28 June 2022

By Maynard Paton

Results summary for S & U (SUS):

- A “lower than normal” bad-debt provision underpinned a record full-year profit, which in turn supported fresh highs for net asset value (NAV) and the dividend.

- Very mixed signals are emerging from the main motor-loan division, with encouraging collection rates offset by “a more heightened risk of an adverse economic environment” and higher expected write-offs among new loans.

- Further surplus cash from the motor-loan division was redirected into the property-loan subsidiary, which reported a bumper performance and prompted optimistic near-term management predictions.

- ROCE levels remain modest and suggest SUS’s inherent value is biased towards the asset value of its loan book rather than annual earnings.

- Despite current-year profit running “above budget“, the £21 shares trade at 1.24 times NAV and offer a 6% yield. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own SUS

- Results summary

- Revenue, profit, net asset value and dividend

- Advantage Finance: Loan provisions

- Advantage Finance: Collections and credit quality

- Advantage Finance: Payment holidays

- Advantage Finance: New loans

- Aspen Bridging

- Financials

- Valuation

News links, share data and disclosure

News: Annual results, presentation and webinar for the twelve months to 31 January 2022 published/hosted 29 March 2022 and AGM trading update published 26 May 2022

Share price: 2,100p

Share count: 12,150,760

Market capitalisation: £255m

Disclosure: Maynard owns shares in S&U. This blog post contains SharePad affiliate links.

Why I own SUS

- Provides ‘non-prime’ credit to used-car buyers and property developers, where disciplined lending and reliable service have supported an enviable dividend record.

- Boasts veteran family management with a 40-year-plus tenure, 42%-plus/£107m-plus shareholding and a “steady, sustainable” and organic approach to long-term growth.

- Very promising property-loan subsidiary offers the prospect of improved progress post-pandemic.

Further reading: My SUS Buy report | All my SUS posts | SUS website

Results summary

Revenue, profit, net asset value and dividend

- Positive statements during December…

“The Group continues its growth rebound and is trading strongly, as the economy tentatively returns to normal despite the continuing uncertainty over the course of the Covid pandemic. Growth is accelerating in both businesses, despite a relative lack of used car supply and a quieter housing transaction market over the past quarter.”

- …and February…

“Founded on an excellent collections and debt quality performance and the expected rebound in sales as the Covid pandemic gradually abates, S&U’sprofit before tax for the year is now set to exceed current consensus expectations.”

- …had already indicated these FY 2022 figures would trumpet a substantial improvement on the pandemic-disrupted FY 2021.

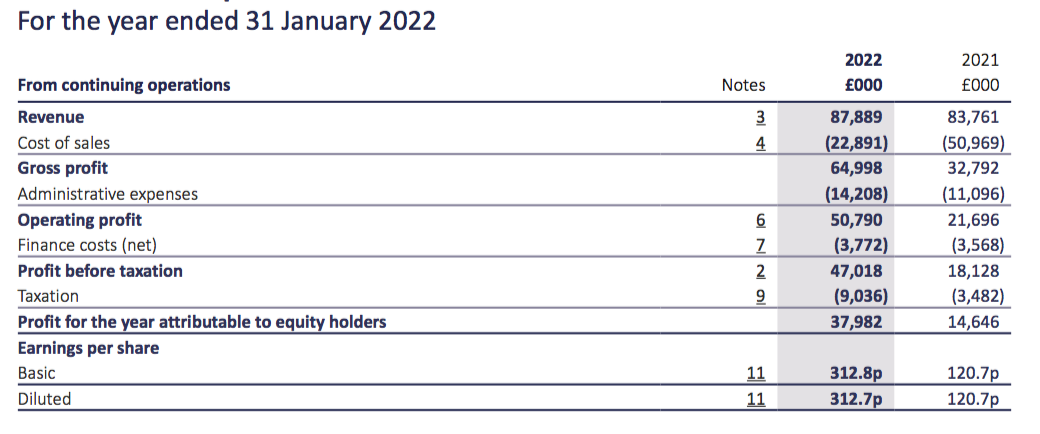

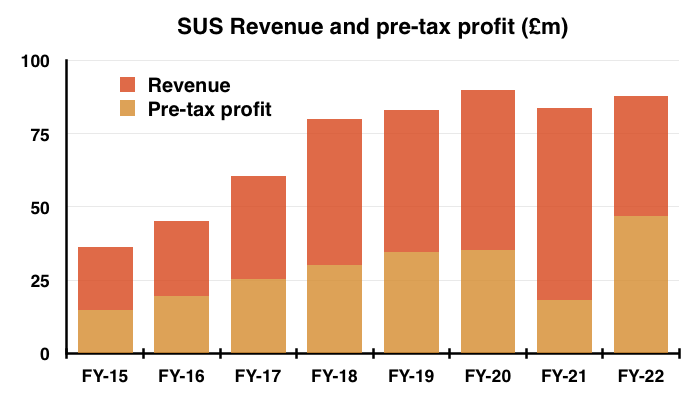

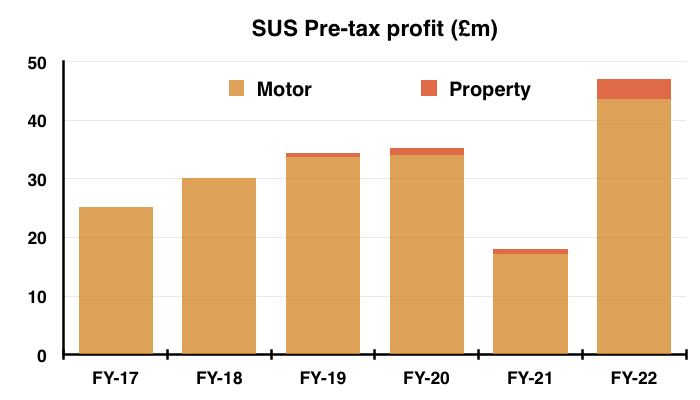

- Revenue improved 5% to £88m but pre-tax profit more than doubled to £47m to set a new full-year record:

- The profit surge followed a “lower than normal loan loss provisioning charge” for potential bad debts.

- The comparable FY 2021 suffered an additional Covid-related loan provision of £20m, while this FY’s entire provision was only £4m following “good collections and less utilisation of the impairment provisions made in the dark days of January 2021″.

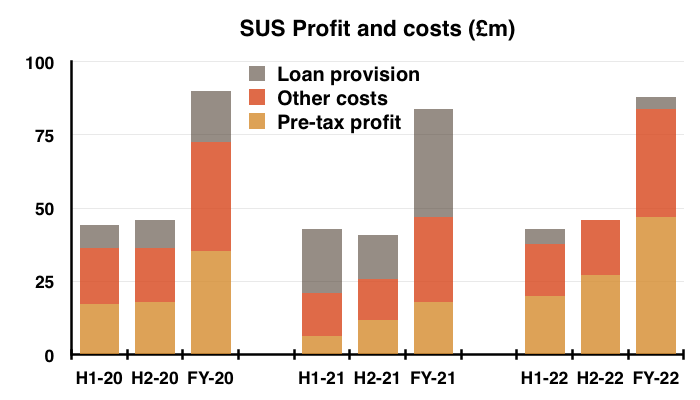

- The loan provision for H1 2022 was £5m, meaning H2 recorded a £1m provision write-back:

- The provision fluctuations related entirely to Advantage Finance, the group’s motor-loan subsidiary (see Advantage Finance: Loan provisions).

- Management confirmed during the results webinar the £4m motor-loan provision was not sustainable, and indicated a return to the £16-17m yearly motor-loan provisioning that occurred prior to the pandemic.

- The ultra-low provisioning for this FY therefore flattered the group’s performance and financial ratios.

- SUS’s property-loan division, Aspen Bridging, meanwhile enjoyed a bumper profit following its involvement with the Coronavirus Business Interruption Loan Scheme (CBILS) (see Aspen Bridging).

- Group profit continues to be dominated by Advantage Finance…

- …although management disclosed during the results webinar that Aspen could grow to represent 20% of group profit during the “next few years“.

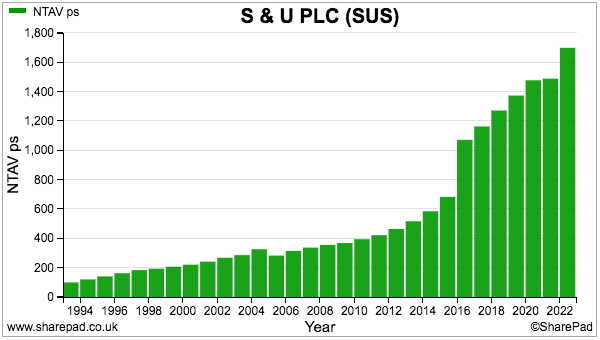

- The performance increased net asset value (NAV) by £26m to £206m — equivalent to £17.02 per share and a fresh NAV record:

- NAV per share has gained 46% during the last five years and now represents 81% of the share price (see Valuation).

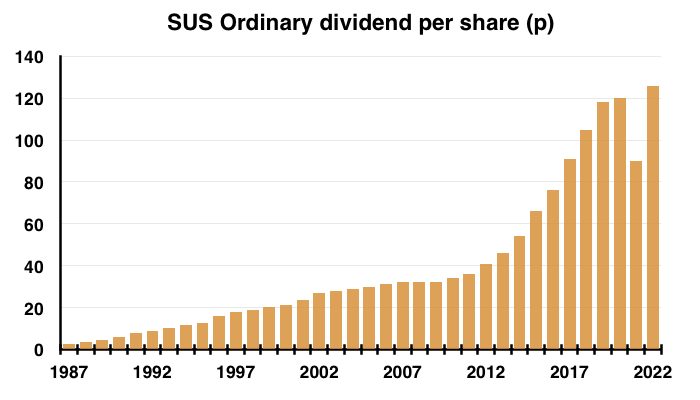

- SUS lifting the H1 dividend by 50% did indeed imply the business had passed the worst of the pandemic.

- SUS took the average earnings reported for FYs 2021 and 2022 to determine the full-year payout:

“We have reflected this [belief] at S&U in a longstanding dividend approach which aims at seeing dividends twice covered. Taking the past two years as a whole earnings per share have averaged just over 216p thus implying a total dividend of 126p per ordinary share this year (2021: 90p)”

- The final dividend was therefore lifted 33% to 57p per share to arrive at the full-year payout of 126p per share — a new record:

- Companies House shows the payout having rallied 50-fold since 1987.

