08 October 2023

By Maynard Paton

Happy Sunday! I trust your shares are coping well during this lacklustre market.

A summary of my portfolio’s progress:

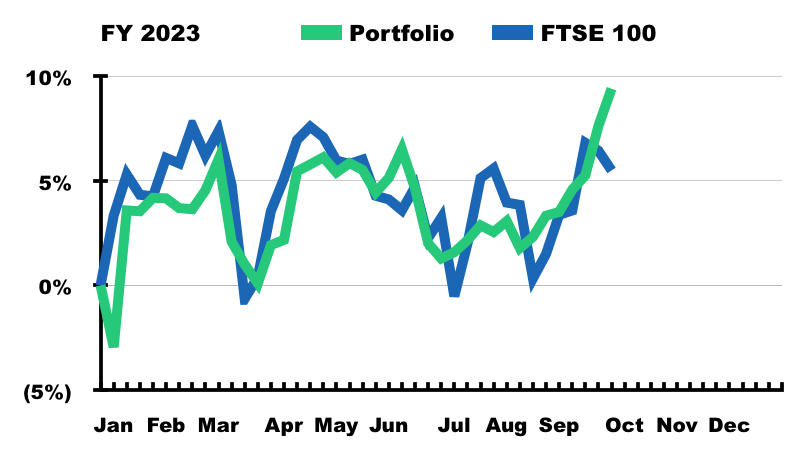

- Q3 return: +8.0%* (FTSE 100: +2.2%).

- Q3 trades: 1 Sell (Tasty).

- YTD return: +9.4%* (FTSE 100: +5.5%).

- YTD winners/losers: 5 winners vs 6 losers.

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

My year-to-date performance has improved as I slowly recover from last year’s 23% drubbing. This Q3 was in fact my portfolio’s strongest three months since June, July and August 2021 (+8.7%), and I now need ‘only’ a 19% advance to revisit my all-time high of December 2021.

Company RNSs from my portfolio during Q3 were generally acceptable, although lower profits were reported by City of London Investment, Mincon and M Winkworth that may limit scope for higher future dividends.

Anecdotally at least, the frequency of small-cap warnings appears to be rising, and I therefore hope my portfolio’s mix of owner-orientated managers, respectable competitive positions and asset-rich balance sheets will help my shares navigate through any difficult times.

My 2023 progress has become dominated by System1, which during this Q3 issued details of a stronger H2 that followed boardroom pressure from disgruntled shareholders. Elsewhere within my portfolio, the market looks to have belatedly woken up to Tristel’s regulatory approval in the United States while an enormous special dividend has helped the share price of Andrews Sykes.

I have summarised below what happened to my portfolio during July, August and September. (Please click here to read all of my previous quarterly round-ups). I will then explain how I have enjoyed 100% returns from ordinary dividends.

Contents

- Q3 share trades

- Q3 portfolio news

- Q3 portfolio returns

- Enjoying 100% returns from ordinary dividends

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tristel and M Winkworth.

Q3 share trades

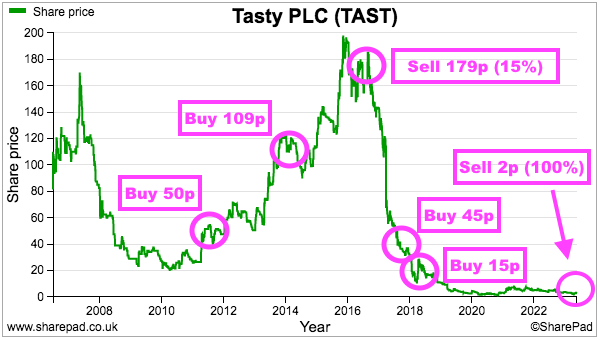

I sold my entire Tasty holding during Q3 at approximately 2p per share including all costs.

I had hoped the hapless restaurant chain could one day instigate a turnaround and prompt the bombed-out share price to stage a dramatic recovery. But some further reflection and sudden liquidity in the shares prompted me to finally exit this disaster story and lock in an 85% overall loss:

I belatedly recognised Tasty’s menu format and cost structure was inherently flawed, and concluded only a radical business overhaul could rescue the business. Lots of lessons to be learnt here, not least that weakened industry economics (e.g. through a much higher minimum wage) can trump an appealing management track record that was achieved during more favourable times.

Tasty becomes the eighth share I have bought and then sold at a loss since the start of 2004. Those eight shares are outnumbered by the 24 winners I have purchased during the same time.

