02 June 2022

By Maynard Paton

Results summary for Mincon (MCON):

- A better-than-expected performance, bolstered by a record H2 and perhaps a cracking Q4 following less pandemic disruption.

- Positive progress was recorded at all three product divisions, with higher commodity prices pushing H2 mining sales up 30%.

- Encouraging development news included the long-awaited Greenhammer system delivering “outstanding” test results and potentially becoming available to purchase this year.

- Despite the long-term commitment to first-class product manufacturing, MCON’s financials sadly still lack signs of an obvious ‘moat’.

- The shares do not appear outrageously expensive, assuming H2 extrapolations and upbeat FY 2022 trading do indeed support a 15x P/E. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own MCON

- Results summary

- Revenue, profit and dividend

- Product divisions

- Greenhammer and other development projects

- Financials: Margin

- Financials: Stock

- Financials: Return on equity and revenue per employee

- Financials: Cash flow

- Valuation

News links, share data and disclosure

News: Annual results and presentation for the twelve months to 31 December 2021 published 14 March 2022 and Q1 trading update published 09 May 2022

Share price: 100p

Shares count: 212,472,413

Market capitalisation: £212m

Disclosure: Maynard owns shares in Mincon. This blog post contains SharePad affiliate links.

Why I own MCON

- Designs and manufactures industrial drills, with sales supported by established reputation, engineering excellence, product patents and technical innovation.

- Boasts veteran family management with 45-year tenure, 56%/£120m shareholding and long-term perspective.

- Offers higher earnings potential through supplying a buoyant mining sector, greater direct sales, prospects of larger construction contracts plus “transformational” new products.

Further reading: My MCON Buy report | All my MCON posts | MCON website

Results summary

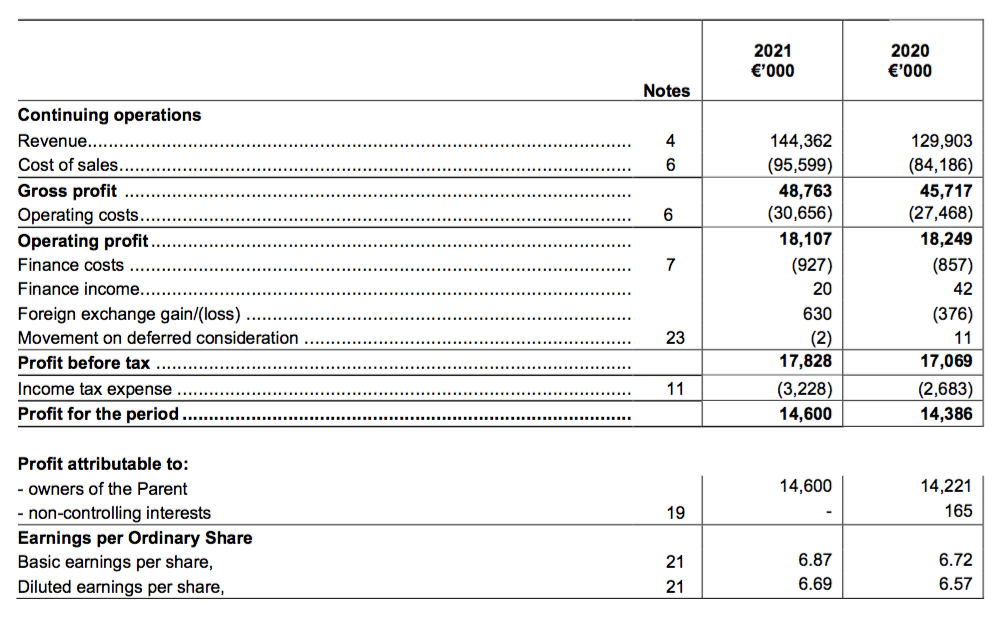

Revenue, profit and dividend

- These FY 2021 figures were better than I had expected following the pandemic-disrupted H1.

- The H1 2021 statement had revealed revenue up 4% and operating profit down 9%.

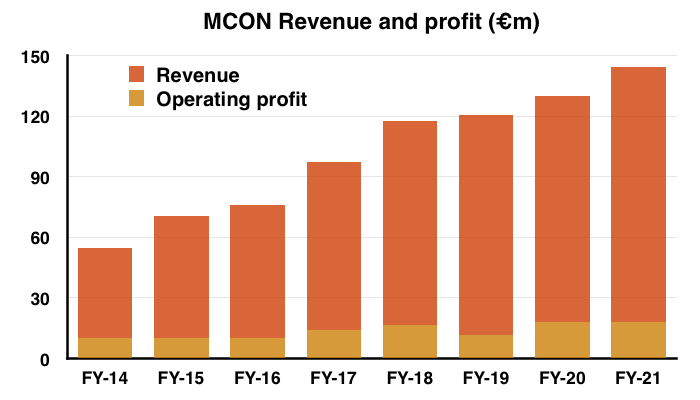

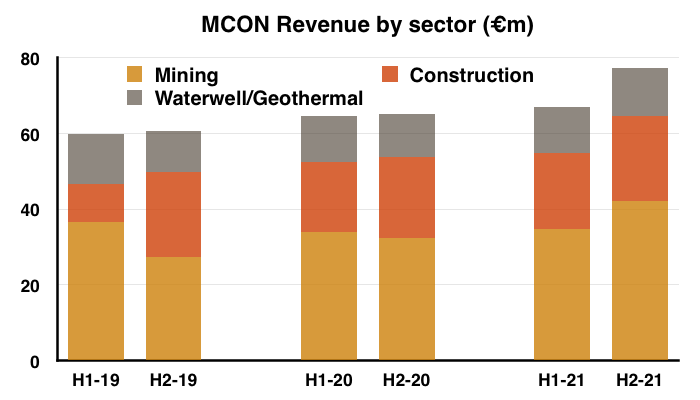

- But these annual numbers implied a much stronger H2, showing full-year revenue up 11% (to €144m) and operating profit down 1% (to €18m):

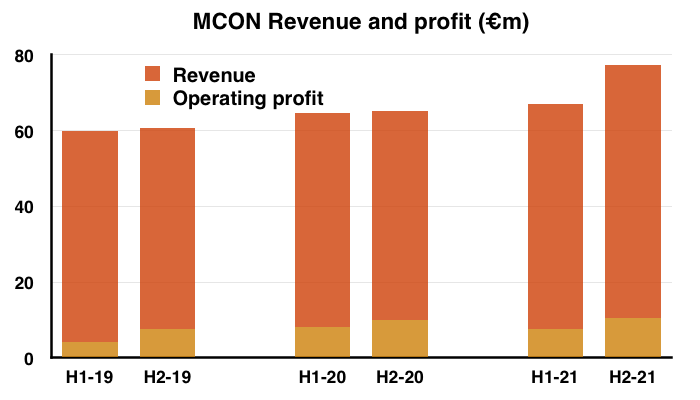

- Revenue in fact registered a new yearly peak, while H2 was MCON’s best ever six-month performance for revenue and profit.

