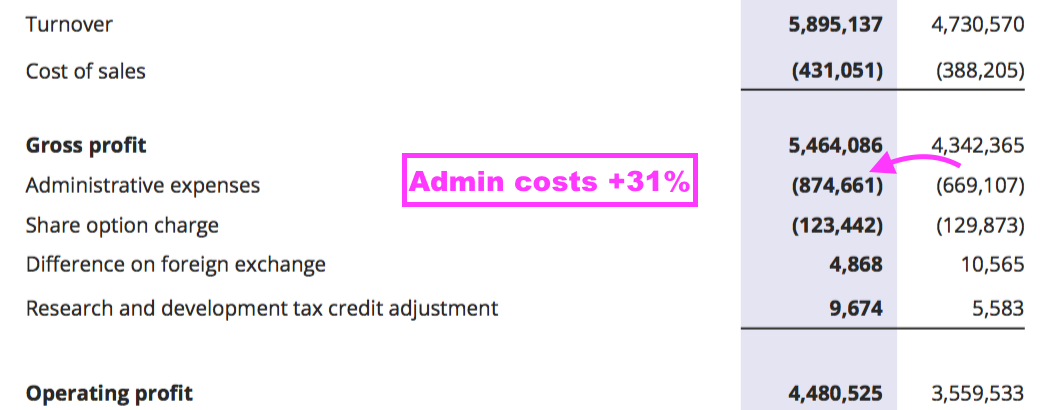

- This H1 could not repeat the astonishing 82% operating margin from the preceding H2 2022. BVXP could convert ‘only’ 76% of revenue into profit:

- Admin costs advanced at a faster pace than revenue (31% versus 25%):

- BVXP’s super margin will be trimmed if admin costs continue to outrun revenue.

- The house broker

was toldsurmised BVXP was not immune to wage inflation:

“Operating cash expenses increased 35% to £0.8m, which reflected inflation-adjusted salary increases, some one-off cost-of-living increases to ensure staff retention and bonus-related accruals“

