01 August 2022

By Maynard Paton

Results summary for FW Thorpe (TFW):

- A record H1 performance bolstered by the acquisition of Spanish firm Zemper and complemented by another special dividend.

- Progress at Thorlux continues to be modest, but a new MD, an order book up 25% alongside growing demand for energy-efficient lighting support future optimism.

- Dutch profit was assisted by the absence of earn-out provisions, with new manufacturing facilities at Famostar underpinning “continued rapid sales growth“.

- Net cash remained significant at £37m after extra stock investment suggested component shortages were no longer as severe as they once were.

- A P/E of 27 seems generous, but could reflect significant ‘ESG’ attractions as TFW showcases its environmental credentials to quoted companies scrambling for LED lighting. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Thorlux

- Netherlands

- Zemper and Ratio

- Other companies

- Financials

- Valuation

News link, share data and disclosure

News: Interim results for the six months to 31 December 2021 published 10 March 2022

Share price: 375p

Share count: 118,935,590

Market capitalisation: £439m

Disclosure: Maynard owns shares in FW Thorpe. This blog post contains SharePad affiliate links.

Why I own TFW

- Develops professional lighting systems with a long-established reputation for high product quality, leading technical innovation, first-class service and sustainable manufacturing processes.

- Board led by a veteran executive and assisted by family non-execs who steward a 45%-plus/£199m-plus shareholding and favour special payouts.

- Conservative accounts display substantial cash reserves, significant freehold property, consistent working-capital management and illustrious rising dividend.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary

Revenue, profit and dividend

- Positive remarks within the preceding FY 2021 results…

“Within the Group we have once again started the new financial year with a very strong order book, exceeding our expectations in most companies, especially Thorlux Lighting, and we look forward to more normal trading conditions returning soon.”

- …followed by satisfactory comments at the AGM…

“The sales order performance suggests our Group as a whole, and the market, is in good shape. We need to see material supply conditions stabilise to enable further improvement on last year’s financial achievements.“

- …had already indicated an acceptable H1 2022 performance.