- H2 revenue surged 19% to €77m and lifted H2 operating profit by 6% to beyond €10m:

- November’s Q3 update disclosed revenue advanced 6% during the first nine months of the year, which implied MCON enjoyed a cracking Q4 given full-year revenue gained 11%.

- The bulk of FY21’s progress was organic, with full-year revenue growth due to acquisitions limited to 3%.

- While MCON blamed the earlier H1 profit shortfall on pandemic interruptions…

“At the beginning of the year, including all of January and most of February, we experienced interruption in our manufacturing in some of our plants due to the pandemic. The largest impact was at our hammer factory in Shannon. Our capacity in the Shannon plant was severely disrupted, with a 35% reduced manufacturing workforce during those initial months of this year.”

- …this FY 2021 statement said simply “the production challenges imposed by the COVID-19 pandemic” had “eased“.

- Profit growth lagged revenue growth due to ongoing logistical headaches and rising supply costs:

“Supply chain challenges and increases in raw material prices had an impact on our margins during the year, along with additional operational costs brought about by the on-going pandemic. For instance, our overall manufacturing freight cost increased by 18%.”

- MCON suggested customers had shared some of the extra-cost burden…

“We have passed on price increases to customers to offset increases in manufacturing and delivery costs, but only when it was considered appropriate to do so.“

- …and would continue to share the burden during 2022:

“Our order books for 2022 remain healthy as the markets remain strong. We are passing on inflationary manufacturing cost, such as increases in energy cost, through price increases to customers.“

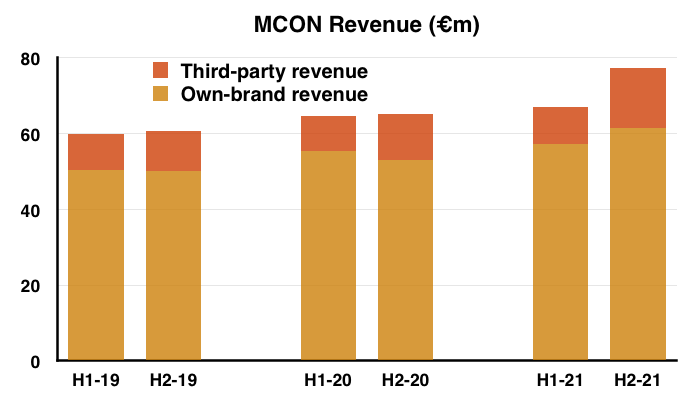

- The logistical headaches forced MCON to sell greater volumes of third-party equipment:

“We were also compelled to purchase local non-Mincon products to fulfil our customer requirements when Mincon manufactured products were subject to freight interruptions at seaports, and this also impacted our gross margin in 2021.“

- Sales of third-party equipment jumped 20% during the year and 30% during H2:

- Sales of MCON’s own-brand equipment gained 11% during the year and represented 82% of total revenue — the lowest proportion since FY 2017 (77%).

- Selling third-party equipment helps MCON satisfy a wider range of customer orders, but incurs much lower margins then selling own-brand products.

- The profit performance was distorted slightly by pandemic-related grants:

“The Group recognised €450,000 in Government Grants in 2021 (2020: €1.3 million). These grants differ in structure from country to country, they primarily relate to personnel costs.“

- Exclude the grants and FY 2021 operating profit climbed 4%.

- Reported profit could also be fine-tuned for capitalised R&D spend without an associated amortisation charge (see Greenhammer and other development projects).

- The logistical headaches prompted greater levels of stock…

“[W]e chose to increase inventory levels of both raw materials and finished goods to ensure we maintain continued strong service to our customers who use our products for business-critical operations.”

- …and the elevated stock level continues to raise questions about MCON’s inherent economics and the reinvestment requirements to deliver higher earnings.

- Indeed, the logistical headaches and rising costs have done nothing to alleviate the continuing absence of indisputable ‘moat’-like financials.

- All told, MCON’s dedication to top-class manufacturing and supplying premium equipment was not obviously apparent within these FY 2021 financials — nor indeed within the results of the previous five years (see Financials: Margin).

- The final dividend was set at 1.05 eurocents a share and gave a full-year payout that matched the 2.10 eurocent distributions for FYs 2018, 2019 and 2020.

Product divisions

- All three of MCON’s product divisions enjoyed positive full-year progress.

- Higher commodity prices prompted MCON’s traditional mining customers to purchase more equipment:

“The mining industry continued with its robust performance from 2020 into 2021 as the price of precious metals remained high throughout the year, along with a strong annual average iron ore price for 2021. Our revenue expansion in the mining industry was particularly encouraging, with organic growth of 16%”

- Mining revenue surged 30% during H2 to €42m and represented 55% of total revenue.

- Note that full-year mining revenue could have expanded even further were divisional sales in Australia not trimmed 6% by pandemic restrictions.

- After a 10% advance during H1, construction revenue climbed 5% during H2.

- Construction progress throughout the year was supported by smaller European projects (revenue up 23%) that counterbalanced lower income from larger American projects (revenue down 12%).

- MCON encouragingly suggested greater construction orders could be forthcoming during FY 2022:

“Although it was quieter in 2021, the construction sector continues to provide excellent growth potential for the Group, and we have tendered for a number of major geotechnical projects, mainly in the United States. We fully expect to be awarded some of these contracts, which, as we saw in 2020, significantly boost our revenue and profit performance.”

- MCON’s construction division was effectively formed during FY 2017 following the purchase of Finnish operator PPV.

- Since then further acquisitions and new products such as the Spiral Flush have helped construction revenue grow to represent approximately 30% of group sales:

- Revenue from waterwell and geothermal equipment gained 11% during H2 and 5% for the year.

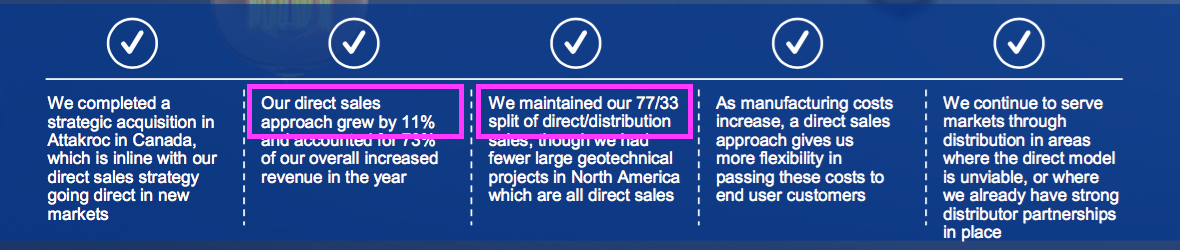

- Three years ago MCON embarked on selling equipment direct to its end customers rather than through intermediaries:

“We are differentiating ourselves from the less developed businesses in low margin activities in the sector, and we are positioning ourselves to deal directly with end customers and to win large contracts.”

“Going forward we plan to… seek long-term partnerships and multi-year contracts with end customers incorporating direct delivery to their sites.”

- The FY 2020 statement was the first to reveal the extent of direct sales at 77%.

- The FY 2021 slides confirmed the split remained at 77%:

- Direct sales should benefit MCON by:

- Cutting out the intermediary margin, and;

- Providing greater insight into future customer requirements.