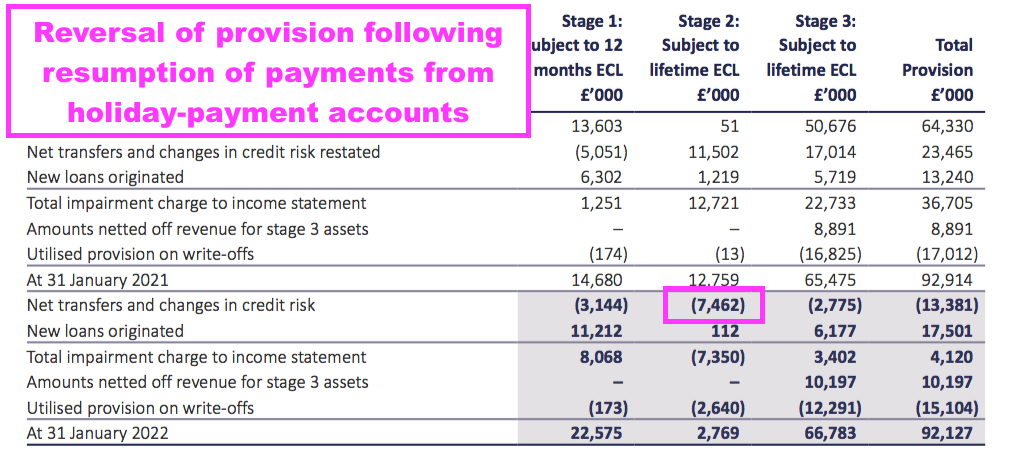

Advantage Finance: Loan provisions

- SUS describes Advantage Finance customers as ‘non-prime’ and the 2022 annual report outlines their typical circumstances:

“This long [21-year] experience has enabled Advantage to gain a significant understanding of the kind of simple hire purchase motor finance suitable for customers in lower- and middle-income groups.

Although decent, hardworking and well intentioned, some of these customers may have impaired credit records, which have seen them in the past unable to access rigid and inflexible “mainstream” finance products.”

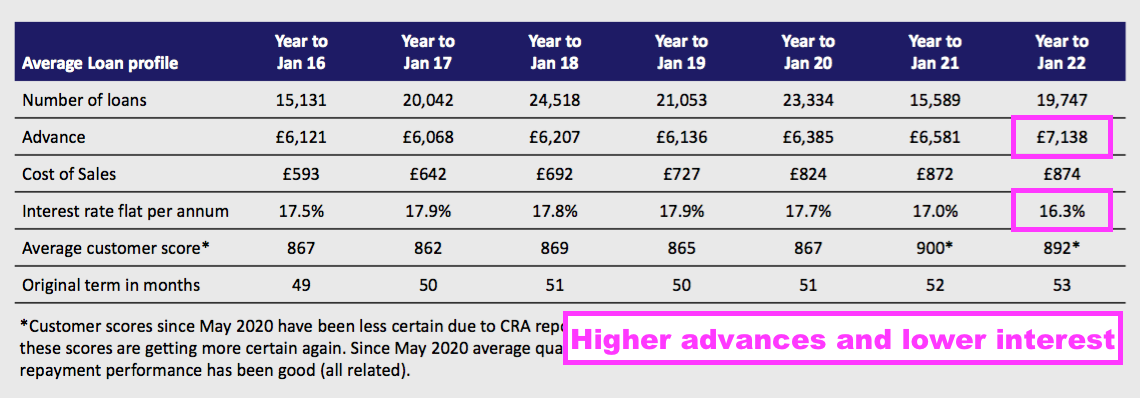

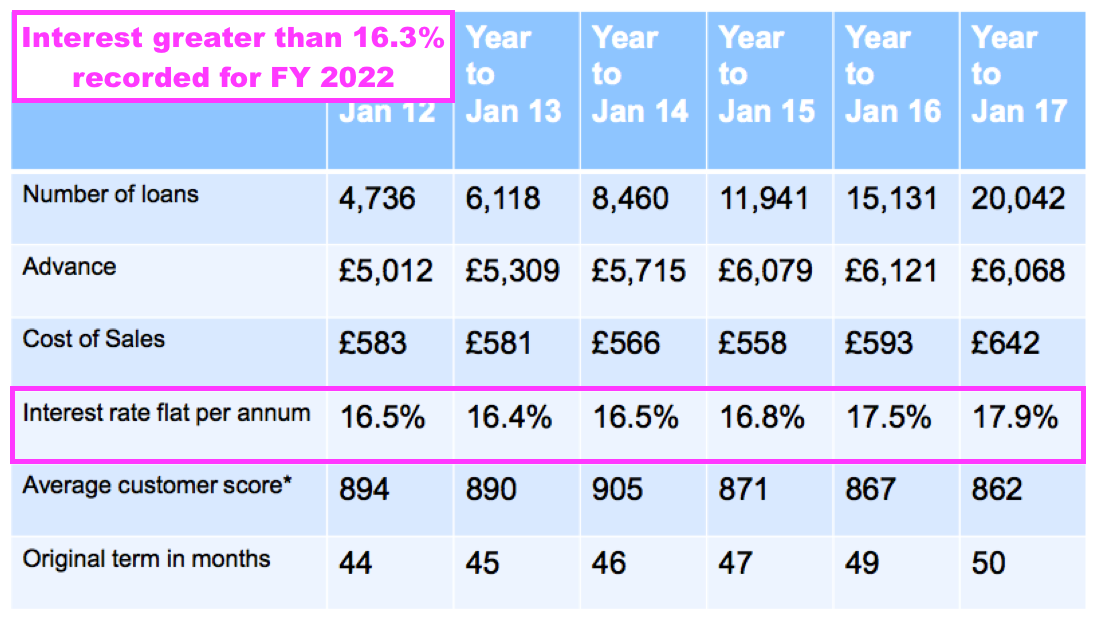

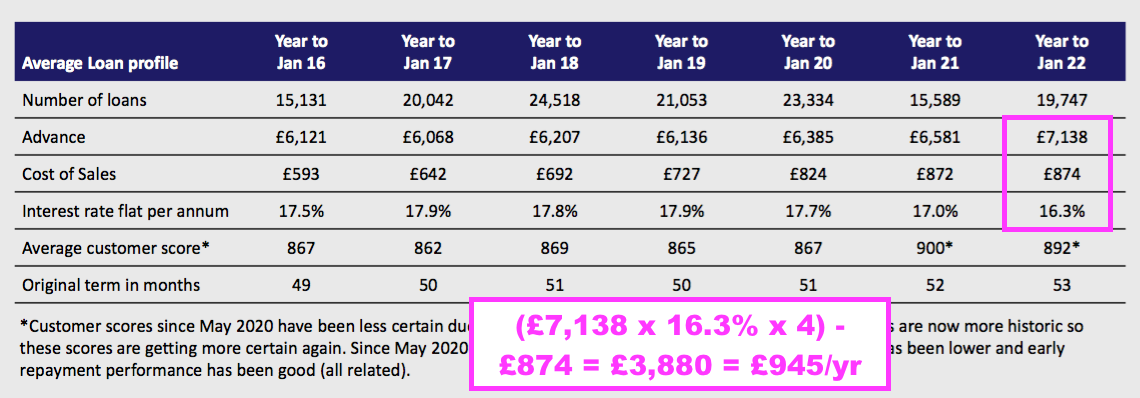

- Advantage borrowers previously took on motor loans of approximately £6.3k, but rising used-vehicle prices have increased the average loan to £7.1k:

- The flat 16.3% interest rate charged by Advantage during FY 2022 was the lowest for at least ten years:

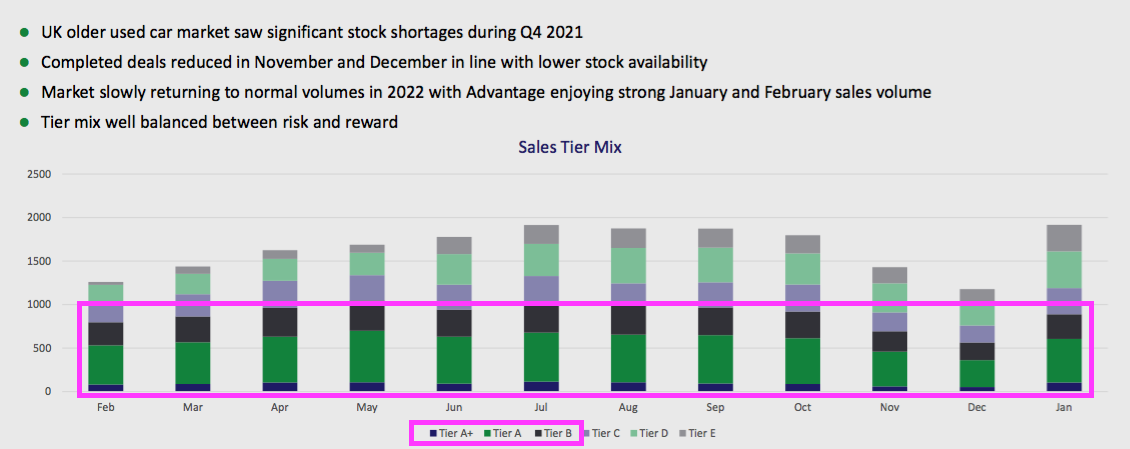

- Management remarked during the results webinar the lower rate was due to a higher proportion of lower-risk Tier A+/A/B customers:

- Borrowing £7k at a flat 16.3% a year over 53 months leads to interest of £5k and a total repayable figure of £12k before administration and other fees.

- Before the pandemic, the typical Advantage borrower eventually repaid almost £10k of that £12k. But I estimate the eventual repayment fell to less than £9k during the pandemic.