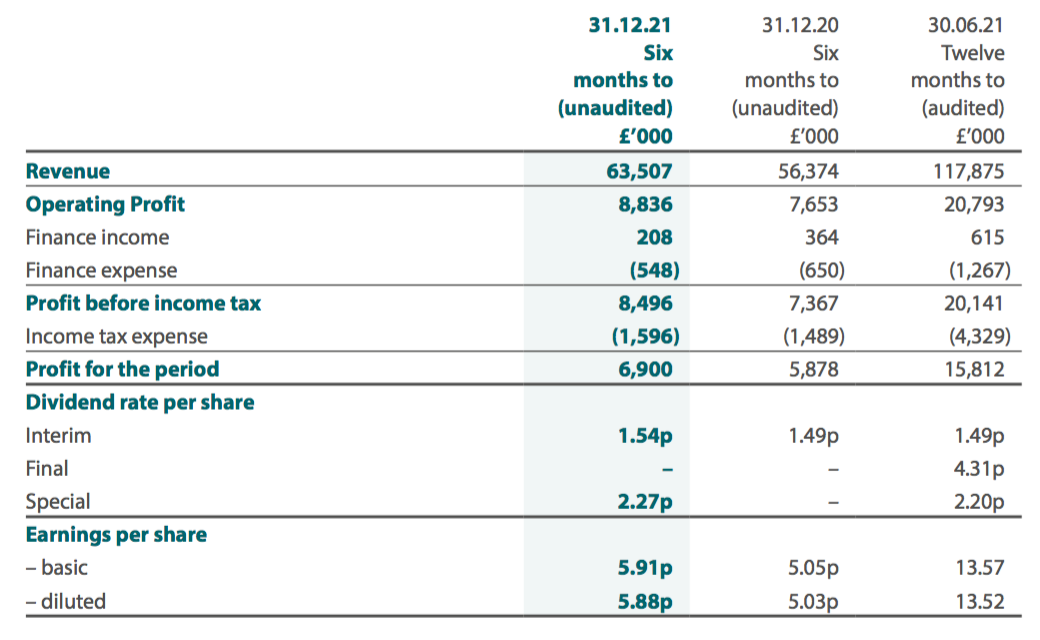

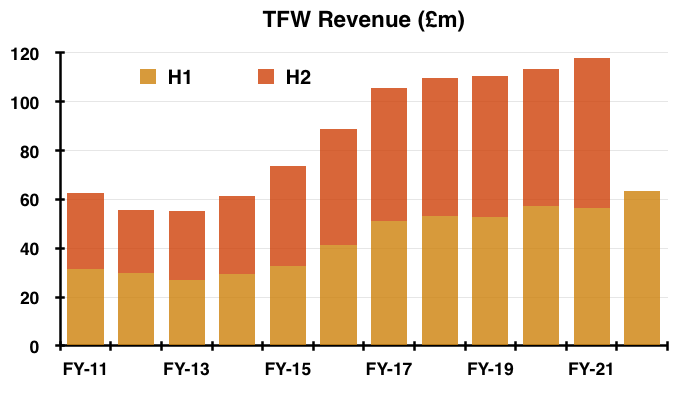

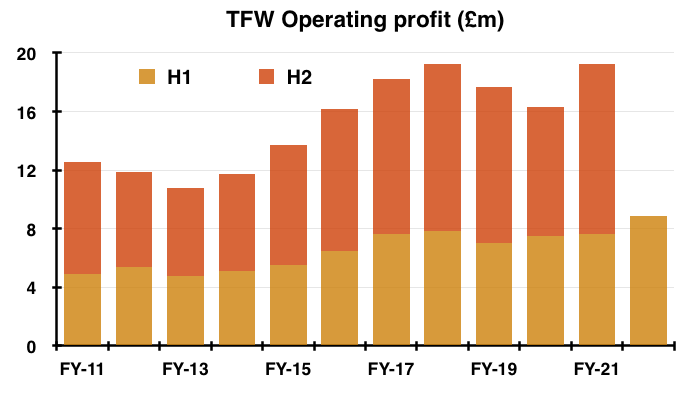

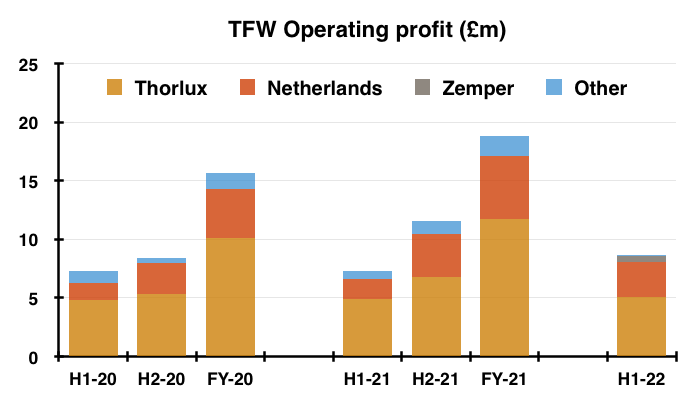

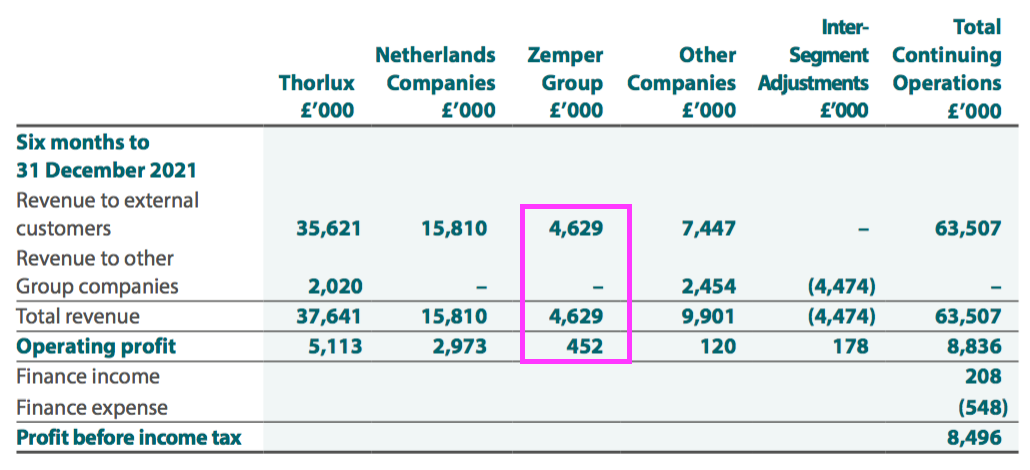

- H1 revenue gained 13% towards £64m while H1 operating profit climbed 15% to nearly £9m:

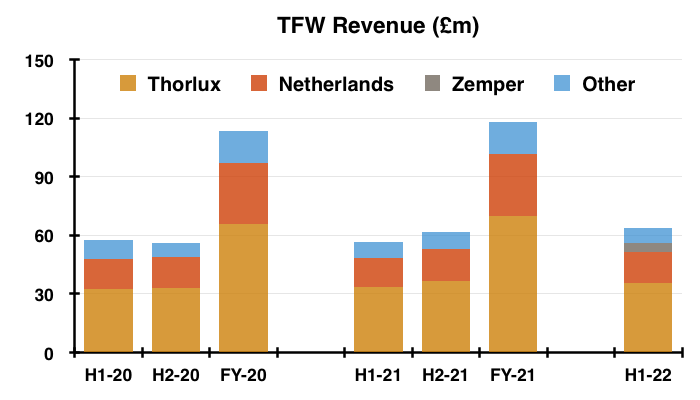

- The purchase of Zemper during October helped underpin what was TFW’s best ever H1 for both revenue and profit. Excluding the Spanish acquisition, revenue would have gained 4% and operating profit would have gained 10%.

- Assisting progress was the absence of earn-out provisions within the Netherlands division, which led to the Dutch subsidiaries representing a third of group profit (see Netherlands):

- TFW’s brief narrative claimed revenue was held back by supply issues:

“[S]ales revenues were suppressed across the Group at +4% (excluding the addition of Zemper), because of each company’s difficulty sourcing sufficient components, in particular electronic components and microchips“

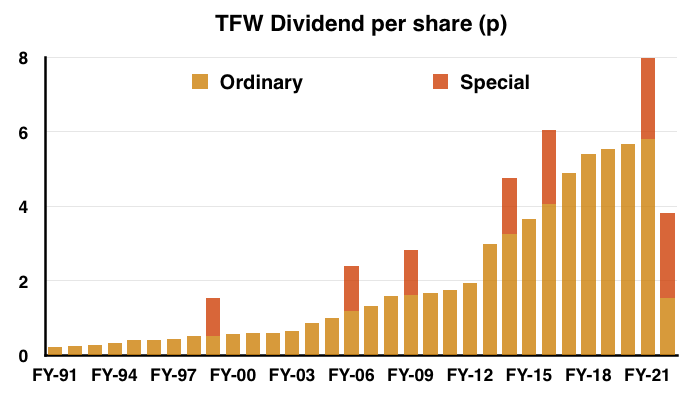

- TFW said its “strong” balance sheet justified a higher dividend, with the H1 payout lifted 3.3% — a slight improvement on the 2.5% advance for FY 2021.

- The greater H1 payout puts TFW on course for its 20th consecutive annual dividend increase:

- The payout has not been cut since at least 1991, although dividend cover at one point reaching 5x did leave plenty of leeway for payout advances.

- The results highlight was the declaration of a 2.27p per share special dividend, which followed the 2.2p per share special declared within the FY 2021 results and five other one-off payouts since FY 1999.