- MCON noted direct sales also provide greater flexibility for lifting prices and passing on elevated costs to customers.

Greenhammer and other development projects

- This FY 2021 statement revealed good progress on new projects.

- Testing on the Greenhammer system has finally taken place and delivered “outstanding results“:

“Our hydraulic Greenhammer ran successfully on our own Mincon rig at a major open pit iron ore mine in north-western Australia during the year. Stringent COVID-19 restrictions in Western Australia materially curtailed our ability to put the outstanding results, in terms of penetration rate increases and reliability, to commercial use.

- MCON also claimed Greenhammer was a “transformational opportunity“:

“As a result, and subject to pandemic restrictions easing in Western Australia, we are working on alternative routes to commercialising this transformational opportunity for the Group and the hard rock surface mining industry. It is important to note that protecting our hard-earned IP will be at the forefront of any agreements that we commit to.”

- To recap, the FY 2018 statement described this new hydraulic drilling system as…

“[A] disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base”.

- …and suggested the design could enjoy a strong competitive advantage:

“This is not a small system or easily replicable, and we have placed patents around the system to protect it. The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.”

- The project appears to have commenced eleven years ago. It was first mentioned within the FY 2016 results while the FY 2018 results said development had started seven years beforehand.

- Although the original plan to commercialise Greenhammer within western Australia has faltered due to the pandemic, MCON appeared positive the system could be sold later this year:

“We are currently examining potential routes to commerciality with other clients, and subject to the lifting of COVID-19 restrictions, we expect that [Greenhammer] will start generating revenue in 2022.“

- My question to management about Greenhammer’s potential at the (online) 2021 AGM elicited the following (paraphrased) response:

“Greenhammer could produce significant incremental profitability and there remains a very big market opportunity for other MCON products.”

- MCON capitalised Greenhammer development costs of €1.1m during FY 2021, of which £0.7m occurred during H2. Total capitalised development expenditure since FY 2016 has been €7.0m:

- Not a eurocent of that €7.0m expenditure has to date been charged against earnings. Amortisation will commence when the system enters commercial use.

- The €7.0m expense represents 8% of the €89m aggregate operating profit before exceptional items reported since the capitalisation began during FY 2016.

- Meanwhile in Malaysia, customer testing of MCON’s “large diameter hammer system” occurred during H2 and set a new drilling record:

“Another testing success was the drilling that was carried out in Malaysia with our new large diameter hammer system to drill 1750mm diameter rock socket friction piles. We believe that these are the largest holes ever drilled with a single hammer.“

- MCON was upbeat about the prospects of this large-diameter system:

“While we need to drill more metres using the system, the performance, which is several times faster than the existing technology, gives us great encouragement. We believe that there is great potential for this product globally as the preferred method for drilling large diameter construction piles more efficiently.“

- Elsewhere within the research pipeline, MCON’s involvement in robotic seabed drilling very much remains in the early stages:

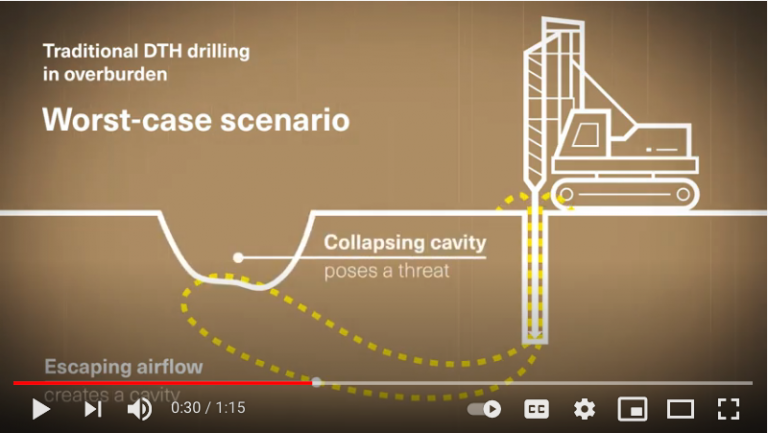

“A small-scale prototype has been test drilled onsite at the Shannon plant and we are continuing to refine this. We are also working with our partners to develop a seabed drill rig as part of an overall system to drill, load test and certify anchor installations at an offshore test site.“

- This video has more:

Financials: Margin

- I bought MCON shares during 2015 partly because of the company’s then attractive margin:

“[H]igh margins underpin the notion that MCON has a respectable competitive advantage. The group converted 19% of revenues into profit during 2014 and above 20% during 2011, 2012 and 2013.”

- This time last year I wrote:

“A 14% margin is reasonable, but not overwhelming evidence of a competitive ‘moat’ and customers having few viable alternatives.”

- The aforementioned logistical headaches and rising costs ensured MCON went another year without overwhelming evidence of a ‘moat’-type margin. The operating margin for FY 2021 was in fact 12.5%.

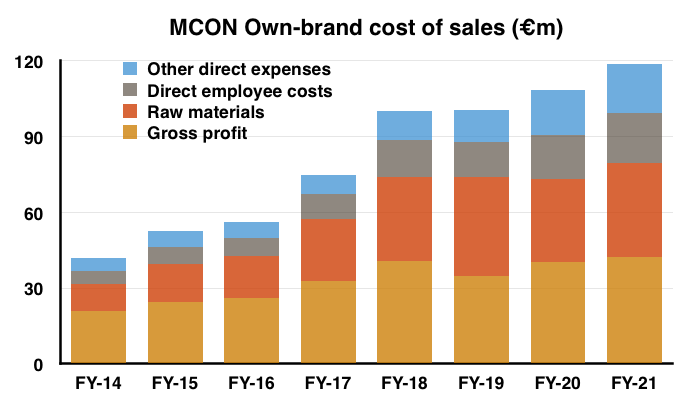

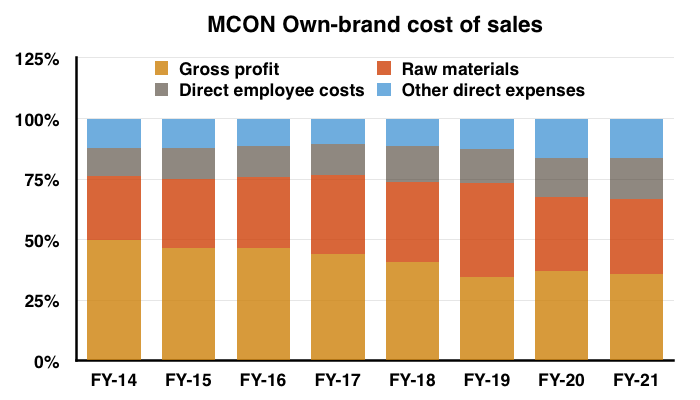

- MCON’s long-term margin decrease has been caused by the greater cost of sales for own-brand equipment:

- Raw materials and direct employee costs have represented a growing part of own-brand revenue since FY 2014 (from a combined 38% to 48%):

- I estimate the gross margin on own-brand equipment has dropped from 50% to 36%.

