04 August 2022

By Maynard Paton

Results summary for Tasty (TAST):

- The absence of pandemic restrictions ensured a bumper H2 performance that TAST acknowledged may not be repeatable during the current year.

- Higher wages, rising utility costs, “prevailing economic uncertainties” plus a June update that did not refer to H1 trading could be other signs of FY 2022 not being that profitable.

- Rent reductions of 27% now appear to be temporary, and explain why total lease obligations remain in excess of £50m.

- Repaying an emergency loan, appointing a new executive alongside plans to open 5-6 new restaurants confirm management’s mindset has moved from ‘survival’ to ‘recovery’.

- Although the £8m market cap could be remarkably cheap if TAST ever sustains a modest margin on decent sales, other shares could offer more dependable returns. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TAST

- Results summary

- Revenue and profit

- Revenue per restaurant and per employee

- Financials: going concern, Barclays loan and new openings

- Financials: cash, cash flow and deferred payments

- Financials: landlords and leases

- Financials: cost analysis

- Immediate prospects, board changes and revised menu

- Valuation

News links, share data and disclosure

News: Annual report for the 52 weeks to 26 December 2021 published 23 March 2022, directorate changes published 22 June 2022 and repayment of bank facility published 23 June 2022

Share price: 5.25p

Share count: 146,315,305

Market capitalisation: £7.7m

Disclosure: Maynard owns shares in Tasty. This blog post contains SharePad affiliate links.

Why I own TAST

- Disastrous ‘legacy’ shareholding bought initially due to experienced family management building and selling two quoted restaurant chains for £200m-plus.

- Repayment of emergency pandemic funding, the appointment of a new executive alongside plans to open 5-6 new restaurants suggest a shift from ‘survival’ to ‘recovery’.

- Bombed-out share price might provide substantial turnaround upside… assuming sales can rebound to pre-pandemic levels and return the group to profit.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary

Revenue and profit

- A promising update during March had already indicated these FY 2021 results would show a much better performance than the pandemic-blighted FY 2020.

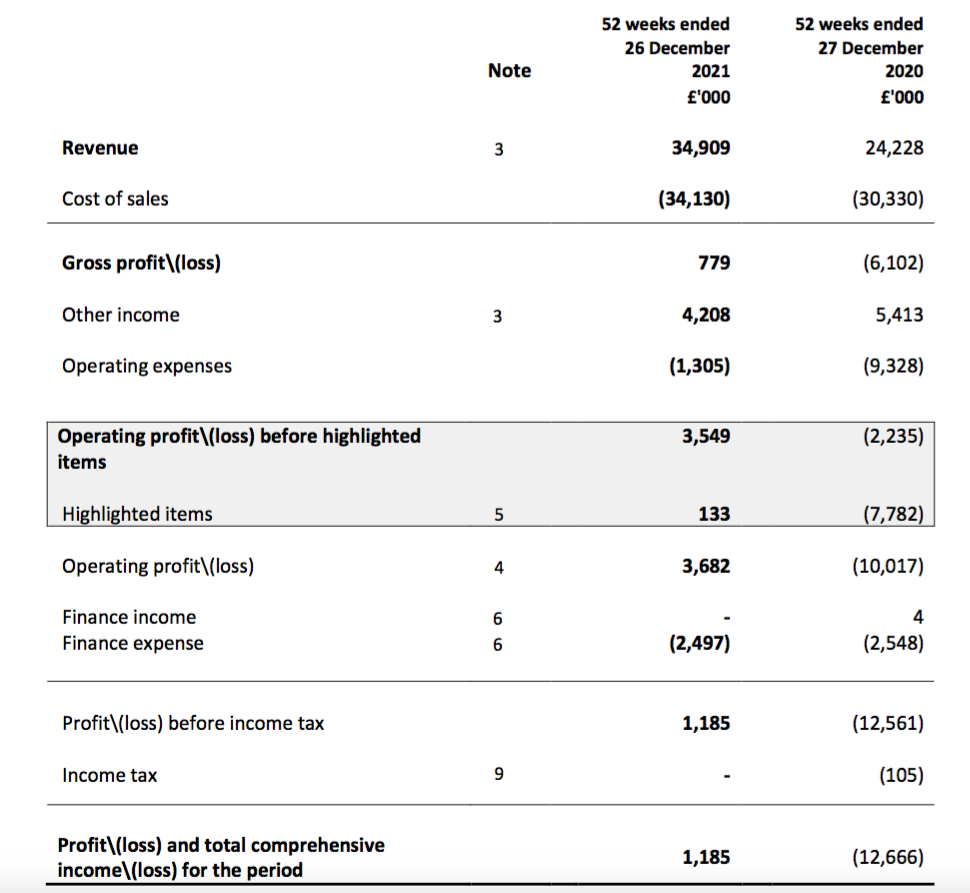

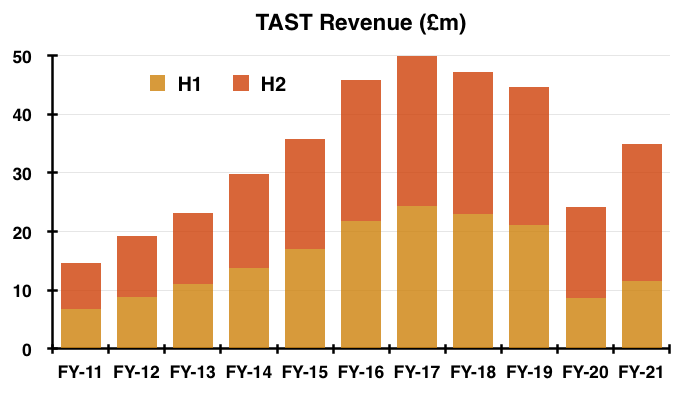

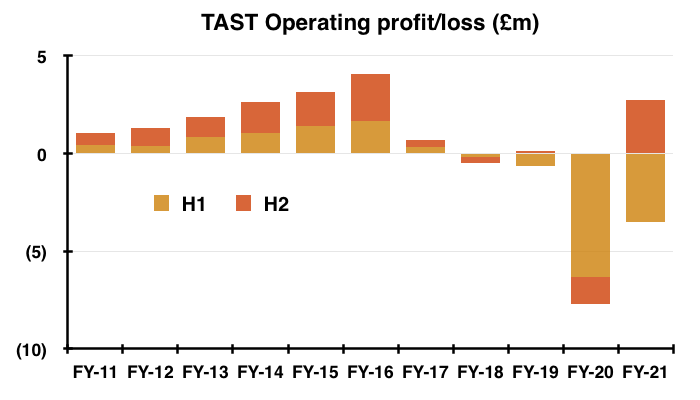

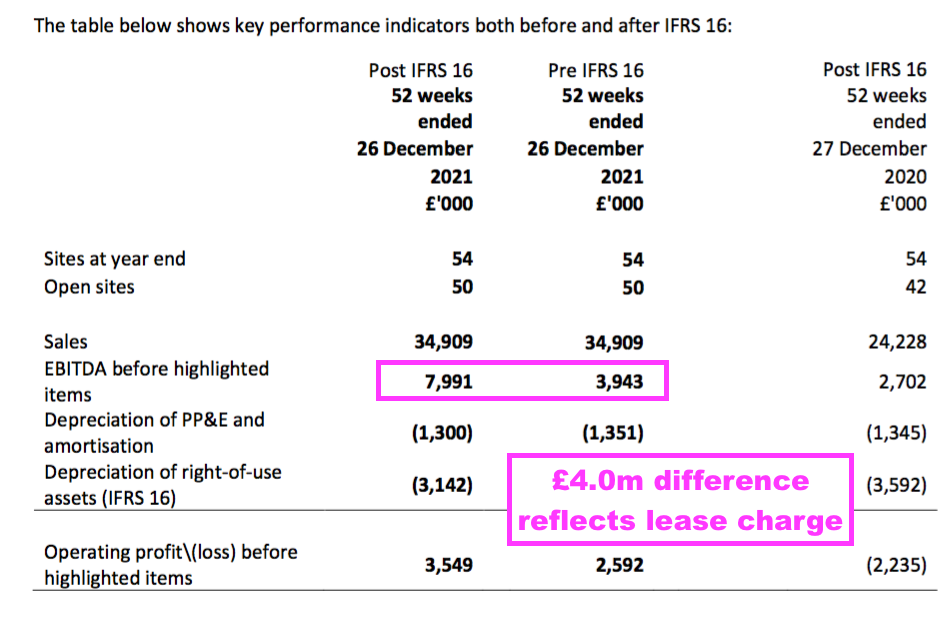

- Full-year revenue did indeed jump 44% to £34.9m while adjusted Ebitda did indeed surge 196% to £8.0m.

