31 March 2024

By Maynard Paton

H1 2023 results summary for M Winkworth (WINK):

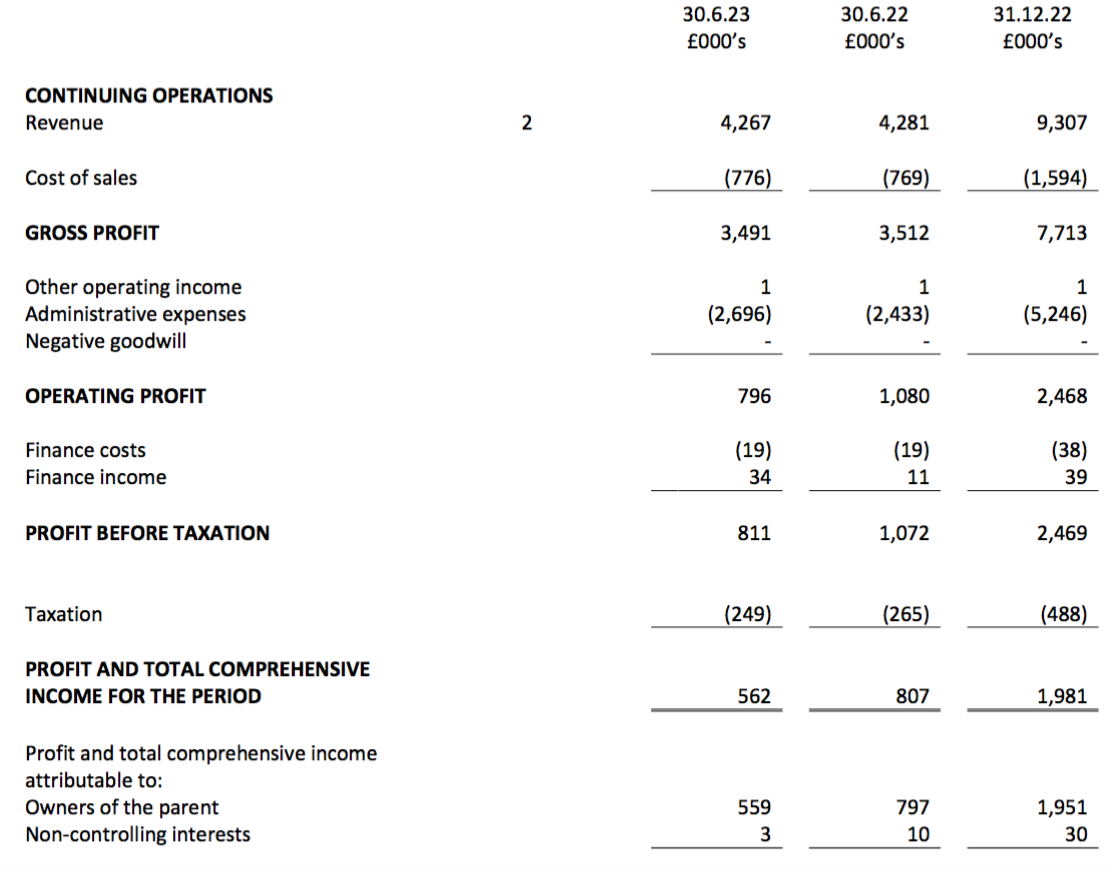

- Only the dividend advanced higher (+7%) after a “more challenging” property market alongside greater costs caused franchisee network income to decline 5%, revenue to remain flat and profit to drop 26%.

- WINK’s franchisees continue to report greater SSTCs and exchanges versus other agents, with sales commissions improving to an estimated £5.4k per transaction and “new blood” being sought to 3-4x franchise revenue at certain London branches.

- A third company-owned office seems on the horizon, although the departure of WINK’s successful Tooting manager plus unclear financial progress at Crystal Palace do raise questions about the in-house approach.

- A lower margin and adverse cash generation reflected this H1’s reduced sales activity, but a post-H1 update indicated a stronger H2 2023 that ought to include greater returns from franchisee loans.

- Projected earnings of c12p per share may limit increases to the 11.7p per share dividend, although net cash of £4m alongside owner-directors committed to a “progressive” payout should sustain the 6.9% yield. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own WINK

- Results summary

- Revenue, profit and dividend

- Franchisees: network branches and competitive position

- Franchisees: sales and lettings income

- Winkworth versus Foxtons

- Company-owned offices

- Financials

- Valuation

News links, share data and disclosure

- Interim results, presentation and webinar for the six months to 30 June 2023 published/hosted 06-07 September 2023;

- Q3 dividend declaration published 11 October 2023;

- Trading update and Q4 dividend declaration published 10 January 2024, and;

- Board change published 13 February 2024.

- Share price: 162.5p

- Share count: 12,908,792

- Market capitalisation: £21.0m

- Disclosure: Maynard owns shares in M Winkworth. This blog post contains SharePad affiliate links.

Why I own WINK

- Operates a London estate-agency franchising business, with progress buoyed by motivated franchisee owners developing their own local agencies and capturing greater market share.

- Franchisor set-up leads to high margins, low capital requirements and a cash-rich balance sheet able to fund attractive franchisee investments.

- Seasoned family management boasts a 47%/£10m shareholding and rewards investors through durable quarterly dividends and occasional special payouts.

Further reading: My WINK Buy report | All my WINK posts | WINK website

Results summary

Revenue, profit and dividend

- July’s Q2 update confessing to a “more challenging” property market due to higher interest rates….

“After a first quarter that was in line with management expectations, the sales market proved to be more challenging in the second quarter of 2023 as interest rates rose higher and faster than anticipated.“

“Mortgage approvals, which in Q1 recovered from the low levels seen in Q4 2022, were reported below the levels seen in the first half of last year… Property prices have held up reasonably well but transactions have slowed, leading to a high number of agreed sales being delayed to the second half of the year.“

…

“Preliminary gross network income figures for H1 2023 indicate an overall fall of 6%, with lettings revenue approximately 11% higher and sales revenues down by 20% compared with H1 2022.“

- …had already admitted this H1 would see a lower profit as well as warn on FY 2023 profit:

“As a result, the Directors expect H1 2023 pre-tax profits to be below last year’s level. While the Directors believe that confidence will return once buyers can access a broader choice of mortgage finance, the outlook for sales in the second half of the year remains uncertain and the shortfall in H1 2023 means that full year pre-tax profits are likely to fall below market expectations.”

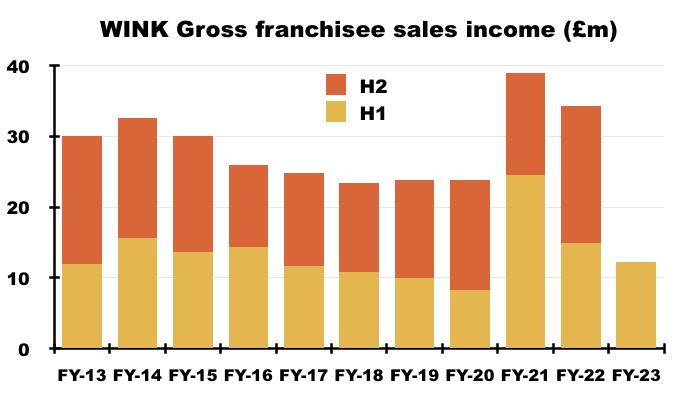

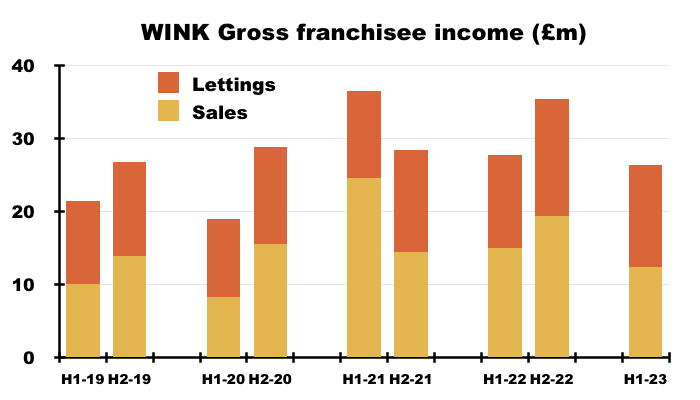

- Gross franchisee network income was slightly better than July’s Q2 update had indicated, declining 5% (not 6%) to £26.3m. Gross franchisee sales income dropped 18% (not 20%) to £12.3m while gross franchisee lettings income climbed 10% (not 11%) to £14.0m:

