28 July 2022

By Maynard Paton

***SharePad 25% OFF Special Offer***

Use promo code mp25 to claim your 6-month discount. Click here for details. #ad

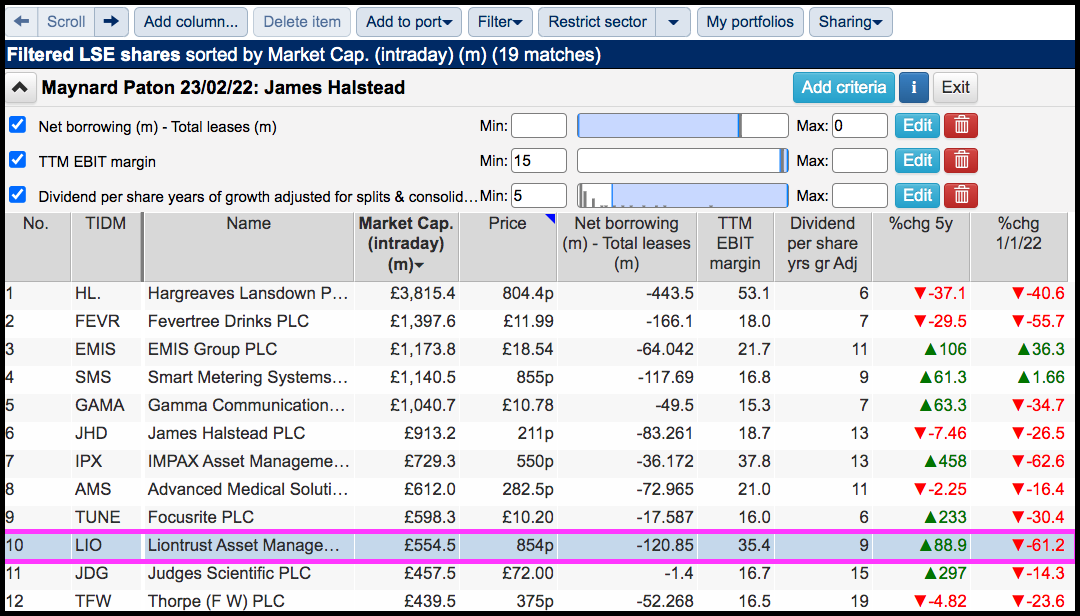

Difficult market conditions have prompted yet another bout of ‘back to basics’ filtering.

Introduced the other month to identify James Halstead, this screen short-lists companies that offer cash-flush balance sheets, robust margins and dependable dividends. SharePad returned 19 matches:

I selected Liontrust Asset Management because the shares were highlighted by ace fund manager Keith Ashworth-Lord within his latest Buffettology fund factsheet. Mr Ashworth-Lord wrote:

“Liontrust Asset Management (-15.5%) announced final results which showed substantial growth in average AUM (+43%), revenue (+41%), dividends per share (+53%) and free cash flow (+122%).

The reaction of Liontrust’s share price — which will be seen by the teenage scribblers in the City as high beta — is symptomatic of current market sentiment. As a result, the shares trade on a trailing free cash flow yield of 15% and a trailing dividend yield of 8%. Talk about ‘value’.”

Let’s take a closer look.

Read my full Liontrust Asset Management article for SharePad.

Maynard Paton

G’day Maynard, i have three things

1) fantastic LIO sharepad piece. I own the business and added some new shares last week so your overview was very timely and well thought

2) this is an interesting comment on ASY I saw this morning https://uk.advfn.com/cmn/fbb/thread.php3?id=11502813&from=2386

3) any ideas on the direct line trading update comparison for SUS?

Adek

Thanks Adek. Glad you liked the LIO article. Some good work by the ADVFN poster on ASY. I am well behind on my results reading, and have yet to look at ASY’s 2021 report, but I recall from the 2020 report ASY outlined in some depth some ‘stress test’ scenarios that gave a clue as to management’s best performance guess. An earlier post on ADVFN about ASY’s blog saying the company has been very busy seems encouraging, too. I am not clear whether Direct Line’s insurance update has any clear impact on SUS’s car-loan business, other than costs generally are increasing that could make loans less affordable to some borrowers.

Maynard