- The performance meant H2 enjoyed revenue of £23.3m, up 50% on H2 2020 and — more importantly — almost level with the £23.4m registered during pre-pandemic H2 2019.

- Reported profit included various ‘highlighted’ items alongside government pandemic support of £3.9m. Excluding such expenses and income, H2 enjoyed a £2.7m operating profit:

- TAST’s H2 in fact the witnessed the group’s best ever six-month operating profit since H2 2016 (£2.8m).

- Unlike H2 2020, H2 2021 suffered no pandemic restrictions and all restaurants were allowed to serve diners inside for the full 26 weeks.

- TAST acknowledged the H2 2021 performance may not be repeatable during FY 2022:

“We are conscious that performance was assisted by VAT and business rate support, staycations, pent-up demand and unusually high level of disposable income. We are expecting that most of the support and peaks in consumer trends will follow a more normalised path during 2022 and we have planned for rising costs and labour shortages. “

- VAT and business-rate support finished at the end of March 2022.

- Mind you, H2 did suffer the Omicron outbreak and Christmas trading was poor:

“Trading was highly encouraging when dine-in was permitted from May 2021, but impacted in December 2021 as the Omicron variant took hold and spread amongst the UK population. Subsequent Government advice meant that Christmas trade, traditionally our most profitable period, and specifically December 2021, was much weaker than we had anticipated.“

- Without Omicron, H2 may well have been TAST’s best ever six-month performance for revenue and profit.

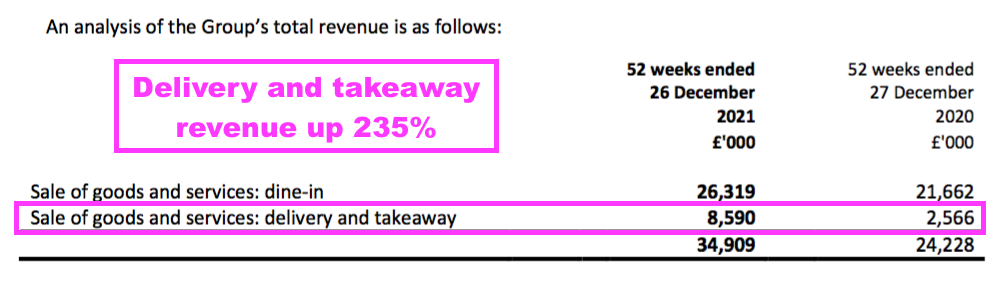

- Underpinning the revenue performance was delivery and takeaway sales, which notably “rejuvenated” TAST’s five dim t restaurants:

“With an increased appetite for delivery and takeaway, we have seen strong sales growth. We plan to capitalise on this by expanding our virtual brands and different formats in new locations to optimise growth. Dim t has been rejuvenated through its successful takeaway and delivery sales growth. “

- TAST’s dim t format has for many years operated as a sideshow to the group’s 49-site Wildwood chain.

- These FY 2021 results were the first to segment dine-in revenue from delivery/takeaway sales:

- Delivery/takeaway revenue rallied 235% during the year, versus 21% for dine-in.

- Delivery/takeaway income represented 25% of total revenue last year, and further growth might prevent a return to the marginal dine-in profits witnessed prior to the pandemic.

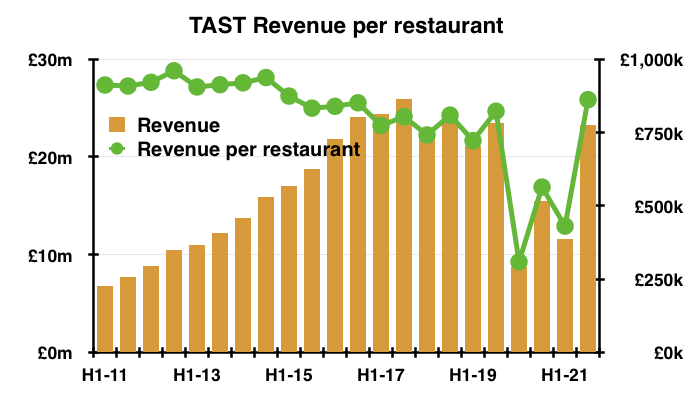

Revenue per restaurant and per employee

- TAST leased 54 restaurants throughout FY 2021. Six sites were not trading at the start of the year while four remained closed at the end of the year.

- Revenue per restaurant for the full year was £646k (£34.9m/54), but was an annualised £862k for the bumper H2 (£23.3m*2/54):

- £862k per restaurant compares to £823k for (pre-pandemic) H2 2019 and was the best six-month performance for that measure since H1 2015 (£874k per restaurant).

- The annualised H2 2021 calculation could arguably be £931k per restaurant based upon the 50 open sites at the end of the year.

- And the annualised H2 figure may well have reached £1m without the Omicron interference.

- Revenue per employee showed a similar bounce back for FY 2021:

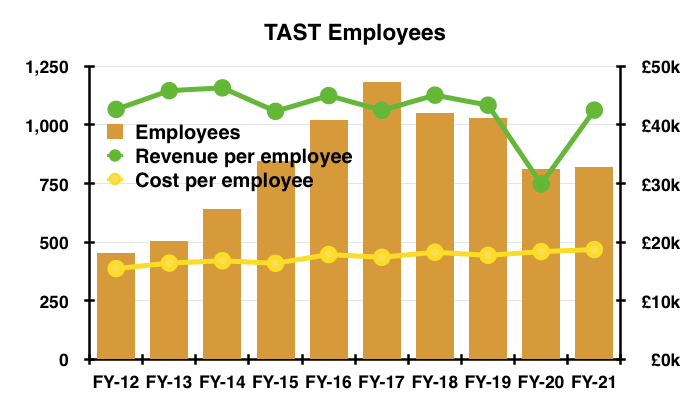

- Revenue of £42.5k from an average 821 employees was just about on a par with the £42k-£46k seen since FY 2011.

- Unlike previous years, TAST this time revealed the average number of staff employed during H2:

“The average number of persons, including Directors, employed by the Group during the period was 821 of which 805 were restaurant staff and 16 were head-office (2020 – 810 of which 796 were restaurant staff and 14 were head-office staff). The second-half of 2021 the average number of staff was 934.“

- Annualised revenue per employee was therefore a super £49.9k (£23.3m*2/934) during H2.

- That level of employee productivity may not be sustainable. TAST said its headcount was close to 1,000 but still 5% short of requirements:

“We are pleased to report that on 26 December 2021, we employed just under 1,000 people across the business: an increase of 330 from the previous year…

Like many competitors and other industries, we have been impacted by labour shortages and are currently 5% short of the full employment levels required.”

- Annualised H2 revenue from, say, 1,050 employees gives £44k per head to match the staff productivity witnessed prior to the pandemic.

- Underlining the staff shortages, 821 employees at 50 open restaurants during FY 2021 gives 16.4 employees per site, versus more than 17 for FY 2019 and earlier.

- The total cost per employee during FY 2021 inched higher to £18.7k, and is likely to rise further. TAST admitted:

“Targeted wage increases have been applied, which should help us retain our teams in the long-run. Since Brexit and the pandemic, we found that flexible working has helped to attract a different demographic. This change provides us with new opportunities as we grow our talent pool.

Financials: going concern, Barclays loan and new openings

- TAST’s prior-year FY 2020 results disclosed “the existence of a material uncertainty” within the ‘going concern’ text:

“However, the Directors note that the effects of Covid-19 and the impact of ongoing losses indicate the existence of a material uncertainty that may cast doubt over the Group’s ability to continue to apply the going concern basis of accounting.”