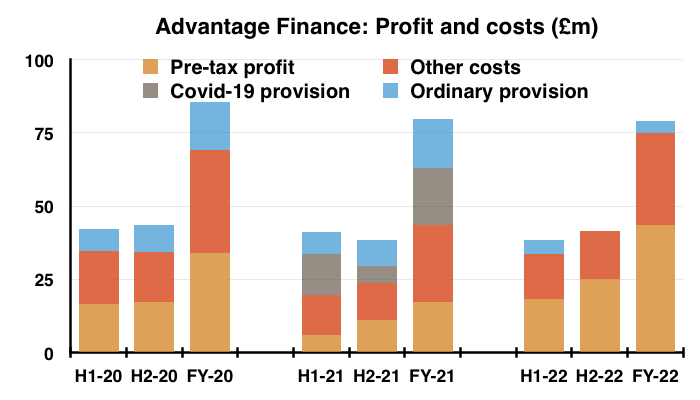

- The chart below shows the impact of the extra £20m Covid-19 bad-debt provision (grey boxes) on Advantage’s profit during the comparable FY 2021:

- The ordinary provision (blue boxes) was between £16m and £17m for FYs 2019 and 2020, versus only £4m for this FY 2022.

- A pre-pandemic £17m impairment for this FY would have increased Advantage’s loan provision by £13m and reduced group pre-tax profit from £47m to £34m — equal to that recorded for FYs 2019 and 2020.

- Total Advantage provisions during FY 2021 (£36m) and FY 2020 (£4m) came to £40m, or a £20m average for the two years.

- The two-year £20m average is £3m higher than the pre-pandemic annual £17m impairment.

- Whether ‘normal’ provisions from here will run at £17m (as per management comments during the results webinar) or £20m is hard to say.

- But this small-print within the 2022 annual report is not encouraging:

“The macroeconomic overlay assessments for 31 January 2022 reflect that further to considering such external macroeconomic forecast data, management have judged that there is currently a more heightened risk of an adverse economic environment for our customers and the value of our motor finance security.“

- Furthermore, inflation is now considered within the provisioning sums:

“Inflation rates have not previously been factored into the macroeconomic overlay but at 31 January 2022 we have included them due to the extraordinary increases currently forecast for the next 12 months period and the potential impact on our customers and their repayments…

An increase by 0.5% in the weighted average inflation rate would result in an increase in the impairment loss by £401,572. A decrease by 0.5% would result in a decrease in the impairment loss by £401,572.”

- The upshot is higher expected write-offs among new loans.

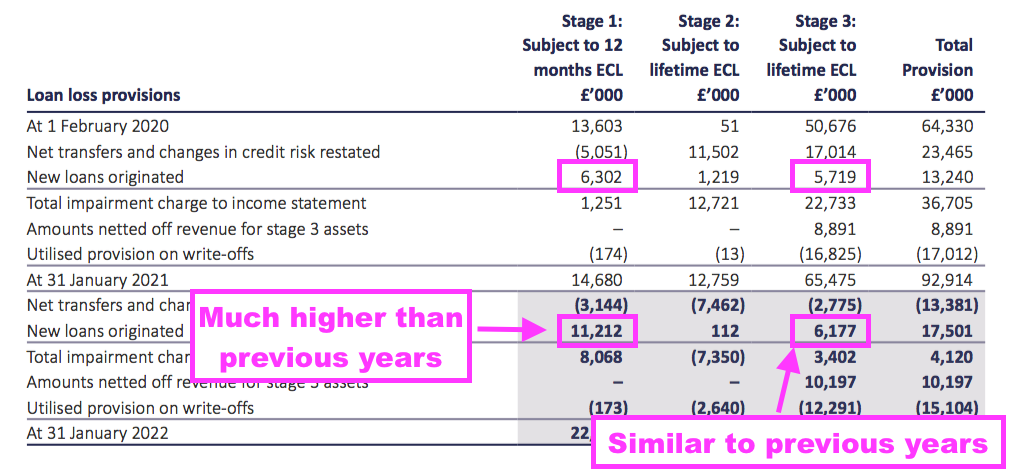

- SUS’s loan provisions are classified as:

- Stage 1, which reflect expected write-offs from newly opened accounts (i.e. accounts without any history of arrears);

- Stage 2, which essentially reflect expected write-offs from accounts that enjoyed an FCA-mandated payment holiday (i.e. accounts that are technically in arrears), and;

- Stage 3, which reflect expected write-offs from accounts in arrears due to missed payments.

- New loans attracted an £11m Stage 1 provision during the year, much higher than the £6m or so applied during the preceding three years:

- Note that the £11m Stage 1 provision is an estimate of expected write-offs, and only future results will show whether this Stage 1 estimate leads to higher actual defaults.

- At least the Stage 3 provision on new loans for this FY matched the levels of previous years at £6m, suggesting new accounts are not defaulting beyond historical norms.

- The higher £11m Stage 1 provision was counterbalanced by a £7m reduction to Stage 2 provisions. This £7m reduction reflected the resumption of payments by most borrowers who enjoyed payment holidays during the pandemic:

- SUS’s talk of “a more heightened risk of an adverse economic environment” alongside that higher Stage 1 provision suggests motor-loan provisions for FY 2023 may be greater than the £17m witnessed before the pandemic.

- The additional Covid-related provisions from FY 2021 still sit on the balance sheet.

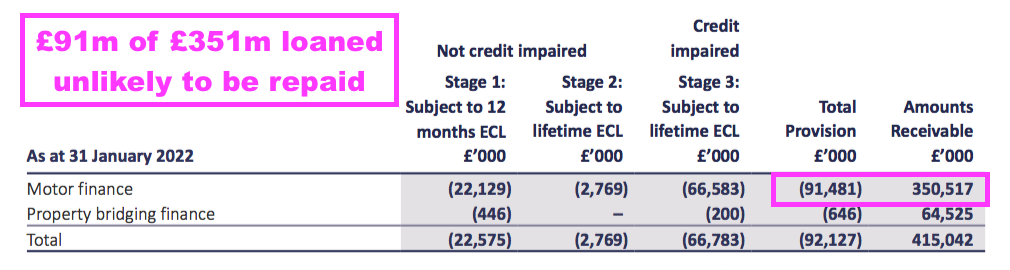

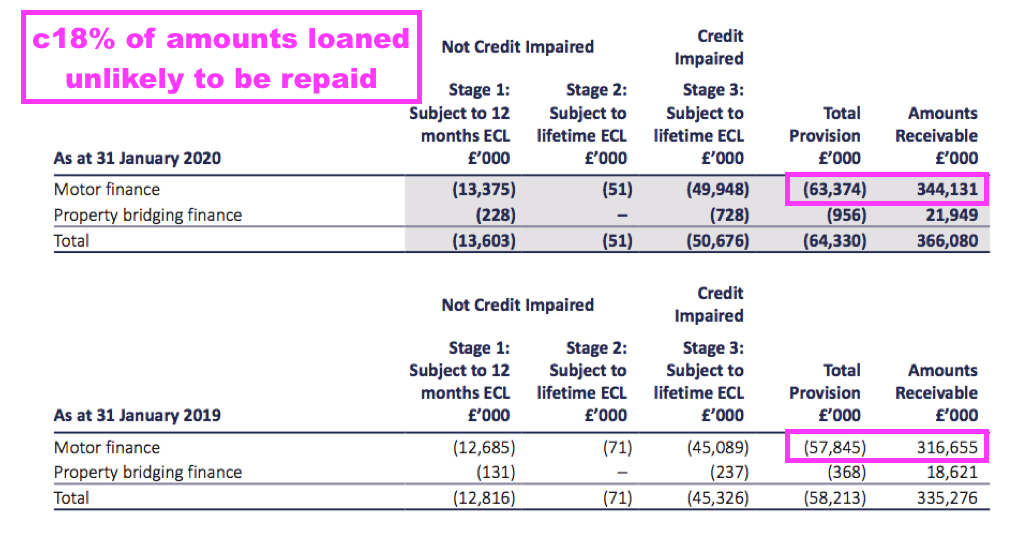

- At FY 2020 (i.e. just before the pandemic), Advantage had lent £344m to customers of which £63m, or 18%, was provided for as a bad debt to leave the net amount receivable at £281m:

- For this FY 2022, a bad-debt provision of £91m represented 26% of the total £351m loaned:

- Given SUS said additional Covid-related provisions were £20m during FY 2021, the total non-pandemic provision could be £71m (£91m less £20m).

- A £71m provision versus the £351m total loaned is 20% — higher than the 18% pre-pandemic proportion for FYs 2019 and 2020, and more evidence perhaps of adverse expectations concerning future bad loans:

Advantage Finance: Collections and credit quality

- Customer repayments ultimately determine the quality of Advantage’s loan book and underwriting process.

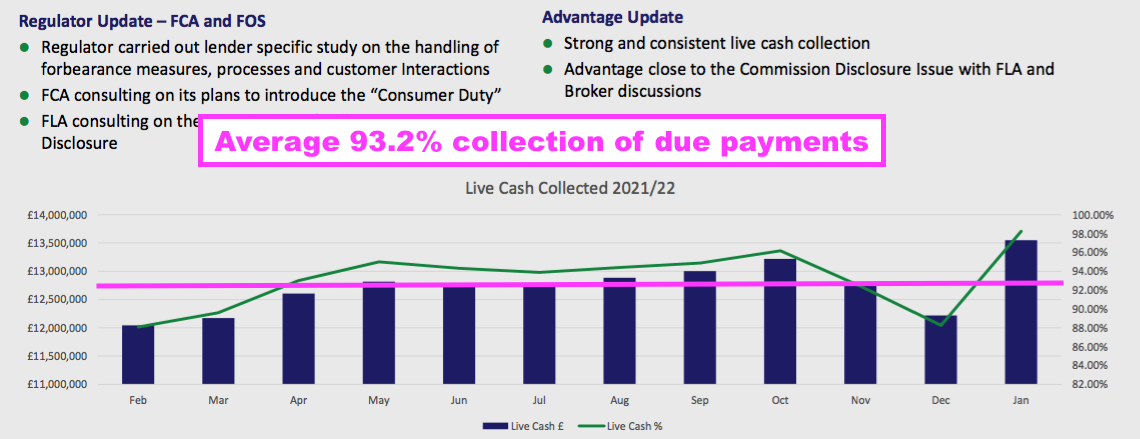

- SUS said Advantage’s collections performance for this FY was “superb”. The collection rate, at 93.2% of due, almost matched the 93.5% for pre-pandemic FY 2020:

