30 April 2022

By Maynard Paton

Results summary for Tristel (TSTL):

- An underwhelming pandemic-disrupted performance, with the dividend held for the first time since FY 2013 as hospital customers delayed resuming normal purchasing activity.

- Progress was complicated by the understandable culling of numerous ‘non-core’ products, although the associated reclassification revealed TSTL’s surface disinfectants to be less profitable than previously declared.

- Sector “lobbying” within the United States for EPA-approved disinfectants might have created a new “commercial opportunity” for TSTL’s DUO foam.

- Brexit stock-piling, share options and US costs offered a wide range of profit outcomes, but cash flow remained respectable and bolstered net cash to a useful £9m.

- A 50% lower share price on a possible 32x multiple is not an obvious bargain, especially if patent expiries, automated competition or single-use medical equipment cause disruption. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Discontinued operations: rationale and savings

- Discontinued operations: product reclassification

- Discontinued operations: geographical reclassification

- Reporting disclosure

- United States

- Patents

- Share options

- Financials

- Valuation

News links, share data and disclosure

News: Interim results, presentation and webinar for the six months to 31 December 2021 published/hosted 21 February 2022

Share price: 300p

Share count: 47,185,043

Market capitalisation: £142m

Disclosure: Maynard owns shares in Tristel. This blog post contains SharePad affiliate links.

Why I own TSTL

- Develops medical-device disinfectants that are repeat-purchase and face limited direct competition due to multiple patents, instrument-manufacturer approvals, scientific testimonies, secret ingredients and regulatory hurdles.

- Enjoys a sizeable and resilient UK market position alongside worthwhile expansion opportunities abroad — most notably within the United States.

- Boasts financials that, pandemic-disruption aside, showcase high margins, robust returns on equity, decent cash conversion and no debt.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary:

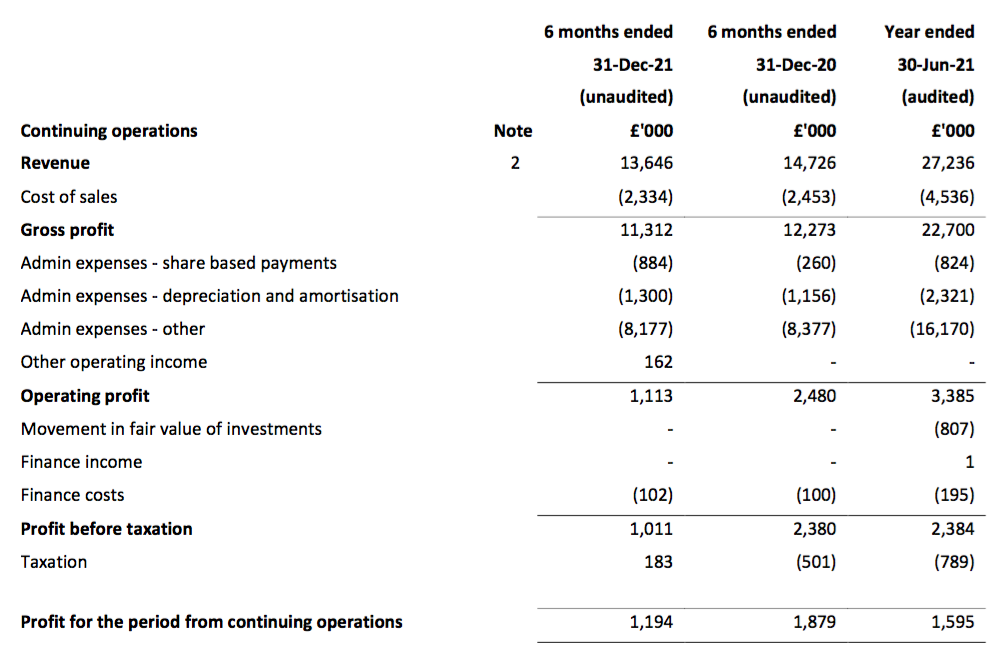

Revenue, profit and dividend

- December’s AGM update had already heralded H1 revenue of at least £15m and a performance complicated by Brexit stock-piling:

“We expect revenue to exceed £15m compared to £16.8m in the first half last year, noting revenue last yearincluded a one-off sale of £0.9m to the NHS for Brexit-related inventory. This stock was released back to UK hospitals during this first half, creating a £1.8m period-on-period distortion.”

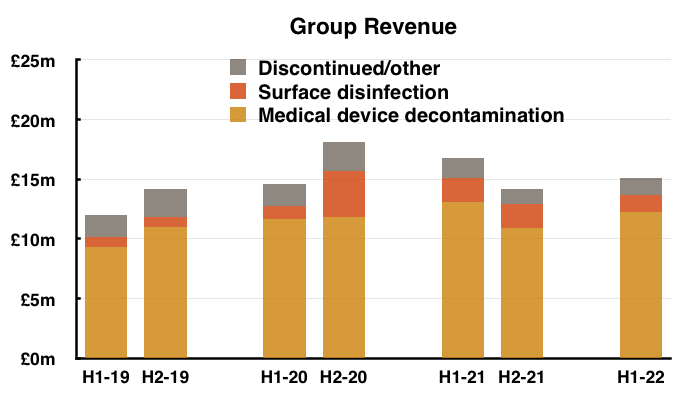

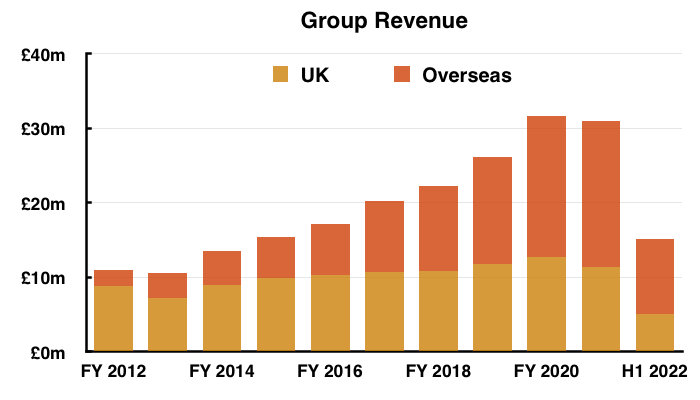

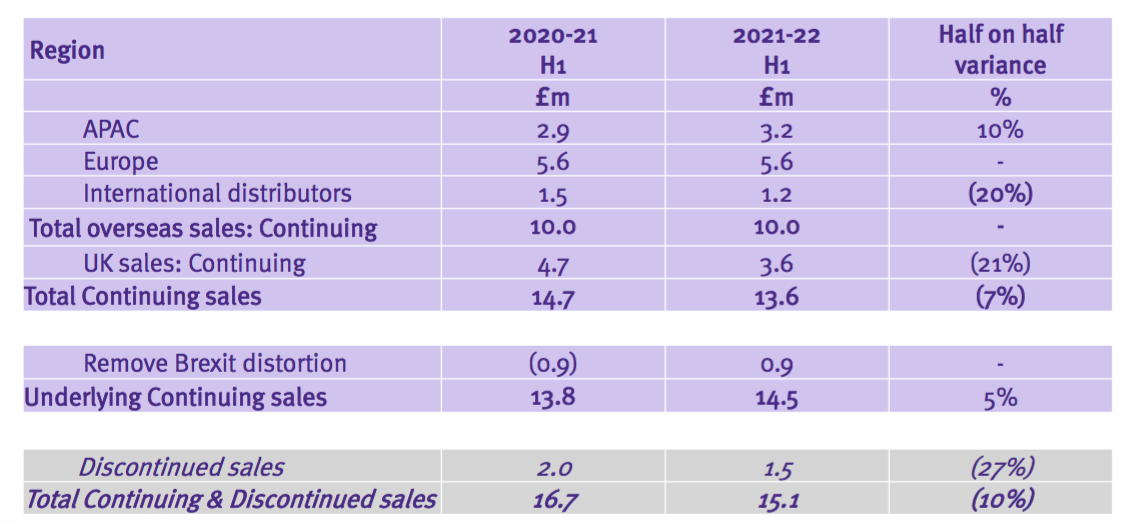

- Total revenue for this H1 did indeed exceed £15m at £15.1m:

- The discontinuation of various ‘non-core’ products was by far the most significant development during this H1 (see Discontinued operations: rationale and savings).

- The discontinuation further complicated this H1 performance and probably explained why December’s AGM update had not referred to profit.

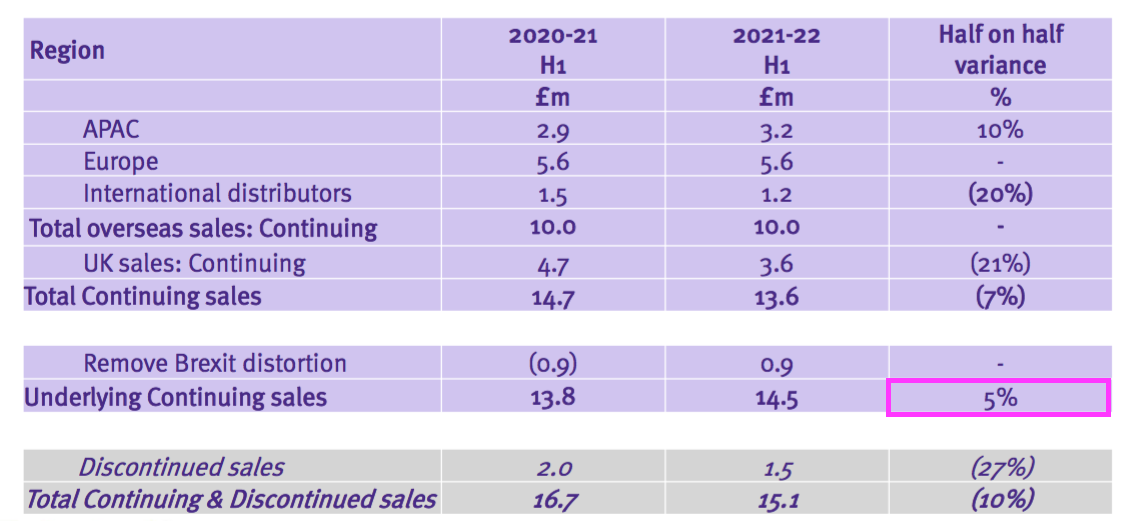

- Total H1 revenue declined 10%, but TSTL claimed underlying sales (i.e. adjusted for Brexit stock-piling and discontinued products) gained 5%:

- Total revenue of £15.1m thankfully surpassed the £14.2m collected during the preceding — and somewhat disappointing — H2 2021.

