01 February 2024

By Maynard Paton

H1 2023 results summary for Mincon (MCON):

- An underwhelming H1 performance caused by reduced mining-customer activity, with revenue down 5%, profit down 12% and an unchanged dividend paid more than two months later than normal.

- This H1 was overshadowed by October’s Q3 update, which warned of weaker sales, lower margins, exceptional costs and H2 Ebitda dropping 45%.

- The Q3 update — and possibility of a difficult FY 2024 — heightened concerns about the group’s debt covenants, capital-intensive growth strategy, dividend payments and boardroom personnel.

- Hopes of improved financials seem to rest upon a mining-customer revival, further geothermal installations plus R&D projects such as Greenhammer and subsea micropiling becoming commercial successes.

- The shares currently trade below their 2013 flotation price and leave minority investors trusting the 56% family owners take the necessary action to safeguard the business. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own MCON

- Results summary

- Revenue, profit and dividend

- Sector performances

- Greenhammer

- Subsea micropiling and large-diameter hammer systems

- Financials: margin

- Financials: stock

- Financials: cash flow and net debt

- Q3 trading update

- Boardroom and strategy

- Valuation

News links, share data and disclosure

- Interim results and presentation for the six months to 30 June 2023 published 08 August 2023;

- Appointment of chief operating officer published 04 July 2023, and;

- Q3 trading update published 09 October 2023.

- Share price: 54p

- Share count: 212,472,413

- Market capitalisation: £115m

- Disclosure: Maynard owns shares in Mincon. This blog post contains SharePad affiliate links.

Why I own MCON

- Designs and manufactures industrial drills, with sales supported by established reputation, engineering excellence, technical innovation and first-class service.

- Boasts veteran family management with 46-year tenure, 56%/£64m shareholding and very long-term perspective.

- Market cap close to book value offers recovery potential should mining revenue rebound and “transformational” new products enjoy commercial success.

Further reading: My MCON Buy report | All my MCON posts | MCON website

Results summary

Revenue, profit and dividend

- A mixed Q1 trading update during May that referred to reduced mining-customer activity…

“While revenue in Q1 2023 was marginally behind the same period in the prior year, we are pleased with further improvement in our gross margin in the first quarter. The reduced revenue in Q1 is a result of lower revenue than expected in the mining industry, due to reduced activity in the exploration sector during the quarter and resultant lower orders from some specific large customers as they adjust their inventories in response. However, we remain confident in our outlook for this segment and expect that our mining revenue will improve as the year progresses.”

- …had already suggested this H1 2023 would not be spectacular.

- Both revenue and profit in fact registered declines versus the comparable H1.

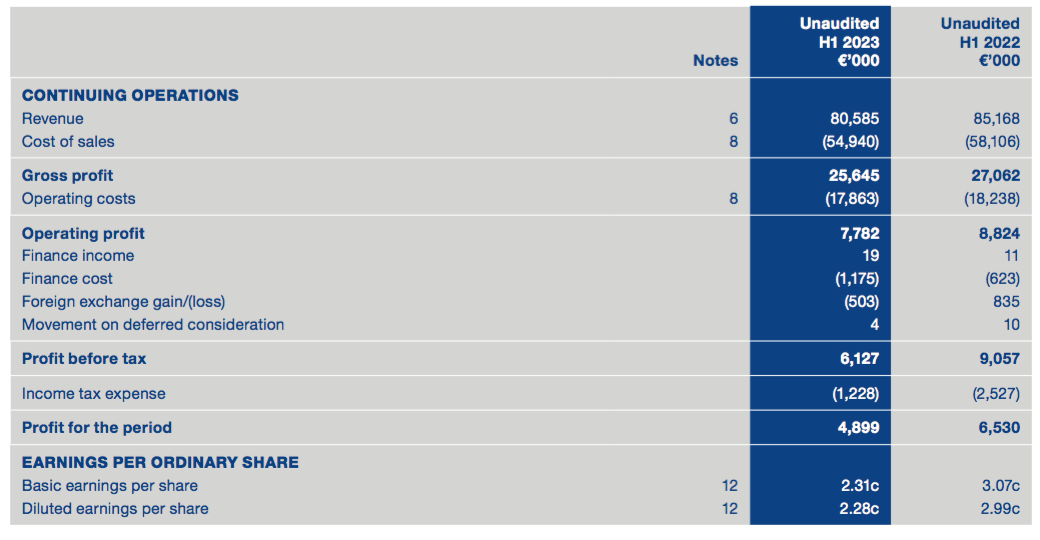

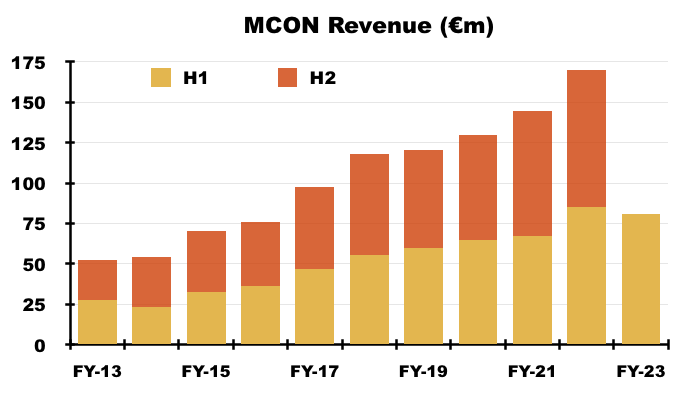

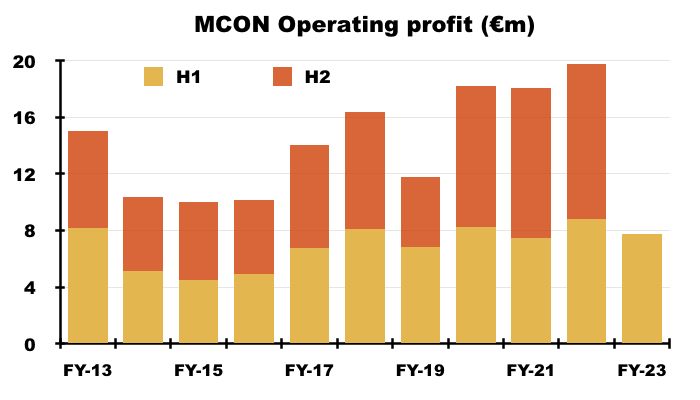

- H1 revenue slid 5% to €81m to leave H1 operating profit down 12% at €7.8m:

- This H1 reiterated how slower mining activity had curtailed progress:

“H1 2023 has been a challenging period for Mincon with our revenue behind the same period in the prior year, primarily due to a shortfall in our sales to the mining industry and FX headwinds. This performance in the sector is down to several factors but mainly due to reduced exploration activity and certain larger customers taking advantage of improved freight conditions to reduce inventories. We are, however, working on regaining some of this revenue with some positive drilling results from customer testing that we are doing in all our regions, most notably in APAC.”

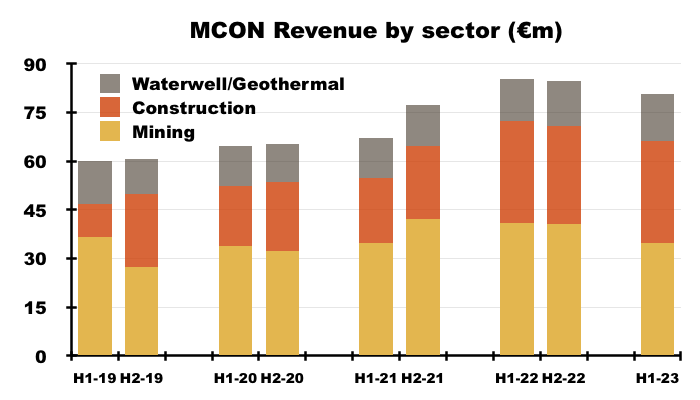

- Mining-related sales actually declined 15%, with construction-related revenue flat and waterwell/geothermal-associated sales up 10% (see Sector performances).

- MCON claimed adverse currency movements alone were responsible for total revenue sliding 3%.

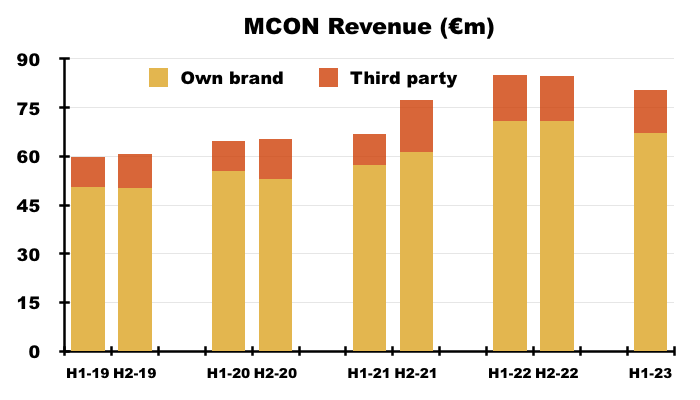

- Both MCON-developed products and third-party equipment suffered sales shortfalls of approximately 5%:

- May’s Q1 update had mentioned “better margins“:

“Our price increases, introduced in 2022 to offset manufacturing and operating cost increases, have also contributed to better margins than in the first quarter of 2022.”