- But the ‘going concern’ text improved for the subsequent H1…

“The Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. In reaching this conclusion the Directors have considered the financial position of the Group, together with its forecasts for the next 12 months from the date of approval of these interim accounts and taking into account possible changes in trading performance should Government restrictions be reintroduced. The Group monitors cash balances closely to ensure there is sufficient liquidity. Accordingly, the Directors believe that it remains appropriate to prepare the financial statements on a going concern basis.“

- …and improved further for this FY by not referring to “Government restrictions” or “sufficient liquidity“:

“At the time of approving the financial statements, the Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. In reaching this conclusion the Directors have considered the financial position of the Group, together with its forecasts for the next 12 months and taking into account possible changes in trading performance. The going concern basis of accounting has, therefore, been adopted in preparing the financial statements.“

- Talk of a Company Voluntary Arrangement (CVA) looks to have ceased, too:

“Through the pragmatic approach and support of our landlords we have managed to avoid a formal procedure such as a company voluntary arrangement (“CVA”)“

- A post-results update during June provided further evidence that TAST no longer risks financial trouble.

- The June statement confirmed TAST had repaid an emergency £1.25m loan from Barclays that was taken on during the pandemic.

- News of the loan repayment was accompanied by resilient comments about the “prevailing economic uncertainties“:

“The Board believes that, with its current net cash and future cashflow, it will have sufficient funds to weather the prevailing economic uncertainties and cost pressures and also satisfy its measured expansion plans for a pipeline of up to five to six new units in 2022. The Board is progressing this strategy and has one new site under offer and is currently negotiating on three others.“

- The June update also reiterated plans to open five or six new restaurants.

- Mentioned initially with the March trading update and then reiterated within these FY 2021 results…

“We expect to facilitate a measured expansion plan for a pipeline of five to six new units, however, any expansion will be at a steady pace“

- …plans to open new outlets must surely confirm TAST’s management has moved from a ‘survival’ mindset to one of ‘recovery’.

- Mind you, these FY 2021 results did say a “pipeline of five to six new units“, while the subsequent June update said a “pipeline of up to five to six new units“.

- The “prevailing economic uncertainties” seem to have trimmed TAST’s expansion plans before the first pipeline site has even opened!

Financials: cash, cash flow and deferred payments

- TAST confirmed its £11m cash position was enhanced by deferring payments to various creditors:

“At 26 December 2021 cash at bank was £11.0m (2020: £8.0m). Net cash after outstanding bank loan [of £1.25m] at the balance sheet date was £9.8m (2020 – net cash £8.0m). The cash balance at year-end reflects our cash preservation strategy and deferring payments due to landlords, HMRC, and other trade creditors. After reflecting these outstanding payments, our net cash at year-end was approximately £6.8m.“

- Deferred payments were therefore £11.0m less £1.25m less £6.8m = £3.0m.

- Deferred payments were previously £4.4m for the preceding H1 and £6.5m for FY 2020, indicating £3.5m was repaid during this FY with £1.4m cleared during H2.

- The cash position increased by £3.0m during FY 2021, which excluding the Barclays loan (£1.3m), recognised government benefits (£3.9m) and repayment of deferred creditors (£3.5m) gives £3.0m less £1.3m less £3.9m plus £3.5m = a £1.3m inflow.

- A £1.3m underlying cash inflow feels somewhat reassuring in the circumstances given TAST spent three months during H1 selling only via takeaway and delivery.

- June’s update said net cash was £8.6m:

“The Company has now repaid the amount outstanding under the Facility of £1.1 million in full and has subsequently cancelled the Facility, leaving the Group with a net cash balance of approximately £8.6 million and no debt.”

- £8.6m is less than the £9.8m net cash position at the end of FY 2021.

- The lower cash position following the year-end is due presumably to TAST repaying all the money owed to its deferred creditors. After all, those deferred creditors would not be happy remaining out-of-pocket when TAST can now afford to open new sites.

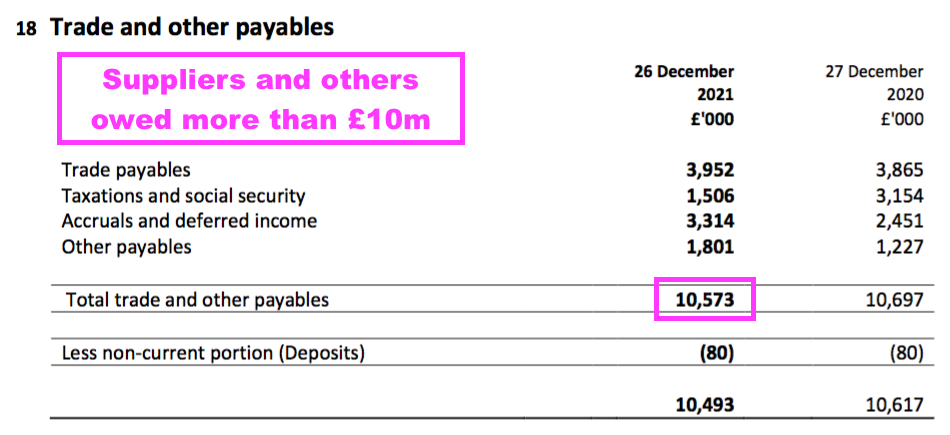

- Even if all the deferred creditors have been cleared, TAST’s £8.6m cash position is not truly surplus to requirements.

- The cash position is inherently a by-product of owing money to suppliers, with £10m-plus outstanding at the year-end suggesting approximately £7m was owed excluding deferred creditors:

Financials: landlords and leases

- This FY statement gave a short update on rent negotiations:

“The Group has successfully achieved consensual lease concessions and rent reductions for the lockdown period for most of the estate. There remain a few sites for which negotiations are ongoing… We are extremely grateful for all the assistance received.”

- The text differed slightly to that of the preceding H1…

“The Group has been successful in achieving rent reductions and lease concessions across most of the estate. Landlords have, in the main, been extremely understanding and supportive.”

- ...which did not mention “for the lockdown period“.

- And given the FY 2020 results referred to “March 2021“…

“The Group has now successfully achieved consensual lease concessions and rent reductions to March 2021 on more than two-thirds of the estate“

- …TAST therefore appears to be enjoying lower rents for a temporary period only.