- December’s AGM update had declared:

“Overseas revenues are expected to account for 64% of worldwide sales during the half compared to 60% in the comparable period last year.“

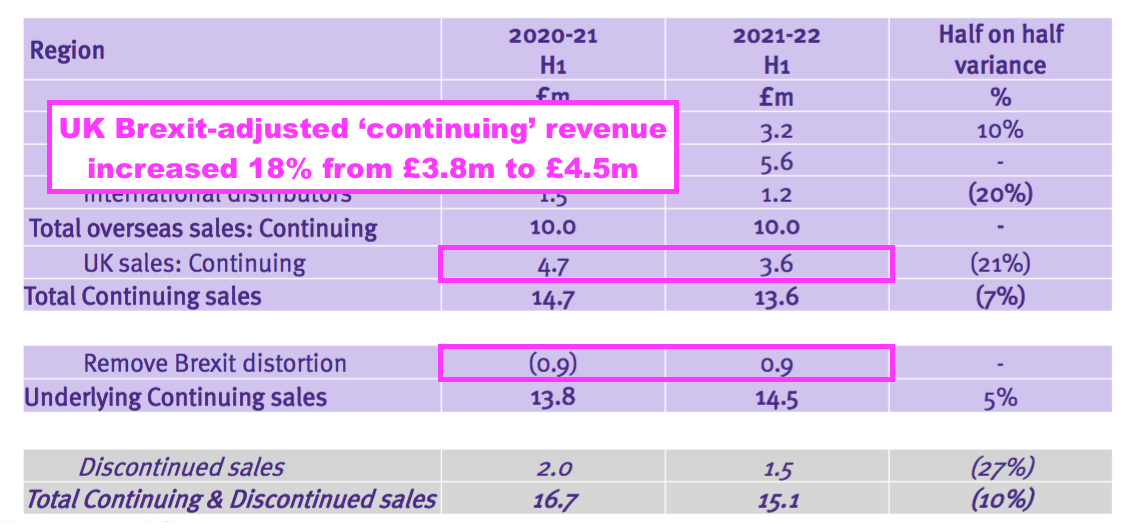

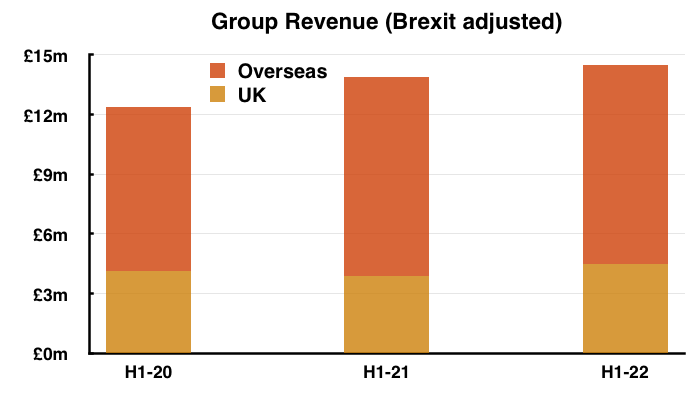

- Overseas sales at £10m in fact represented 66% of total revenue:

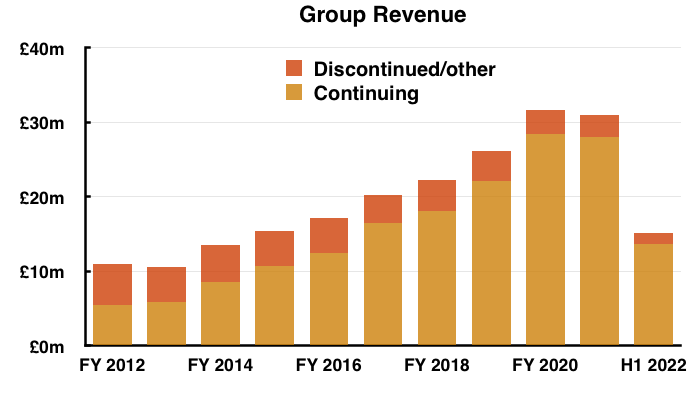

- Note: All my revenue charts above include what are now deemed discontinued operations. Figures for previous years have not been restated.

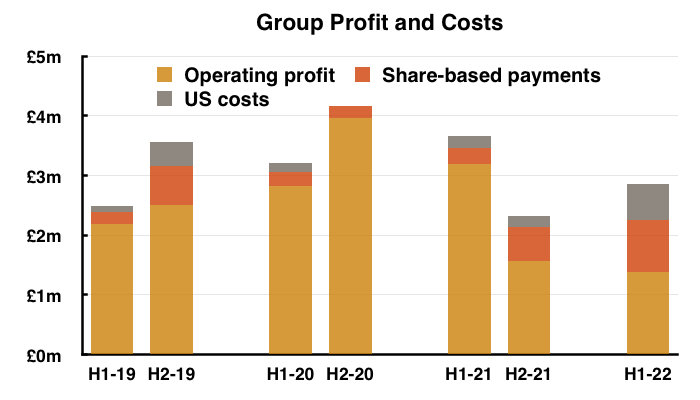

- As well as Brexit stock-piling and terminated products, reported profit was complicated even further by TSTL’s usual:

- Share-based payments (see Share options), and;

- Costs associated with the US regulatory programme (see United States):

- Other operating income of £162k (relating to chemical-data fees and formulation transfers) also influenced reported profit.

- Including every operating charge and credit, H1 operating profit fell 57% from £3.2m to £1.4m.

- Excluding share-based payments, US costs, other operating income and discontinued products, H1 operating profit declined 17% from £3.0m to £2.4m.

- The comparable H1 was bolstered by Brexit stock-piled revenue of £0.9m, which TSTL said was “released back to UK hospitals during this first half”.

- In other words, total H1 revenue really should have been £0.9m higher at £16.0m while the comparable total H1 revenue should have been £0.9m lower at £15.8m.

- Judging the profit effect of the Brexit stock-piling is difficult. But with a product gross margin of more than 80%, perhaps gross profit could have been £0.7m higher and the comparable H1 gross profit could have been £0.7m lower.

- Mixing all the adjustments, guesswork and interpretation together, my best estimate of operating profit — excluding share-based payments, US costs, other operating income, discontinued operations and Brexit stock-piling — is approximately £3m for this H1 versus approximately £2.4m for the comparable H1.

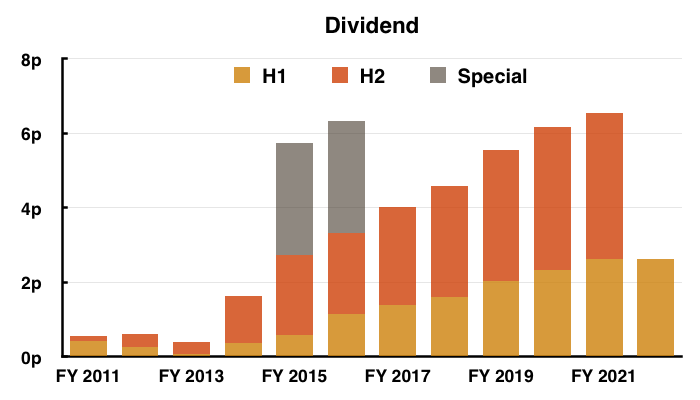

- At least the dividend did not require any adjustments, guesswork or interpretation:

- The interim payout was unchanged — the first time the dividend was not lifted since FY 2013.

- The standstill payout reflected TSTL’s generally underwhelming progress since the pandemic disruption began during FY 2021.

- TSTL’s revenue is dependent mostly on the wipes and foams that decontaminate diagnostic medical instruments such as nasendoscopes, cardio echo probes and tonometers…

- …and the number of patient appointments requiring such medical instruments reduced during the pandemic as hospitals were overwhelmed by Covid-19 matters.

- The FY 2021 results previously claimed a resumption of normal trading:

“For the first time in eighteen months, we are confident that our normal predictable pattern of business has resumed.“

- But that “normal predictable pattern” was replaced by a “start-stop-start pattern” for this H1:

“Throughout the first half, COVID-19 has put enormous pressure on healthcare provision in all our markets. However, there are signs that hospitals are returning to pre-pandemic levels of service, although this improvement is neither uniform nor consistent.

Whilst we expect this “start-stop-start” pattern to continue through the second half, the number of diagnostic procedures that generate demand for our products is reviving globally.“

- TSTL nonetheless expressed optimism about normal trading one day returning:

“As the impact of the pandemic recedes and the number of endoscopies, ultrasound scans and other diagnostic procedures return to their pre-COVID-19 levels, we are confident that we will return to the growth trajectory we were on before 2020. The backlog for these procedures is front page news in all countries.”

- TSTL also expected an improved H2:

“We anticipate that second half revenue from Continuing operations will be higher than first half revenue.“

- H2 revenue really should be greater than H1 revenue, given H1 was distorted by the aforementioned Brexit stock-piling.

Discontinued operations: rationale and savings

- The discontinuation of ‘non-core’ products was mentioned within the preceding FY 2021 results:

“The remainder of our revenues derived from other chemistries and sectors outside of the hospital which we consider to be non-core, and it is our intention to discontinue many of these products in the current financial year because they are lower margin than our chlorine dioxide products and draw upon our resources disproportionately to the contribution they make to our financial and strategic objectives.“

- This H1 statement said the discontinued products exhibited unfavourable economics:

“Whilst the product ranges have always made a net profit contribution and have generated cash, the revenue decline could only be reversed by making a substantial and high-risk investment in bulking up our sales and marketing activities in markets which are dominated by multinationals manufacturing generic cleaning and disinfectant products at a scale which we did not believe we would be able to match.“

- Management confirmed during the webinar the discontinued operations had effectively ceased during H1.

- Management believed H2 revenue from the terminated products would be less than £100k and the associated H2 costs would be minimal.

- The cull of ‘non-core’ products was finished ahead of schedule. Management revealed during the webinar the rationalisation had been expected to take “until 2023 to complete“.