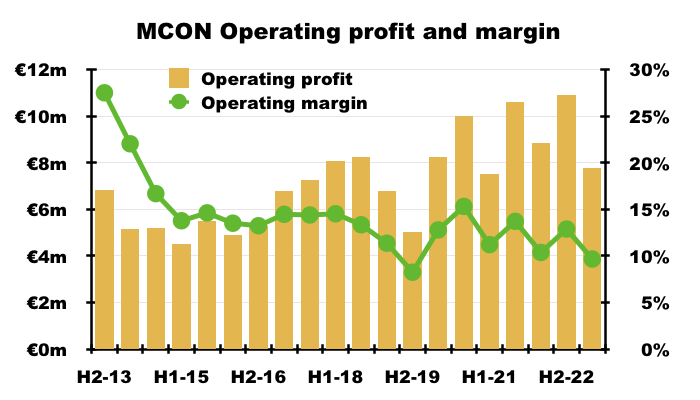

- But the 31.8% gross margin for this H1 only matched the 31.8% registered during the comparable H1, while the 9.7% operating margin for this H1 was below the comparable 10.4% (see Financials: margin).

- The 9.7% H1 operating margin was in fact the lowest H1 operating margin since MCON floated during 2013, and raised further questions about why the group’s “innovative engineering and industry-leading quality” (point 1) cannot translate into superior profitability.

- This H1 was overshadowed by October’s Q3 update, which admitted to:

- Year-to-date sales declining 7%;

- Q4 suffering deferred and/or cancelled construction-project revenue;

- The year-to-date gross margin reducing to 30.8%, and;

- Full-year Ebitda sliding to approximately €20m, which suggested H2 Ebitda would dive 45% (see Q3 trading update).

- Suffice to say, the Q3 update raised even further questions as to whether the group’s “innovative engineering and industry-leading quality” will one day translate into superior profitability.

- The Q3 update also raised concerns about MCON’s debt covenants and dividend policy (see Financials: cash flow and net debt).

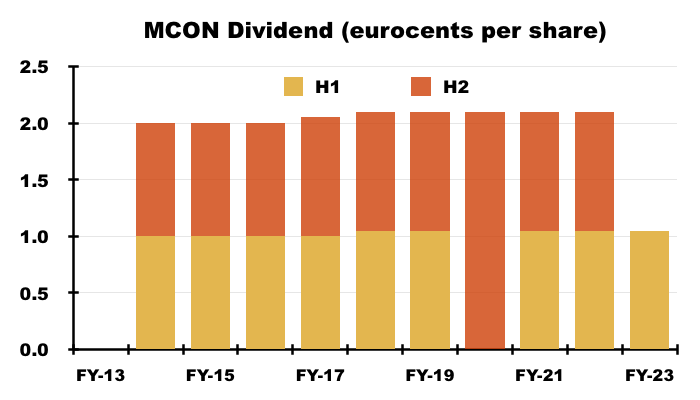

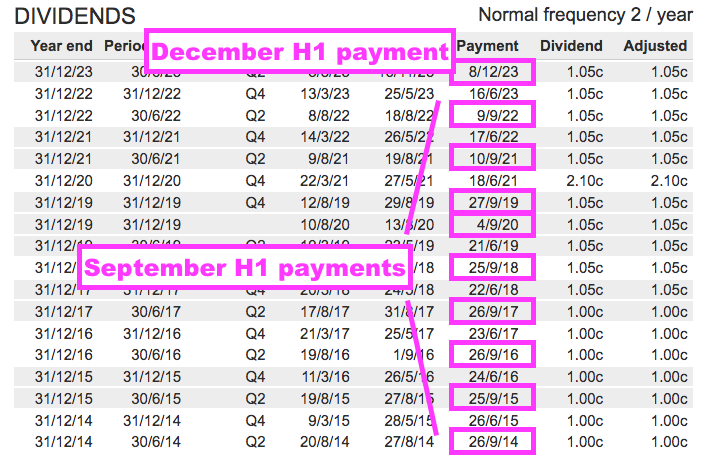

- The H1 dividend was set once again at 1.05 eurocents a share…

- …and was paid during December:

“The Board of Mincon has approved the payment of an interim dividend in the amount of €0.0105 (1.05 cent) per ordinary share, which will be paid to shareholders in December 2023.”

- Previous H1 dividends were paid during September:

- Delaying the dividend payment by a few months was (with hindsight) an omen that all was not well with trading and/or cash flow.

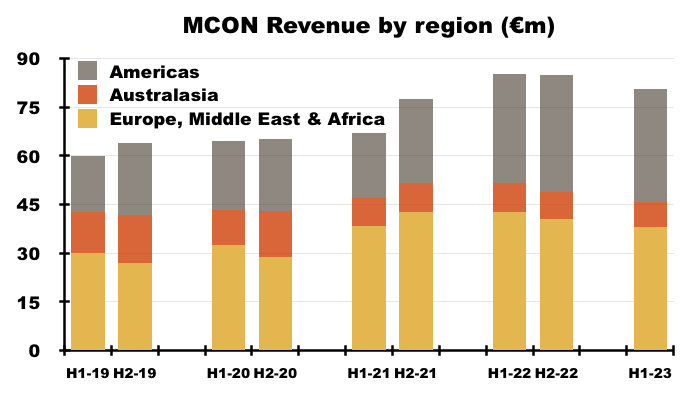

Sector performances

- The reduced mining-customer activity left H1 mining revenue at approximately €35m to represent 43% of total revenue:

- 43% is the lowest mining-revenue proportion since at least H1 2019, during which the sector supported 61% of group sales.

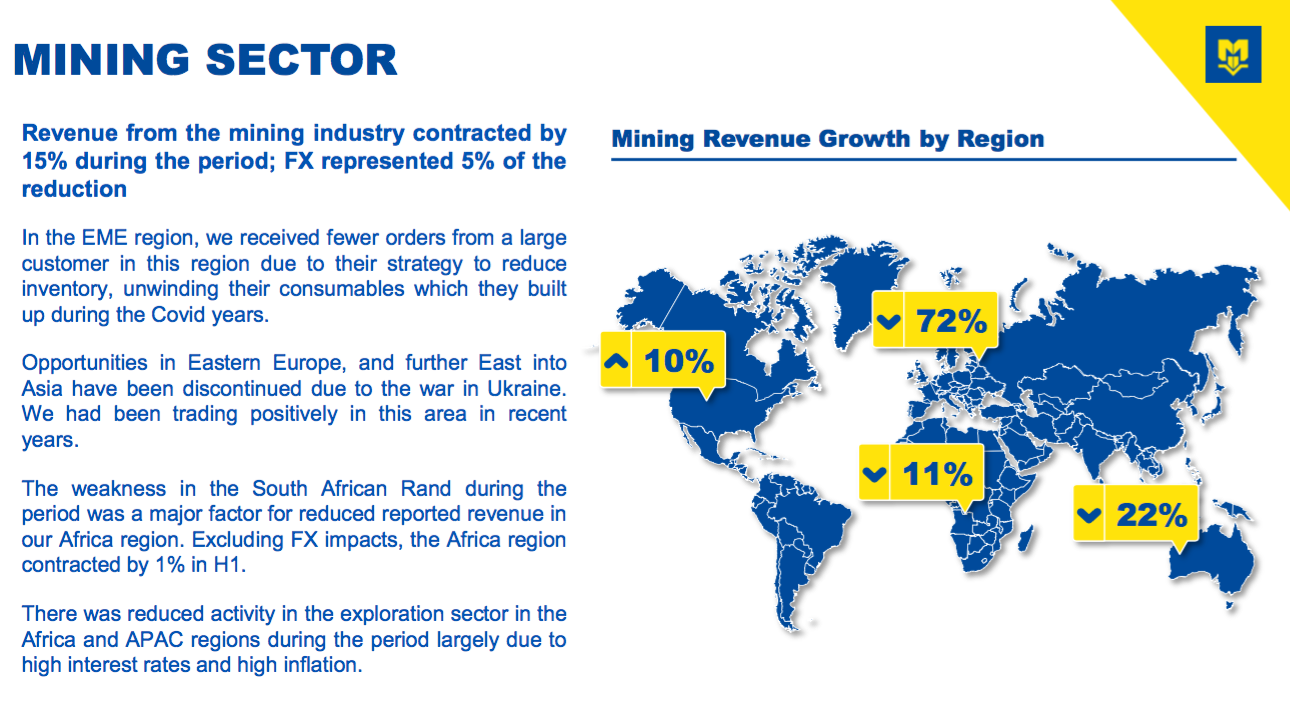

- Demand for MCON’s mining drills suffered wide regional variations during this H1, with Europe/Middle East suffering badly due to de-stocking by a large customer:

- The mining division’s H1 performance contrasted with the sanguine commentary expressed at the previous FY:

“Despite the difficult conditions prevailing in the global markets right now, we don’t expect any significant changes in the mining sector.