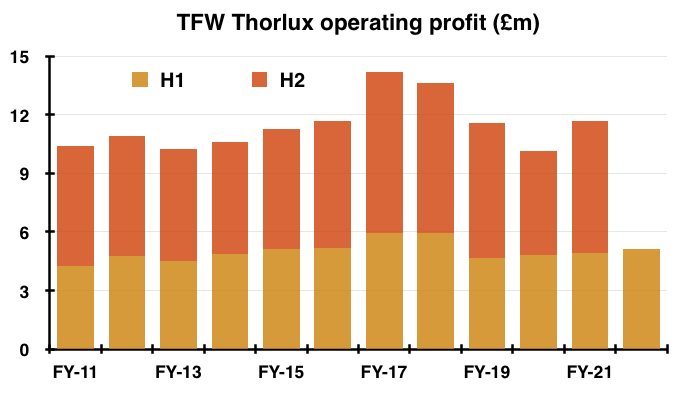

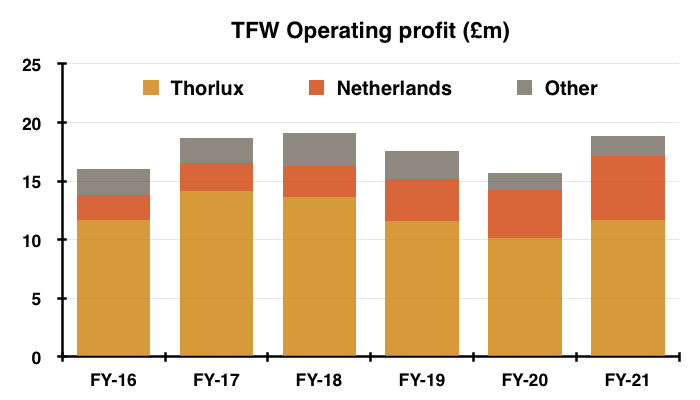

Thorlux

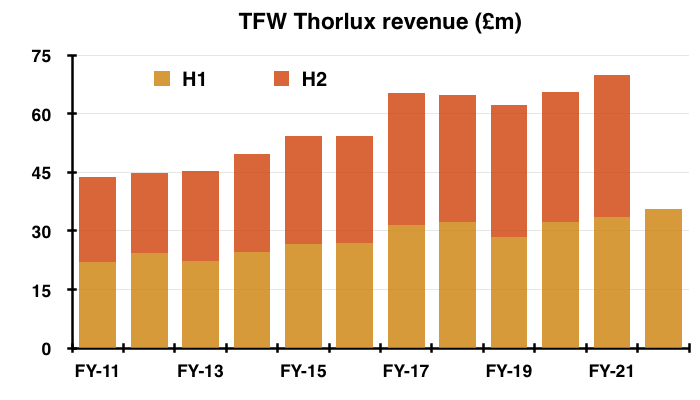

- Thorlux manufactures a wide range of professional lighting equipment and represents almost 60% of the group:

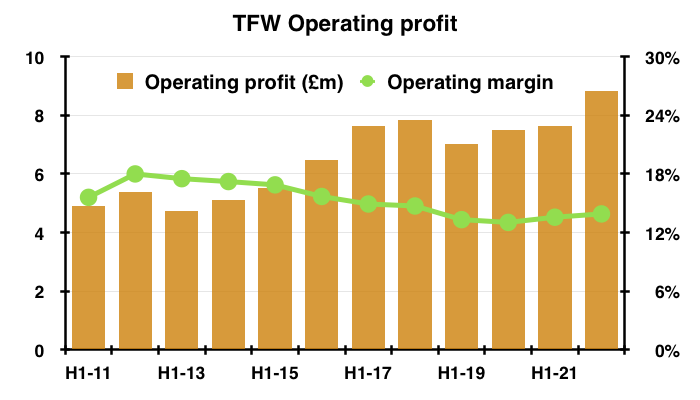

- Thorlux reported revenue up 6% and profit up 4% for this H1:

- Thorlux has experienced mixed longer-term progress.

- H1 divisional profit of £5.1m has not yet recovered to the level enjoyed during the LED boom of a few years ago, and was only 7% higher than the level witnessed for H1 2012.

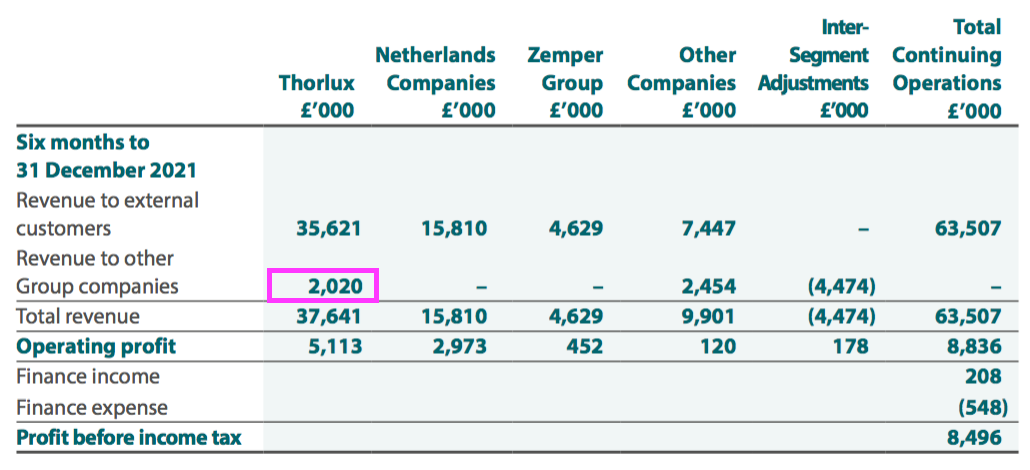

- Thorlux does supply products to different group subsidiaries, though, and the majority of profit generated when those products are sold to the customer may accrue to those different subsidiaries and not Thorlux.

- Products of £2m were sold to other subsidiaries during this H1, and the yearly figure has bobbed between £3m and £4m since FY 2017:

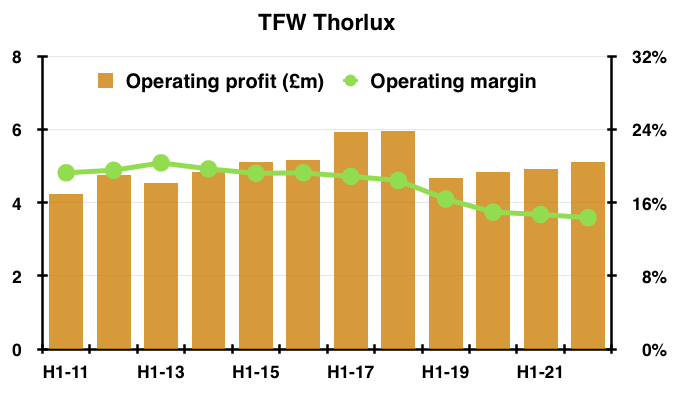

- Although new lights such as Flexbar, Visio, Blox and Kast alongside the SmartScan monitoring service…

- …have been able to push Thorlux’s sales higher, the division’s H1 margin has been trending lower for years:

- True, recent component supply issues will not have helped costs.

- But Thorlux’s H1 margin has reduced from 20% to 14% during the last ten years, and the reasons for the decline — perhaps greater development costs and/or growing pressure on pricing — have not really been made clear.