- TSTL said:

“We have simplified the business and sharpened our focus on the hospital and our proprietary chlorine dioxide chemistry.”

- The decision to discontinue a large range of low-revenue products was very understandable:

- Annual sales per stock-keeping unit (SKU) among the continuing products are approximately £150k versus only £17k for those SKUs now culled.

- The terminated products earned a £1.4m operating profit during FY 2021…

- …which implied a remarkable 37% operating margin on the associated revenue of £3.8m.

- Despite generating that £1.4m profit during FY 2021, the terminated products were effectively valued at zero by their discontinuation.

- A £2.4m write-off relating to the discontinuation arguably meant the terminated products had a negative value — at least to TSTL.

- TSTL reckoned the value of the terminated products would be shown through cost savings witnessed during H2 and beyond:

“The positive impact of the rationalisation on overhead will start to be felt in the second half, and the full impact will be experienced next financial year. “

- Management said during the webinar the regulatory cost of the terminated products was up to £100k per “active substance“, of which 15 were used within the discontinued range.

Discontinued operations: product reclassification

- Revenue from discontinued products differed to what was previously defined as ‘Other’ revenue.

- The 2021 annual report defined ‘Other’ revenue as:

“The other segment, which we regard as non‐core, represents the remainder of our revenues which derive from other chemistries and sectors outside of the hospital.“

- That description seemed to match this H1’s description of the terminated products:

“We have discontinued the manufacture and sale of products that are:

* Non-chlorine dioxide based

* Not sold into our core hospital market”

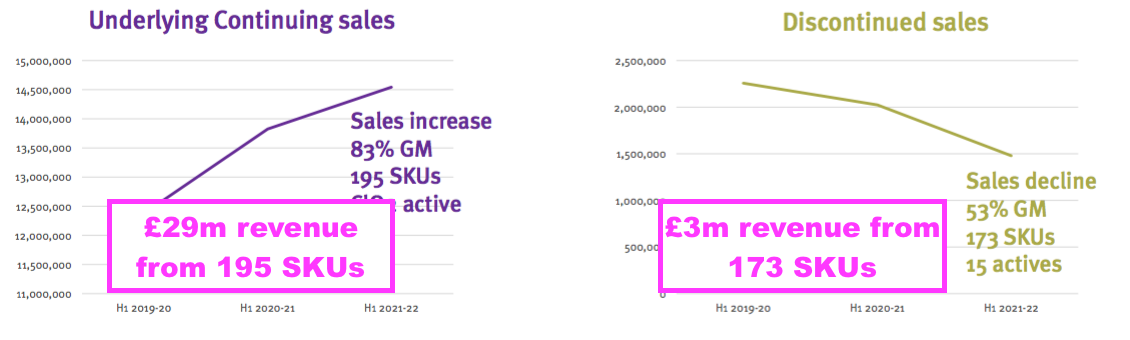

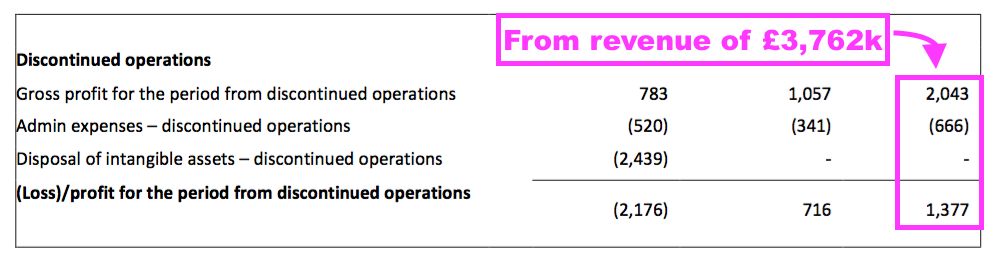

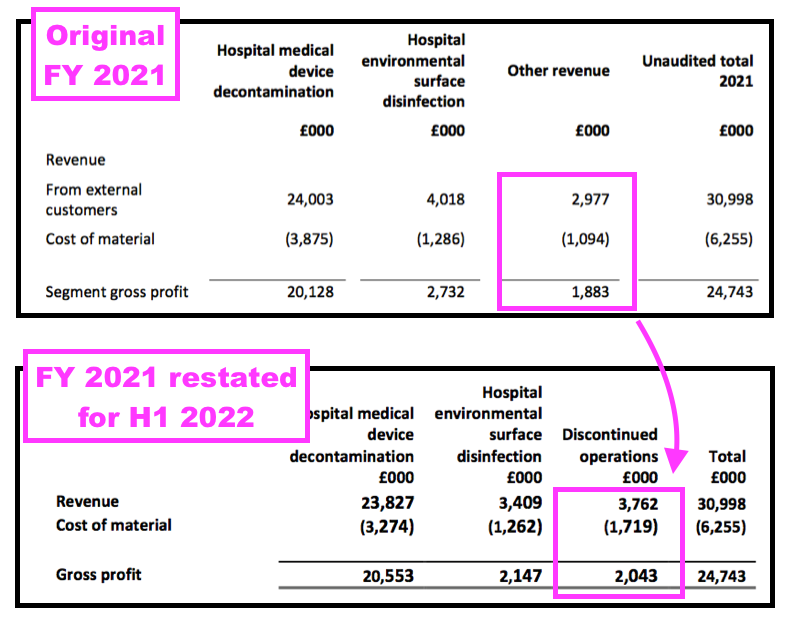

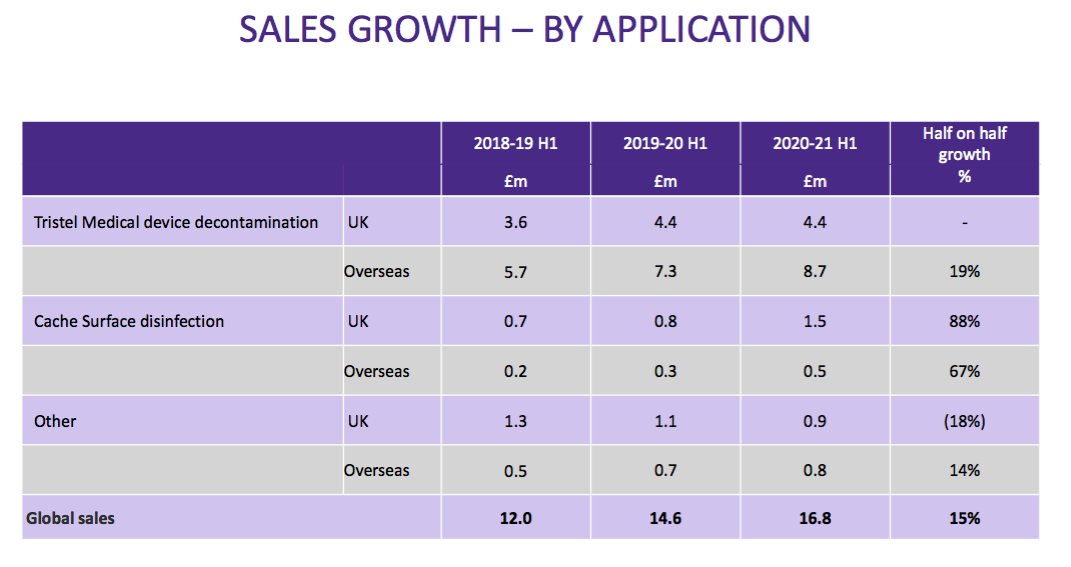

- The FY 2021 results had originally declared Other revenue of £3.0m, while this H1 now showed discontinued revenue for FY 2021 at £3.8m:

- The difference at the gross profit level — from £1.9m to £2.0m — was not as pronounced.

- Nonetheless, the differences meant some products now deemed ‘non-core’ were not deemed ‘non-core’ within the preceding FY 2021 results.

- Last year’s contribution from TSTL’s surface disinfectants changed significantly following the discontinuation reclassification.

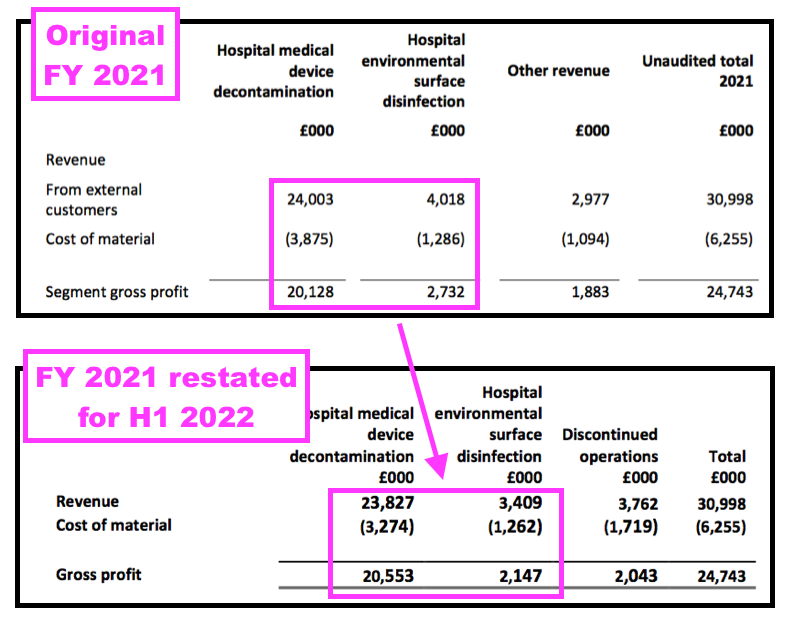

- The FY 2021 results originally showed a gross profit of £2.7m from surface disinfectants:

- But this H1 restated that £2.7m to £2.1m, down 21%.

- Note the gross margin for surface disinfectants actually declined following the reporting reclassification.

- The FY 2021 calculation was originally 68% (£2.7m/£4.0m), but this H1 statement indicated the division had achieved 63% (£2.1m/£3.4m) during FY 2021.

- The gross margin for medical-device wipes and foams in contrast increased following the reclassification.

- The FY 2021 calculation was originally 84% (£20.1m/£24.0m), but this H1 statement indicated 86% (£20.6m/£23.8m).

- The ‘non-core’ reclassification effectively admitted the surface-disinfectant division to be less lucrative than shareholders had previously thought.