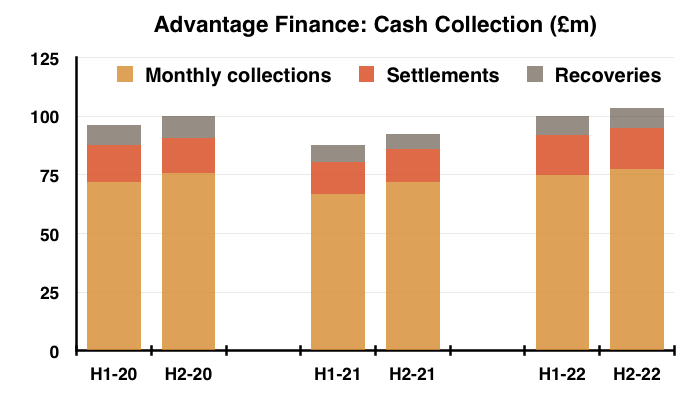

- Total collections, recoveries and settlements amounted to £104m for H2 to slightly exceed the pre-pandemic collection performance of H2 2020:

- SUS said Advantage’s collection rate was made possible by the division’s “close and harmonious customer relations, responsible lending, the success of a new customer payment portal… and… the professionalism and empathy of our customer-facing teams.“

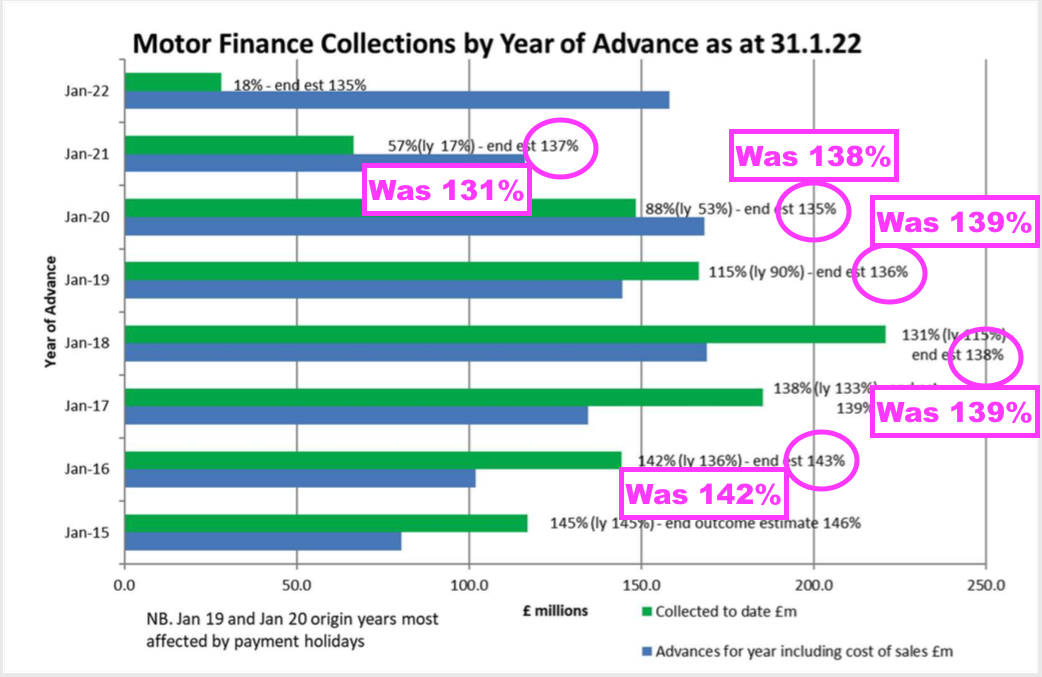

- SUS’s estimates of future collections have been revised slightly:

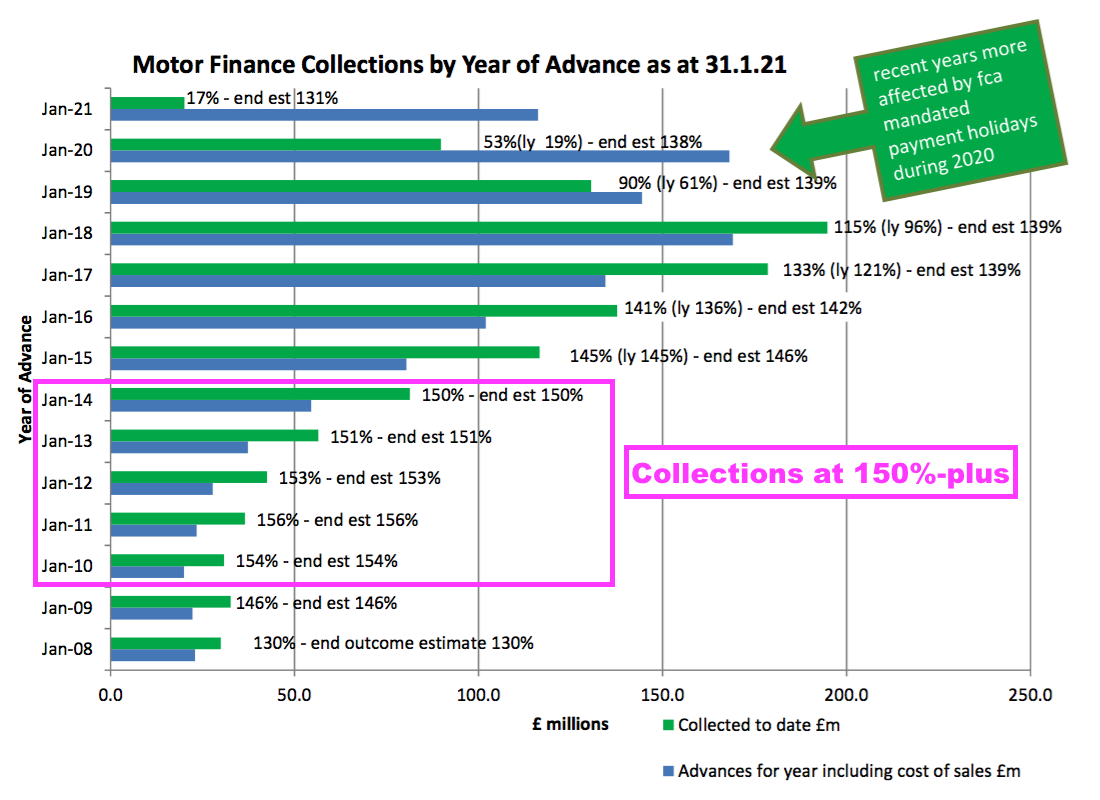

- Collecting between 135% and 138% of the original loan remains some way off the 150%-plus collected for money lent between FYs 2010 and 2014:

Advantage Finance: Payment holidays

- Customers that enjoyed payment holidays are repaying at a greater rate.

- The pandemic prompted the FCA to allow borrowers to apply for payment holidays lasting up to six months. All payment holidays ended on 31 July 2021.

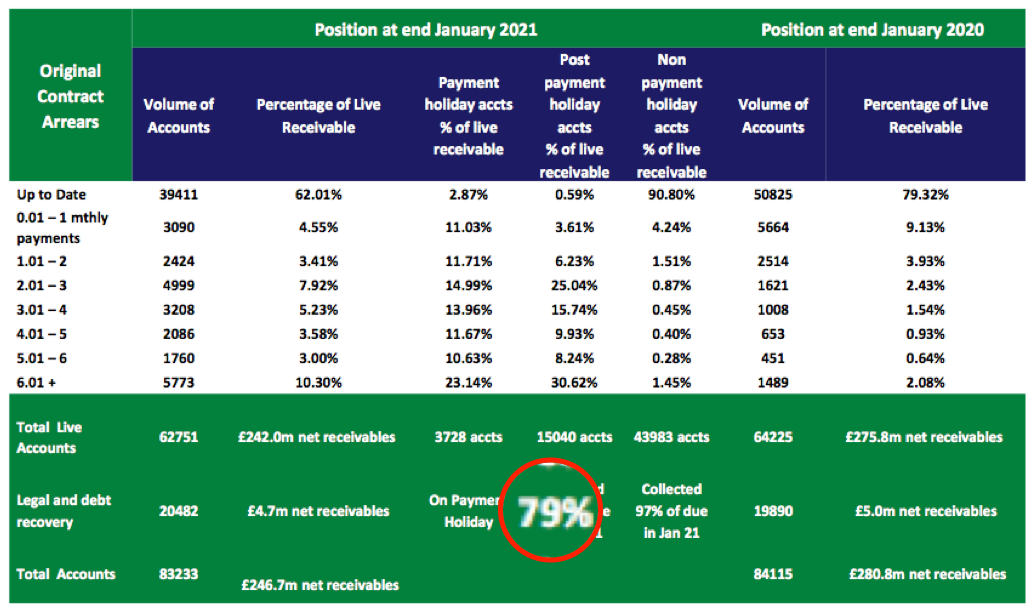

- During January 2021, customers that had taken payment holidays were paying 79% of due…

