I have recorded another episode of The Private Investor’s Podcast with my good friend Mark Atkinson. We discussed City of London Investment (CLIG) and my recent share purchase, my AGM attendance and the company’s 9% dividend yield:

A somewhat better-than-expected FY performance, with record revenue and earnings supported by an exceptional H2 profit (+30%) that was bolstered by a post-pandemic recovery and stronger USD.

Encouraging sales progress from best-seller vitamin D (+13%), future big-seller troponin (+81%) and sudden surprise-seller biotins (+67%) more than offset lost income from an expired product.

Tweaks to management’s commentary plus a revised pipeline grid suggest the development work on dementia research now offers a greater chance of becoming a real money spinner.

The accounts remain in great shape, with an astonishing 82% H2 margin, terrific employee productivity and robust cash conversion leading to the company’s seventh consecutive annual special dividend.

Troponin’s finite income and a basic sum-of-the-parts valuation may explain why the £36 shares have not made headway during the last three years. I continue to hold.

Read a set of company results, and chances are you will spot a reference to Trustpilot. Examples of quoted businesses mentioning the popular review website include:

AJ Bell:“Our operational performance indicators have shown excellent levels of customer service as demonstrated by our high 4.5-star Trustpilot score.“

AO World: “Over 350,000 Trustpilot ratings, averaging an “Excellent” 4.6/5 stars.“

Big Yellow: “We have over 3,200 reviews from the independent review site TrustPilot. These reviews average a 4.7 out of 5-star rating, labelled as “Excellent” on the TrustPilot ratings scale.”

Procook: “We are pleased to have retained our excellent-rated Trustpilot score of 4.8.“

Redde Northgate: “Customer satisfaction is the cornerstone of our business success and the ‘excellent’ satisfaction scores achieved across our businesses from Trustpilot.“

Redrow: “We continue to be rated as ‘excellent’ on Trustpilot.“

ScS Group: “Improved Trustpilot rating to the maximum 5 stars, maintaining our ‘Excellent’ rating with over 370,000 reviews.”

Travis Perkins: “The experience with Toolstation remains best-in-class with the business achieving a 4.6-star rating on Trustpilot.“

With so many quoted companies trumpeting their Trustpilot reviews, is Trustpilot itself worthy of a 5-star investment rating?

An acceptable H1 performance that would always struggle against the comparable (and exceptional) H1 but encouragingly matched the preceding H2.

The subsequent Q3 update provided reassuring ‘mini-budget’ commentary, reiterated an earlier £2.1m profit forecast and announced a further 23% quarterly dividend lift.

Claims of a leading SSTC market share may contradict statistics from Foxtons, with fresh leadership at the London rival set to create stiffer competition.

A robust 25% margin plus £4m net cash left the accounts in good order, although cash conversion was impacted by rising intangible expenditure and more franchisee loans.

The gloomy outlook for the economy and housing market looks responsible for the possible 10-13x P/E and yield that approaches 7%. I continue to hold.

I have recorded another episode of The Private Investor’s Podcast with my good friend Mark Atkinson. We talked about System1 and the investment potential of testing adverts:

Results summary for City of London Investment (CLIG):

Rough market conditions causing funds under management (FuM) to fall 17% to $9.2b led to H2 net fee income dropping 5% and H2 profit diving 20%.

A post-year update showed FuM sliding a further 8% to $8.5b, but also the fourth consecutive quarter of net FuM inflows that may signal clients re-appraising CLIG’s ‘value’ approach.

Buying SPACs at discounts to cash helped merger partner KIM outperform the original CLIM division with 6% five-year annualised returns versus 3-4%.

Revenue “100%” denominated in the stronger USD, handy cash conversion plus net funds and investments of £30m counterbalanced an H2 margin squeezed to ‘only’ 42%.

Near-term earnings could now be running at 36p per share, which should still support the 33p per share dividend and 8%-plus yield at 400p. I continue to hold.

***ShareScope New Subscriber Special Offer*** Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

20 October 2022 By Maynard Paton

Difficult market conditions have led to depressed ratings for many asset-flush shares.

Hence a new screen to pinpoint companies offering cash-rich balance sheets and market caps below their book value. I have attempted to avoid ‘value traps’ by demanding the shares pay a dividend and offer a history of trading above book value.

The exact filter criteria I employed for this search were:

A price to net tangible assets of no more than 1;

A dividend being paid during the most recent year;

A 10-year average price to net tangible assets of at least 1;

Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations), and;

A share price denominated in pounds sterling.