- Management said during the webinar:

“What’s left in the surface range is all chlorine dioxide, which has a greater potential for growth and has a greater potential for gross margins.“

- Despite lots of previous management talk about new surface disinfectants…

* “The presentation slides referred to a new product called Shot. Essentially it is a bottle with a clever ‘dosing head’ that allows a TSTL disinfectant capsule to be mixed with exactly 10ml of water.” (FY 2018)

* “This year’s star product was Cache, a disinfectant used by hospitals for cleaning mattresses, bedside tables and other surfaces touched by patients.” (FY 2020)

* “Management said during the webinar that a new capsule range of surface cleaners called Shot had been launched after the year end and had enjoyed a ‘great response’ “. (FY 2021)

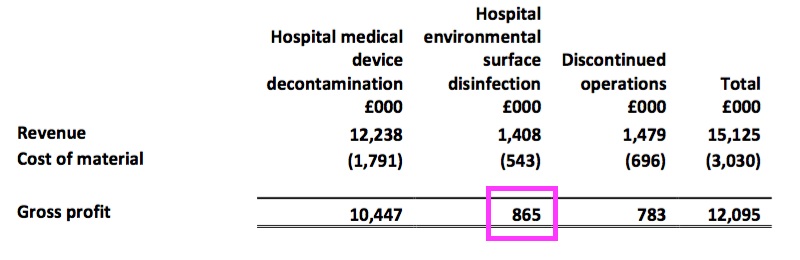

- …this H1 showed the continuing surface products contributing gross profit of only £865k — or just 8% — of the total £11.3m continuing gross profit:

- The rationalisation programme has therefore left TSTL even more dependent on its medical-device wipes and foams.

Discontinued operations: geographical reclassification

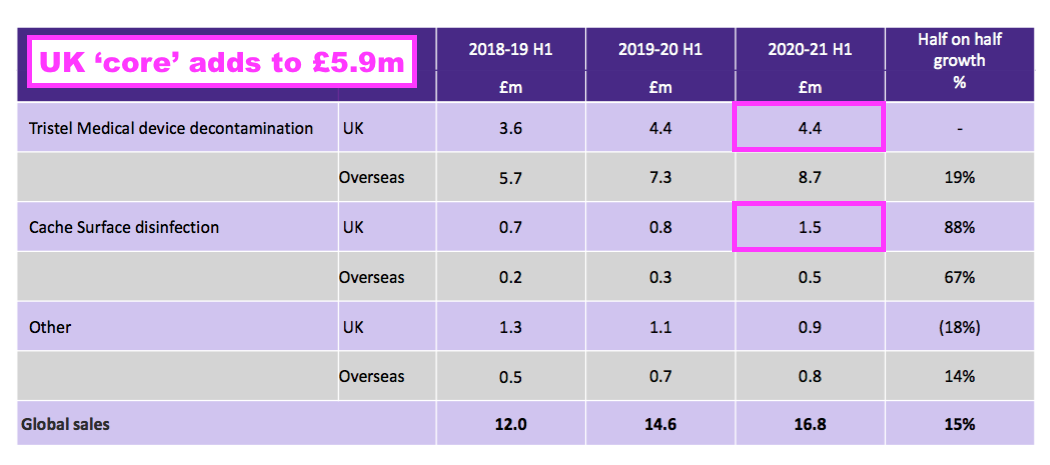

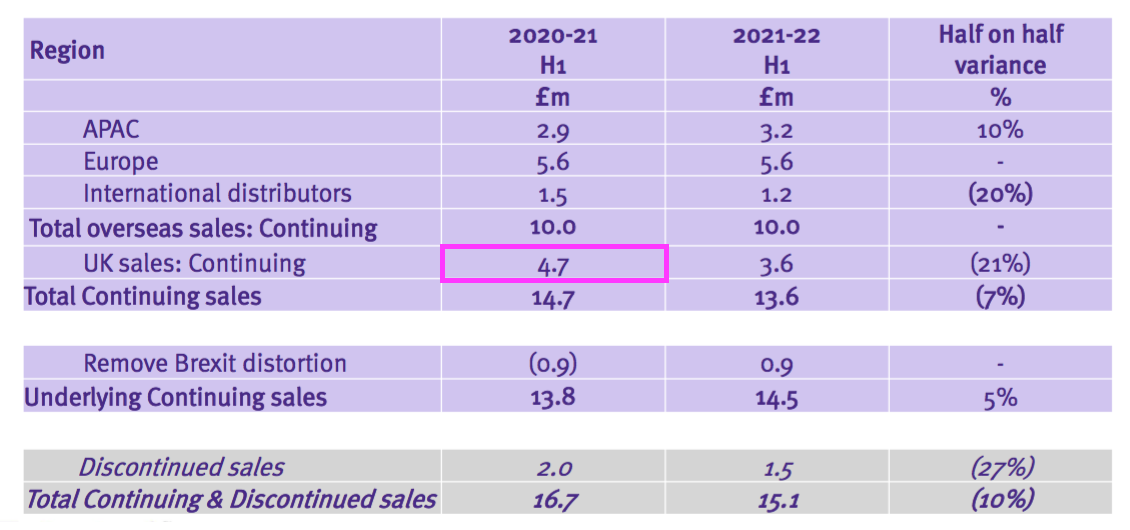

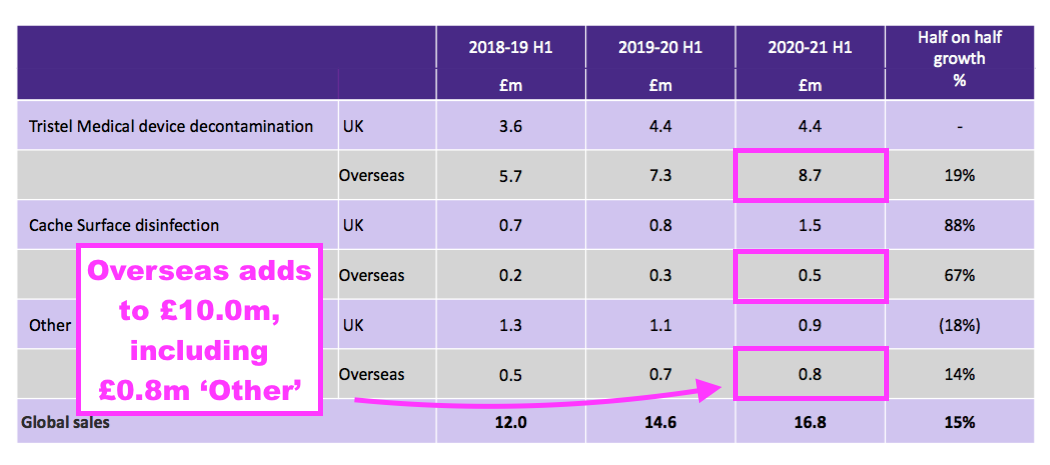

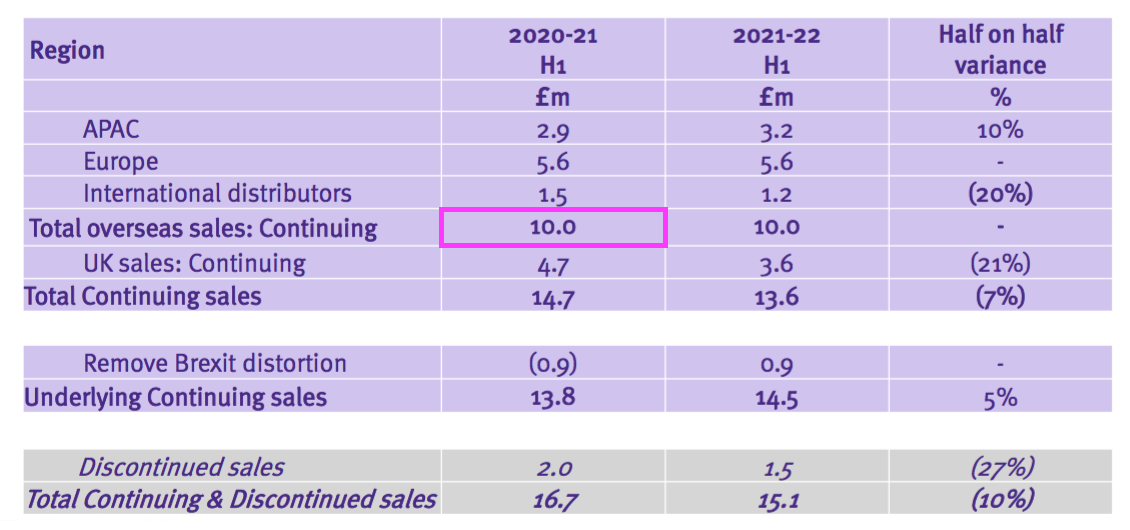

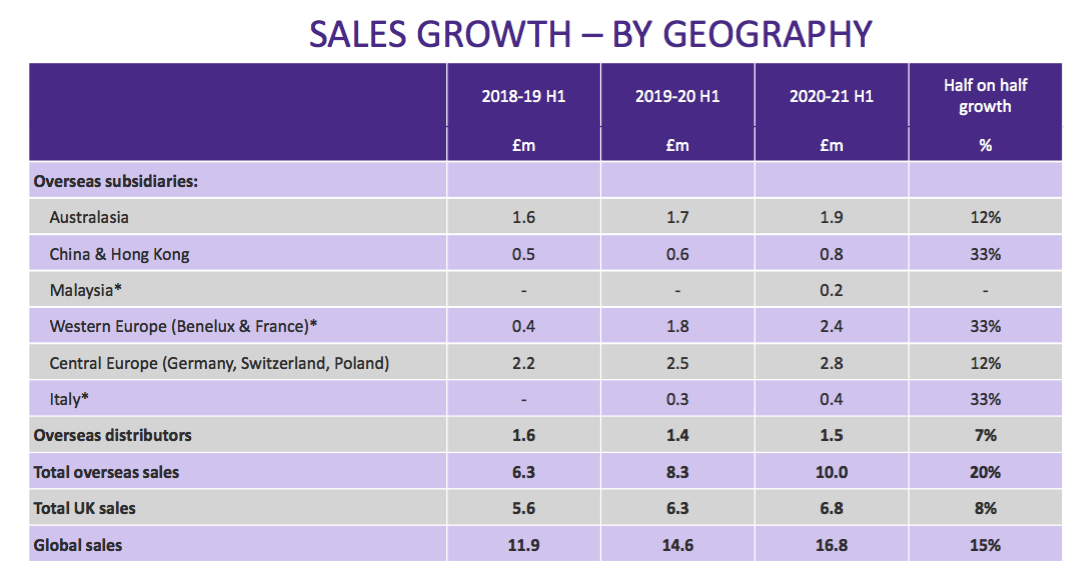

- TSTL’s geographical revenue slide provided further confusion to the discontinued operations.