- My question to management about MCON’s operating margin at the (online) 2021 AGM elicited the following (paraphrased) response:

“The 20% margin of the past was achieved on much lower revenue when the company was manufacturing only part of the drill string and the more profitable DTH [down-the-hole] drills represented a greater part of the business.

Today the company manufacturers the full drill string, and as such has been able to win large direct contracts and therefore increase profit. That said, 14% is not our level of ambition.”

- In other words, MCON has evolved from operating as a niche, high-margin drill supplier with perhaps modest growth prospects to a wider, middle-margin drill supplier with possibly better growth prospects.

- Margins could of course improve as and when rising supply costs are passed on to customers.

- But a sub-15% operating margin since FY 2015 is not really commensurate with MCON’s focus on tip-top engineering and the annual report citing:

- Highest design specifications;

- Best manufacturing methods and processes, and;

- Delivery of superior products to our customers.

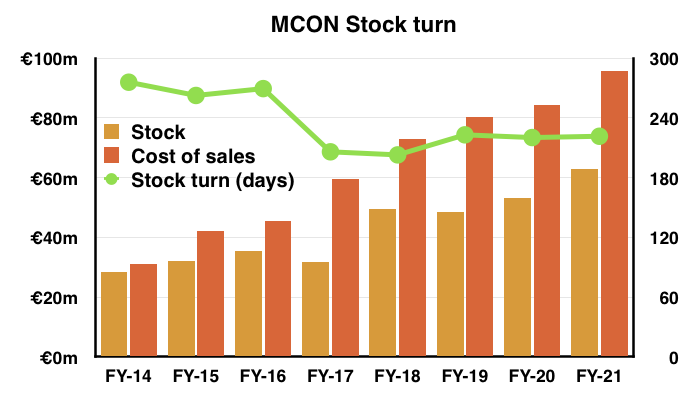

Financials: Stock

- The aforementioned logistical headaches prompted greater levels of stock:

“[W]e chose to increase inventory levels of both raw materials and finished goods to ensure we maintain continued strong service to our customers who use our products for business-critical operations.”

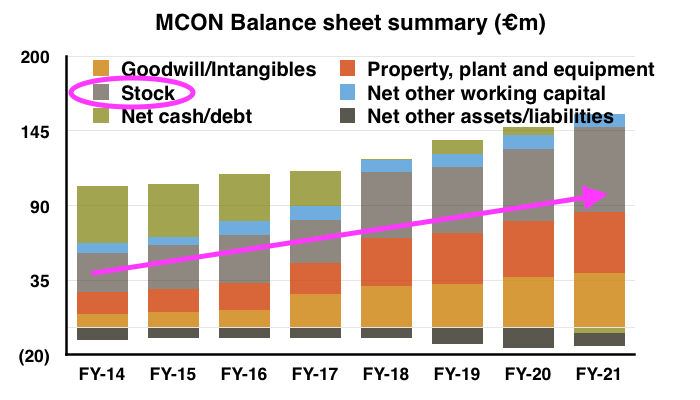

- Significant levels of stock have long been an unfortunate feature of MCON’s balance sheet.

- Stock has grown from 30% (€28m) to represent 44% (€63m) of net asset value between FYs 2014 and 2021:

- All my other portfolio companies operate with stock levels representing less than 20% of their balance sheets.

- Carrying large amounts of stock could mean a company:

- Manufacturers slow-moving items that carry a greater risk of obsolescence;

- Applies inefficient working practices, and/or;

- Will require greater cash investment into extra stock to support future growth.

- High stock levels appear a fundamental part of MCON’s business.

- In particular, the shift towards direct selling has required extra warehouses to support local customers:

“Our continued direct sales approach, particularly in North America, required new sales and warehouse locations. Through these locations we increased our market share and footprint in North America.“

- Customers demand “timely availability” of equipment, too:

“The sourcing of raw material and the lead times on delivery were key challenges for our factories to overcome in 2021. To help mitigate those challenges we decided to invest further in our raw material inventory, which increased our holdings by 6%, on a constant currency basis, to ensure supply of all required material types and sizes. A shortage of a particular raw material could delay the completion of finished product and hence reduce the timely availability of products to customers which could endanger future supply contracts.“

- MCON’s mining customers presumably operate in remote locations and can’t afford staff to idly wait for new equipment. Hence the requirement for MCON to operate local warehouses with plenty of stock.

- At least MCON’s stock is not perishable and write-downs for the last two years have been small:

“The Group recorded an impairment of €22,000 against inventory to take account of net realisable value during the year ended 31 December 2021 (2020: €80,000). Write-downs are included in cost of sales.“

- Stock turn has improved over time but remains lengthy. My calculation of average stock employed during the year divided by cost of sales gives 220 days (7-8 months):

Financials: Cash flow

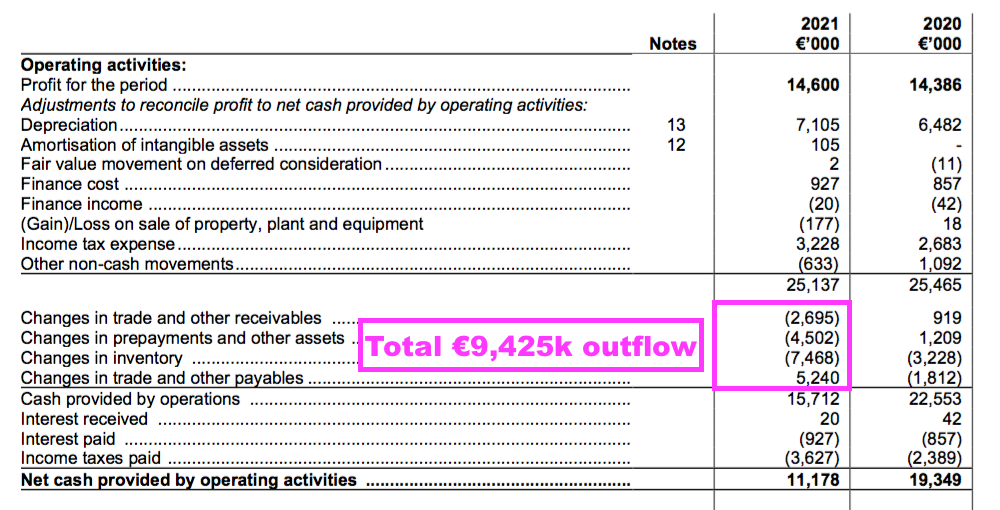

- The extra stock investment did not help MCON’s cash conversion. Some €7.5m was spent boosting stock during the year, split €4.2m for H1 and €3.3m for H2.

- Cash invested into working capital came to a net €9.4m, including €4.5m funding prepayments for manufacturing equipment:

- Cash absorbed into working capital during the last five years totals a material €30m:

| Year to 31 December | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit (€k) | 14,040 | 16,352 | 11,810 | 18,249 | 18,107 |

| Depreciation* (€k) | 3,014 | 3,896 | 3,898 | 4,666 | 5,209 |

| Net capital expenditure** (€k) | (5,639) | (12,552) | (7,930) | (6,981) | (7,024) |

| Working-capital movements (€k) | (4,408) | (14,870) | 2,095 | (2,912) | (9,425) |

| Free cash flow (€k) | 3,270 | (11,118) | 3,175 | 11,393 | 3,015 |

| Net cash (€k) | 26,142 | 846 | 5,586 | 461 | (4,342) |

(*excludes IFRS 16 depreciation **excludes Greenhammer expenditure)

- Five-year expenditure on tangible assets beyond the depreciation charged against earnings meanwhile stands at €19m.