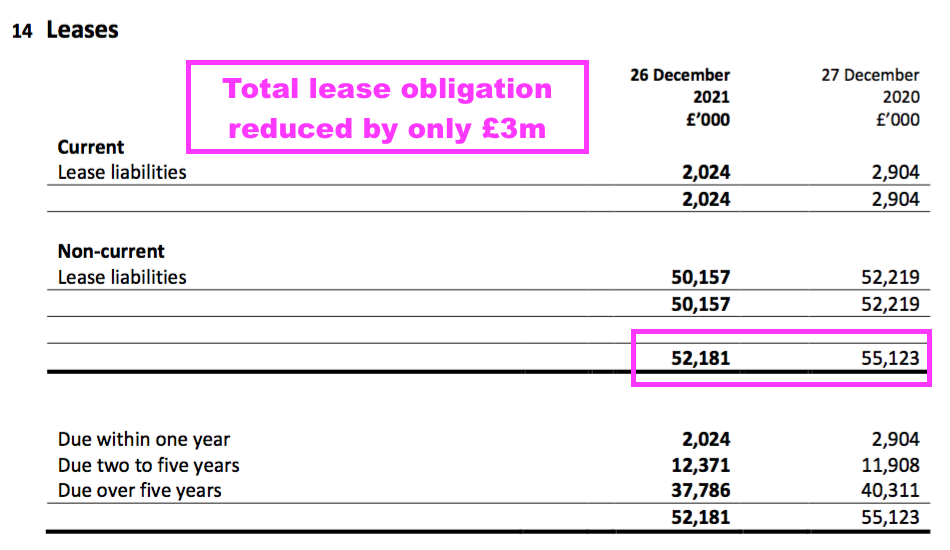

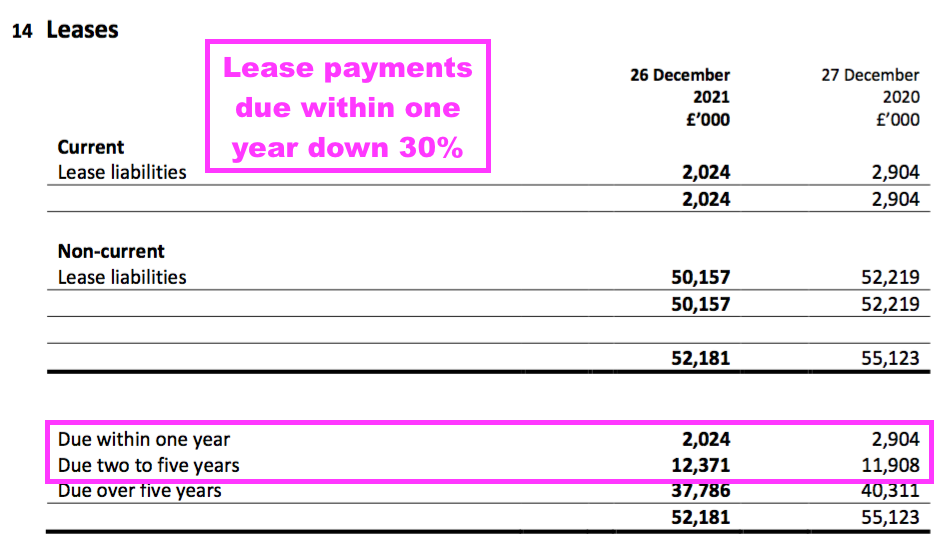

- Temporary lower rents may explain why TAST’s total lease obligations (on a net present value basis) reduced by just £3m to £52m during this FY:

- I had hoped TAST’s total lease obligations would be reduced by much more than £3m following some notable rent reductions.

- TAST commendably publishes pre- and post-IFRS 16 versions of its headline profit performance, from which rent payments can be deduced:

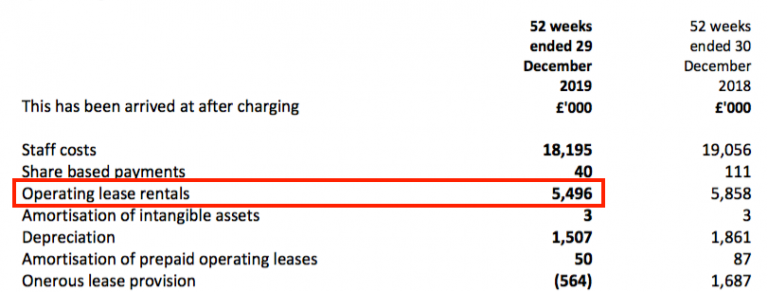

- The £4.0m difference between the FY 2021 Ebitda numbers represents the pre-IFRS 16 lease cost that, post-IFRS 16, is now reflected within the depreciation expense and financing charge.

- £4m compares to the pre-IFRS 16 lease cost of £5.5m for FY 2019:

- £4m versus £5.5m implies rent costs being cut by 27%.

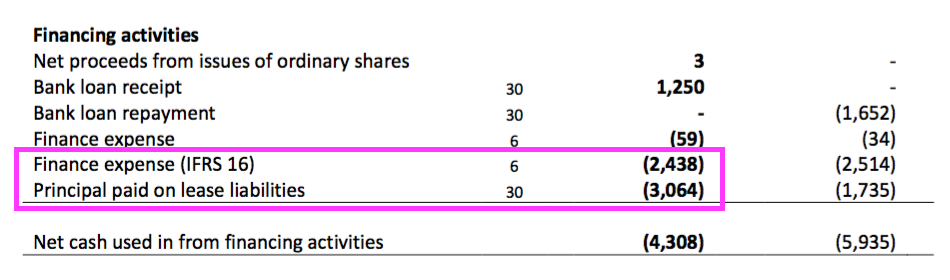

- Cash lease payments were £5.5m during this FY, which I presume exceeds the £4m pre-IFRS 16 lease cost because of TAST also repaying its deferred creditors (e.g. overdue rent):

- The accounting notes indicate rent payments for FY 2022 could be lower, but then increase slightly over the subsequent few years:

- This FY statement mentioned a possible “re-gearing” of leases for restaurants that remain closed:

“However, the Group will continue to consider selling two or three of those restaurants or re-gearing their leases to reflect current market conditions.”

- I presume “re-gearing” means asking landlords for rent reductions to make the sites viable.

- TAST’s right-of-use lease asset ended FY 2021 at £37m, which arguably suggests the group would pay £15m (£52m minus £37m) less to rent its properties were it to commence the same leases today.

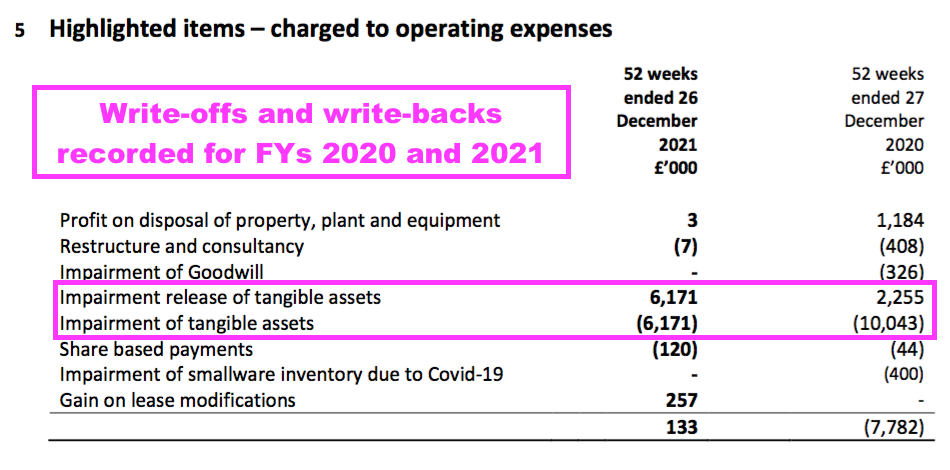

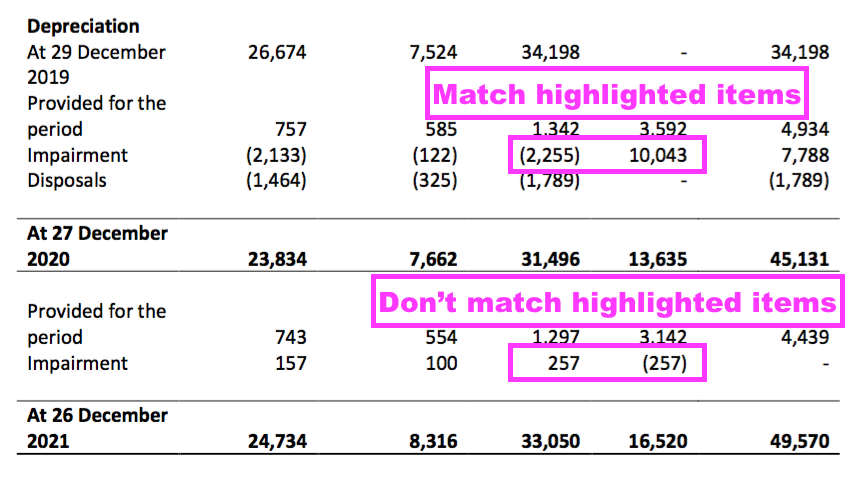

- TAST’s highlighted items showed a confusing pair of balancing £6,171k entries for the impairment and impairment release of tangible assets:

- Corresponding figures elsewhere in the accounts showed matching figures of £257k:

- At least the overall effect was no further asset write-offs which, alongside minimal other ‘highlighted’ expenses, now imply some sort of stability within the accounts.

Financials: cost analysis

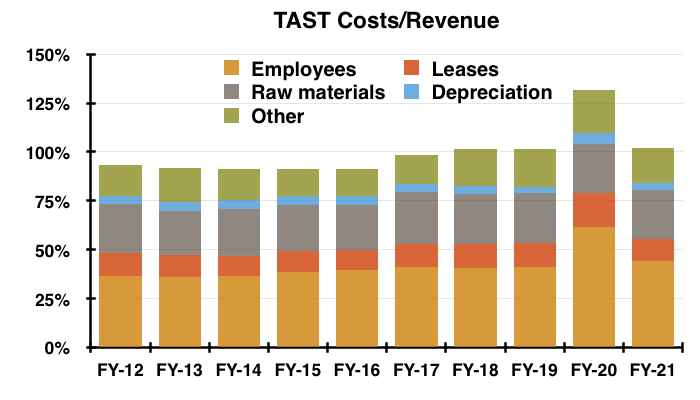

- Evaluating TAST’s past costs can help determine whether the business can emerge from the pandemic with stronger margins.