- A year ago TSTL said H1 2021 UK revenue from the ‘core’ hospital disinfectants was £5.9m:

- But this H1 showed ‘continuing’ UK revenue at £4.7m:

- Furthermore, a year ago TSTL said H1 2021 overseas revenue — including ‘other non-core’ revenue — was £10.0m:

- But this H1 showed continuing overseas revenue equal to that £10.0m:

- These differences suggest during the comparable H1 2021:

- ‘Core’ UK revenue of £1.2m was in fact ‘non-core’, and;

- ‘Non-core’ overseas revenue of £0.8m was in fact ‘core’.

- The differences also suggest:

- The discontinued products were sold entirely in the UK, and;

- Some products not based upon chlorine dioxide and/or not bought by hospitals are still sold overseas.

- TSTL effectively claimed underlying UK sales (i.e. from continuing products adjusted for Brexit stock-piling) gained 18% to £4.5m during this H1:

- Assuming all overseas revenue is continuing, H1 UK continuing revenue adjusted for Brexit stock-piling grew approximately 8% from H1 2020 (pre-pandemic, £4.1m ) to this H1, which does not feel too awful:

- Total H1 overseas revenue has gained 21% during the same two years.

Reporting disclosure

- TSTL’s reporting disclosure for this H1 was unfortunately not as informative as for previous results.

- This time last year TSTL published slides detailing revenue by country…

- … and product category:

- This time the powerpoint disclosed revenue only by region:

- As such, determining the sales progress of TSTL’s most profitable products (the medical-device wipes and foams) within its most profitable market (the UK) has become impossible.

- Management could be forgiven for condensing the disclosures as the ongoing business has become dominated by the medical-device wipes and foams.

- But I trust UK revenue will still be disclosed separately from other regions. The UK is by far TSTL’s most mature market and therefore serves as a guide for the sales potential of other countries.

- Management explained during the webinar why geographical revenue had been compacted within the powerpoint:

“We’ve combined them because the list was getting longer and longer and it was not going to fit on the page.“

- Management did reveal during the webinar that H1 sales were:

- £2.7m versus £2.8m for H1 2021 within Central Europe;

- £2.3m versus £2.4m for H1 2021 within Western Europe, and;

- £600k versus £400k for H1 2021 within Italy.

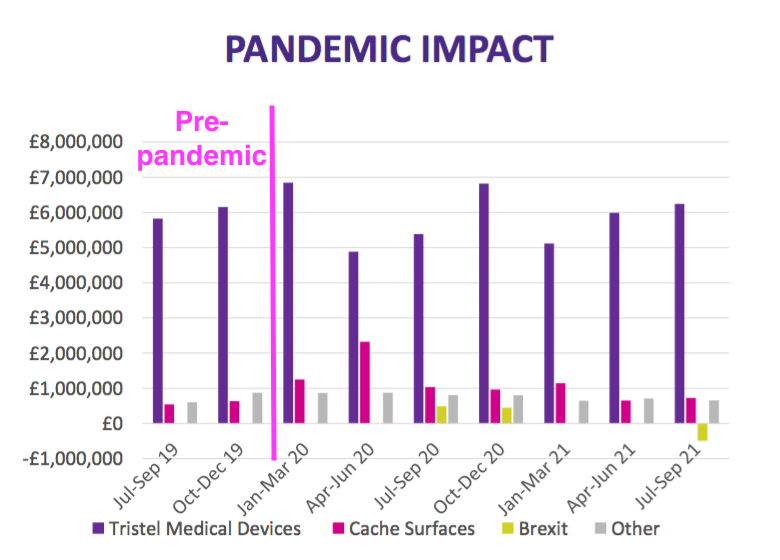

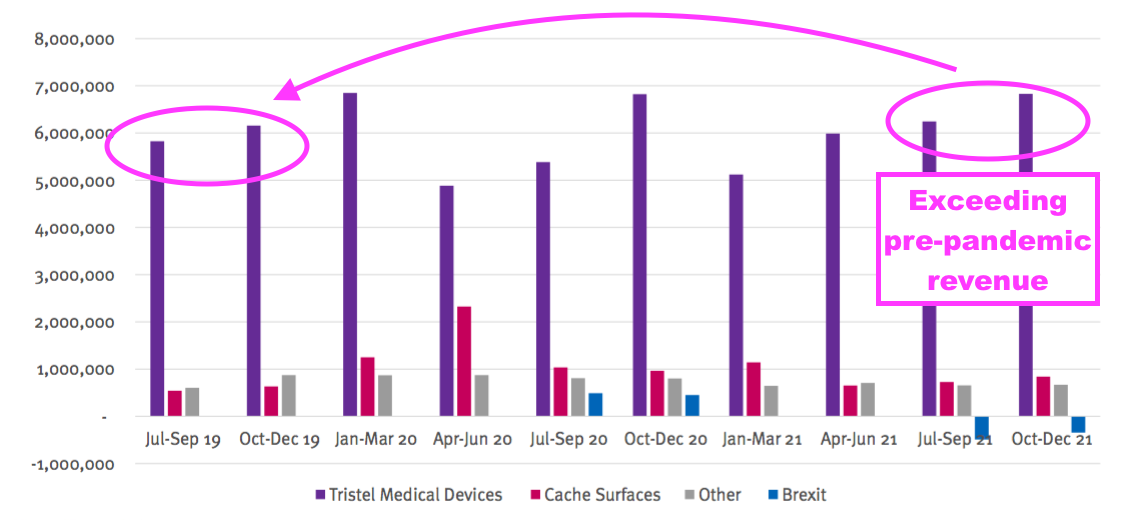

- Previous presentations had included a Pandemic Impact slide:

- But this H1 presentation did not.

- My conversation with management following the webinar prompted an updated presentation that included an extra Pandemic Impact slide:

- The extra slide encouragingly showed revenue from the medical-device wipes and foams exceeding the level achieved before the pandemic.

- Note: The extra Pandemic Impact slide is based upon the old reporting standard and includes products now discontinued.

- I mentioned to management after the webinar that shareholders ought to be given as much information as possible, and they can then decide whether to study or ignore any particular slide.

United States

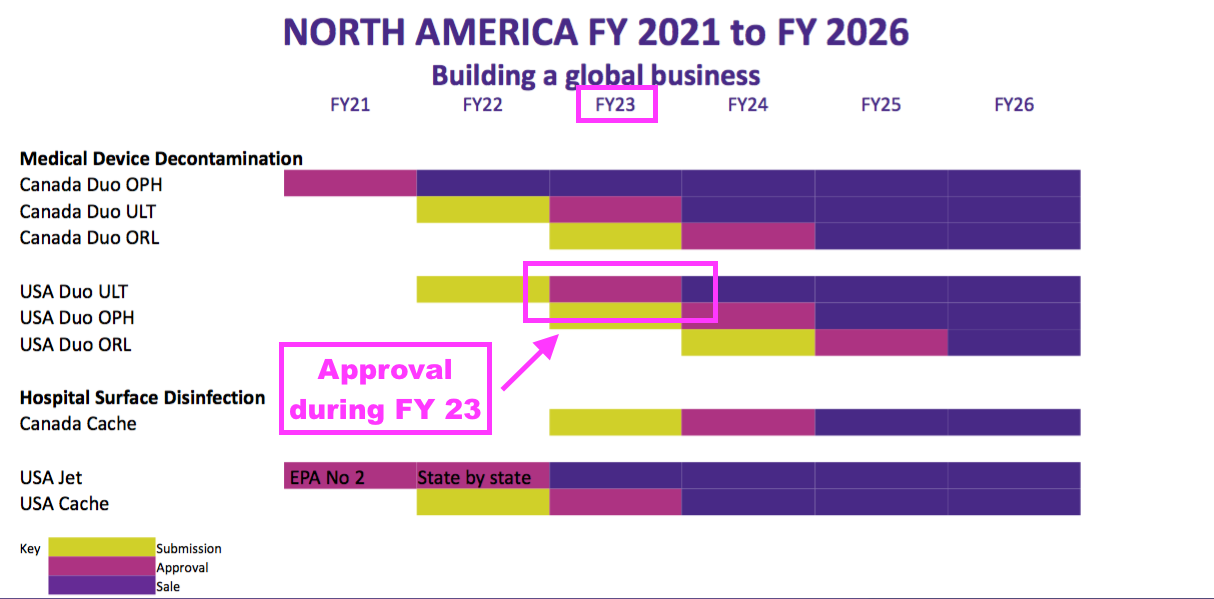

- The timescale for TSTL to obtain FDA approval to sell a high-level disinfectant within the United States appears to have lengthened slightly.

- TSTL reiterated the FDA application for the DUO foam that decontaminates ultrasound equipment would be made by 30 June 2022.

- But management said during the webinar:

“Once submitted, we will then be looking at a 12- to 18-month period of time during which the FDA reviews our submission.“

- The slides accompanying the FY 2021 results previously indicated the FDA would take a year to review the application:

- Veteran shareholders may not be perturbed by waiting an extra six months.

- After all, TSTL started the US regulatory process back in 2014 and bungled an FDA pre-application during 2018. My notes from October 2015 recount TSTL hoping to have obtained FDA approval by June 2017:

“Hope to submit product to FDA by June 2016 and receive approval by June 2017. Approval investment expensed via P&L, will be c£600k.”

- Management said during the webinar that 12 to 18 months for an FDA review was its “best guess“. Management added:

“We can look at the FDA’s website and we can see how long on average De Novo submissions are taking from submission to approval. A lot get abandoned on that journey; we are assuming ours won’t get abandoned. We have a view, [our US distributor] Parker has a view, our lawyers have a view, our technical consultants have a view.”