- Factor in the €7m spent on Greenhammer, a net €23m spent on acquisitions and €22m spent on dividends, and no wonder net cash has reduced from €35m at FY 2016 to net borrowings currently at €4m.

- Total gross bank loans/finance leases stand at €34m and do not appear too alarming versus cash of €19m, FY 2021 earnings of approximately €15m and my calculation of an effective 3.3% borrowing rate.

- But operating with net debt is never ideal and as the pandemic showed, companies with cash set aside for a rainy day stand more chance of sustaining dividends and avoiding rights issues when unfavourable events occur.

- The prospect of material capital expenditure seems likely for the near term. MCON said:

“Our intention is to invest further in new and improved manufacturing techniques to increase efficiencies in our manufacturing processes, as the business continues to grow.”

- A small acquisition conducted after the year end suggests MCON’s strategy of purchasing new subsidiaries — a dozen or so have been acquired since the 2013 flotation — will absorb future cash as well.

- Another consideration is the €4.2m payable to clear earn-outs from past acquisitions.

- At least MCON’s accounts are not complicated by pension obligations.

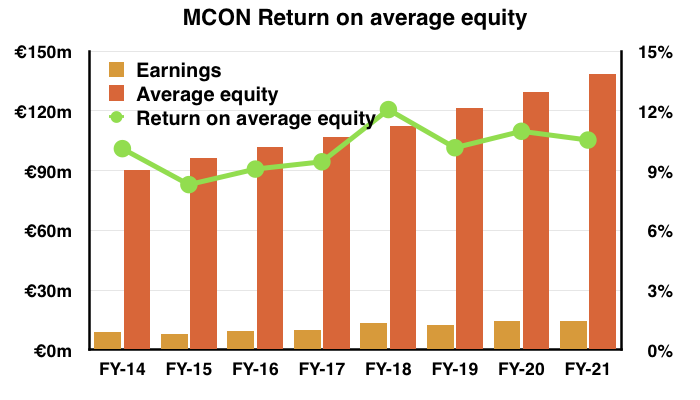

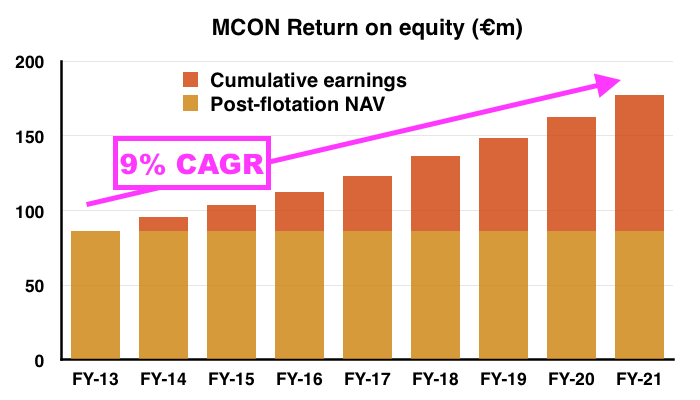

Financials: Return on equity and revenue per employee

- MCON’s modest margins and hefty cash expenditure have translated into return on equity numbers of approximately 10%:

- The 10% calculation is underpinned by evaluating MCON’s progress following the group’s 2013 flotation.

- When MCON became a public company, shareholder equity was €86m and net cash was flush from the flotation proceeds at €49m.

- Subsequent reported earnings have totalled €91m:

- Effectively investing €86m to earn an aggregate €91m over eight years equates to a 9% annual average compound return.

- Earning 9% a year on shareholders’ equity is not awful but is not exceptional either.

- For perspective, the same eight-year calculation for fellow portfolio member Andrews Sykes is 17% (based on an aggregate £109m earned from a £43m starting equity base).

- Perhaps one day Greenhammer, the large-diameter drills and/or the seabed micro-piling will all attract customers prepared to pay premium prices for advanced equipment, which in turn lifts equity returns to more respectable levels.

- Revenue per employee does provide hope that MCON is an above-average business. During the eight years since the flotation, revenue per employee has averaged a useful €259k and was €243k during FY 2021.

- My rule of thumb with revenue per employee is anything beyond £200k might indicate the employees develop higher-value products that could sustain a competitive ‘moat’.

- I hope MCON’s revenue per employee can improve over time to reflect customer price increases and new product launches.

Valuation

- A Q1 update issued during May did not read that badly.

- Revenue looks to have encouragingly held up following the record H2:

“We have carried the positive revenue momentum from H2 2021 into the first quarter of 2022, while continuing to build on our order books during this quarter, driven by the strong underlying demand for our products across the Construction, Mining and Waterwell/Geothermal sectors.”

…

“We are experiencing significant growth in our three industries versus Q1 2021. The majority of this is organic growth in both mining and construction, and through the acquisition of Attakroc in mid-2021, which has been a solid contributor to the Group and has grown our market share in Eastern Canada.“

- But costs remain stubbornly high:

“Whilst we have experienced margin pressure during the quarter due to the lag in recovering increases in manufacturing and operational costs through price increases to customers, we expect to recover our margin position in the coming months.”

“Substantial increased energy costs have been a main driver behind our margin pressure and trying to mitigate the effect of these is paramount.”

- MCON’s shares could be reasonably valued assuming the record H2 is sustained during FY 2022.

- Doubling up the €10.6m H2 operating profit gives €21.2m, which after the average 16% tax applied during the last five years leaves earnings of €15.1m or 7.1p per share with GBP:EUR at 1.18.

- Adjusting the £212m market cap for cash of €19m, debt and finance leases of €34m and the deferred consideration of €4m gives an enterprise value of £229m, or 108p per share.

- Dividing that 108p per share by my 7.1p per share earnings guess then gives a possible P/E of 15x.

- While the sums could be fine-tuned for the Greenhammer expense and other items, my rudimental rating does not appear bargain cheap nor outrageously expensive.

- For now I am hopeful a mix of:

- An easing of supply-chain headaches following the pandemic;

- Further demand in the mining and construction sectors;

- Greater direct sales of equipment, and;

- Greenhammer and other development projects bearing fruit…

- …can lead to respectable financial progress during the next few years.

- Longer-term investment success will depend upon management’s commitment to product quality one day translating into accounting evidence of a competitive ‘moat’.

- For now at least, MCON’s margin, return on equity and cash conversion sadly do not indicate an obvious ‘moat’.

- Shareholder patience could be required before superior returns are enjoyed.

- After all, MCON was established during 1977 and very much remains a family-run business with a corresponding long-term perspective.

- MCON’s founder still works as a company non-exec in his mid-80s while his two sons are the lead executives. The family members own a collective 56%/£120m shareholding.