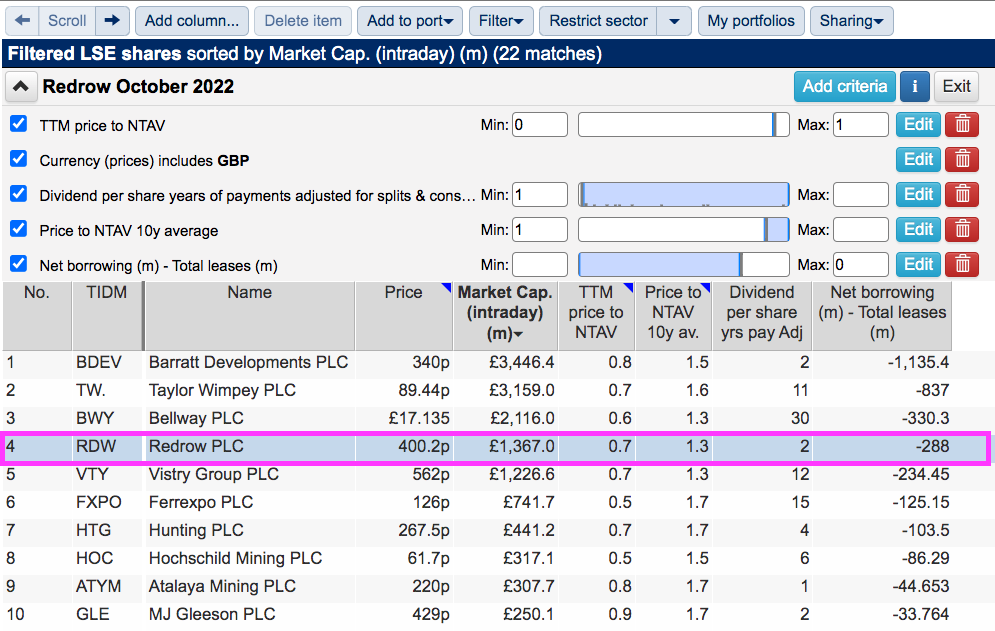

I applied the screen the other day and SharePad returned 22 matches:

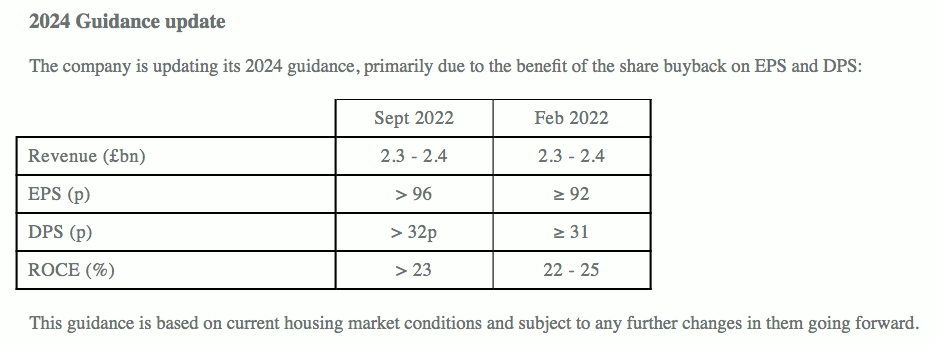

I selected Redrow from the five house builders at the top of the list because the group’s recent results included very clear guidance:

Redrow’s own projections put its 400p shares on a P/E of approximately 4 and a yield of at least 8%

Combined with a net asset value of 554p per share that gives a price to book of 0.72, the FTSE 250 constituent is very much trading at the ‘deep value’ end of the market spectrum.

Happy Sunday! I trust your shares continue to perform better than mine during 2022.

A summary of my portfolio’s progress:

Q3 return: -9.2%*.

Q3 trades: None.

YTD return: -23.4%* (FTSE 100: -3.9%).

YTD winners/losers: 2 winners vs 9 losers.

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, custody fees, paid dividends and cash interest)

I am heading for my worst annual performance for at least two decades after my portfolio fell 9.2% during Q3 to leave my shares down 23.4% for the year so far.

Yet despite another miserable quarter of negative returns, the Q3 newsflow did not seem particularly awful.

Special dividends were in fact declared by Andrews Sykes and Tristel, which takes one-off payments for me this year to six and cements 2022 as my best-ever year for extra income. The quarter also witnessed higher payouts from M Winkworth and S & U.

I have recorded another episode of The Private Investor’s Podcast with my good friend Mark Atkinson. We talked about Greggs and the investment potential of sausage rolls:

A disappointing FY 2022 performance, with a Q4 sales warning alongside greater costs leading to a small H2 loss.