- Maybe the 2020 appointment of a new managing director can herald improved divisional profitability.

- The 2020 annual report (point 6) cited the new MD’s “continuous improvement techniques“:

“A new managing director, Peter Maxwell, has recently been appointed by the Group to lead Thorlux over the next few years, freeing some time for Mike Allcock to focus on product development, new technology and selling activities throughout the Group, as well as the drive into new territories.

Peter will use his expertise and experience to focus on continuous improvement techniques to provide further revenue growth and operating profit gains whilst harnessing the full force of Thorlux’s tremendous deep-rooted lighting knowledge.”

- Bear in mind the new MD is not a lighting expert. He trained initially as an auditor and worked previously for a door manufacturer.

- Perhaps Thorlux’s adverse margin trend explains why TFW’s strategy has evolved to include overseas acquisitions and, more recently, entry into other markets such as charging points for electric vehicles (see Zemper and Ratio).

- At least Thorlux’s development of energy-efficient lighting ought to pay off during the present climate of elevated energy costs.

- The 2021 annual report (point 2) provides a number of case studies of customers employing Thorlux to save energy.

- For example, the United Lincolnshire Hospitals NHS Trust now saves almost £400k a year following what seems to have been a £2.6m investment in new lighting:

“Thorlux SmartScan luminaires have delivered a 91% energy saving compared with the previous lighting installation, resulting in electrical operating savings of £398,570 per annum.

Claire Hall says, “The [United Lincolnshire Hospital NHS] Trust received a grant from the National Energy Efficiency Fund for £2.6 million, enabling the replacement of around 12,000 light fittings with modern LED fittings with smart technology that means lights turn off after a period of inactivity, saving energy and money for the Trust.”

- The payback on new Thorlux lighting may now be shorter, given TFW said within this H1 statement that Thorlux’s own electricity costs have “nearly doubled“:

“Planning permission has now been granted to complete the roll-out of a solar PV installation to the main Thorlux roof later this year, adding a further 3,000 panels to the 909 already installed; this is particularly opportune, considering that the electricity kWh price at Thorlux has recently nearly doubled.“

- Rising energy costs and greater demand for efficient lighting may well explain Thorlux’s bumper order book. This H1 statement revealed divisional orders were up 25% at the half-year point.

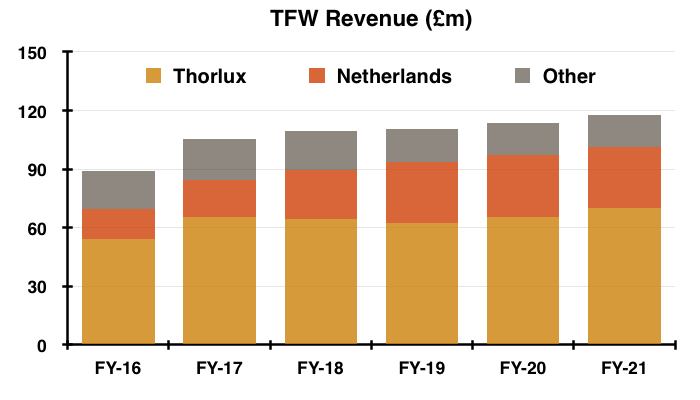

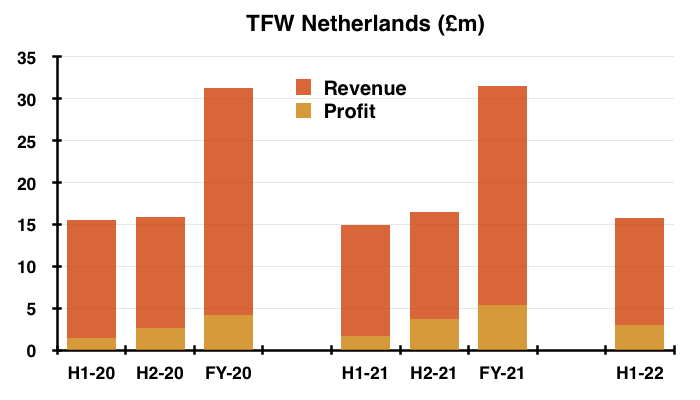

Netherlands

- TFW’s Dutch businesses — Lightronics and Famostar — represent approximately a third of TFW’s profit.

- Lightronics manufactures mostly street lighting and was acquired during FY 2015 for an initial £8.3m that included a £1.9m debt repayment.

- Famostar manufactures mostly emergency lighting and was acquired during FY 2018 for an initial £6.3m.

- Both Lightronics and Famostar appear to have flourished under TFW’s ownership.

- The charts below show their collective revenue and profit contributions to the group:

- Trailing aggregate Lightronics/Famostar revenue has reached £32m versus less than a combined £18m at the time of their purchases.

- Trailing aggregate Lightronics/Famostar operating profit has meanwhile surpassed £6m versus a combined £2.3m at the time of their purchases.

- The FY 2021 performance of the Netherlands division was extremely impressive given Lightronics suffered a fire during H1 2021:

- This H1 statement confirmed Lightronics should soon return from temporary facilities…

“The Lightronics building reconstruction, following the fire, is well advanced and on target, with completion planned for this summer.”

- Construction work at Famostar also seems positive for TFW shareholders:

“The Board has also approved expenditure to double the size of the building for Famostar, to support its continued rapid sales growth.“

- Total Dutch sales gained 5% during this H1 to nearly £16m but profit surged 76% to almost £3m.

- TFW said the profit advance was due to the absence of earn-out provisions:

- “Netherlands performance – positive performance, with improved profitability as a result of first year without earn-out provisions.”