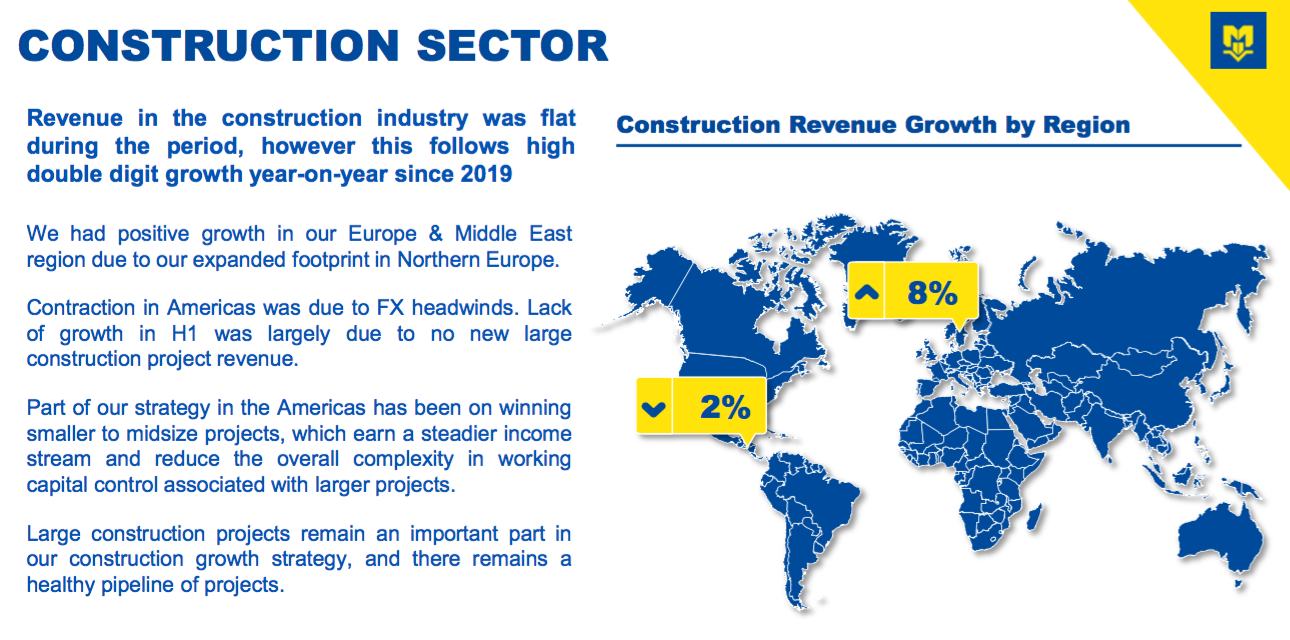

- An absence of large building projects in the United States left H1 construction-related revenue unchanged at approximately €31m:

- Construction sales represented 39% of group H1 revenue, the highest ever proportion for the division.

- This H1 anticipated some large construction projects would return during H2:

“In positive news, it is very pleasing to see that we have consolidated the gains we made last year in the construction sector, and more importantly, the revenue mix includes a higher proportion of smaller projects, which gives a more sustainable spread to the business. It is notable that there continues to be a strong pipeline of large projects that we are looking to land in H2 and beyond.”

- The subsequent Q3 statement sadly admitted some anticipated large projects did not materialise during Q4 (see Q3 trading update).

- Commentary about large mining customers and large construction contracts underlines the “contractual arrangements” and “customer concentration” risks cited with MCON’s annual report (point 2):

“The Group derives some of its revenue from large transactions (which may be non-recurring in nature). Prospective sales are subject to delays or cancellations over which the Group has little, or no control and these delays could adversely affect results…

…

During 2022, the Group’s top ten customers have accounted for approximately 24% of its revenues…”

- 24% of revenue supported by ten customers does not sound overly concentrated, but perhaps the profitability from those ten customers is much more significant.

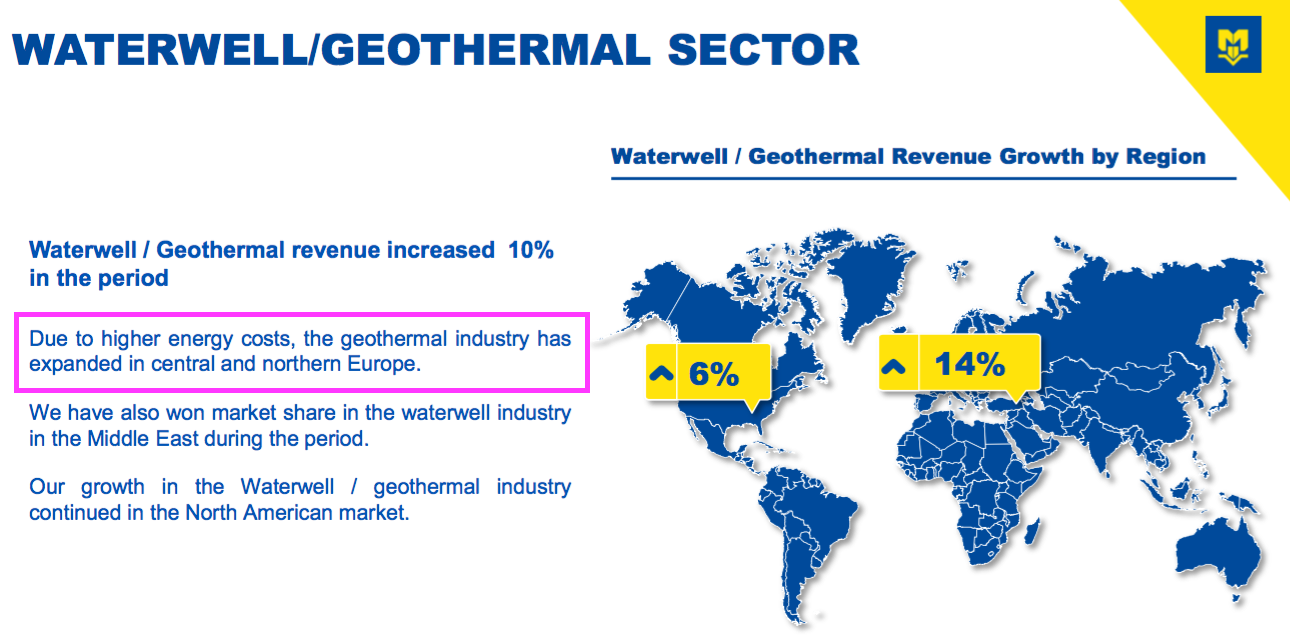

- Waterwells/geothermal was the only division reporting positive H1 progress, with sales up 10% to approximately €15m:

- H1 waterwells/geothermal revenue represented 18% of total revenue, and was within the 15%-22% range witnessed since H1 2019.

- The H1 presentation linked greater geothermal revenue to higher energy costs:

“Due to higher energy costs, the geothermal industry has expanded in central and northern Europe.”

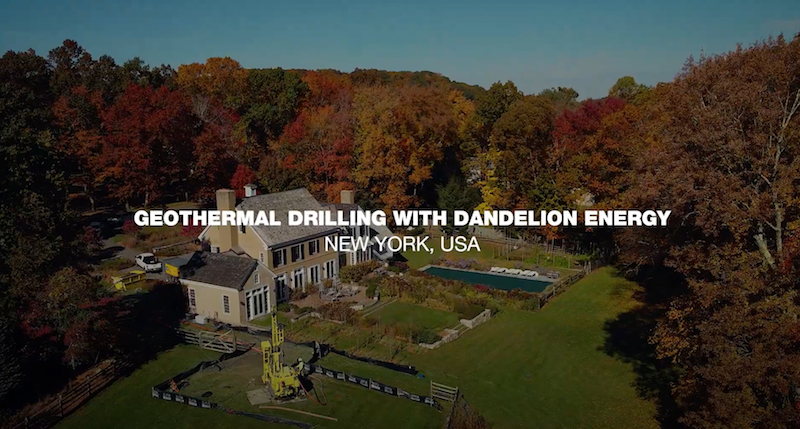

- MCON’s drills are used by Dandelion to ensure quick installations:

“Instead of using large drill rigs like those used to bore artesian wells, Dandelion began experimenting with smaller, more efficient drills that make one or two deep holes just a few inches wide.

The company then installs U-shaped pipes into these holes. This innovation takes up less space and creates less of a disturbance in the back yards of Dandelion customers.