- No family member sold a share at the 2013 flotation and none has sold a share thereafter.

- The lack of family share-dealing indicates MCON’s stewards are in for the long haul, and great change is unlikely to happen overnight.

- As financial signs of an obvious moat are awaited, the trailing 2.1 eurocents, or 1.8p, per share dividend supports a modest 1.8% income (before Irish withholding taxes for UK-resident investors).

Maynard Paton

Mincon (MCON)

Publication of 2021 annual report

Here are the points of interest:

1) CHAIRMAN’S STATEMENT

As usual the chairman’s statement from the annual report was not included within the original results RNS. A few useful snippets:

a) Reiterating product innovation

MCON’s ongoing ambition to become the market leader:

“At Mincon, we pride ourselves on our engineering excellence and we are always striving to deliver improved performance with lower energy input in all our products.

I believe that the excitement of working for a company that is committed to developing new innovative tools for our customers is a significant factor in retaining excellent people, as is the confidence that our senior management will continue to deliver on the Group’s mission to be “The Driller’s Choice”. There is great pride in working for a company where its technical ambitions and abilities are continually demonstrated across the globe.”

b) Large-diameter system drilling

Could be “transformational” for construction work in locations such as Hong Kong:

“One of our most recent innovations has been the large diameter, down the hole hammer. This was recently successfully tested on a pile-boring project in Malaysia. With a drilled hole diameter of 1,750mm, we believe they are the largest diameter holes ever drilled with a single down the hole hammer system. It has achieved penetration rates that are a multiple of times faster than those achieved with existing methods. With sustained productivity rates at these levels, this system can be transformational for the large diameter piling industry, especially in areas of high building density, such as Hong Kong.”

c) ESG

No annual report is complete these days without an ESG mention:

“As can be seen in our product development programme, we continue to focus on our Environmental, Social and Governance (“ESG”) performance. The nature of our research and development programme for new drilling tool applications concentrates on reducing energy input while increasing operating efficiency.

We will complete a detailed review of our ESG performance with recommendations for improvement in the first half of 2022.”

MCON’s ESG reporting in this annual report was not that informative.

2) CHIEF EXECUTIVE OFFICER’S REVIEW

a) Latest acquisition

The chief exec’s report contained a few extra lines not included within the original RNS, with the following about the latest purchase being the most informative:

“In January 2022, we completed the acquisition of Spartan Drill Tools, based in Fruita Colorado, which produces high quality drill pipes and related products. This strategic acquisition introduces this capability into the Americas region to further strengthen our full package offering for the mining, construction, and waterwell/geothermal markets. An important aspect of this deal is that we can integrate certain aspects of drill pipe manufacturing with available capacity and skillsets that we already have in Benton to leverage more efficiencies and hence improve our margins.”

b) Greenhammer test results

The chief exec in the annual report used the adjective “revolutionary” rather than “outstanding“:

“Our hydraulic Greenhammer ran successfully on our own Mincon rig at a major open pit iron ore mine in north- western Australia. Stringent COVID-19 restrictions in Western Australia curtailed our ability to put the revolutionary results, in terms of penetration rate increases and reliability, to commercial use.“

3) CHIEF FINANCIAL OFFICER’S REVIEW

The CFO’s review was as usual not included within the original results RNS. Extra text included:

a) Currency effects on revenue

Not significant:

“The Group revenue grew by 11% in 2021 (10% on a constant currency basis), 8% organically and 3% through acquisitions.”

b) Waterwell/geothermal

I was not aware MCON enjoys a “dominant position” in what is a “mature” European geothermal market:

“The majority of our waterwell/geothermal revenue was earned in Europe through the sale of our products for geothermal drilling and casing. We have a mature business in the European geothermal industry given our dominant market position. We are focused on new revenue opportunities in new geographical markets through acquisitions or start-ups to increase revenue in this industry. During 2021 we had growth of 5% in this industry and this was all achieved through acquisition. ”

c) Product mix

Ah, the 20% increase to third-party revenue was actually mostly due to an acquisition, rather than MCON being “compelled to purchase local non-Mincon products” as I implied in the blog post above:

“The change in mix of Mincon and non-Mincon product sales year on year was mostly due to the acquisition of Attakroc, this company sells a much larger proportion of non-Mincon products.

d) Pandemic impact

A reiteration of earlier pandemic disruption:

“The COVID-19 pandemic had a direct impact on our manufacturing in January and February 2021. Up to 35% of our Shannon – based manufacturing employees were absent due to the pandemic restrictions at the worst point during that period. This reduced manufactured output volumes from this plant and lowered the gross margin as fixed overheads do not reduce accordingly. We also experienced similar pandemic related issues in our other plants, but to a lesser degree. ”

e) Freight costs

Up 18%:

“We used additional air freight when sea freight timings were unfavourable. We also incurred a full year sea freight price increase that was introduced in 2020. As a result, our overall manufacturing freight cost increased by 18%. ”

f) Direct sales and extra costs

The direct-sales model incurs extra costs:

“We expanded the Group operational footprint in the Americas through the opening of new sales centres as we continued to develop our direct sales approach in the region. This increased employee costs and rent, and as a result impacted our operational profit for the year. As those new sales centres develop more local business, we expect to achieve improved returns on this investment in the coming years. ”

g) Stock turn

Confirmation of an unchanged stock turn calculation:

“To ensure that the supply of products to our customers is on time and is available in the appropriate locations, and to ensure that our factories have a suitable level of raw material, we decided to invest further in our inventory during 2021. However, our inventory in terms of months on hand remained relatively flat compared with 2020.

h) A cracking Q4

Seems like MCON did enjoy a busy Q4:

“Our debtors increased by €2.9 million (on a constant currency basis and excluding acquisitions) during the year. The high level of turnover achieved during the final months of the year pushed our debtors days ahead of the prior year end by 8%.

i) Capex

A snippet on where the capex was spent:

“We invested a net €6.8 million in capital equipment into the business in 2021, through this investment and the prior year investment we increased the capacity of our manufacturing plants. The standout investments for 2021 were the commissioning of a new PVA furnace in our carbide business in the UK, and a total refurbishment of our factory in Australia.

j) Normal trading?

I am not entirely convinced about this, but the text suggests cost increases may subside as the pandemic eases:

“The year presented challenges in increased costs, raw material shortages and extended freight times due to the pandemic, but we expect a more normal trading environment as the effects of the pandemic begins to ease.”

4) BUSINESS MODEL AND STRATEGY

a) Competitive advantage

A repeat of previous-year text about the group’s ‘moat’:

“The Group’s overall strategic objective is to develop long term sustainable competitive advantage with our products and services for customers, for the benefit of our shareholders and all stakeholders.

…

We are committed to:

* innovative engineering and industry leading quality

* the creation of new drilling products and technologies and associated intellectual property, supported, inter alia, by patents

* industry leading field service delivery, and

* improving the skill sets of our teams.”

b) Organic growth

A repeat of previous-year text about organic growth:

“We continue to look for opportunities to increase our geographical footprint and the vertical integration of supply lines where they add strategic value for the Group and add margin. However, in the immediate years ahead the company will focus more closely on organic growth of existing products in the regions that we service, and on bringing new drilling technologies, currently in development, to the market.