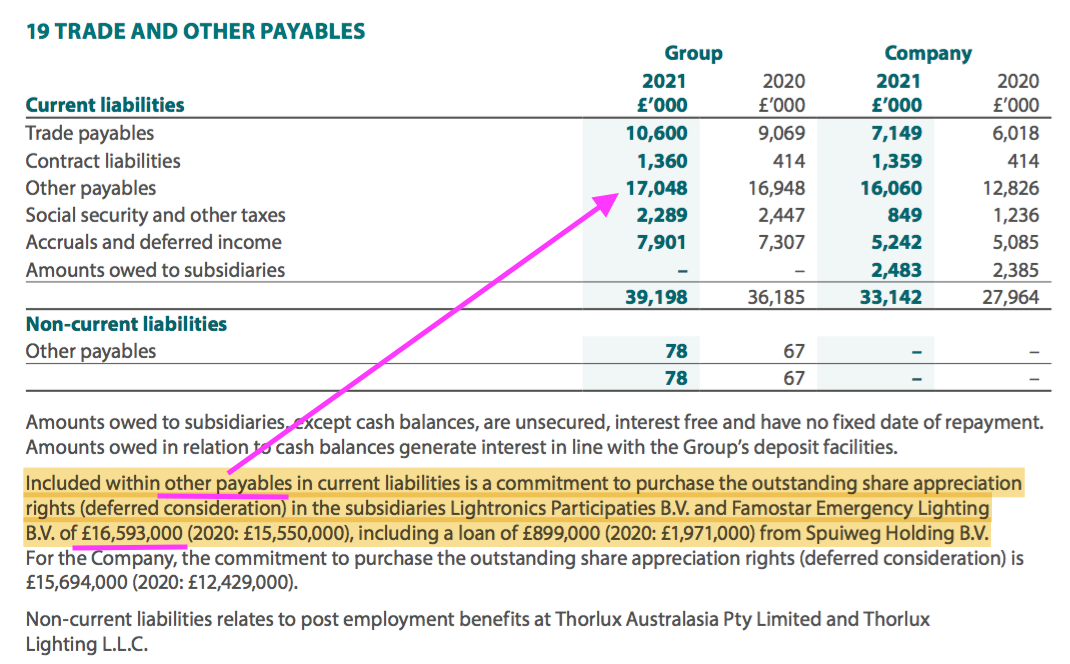

- TFW’s Dutch acquisitions included deferred earn-out payments based on the subsequent performances of the two subsidiaries.

- The 2021 annual report said the amount owed was £16.6m:

- This H1 revealed the final cash payment to be £15.3m:

“On 21 September 2021 the Group completed its commitment to purchase the outstanding share appreciation rights in the subsidiaries Lightronics Participaties B.V. and Famostar Emergency Lighting B.V. The settlement was executed by a cash payment of £15.3m (€17.9m) for the outstanding liability.“

- The £15.3m final payment was £1.3m less than the £16.6m estimate carried within the 2021 annual report.

- I get the impression any changes to the amount owed were taken through the income statement of the Dutch division, and so the £1.3m difference may have led to the sudden H1 profit jump to almost £3m.

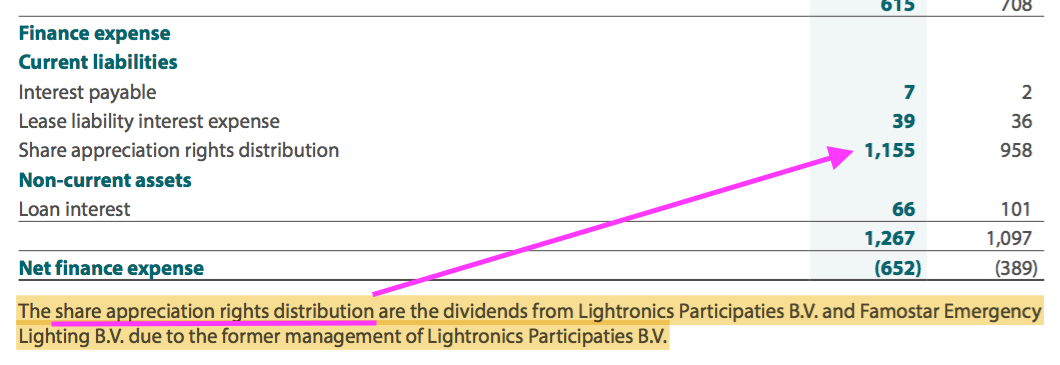

- At least the final payment will mean simpler Dutch accounts and no further dividends (£1m-plus for FY 2021) to the former owners of Lightronics and Famostar:

- TFW’s reported £3m Dutch profit equated to a handy 19% operating margin:

- Quite why the large, healthy and growing Dutch operation does not have any main board representation — when a far smaller UK subsidiary does — remains a mystery to me.

Zemper and Ratio

- Perhaps buoyed by the success of the Lightronics and Famostar acquisitions, TFW undertook two further European deals last year:

- Spanish emergency-lighting group Zemper purchased during October and;

- Dutch firm Ratio, which develops electric-vehicle charging systems, purchased during December.

- The Zemper deal was by far TFW’s largest, with £19.9m spent to acquire a 63% share that included cash of £5.3m.

- For perspective, the initial £19.9m payment exceeded TFW’s entire FY 2021 operating profit of £19.2m.

- TFW said within this H1:

“Zemper has already settled well into the Group, and, whilst it will remain an autonomous operation, Group companies have started to collaborate with Zemper in certain territorial markets and in the technical engineering of emergency lighting products.“

- Zemper’s three-month contribution to this H1 performance was revenue of £4.6m and profit of £0.5m:

- Three-month revenue of £4.6m points to annual Zemper sales of approximately £19m — which might be ahead of the €20m reported at the time of purchase.

- Three-month profit of £0.5m points to annual Zemper profit of approximately £2m — which seems well below the €3.8m reported at the time of purchase.

- The potentially lower profit could be due to the earn-out provision that TFW will pay for the remaining 37% of Zemper.

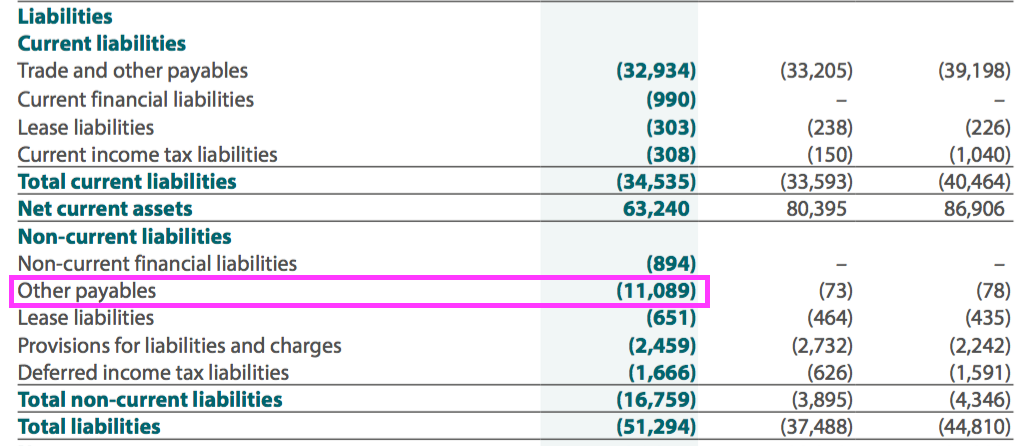

- TFW said the amount owed for the 37% was £16.1m and noted the sum was subject to “future performance conditions“.