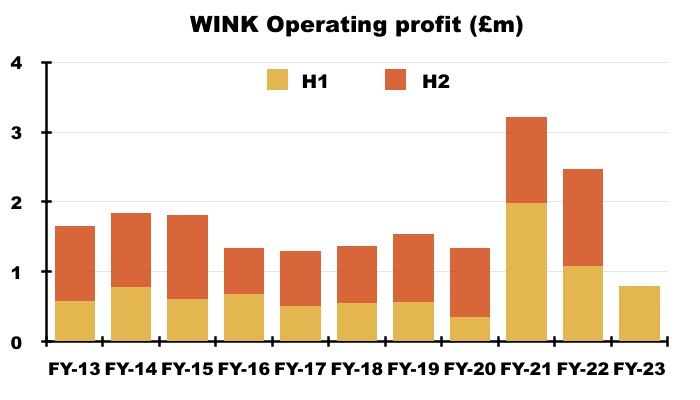

- Operating profit for this H1 fell 26% to £796k, but was still 42% higher than the £562k recorded for pre-pandemic H1 2019:

- The pandemic significantly influenced WINK’s progress, with FY 2020 hampered by Covid lockdowns and FYs 2021 and 2022 enjoying boosts from stamp-duty holidays and “pandemic-induced buyers”.

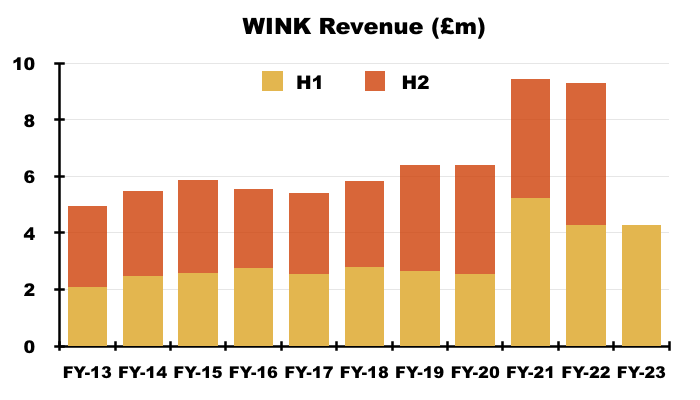

- Gross franchisee network income declining 5% translated into H1 revenue staying flat at £4.3m:

- Revenue remaining flat despite gross franchisee network income declining 5% reflected a greater conversion of franchisee income into WINK’s management service fees (see Franchisees: sales and letting income).

- Profit down 26% despite revenue remaining flat reflected greater costs associated with a new-homes venture and, according to management’s H1 webinar, wage inflation at the company-owned offices (see Company-owned offices).

- Progress was not complicated by adjustments, with non-trading charges limited to only a £7k investment write-down.

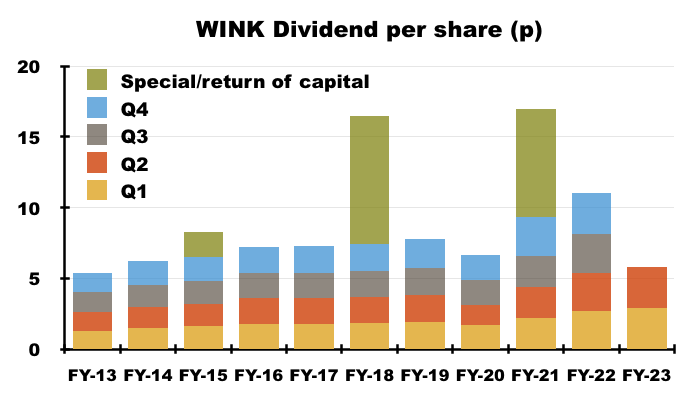

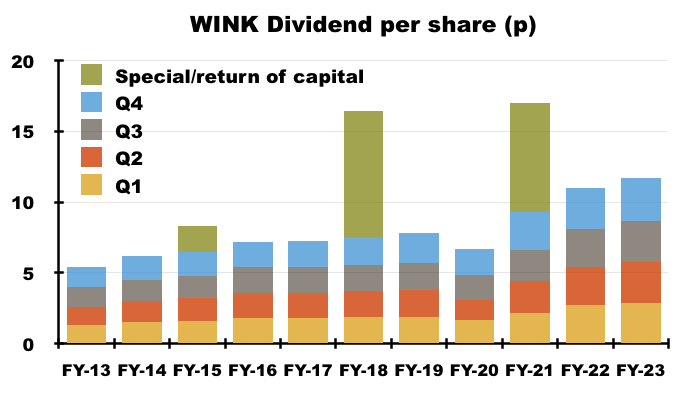

- April’s Q1 update and July’s Q2 update had already revealed quarterly payouts of 2.9p per share to give a total 5.8p per share payout for this H1:

- Following this H1, announcements during October and January declared Q3 2.9p and Q4 3p per share dividends respectively, taking the prospective total FY 2023 payout to 11.7p per share (see Valuation).

- The 5.8p per share paid for this H1 was 7% up on the 5.4p paid for the comparable H1, while the 11.7p per share prospective total for FY 2023 is 6% greater than the 11p per share declared for FY 2022.

Franchisees: network branches and competitive position

- WINK’s franchisee network consists of 101 estate-agency branches located throughout London and affluent areas of southern England.

- Franchisees pay WINK a straight 8% of all of their sales and letting income, plus variable sums towards IT, training, marketing, landlord/tenant referrals and other services (point 7a).

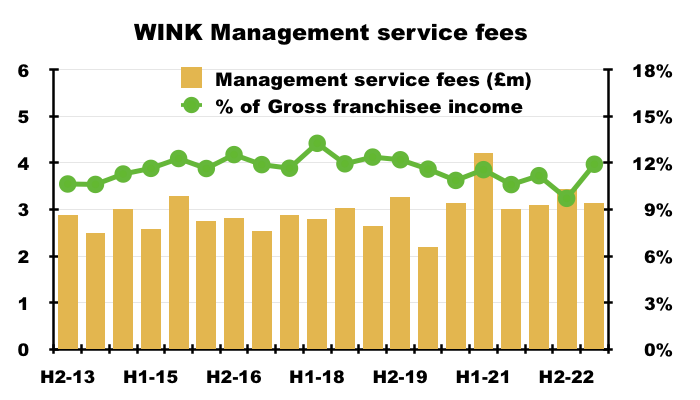

- During this H1, £3.1m, or 11.9%, of the £26.3m earned by the franchisees was taken by WINK as management services fees:

- The 11.9% proportion was the highest since H2 2019 (12.2%) and was a welcome improvement on the preceding H2 2022 proportion of 9.7%.

- I presume the franchisees are back to requesting a more normal level of extra services from WINK. The preceding FY 2022 had implied the 9.7% proportion was due to “the more uncertain economic outlook [having] impacted some of our ancillary services.”

- WINK’s competitive edge is based upon ensuring the franchisees provide a high-quality service (points 2b and 4d):

“In a highly competitive environment, winning and retaining customers is a key objective. Winkworth takes great store in the quality of its brand and maintains it by applying the highest standards of conduct and business practice in its everyday dealings“

“We monitor the market and our competitors’ activities closely and are constantly working to ensure that quality and value remains at the heart of our service offering.”

- As such, not everyone that applies to become a franchisee is successful (point 3d):

“Winkworth has a rigorous vetting procedure for new franchisees and only a small number of applicants are successful in joining the group. Once accepted, franchisees are closely monitored to make sure that they achieve the service levels set down for them and remain compliant with the law by providing regular training through the Winkworth Academy and internal auditing.“

- Appointing higher-quality franchisees helps ensure each branch can generate a healthy level of commissions, which can then leave room for manoeuvre during difficult times without the franchisee going under (see Franchisees: sales and lettings income).

- During this H1 and the preceding H2, total franchisee network income was £61.6m or approximately £600k per branch.

- That £600k compares to almost £200k per branch during FY 2009 and nearly £500k per branch during FY 2016.