Q3 portfolio news

As usual I have kept watch on all of my holdings. The main Q3 developments are summarised below:

- An enormous 59p per share special dividend included within steady H1 figures from Andrews Sykes.

- FY results confirming clients withdrawing $257m and profit down 15% at City of London Investment.

- H1 mining-related revenue down 15% and 25% lower earnings at Mincon.

- An H1 update referring to “current economic headwinds” and signalling a £19 NAV per share at S & U.

- A stronger H2 underpinning the H1 strategic review but FY ‘profit’ still complicated by adjustments at System1.

- A statement indicating a better-than-expected FY performance, with revenue of £36m and profit of £6m, from Tristel.

- H1 profit down 26% but ordinary dividends up 7% at M Winkworth.

- Nothing of major significance from Bioventix, Mountview Estates and FW Thorpe.

Q3 portfolio returns

The chart below compares my portfolio’s weekly 2023 progress to that of the FTSE 100 total return index:

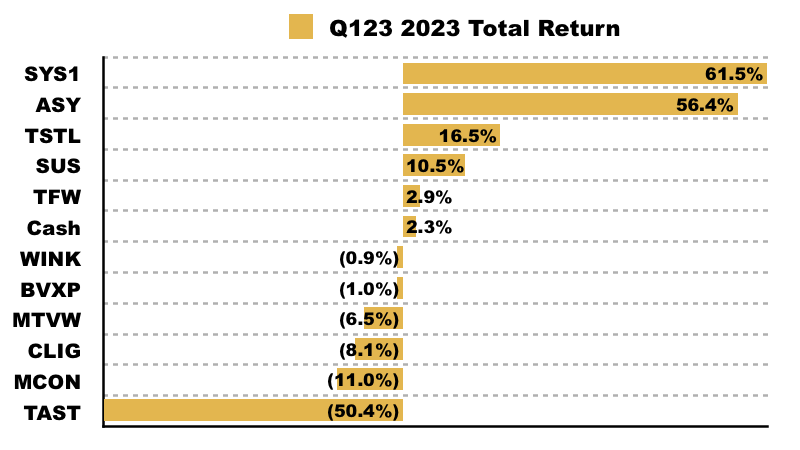

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me year to date:

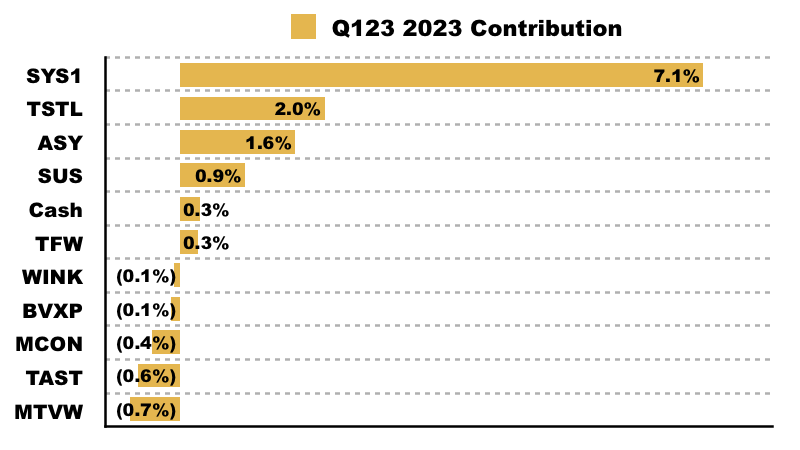

This chart shows each holding’s contribution towards my 9.4% YTD gain:

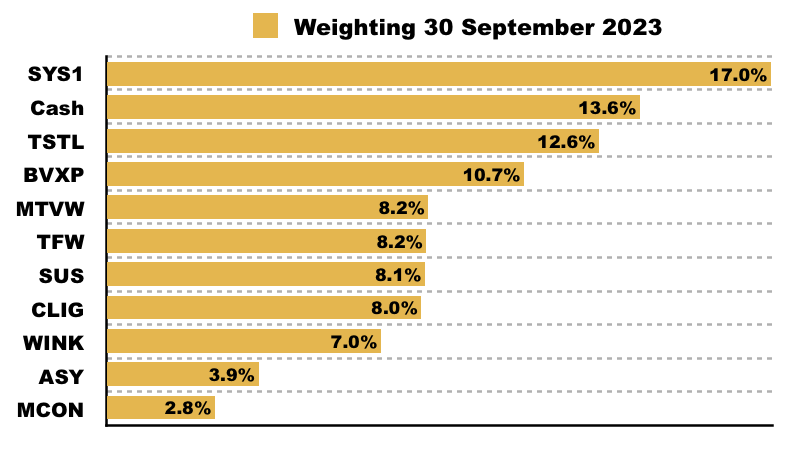

And this chart shows my portfolio’s holdings and their weightings at the end of Q3:

Enjoying 100% returns from ordinary dividends

Perhaps I should become a dedicated dividend investor.