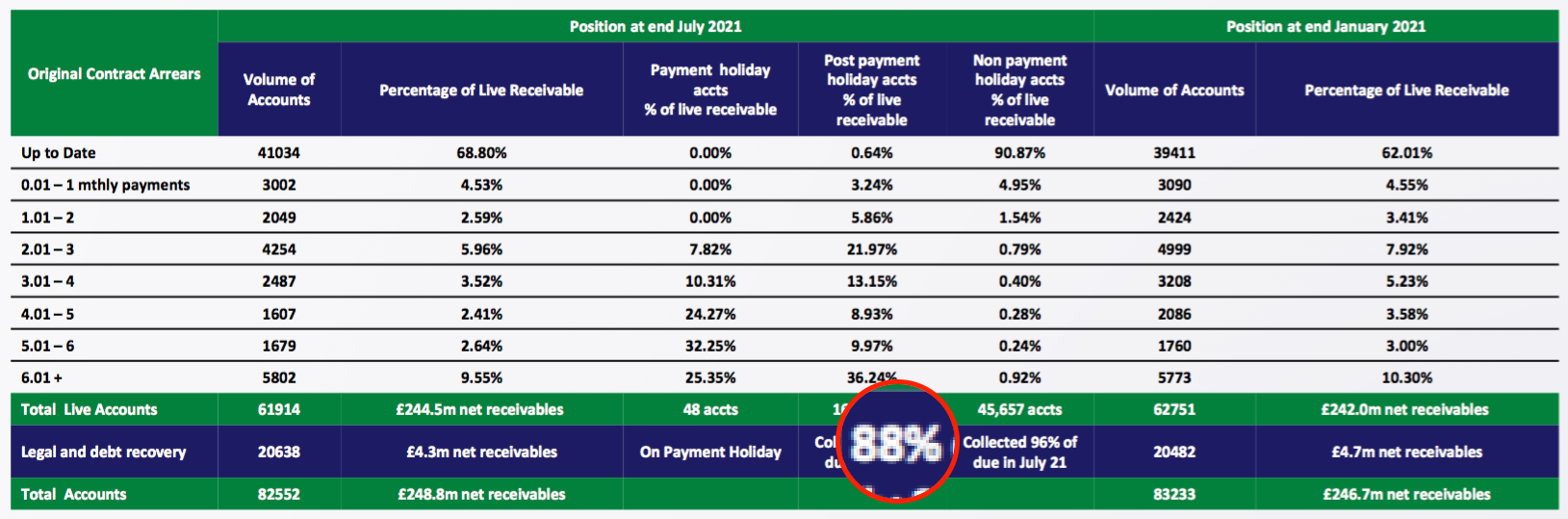

- …but by July 2021 they were paying 88% of due…

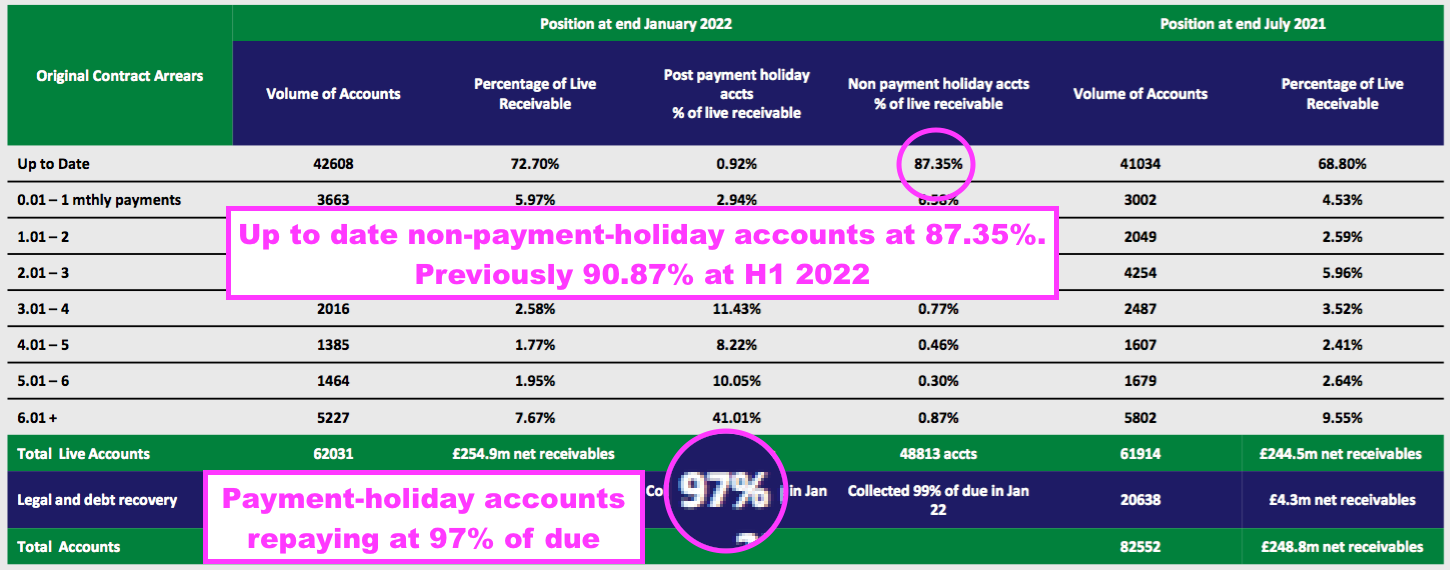

- …and by January 2022 they were paying 97% of due:

- Holiday-payment borrowers repaying their loans ensured the overall percentage of up-to-date accounts improved from 62% for FY 2021 to 69% for H1 2022 to 73% for this FY 2022.

- For perspective, the up-to-date account percentage for pre-pandemic FY 2020 was 79%.

- Note that the percentage of non-payment-holiday accounts classified as up-to-date has slipped from 91% at H1 2022 to 87% for this FY.

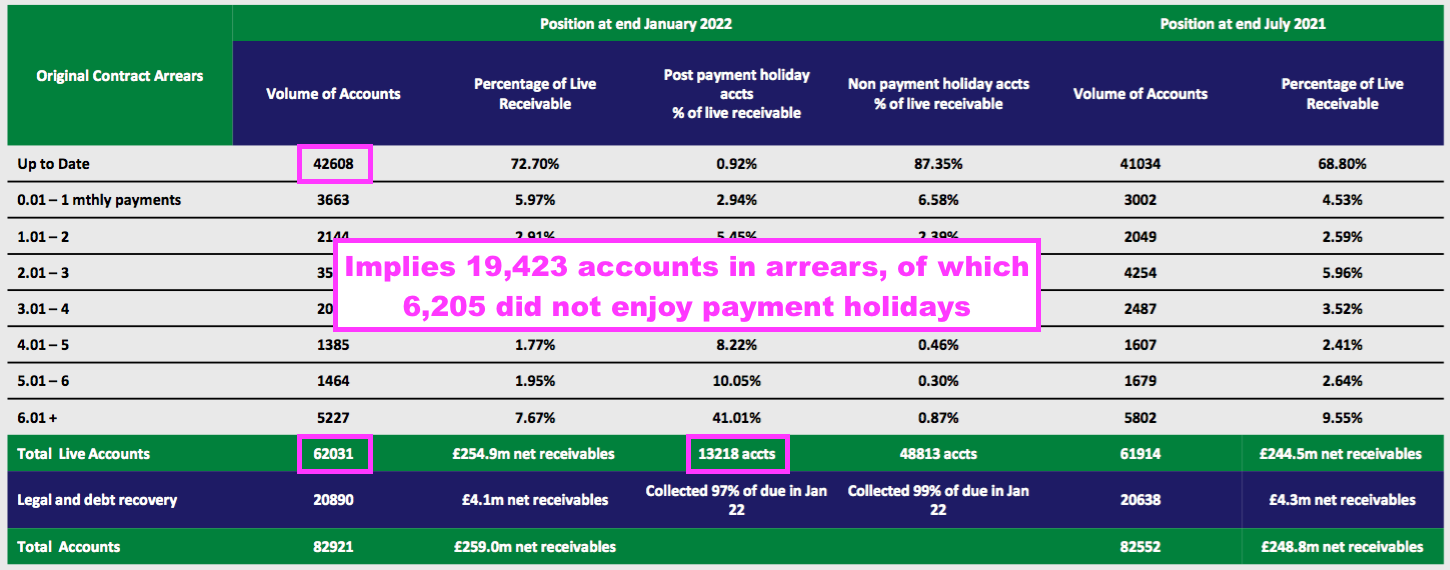

- A total 19,423 (62,031 less 42,608) accounts were overdue at the year-end, which excluding the 13,218 holiday-payment accounts implies 6,205 non-payment-holiday accounts were overdue:

- 6,205 overdue non-payment-holiday accounts compares with 4,623 for H1 2022 and 4,572 for FY 2021.

- This increase to overdue non-payment-holiday accounts is perhaps more evidence of adverse lending conditions starting to emerge.

Advantage Finance: New loans

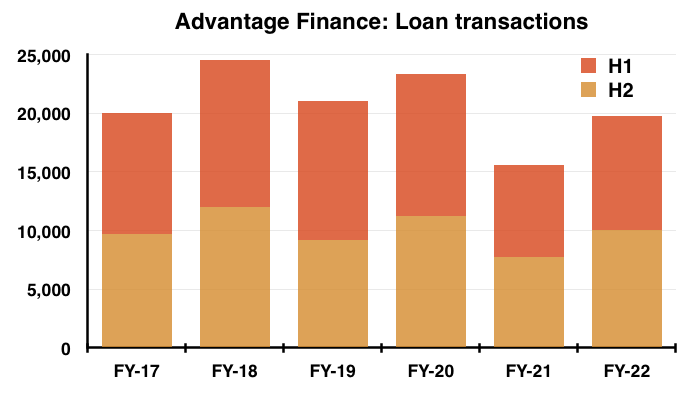

- The 10,050 motor loans issued during H2 took the number agreed for the year to 19,747:

- New loans at levels lower than witnessed during FYs 2017, 2018, 2019 and 2020 were not due to a shortage of applications.

- The 2022 annual report says Advantage receives more than 1.5 million loan applications a year, versus 750,000 cited within the 2017 annual report.

- Rising applications but falling transactions since FY 2017 hopefully means Advantage has been very choosy with its lending.

- SUS expressed caution about motor-loan transactions for FY 2023:

“Although Advantage expects that new loan transactions will continue to grow this year, much will depend upon consumer confidence generally and the economic fall-out from the current crisis in Eastern Europe.

[Advantage’s] prognosis has therefore been sensibly prudent with a return to increased growth forecast for the final third of this financial year, when used car availability is expected to have gradually returned to more normal levels.”

- The caution contrasted with the preceding H1 results webinar, during which management claimed Advantage was “planning for an increase in volumes up towards 25,000 units” for FY 2023.

- 25,000 new loans a year would represent a 27% increase on the FY 2022 performance.