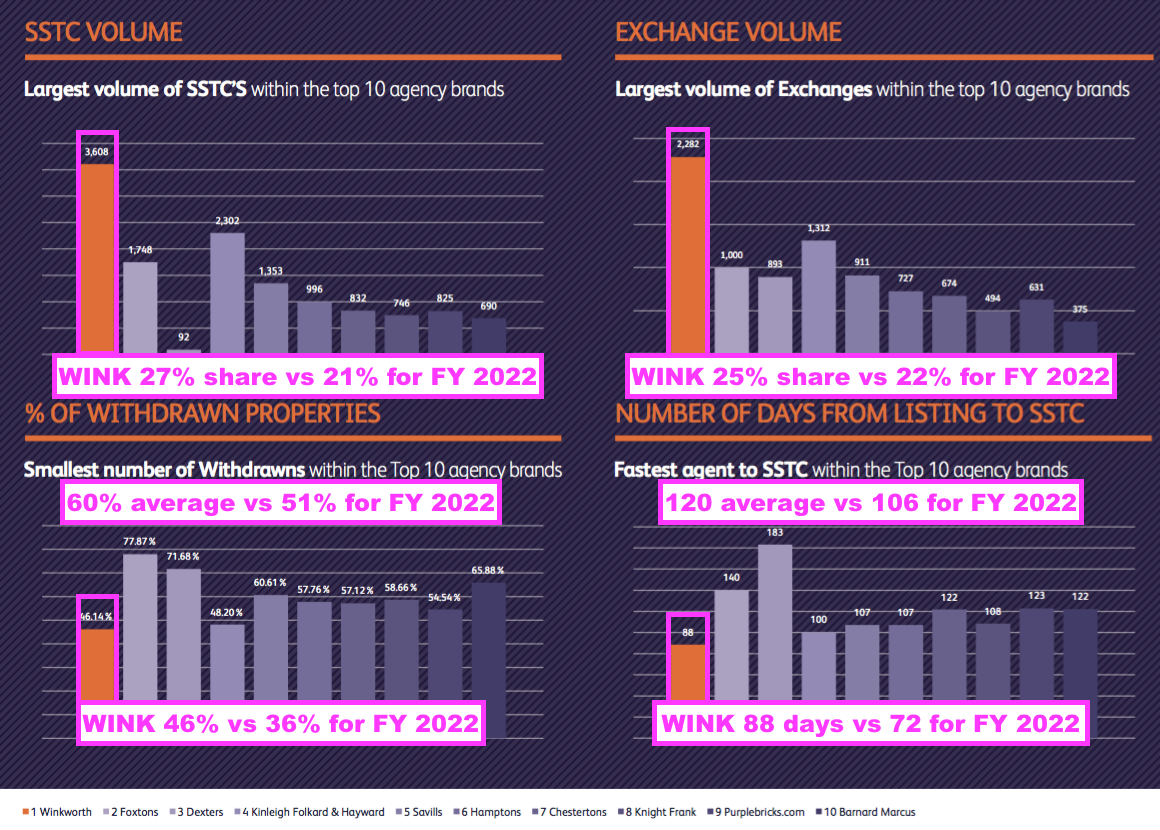

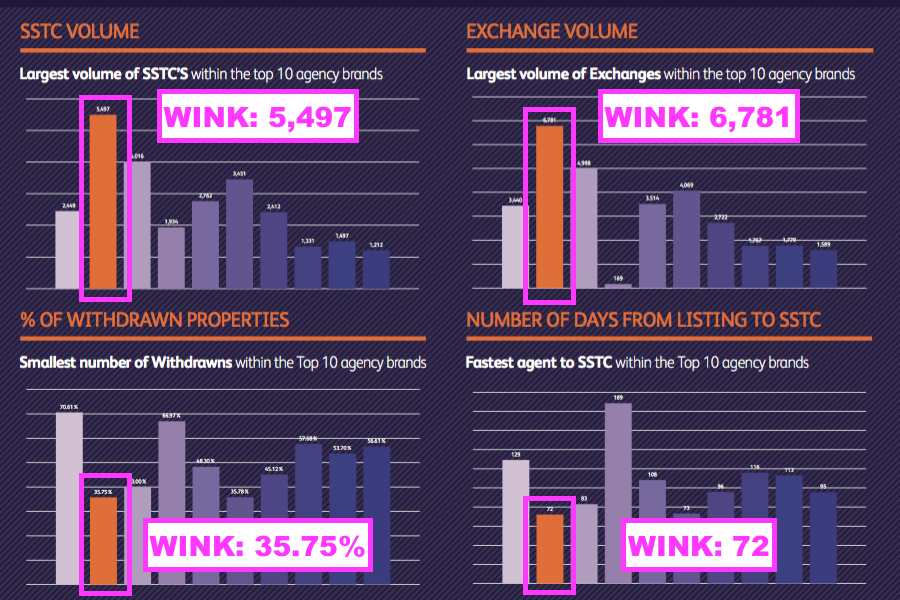

- Various statistics from this H1 underlined the greater effectiveness of the typical WINK franchisee versus nine other sizeable agents within WINK’s “addressable areas“:

- The same statistics from the preceding FY also showed WINK outperforming:

- Comparing this H1 to the preceding FY, WINK increased its share among its nine rivals for sold-subject-to-contract (SSTC) volumes (27% versus 21%) and exchange volumes (25% versus 22%).

- However, both WINK’s percentage of withdrawn properties (46%) and its days from listing to SSTC (72 days) both moved closer to the wider-market average.

- This H1 reiterated each WINK branch ought to be a “top-three contender“:

“Our focus continues to be on providing a platform that can allow an independent business to compete as a top three contender in its local marketplace and, by doing so, ensuring a franchisee can generate a healthy return under differing market conditions. Our experience shows that, in the areas in which we chose to operate, there should always be sufficient transactions for a top three operator to maintain healthy income throughout the cycle. Our strategy remains to match this positioning with best-in-class operators to continue to make the network greater than the sum of its parts.“

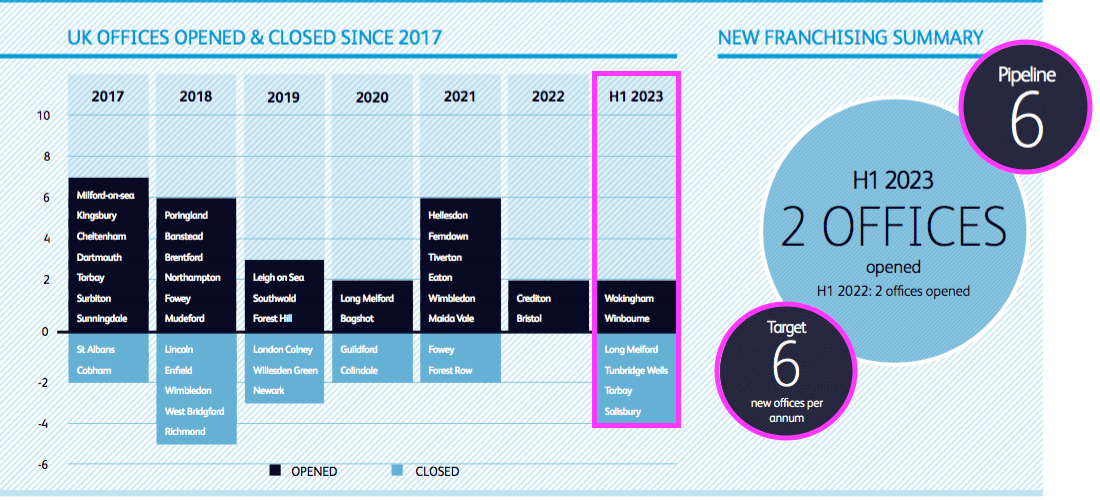

- Branches making only “marginal contributions” therefore risk closure, and four were shut during this H1:

“Four offices, which have made a marginal contribution for several years and have suffered from the fall in market volumes, were closed”

- Branches closed during this H1 were Long Melford, Tunbridge Wells, Torbay and Salisbury:

- Management’s H1 webinar said the Salisbury branch would re-open “imminently“. Long Melford was open only for three years.

- Some 30 branches have been opened and 21 have been closed since FY 2016.

- Opening a net nine new branches over 7.5 years underlines the slow expansion of the franchisee network. Indeed, the 101 franchised branches operating during this H1 compare to 86 quoted within the 2009 flotation document and 94 quoted within the 2016 annual report.

- The target number of new branches remains six per annum, which seems ambitious given WINK’s expansion history.