During my regular podcasts with income guru Roland Head, I have gradually realised four of my ten shares have repaid my initial investment back through payouts alone. A fifth share will achieve the same feat later this month.

If your portfolio — like mine! — has found capital gains somewhat elusive during recent years, then maybe an income bias could assist your total return. Let’s take a closer look at my dividend record.

A portfolio-dividend study

To keep things simple, I have limited this study to my ten current holdings and determined their ‘buy prices’ using my very first purchase of each share.

I have not accounted for any subsequent buys and sells, so the calculations are not a precise reflection of my dividend returns. But I am very sure the overall picture is accurate enough. I have also used SharePad’s comprehensive database for the dividend stats:

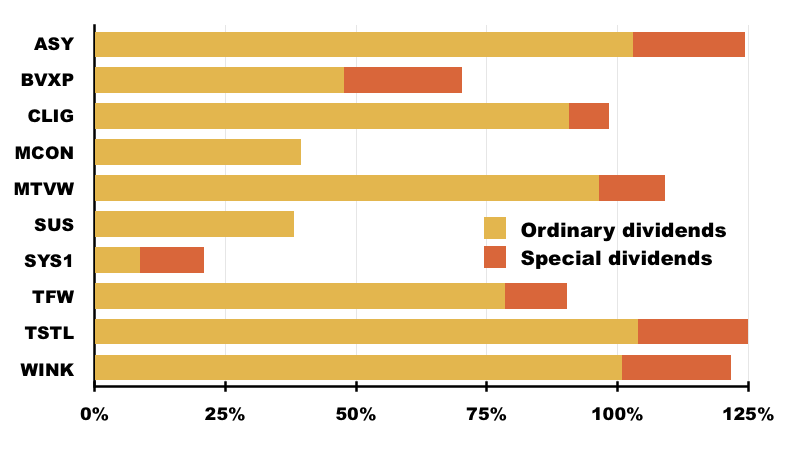

This chart shows the percentage returns:

Tristel, Andrews Sykes and M Winkworth have repaid my initial purchase price through ordinary dividends alone, while Mountview Estates has achieved the same feat with special payouts included.

City of London Investment is 98% there, and the forthcoming payment of its final 22p per share dividend will take me over the magic 100%.

A few more details about these five holdings:

1) Tristel

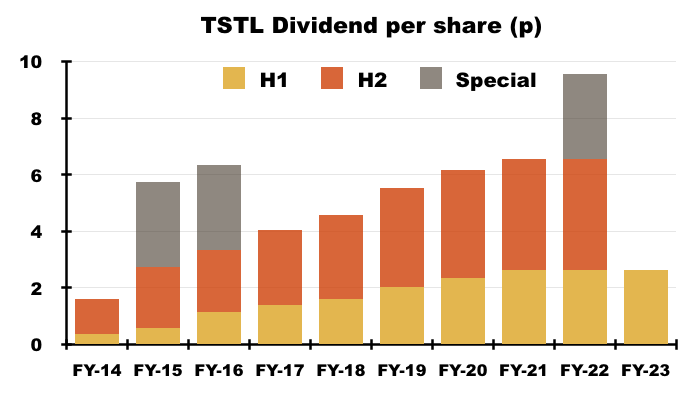

I first acquired Tristel during December 2013 at 42p and my initial twelve-month income was 1.62p per share giving a 3.9% yield.

The ordinary payout has since advanced to 6.55p per share to deliver cumulative ordinary payouts of 43.7p per share. Three specials take that total to 52.7p per share:

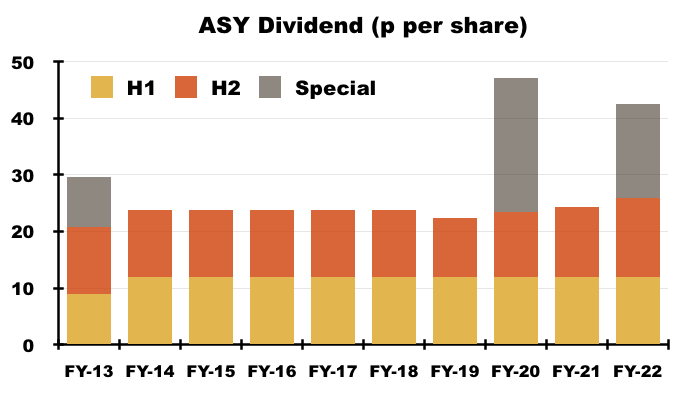

2) Andrews Sykes

I first bought Andrews Sykes during May 2013 at 229p and my initial twelve-month income was 20.8p per share giving a 9.1% yield.