Using the new equipment, installation of the ground loop pipes can be completed in days instead of a weeks, saving customers time and money.“

- The mixed divisional performances did not alter MCON’s geographical diversity, with revenue still split 47% from Europe/Middle East, 43% from the Americas and 10% from Australasia:

Greenhammer

- This H1 reiterated the “transformational” potential of MCON’s most promising new product:

“[Greenhammer:] Remains a transformational opportunity for Mincon as well as the hard rock surface mining industry, especially with regard to industry emissions reduction targets”

- To recap, Greenhammer was first mentioned within the FY 2016 results while the FY 2018 statement described the new drilling system as…

“[A] disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base”.

- …and suggested the design could enjoy a strong competitive advantage:

“This is not a small system or easily replicable, and we have placed patents around the system to protect it. The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.”

“Mincon is pleased to announce the signing of the first commercial contract for the Greenhammer system.

This milestone is the culmination of many years of development work and is the first step toward revenue generation with a unique drilling system that has a transformational potential for Mincon and the hard rock surface mining industry. The Greenhammer contract is with a blue-chip mining contractor operating on a major gold mine in Western Australia.“

- MCON also claimed the first contract had the potential to become a “multi-million-euro” deal, with initial revenue initially expected during H2 2022:

“The contract provides for the mobilisation of the Greenhammer system to be run on a Mincon-owned test rig as well as a full Mincon team to support drilling blastholes on an agreed price per metre drilled. The Greenhammer system is expected to be onsite at the mine and generating revenue early in Q4 2022.“

- But the FY 2022 statement cited ongoing discussions with rig manufacturers to create a reliable drilling platform:

“We believe that the successful roll out of this innovative [Greenhammer] drilling system will require that we closely collaborate with drilling manufacturers to ensure the system is properly supported on a reliable drill rig platform. With that in mind we have engaged in discussions with rig manufacturers with a view to developing mutually beneficial working relationships.”

- Sure enough, this H1 confirmed Greenhammer progress remains beset by rig problems:

“The [Greenhammer] system has been running on the gold mine in Western Australia but we continued to experience issues with the output of the rig in H1.

These issues are due to a lack of reliable rig power output and are unrelated to the Greenhammer system. We are still working on this and will have an update soon.

This emphasises the importance of our collaboration with a major rig manufacturer which is well progressed since our last update.“

- This H1 also announced Greenhammer was now being trialled within the US:

“We have engaged with a major rig manufacturer on a collaboration to prove out the system by converting one of their rigs and testing it at a location in the US. This is an attractive location as the largest rig population suitable for conversion to Greenhammer is in this market.”

- Development work on Greenhammer commenced around 2011, so an extra year or two waiting for the commercial success of the system may not be too concerning for MCON’s veteran board (see Boardroom and strategy).

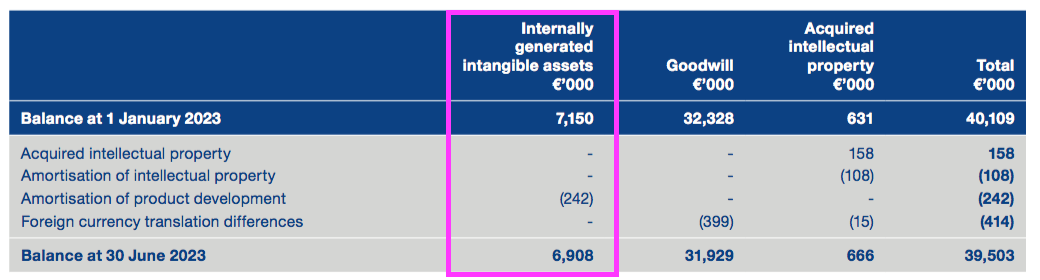

- Greenhammer amortisation of €242k was charged during this H1, leaving capitalised Greenhammer expenditure since FY 2016 of €6.9m still to be expensed against future earnings:

- The €242k six-month amortisation reflects the 15-year useful life of the Greenhammer system (point 13).

- 15 years is a long time to amortise past development expenditure, and implies MCON expects to receive income from Greenhammer systems until 2037.

Subsea micropiling and large-diameter hammer systems

- Delays have also beset MCON’s subsea drilling project. This H1 said:

“We have experienced delays in delivery of externally sourced systems [such as] the rig subsea hydraulics and control system. This delay could have a knock-on to our offshore testing schedule, and we are working hard to mitigate this.“

- At least MCON also said testing might start within six months (i.e. by February 2024), and claimed subsea micropiling could present an “enormous opportunity“:

“We are working hard to have the subsea testing underway within the next six months. There remains an enormous opportunity for Mincon with this exciting project on the successful completion of our collaboration with Subsea Micropiles and our University partners.“

- Subsea partner Subsea Micropiles reckons its market opportunity could be $5b.

- This H1 said an AGM demonstration was well received:

“Our Subsea project has been gathering momentum and at our recent AGM we made a presentation to assembled shareholders and guests in conjunction with our collaboration partners, Subsea Micropiles. We had very positive feedback from this event, and we have commenced the assembly of the subsea rig at our facility in Shannon”

- This 1m50s video explains the subsea project for shareholders that did not attend the AGM:

- MCON’s robotic drill aims to overcome the disadvantages of current subsea drilling, which are: slow installations, complex hammers, dependence on large support vessels and limitations with certain seabed geologies.

- This H1 revealed “excellent performance figures” have emerged from MCON’s large-diameter hammer prototype:

“Another project which can deliver positive efficiency gains is our large hammer and bit project that we have been testing in Malaysia. We have had excellent performance figures when it has been run and we have been onsite a number of times to see the system in action. We see a great opportunity to push this out to the large diameter drilling market to replace incumbent systems that have much lower productivity with resulting higher emissions.

- The “great opportunity” for this system is hopefully underpinned by the “commercial enquiries” now appearing:

“We have started to get commercial enquiries for the system from the large-diameter piling industry.

- I wonder if large-diameter hammer systems could even pip Greenhammer to become first to establish notable commercial success.

- Mind you, Greenhammer’s history emphasises some time can elapse between commercial enquiries and commercial success.

Financials: margin

- The lowly 9.7% operating margin for this H1 triggered cost cuts for H2:

“In the short term we expect to deliver revenue growth in H2, while also realising the benefits of our cost reduction program to deliver a much improved margin in H2 2023 over H1 2023.“

- October’s Q3 update sadly implied the “much improved margin in H2 2023” did not occur (see Q3 trading update).

- I have bemoaned MCON’s margin performance for some time.

- I bought MCON shares during 2015 partly because of the group’s then attractive 19% operating margin. I wrote at the time:

“[H]igh margins underpin the notion that MCON has a respectable competitive advantage. The group converted 19% of revenues into profit during 2014 and above 20% during 2011, 2012 and 2013.”

- But the margin subsequently bobbed between 10% and 15%, and has now dipped below 10%:

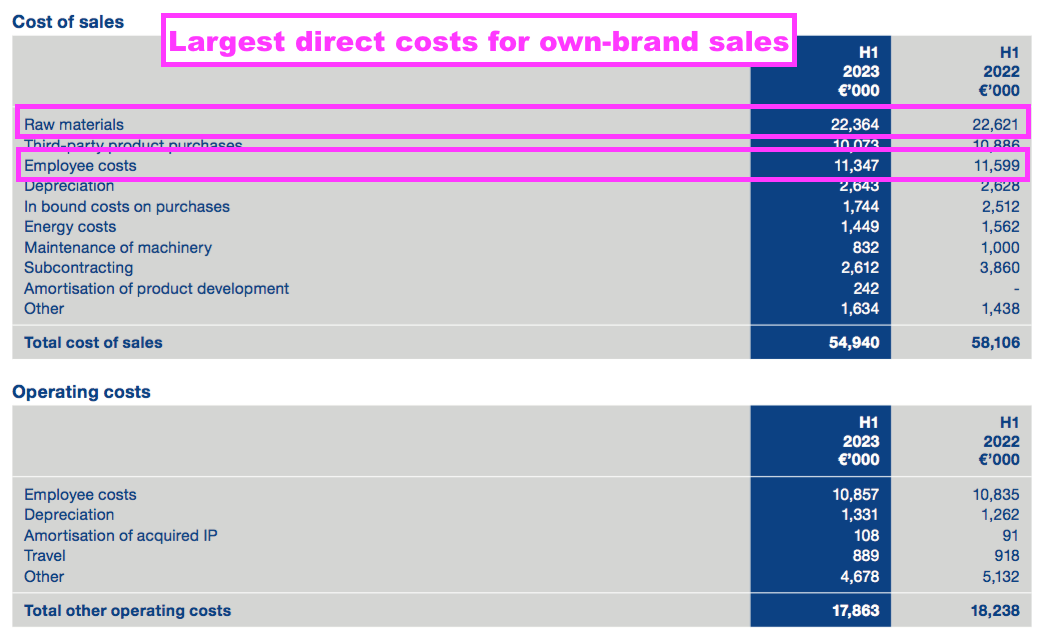

- MCON commendably lists its major operating costs:

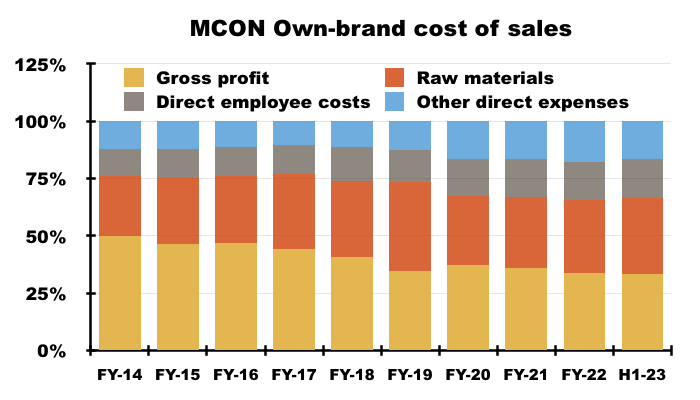

- I reckon the long-term margin decline has been caused by the group’s own-brand equipment incurring greater costs:

- Since FY 2014, the gross margin on own-brand equipment has dropped from 50% to 33% due to:

- Raw materials increasing from 26% to 33%;

- Direct employee costs increasing from 12% to 17%, and;

- Other direct expenses increasing from 12% to 17%…

- …of own-brand revenue.

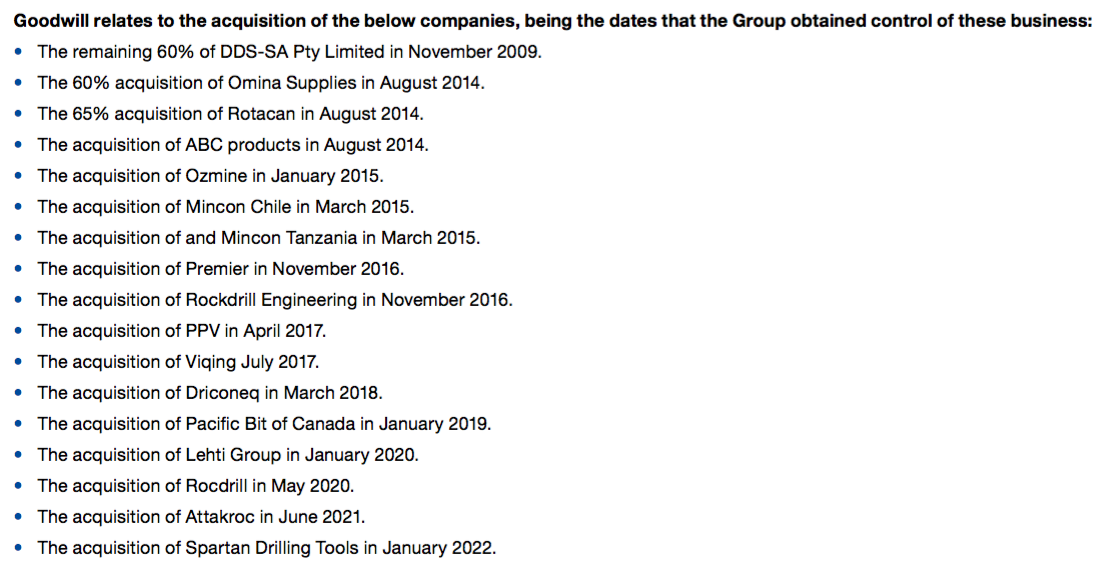

- Following the 2013 flotation, MCON has acquired at least 16 businesses to broaden its product range in order to become an industry “one-stop-shop“…

- …and in doing so has evolved from operating as a very niche, high-margin drill manufacturer with perhaps modest growth prospects into a wider, middle-margin drill supplier with possibly larger growth prospects.

- The more diverse product range alongside entry into the construction industry has certainly brought growth — revenue has a more than tripled since the flotation — but has it brought growth into lower-quality lines of business?

- The decade-long margin decline indicates MCON has been unable to pass on the higher cost of raw materials (and other expenses), which suggests an increasing lack of pricing power and a diminishing competitive position.

- An alternative assumption could be MCON has simply become too large and/or complex for the present management, and is now saddled with excess costs and inefficiency (see Boardroom and strategy).

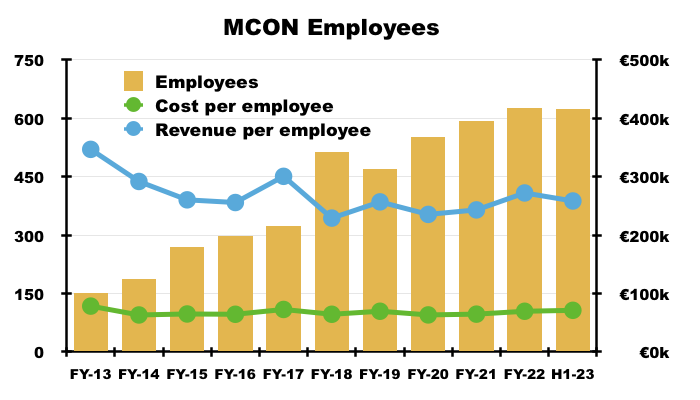

- Potentially supporting the case for greater inefficiency, employee productivity has not improved during recent years.

- Revenue per head has bobbed around €250k since FY 2018 (point 15):

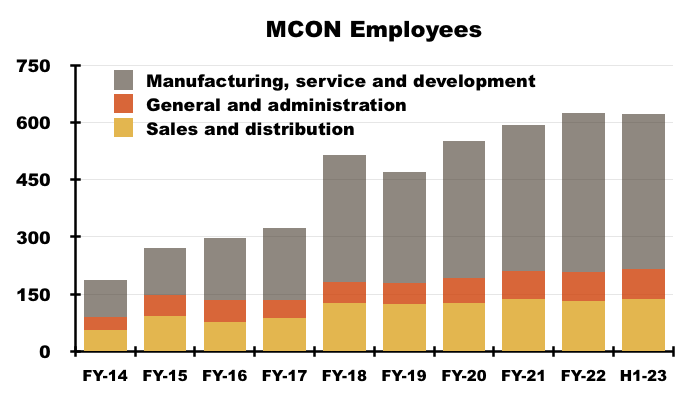

- Maybe not enough people are employed in a sales function to boost revenue. The proportion of employees deemed to work in ‘sales and distribution’ has reduced from 30% to 22% since FY 2014:

- Efforts to generate more revenue from the workforce may include this H1’s reference to “robotic machining cells“:

“This will be followed up with the commissioning of a new manufacturing building at our Shannon site and installing purpose-built robotic machining cells in the extension to cater for the growth opportunities we see.”

- This H1 also referred to a “reduced… headcount in administration and sales” and a “considerable saving in employee costs in H2 2023“.

Financials: stock

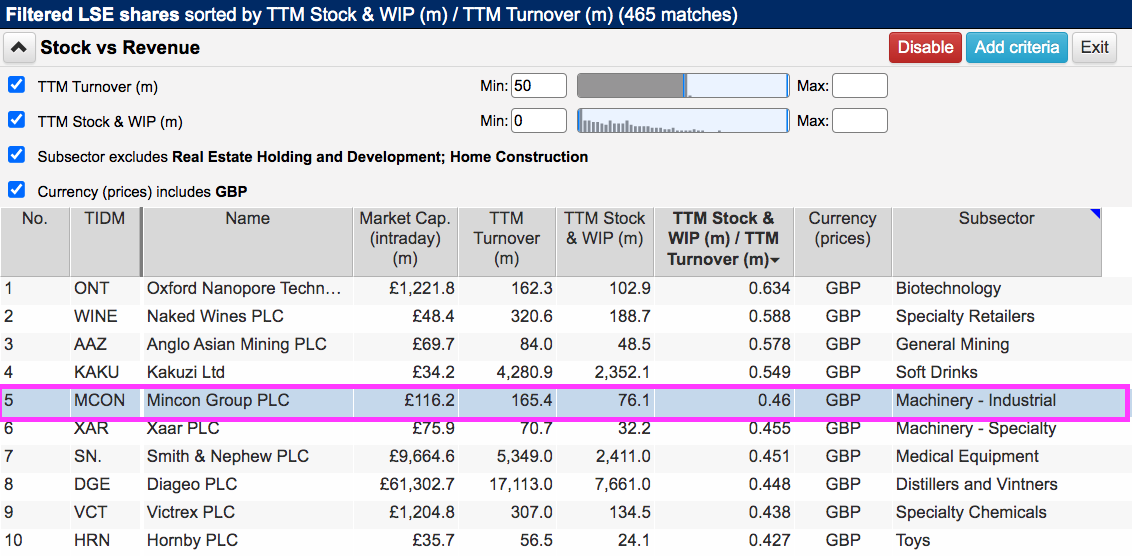

- MCON’s stock levels remain excessive. This H1 ended with stock at €76m, equivalent to a huge 46% of trailing twelve-month revenue of €165m.