- Mind you, January’s Q4 update following this H1 revealed the potential for eight new branches during FY 2024:

“After opening four new offices in 2023, we are in negotiations for some eight additions in 2024, in line with our long-term target.“

- Revenue growth is not entirely correlated to opening new branches. This H1 claimed “new blood” could reinvigorate existing London branches and triple or quadruple their revenue:

“In London, we have identified further opportunities to both introduce new blood to existing businesses and to significantly improve the sales performance of offices with strong underlying lettings businesses. We believe that in certain situations we may be able to increase the available franchise revenue three or four-fold, the equivalent of opening multiple cold start offices.“

- “New blood” seems to have taken on at least three London branches of late. The question below was submitted to management’s H1 webinar:

“The loss of the franchisee who operated in Battersea, Clapham and Pimlico, will be keenly felt. Hopefully for these valuable areas, new franchisees will be quickly found. Appreciate it took a court case to resolve, but just a little surprising no formal announcement was made or investors informed.“

- Management gave the following response:

“Due to compliance-related reasons, Winkworth decided not to renew the franchisee. The franchisee contested that decision, and unusually and unfortunately, we had to take legal action around that. On 17 July [2023], the court awarded in our favour, and so the franchisee’s franchises were terminated.

We are now in a transitional period where we are completing the legal proceedings and the settlement agreement associated with that, so unfortunately we are unable to say any more at this time.“

- The “compliance-related reasons” concerned the franchisee’s failure to submit his 2020 accounts to WINK on time. This link provides a useful summary of the case, and refers to the franchisee having agreements for five franchised branches.

- WINK’s website shows the Battersea, Clapham and Pimlico (and Westminster) branches still open for business, with Battersea and Clapham sharing a manager with the Kennington franchisee and Pimlico seemingly run by a new WINK employee.

- This H1 referred to the Battersea, Clapham and Pimlico termination in a roundabout way:

“As part of our management of the network, we proactively introduce new buyers to offices that may be looking to exit or for whom the platform is no longer suitable.

In certain cases, if the group’s conditions of business are not met, we are compelled to negotiate the exit of a franchisee to maintain our high standards. We have this year had to take these steps on several valuable franchise territories that we will look to re-franchise to talented operators in the near future.

As a result of this, we anticipate no net change in the number of offices this year, but are confident of going into 2024 with a stronger portfolio.“

- WINK’s recent appointment of its General Counsel as a main board executive may reflect the greater importance given to legal matters in what is becoming a tougher climate for the property market.

Franchisees: sales and lettings income

- The lower sales income and greater lettings income generated by franchisees during this H1 were spread throughout the branch network:

- Sales transactions down 21% versus gross franchisee sales income declining by the aforementioned 18% suggests the franchisees collected slightly higher commissions per transaction during this H1.

- This H1 disclosed WINK’s franchisees undertook 2,282 property exchanges during the six months:

- 2,282 exchanges and gross franchisee sales income of £12.3m implies the average transaction generated a £5.4k commission for the agent.

- For the preceding FY, 6,781 exchanges and gross franchisee sales income of £34.3m implies the average transaction then generated a £5.1k commission for the agent.

- Higher commission per exchange transaction underpins WINK’s aim to “uphold fees” in a “low-volume market” (point 3c):

“Risk: In a low-volume market, pressure on commission margins can increase, which may lead to lower revenues on a smaller number of transactions.

Management action: We have strong local market knowledge and expertise, both in London and in the country markets, and aim to uphold our fees by providing the highest level of service to satisfy the requirements of our customers.“

- This H1 said lettings activity remained “very busy” despite applications declining by 16%:

“Lettings saw a slight slowdown after a frenetic year in 2022. Although applicants were down by 16% on H1 2022, the business remained very busy, with Winkworth’s H1 rental income 10% ahead.

With an ongoing reduction of supply in the private rental sector due to landlords exiting the market following increasing costs and proposed new changes in legislation, the competition for properties to rent continued to be extreme.”

- H1 gross franchisee lettings income gained 10% due in part to more landlords employing WINK’s full property-management service.

- Full property-management services have become more appealing to landlords following additional rental legislation.

- WINK’s Six-Step Guide to Lettings recommends landlords use the group’s (more expensive) full management service and leave the (less expensive) basic lettings service to “experienced landlords, who are able to keep up to date with the ever changing legislation“.

- Lettings income has grown at a relatively consistent pace, and has almost doubled between H1s 2013 and 2023:

- The sales-rental split during this H1 was 47%:53%.

- This H1 suggested the sales-rental split may reverse to favour sales for H2:

“Pipelines of agreed sales have begun to rebuild since the start of the year but, as transaction timeframes have been slow, many of these agreed sales will not complete until H2 of this year. As a result, we would anticipate that the number of completions will firm up as the year progresses.“

- But January’s Q4 update then suggested the sales-rental split may not have reversed during H2:

“A substantial number of already agreed and contracted sales will now be reported in 2024.”

Winkworth versus Foxtons

- Foxtons (FOXT) claims to be “London’s leading estate agency and largest lettings agent” and remains as good a benchmark as any to assess WINK’s relative progress.

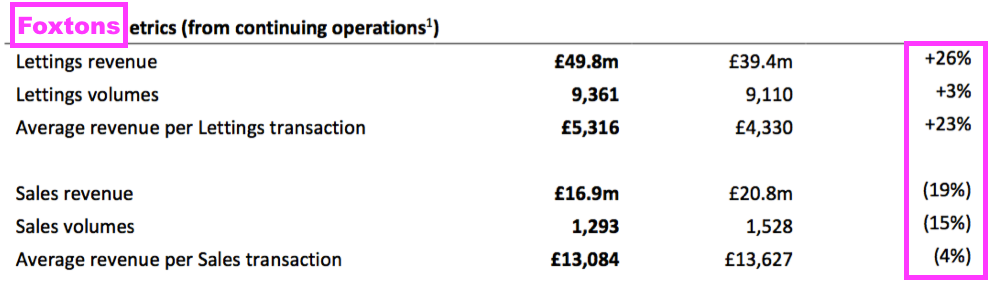

- FOXT experienced a similar H1 2023 to WINK, with sales revenue down and lettings income up:

- Note the £13k average revenue per sales transaction earned by FOXT, which compares to the aforementioned £5.4k for WINK’s franchisees.

- FOXT charges a standard 2.5% + VAT for sole agency status for selling a London property.

- Charging 2.5% + VAT for sales commissions seems high, but all credit to FOXT for also trying to “uphold” its fees in a low-volume property market.

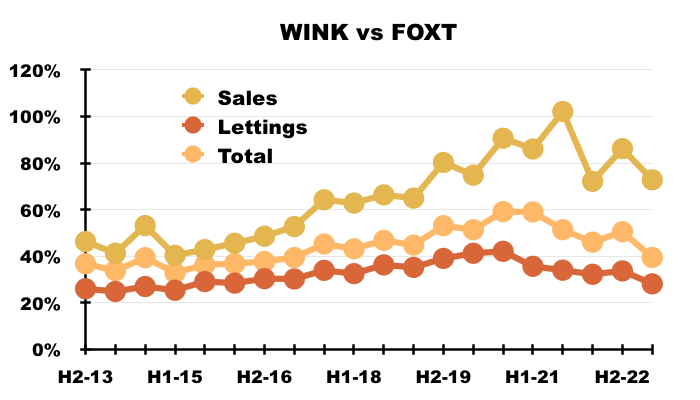

- The chart below expresses the sales, lettings and total franchisee income of WINK as percentages of the comparable FOXT revenue:

- The rising trends until FY 2021 indicate WINK’s self-employed franchisees handled London’s property market during Brexit and the pandemic far better than FOXT’s conventional employees…

- …although FOXT has improved its performance markedly versus WINK since FY 2022.

- FOXT’s improvement is linked to the 2022 appointment of a fresh chief executive.