The ordinary payout has since advanced to 25.9p to deliver cumulative ordinary payouts of 236p per share. A trio of specials take that total to 285p per share:

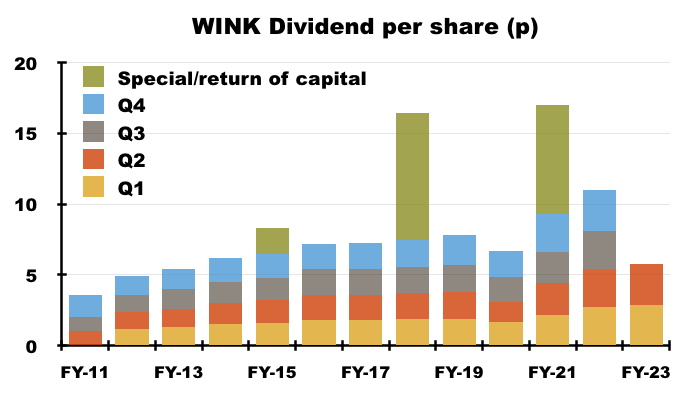

3) M Winkworth

I first purchased M Winkworth during June 2011 at 89p and my initial twelve-month income was 4.8p per share giving a 5.4% yield.

The ordinary payout has since advanced to 11.4p per share to deliver cumulative ordinary payouts of 89.5p per share. Various specials and a return of capital take that total to 108p per share:

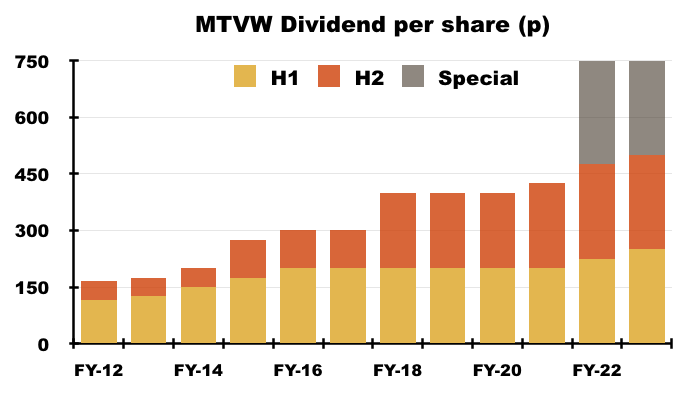

4) Mountview Estates

I first acquired Mountview Estates during November 2011 at £41.64 and my initial twelve-month income was 165p per share giving a 4.0% yield.

The ordinary payout has since advanced to 500p per share to deliver cumulative ordinary payouts of £40.15 per share. Two specials take that total to £45.40 per share:

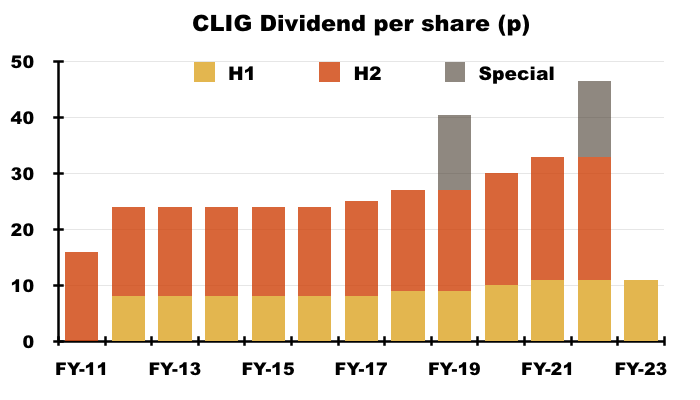

5) City of London Investment

I first purchased City of London Investment during August 2011 at 355p and my initial twelve-month income was 24p per share giving a 6.8% yield.

The ordinary payout has since advanced to 33p per share to deliver cumulative ordinary payouts of 322p per share. Two specials take that total to 349p per share:

Capturing a dividend ‘bagger’

Those five shares offer five points to help you enjoy 100% returns on your investments through dividends alone:

1) Lots of patience: Recouping your investment from dividends will require a long holding period. Tristel became an income ‘bagger’ for me after nine years, with Andrews Sykes taking ten years and M Winkworth and Mountview Estates taking twelve.