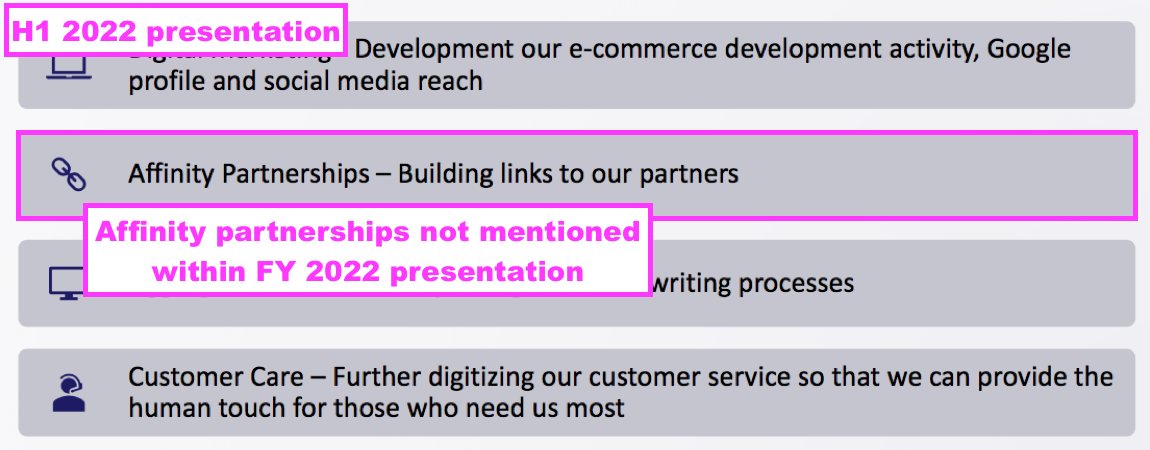

- No mention of transactions increasing to 25,000 was mentioned during the latest webinar.

- Also absent during the latest webinar were remarks about potential affinity partnerships, whereby Advantage could receive applications rejected by mainstream loan providers:

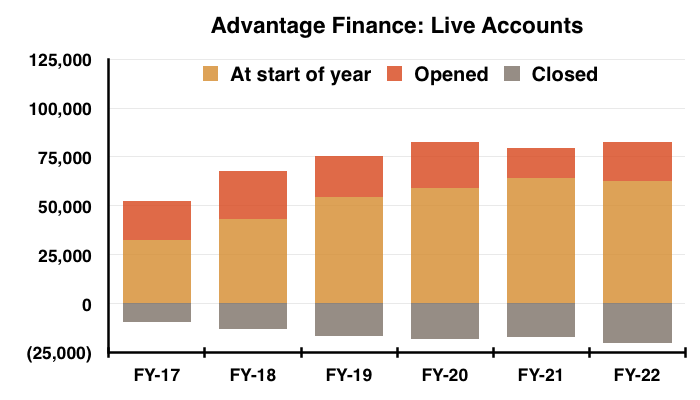

- The 19,747 new loans issued during this FY were offset by 20,467 accounts closed due to finished repayments, voluntary terminations or the commencement of legal proceedings:

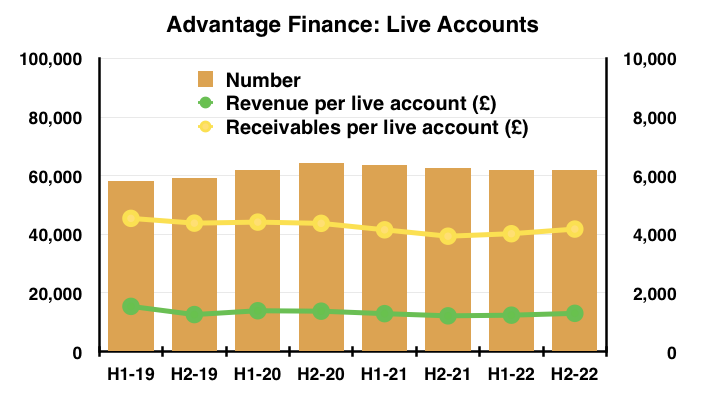

- The account openings and closures meant total ‘live’ accounts remained at approximately 62,000:

- Revenue per account continues around the £1,300 mark, while customers owe approximately £4,100 each.

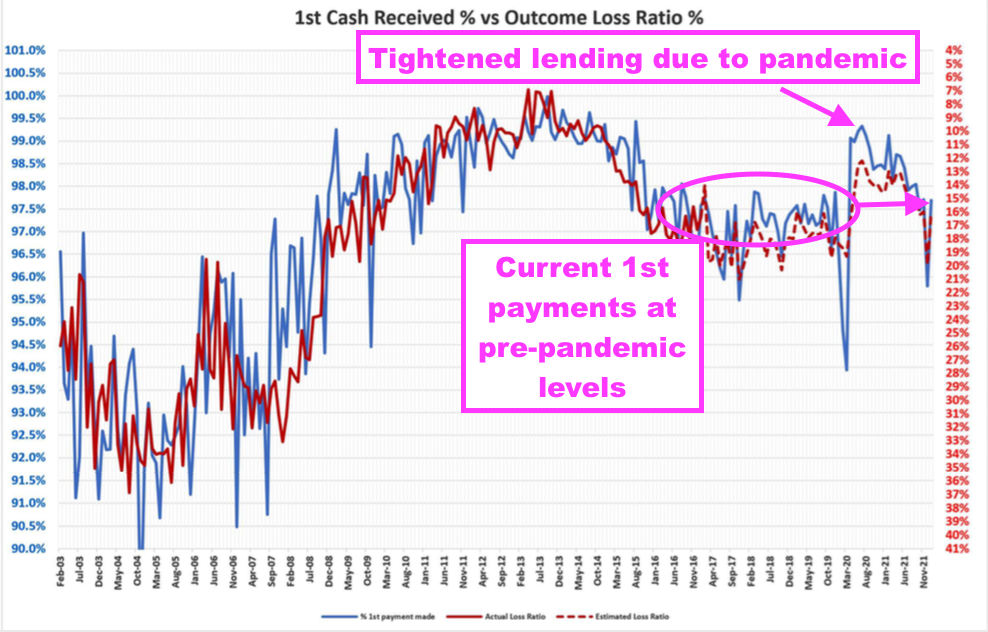

- Advantage’s first-payment statistics still appear satisfactory:

- The blue line (left axis) reflects the percentage of customers making their first payment on time.

- The proportion at almost 98% remains at levels seen on a regular basis before the pandemic.

- (The 99%-plus first-time payments achieved during 2020 were due to the stringent lending applied as the pandemic struck).

- The unbroken red line (right axis) shows the actual ‘outcome loss ratio’, which correlates strongly to the first payment percentage.

- The dotted red line (right axis) shows the estimated ‘outcome loss ratio’, which had diverged from the blue line to reflect the greater uncertainty of repayments following the pandemic.

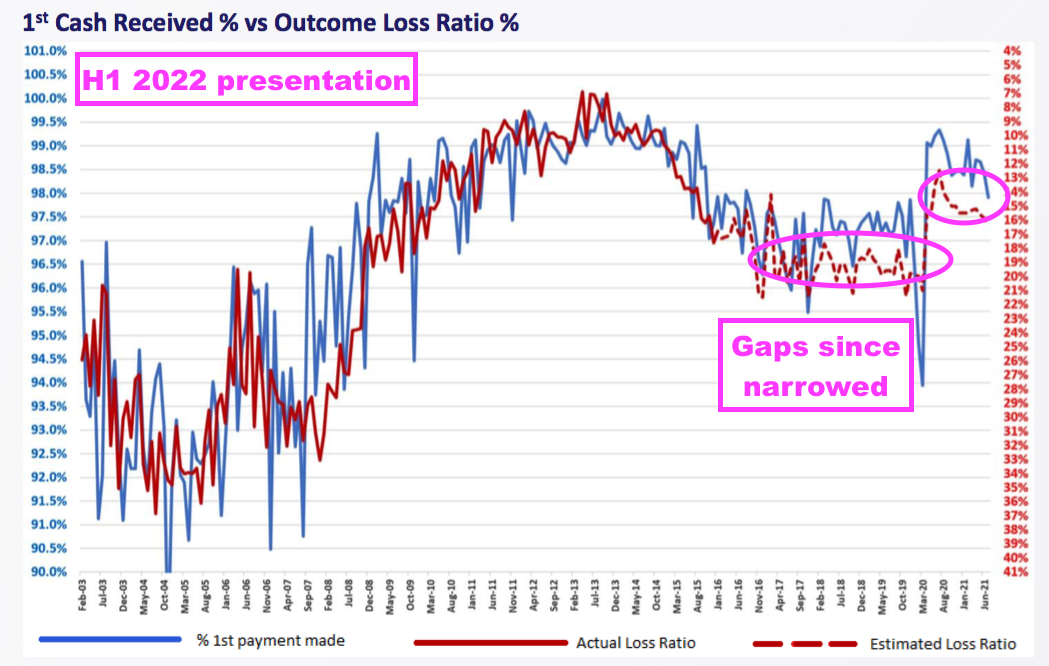

- The gap between the blue line and the dotted red line is now closer than the same gap within the preceding H1 2022 presentation below…

- …and implies improved repayment levels ahead.

Aspen Bridging

- Established at the start of FY 2018, Aspen offers property bridging loans for small/individual property developers with awkward financial circumstances.

- Aspen’s rate card says developers borrowing against residential properties pay a flat monthly interest rate of 0.69% on a 70% loan-to-value arrangement. These case studies give a flavour of the transactions involved:

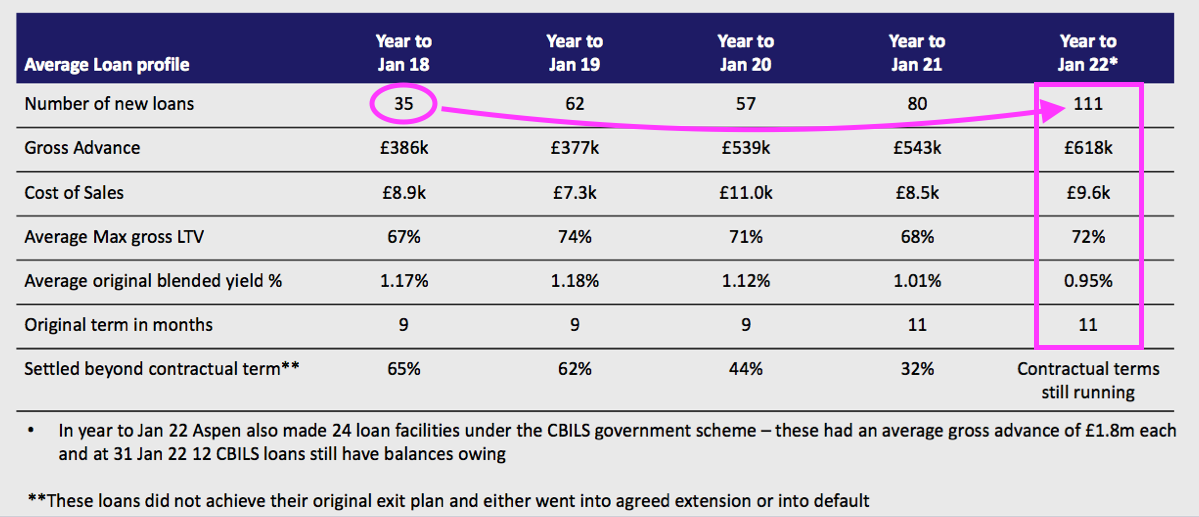

- Excluding CBILS activity, developers last year were advanced an average £618k for 11 months. The number of loans agreed per year has more than tripled since the division’s formation:

- Aspen’s participation in the government’s CBILS scheme bolstered divisional progress during this FY.