- The balance sheet showed other payables of £11.1m, which I believe to be the £16.1m discounted to its net present value:

- The balance sheet now carries financial liabilities of almost £2m, which could be borrowings held by Zemper.

- The acquisition logic behind the Zemper deal — to extend the group’s emergency-lighting offering — is more straightforward than the rationale for the Ratio investment.

- At the time of the investment, TFW explained Ratio would extend the group’s activities beyond lighting into electric-vehicle charging:

“FW Thorpe’s know-how in electrical engineering, manufacturing and lighting, combined with Ratio’s experience in electrical vehicle charging will allow the introduction of new products into the UK market as well as supporting growth in Ratio’s existing markets.

We see similarities in technology and engineering skills, giving the Group the opportunity to diversify into new areas of engineering with high growth potential.“

- The original purchase announcement said TFW had paid £5.8m for 50% of Ratio.

- But this H1 statement disclosed TFW had paid only £4.8m, with a further £0.9m to be paid within two years.

- This H1 confirmed Ratio’s 2021 results were in line with expectations:

“As previously announced, in December the Group concluded its investment in a 50% interest in Ratio Electric, a Dutch manufacturer and supplier of electrical connection and distribution systems. Its results for 2021 are in line with expectations, and the Group is making progress on introducing Ratio Electric’s vehicle charging products into the UK.”

- TFW had previously expected Ratio to deliver 2021 revenue of €8m and a profit “in keeping with Group operating profit levels”.

- Whether the move into electric-vehicle charging generates margins akin to those enjoyed by Lightronics and Famostar (or even Zemper) remains to be seen.

- But what has become very clear is TFW’s desire to expand beyond the UK through notable purchases.

- Gross expenditure acquiring Lightronics/Famostar (approximately £30m), Zemper (possibly up to £37m) and 50% of Ratio (£6m) could eventually top £70m.

- In contrast, during the 20 or so years prior to buying Lightronics, TFW’s acquisitions were limited to a handful of smaller UK lighting firms for an approximate £5m total.

- The collective performance of TFW’s smaller UK outfits during this H1 possibly explains why the group prefers to concentrate on larger overseas operators.

Other companies

- TFW’s Other companies consist of:

- TRT Lighting, which was launched during FY 2012 and supplies lighting for road tunnels;

- Philip Payne, Solite and Portland, which supply emergency lighting, cleanroom lighting and shop lighting respectively, and;

- A trio of overseas Thorlux offices.

- By far the best performing Other company is TRT Lighting, which has gone from nothing to sales beyond £10m during the last ten years.

- The 2021 annual report (point 3) provided an optimistic snippet on TRT’s immediate prospects:

“Revenue has been boosted by a large scale tunnel refurbishment project on the M25 motorway and the company’s continued support of large scale rail projects in conjunction with Thorlux. TRT expects further tunnel projects to be given the go-ahead in 2021/22 and demand in street lighting to be maintained.”

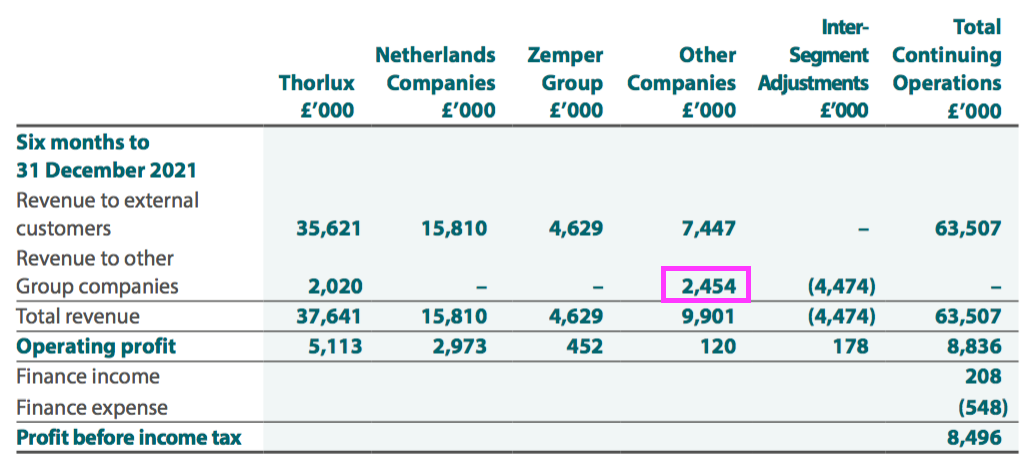

- But the remaining Other subsidiaries seem to have stagnated and, together with TRT Lighting, contributed a tiny £120k profit during this H1:

- I assume Philip Payne, Solite and Portland are kept on by TFW primarily because they supply products to Thorlux and the Dutch businesses:

- I do wonder if Philip Payne, Solite and Portland actually made any money during this H1.

Financials

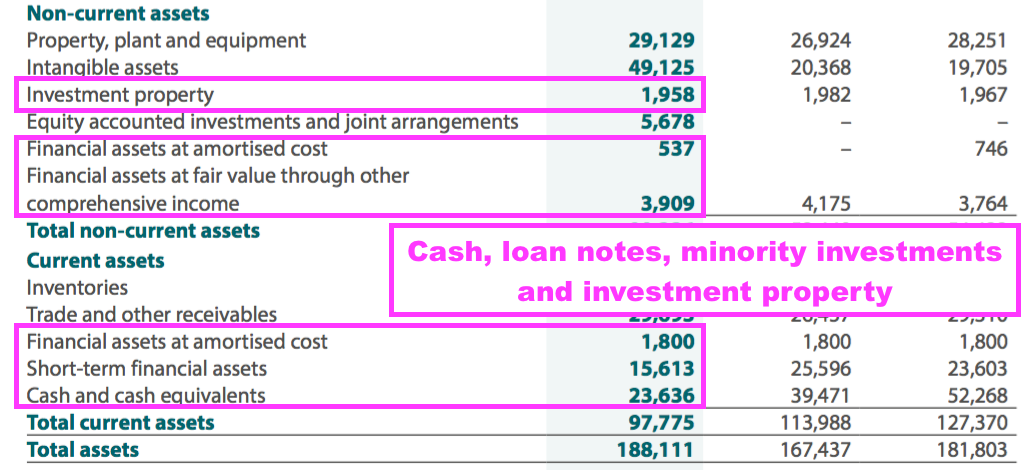

- TFW’s accounts remain flush with cash despite the payments for Lightronics/Famostar (£15m), Zemper (£20m) and Ratio (£5m).