- One positive US development concerned the intermediate-level EPA approval for the DUO foam. TSTL said:

“Working closely with our USA manufacturing and distribution partner, Parker Laboratories (“Parker”), we took the decision during the half to restart the state registration of DUO under its USA EPA approval… Whilst this approval relates to ultrasound equipment it restricts DUO’s use to skin surface ultrasound probes and other surfaces of the ultrasound console. “

- TSTL had previously paused the EPA registration programme because management and manufacturer Parker were “unsure of the commercial opportunity for the use of DUO with the EPA approval”.

- But the “commercial opportunity” now appears more certain.

- This H1 statement in fact referred to sector “lobbying” for products such as TSTL’s DUO foam to disinfect skin-surface ultrasound probes under certain circumstances:

“There is a groundswell of professional opinion in the USA that a product like DUO, with the efficacy claims it has achieved, is more appropriate for skin surface probe disinfection, when the probe is used to guide the placement of venous catheters than more expensive equipment-based disinfection products that have FDA approval. A growing body of ultrasound practitioners is lobbying for the use of intermediate level disinfection in such circumstances rather than high-level disinfection.”

- Management said during the webinar that the sector lobbying for products such as DUO foam was in response to lobbying from Nanosonics (NAN), a quoted Australian company that manufactures the Trophon disinfection machine:

“Parker consulted with us and said: ‘Let’s enter the market with our EPA approval for DUO as quickly as we possibly can because then we can help the American Society of Sonographers and others to push back against this lobbying by Trophon‘.“

- I am not sure what American sonographers currently use to disinfect skin-surface ultrasound probes.

- But TSTL claimed the lobbying from Nanosonics and its own counter-lobbying had led to a “substantially expanded commercial opportunity in the United States ultrasound market“.

- Management remarks during the webinar did not hint at the “lobbying” leading to an immediate US sales bonanza:

“With the EPA approval, once it is state-by-state [registered], [we can] start marketing our DUO product. So the strategic intent between us and Parker is to get into the market, establish our brand, acquire a user base and position ourselves for when the FDA approval is ultimately granted to us“

- H1 2022 results from Nanosonics did not revise the Australian group’s opportunity for 60,000 Trophons to be installed within the States.

- Nanonsics presently has almost 25,000 Trophons installed in North America with trailing yearly revenue of AU$106m or approximately $75m.

- 60,000 Trophons therefore suggest a $180m market opportunity.

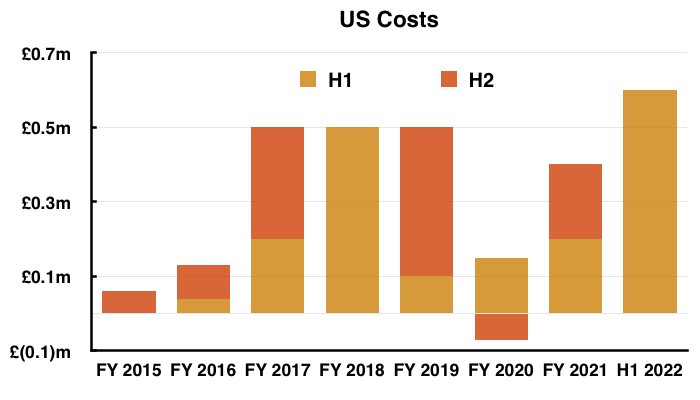

- Management said during the webinar that costs associated with the US regulatory programme to date were £2.8m and were expected to reach £3m by the end of H2.

- The FY 2021 results stated total US investment was £2.2m, implying US costs were £0.6m during this H1 and will be £0.2m during H2.

- Adjusting TSTL’s reported profit for US costs allows shareholders to better judge the group’s underlying profitability. US costs are of course presently accompanied by no US revenue.

Patents

- TSTL’s annual reports have regularly cited patents as part of the group’s competitive advantage:

“In its broadest sense, our intellectual property relates to:

1. Patents, trademarks, and registered designs;

2. The scientific validation of our chemistry and our products that has entered the public domain via 29 peer-reviewed and published papers;

3. 19 guidelines have been published by professional clinical bodies, infection prevention bodies, and national healthcare institutions that reference the use of chlorine dioxide recognisable as one of our products, and;

4. The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 55 medical device manufacturers, with respect to 1,845 of their individual models.”

- Patents do not last forever and some of TSTL’s patents are due to expire within the next few years.

- Patents cited for TSTL’s Sporicidal Wipes include:

- UK: GB 240 4337

- EU: EP 174 2672

- US: US 808 0216

- Google Patents shows the expiry dates of those patents as:

- UK: 7 May 2024

- EU: 26 July 2024

- US: 7 September 2024

- Patents cited for TSTL’s DUO include:

- UK: GB 242 2545

- EU: EP 184 3795

- US: US 884 0847

- Google Patents shows the expiry dates of those patents as:

- UK: 27 January 2026

- EU: 27 January 2026

- US: 11 September 2030

- Management confirmed during the webinar that some patents do indeed expire within the next few years. But management believed the expiries would not create generic competition:

“Will there be generic market entrants? I don’t think there will be because it is more than the patent that gives us our protection. There is proprietary know-how that is in the formulation. It is what it is. The patents have come to the end of their patent lives.“

- Establishing the exact nature of this “proprietary know-how” is difficult for layman shareholders.

- But TSTL’s flotation document from 2005 did state:

The key features of the Tristel technology, some of which form the patented claims, include:

* the speed of the reaction: chlorine dioxide is generated very rapidly;

* the pH at which the reaction takes place (4.5 – 6.5): the Directors believe that most other aqueous systems operate in highly acidic conditions to produce a fast reaction, and;

* the effectiveness of the corrosion inhibition system: this is especially relevant for the sterilisation of sensitive endoscopic and ultrasound instruments.

- The text “some of which form the patented claims” implies at least one of those “key features” is outside the patents and might therefore reflect the “proprietary know-how that is in the formulation”.

- But which of those three key features is outside the patents?

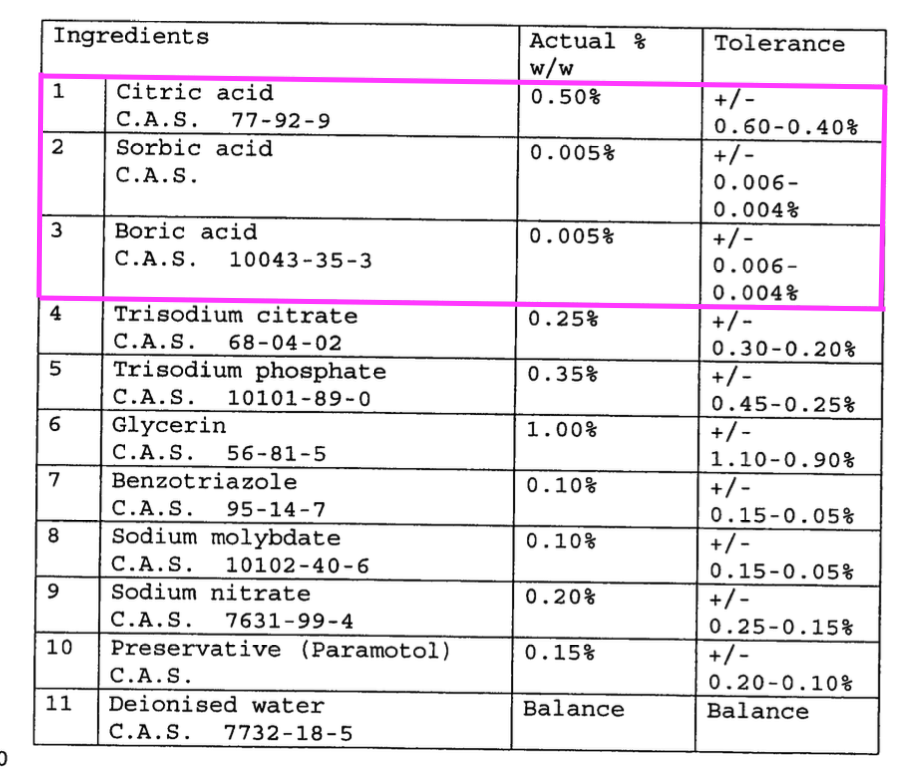

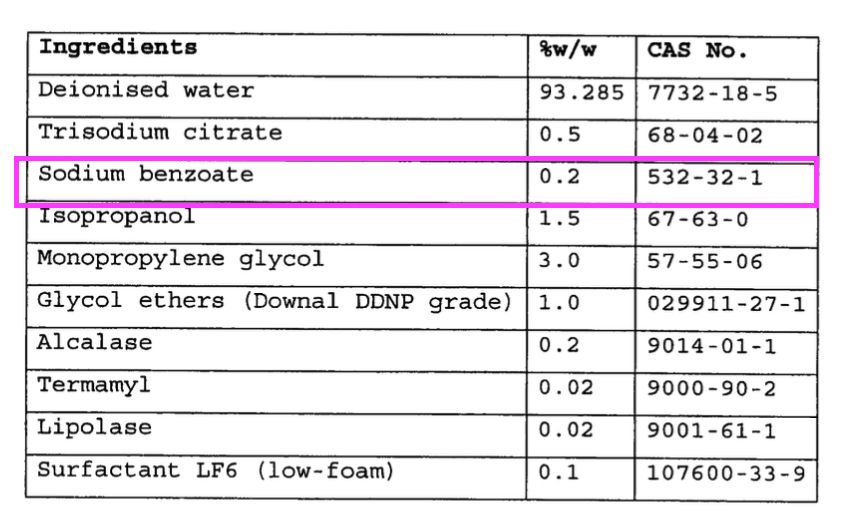

- Patent GB 241 3765 refers to TSTL’s Trio Wipes System and cites:

- “In a preferred embodiment, a mixture of acid is used, notably a mixture of citric, sorbic and boric acid“, and;

- “Sodium benzoate functions as a preservative and corrosion inhibitor“.

- “A mixture of citric, sorbic and boric acid” possibly relates to the “pH at which the reaction takes place” key feature.

- “Sodium benzoate functions as a preservative and corrosion inhibitor” possibly relates to the “effectiveness of the corrosion inhibition system” key feature.

- I could not find anything in patent GB 241 3765 about substances associated with the “speed of the reaction” key feature.