- Aspen agreed 24 CBILS loans totalling £43m (£1.8m average), of which 22 totalling £35m (£1.6m average) occurred during H1.

- H2 therefore witnessed two CBILS transactions worth £8m (£4m average).

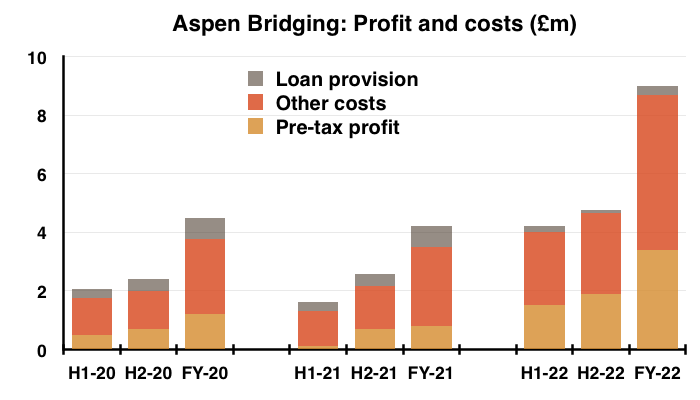

- Profit during H2 came in at £1.9m versus £1.5m for H1 and £1.2m for the pre-pandemic FY 2020:

- Aspen’s credit quality remains exceptional.

- Of the 369 loans advanced since formation, 267 have been repaid and only two of the remaining 102 have defaulted.

- Expected write-offs from Aspen’s £65m loan book amount to just £646k.

- Loan impairments during this FY were £315k, with only £92k charged during H2.

- SUS explained Aspen’s low write-offs were due to the division’s “thorough, painstaking and rigorous approach to underwriting involving a personal visit to every property financed.“

- Aspen’s enlarged loan book currently represents 20% of SUS’s entire lending.

- Excluding CBILS, Aspen lent £69m last year of which £40m was lent during H2. Perhaps gross lending could reach £80m for FY 2023 and maybe even £100m for FY 2024?

- Management talk during the results webinar was optimistic, suggesting Aspen’s profit could “more than double” during the next two years.

- The upbeat comments backed up the bullish remarks from the FY 2021 webinar, which cited a £5m Aspen profit within 2-3 years (i.e. by FY 2024).

- I do wonder whether Aspen will one day surpass Advantage to become SUS’s largest division.

- Group executive director Jack Coombs co-started Aspen and is part of the founding Coombs family that owns at least 42% (£107m) of the company.

- SUS’s lead executives — Anthony and Graham Coombs — are presently both 69 years old while their cousin Jack is 34.

- Jack Coombs therefore seems likely to be leading SUS at some point, and maybe the lending focus of the group may alter thereafter.

- Aspen’s early years have been more profitable than the early years at Advantage.

- Advantage took more than a decade to grow from start-up (FY 2000) to report a £3m-plus profit (FY 2011); Aspen has meanwhile reached £3m in just five years.

Financials

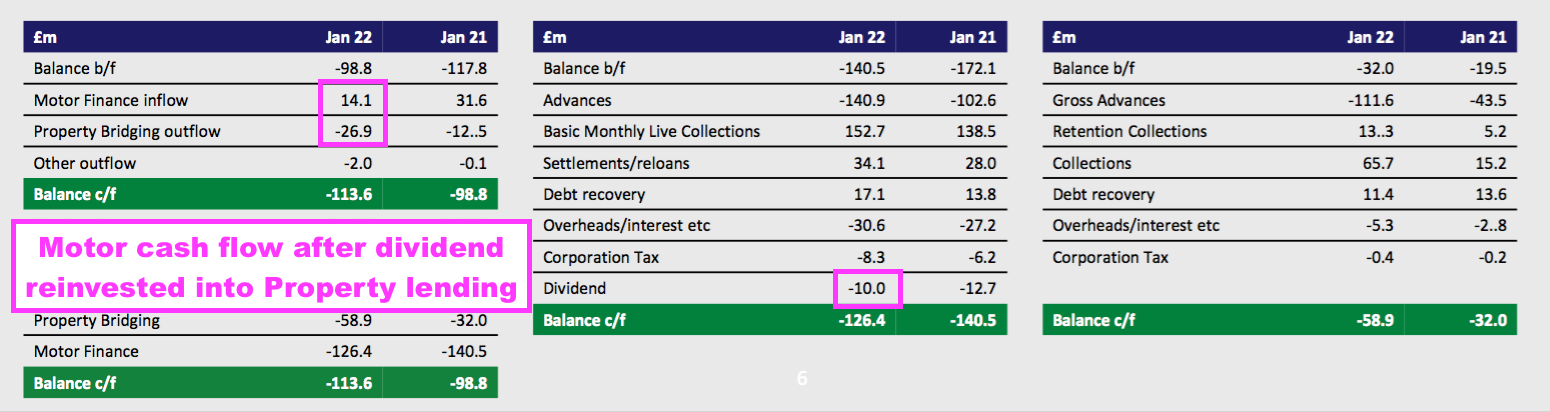

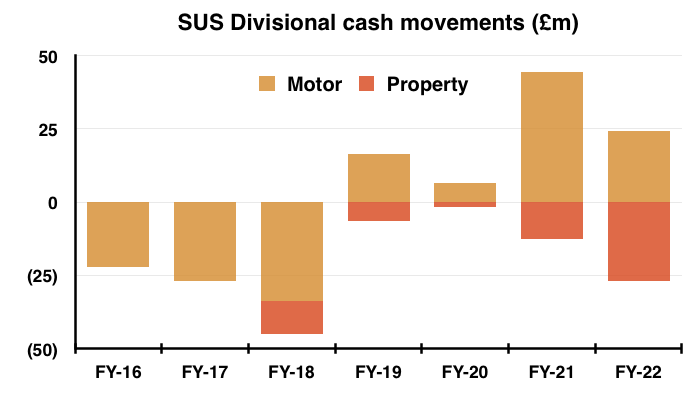

- The results presentation emphasised how money coming in from Advantage is funding new business for Aspen:

- During this FY, Advantage generated free cash of £24.1m of which £10.0m was paid as dividends and £14.1m was used to support Aspen.

- The three preceding years also saw Advantage generate surplus cash that was used to support Aspen:

- The cash movements from the last few years suggest Advantage is experiencing fewer lending opportunities, and better potential returns may now be enjoyed through Aspen.

- After all, SUS does have debt facilities of £180m to fund new Advantage loans, but chooses instead to deploy surplus cash within Aspen.

- SUS said during the preceding H1 2022 that the £180m facility gave “substantial headroom for accelerated growth“.

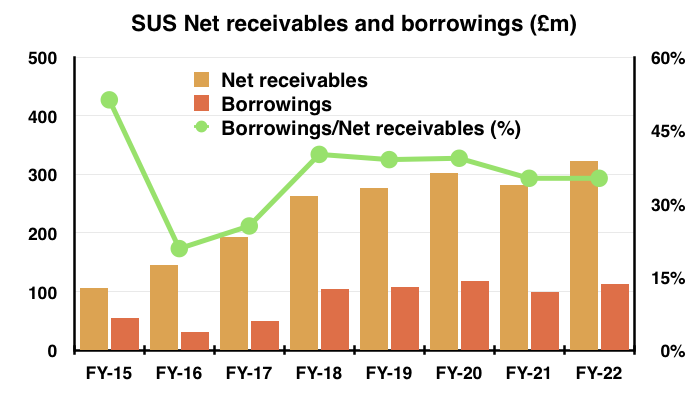

- But debt finished the year at £114m and was kept at 35% of the amount owed by customers:

- Debt in fact reduced by £2m during H2, and SUS’s latest commentary on using that £180m facility was toned down to giving “sufficient headroom for the anticipated organic growth in both businesses in the next year.”

- Bank interest paid during the year was £3.6m, implying SUS’s borrowings incur interest at a reasonable 3.4%.

- Interest cover does not feel too worrying at approximately 10 times the average operating profit from FYs 2021 and 2022.

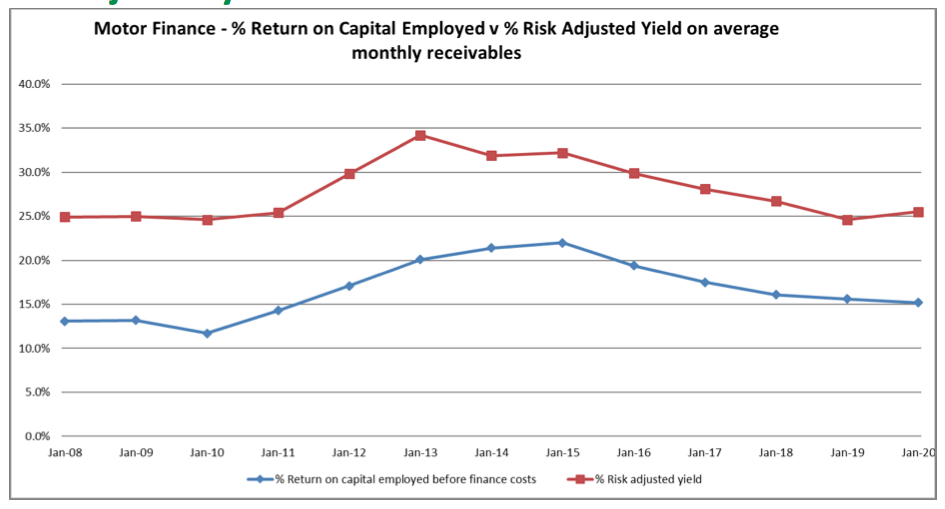

- Return on capital employed for Advantage remains modest.