- FOXT’s new boss quickly identified his company’s shortcomings…

- …and how to fix them:

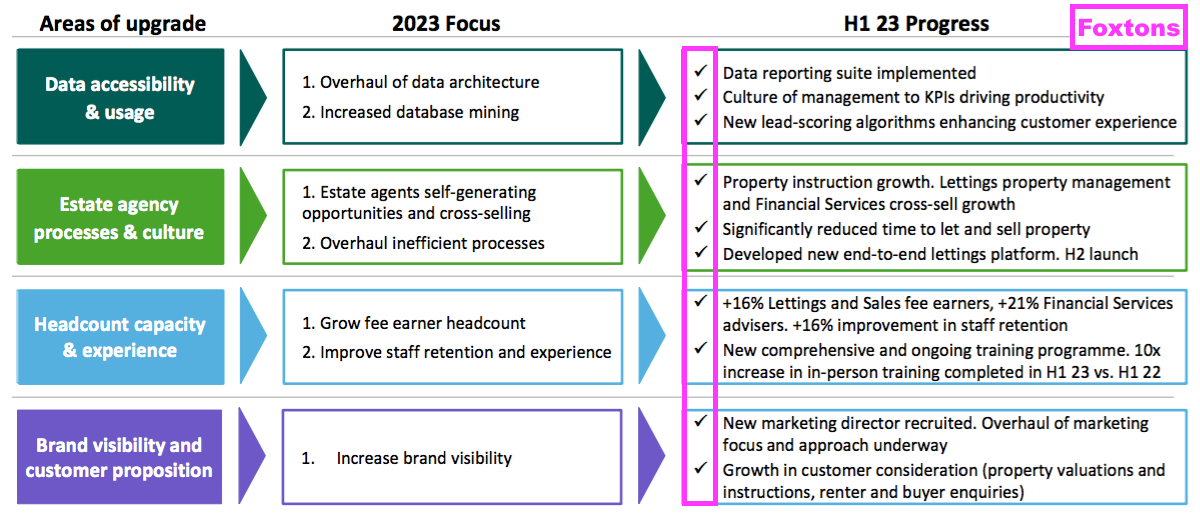

- FOXT’s H1 2023 showed lots of ticks within various “areas of upgrade“:

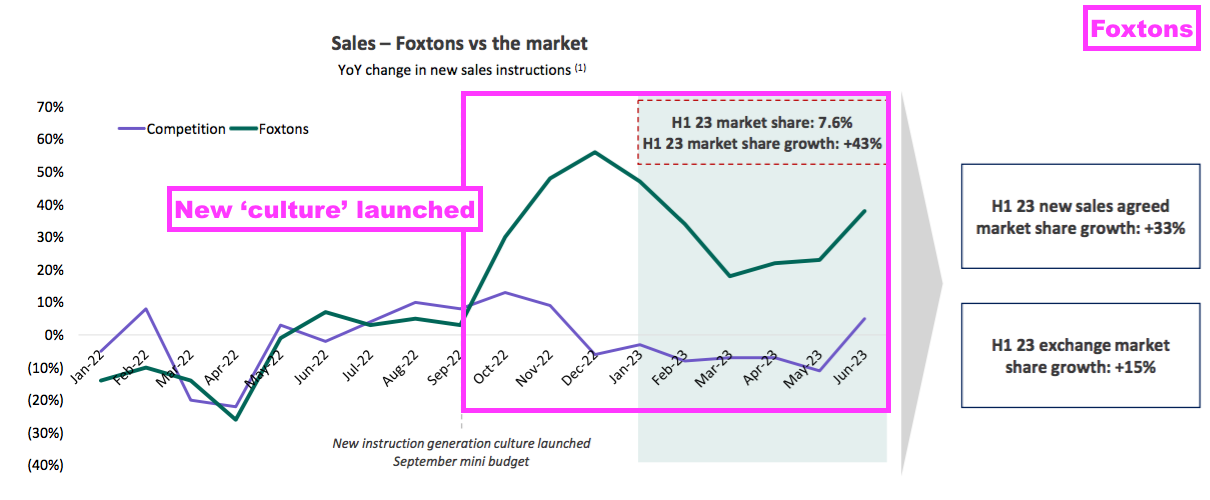

- FOXT’s sales in particular appear to have taken off versus the competition:

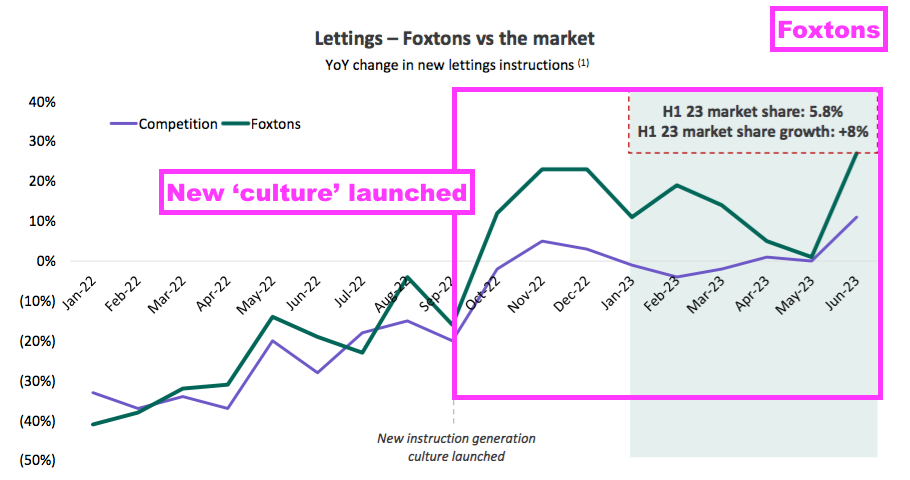

- FOXT’s lettings have also shown outperformance:

- FOXT’s adjusted operating profit for this H1 was £7m, and the new boss has said annual profit of £25m-£30m is a “medium-term ambition“.

- Meeting that £25m-£30m ambition in a slowing housing market could mean FOXT becomes very focused on taking market share from WINK and other agents.

- Note that comparing WINK with FOXT is not strictly like-for-like. FOXT generates almost all of its revenue from branches within London while WINK’s franchisees have historically generated approximately 80% from the capital.

- Further comparison distortion is caused by FOXT and WINK acquiring and/or selling businesses.

- Nonetheless, FOXT’s revitalised leadership could leave WINK facing stiffer competition in what may be a subdued time for the housing market generally (see Valuation).

Company-owned offices

- This H1 said WINK’s two controlled offices — Tooting and Crystal Palace in London — had continued to show “operational improvements“.

- To recap, WINK acquired:

- The 2020 annual report (point 15) claimed the two offices would lead to greater “front-end” insight:

“As with the acquisition of Tooting Estates Limited as a subsidiary, Crystal Palace Estates Limited will keep Winkworth in touch with and learning from front-end experiences and industry trends, It will also provide a live platform to test and develop future digital initiative and evolve our centralised CRM systems, which be of benefit to all our franchisees.”

- But subsequent management comments have suggested the purchases were driven more by improving lacklustre branches.

- For example, management’s H1 webinar talked of “new blood” being able to “maximise the revenue” at company-owned offices and “earn equity based on their success”:

“The nature of the business is that young and energetic new blood can regenerate offices. We looked at how we can get the best possible people as a business… to open new offices. [We are] developing talent that may not have the funds to [start a franchise] themselves. We [have] come up with a model where they would be able to earn equity based on their success and we would be partners. We are not trying to replicate a wholly-owned network, with all the issues that might arise from that.

We want to be a partner with people and we want it to be their business, and clearly we sit behind them. The benefit for us is that we maximise the revenue of these offices, and where we have done this we can see revenue increase three or four times, as just a result of new blood.”

- WINK has never made clear whether the equity to be earned by the “new blood” is equity in the particular office or equity in WINK.

“In South-east London, 30-year-old Jake Woolford runs Winkworth’s Crystal Palace office and is another rising star who will receive performance-related shares in the business.”

- WINK presently owns 100% of Tooting. The group acquired a further 35% of Tooting for £137k during FY 2021, and acquired the remaining 10% for £137k following this H1.

- Crystal Palace meanwhile remains 100% owned by WINK.

- Note that the agent appointed originally by WINK at Tooting departed last year to start his own business (point 16). At least the agent’s social-media messaging at the time of his departure was very cordial towards WINK.

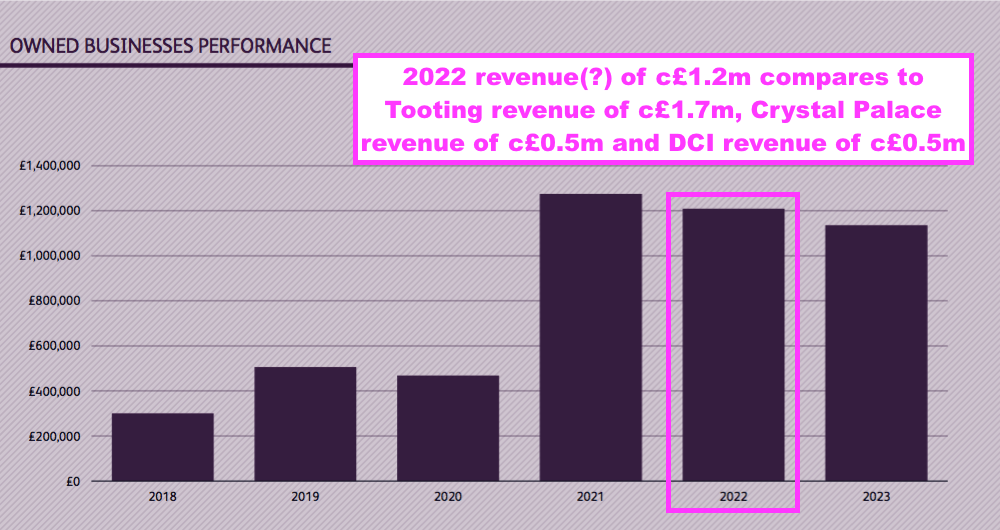

- The agent appointed by WINK at Tooting improved the office’s revenue significantly. Tooting revenue was £871k during FY 2019, then £979k (+12%) during FY 2020, £1,679k (+72%) during FY 2021 and £1,743k (+4%) during FY 2022.