- MCON is ranked 5th out of 465 companies (excluding house builders and property developers) with revenue of £50m or more on a stock-to-revenue basis:

- MCON used this H1 to announce plans to reduce stock levels:

“We have implemented a Group-wide inventory reduction program, with the goal of reducing our overall inventory levels in terms of months. Targets have been set for each subsidiary in the Group with timelines attached. We expect to make inroads in our goals on this important project for the Group by the end of this year.“

- Management bonuses are partially dependent on stock levels (point 9)…

“• The achievement of budgeted profit after tax for the year (up to 40% of salary)

• The delivery of targeted number of weeks’ inventory being carried at the end of the year (up to 7.5% of salary)

• The delivery of a targeted number of debtors days (up to 2.5% of salary)”

- …although the value of stock carried does make me wonder if the bonus pays out when stock levels increase!

- Companies carrying large amounts of stock can generate higher incidences of shareholder problems because they:

- Manufacture slow-moving items that carry a greater risk of obsolescence;

- Employ inefficient working practices, and/or;

- Require greater cash investment into extra stock to support future growth.

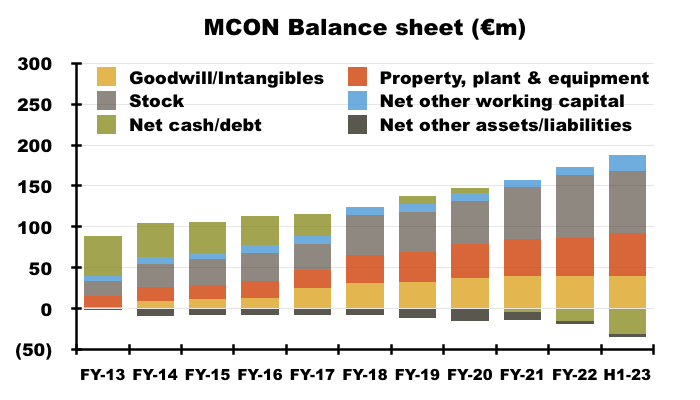

- Significant levels of stock have long been an unfortunate drawback of MCON’s balance sheet.

- Stock has grown from 21% (€18m) to represent 49% (€76m) of the group’s net asset value between FY 2013 and this H1:

- Elevated stock levels do appear fundamental to MCON’s business.

- MCON’s customers are located throughout the world (often in remote mining locations) and require a “timely supply” of drilling equipment:

“The Group manufactures and sells rock drilling consumable products, and the timely supply and service of these products is paramount to our business model. Since the markets that we serve across the world are geographically dispersed, and the lead times for delivery are set by customer requirements and competition to a large degree, we have built a wide network of customer service centres backed by manufacturing plants in key markets.“

- At least MCON’s stock is not perishable and write-downs during this H1 were not material at €58k.

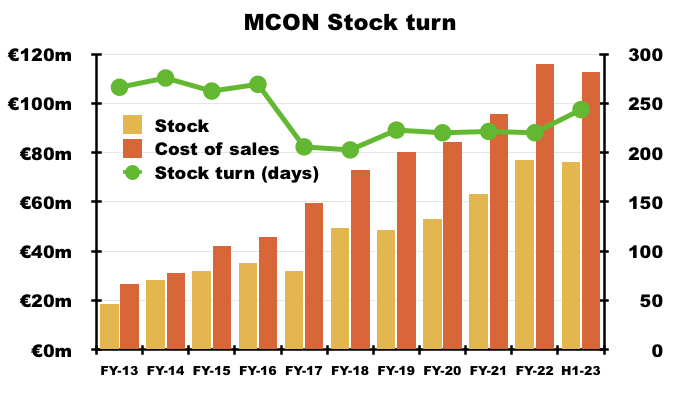

- Stock turn has remained consistent during recent years but is still lengthy. Average inventory employed during the preceding H2 and this H1 (€75m) divided by trailing twelve-month cost of sales (€113m) gives 244 days (c8 months):

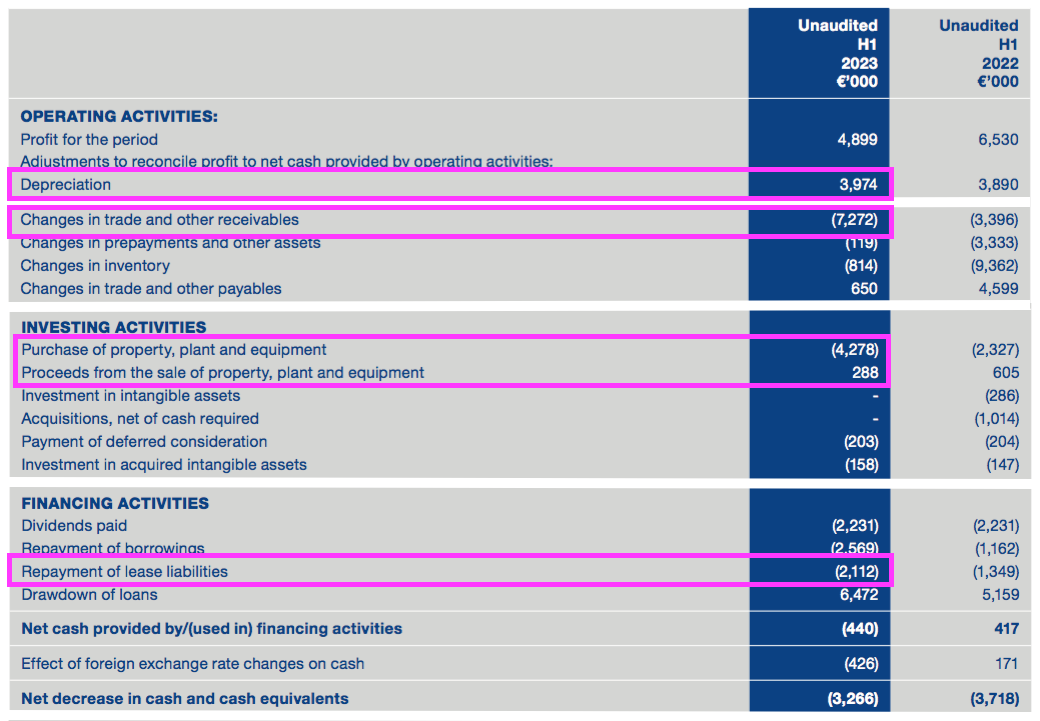

Financials: cash flow and net debt

- Cash conversion during this H1 was poor.

- Reported H1 earnings of €4.9m translated into an H1 free cash outflow of €4.2m.

- Impacting the H1 cash conversion were:

- Trade and other receivables absorbing cash of €7.3m, and;

- Capital expenditure of €4.3m plus lease costs of €2.1m exceeding the deprecation of €4.0m charged against earnings.

- MCONs cash flow has regularly emphasised the group’s capital-intensive nature.

- During the five years to FY 2022 for example, cash absorbed into working capital (including equipment prepayments) totalled a substantial €40m — equivalent to almost half of the €84m aggregate operating profit reported during the same time:

| Year to 31 December | 2018 | 2019 | 2020 | 2021 | 2022 |

| Operating profit (€k) | 16,352 | 11,810 | 18,249 | 18,107 | 19,749 |

| Depreciation* (€k) | 3,896 | 3,898 | 4,666 | 5,209 | 5,623 |

| Net capital expenditure** (€k) | (12,552) | (7,930) | (6,981) | (7,024) | (6,313) |

| Working-capital movements (€k) | (14,870) | 2,095 | (2,912) | (9,425) | (14,325) |

| Free cash flow (€k) | (11,118) | 3,175 | 7,938 | (575) | (2,527) |

| Net cash (€k) | 846 | 5,586 | 461 | (4,342) | (14,909) |

(*excludes IFRS 16 depreciation **excludes Greenhammer expenditure)

- Five-year expenditure on tangible assets (€41m) beyond the depreciation charged against earnings (€23m) meanwhile stands at €17m.

- Factor in €6m spent on Greenhammer, a net €20m spent on acquisitions, €11m spent on IFRS 16 lease costs and €22m spent on dividends, and no wonder net cash reduced from €26m to net bank borrowings of €15m during those five years.

- The adverse cash movements during this H1 left cash at €13m, debt at €35m and net debt therefore at €22m.

- MCON irritatingly does not differentiate between loan-interest costs and IFRS 16 lease-interest costs within its H1 statements.

- Total H1 finance costs were €1.2m, and up significantly versus €0.6m from the comparable H1 and €0.9m from the preceding H2.

- The 2022 annual report stated “interest rates on current borrowings are at an average rate of 4.89%“, which suggests MCON may have paid loan-debt interest of approximately €800k during this H1 on average H1 debt of nearly €33m.

- October’s Q3 update indicated a lower-than-expected profit that now places the group’s debt under greater scrutiny (see Q3 trading update).