- Cash and short-term deposits ended the half at £39m, while “financial liabilities” (possibly borrowings associated with Zemper) were less than £2m.

- TFW operates with a high cash balance to reassure customers, suppliers and shareholders (point 11):

“The Group’s policy has been to maintain a strong capital basis in order to maintain investor, customer, creditor and market confidence. This sustains future development of the business, safeguarding the Group’s ability to continue as a going concern in order to provide returns for shareholders and benefits for other stakeholders.

The Group has a long-standing policy not to utilise debt within the business, providing a robust capital structure even within the toughest economic conditions.“

- TFW’s balance sheet also carries investment property of £2m (point 18), a long-standing loan note of £2m (point 19) and an investment portfolio of £4m (point 20):

- Cash conversion looked very satisfactory. H1 operating cash flow of £11.6m less tax of £2.7m and capex of £2.4m meant reported earnings of £6.9m translated into free cash of £6.5m.

- The £15.3m Dutch earn-out, the £19.9m paid for Zemper, the £5.3m cash acquired with Zemper, the £4.8m invested in Ratio and the £7.6m spent on dividends then ensured total cash finished the half £36.6m lighter than the preceding year-end.

- The 2.27p per share special dividend will cost £2.7m and will not make a great dent in the £39m cash position.

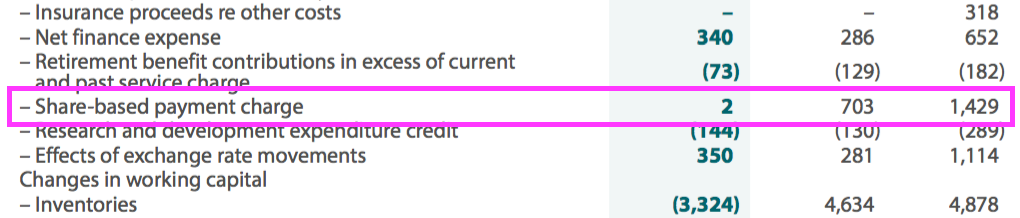

- The cash flow statement revealed a much lower share-based payment charge, which may reflect the absence of the Dutch earn-out provisions:

- Cash flow also incurred a lower £73k catch-up pension-scheme contribution.

- Although TFW’s final-salary pension scheme sports a small £2m surplus, contributions may have to be increased to maintain last year’s paid benefits of £2.6m if asset returns are poor (point 23).

- The preceding FY 2021 balance sheet had carried stock of £20.4m — the lowest since FY 2016 and, at 17.3%, the lowest proportion of annual revenue since FY 2008 (16.7%).

- At the time the low stock levels reflected “severe shortages and rising costs for many of the basic components necessary for making Group luminaires, such as steel, plastics, cardboard, electronic components and microchips.

- But this H1 provided some optimism by revealing “supply chain issues [are] easing, to some extent, especially for commodity items like steel and cardboard.“

- Indeed, TFW investing a further net £3m into stock during this H1 implied component shortages are no longer as severe as they once were. Stock ended the half at £27m, TFW’s highest level ever.

- The mix of divisional profit performances led to a rather average 13.9% H1 group operating margin:

- The group’s H1 margin has sadly not yet recovered to the 17-18% level achieved a few years ago.

Valuation

- TFW’s outlook felt positive but acknowledged the economic environment:

“Most Group companies are looking forward to an improved second-half performance…. Within the Group we are, however, mindful of significant cost inflation for purchased items as well as increases for labour and utilities. We have increased our prices in the market to compensate, but are only now starting to see the positive effects.”

…

“Supported by the Group’s healthy order book, I foresee a good second-half revenue performance, provided the component shortages continue to improve. Operating results remain the focus and will improve once the recent headwinds experienced for most businesses subside.“

- Lifting prices to cover higher costs could mean margins may recover at Thorlux and the Other companies.

- Trailing twelve-month revenue and profit excluding Zemper are £120m and £20m respectively.

- Assuming revenue of £19m and profit of £2m from Zemper (and 100% ownership), total revenue and profit comes to £139m and £22m respectively.

- Applying the forthcoming 25% UK tax rate then gives earnings of £16m or 14.1p per share.

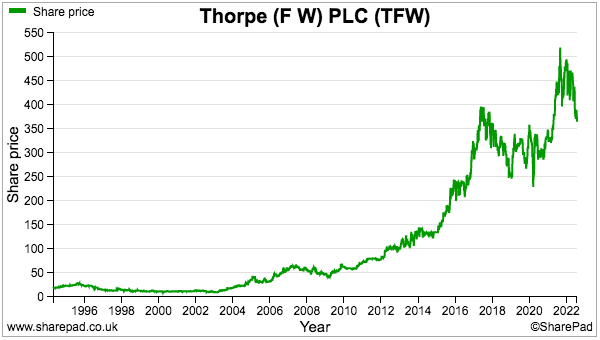

- The implied 27x rating at 375p appears generous given the modest progress during recent years.

- Between FYs 2016 and 2021, sales and profit have expanded at approximately 4-6% per annum. Between FYs 2014 and FY 2019 (i.e. pre-pandemic), TFW’s growth rate was approximately 10% per annum.

- This year’s rough market for many smaller shares leaves the 27x rating somewhat exposed, too.

- The calculations could be fine-tuned further for the cash position (£39m), Zemper earn-out (£11m) and all those other financial assets and liabilities (approximately £6m), but such adjustments will not make a significant difference to the £439m market cap.

- Perhaps investors are still willing to apply a premium multiple because of TFW’s:

- Operating resilience displayed during the pandemic;

- Possible desire to acquire further overseas businesses;

- Positive comments about current trading, and/or;

- Growth opportunities beyond traditional lighting systems (e.g. SmartScan, vehicle charging points).