- This H1 indicated both company-owned offices were top-three local operators…

“In H1, Tooting maintained its position as the leading agent by the number of sales agreed in its area (2022 Number 1 SSTC) while Crystal Palace’s market share continues to grow, moving up to second in sales agreed in its area (2022 Number 4 SSTC).

- …and both would experience stronger H2s:

“Both performances come after a poor end to last year and a positive start to 2023, with extended transaction times pushing the bulk of their completions from sales agreed in H1 into H2. This, combined with the busiest letting months traditionally falling in August and September, means that their contribution will be more heavily weighted towards H2 than usual.”

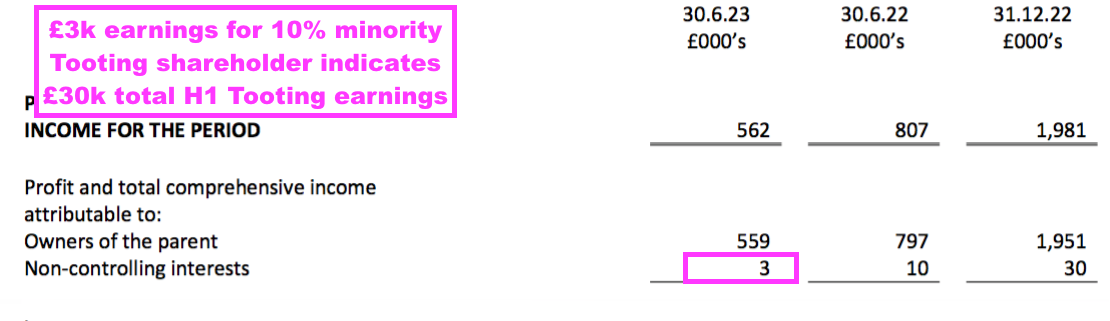

- This H1 seemed very weak for Tooting. The 10% minority Tooting shareholder earned only £3k during the six months versus £30k for the preceding FY:

- WINK’s Tooting investment had appeared extremely lucrative. In particular, the 35% purchase for £137k during FY 2021 compared to total Tooting earnings of £301k during FY 2022.

- But the post-H1 £137k investment for the final 10% of Tooting may not be as lucrative, given total Tooting earnings were £30k for this H1.

- The investment returns from Crystal Palace remain very unclear. Companies House shows the office reporting retained losses increasing from £90k to £198k during FY 2022:

- This H1 revealed a third company-owned office may be on the horizon:

“We are in ongoing negotiations for a new opportunity to replicate the successful models of Crystal Palace and Tooting.”

- I must confess to being in two minds about further company-owned offices.

- On the one hand, the returns so far from Tooting have been impressive and similar returns from another London office would be most welcome.

- But on the other hand, the general economics of owning an estate agency are not great for external shareholders.

- For example, last year LSL Property Services (LSL) converted the remainder of its owned estate-agency network into franchises. LSL said the advantages of a franchise network included:

- A higher-margin business with a significantly smaller fixed cost base, resulting in improved and substantially less volatile earnings through housing market cycles.

- The potential to grow network footprint without significant additional investment by supporting the expansion of franchisees and recruiting new franchisees

- The opportunity to benefit from the entrepreneurship and agility of independent franchisees, resulting in a more productive, flexible, and resilient business model

- I can only trust WINK does indeed limit its company-owned offices to the “best possible people“. WINK still claims its company-owned offices are “not a departure from [its] traditional franchising approach” (point 4b).

- The H1 slides indicated how a company-owned office can perform:

- I could not correlate the values within the above chart with the published revenue figures for Tooting nor the group’s entire ‘Estate agency and lettings’ segment.

- Complementing the two company-owned offices is WINK’s Development and Commercial Investment (DCI) agency, which provides advice about converting business premises into residential accommodation.

- This H1 said FY 2023 DCI revenue should be greater than the level achieved during the preceding FY:

“Despite being more affected by the cost of finance then residential property due to its transactional nature, our commercial property business continued to grow and is on track to exceed 2022 revenues. Our market share of mixed- use properties for sale in London now stands at 4.5%.”

- Companies House shows DCI revenue of £509k for the preceding FY:

- The preceding FY announced “a plan to launch a new homes operation” within the DCI venture and this H1 confirmed the operation was underway:

“As planned, we launched a new homes business to further our commercial activity, providing more properties to the network to sell and increasing revenue for both our commercial property business and our franchisees. In a difficult market for new homes, we see an opportunity to gain market share through the breadth and strength of our network.“

- This H1 noted the new-homes venture had incurred start-up costs but had also displayed “signs of promise“:

“We have re-entered the new homes business, the cost of investment being carried in the first half of 2023, an area which is showing signs of promise, with benefits expected to be realised in 2024.“

- Total H1 revenue from Tooting, Crystal Palace and DCI fell 4% to £1.1m:

- Revenue from the company-owned offices represented 27% of total revenue during this H1, versus 30% for the preceding FY and 24% for FY 2021:

- H1 Tooting earnings of £30k equated to only 5% of the group’s H1 £562k earnings. The proportion was 15% during the preceding FY (£0.3m/£2.0m).

- My guesswork suggests Tooting, Crystal Palace and DCI combined to generate a breakeven performance during this H1 (see Financials).

Financials

- This H1 demonstrated the impact of the slower property market on WINK’s margin.

- WINK converted 18.7% of revenue into profit, the lowest for any H1 or H2 since at least H1 2009 aside from the pandemic-disrupted H1 2020 (13.9%):

- The lower margin coincides with reduced sales transactions, owning two agency offices and incurring start-up expenses for the new-homes venture. This H1 admitted:

“All these initiatives, together with our investment in the Tooting and Crystal Palace offices, have broadened Winkworth’s streams of revenue. Inevitably, this has had an impact on costs but, even with the slower market of 2023, we are building new sources of profitability to add to reinvigorated franchise royalty growth.”

- The average H1 margin between H1 2009 and H1 2019 — during which WINK operated as a pure franchisor — was 25.3%.

- Applying that 25.3% margin to this H1’s management services fees of £3.1m gives an approximate £800k profit, which coincidentally matches this H1’s group profit and therefore suggests WINK’s Tooting, Crystal Palace and DCI operations may have delivered an overall breakeven H1 performance.

- H1 cash generation was not great.

- Operating cash flow of £1,059k funded an adverse £746k working-capital movement, net capex of £161k, ‘assisted acquisition support’ of £168k, tax of £353k and other items amounting to £65k, which left free cash flow at a negative £434k.

- The payment of a £763k dividend offset by £180k received from option exercises (point 19) left H1 cash £1,017k lighter at £4,234k (33p per share).

- Operating cash flow during recent FYs has been approximately two-thirds weighted towards H2, and January’s Q4 update indicated cash generation did indeed improve during H2 with FY 2023 cash “to be at least £4.4m“.

- The cash position remaining around the £4m mark is due to WINK distributing the vast majority of its reported earnings as a dividend (see Valuation).

- WINK’s balance sheet remains free of bank debt and defined-benefit pension obligations.