5) PRINCIPAL RISKS AND UNCERTAINTIES

a) Customer concentration

Top ten customers represented 28% of revenue (versus 27% for FY20):

“During 2021, the Group’s top ten customers have accounted for approximately 28% of its revenues.

b) Climate change

A new risk for this annual report:

“The Group is at risk from climate change. This is demonstrated in ways such as pollution, access to resources which can effect supply chain, raw material prices, changes to local laws and regulations, increases in taxes and local tariffs. If the Group does not seek new methods of manufacturing to reduce our carbon footprint, or continue to resource raw materials from ethical supply chain, the Group risk to climate change will increase. The ongoing projects the Group is directly involved in relation to climate change can be viewed on our corporate website at corporate.mincon.com/esg/ environmental-governance/”

c) Cyber risk

Another new risk for this annual report:

“Cyber fraud is an increasing risks as the business relies more on online systems, this is inclusive of our manufacturing software systems, customer service systems and banking systems. The security and processes around the Group’s IT and banking systems are subject to review by subsidiary management, regional management and Group management.

Mincon has adopted the appropriate controls and procedures to mitigate the risks detailed above. The Group has recruited experienced management with the necessary skills and experience to manage and alleviate risk where possible.

The Group management report to the Audit Committee annually with a detailed risk report, including all possible risks to the Group. This report covers, but is not limited to, level of acceptable risk to ensure that risk awareness is set at an appropriate level and mitigating factors around these risks. This enables execution of the Group’s business strategy as outlined above while the comfort of mitigating the Group’s overall risk exposure. ”

6) DIRECTORS’ REPORT

a) KPI reviews

A new snippet for this year, indicating the directors do monitor working-capital levels:

“The Director’s review KPI’s for Operating Profit, Inventory and Debtors throughout the year.”

b) Going concern

No mention of Covid-19 this year. Instead the text refers to borrowings:

“The Group availed of the option to enter into overdraft facilities and to draw down loans of €15.2 million during 2021. Mincon Group has loans and borrowings totalling €34.5 million as at 31 December 2021, of which €11.2 million is recognised as current, as detailed in note 18 to the financial statements. The low level of total debt as a percentage of total assets and the availability of funds if required gives the directors comfort that there are minimal Going Concern indicators as at 31 December 2021.

The directors have also taken account of the financial outlook to 31 March 2023 which included reviewing the Group’s cash flow forecast. The directors separately considered the Fair Value less Cost to Sell (FVLCS) impairment assessment highlighted in note 12 of the financial statements which did not indicate an impairment issue. This compounded with the Groups cash forecast review indicates the appropriateness of the Director’s opinion on adopting the Going Concern basis of accounting.”

7) CORPORATE GOVERNANCE

There were no signifiant changes from the prior-year text.

a) Board evaluation

A review took place and recommendations were made, but those recommendations were not disclosed:

“The Board engaged an external party to conduct a performance review of the Board and its committees in 2021. The main recommendations arising from the review were prioritised to be actioned during 2021/2022. The Board will have another independent review carried out in 2023. ”

8) AUDIT COMMITTEE

Just the one signifiant change from the prior-year text.

a) Whistleblowing arrangements

Absent this year was last year’s whistleblowing text:

“The Group has an independent and confidential whistleblowing policy which allows employees through an anonymous submission to raise concerns regarding all aspects of the business. The Committee ensures that arrangements are in place for a proportionate, independent investigation and appropriate follow up of such matters.

The Committee and the Board reviewed the Group’s whistleblowing policy during the year to ensure that it meets the needs of the Group, in particular as the business continues to grow and expand.”

But MCON looks to have maintained a whistleblowing policy, as elsewhere in the report is this text repeated from last year:

“Our whistleblowing policy exists to enable all staff across our Group to feel confident that they can expose wrongdoing without any risk to themselves. Mincon will not tolerate malpractice and attaches extreme importance to identifying and remedying any issues in relation to corruption or bribery.”

9) NOMINATIONS COMMITTEE

a) Board diversity and search for a new non-executive director

The board is now looking for a new non-exec. Ideally female, not Irish and from the renewable-energy sector:

“The Committee agreed to recruit another independent non- executive board member. The candidate would ideally be non-Irish and female, satisfying both gender and geographical diversity criteria. They should also have experience and knowledge of the renewable energy sector as the Committee agreed that this sector was one which was likely to be a significant growth market for the Group in coming years. The Committee obtained the services of a recruitment firm to locate a suitable candidate and are in the process of finalising a visit to Group headquarters in Shannon for their preferred candidate once the Covid-19 situation permits.”

Note how renewables could be a “significant growth market“.

b) ESG

An ESG review is due in next year’s annual report:

“The Committee discussed the Groups ESG performance as disclosed in our latest annual report. The Committee informed management that ESG reporting in the annual report could be strengthened and improved upon. As a result it’s the Group’s intention to complete a detailed review of our ESG performance with recommendations for improvement in the first half of 2022, and thus will be detailed in the 2022 annual report.”

I noted earlier this year MCON did not provide a CESR review.

c) Term limits for non-executive directors

Seems as if non-execs could serve up to 10 years, which is one year longer than the standard 9-year corporate-code maximum:

“The Committee discussed proposed term limits for non- executive directors, and it was agreed that a normal term of 7 years followed by an additional potential term of up to 3 years with Board approval should be the appropriate limits. The Board approved this proposal from the Committee.”

I would like to think founder Patrick Purcell will remain a non-exec for as long as he wants!

d) Succession planning

Last year’s text on succession planning was not repeated this year:

“During the year, the Nomination Committee reviewed Senior Management’s succession plan to ensure that the Company has the appropriate level of skills and diversity. The plan was completed for all critical roles in place, and this will be maintained on an ongoing basis. This allows Mincon Group to proactively plan and react to any senior management changes, help retain critical talent in the organisation, protect and sustain our financial targets and ensure the optimal foundation for future business expansion.”

The board has been relatively stable to date and the executives — both in their 50s — may not be thinking about retiring just yet.

10) REMUNERATION COMMITTEE

No major changes to the text and just three meetings during the year.

a) Bonuses

Still capped at 50% of salary, with an ongoing eye on stock and debtor levels:

“The Committee agreed a short-term incentive program for the 2021 financial year, in line with the 2020 scheme, through which the senior management team could earn up to 50% of their salary based on:

* The achievement of budgeted profit after tax for the year (up to 40% of salary)

* The delivery of targeted number of weeks’ inventory being carried at the end of the year (up to 7.5% of salary)

* The delivery of a targeted number of debtors days (up to 2.5% of salary)”

MCON has awarded executive bonuses only for this year and last, with the bonus for this year at c32% of salary (see below).

b) Director pay

Executive salaries were held for FY 2021, with bonuses trimmed a little:

Executive pay seems under control. The chief exec has collected c€300k through salary, bonuses and benefits every year since FY 2017. The payments do not feel outrageous given the €18m level of operating profit.

Founder Patrick Purcell now collects €55k after waiving his fees for FY 2020 and collecting €30k for FY 2019.