- I therefore guess the “proprietary know-how that is in the formulation” — but is not cited in the patent — relates to the faster chemical reaction.

- I suspect a determined competitor could one day replicate this “proprietary know-how” for a copycat product.

- But a copycat manufacturer would still have to:

- Obtain regulatory approval;

- Obtain certification from medical-device manufacturers for compatibility, and;

- Persuade hospitals to switch from TSTL’s products.

- Management said during the webinar:

“We have laid down four new patent applications that have gone to grant that give us technology which I think gives us protections into the future, gives us a new generation of manual reprocessing and will address the greatest concern that users have with our product that our surface coverage can’t be assured and verified independently of the individual doing the job.“

- Google Patents shows the four new patent applications to be:

- Patent GB 259 7069, which proposes “to include in one of the components a pH-sensitive indicator which changes colour or becomes clouded when adequate mixing has occurred“, and;

- Patents GB 259 7911, GB 259 7912 and GB 259 7913, which all cover the “validation of procedures in a decontamination process” that involve “capturing a video stream of a work area… in which the… procedure is carried out by a user [and] analysing the video stream…”

- Management suggested during the webinar the worry lies not with competition from generic copycats but with competition from machines:

“We have been… innovating to address some of the concerns that prospective users and existing users and regulators have with the manual process, which fundamentally means ‘how do I know that with your hands that you have covered the entire exterior surface of the instrument?’ It is the biggest challenge that we have day in and day out that we have always had and will always have.”

- Supporting the greater threat of automated competition, not-yet-approved patent GB 259 7069 admits:

“As the medical industry develops there are pressures to move towards automated disinfection systems that are perceived to provide additional assurances that the disinfection process has been successfully completed.”

- I can’t recall TSTL ever reporting patent infringement problems or disputes with competing wipes and foams, and TSTL has always claimed its chlorine-dioxide disinfection process is unique.

- An army of generic rivals may therefore not be on the sidelines ready to compete just yet.

- But the 80%-plus gross margins enjoyed by TSTL could well attract a competitor when the patents can be circumvented and a suitable formulation is developed.

- The four new patent applications might also imply TSTL’s competitive advantage does in fact require some patents to keep rivals at bay.

- The forthcoming patent expiries cannot be seen as a positive for TSTL. But right now I remain undecided as to how negative the expiries will become.

- The recruitment during 2020 of a non-executive director who has “advised a variety of global businesses on their IP related commercial issues particularly in the healthcare and technology sectors” would therefore seem very useful.

Share options

- Significant share-based payments have featured regularly within TSTL’s accounts.

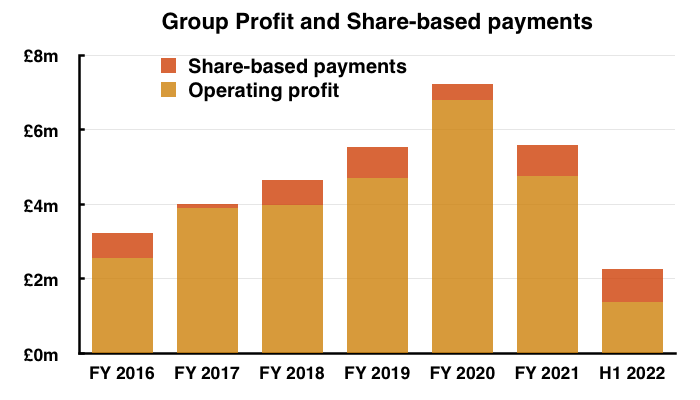

- Between FY 2016 and FY 2021, share-based payments reduced the aggregate pre-exceptional operating profit by £3.6m, or 12%:

- This H1 witnessed share-based payments reduce pre-exceptional continuing operating profit by £884k, or 44%.

- IFRS 2 requires all companies to calculate a share-based payment charge even if the options eventually become worthless (i.e. the performance targets are not achieved).

- TSTL’s (somewhat contentious) 2015 senior management options were granted when the shares were 96p and would vest if the price topped 134p.

- TSTL’s (less contentious) 2018 management options were granted when the shares were 275p and would vest if the price reached 350p, 425p and 500p.

- All the 2015 and 2018 options vested as the share price climbed from 96p to 500p.

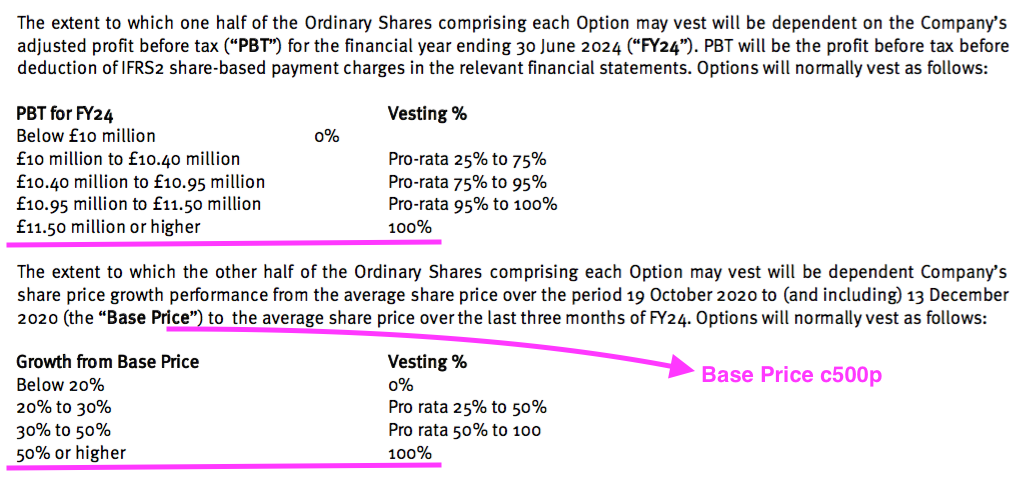

- TSTL granted 800k further options at the start of calendar 2021 when the shares were 500p.

- These 800k options will vest in full if profit before tax (and share-based payments!) surpasses £11.5m and the share price tops c750p during FY 2024:

- For any of the 2021 options to pay out, profit before tax and share-based payments has to reach £10m during FY 2024 (versus £5.4m for FY 2021) or the share price has to trade at a c600p average during Q4 2024.

- TSTL’s pandemic-hindered progress during both FY 2021 and this H1 suggests profit before tax reaching £10m — let alone the maximum £11.5m threshold — by FY 2024 to be remote.

- This latest batch of 800k options therefore stand a fair chance of becoming worthless — and the £884k charge becoming very irrelevant.

- My H1 2021 write-up explained how I assess TSTL’s option schemes in more detail.

- I wrote back then:

- “I welcome options where vesting is dependent on share-price advances, because such options:

- Are straightforward to understand;

- Have targets that cannot be fudged, and;

- Only come good if outside investors have benefited, too.“

- The downside to options where vesting is dependent on a share-price advancing is the share price advance may not be sustained after vesting.

- Option holders who benefited from the shares reaching 500p are not quite in the same boat as ordinary shareholders who still hold the shares at the recent 300p.

- Mind you, options where vesting is dependent on earnings, return on equity or some other measure carry the risk of earnings, return on equity or some other measure not being sustained after vesting

Financials

- TSTL’s accounts appear in adequate shape, and should improve once the benefits emerge from terminating the ‘non-core’ products.

- Excluding share-based payments, US costs, other operating income and the discontinued products, an operating profit of £2.4m equated to a useful 17.8% operating margin.

- TSTL implied margins could be sustained despite inflationary pressures:

“We are experiencing labour cost increases and component and raw material price increases across the Group and are increasing prices this year to match them.“

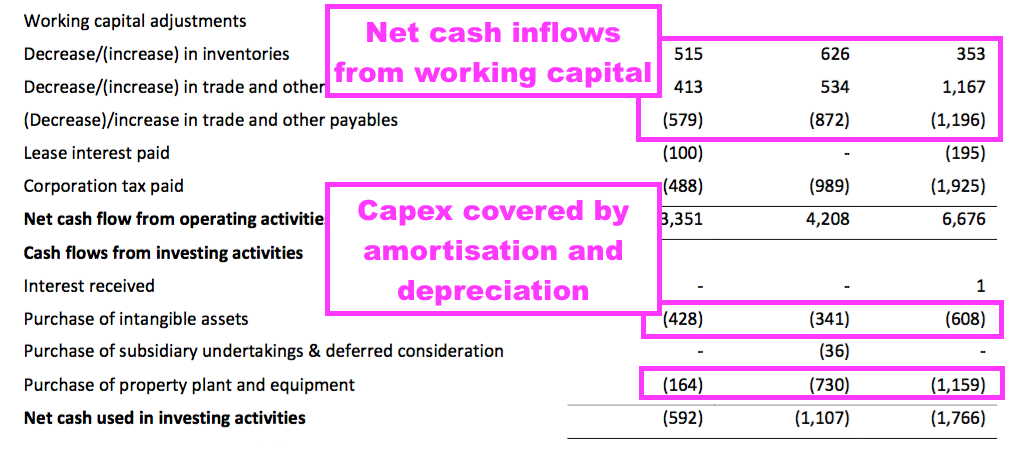

- Cash flow remained respectable.

- The half-year ended with cash at £8.8m, up £0.8m, after £2.4m was generated by the business, £0.3m was raised through options and £1.9m was paid as dividends.

- Cash flow was assisted by favourable working-capital movements (in particular, reduced stock levels producing £0.5m) and modest tangible capital expenditure (less than £0.2m):

- Cash flow was also assisted by the discontinued ‘non-core’ products, which generated an operating profit of £0.3m.

- Management said during the webinar that cash had since advanced from £8.8m to £9.4m.

- Lifting the cash position by £0.6m during the first seven weeks of 2022 seems about right after the business produced free cash of £2.4m during the preceding 26 weeks.

- TSTL carries no bank debt and no final-salary pension obligations.