- What TAST described as “challenging” trading conditions led to minimal profits (or losses) during FYs 2017, 2018 and 2019 as total costs reached 100% (or more) of revenue:

- TAST kept lease costs under control before the pandemic at between 10% and 12% of revenue. They were an estimated 12% of revenue during FY 2021.

- Raw materials (essentially ingredients) were also kept reasonably steady at between 23% and 25% of revenue before the pandemic. They were 25% of revenue during FY 2021.

- In contrast, employee costs increased from 36% to 41% of revenue between FY 2012 to FY 2019. And my estimate for FY 2021 is 44%.

- TAST employs mostly lower-paid staff, and past increases to the minimum wage and the introduction of the national living wage seem to have caused staff costs to out-pace revenue.

- The wage omens are not great for FY 2022. TAST admitted:

“With the increase in National Insurance of 1.25%, National Living Wage and wage increases, there will inevitably be wage inflation, which will be impossible to completely absorb.“

- Other costs rising from 16% to 19% of revenue between FY 2012 and FY 2019 were another contributor to the pre-pandemic margin collapse.

- TAST hinted of “utility price volatility” increasing its other costs for FY 2022:

“2022 will not be without its challenges with labour shortages, food inflation, the ending of Government support in terms of reduced VAT and business rates and utility price volatility, impacting profitability.”

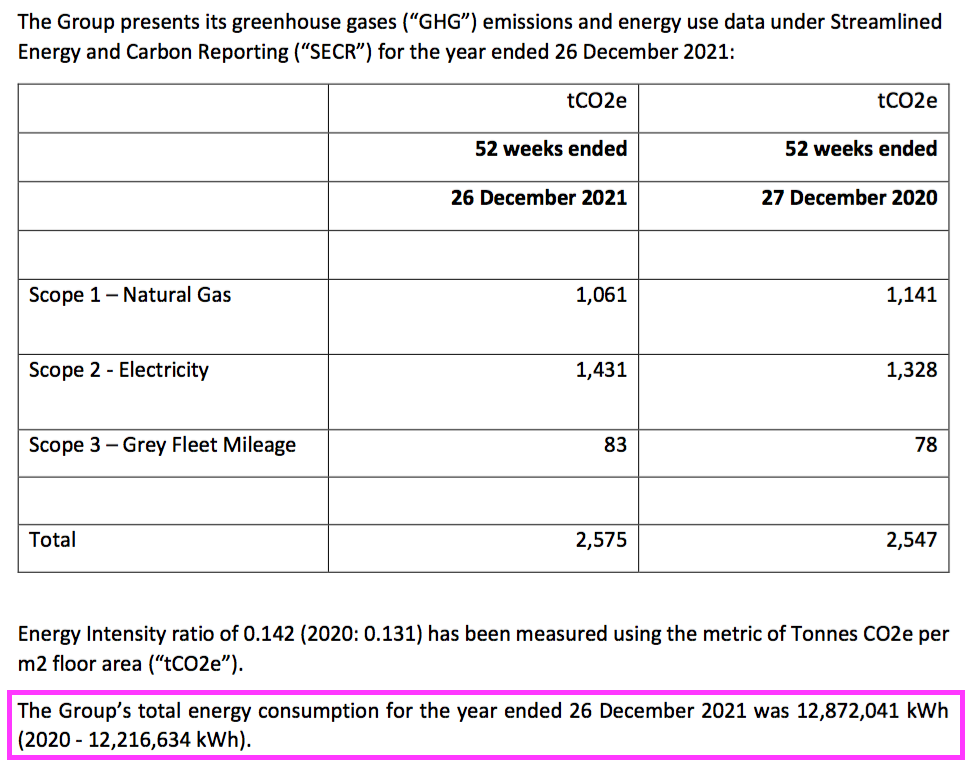

- The 2021 annual report showed TAST consuming a similar level of energy during FY 2021 to FY 2020:

- My rough sums earlier this year indicated the group may be liable to pay an extra £1m for gas and electricity. TAST also looked very energy inefficient versus fellow restaurant operator Fulham Shore.

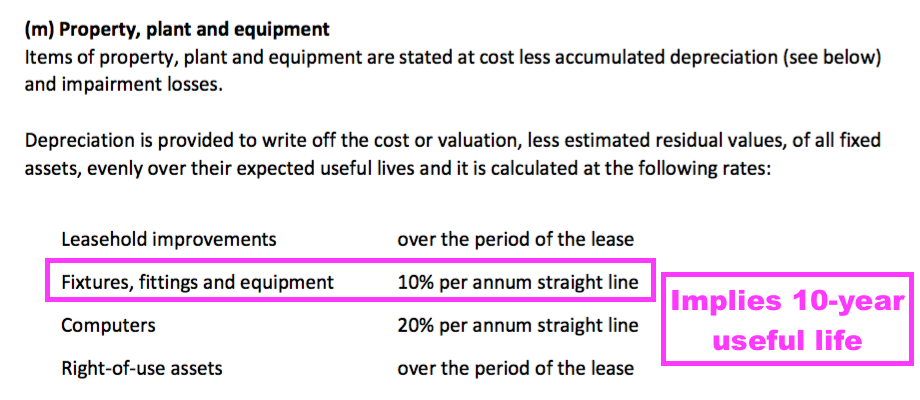

- Depreciation has bobbed around the 4-5% level of revenue for years and was 4% for FY 2021.

- But TAST’s depreciation policy does seem relatively generous with an effective ten-year useful life for fixtures, fitting and equipment:

- By way of comparison, both Restaurant Group and Fulham Shore depreciate their fixtures, fittings and equipment between three and ten years.

- True, TAST’s depreciation policy has not been too relevant of late as the group curtailed capex and instead raised money by selling leases:

| Year to c31 December | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit* (£k) | 1,101 | (478) | (542) | (2,279) | 3,429 |

| Depreciation** (£k) | 2,146 | 1,861 | 1,557 | 1,342 | 1,297 |

| Net capital expenditure (£k) | (5,777) | 2,889 | 55 | 1,919 | (541) |

| Change in working capital (£k) | (319) | (731) | 1,199 | 5,413 | (377) |

| Net cash/(debt) (£k) | (5,157) | (2,105) | 2,918 | 8,028 | 9,755 |

(*Including other income and excluding highlighted items **excluding IFRS16 depreciation)

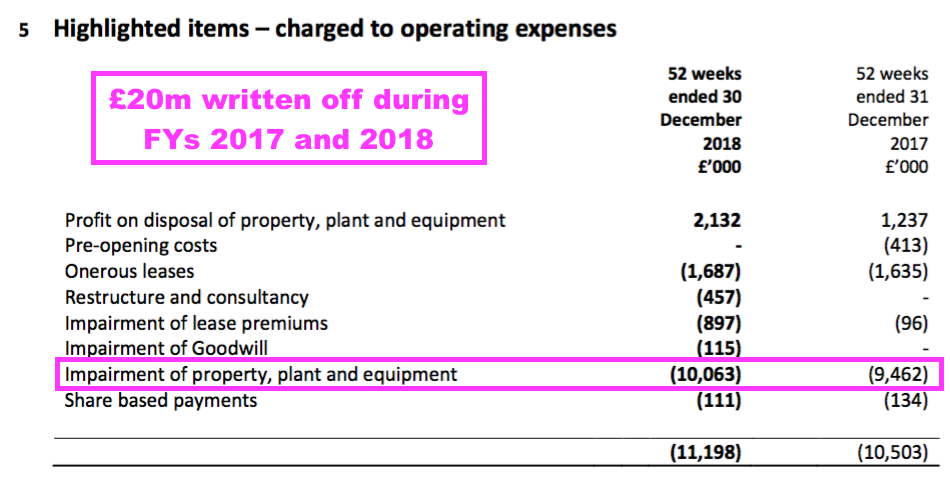

- But let’s not forget TAST’s operating troubles during FYs 2017 and 2018 led to write-offs of £20m before the pandemic:

- Those write-offs may not have been so hefty had a more conservative depreciation policy been applied. They also suggest earnings prior to FY 2017 were flattered somewhat.

