***SharePad 25% OFF Special Offer***

Use promo code mp25 to claim your 6-month discount. Click here for details. #ad

25 August 2022

By Maynard Paton

Another month and another round of ‘back to basics’ filtering.

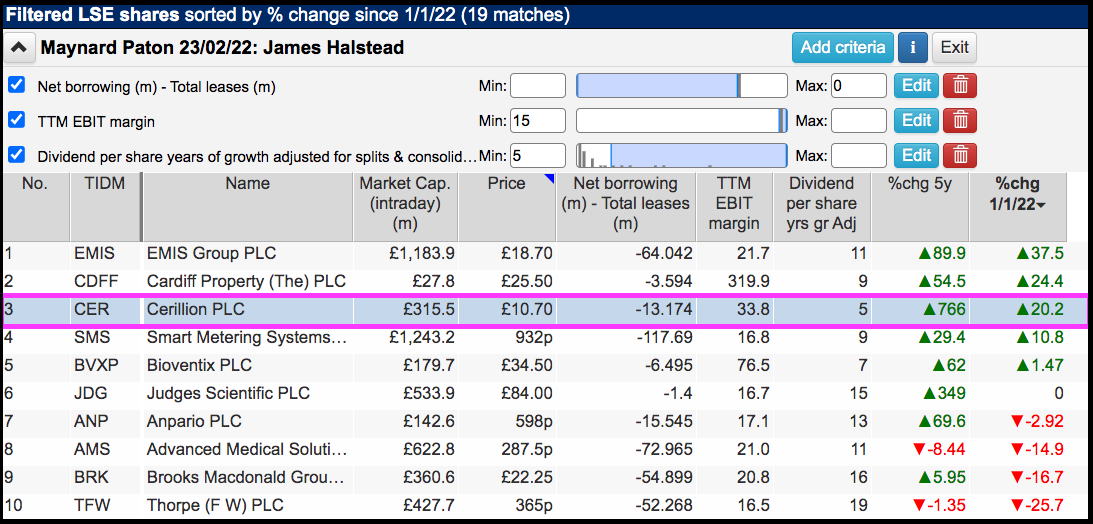

Introduced earlier this year to identify James Halstead, this screen shortlists companies that offer cash-flush balance sheets, robust margins and dependable dividends. SharePad returned 19 matches:

I selected Cerillion because the shares were among the few on the shortlist to have moved higher this year. I passed on EMIS and Cardiff Property because the former was subject to a bid and the latter was too small.

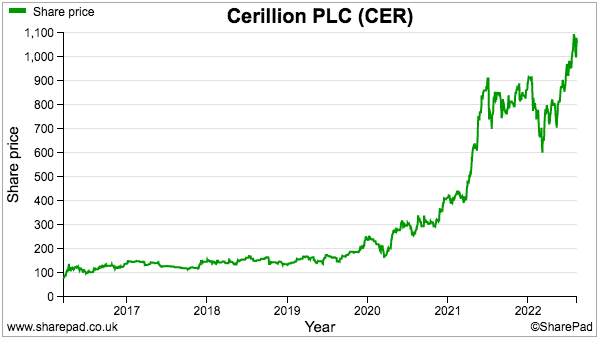

Cerillion’s shares have actually five-bagged since the pandemic lows of March 2020 and remain very close to their £11 all-time high:

Let’s take a closer look.

Read my full Cerillion article for SharePad.

Maynard Paton

Hi Maynard

Great work.

My question relates to the Sharepad Adjusted EPS forecast for FY22 of 28.2p for CER.

For the six months ended 31 March 2022, CER reported Adjusted EPS of 18.6p

To end the year with 28.2p, 2H22 Adjusted EPS will need to decline by a third year-on-year.

What is the thinking behind such a dismal 2H?

Your valuation-based conclusion on CER using the Sharepad forecasts seem sensible…but less sensible if Sharepad has made a glaring error?

Looking forward to your feedback.

Regards

Eric

Hi Eric

Thanks for the message. I can only guess the weaker H2 relates to the timing and recognition of CER’s ‘lumpy’ contract-work income, whereby for FY22, H1 looks to have been strong for such revenue and H2 just may not be as strong. A growing cost base may also be a factor, whereby resources taken on to undertake future contracts are expensed but have no associated revenue at present.

The forecasts for FYs 23 and 24 show further 20%pa EPS growth, so the FY22 forecast does not seem a glaring error (at least to me). Best to do your own research though, just to make sure!

Maynard