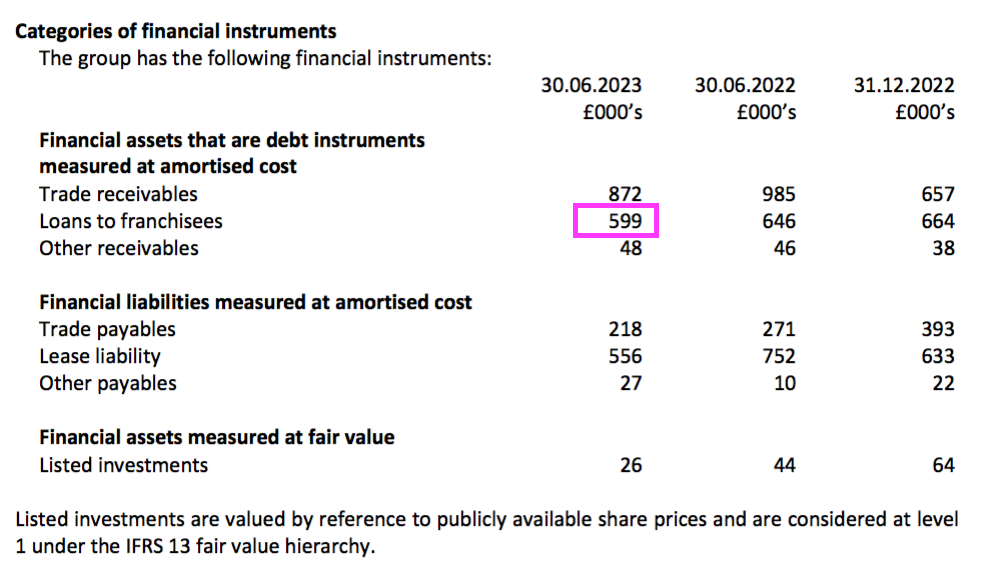

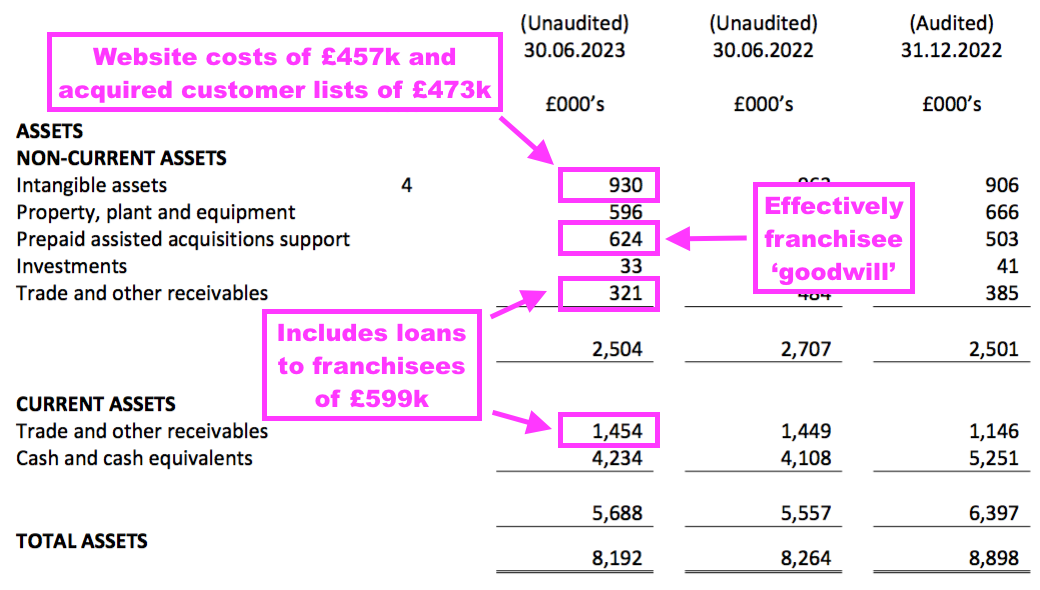

- The balance sheet also includes loans to franchisees of £599k:

- Other balance sheet items include capitalised website costs of £457k, mystery investments of £33k and ‘prepaid assisted acquisitions support’ of £624k:

- ‘Prepaid assisted acquisitions support’ are sums paid by WINK to:

- Convert existing independent agencies into franchisees, and;

- Acquire additional businesses to operate within existing franchisees.

- Management’s FY 2021 webinar talked of WINK paying four years’ worth of 8% commission to a suitable independent agent to convert into a WINK franchisee.

- Management’s FY 2022 webinar talked of paying an amount equivalent to three times 8% of the revenue of a target lettings portfolio on behalf of a franchisee.

- The carrying values of prepaid assisted support (£624k), ‘customer lists’ acquired with Tooting and Crystal Palace (£473k) and capitalised website costs (£457k) amount to almost £1.6m, all of which has yet to be expensed through the income statement.

- Finance income earned on the £4.7m average H1 cash position and the £632k average H1 loans to franchisees was £34k and equivalent to an annualised 1.3%.

- £34k/1.3% seems too low, especially as loans to franchisees ought to be paying WINK much more than standard bank interest. For perspective, NatWest for example offers an instant-access business account paying between 1.46% and 1.92% AER (variable).

- I trust WINK’s finance income improved significantly during H2.

- Management’s H1 webinar did indeed foretell of greater H2 interest:

“We are seeing interest being paid on our deposits, and we expect that to increase over the rest of the year. We have various investments that we are looking at at the moment, so it is difficult to lock away money for an extended period of time. It is something that we continue to monitor.“

Valuation

- This H1 gave an equivocal view of the property market:

“The outlook for the rest of the year depends to a large extent on the perceived and actual end of the tightening cycle and the Bank of England’s success in managing inflation down towards its target.

This will continue to impact directly on the stability of the mortgage market and the number of products available as well, of course, on buyers’ confidence. We expect, however, sales market activity to be underpinned by strong employment, sellers coming to the market to manage mortgage cost increases, and buyers motivated by the lack of availability of suitable rental accommodation.”

- January’s Q4 update confirmed FY 2023 sales transactions fell 19%, which was a small improvement on the 21% decline during this H1:

“The rise in interest rates, which began after the mini budget in Q4 2022 and was sustained through 2023 by the fight against inflation, took its toll on the UK property market…

Hesitancy on behalf of buyers, however, along with legal delays in conveyancing, led to a downturn in transactions. Winkworth’s network completed sales for the year fell by some 19%.”

- January Q4 update also revealed FY 2023 gross franchisee lettings income advanced 5%

“The shortage of rental property in 2023 and consequent rise in prices translated into an increase in our network revenues of around 5%, offsetting the slower sales completions.”

- That 5% advance compared to the 10% lettings uplift during this H1, suggesting H2 experienced minimal lettings growth.

- January’s Q4 update was not overly bullish on lettings for FY 2024:

“We believe that the rise of accidental landlords, postponing their sales due to price uncertainty and switching to the lettings market, combined with tenants hitting affordability ceilings, will lead to lower growth in 2024 and slowing rent increases. Price increases from previous years, however, will continue to feed through as properties come up for re-letting, underpinning growth in the sector.”

- The Q4 update said FY 2023 pre-tax profit should be approximately £2.1m:

“Winkworth’s full year pre-tax profits, subject to audit, are expected to be in line with the current market forecast of £2.1m (31 December 2022: £2.47m) and net cash at year end, following increased investment in new offices in 2023, to be at least £4.4m (31 December 2022: £5.25m).“

- FY 2023 pre-tax profit of £2.1m means H2 recorded a £1.3m pre-tax profit — down only 7% on H2 2022.

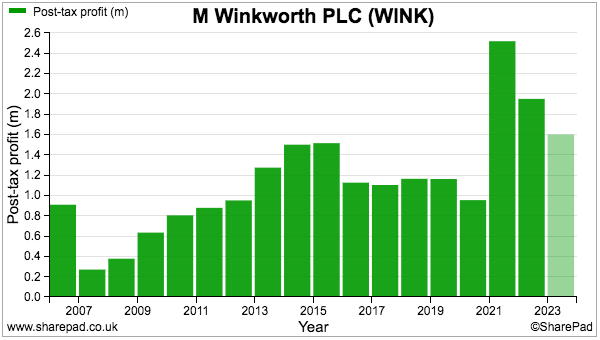

- FY 2023 pre-tax profit of £2.1m compares to £2.5m for (pandemic-boosted) FY 2022, £3.2m for (pandemic-boosted) FY 2021, £1.5m for (pandemic-blighted) FY 2020 and £1.6m for (pre-pandemic) FY 2019.

- £2.1m after standard 25% UK tax gives earnings of £1.6m or 12.2p per share.

- Earnings of 12.2p per share does not leave much room for dividend advances given January’s Q4 update confirmed the FY 2023 payout will be 11.7p per share:

- Management’s H1 webinar nonetheless reiterated WINK’s “progressive” dividend:

“We are as a company committed to paying a progressive dividend as long as trading conditions permit. As we pay dividends on a quarterly basis, we are in regular discussion with the board about the level of that dividend and its appropriateness.“

- This H1 even hinted the group’s cash position could shore up the payout if need be:

“The policy of holding cash reserves is not only to underpin our dividend, but also to increase revenues through assisting the purchase of new franchise businesses or buying rental portfolios.”