11) CORPORATE RESPONSIBILITIES

a) Corporate environmental responsibilities

All new text for this year signalling the company going ‘green’:

“At Mincon, we strive to be a responsible global business, which includes actions to reduce our impact on the environment.

Our Group goal is to achieve net zero emissions by 2040 – one decade ahead of the 2050 deadline for EU member states to achieve carbon neutrality.

Energy efficiency is the core focus of our engineering efforts. As such, we’re also motivated to reduce the energy requirements – and related emissions – associated with the manufacturing of our products. Our engineering ethos complements our environmental approach, and as such our efficiently manufactured drilling solutions will continue delivering energy savings when in our customers’ hands.

Our corporate environmental responsibility goals will be achieved by implementing guidelines set out in the Greenhouse Gas (GHG) protocol – a group-wide effort that will span all areas of our operations.

For our full environmental statement, emissions reduction plan, and related updates, please visit: corporate.mincon.com/esg/environmental”

b) Corporate social responsibility

All new (commendable) text for this year:

“Mincon has always been an active member of the communities in which it which it does business.

Originally founded in 1977, as a family-run business, our core values today continue to build on that heritage. This includes:

* Creating opportunities for those in need

* Making a positive impact on society

* Leaving a better world for the next generation

In addition to the Group-funded CSR activities, all Mincon businesses participate in programmes that bene t their local communities, such as;

* Equality: We are removing social obstacles for young girls to attend school in developing communities

* Water: We will be providing essential needs for schools such as clean water

* Education: We will be providing internet access for rural schools

* Community: We have been working with charities to give back to local communities around the world

* Environment: Offering waste-management systems and education and schools.

For our full CSR statement, social programmes, and updates, please visit: corporate.mincon.com/esg/social-responsibility.”

12) INDEPENDENT AUDITOR’S REPORT)

a) Materiality

A standard 5% of pre-tax profit:

“The materiality for the Group financial statements as a whole was set at €0.8 million (2020: €0.8 million). This has been calculated using a benchmark of Group profit before taxation, from continuing operations (of which it represents 5% (2020: 5%))…”

b) Scope

Not great disclosure. Best practice is to disclose the percentage of group revenue, profit and assets subject to full-scope audits.

“Of the Group’s 42 (2020: 43) reporting components, we subjected 11 (2020: 11) to full scope audits for Group purposes. An additional 3 components (2020: 2) were subjected to account balance testing in order to provide sufficient coverage over the Group’s key financial statement lines.”

c) Key audit matters

Unchanged from the previous year — revenue recognition and valuation of intangible assets/goodwill.

13) SIGNIFICANT ACCOUNTING PRINCIPLES, ACCOUNTING ESTIMATES AND JUDGEMENTS

a) Revenue recognition

New clarification of service revenue recognition.

“Where the Group provides a service to a customer, who also purchases Mincon manufactured product from the Group, the revenue associated with this service is separately identified in a set period (typically one month) and is recognised in the Group’s revenue as it occurs.”

14) COST OF SALES AND OPERATING EXPENSES

Disclosure that freight costs jumped 21% and energy costs surged 35%:

Plus admin costs up 42%:

15) EMPLOYEES

No great changes to employee productivity:

As mentioned in the blog post above revenue per employee was €243k versus €235k for FY 2020 and the €259k average since the 2013 flotation.

The average cost per employee was €64k, €1k higher than FY 2020 and matching the general level witnessed since the flotation. And employee costs absorbed 27% of revenue, the same proportion for the previous three years.

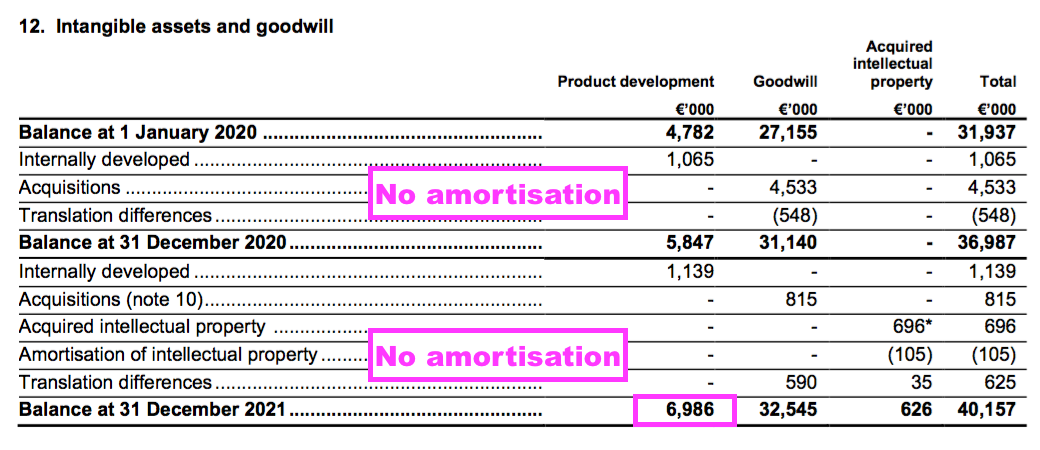

16) ACQUISITIONS AND GOODWILL

A useful list of past acquisitions:

The ‘fair value headroom’ of the carried goodwill has reduced by a very significant €25.5m:

Minor tweaks to the assumptions — notably the Ebitda margin reducing by more than 1 percentage point — have prompted the reduced value. The €25.5m reduction essentially means MCON thinks its past acquisitions now have a DCF value €25.5m less than previously thought, which is not ideal.

Whether these tweaks suggest MCON’s future is likely to be less profitable generally than previously expected is difficult to say. The reduction could be due just to the sensitivity of DCF sums. MCON did not provide ‘fair value headroom’ figures prior to FY 2020.

MCON discloses the assumptions needed for the ‘fair value headroom’ figure to reduce to zero:

Confirmation that Greenhammer and other capitalised projects will be amortised over an acceptable 3-5 years:

17) LAND AND BUILDINGS

A reminder that part of MCON’s notable capex has purchased land and buildings, the value of which ought not to erode too much over time:

€9m has been spent on land and buildings since FY 2017:

18) STOCK

Finished goods continue to dominate MCON’s hefty inventory balance:

MCON now discloses work in progress separately and restated the FY 2020 figures.

19) RECEIVABLES

Irritating that MCON lumps together all receivables and does not separately disclose trade receivables (i.e. outstanding customer payments).

Still, the ratios over time have been consistent, with FY 2021 no exception:

Net receivables was 17% of revenue, in line with the previous three years, while impaired receivables were 4% of gross receivables, in line with the previous three years as well.

20) PAYABLES

Conversely MCON does disclose trade creditors (i.e. payments owned to suppliers):

21) INTEREST COSTS

The effective interest rates do not appear too exorbitant:

Note certain lease costs can reach 15%.

22) OPTIONS

Almost 6 million options equates to potential dilution of 3%:

The directors’ options require EPS growth of 5% plus CPI over 3 years.

23) POST-YEAR ACQUISITION

Financial details of the latest acquisition:

Maynard