- All told, these FY 2021 figures sadly do not suggest a radical change to TAST’s cost structure and profit margin any time soon.

- The major hope remains TAST’s growing delivery/takeaway services can somehow lead to improved revenue per restaurant and/or per employee without commensurate increases to overall costs.

Immediate prospects, board changes and revised menu

- TAST’s FY 2021 outlook expressed “cautious optimism” despite a long list of “challenges“:

“Trading prior to Christmas was strong and the start of 2021 is encouraging, but this must be tempered by the challenges which the Group expects following the end of Government support including VAT and business rates, the risk of a reduction in pent-up demand, disposable income and staycations as well as a steep rise in inflation in relation to wages, utilities and input supplier costs as the UK adjusts to Brexit, the aftermath of the pandemic and the current war in Ukraine. Accordingly, the Board views the future with cautious optimism.“

- I would like to think the aforementioned plan to open new restaurants signals a little bit more than “cautious” optimism.

- Changes to the board provide some confidence. The appointment of Harald Samúelsson as an executive during June was particularly notable.

- Mr Samúelsson has enjoyed a long and seemingly successful industry career:

“From 2000 to 2008, Harald helped grow Strada Restaurants from 4 to 54 restaurants in the UK in a senior operations position. In 2008, Harald joined Côte Restaurants as joint Managing Director, growing the group from 2 to 72 restaurants. In 2013, Harald co-led a management buy-out of Côte with CBPE Private Equity for £100m and in 2015 co-led a sale of Côte to BC Partners for £245m. During his Côte tenure, Harald was also joint Managing Director at Bill’s restaurants from 2010 to 2012. In 2016, Harald joined Honest Burgers as a Senior Advisor and set up a property development company in Spain with projects in the Valencia, Madrid and Barcelona areas.”

- This interview with The Caterer reveals how Mr Samúelsson’s career started “almost by accident after getting a part-time job in a local bar and restaurant“.

- The following quote from Mr Samúelsson during the interview feels reassuring for TAST shareholders:

“The main components of the business are the food and the service, so for us it is really looking at where can we provide the best service and the best-quality food possible and to see where we can exceed expectations on both fronts.

That is why it is so important we recruit the right people and train them, because we own the standards we exceed. We are very strict on the standards we expect from our staff.“

- Mr Samúelsson’s ‘front of house’ skills should complement the chief exec’s property background:

“Jonny is a graduate in Accounting & Finance who converted to Property, Valuation & Law at City University. He joined a London-based commercial surveying practice in 1991, qualified as a Chartered Surveyor in 1994 and for seven years was involved with valuation, general agency, and landlord and tenant matters“

- Mr Samúelsson spent a year as a TAST non-exec before his executive appointment, and choosing to become an executive would seem unlikely if TAST’s prospects were limited.

- And TAST must be doing well if it can afford another executive salary!

- The non-exec appointment of Wendy Dixon, a senior manager at marketing agency M&C Saatchi, could meanwhile help with TAST’s promotions.

- Whether Mr Samúelsson or even Mrs Dixon will chip in with menu ideas remains to be seen.

- The pandemic could have been an opportunity for a radical menu overhaul, but TAST’s primary Wildwood format remains based on a broad mix of pizzas, pastas and burgers.

- A broad mix of pizza, pastas and burgers did not attract

hoardshordes of diners during the “challenging” (pre-pandemic) FYs of 2017, 2018 and 2019.

- But pizzas, pastas and burgers might be very suitable for deliveries and takeaways, which could explain why such revenue improved faster than dine-in sales last year.

- The following 15 dishes featured on the Wildwood menu during January 2022 and remain on the latest version:

Starters

Mixed olives: were £3.25, now £3.95

Garlic tiger prawns: were £7.75, now £8.35

Minestrone soup: still £5.45

Grill

Vegan burger: was £12.50, now £13.25

Philly cheesecake sandwich: was £14.15, now £14.95

Full rack of ribs: was £17.95, now £18.95

Pizza

Margherita: was £9.10, now £7.95

Piccante carne: was £12.55, now £12.95

Grilled courgette & goat’s cheese: was £10.95, now £12.25

Pasta

Classic spaghetti pomodoro: was £8.95, now £7.95

Traditional Bolognese: was £10.75, now £11.75

Over-baked chicken and mushroom penne: was £12.75, now £12.95

Other

Chicken & asparagus risotto: still £12.95

Caesar salad: was £11.15, now £11.45

Fries: were £3.95, now £4.35

- Prices have been increased for most menu items since the start of the year, but a few have remained unchanged and at least two — the margherita pizza and the classic spaghetti pomodoro — have in fact had their prices reduced.

Valuation

- 54 restaurants operating normally and returning to FY 2018/2019 sales of £750k each would generate group revenue of £40m.

- Revenue of £40m does not require a huge operating margin to leave a profit that would make the £8m market cap appear remarkably cheap.

- A margin of 4% on £40m for example leads to a £1.6m operating profit and a possible P/E of less than 7.

- The obvious worry is the H2 2021 performance was exceptional and a host of macro-economic problems will soon dampen sales and lift costs to then restrict TAST to minimal profits at best.

- Although the statement during June appeared positive…

“The Board believes that, with its current net cash and future cashflow, it will have sufficient funds to weather the prevailing economic uncertainties and cost pressures and also satisfy its measured expansion plans for a pipeline of up to five to six new units in 2022.“

- …the text did not update on trading for H1 2022, which at the time had less than one week left to run.

- A really positive H1 performance would surely have merited some management remarks within that June statement.

- Note, too, that TAST signalled higher expenditure within these FY 2021 results:

“As we come out of the pandemic, we are gearing towards investment in our existing sites, new sites, people and development.”

- TAST has spent only £1m on capex during the last three years, and the entire restaurant estate could be due an overhaul that may eat into the cash position.

- Options awarded to the chief exec at the start of FY 2021 revealed what the board thought could be possible with the share price.

- The scheme pays out:

- 5.2 million shares if the share price has traded at a 90-day average of 6p by the start of FY 2022;

- A further 5.2 million shares if the share price has traded at a 90-day average of 8p by the start of FY 2023, and;

- A further 5.2 million shares if the share price has traded at a 90-day average of 16p by the start of FY 2025.

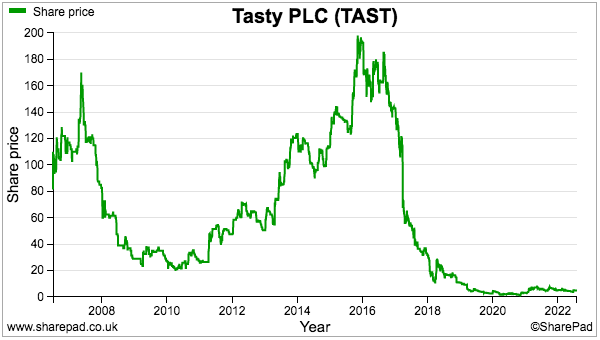

- The 16p target is tantalising given the recent 5.25p share price

- TAST has confirmed the 6p target was met earlier this year and the chief exec now owns 8.4% of the company.

- TAST does provide an investing dilemma.

- Yes, the shares could be very cheap and may well multi-bag should sales boom and margins recover.

- But the economics of TAST’s restaurants were not exactly superb before the pandemic and remain very unclear after the pandemic.

- And the main Wildwood chain seems unlikely to enjoy a lucrative long-term niche by sticking to a middle-of-the-road menu with middle-of-the-road pricing.

- Other shares could offer more dependable returns. At least three of my holdings presently yield 6% or more (here, here and here) and support greater conviction towards any additional investment.

- The over-riding risk with buying more TAST is becoming trapped in an illiquid share that, having survived the pandemic, slips back to its pre-pandemic ways and fails to earn suitable profits from new sites and estate revamps.