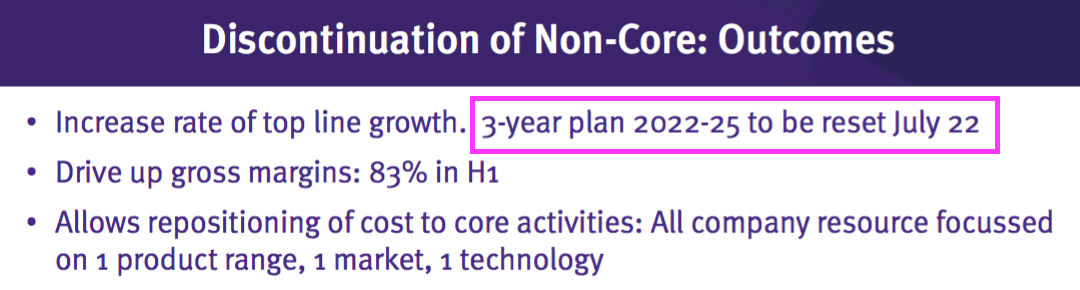

Valuation

- TSTL confirmed new three-year financial guidance would be set during July:

- Management disclosed during the webinar that by July the company would be able to judge how its overseas markets were “progressing out of Covid”, which in turn would give “better visibility on what those [guidance] targets should be“.

- The discontinuation of ‘non-core’ products should make determining the new financial guidance somewhat easier.

- TSTL’s previous guidance for FYs 2020, 2021 and 2022 projected revenue growing at an annual average compound rate of between 10% and 15%.

- Meeting the bottom-of-the-range 10% level required FY 2022 revenue of £34.8m — which feels very unlikely to be achieved given this H1 delivered total revenue of £15.1m.

- Doubling up my aforementioned best estimate of operating profit — excluding share-based payments, US costs, other operating income, discontinued operations and Brexit stock-piling — of approximately £3m gives a possible full-year operating profit of £6m.

- Taxed at next year’s 25% UK standard rate then leads to earnings of £4.5m or 9.5p per share.

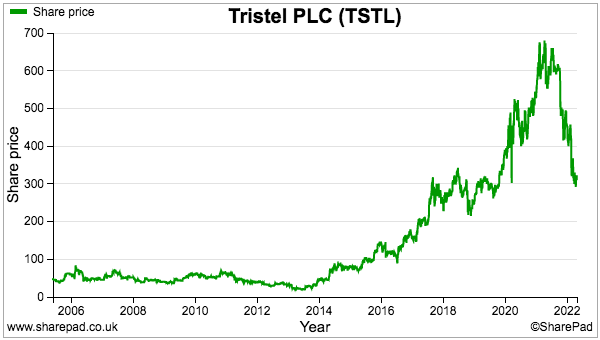

- The valuation sums could be fine-tuned further for lease costs, tax credits and the cash position, but the 300p share price at 32 times my 9.5p per share calculation does not suggest an obvious bargain.

- This time last year the shares were 600p and my calculation pointed to earnings of 12.6p per share and a 48x multiple.

- The shares have fallen 50% during the intervening twelve months because:

- Hospital customers have taken longer than expected to return to ‘normal’ activities following the pandemic;

- The prospect of meaningful US sales remains as distant as ever;

- Products that earned a £1.4m profit during FY 2021 have become discontinued, and;

- Macro-economic concerns have prompted a general re-assessment of many highly valued shares.

- A premium share-price rating may still be justified if:

- TSTL’s collection of product patents, scientific papers, manufacturer agreements and regulatory approvals continue to underpin a worthwhile competitive ‘moat’;

- The renewed focus on chlorine-dioxide disinfectants enhances TSTL’s margin, return on equity and employee productivity;

- TSTL enjoys further meaningful growth within its established overseas markets, and;

- FDA approvals are eventually received, US sales take off and the country’s ultrasound disinfection market (as implied by Nanosonics) really is worth up to $180m a year.

- But I recognise the share-price downside could still be significant were the ‘moat’ to become breached by patent expiries, automated competition, single-use medical equipment or some other disruption.

- A failure to obtain FDA approval after eight years of preparing a submission would also would hurt the shares.

- While shareholders await a return to the pre-pandemic “growth trajectory” alongside a successful FDA submission, the trailing 6.55p per share dividend supports a modest 2.2% income.

Maynard Paton

Tristel (TSTL)

Investor presentation 12 May 2022

A useful 23 minute presentation. Points I noted:

* FDA response expected within 12 months of submission (versus 12-18 months stated at the interim results presentation).

* Hope to renew 3-year financial targets at a shareholder open day 18th July . “Anticipate rolling over the targets” –> 10-15%pa sales growth and ebitda margin of at least 25%.

* “Think we will have returned to top-line growth this financial year (FY22) taking into account discontinued activities.”

* Pandemic impact slide included (omitted originally from interim results slide)

* Useful confirmation that the ingredients used to create a quick chemical reaction within the chlorine dioxide is indeed outside the patent:

“To get the reaction to take place as quickly as we enable it to, and to do it at a neutral pH, there is some clever chemistry that is embedded in the formulation, that goes right back to the beginnings of the company, the chemist that developed that technology is still with us, so there is proprietary know-how that we regard as trade secret.”

* Interest from other companies? “Very high valuation has been protection against approaches.

* Ebidta margin of 25%+ sustainable? “Yes I believe it is”

* Chinese division — £600k-700k revenue — “not been able to ship a product because the warehouse is closed and all of our staff are locked in their apartments [due to Covid]”

Maynard

Tristel (TSTL)

De Novo FDA submission for Tristel Duo ULT published 30 June 2022

Hurrah! Confirmation of the long-awaited FDA submission, announced on the 30 June 2022 deadline TSTL had previously defined. Here is the full text interspersed with my comments:

——————————————————————————————————————

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, reports that it has submitted its De Novo request for approval to the FDA, the United States regulatory body responsible for medical device disinfectants. Tristel Duo ULT is used for the disinfection of ultrasound probes.

Tristel Duo ULT is a high-level disinfectant foam that can be used on ultrasound probes used for intra-cavitary and skin surface diagnostic procedures. Ultrasound probe disinfection is one of Tristel’s most important areas of focus within the hospital infection prevention market and accounts for approximately 40% of the Company’s global revenue which analysts forecast at £28 million for the current financial year.

To the Company’s knowledge, Tristel Duo ULT is the first disinfectant to make a De Novo request to the FDA, reflecting the novelty of the product. Duo ULT is widely used throughout Europe, the Middle East, Asia, and Australasia and during the Company’s current financial year the product will have been used in over 8 million disinfection procedures of ultrasound probes worldwide.

——————————————————————————————————————

40% of £28m gives revenue of £11m a year for ultrasound disinfection.

But this update from 2021 said:

“Worldwide sales of all Duo branded products for medical device disinfection, including Duo ULT and Duo OPH, will exceed £4.3m in FY21.”

So the Duo foam ultrasound product to be used in the States represents perhaps £4m of the £11m — with the balance presumably generated by the Trio wipes system. The wipes are not yet on the FDA submission horizon. I do worry early Duo revenue from the States may not be truly significant, although the US market as indicated by Nanasonics (see blog post above) is sizeable.

Duo ultrasound revenue of say £4m versus 8-plus million procedures gives revenue of up to 50p per procedure.

——————————————————————————————————————

The FDA’s De Novo review and approval process stipulates a 150-day decision timeframe. Additional data requests are commonplace, and the FDA website states that the average duration for review and approval is approximately 11 months.

The Company is also proceeding with the state registration of another version of Duo which has been approved by the United States EPA for the disinfection of general medical surfaces. The Company has received 24 state approvals and anticipates that all others will have been received by the end of 2022.

The Company will manufacture and distribute both Duo products via its commercial partnership with Parker Laboratories, New Jersey (“Parker”). Parker is a leading manufacturer in the USA market for the conductive gels and sheaths that are used in all ultrasound procedures, and Parker has a nationwide distribution network.

——————————————————————————————————————

An average of 11 months for review and approval is better than the 12 (or 12-18) months TSTL had previously cited.

The EPA registration process looks to have slipped by six months. The H1 2022 slides showed a 30 June 2022 completion target:

The EPA-approved product will be used to clean surfaces — including ultrasound consoles and cords that connect to the ultrasound probe.

The tie-up with Parker appears to validate this entire US project. Parker is a prominent name in ultrasound gel and I doubt would get involved unless TSTL’s foam stood a good chance of selling well.

——————————————————————————————————————

Paul Swinney, Chief Executive of Tristel plc, comments: “After five years of testing and data generation we are very pleased to have finally submitted our De Novo request for approval to the FDA. We have made an investment of £2.8 million in the project which has all been expensed.

“The United States is the largest ultrasound market in the world and our competitors will be the same as those we compete with in all our other markets worldwide. To our knowledge no new high-level disinfectant has been approved by the FDA and introduced into the United States since 2011, other than variants of previously approved products. Duo ULT is recognised as a leading high-level disinfectant throughout the rest of the world, and our entry into the United States market will be a significant inflection point for the Company.”

——————————————————————————————————————

The £2.8m US costs were cited at the half-year stage, so no change there. The high-level disinfectant approved by the FDA in 2011 was the Nanosonics Trophon machine.

“…will be a significant inflection point” sounds bold; let’s just hope FDA approval is received.

Maynard

You don’t seem a happy bunny with this outfit. They do not seem to have a unique chemical; you can buy citric, sorbic acids, sodium benzoate over the counter. There is no prescription only product, which can represent “the moat”. In my ignorance, I thought that they would have made a whack during covid with disinfection being a must in your comfort zone.I get the impression that they are hoping to get FDA approval. I am not sure what their niche is. They say they have a “trade secret” Yeah, Right. Maybe the ultrasonic will be huge.

I am not so much interested in the financials, what is in the pipeline?

Hi Bertie

Yes, these results were not perfect and contained some niggles with the restructure and the revised profit of Surface products. I attended TSTL’s open day the other week (I spoke about it here) and talked to the inventor of the chemistry, and he mentioned the ‘secret’ ingredients were not only secret, but were manufactured in a ‘secret’ way. The gist of the conversation was that several larger companies have had a go at trying to replicate the chemistry, and none had succeeded. So perhaps TSTL’s chemistry really is a secret that can sustain a ‘moat’? All I know is that TSTL has repeatedly said nobody else has ever developed a similar chemistry for manual disinfection of medical devices. The 80% or so gross margin suggests some advantage in the marketplace. The pipeline essentially contains only new Surface disinfection products, which are now priced to compete with low-level disinfection wipes currently used by hospitals. Future growth is mostly based upon entry into new countries and greater sales of the present wipe/foams within existing markets.

Maynard