- The 2022 annual report disclosed the following debt covenants (point 24):

“The Group has been in compliance with all debt agreements during the periods presented. The loan agreements in Ireland of €13.5 million (2020: €10.5 million) carry restrictive financial covenants including, EBITA to be no less than €18 million at end of each reporting period, interest cover to be 3:1 and to maintain a minimum cash balance of €5 million.”

- October’s Q3 update predicted Ebitda of €20m for FY 2023, which I estimate means Ebita could be €12m if the depreciation of €4m for this H1 is repeated for H2.

- Ebita of €12m is below the €18m covenant cited in the 2022 annual report and suggests MCON might now be in trouble with its lenders. I therefore contacted MCON to clarify the covenant situation. MCON replied:

“The letter “D” is missing from EBITDA on note 18 in the report, that is an error in the typing.

We’ll update that note in the 2022 annual report and upload to our website once done”

- A typo within the covenant small-print is not ideal. And the typo does not mean MCON is completely free of possible debt trouble.

- You see, the anticipated Ebitda of €20m for FY 2023 is only €2m above the €18m Ebit(d)a covenant… and a tough FY 2024 might well see that covenant tested.

- Note that the €18m Ebit(d)a covenant relates to loans of €13.5m out of more than €30m. The covenants for the other loans are irritatingly not disclosed.

- Shareholders are also left to guess:

- The split between fixed-rate and variable-rate debt, and;

- Whether the aforementioned 4.89% average rate is linked to any particular interbank benchmark.

- Whether MCON should be declaring dividends given its debt position is very debatable.

- On a five-year view, a total free cash outflow of €3.1m has clearly not covered the €22m used to pay dividends (let alone acquisition spend of €20m) during the same time:

| Year to 31 December | 2018 | 2019 | 2020 | 2021 | 2022 |

| Free cash flow (€k) | (11,118) | 3,175 | 7,938 | (575) | (2,527) |

| Dividends paid (€k) | (4,421) | (4,426) | (2,222) | (6,693) | (4,462) |

| Net acquisitions (€k) | (9,264) | 6,147 | (9,910) | (2,927) | (3,789) |

- MCON’s dividends ought really to be funded by surplus-to-requirements cash flow and not by extra borrowings.

- MCON must consider whether its €4.5m annual dividend remains appropriate given the:

- Absence of free cash generation during the past five years;

- Immediate prospect of lower profit, and;

- Proximity to a debt-covenant breach.

- I would venture the dividend should be suspended to shore up the cash position.

- But whether the 56% family shareholders wish to forego their €2.5m dividend income remains to be seen (see Boardroom and strategy).

Q3 trading update

- October’s Q3 update admitted revenue during the first nine months of 2023 had declined 7%:

“Further to the most recent commentary provided about the challenging market conditions in which the Company is currently operating, Group revenues contracted further during Q3 2023 and, for the first nine months of 2023, are currently 7% below revenues in the same period in 2022. The revenue decrease in Q3 is attributable to contraction of our sales into the mining industry in some regions with a particular weakness in Africa in recent months.”

- Given H1 revenue fell 5%, Q3 revenue may have dropped by approximately 11% to arrive at a nine-month decline of 7%.

- Talk of postponed contracts implied Q4 revenue has also disappointed:

“In addition, we had anticipated commencing two large scale construction projects in North America early in Q4 which will no longer take place as planned, albeit the larger of the two will now commence in 2024. Elsewhere, we have seen single digit growth in the waterwell / geothermal industry.”

- Improved cash conversion has been reinvested into product development rather than debt reduction:

“Our overall working capital position has improved during the period through our previously announced inventory reduction programme. Our debtor position has also improved since H1 2023, resulting in decreased payables and an improved cash position, which has facilitated continued investment into our new product development projects and positioning the Group for future growth.”

- The gross margin for the first nine months of 2023 was 30.4%:

“The progress made on our inventory reduction programme, along with reduced revenue in the mining industry, has resulted in lower output from our factories. This, together with a more competitive mining market, has resulted in a reduced gross margin for the year to Q3 2023 (c. 30.4% vs 32.0% in Q3 2022).”

- The H1 gross margin was 31.8%, which suggests the Q3 gross margin may have been less than 28% to arrive at a nine-month average of 30.4%.

- ‘Exceptional’ costs have emerged during H2:

“As previously guided within our half year results, to progress the competitiveness of the business into the future, we have continued to implement our cost reduction programme in the period. The exceptional cost associated with this (€0.8m year to date) has impacted on our 2023 results but should yield benefits in 2024 and beyond.”

- I speculate the €0.8m ‘exceptional’ cost is for Q3 only, and Q4 will incur a further ‘exceptional’ charge.

- Ebitda for FY 2023 is set to be €20m:

“In light of the above, looking ahead to the remainder of the year we now expect to deliver full year EBITDA of approximately €20 million.”

- Ebitda during this H1 was €11.8m, which indicates €8.2m should be achieved for H2 2023.

- Ebitda during the preceding H2 2022 was €14.8m, indicating Ebitda will drop 45% (to €8.2m) during H2 2023.

- The outlook referenced the “medium term“…

“Our outlook for the medium term is positive, we will continue to invest, to improve our competitiveness within our current industries, and focus on delivering new opportunities in current and new industries to deliver better returns for the Group.”

- …which typically means the short term may not be so favourable.

Boardroom and strategy

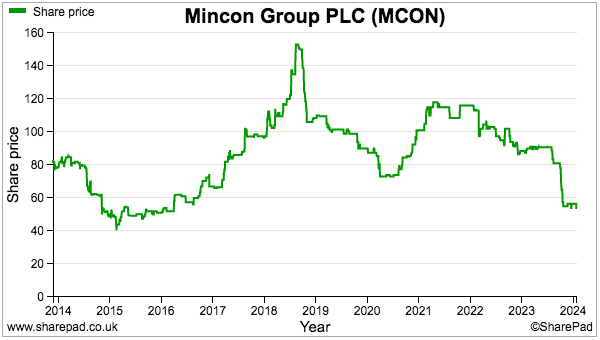

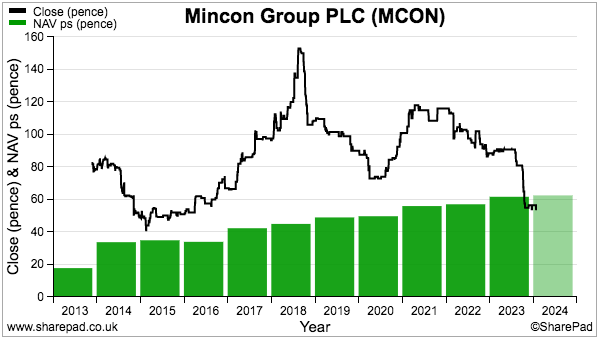

- MCON floated during 2013 at 73p and the price chart tells a frustrating story with the mid-price recently at 54p:

- The original strategic goals cited within the flotation document included:

- “Double the size of the business by the end of 2015″, and;

- “Complete and integrate 2 to 3 acquisitions in the rock drilling consumables space thereby substantially utilising the net proceeds from the Placing”.

- The over-riding plan was to become a “one-stop-shop” for customers that would “maximise” the group’s margin:

“The aim is to increase the Mincon share of this market through organic growth and through acquisitions with the objective of becoming a ‘‘one-stop-shop’’ for rock drilling consumables. Controlling the supply chain from manufacture to end-user, providing a high quality customer service and receiving real-time feedback from customers to inform product development is expected to enable the Group to maximise its margins.”

- The flotation document said the purchase prices for individual acquisitions was “expected to be based on enterprise value in the region of €10-30m“.

- But MCON eventually purchased numerous smaller businesses for less than €10m each, which seems very much like a Plan B.

- The plan to “maximise” the group’s margin has not worked either (see Financials: margin), which may well reflect that Plan B.

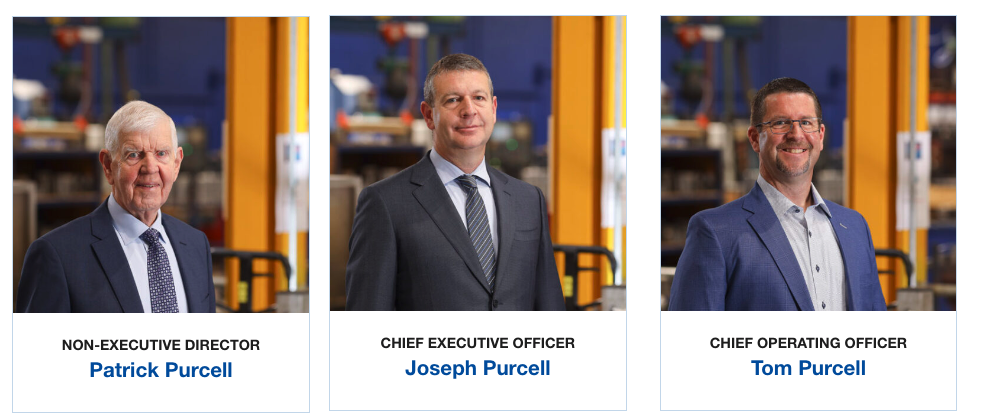

- MCON was established during 1977 by Patrick Purcell, who ran the business until 2012 and still works in his 80s as a group non-exec.

