***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

20 June 2026

By Maynard Paton

Shares trading close to their 52-week lows can often provide lucrative buying opportunities for contrarian investors.

In particular, promising companies that appear temporarily out of favour can generate very worthwhile returns as and when profits recover and the market re-rates the share price.

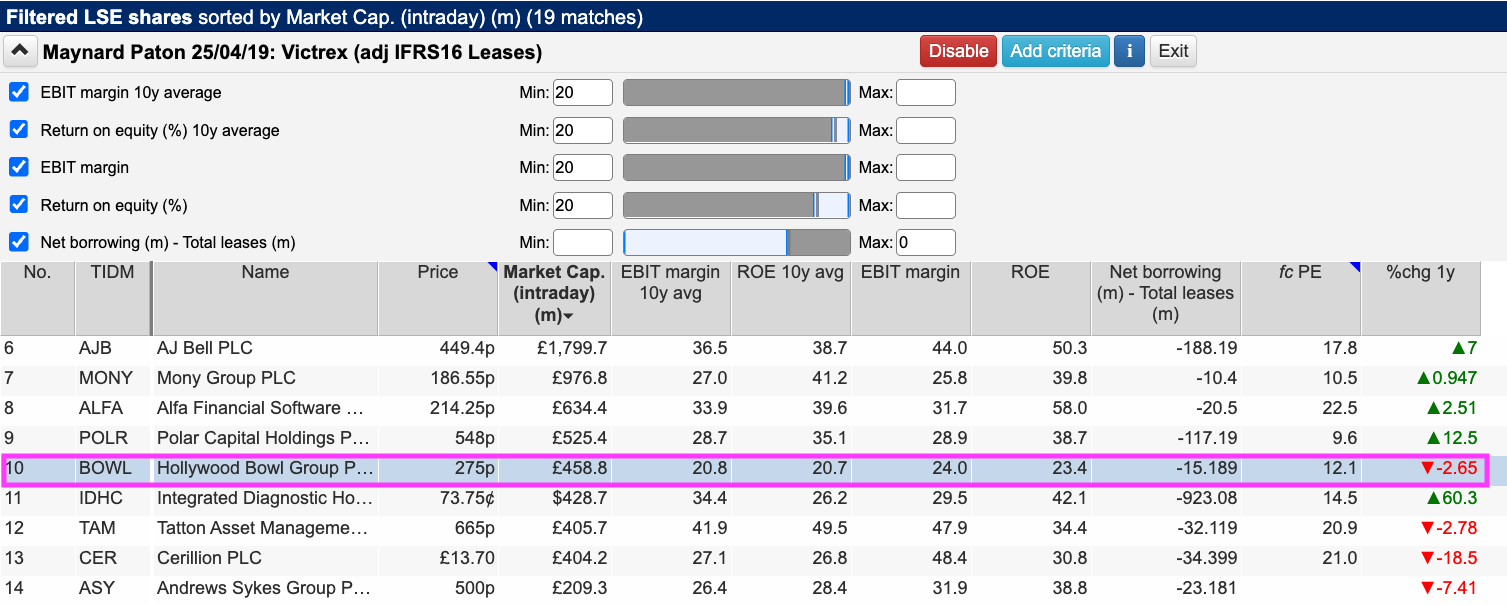

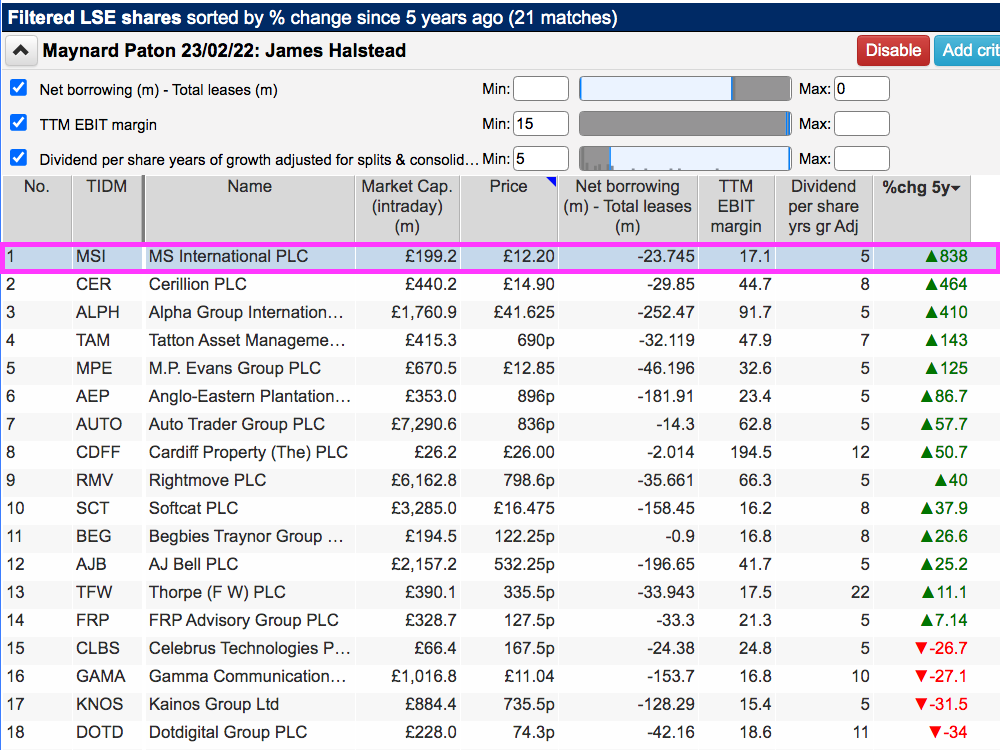

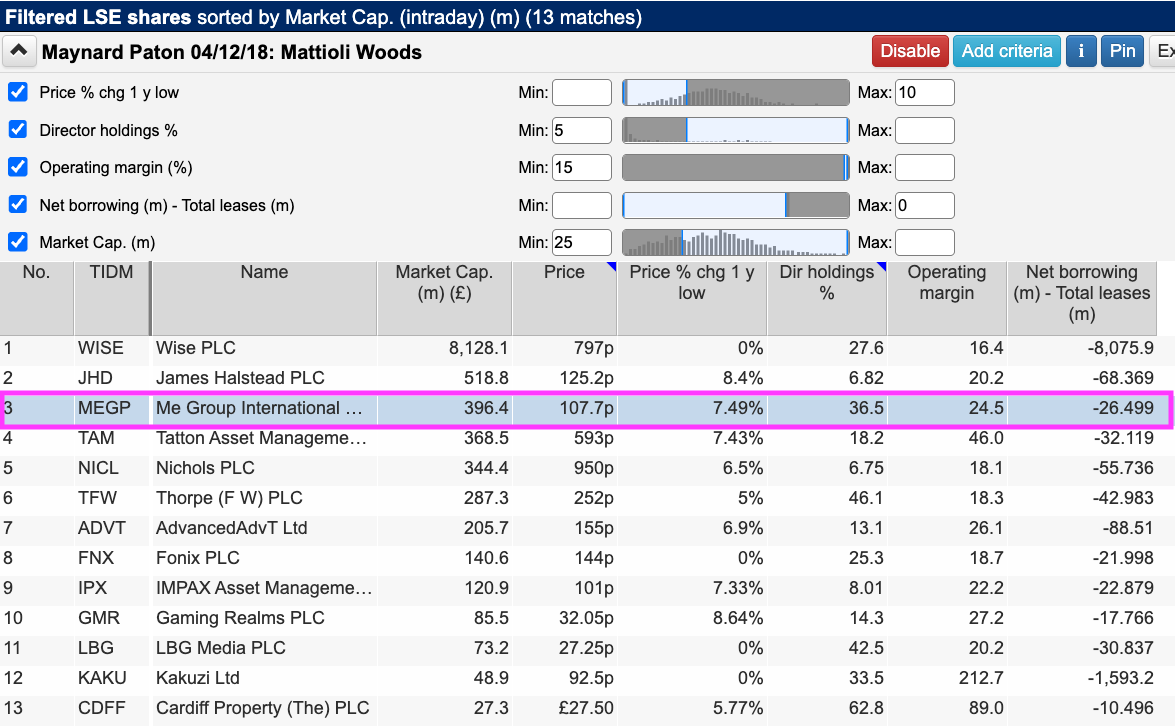

The other day ShareScope revealed some 458 names trading within 10% of their 52-week lows, with further filtering to find only ‘promising companies’ narrowing the list down to 13:

The exact screening criteria I redeployed were:

- A share price within 10% of its 52-week low;

- Director ownership of at least 5%;

- An operating margin of 15% or more;

- Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations), and;

- A minimum market cap of £25m.

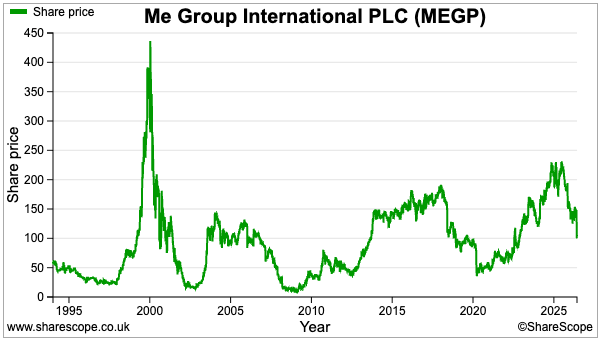

I selected ME Group because this company has for years popped up on my various ShareScope filters and coverage had become very overdue. A recent profit warning meanwhile established a new 52-week low at 100p:

Let’s take a closer look.

Read my full ME GROUP article for ShareScope >>Maynard Paton