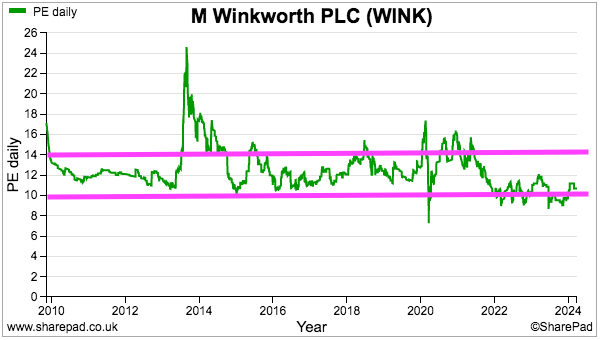

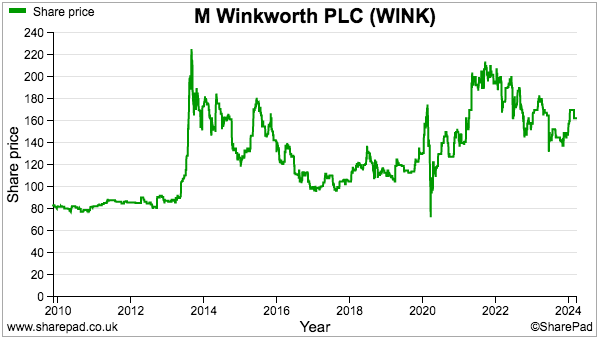

- Dividing the 170p offer price by my 12.2p per share earnings guess gives a P/E of 14x.

- Assume the £4.2m/33p per share cash position is not required for the business to operate successfully (or shore up the dividend!), the cash-adjusted P/E could be (137p/12.2p) = 11x.

- A multiple of 11x or 14x or somewhere in between is not outrageous, but nor is it out of keeping with WINK’s typical trailing P/E of 10x-14x:

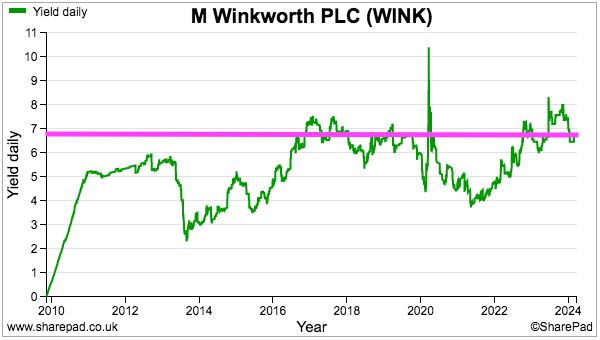

- The FY 2023 11.7p per share dividend meanwhile supports a 6.9% income — a level that has been witnessed previously on occasion:

- WINK’s current rating no doubt reflects the slower housing market and perhaps the prospect of stagnant earnings beyond FY 2023:

- Mind you, management was positive during this WINK podcast from February:

“Home buyers are feeling upbeat. We are seeing registrations 29 per cent ahead of last year and an uplift in instruction of 40 per cent ahead of last year.”

- Nonetheless, the headlines from Property Industry Eye support the notion the country’s property market remains somewhat dysfunctional:

- “Dame Kate Barker to lead new study into England’s housing shortage“

- “UK housing is ‘worst value for money’ of any advanced economy – thinktank“

- “Brave politicians required to free the shackles from the housing market“

- “MPs launch inquiry on improving the home buying and selling process“

- “Estate agency regulation is coming, and we for one will welcome it“

- “Over four out of five tenants remain unaware of the Renters (Reform) Bill“

- “CMA frees hundreds more leaseholders from costly contract terms“

- “Major changes to crack down on long-term empty homes fast approaching“

- “Property guru turned TV star misled investors to raise £731k“

- “Hike in complaints against agents leads to sharp rise in compensation“

- Statistics from Rightmove indicate transaction volumes nationally have yet to recover from their 2007 heyday — and industry ‘growth’ therefore has been supported only by higher asking prices:

- I first bought WINK during 2011 at 90p and the shares have since delivered a very generous income. Total payouts (ordinary and special) throughout the last 13 years have totalled 114p per share to recoup my entire initial investment.

- Capital gains during the same twelve years have in contrast been somewhat muted:

- The risk for long-term shareholders is the “progressive” dividend that has dominated past returns eventually becomes untenable as:

- A challenging housing market becomes even more challenging;

- Lower profit stays low, and;

- The thin dividend cover becomes even thinner.

- Long-term shareholders include the chairman, who owns 41%/£8.5m, the chief executive (and chairman’s son), who owns a further 6%/£1.2m, and a non-exec, who owns another 3%/£0.6m.

- The board therefore has good reason to ensure the dividend is sustained during difficult times.

- Difficult times may also provide WINK’s franchisees outside of London with greater expansion opportunities in readiness for a market upturn. This H1 claimed:

“The change in market conditions has led some of the national networks to slow their pace of acquisition. We see opportunities for our own increasingly established network of country franchisees to strengthen and grow their footprint through expansion supported by our balance sheet.”

- As a market upturn is awaited, the chairman’s 41% shareholding has potential to create some intrigue.

- The chairman bought WINK outright during 1974 and turned 81 years old last year. Will his 41% stake one day be handed to other family members, or could WINK be sold outright?

- The recent merger between Property Franchise and Belvoir — two major lettings-agency franchisors — is proof sector consolidation has not yet subsided.

Maynard Paton

Hi Maynard,

Was wondering what you’re take is on the negative goodwill. For me, as the acquisition of the Pimlico office causing a negative Goodwill of £252K comprising an intangibles of £336K and a deferred tax liability of £84K.

My immediate reaction is to remove the £252K from the earnings which reduced the eps to 11.05p as the previous franchisee returned it rather then either renewing or trying to sell the goodwill on. The net cashflow prior to investments and financing is also down 50% from 2022.

I therefore make their P/E 15.8 a relatively high rating for the current market and economy.

What are your thoughts?

Hi H,

Agreed, I would remove the negative goodwill from earnings and any valuation sums as the entry is not a trading profit. I must confess I have never been truly convinced about the value of WINK’s intangible ‘customer lists’ and why they are amortised over 15 years, which is a long time. Still, i) the accounting rules do dictate companies must identify intangibles on any transaction and ii) the values involved are not hugely material at WINK. I suppose the share price reflects the upbeat outlook commentary and the 3p quarterly dividends that support a 6%-plus yield. Although dividend cover is very thin, or has disappeared for now going on your 11p EPS!

Maynard

A 6.3% earnings yield seems tight. I guess the low capital requirements and high returns on equity/ capital help, along with the growth opportunities and funding help.

I recently skimmed through their listing documents and noticed that they’ve stepped back from international expansion. On the documents they had some offices in Portugal and something or other in France. That no longer seems to be in their plans.

Hi H

I believe there is currently one international office, but it is never mentioned. I can’t really see the WINK model working overseas, as few vendors in, say, Portugal will be convinced of selling through WINK just because they may attract a buyer moving from London. Might as well sell through a local agent. I suspect relatively few vendors using WINK’s London offices will want to move abroad, too.

Maynard

M Winkworth (WINK)

Q1 Dividend Declaration published 10 April 2024

A short statement announcing a 3p per share Q1 payout. Here is the full text:

——————————————————————————————————————

“The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 3.0p per ordinary share for the first quarter of 2024 to shareholders.

The timetable is as follows:

Ex-Dividend Date* 18/04/2024

Record Date** 19/04/2024

Expected Payment Date 16/05/2024

The Company will announce its audited financial results for the year ended 31 December 2023 on 17th April 2024.

* Shares bought on or after the ex-dividend date will not qualify for the dividend

** Shareholders must be on the Winkworth share register on this date to receive this dividend.”

——————————————————————————————————————

The 3p per share dividend is a 0.1p per share improvement on the comparable Q1 2023 and matches the preceding Q4 2023 payout. The FY 2024 payout ought therefore to be at least 12p per share.

The higher Q1 payout is reassuring given January’s Q4 2023 update signalled H2 pre-tax profit declining 7% (see blog post above). That said, the subsequent FY 2023 results (review coming soon!) disclosed earnings of 13p per share, which do not leave that much room for further payout advances.

Maynard