2) Generous starting yield: The 9.1% early income at Andrews Sykes required only a 2% annual compound dividend increase to recoup my initial investment, while the 6.8% yield at City of London Investment needed the payout to compound at just 3% a year.

3) High dividend growth: Tristel’s dividend quadrupled over nine years to give super 15%-plus annualised increases. Pinpointing such income growth in advance is not easy, but if achieved can deliver sensational income returns (as well as immense capital gains!).

4) First-class financials: Strong businesses with superior financials are more likely to withstand market trouble and keep their payouts going. At the time of my purchases, robust margins, net cash and healthy cash conversion were exhibited by Andrews Sykes, City of London Investment and M Winkworth, while Mountview Estates was backed by decades of illustrious NAV growth.

5) Owner managers: Board members aligned fully with outside investors may well be the most important feature of 100%-plus dividend returns…

…not least because such leaders are less likely to waste surplus cash on daft acquisitions or strategic follies.

Andrews Sykes, M Winkworth, Mountview Estates and City of London Investment offered significant insider ownership at the time of my purchases and then throughout my shareholder tenure. Their respective boards simply focused on generating surplus money to return to shareholders through ordinary and special payments.

A bias towards owner managers has also led to eight of my ten shares paying special dividends during my time as a shareholder.

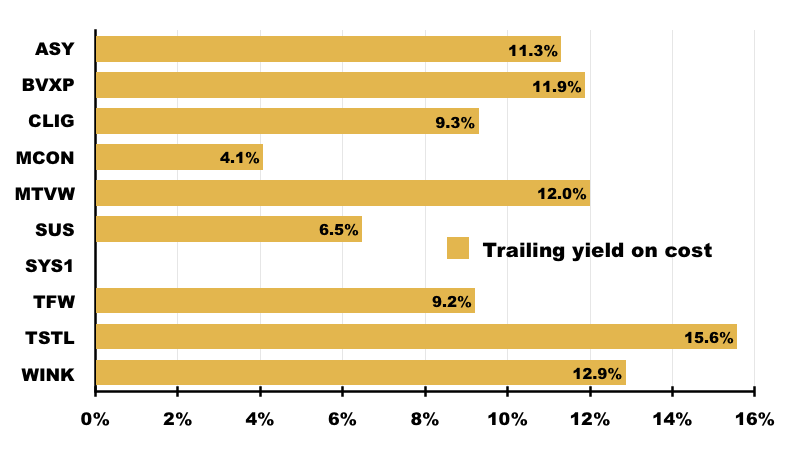

Double-digit yields on cost

This next chart shows the trailing yields I currently enjoy based on my initial purchase cost:

I am pleased five of my shares have lifted their dividends to now supply yields-on-cost of 10% or more. Another two are presently yielding 9% on cost.

Of the shares yet to become dividend ‘baggers’, FW Thorpe should achieve the magic 100% mark within the next twelve months. Bioventix meanwhile may take until late 2025 assuming it continues to maintain its regular special payout. Both of these shares match points 3), 4) and 5) above.

S & U could sadly take another ten years if its ordinary dividend remains static, which just goes to show how owner-managed companies may not deliver great returns if you invest at too high a price!

Then there’s Mincon, which by my reckoning could take another 15 years to recoup my initial investment if its dividend is left unchanged. The drill group’s payout has barely moved (jn EUR terms) since my initial purchase eight years ago on a 3% income.

Finally System1, which scrapped its payout three years ago during a bold transition from consultancy work to data supplier.

This market researcher once offered decent margins, respectable cash flow, net cash, a rising ordinary payout, the occasional special dividend and substantial director shareholdings — which just goes to show what seems like a sensible investment can still evolve into a major income disappointer.

Let me finish by saying I hope to improve my dividend returns further through ongoing discussions with Roland. You can listen to our conversations through this premium podcast service >>

Until next time, I wish you safe and healthy investing.

Maynard Paton

This is really good Maynard. Probably your best piece yet. Although we have shared stocks in our portfolios over the years (BVXP, TSTL) I have never taken dividends seriously as my main priority has been to aim for capital gains. Dividends have always been a bi-product, a good to have but not necessary, after reading this I will have to consider this more seriously. I do have some holdings which I have held onto and bought at sig lower prices that have provided generous dividends (well at least to me!) ELIX, NIOX though so that goes to my credit. Well done!

Thanks MG. Must admit for years I never took dividends that seriously until I decided to add up what I had collected. Dividends can help our total shareholder returns, especially when capital gains are elusive/temporary.

Maynard