Maynard Paton

As usual, a superb analysis. Thank you, Maynard.

Malcolm

PS “Hordes”, not “hoards”!

Thanks Malcolm. My poor spelling now corrected!

Maynard

Tasty (TAST)

Publication of 2021 annual report

Here are the points of interest beyond those noted in the blog post above:

1) STRATEGIC REPORT

a) Principal risks and uncertainties

The principal risks remain Covid-19, Brexit, competition, people, food standards/safety and supply chain.

Various text changes were made for 2021, although nothing of significance.

Revised text for the Covid-19 risk confirms the avoidance of a CVA:

“We have avoided a more formal procedure such as a CVA as a result of the support of our landlords.”

Revised text for the Brexit risk indicates higher costs:

”Brexit has impacted food and drink primarily in the form of inflation and shortages. ”

Revamped text for the People risk suggests a greater focus on HR matters:

“We have continued to focus on selection, induction, training and retention of our employees. The Group has made significant improvements in its selection process, onboarding training programmes and career development paths. New HR and recruitment systems have been established and proposed to provide consistent and swift support to all colleagues. We have also strengthened our teams. The Group offers competitive remuneration and is reviewing its overall benefits package.”

2) REPORT OF THE DIRECTORS

a) Section 172 report

No changes for 2021.

b) Directors’ interest in shares

The chief exec’s shareholding changed materially after this annual report was published:

He now owns 8% following this RNS:

“The Company announces that in the period ending 15 January 2022, the 90 day VWAP of the Ordinary Shares exceeded 6 pence and accordingly the Company has received notice from Jonny Plant to convert 5,225,546 B Ordinary Shares (the “Vested B Shares”) into 5,225,546 new Ordinary Shares, representing 3.33% of the entire issued Ordinary Share capital at the date of the adoption of the Growth Shares Scheme.

Following Admission, Jonny Plant will hold an interest in the Company comprising 12,317,448 Ordinary Shares, representing 8.42% of the Ordinary Shares in issue, and a residual balance of 10,451,094 B Ordinary Shares, which remain subject to the terms of the Growth Shares Scheme.”

The chief exec has missed out converting further B shares into ordinary shares as the share price did not average 8p during the 90 days to 15 January 2023. The chief exec’s final chance for B share conversion is the share price averaging 16p during the 90 days to 15 January 2025.

The FD’s options vested in October as she completed three years of service. Not sure whether that timescale prompted a new FD, who was announced last week. The former FD had a rough time in office after being appointed in September 2019 — just six months before the pandemic. I suspect she had anticipated greater gains from her 3.25p options with the shares currently at 3.5p.

c) Environment

New for 2021 — no more plastic straws:

“We have stopped using plastic straws, committed to a policy recommended by the Humane League and currently looking at ways to reduce our carbon footprint.”

As mentioned in the blog post above, energy use during 2021 was very similar to that of 2020:

Given (I think) longer Covid-19 site closures during 2020 than 2021, TAST seems to have become more energy efficient. But a comparison with fellow restaurant chain Fulham Shore last year showed TAST was relatively extravagant with its energy usage.

3) CORPORATE GOVERNANCE

Lots of revised and new text explaining how TAST applies the QCA’s 10-principle corporate code:

a) Establish a strategy and business model…

TAST has apparently strengthened its operating model:

“Throughout the pandemic the Group has been quick to implement various measures to stabilise the business and safeguard and preserve the wellbeing of our people and customers. In response to the experience of the last two years we have strengthened our operating model.

b) Take into account wider stakeholder and social responsibilities…

All completely new text for Employees and Training and Development (including Christmas party details!), suggesting the workforce is becoming of greater importance to the group:

“Employees:

Since Brexit and the pandemic, we have seen a shift in the demographics of the team with an increasing number of younger team members. This change provides us with many opportunities as we grow our talent pool. We recognise that there are also challenges so we have established a safeguarding group and launched a confidential route to encourage anyone to report any concerns they may have. Whilst 2021 was challenging in terms of retention due to the pandemic and Brexit, more recent data suggests our team is more stable and there are encouraging signs that length of service is growing.

We have been able to reintroduce manager roadshows to make our wider team feel included in our business and to have time away from their restaurants to sample new recipes, network and chat to our Board members and senior leadership team. In March 2022 we will also reinstate the delayed post-Christmas party for head office, managers, and head chefs, providing a chance to get together and share the vision for Tasty.

We have reintroduced both online and face-to-face exit surveys to gather as much information as possible regarding how colleagues regard their experiences at Tasty. In 2022 we will also reintroduce engagement surveys, having taken a break due to the pandemic. The results will, again, support our planning and decision making.

A full pay and benefits review has been completed to make sure we continue to be seen as an attractive company to work for whilst remaining financially prudent.

Training and development:

We continually review and update “Flow”, our online learning platform, to make sure all modules are as effective and relevant as possible and the number of restaurants with 100% completion scores continues to grow.

In 2021 we began our ambitious leadership development programme and launched discrimination, recruitment, and onboarding training to our senior team.

Our restaurant managers are all focusing on delivering an exceptional customer experience and train their teams on a daily basis to achieve this. “Feeditback”, our sophisticated system for tracking customer experience across our estate, provides regular information to restaurants and this data is used to promote excellent service.

Having the in-house apprenticeship team has allowed us to become a centre for the British Institute of Innkeeping (“BIIAB”), so we can deliver accredited training and examinations within food safety, health and safety and licensing law, with further scope to offer this commercially and to add in additional courses.”

Plus useful employee stats within the gender pay disclosure: the balance of full-pay workers within the entire workforce (which may impact revenue per employee trends if the balance changes):

“Diversity:

For our Gender Pay Gap (“GPG”) figures for 2021, we reported on a smaller number of “full-pay relevant employees” (“FPE”) at 149 employees of the 707 “relevant employees” (“RE”). The FPE accounted for 21% of RE mainly due to the pandemic and many employees receiving furlough pay. Pre pandemic in 2019, we had 867 FPE. Even without the benefit of including the wider workforce, this measure is a valuable exercise for us.”

And more hints of rising costs:

“Suppliers:

We have built up a close relationship with most of our suppliers over a number of years and have a good understanding of our mutual business needs. We have worked with them to ensure shortages do not impact the business longer-term, however we are beginning to see inflationary impact. ”

c) Maintaining the board…

An amazing 23 board meetings were held during 2021:

”Board meetings were held monthly, with supplementary board meetings, as needed, in normal circumstances pre pandemic. In 2021 we held 23 board calls/meetings and in 2022 we plan to revert to monthly meetings. Almost all of the Board meetings were attended by the full Board. The Board is fully committed to Tasty plc and will contribute hours as required.”

d) Ensure that between them the Directors……

Not a great issue given TAST’s more pressing problems, but all directors standing for re-election every year is now best practice:

“The Company’s Articles of Association require that one-third of the Directors must retire and, if desired, may stand for re-election by shareholders annually in rotation;”

e) Maintain corporate governance structures…

New for 2021, a report from the audit committee:

The Committee has primary responsibility for ensuring that the financial performance of the Group is properly measured and reported on. The Committee receives and reviews reports from the Group’s management and auditor relating to the interim and annual accounts and the accounting and internal control systems in use throughout the Group. The Committee meets at least twice times a year at appropriate intervals in the financial reporting and audit cycle and otherwise as required. The Committee has unrestricted access to the Group’s auditor. The principal areas of focus during the year included the following items:

* review of the Annual Report and financial statements.

* approval of the management representation letter.

* review of the auditors fees and engagement letter. The Committee met with the external auditors to review their Audit Plan, their report and significant findings arising during the audit.

f) Communicate how the Group is governed…

New for 2021, a report from the remuneration committee:

Executive Directors’ Remuneration report

The Group’s remuneration policy is designed to provide competitive rewards for its Executive Directors, taking into account the performance of the Group and the individual Executives, together with comparisons to pay conditions in the sector in which the Group operates. The committee seeks to establish a basic salary for each Executive determined by individual responsibilities and performance, taking into account comparable salaries for similar positions in companies of a similar size and sector.