- TFW’s ‘ESG’ angle may also be an important attraction. This H1 said:

“Just before Christmas, external third-party auditors completed an assessment of the Group’s carbon emissions and I am pleased to report that the Group is considered carbon neutral for its manufacturing operations. Within the Group we continue with vigour, nonetheless, to improve further ourenvironmental credentials, with targets set for all Group companies”

- The 2021 annual report (point 6) devoted several pages to environmental matters:

- A SharePad search through the RNS for ‘LED lighting’ shows plenty of quoted companies that may well be (or become) TFW customers:

- While the impact of the “healthy” order book, Zemper acquisition and greater interest towards energy-efficient lighting are awaited within the forthcoming FY 2022 results, the trailing 5.85p per share ordinary dividend supplies a 1.6% income at 375p.

Maynard Paton

Thanks very much Maynard for another excellent analysis. Perhaps one other reason investors may allow the premium multiple to remain is the perception that Thorpe’s management is able to successfully execute the “serial acquirer” business model which, in a sector such as this, tends to create an almost limitless runway of growth. The lack of reliance on large and distant manufacturing facilities in Asia is also proving to be a benefit as worldwide logistic problems persist. It also looks as though the company has not been badly affected by inflation. It is interesting to compare this with a company like XP Power where issues such as component availability, logistic costs and general inflation appear to be having a much greater impact.

Hi John

Thanks for the message. Yes, I should have worded the text “Possible desire to acquire further overseas businesses;” a little better to include the potential for a ‘buy and build’ approach that Halma (and others) have adopted successfully. I did write about that possibility in a bit more detail in my previous TFW review (here) Good point on the local manufacturing, which is working in TFW’s favour. TFW has suffered some component issues, and has had to promptly redesign products to compensate. But as you say, the company seems to be coping relatively well with the wider logistical problems.

Maynard

FW Thorpe (TFW)

Clarification of earn-out provisions

I have contacted TFW to clarify the earn-out situation. I missed the following line from the 2021 annual report that explained what had occurred:

“The operating results were further suppressed by the provision of an additional £1.5m (2020: £2.0m) to finalise the pay-outs on the Lightronics and Famostar earn-outs due to the continuing success of both businesses. These payments have been made during September 2021.

I noticed the same line within the 2018 report (point 21) but frustratingly did not realise the additional earn-out provisioning was suppressing reported Dutch profit.

Anyway, additional Dutch earn-out provisions for FYs 2017-2021 were £0.9m, £1.5m, £2.2m, £2.0m and £1.5m. Reported Dutch profit with the provision added back were therefore £3.3m, £4.2m, £5.8m, £6.1m and £6.9m assuming the entire provision was accounted for as an operating cost (in reality the provision is spread between operating costs and financing expenses). I already knew the Dutch businesses had performed well since their respective purchases, but adjusting for the earn-out provisions confirms they have in fact performed really well.

TFW also confirmed there was no over-provisioning before the actual cash earn-out payment and so the £3.0m Dutch profit for H1 2022 is a ‘genuine’ number.

Zemper’s reported profit was reduced due to amortisation charges and the three-month contribution covering the slow Christmas period. Earn-out provisions for Zemper are apparently unlikely to be as significant as those of the Dutch businesses.

Maynard

FW Thorpe (TFW)

Acquisition published 26 September 2022

News of what appears to be a sensible acquisition that extends TFW’s European expansion. Here is the full text:

——————————————————————————————————————

FW Thorpe is pleased to announce the acquisition of 80% of the share capital of SchahlLED Lighting in Germany, a turnkey provider of intelligent energy saving lighting products for the industrial and logistics sector.

The acquisition is expected to enhance earnings per share in the financial year ending 30 June 2023, solidifying our business in Germany and providing further growth opportunities.

FW Thorpe has paid an initial consideration of €14.6m (circa £12.8m) and could pay an additional amount to be determined by SchahlLED’s EBITDA performance in the year ending 30 June 2023.

The initial consideration has been funded from the Company’s existing cash reserves, these reserves and the cash generated from SchahlLED over the next few years will fund the purchase of the remaining share capital in the future.

The senior management team will remain in the business and report directly to the board of Thorlux Lighting.

About SchahlLED

SchahlLED Lighting is a turnkey provider of intelligent LED solutions for the industrial and logistics sectors with more than 50 years of lighting and 20 years of LED experience currently employing 26 people.

The company is based in Unterschleißheim near Munich and has sales offices in Cologne and Weyhe close to Bremen. It is active in Germany, Austria, Switzerland and Poland. As both manufacturer and full-service provider, SchahlLED plans lighting concepts and supplies intelligent LED lighting systems.

With an extensive network of sales and service partners, SchahlLED completes more than one hundred projects annually. SchahlLED and Thorlux have worked together since 2019 distributing SmartScan products primarily into the German market. For more information visit http://www.schahlled.de

During the last financial year ending 31 December 2021, SchahlLED achieved revenues of €15.9m with EBITDA of €2.8m. Net assets as at 31 December 2021 were €3.5m.

The addition of SchahlLED will further strengthen the Group’s presence in Europe and provide opportunities for the Group to grow SmartScan revenues into Germany and other selected European territories.

Chairman, Mike Allcock commented:

“I would like to welcome the SchahlLED team to the Group. We aim to build upon our successful partnership, distributing our market leading SmartScan products into Germany and surrounding areas and continuing to grow our presence across Europe.

We are looking forward to the opportunity to generate further value for our shareholders by building on the success of this partnership for years to come.”

——————————————————————————————————————

TFW’s European expansion continues, this time moving into Germany to complement operations acquired within the Netherlands and Spain.

Cost of €14.6m for 80% equals €18.3m for 100%, which versus Ebitda of €2.8m is in line with past acquisitions at 6-7x Ebitda.

Net cash at the last count topped £30m, so funding the €14.6m is not a problem.

A 50-year history and 20 years with LEDs suggest an established operator. Just 26 employees, too, which with revenue of €15.9m gives revenue per head of £13.9m/26 = a super £536k. So this business makes high-spec equipment.

Another positive is TFW having worked with SchahlLED for three years before purchase. I guess those three years provided good insight into SchahlLED that ought to bode well for a smooth integration.

Maynard