SYS1’s ‘Reasons to Believe’ have been diluted, and hint at reduced long-term expectations following the disappearance of a £100m revenue ambition.

The transition to new data and consultancy services continues, with such income representing 51% of total revenue for FY 2022 and possibly 70% for Q1 2023.

A fresh non-exec reveals the agitated shareholder who has initiated a strategic review, which in turn led to the sensible cancellation of a tender offer.

Net cash represents 31% of the market cap, with long-term multi-bagger potential presently obscured by weak legacy services and costs running ahead of new-product revenue. I continue to hold.

A trio of upbeat trading statements caught the market’s attention this summer.

The first occurred during June and referred to “strong margin improvements“:

“29 June: Shoe Zone is pleased to announce that since the publication of its interim results in May, the business has been trading well andhas also seen strong margin improvements and cost savings, in particular as a result of rent reductions and good supply chain management, which are expected to continue into Q4 of the Company’s financial year for the 52 weeks to 2 October 2022″.

The second update followed in July, and revealed “stronger than expected” trading:

“26 July: Shoe Zone is pleased to announce that since the publication of its trading update on 29 June 2022, trading has been stronger than expected due to higher than expected demand for summer products, particularly in the last two weeks. The Company has also continued to experience margin improvements as a result of good supply chain and cost management.”

And the third update occurred last month, and confirmed trading had “continued to exceed expectations“:

“31 August: Shoe Zone is pleased to announce that since the publication of its trading update on 26 July 2022, trading has continued to exceed expectations due to continued strong demand for summer and back-to-school products throughout August. The Company also continues to benefit from the margin improvements as outlined in recent trading updates.”

The remarkable run of RNSs also revealed the group lifting its current-year profit expectations from “not less than £8.5 million” to “not less than £10.5 million“.

The profit upgrades and share-price surge will of course be welcomed by shareholders, although the company’s longer-term performance could mean the positive summer may not be a persistent phenomenon.

The shares joined AIM at 160p during 2014 and, eight years later, the price stands at… 160p:

A steady FY 2022 performance, buoyed by an H2 that saw property sales achieve a record £379k average and realise a 66% premium to their 2014 Allsop valuation.

The final dividend was lifted 11% while expenditure on new properties fell to a 13-year low after management expressed a desire to “not chase purchases at any price“.

Net debt remains very modest at just 5% of the property estate and reflects management’s concerns of forthcoming “difficult economic circumstances“.

Friction between major shareholders continues, with revised director-pay arrangements perhaps encouraging significant protest votes at the latest AGM.

Net asset value remains at £101 per share, although the balance sheet could be worth £210 per share assuming all owned properties enjoy immediate ‘reversionary’ gains and are then sold at fair-market value. I continue to hold.

I have recorded another pilot episode of The Private Investor’s Podcast with my good friend Mark Atkinson. We talked about Somero Enterprises and the investment potential of the company’s concrete levelling machines:

An unspectacular H1 performance, albeit accompanied by a 21% dividend lift, after further pandemic disruption left revenue down 8% and adjusted profit down 9%.

Muted progress from vitamin D and other established antibodies continues to leave near-term growth dependent on the fast-selling troponin product.

The “exciting” potential of a Tau biomarker alongside the BVXP website selling pyrene test kits suggest positive developments within the research pipeline.

Net cash at £5m is the lowest for six years, and combined with standstill earnings seems likely to reduce the size of any FY 2022 special payout.

Troponin’s finite income and a resultant sum-of-the-parts valuation do not indicate an obviously compelling £33 share price. I continue to hold.

Rhys Thomas: “Maynard, I have really enjoyed reading your column, and your original contributions back in the TMF days. Many thanks for…” 30 Mar 2026

Roger: “I’m late to the party with my comments – apologies. I’m sorry that you have to stop and enjoyed reading…” 27 Mar 2026

Johnny boy: “Maynard, I have really enjoyed reading you write-ups over the years. Please don’t lose your passion for individual stock picking.…” 16 Mar 2026

NIGEL: “Maynard I would also like to thank you for all the work you have done over the years. I have…” 25 Feb 2026

James H: “Hi Maynard, I’d like to put on record my thanks to you for all of the content over recent years.…” 14 Jan 2026

Zach: “Hello Maynard, You may or may not remember me. I joined the company you retired from just a month or…” 09 Jan 2026

Simon Brenncke: “Thanks for this instructive summary of your portfolio developments, and all the best!” 09 Jan 2026

Anonymous: “Thank you for such meticulous and fascinating insight over the years. I’ve only followed your output relating to one company…” 07 Jan 2026