Basic Salary

Basic salaries are reviewed on an annual basis or following a significant change in responsibilities. The committee seeks to establish a basic salary for each Executive by references to individual responsibilities and performance, taking into account comparable salaries for similar positions in companies of a similar size and sector.

Incentive Shares

These are designed to reflect the Group’s share price performance, aligning participants interests with those of shareholders. Further details of the scheme are set out on page 66.

Benefits

The Executive Directors are entitled to a range of benefits, including contributions to individual personal pension plans, private medical insurance and reviewing life assurance.

Service Contracts and Notice Periods

The Executive Directors are employed on rolling contracts subject to three or six months’ notice. Service contracts do not provide explicitly for termination payments, but the Group may make payments in lieu of notice, being basic salary and other relevant emoluments for the notice period.

Non-Executive Directors

All Non-Executive Directors have a letter of appointment subject to three months’ notice. In the event of termination of their appointment they are not entitled to any compensation. Non-Executive Directors’ fees are determined by the Executive Directors having regard to the needs of the Group and comparative fees paid in the sector in which the Group operates. They are not eligible for pensions or other benefits.

Directors’ Emoluments

The remuneration of each Director is set on page 54.”

4) INDEPENDENT AUDITORS’ REPORT

A few points here, but nothing too untoward. Thankfully the report did not repeat the “material uncertainty” text from 2020.

a) Key audit matters

‘Revenue recognition’ and ‘recognition of Covid-19 grants’ are now included as key audit matters alongside ‘risk of impairment of plant, property and equipment and other assets’. The ‘transition to IFRS16’ matter for 2020 was understandably dropped for 2021.

Recognition of takeaway sales are apparently of higher risk:

“We performed specific testing on revenue recognised around the year end (“cut off” testing) to assess the risk that revenue had been recognised in the wrong periods, this testing included a review of revenue from takeaway orders which was considered to be a higher risk.”

Impairment calculations could do with further fine-tuning:

“We reviewed the financial statement disclosures and recommended that additional sensitivities were included.”

I noted in the blog post above that TAST had written off £20m of assets prior to the pandemic, and I do wonder if TAST’s implied 10-year useful life of fixtures, fittings and equipment is prudent.

b) Materiality and scope

Can’t recall a company ever referring to draft operating profit before:

“The materiality for the Group financial statements as a whole was set at £220,000 (29 December 2020 – £200,000). This was determined as being 7.5% of draft operating profit before highlighted items.”

£220k equalling 7.5% of draft operating profit means total draft operating profit before highlighted items was £2,933k.

But the reported operating profit before highlighted items was £3,549k, so perhaps TAST was very conservative when drawing up its draft figures. Note, most company auditors tend to use 5% of pre-tax profit for materiality purposes.

Scope was 100%:

“Audit work to respond to the assessed risks was performed directly by the audit engagement team who performed full scope audit procedures on the Parent Company and the Group as a whole.”

5) ACCOUNTING POLICIES

No huge changes for 2021, with a lot less text about ‘going concern’ and IFRS 16 this year.

a) Going concern

Now includes talk of “encouraging trade” for early 2022 but also uncertainty over customers “holidaying abroad“:

“Since dine-in reopened in May 2021, trading until December 2021 was highly encouraging. Following the Government’s advice in December and the spread of the Omicron variant impacted Christmas sales, December was weaker than we anticipated. Trade for the start of 2022 is encouraging.”

“The Group monitors cash balances and prepares regular forecasts, which are reviewed by the Board. These forecasts include our best estimates and judgements based on currently available information and current environment. Judgement is particularly required as to the impact on trade of the restrictions being eased as this will also mean that many more people will be holidaying abroad.“

b) Covid-19 related rent concessions

New text for 2021, although I am not sure how this modification accounting works:

“IFRS 16 defines a lease modification as a change in the scope of a lease, or the consideration for a lease, that was not part of the original terms and conditions of the lease. The Group has considered the Covid-19 related rent concessions and applied the lease modifications accounting.”

c) Share-based payments

Text revamped and now refers to the Monte-Carlo model, due to the chief exec’s grant of the aforementioned B shares (see point 2b):

“The cost of this is measured by reference to the fair value at the date on which they are granted. The fair value is determined by using an appropriate pricing model (e.g. binomial or Monte Carlo model).”

6) HIGHLIGHTED ITEMS

As per the blog post above, I am still not sure what is going on here:

The matching £6,171k write-off and write-back of tangible assets for 2021 seems very odd. Not a typo it seems, as the text underneath says:

“This net impairment movement is £nil, however for some sites there was an impairment charge of £6.2m and for other sites a release of £6.2m. ”

7) EMPLOYEES

Confirmation of the employee details mentioned in the blog post above:

TAST commendably discloses restaurant staff and head-office staff details, which in turn can fine-tune employee productivity ratios.

So, revenue per restaurant employee for 2021 was £43.4k, versus £30.4k for 2020 and between £42k and £47k for 2010-2019.

Restaurant staff per restaurant was 14.9 for 2021, versus 14.3 for 2020 and at least 16.6 for 2019 and earlier. Meanwhile the cost of restaurant staff versus revenue was 41% for 2021, versus 57% for 2020 and 39% for 2019, 36% for 2015 and 33% for 2011.

Staff numbers per site may be skewed by a changing mix of part-time/full-time staff and outlet closures/re-openings following the pandemic. But a definite trend is growing staff costs versus revenue, which I suspect will not ease anytime soon given broader labour trends.

8) DIRECTOR PAY

No complaints here:

Basic executive wages at £135k seem reasonable given TAST’s position. Presumably the new FD and new exec Mr Samuelsson will be paid something similar.

9) PROPERTY, PLANT AND EQUIPMENT AND RIGHT OF USE ASSETS

I am still none the wiser why this note shows counter-balancing £257k entries when other parts of the accounts show counter-balancing £6,171k entries (point 6):

The text below reiterates the £257k entries:

“During the 52 weeks ended 26 December 2021, the Group recognised an impairment charge of £nil (2020: £7.8m) due to impairment of ROU assets £0.26m (2020: £10.0m) and release on fixed assets £0.26m (2020: £2.2m). ”

Note how only small changes to the discount rate can create significant impairment write-offs and write-backs:

“The impairment movement is due to the reassessment by each individual CGU following a change in performance and/or change in assets. The impairment calculation is sensitive to changes in the assumptions and estimates used. For example a 1% decrease in the discount rate would result in a release of the net impairment by £1.2m, an increase of 1% would result in an impairment charge of £1.2m and a 1% growth rate would result in a release of the impairment charge by £0.5m.”

10) INVENTORIES

No issues here:

Raw materials and consumable inventory expenditure of £8.6m represented 25% of revenue versus 23%-27% since 2012.

Market cap at 3.5p per share is approximately £5m, and stock valued at £2m puts the valuation into some perspective.

11) TRADE AND OTHER RECEIVABLES

No issues here:

All numbers are small versus 2021 revenue of £34m.

12) TRADE AND OTHER PAYABLES

As mentioned in the blog post above, the £10m-plus owed to suppliers and similar underpins the net cash position:

Payments postponed to creditors (HMRC, landlords etc) due to the pandemic were £3m at the year-end and will be included in the £10m-plus total above.

13) PROVISIONS

A small note that confirms £297k is expected to be spent repairing leasehold properties before they are returned to the landlord (‘dilapidations’):

The £38k utilisation meant £38k was spent on dilapidations during 2021 that had been charged to the income statement during a prior year.

14) BORROWINGS

All academic now as the £1.25m was repaid during June

15 LEASES

This note shows TAST’s income from the properties it sub-lets:

Looks like TAST will collect £290k a year for just over 11 years.

16) SHARE-BASED PAYMENTS

Confirmation that TAST’s options are dominated by the 15,677k B shares issued to the chief exec (point 2b):

Less the 5,226k B shares since converted into ordinary shares, total options/B shares are 10,451k or c7% of the share count. The 3,265k options other than the chief exec’s B shares have a c4p exercise price, so dilution from them is not imminent given the 3.5p share price.

17) RELATED PARTY TRANSACTIONS

These all relate to properties let to TAST by members of the Kaye family, who have since departed the board hence the lower levels of monies involved:

No RPTs should occur for 2022.

Maynard