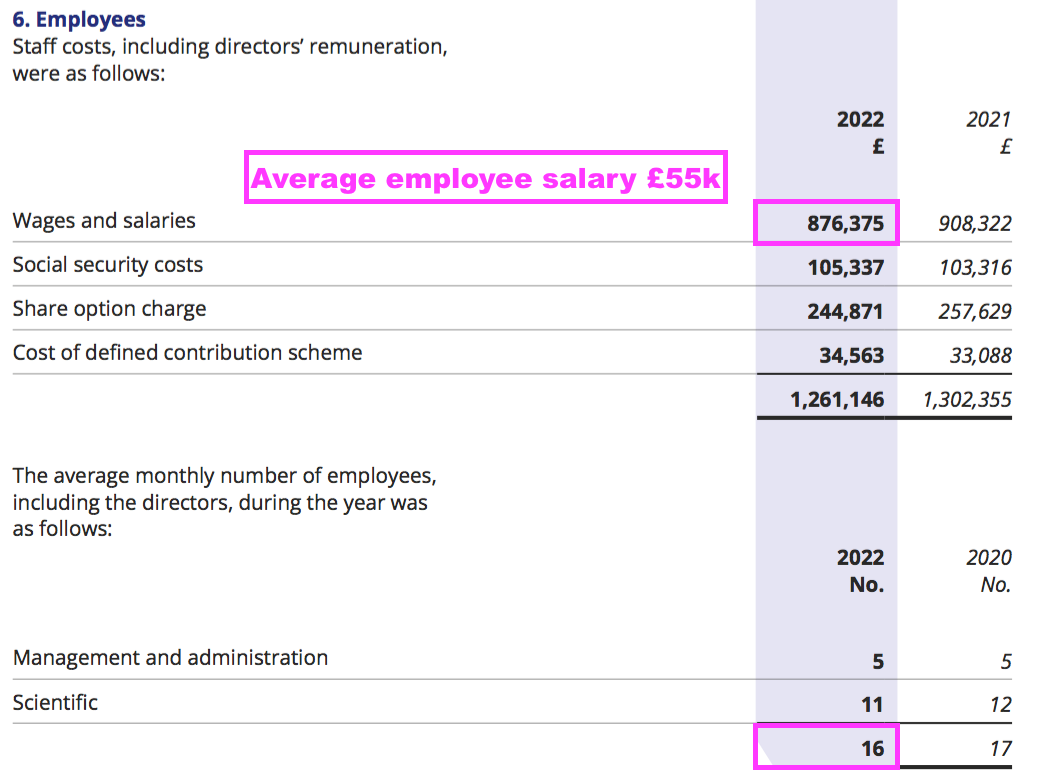

- The preceding FY showed 16 employees being paid total salaries of £876k or £55k each:

- I do wonder whether BVXP’s employees will ever demand much greater salaries to reflect the significant economic value they have created for shareholders.

- After all, the gap between employee costs and revenue per employee has expanded to beyond £600k…

- …which leaves ample room for further pay rises.

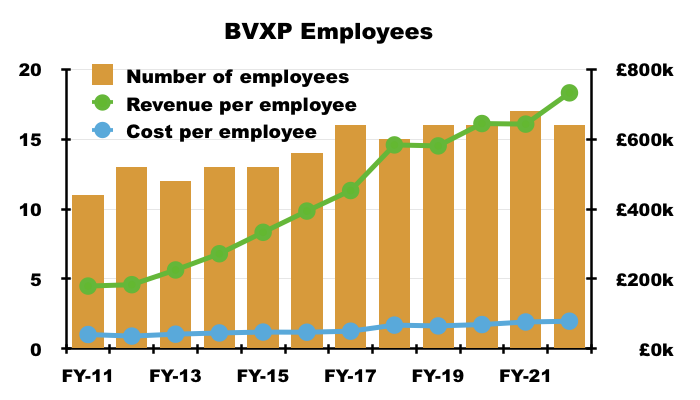

- BVXP’s employee costs are mostly R&D, which is all expensed as incurred and at present generates no associated revenue.

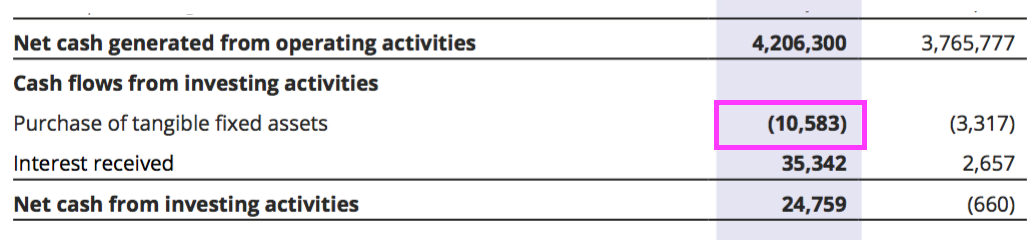

- As well as employing only 16 people, BVXP’s capex during this H1 amounted to just £10k:

- The tiny capex plus a favourable debtor movement allowed earnings of £3.7m to convert into free cash of £4.2m, which in turn helped fund the preceding FY’s H2/special dividends of £5.2m.

- BVXP’s cash position therefore finished the six months £1.0m lighter at the aforementioned £5.1m.

- The balance sheet carries no bank debt and no pension complications.

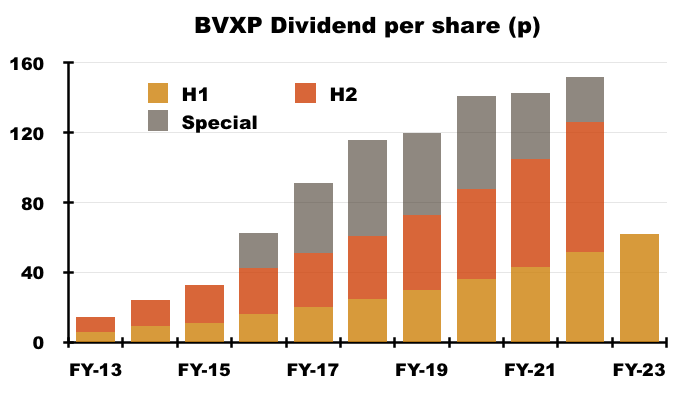

- BVXP has declared special dividends during each of the last seven years, but unless a very strong H2 occurs, the eighth special dividend could be BVXP’s lowest.