- Patrick Purcell and his family control a collective 56% of MCON and did not sell a share at the flotation and have not sold a share since:

- Kevin Barry was MCON’s chief executive between 1991 and 2015, and owned 14% of MCON after the flotation. Mr Barry’s annual-report biography described his accountancy background:

“Kevin commenced his career as a trainee accountant in practice in 1973. He joined Kraus & Naimer Ireland Limited as an accountant in 1977. He qualified as a Certified Public Accountant (‘‘CPA’’) and began working with Mincon International Limited in 1984 as Financial Controller. He was appointed Chief Executive Officer of the Mincon Group of companies in 1991. Kevin has been responsible for expanding the Group’s activities since becoming Chief Executive Officer by extending the Mincon product range through organic growth and by setting up the various overseas subsidiaries.”

- Joseph Purcell succeeded Mr Barry as chief executive. Joseph Purcell is the son of founder Patrick Purcell and joined MCON during 1988. He became chief technical officer during 1998 before becoming chief executive during 2015.

- MCON’s other board executive is Thomas Purcell, who is also the son of founder Patrick Purcell. Thomas Purcell rejoined MCON during 1999 and, among other roles, has served as the group’s sales director. He was appointed chief operating officer during 2023.

- Both Joseph and Thomas Purcell are the common executive dominators during MCON’s ten-year quoted history. I believe they have to take responsibility for deploying the group’s “one-stop-shop” strategy and the subsequent disappointing financial performance.

- Joseph Purcell has an engineering background while Thomas Purcell has a sales background. I speculate both Purcell executives may be more suited to their particular specialities rather than broader management roles.

- Perhaps a Kevin Barry-type chief executive is now required to ensure the “one-stop-shop” strategy generates the returns outside shareholders have long expected from MCON’s “innovative engineering and industry-leading quality“.

- Mind you, Kevin Barry was a 14% shareholder and perhaps more likely to question the actions of the Purcell executives despite their 56% family control. A standard chief executive may be less likely to quibble with the majority owners.

- MCON’s four non-Purcell non-execs seem unlikely to interfere with proceedings, given their collective shareholding is worth €44k at 54p.

- I am hopeful last year’s appointment of Thomas Purcell as chief operating officer can lead to greater efficiencies and improved financials. He will oversee “the daily operations of the company with a focus on our global business of manufacturing, sales, marketing and service”.

- For now though, the past strategic decisions of the Purcells remain up for debate.

- Enormous sums have been spent on acquisitions (€20m), capex (€41m) and extra stock (€38m) during the last five FYs, but the additional returns from such expenditure is not clear.

- Indeed, the €20m Ebitda expected for FY 2023 equals that reported for FY 2018. The dividend has not changed since FY 2018.

- I trust MCON’s board will soon take a pragmatic view of the group’s strategy, and consider whether the past expansion has really delivered superior returns to outside shareholders.

- I recognise MCON’s family executives are genuine long-haul managers and the Q3 update may be seen as a blip in years to come.

- But I worry borrowings may become very uncomfortable should MCON’s mining customers continue to curtail spending and FY 2024 profit suffers badly.

- I also worry the 56% majority shareholders may not embrace non-family board executives who might be able to improve the group’s financial decision making.

- I do wonder if decisive action will only be taken when MCON’s lenders start questioning the viability of the dividend and tell the Purcell family its annual €2.5m income is unsustainable.

Valuation

- The anticipated Ebitda of €20m for FY 2023 may translate into an operating profit of €12m after deprecation and amortisation of approximately €8m.

- Operating profit of €12m is close to £7m at GBP:EUR 1.17.

- The market cap of £115m at 16x that near-£7m operating profit implies the 54p mid-price is far from bargain levels, especially as:

- Reported profit converts poorly into cash, and

- Borrowings, lease expenses and tax have not been considered.

- MCON’s ongoing capex and stock investment probably makes the balance sheet a better valuation yardstick.

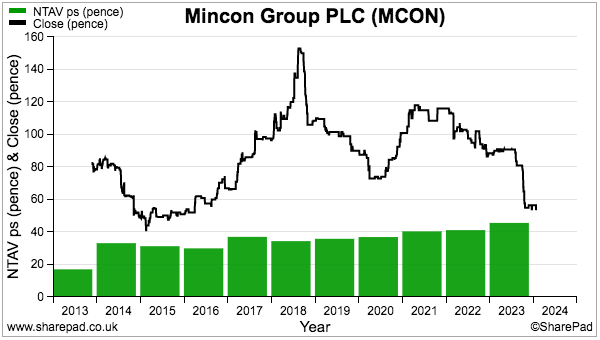

- This H1 showed net tangible assets at €114m or 46p per share, which support 85% of the 54p mid-price:

- Including intangibles of €40m, net assets are €154m or 62p per share, which exceeds the 54p mid-price and implies the market may not believe the €40m of acquired goodwill and Greenhammer expenditure is really worth €40m:

- I invested at 45p during early 2015 when the shares traded close to net book value.

- But back then, margins were high, the balance sheet sported net cash and the financials generally seemed to offer limited downside.

- Almost nine years later, and MCON’s significant expansion has obscured any evidence of a competitive ‘moat’ and has now even brought the group’s borrowings into the spotlight.

- I have asked MCON to comment upon the debt and covenant situation within its forthcoming FY 2023 results. I trust the board will confirm to shareholders whether (or not) the borrowings remain appropriate.

- The FY 2023 results may even consider whether (or not) the “one-stop-shop” strategy, boardroom personnel and/or dividend remain appropriate.

- MCON represents less than 2% of my portfolio and, for now at least, the case for keeping the shares includes:

- The market cap at close to net tangible asset value already anticipates further bad news;

- The weak Q3 update mostly reflects a cyclical mining downturn and a natural upturn will one day arrive;

- The 56% family managers are true owner-operators and will take the necessary action to ensure their £64m shareholding is not destroyed, and;

- Innovations such as Greenhammer, subsea micropiling and large-diameter hammer systems will eventually revitalise the group’s financials.

- The most likely bear outcome is (continuing) to be stuck in an illiquid ‘fiefdom value trap’, with the board soldiering on building a capital-intensive business with lower margins funded by growing debt.

- A more fundamental risk is the lack of any superior alternatives to the board’s present strategy and personnel. The general economics of industrial-drill manufacturing could in fact be inherently poor and, despite lots of skilled employees and creative R&D, may never improve.

- If management retains the yearly 2.1 eurocents (c1.8p) per share dividend, shareholders holding out for a recovery would collect a 3.3% income at a 54p mid-price (before Irish withholding taxes for UK-resident investors).

Maynard Paton

Mincon (MCON)

Trading Update published 06 February 2024

I am pleased this update did not unveil a further weakening of activity following October’s Q3 update (see blog post above). Here is the full text:

——————————————————————————————————————

“Mincon Group plc (Euronext:MIO; AIM:MCON), the Irish engineering group specialising in the design, manufacture, sale and servicing of rock drilling tools and associated consumable products, today provides the following trading update ahead of the publication of the Group’s results for the financial year ended 31 December 2023.

Whilst market conditions continue to be challenging, as the mining and construction markets experience weaker demand, the Group’s performance in Q4 was in line with expectations and we expect to achieve full-year EBITDA slightly ahead of the prior guidance of €20 million.

We made successful inroads in reducing our working capital position during 2023, particularly through our inventory reduction programme, and we expect to see continued improvement in this initiative into 2024. This, together with a reduced requirement for new capital equipment in our factories following the significant investments made by the Group in recent years, is expected to have a continued positive knock-on effect on our net debt position during 2024.

As a result of the proactive steps taken during 2023 to improve the Group’s competitive position, including the ongoing investment in our product development initiatives and the actions taken on costs and inventory management, we believe Mincon is well positioned for growth over the medium-term.

The Group expects to publish its final results for the year ended 31 December 2023 on Monday, 11 March 2024.”

——————————————————————————————————————

FY Ebitda coming in “slightly ahead” of the €20m mentioned in October is somewhat of a relief. I am also encouraged by the “successful inroads in reducing our working capital position“, which this update implies will reduce net debt during FY 2024.

Perhaps unfairly, but I am interpreting “proactive steps taken during 2023 to improve the Group’s competitive position” to mean MCON is trying to catch up with the competition.

Mentioning “over the medium-term” again suggests results during the short term will not be spectacular.

I am hopeful management will use the forthcoming FY 2023 results to comment upon the suitability of the group’s strategy and acknowledge that change is required to improve margins and reduce capital intensity.

Maynard