- A 19% lift to the H2 dividend (to 88p per share) to match this H1’s 19% dividend advance would supply a total 150p per share ordinary payout that would cost £7.8m.

- Doubling up this H1’s free cash flow gives £8.5m — leaving £0.7m spare for a special payout if BVXP were indeed to pay total FY 2023 ordinary dividends of £7.8m.

- £0.7m equates to just 13p per share, and compares to the 20p, 40p, 55p, 47p, 53p, 38p and 26p per share special payouts declared since FY 2016.

- BVXP has a commendable history of returning the vast majority of earnings to shareholders. Between FYs 2016 and 2022, BVXP has declared aggregate earnings of £42m while paying cash dividends of £39m.

- This H1 mentioned tax changes, which may be management code to expect lower dividend growth:

“Forthcoming changes to both the UK Corporation Tax structure in respect of Research and Development and the headline rate of Corporation Tax will have an impact on our future reported earnings and cash flows. Nevertheless, we will endeavour to follow our established dividend policy…“

- Within the preceding FY, BVXP commendably disclosed the new 25% tax rate would have lifted the company’s tax charge from 17% to 23% — and would have reduced earnings by nearly 7%:

“Factors that may affect future tax charges

The rate of corporation tax in the UK is set to be increased from the current rate of 19% to 25% with effect from 1 April 2023. This change will increase the tax charge in future years such that, had the change been in place in the current year, it would have increased by £517,163 from £1,603,874 to £2,121,037.“

- BVXP may well declare an FY 2023 special payout that leaves total dividends uncovered by earnings. The preceding FY for example declared earnings of 147p per share that did not entirely cover the 126p per share ordinary dividend and 26p per share special payout.

- The aforementioned £5.1m cash position generated H1 interest of £35k — BVXP’s highest ever for an H1 and a reflection of higher bank rates.

Valuation

- BVXP’s outlook did not appear too negative:

“In conclusion, after the difficulties experienced during the pandemic, we are pleased to see a solid performance of our core business and look forward to this continuing over the remainder of the year. We remain optimistic about our troponin revenues and the success of these high sensitivity troponin products around the world and we look forward to reporting further progress in the second half of the year. “

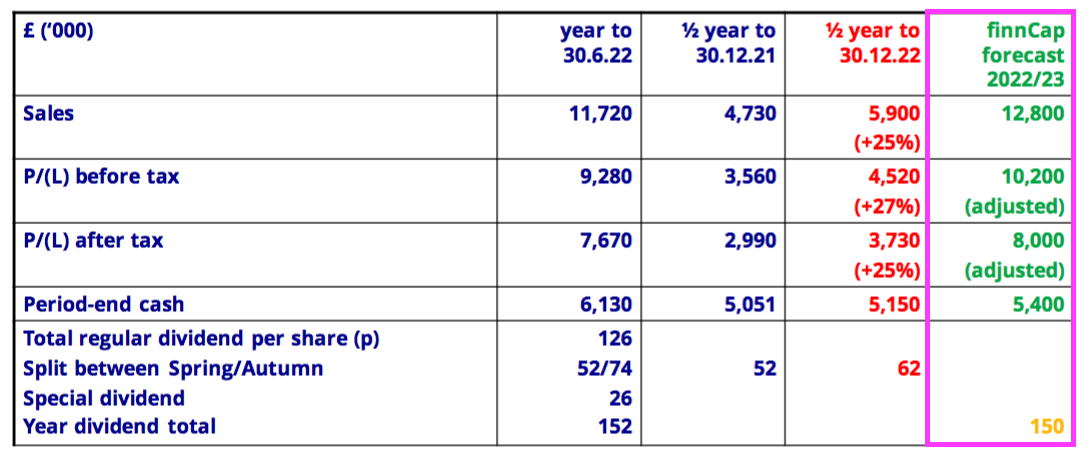

- The H1 presentation included the house broker’s forecasts for FY 2023:

- Predicted FY 2023 revenue of £12.8m implies H2 2023 revenue of £6.9m — a fraction lower than the £7.0m reported for the preceding H2.

- Predicted FY 2023 pre-tax profit of £10.2m implies H2 2023 pre-tax profit of £5.7m — equal to the £5.7m reported for the preceding H2.

- Predicted FY 2023 post-tax profit of £8.0m implies H2 2023 post-tax profit of £4.3m — 9% less than the £4.7m reported for the preceding H2 due to a higher projected (22%) tax rate.

- Predicted FY 2023 earnings of £8.0m equate to 153p per share and support a 23x multiple with the share price at £35.

- Earnings of 153p per share do not cover the trailing ordinary and special dividend total of 162p per share.

- Bear in mind troponin revenue will cease during 2032 and the associated profit should not therefore be valued on a simple multiple.

- Assuming troponin revenue:

- Averages (a possibly optimistic) £3.5m for the next nine years before expiry;

- Has no associated cost, and;

- Is taxed at the new 25% standard UK rate…

- …gives an after-tax value of £24m before any time-value discounting.

- The table below derives the possible earnings from BVXP’s vitamin D and other commercialised antibodies by:

- Estimating calendar-year 2022 revenue without troponin;

- Then subtracting all cost of sales and administration expenses;

- Then adding back (estimated) R&D costs, and;

- Ignoring foreign-exchange gains, share-based payments and R&D tax credits:

| Estimated CY 2022 for vitamin D and other antibodies | (£k) |

| Revenue | 12,884 |

| Less troponin revenue | (1,530) |

| Less cost of sales | (753) |

| Less admin expenses | (1,811) |

| Add back R&D expenses | 1,100 |

| Operating profit | 9,890 |

| Less tax at 25% | (2,472) |

| Earnings | 7,417 |

- Applying a 20x multiple to the derived £7.4m earnings values BVXP’s vitamin D and other commercialised antibodies at £148m.

- The present £183m market cap less the £24m troponin estimate less the £148m vitamin D/other estimate therefore leaves the pipeline valued at £11m.

- Valuing the pipeline at £11m might seem optimistic given:

- Annual R&D costs are approximately £1m;

- The pipeline effectively rests on Tau, and;

- Tau commercialisation is not expected until 2030 at the earliest.

- True, these valuation sums could be fine-tuned to:

- Calculate a more realistic net present value for troponin;

- Include R&D tax credits;

- Allocate cost of sales to the appropriate antibody, and;

- Apply different multiples to that £7.4m vitamin D/other earnings estimate…

- …but right now signs of a compelling valuation are not truly obvious.

- The sums could explain why the shares have not made headway during the last four years:

- A premium rating is nonetheless understandable. Shareholder attractions remain:

- The predictable and ongoing income from antibodies (pandemics aside) for ten years or more, due in part to the cost/time/upheaval/risk of replacing proven blood-test biomarkers with upgraded versions.

- A competitive ‘moat’, helped in part by protracted development/regulatory timescales and ‘captive’ end-customers (e.g. hospitals) restricted to particular blood-test machines (and therefore particular diagnostic antibodies), and;

- The amazing margins and minimal reinvestment requirements, which underline the terrific economics of antibody commercialisation.

- The present market cap seems to reflect the “sustainable” 8-10% growth rate cited with the preceding FY.

- Longer-term upside therefore seems very dependent on the success of the pipeline, with the Tau project most likely to generate a step-change to future earnings.

- While further Tau developments are awaited, the trailing 136p per share ordinary dividend supplies a 3.9% income from the £35 shares.

Maynard Paton