- Although the slide below from the FY 2020 presentation has not been updated for two years…

- … SUS did say ROCE for Advantage was 19.4% for FY 2022 and 8.6% for FY 2021, giving a two-year average of 14%.

- Advantage seems unlikely to enjoy superb ROCE levels.

- Charging a flat 16.3% annual interest on a £7,138 loan less cost of sales of £874 leaves approximately £945 a year over four years before admin costs, non-payments and tax:

- £945 a year from loaned capital of £7,138 equates to a 13.2% return before admin costs, non-payments and tax.

- That 13.2% compares to 15.0%, 14.9%, 14.5%, and 13.7% for FYs 2018, 2019, 2020 and 2021 respectively.

- The lower trend is not ideal, especially if higher inflation does indeed cause more loans to go unpaid.

- But SUS’s returns are enhanced by debt.

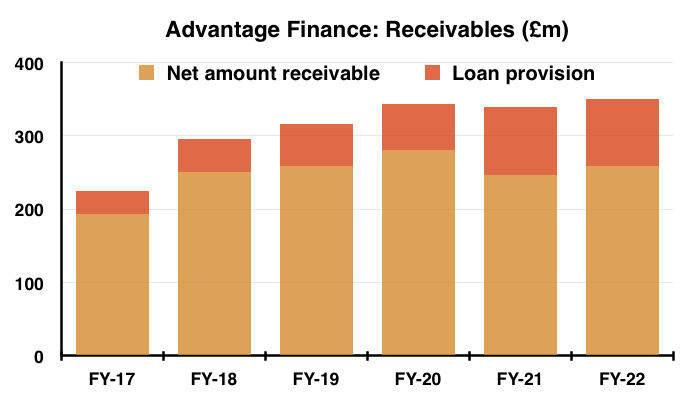

- Advantage’s loan book stands at £351m before provisions, of which £127m (or 36%) was funded by divisional debt and the rest through shareholder equity.

- As such, £2,570 of the average £7,138 loan advanced during FY 2022 was funded through debt while £4,568 was funded through shareholder equity.

- The aforementioned £945 equates to a useful 20% of that £4,568 funded through equity — albeit the 20% is before admin costs, non-payments, tax and debt costs.

- Aspen’s ROCE shows early indications of similarly modest ROCE.

- Customer interest charged monthly at say, 1%, for a year would give a ROCE of 12% before other costs and tax. Aspen’s divisional accounts indicate the division is funded purely through shareholder equity.

- The modest ROCE levels do suggest SUS’s inherent value should be biased towards the asset value of the group’s loan book rather than annual earnings.

- SUS’s other assets and liabilities — including a tiny defined-benefit pension scheme — amount to only £3m.

Valuation

- SUS’s outlook comments were watered down from the preceding H1:

- Back then SUS talked of a “bright” future:

“The Covid induced tribulations of the past year have seen S&U emerge more profitable, more competitive and more attuned to our customers ‘ needs . Add to that the buoyant markets in which we operate, our strongest ever financial base and our loyal and committed workforce, and prospects for the future are bright indeed.“

- But this FY statement referred to the “challenges now facing all of us“

“Like all successful businesses with a long history, S&U recognises that it must tailor its products and services and trim its operational tack to its economic, political and regulatory environment, over which it may have little control but to which it can nevertheless adapt and therefore thrive.

Whilst this year’s resounding results clearly show our, and most important our loyal people’s, ability to do this, their work in preparing and priming the Group for both the opportunities and challenges now facing all of us, gives me a quiet but determined confidence in S&U’s future.“

- References to “operational tack” probably referred to regulation, as SUS’s statement took issue with the “tsunami of regulation, sometimes ill-coordinated and even contradictory, apparently designed to remove all risk for consumers irrespective of circumstances.“

- Aspen’s positive progress versus Advantage may in part be due to property-bridging loans being unregulated.

- The cautious outlook remarks were followed by an encouraging AGM statement that revealed profit running “above budget“:

“Following the Group’s “resounding results” announced in S&U’s annual report and our “quiet but determined confidence” in building on them even in uncertain times, we are pleased to report further steady progress.

Group profit before tax for the period was above budget for both Advantage Finance, our motor finance division, and Aspen Bridging, our property bridging division.“

- Mind you, SUS continued to recognise an uncertain economy:

“Although we currently expect to meet growth targets for this year, S&U remains focused above all on maintaining the excellent quality of its own books and service to its customers. This will ensure a firm base for faster expansion when the macroeconomic skies brighten. That balance between quality and growth has always served S&U well.“

- Last month’s AGM update confirmed SUS’s financials had not altered dramatically. The group’s loan book and debt now stand at £340m and £125m respectively, versus £323m and £114m at the end of FY 2022.

- The share price has altered dramatically, falling from £28 last October to £21 of late:

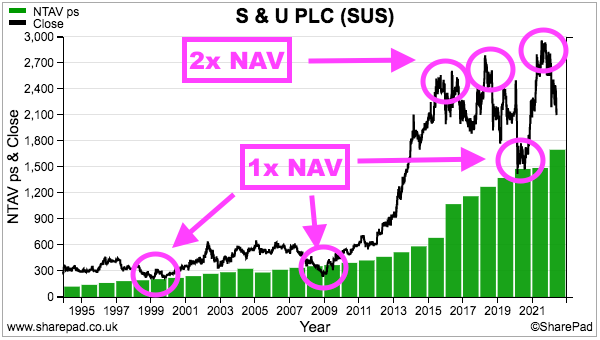

- The £21 shares presently trade at 1.24 times NAV of £17 per share:

- The very best buying opportunities have occurred when the shares trade at NAV or below, while upside has tended to be limited when the shares trade at 2x NAV or more.

- The 1.24x NAV rating suggests the market is worried that economic trouble will lead to greater write offs — and the “above budget” profit for FY 2023 will not be sustained.

- But the veteran executives, who have been involved at SUS since the mid-1970s and steward at £107m-plus shareholding for their wider family, have successfully navigated many previous downturns (not least the pandemic).

- The 2022 annual report reminded shareholders of the long-term benefit of these owner-managers:

“Our over-arching factor in the success of our business over 80 years and through three family generations of management is our business philosophy. The identity of interest between management and shareholders has fused our ambition for growth with a conservative approach to both credit quality and funding.”

- Management’s “conservative approach to both credit quality and funding” ought to (again) prove its worth should difficult times emerge.

- The record 126p per share dividend meanwhile provides a handy 6% yield at £21.

Maynard Paton

As ever, a great insight into the company and your thought process for evaluating holdings.

Thanks again!

S & U (SUS)

Trading Update published 10 August 2022

A promising statement that claimed the business was performing ahead of expectations and included somewhat defiant comments from the chairman. Here is the full text interspersed with my comments:

——————————————————————————————————————

S&U plc, the specialist motor and property bridging lender, today issues its trading update for the period from its AGM Statement of 26 May 2022 to 31 July 2022. It will announce its half-year results on 27 September 2022.

Although it is only just over two months since our last trading update, S&U is pleased to report that both its motor and property bridging divisions continue to outperform its expectations, both in transactions growth, and in the quality of its book and the new business it is writing. Current Group receivables now stand at approximately £370m against £340m in May, and profitability exceeds that of H1 last year. Debt quality is reflected in strong collection rates and supported by low levels of default at Advantage, our motor finance business, and at Aspen, our property bridging lender.

However, these results do not mean that S&U has become either hubristic or Panglossian. Current political instability and differing views on fiscal policy, together with persistent UK economic headwinds do not allow for any complacency. We recognise that a potentially shrinking economy, higher inflation and interest rates, historically low levels of consumer confidence and a possible technical recession in the UK, have all contributed to a manically depressed view of the future, particularly in the UK equity markets.

Hence, although growth currently exceeds budget and expectations, we judge it sensible in light of current uncertainty about economic prospects, to temper optimism with caution, particularly in our underwriting policy. Recent adjustments are designed to continue to ensure that our customers have sufficient comfort and headroom to withstand any pressure on their household disposable incomes, which might be felt later in the financial year. These will help protect our credit quality throughout the Group, whilst in the case of motor finance, anticipating the new outcome-based Duty of Care to customers, to be introduced by the Financial Conduct Authority in one year’s time.

——————————————————————————————————————

Certainly “both its motor and property bridging divisions continue to outperform its expectations” sounds promising. As does “profitability exceeds that of H1 last year“, because H1 last year saw a record £20m pre-tax profit that was bolstered by a lower-than-normal £5m bad-loan provision.

Adjustments to the underwriting procedures look very sensible given the domestic economic outlook (Panglossian means being unreasonably optimistic).

——————————————————————————————————————

Advantage Finance

Advantage Finance, our motor business based in Grimsby, continues its excellent post-pandemic progress to historic levels of growth and credit quality. Applications for motor loans remain robust in a buoyant used car market. This has meant growth in transactions of nearly a quarter on last year and an increase in net receivables to approximately £280m in July against £268m in May and £249m in July 2021. Credit quality remains high, measured by higher collections against due and by the lower incidence of voluntary terminations and bad debts. In addition, a revised scorecard and the introduction of further credit reference information, as well as strengthened buffers on customer affordability, are designed to ensure that it remains so.

What is prudent for our customers also applies to our own excellent, loyal and expert staff. Whilst administrative costs remain well controlled and within budget, provision is being made to help those lower paid individuals who may be feeling cost of living pressures more acutely. This will bolster Advantage’s excellent staff morale and minimise staff turnover.

——————————————————————————————————————

Advantage is more sensitive to economic difficulties than the Aspen property-bridging division, and so Advantage’s collections remaining high and bad debts being low is reassuring.

Transaction numbers in the previous H1 were 9,697, so an improvement of nearly a quarter gives c12,000, which if repeated for H2 would put Advantage at close to the record near-25,000 accounts opened during FY 2018.

——————————————————————————————————————

Aspen

Despite some doomsayers and “cliff-edge” addicts who have commentated on the UK’s residential property market, the real world has allowed Aspen to continue its growth in serving its niche developer and investor market. Net receivables in the period have now reached approximately £90m in July against £72m in May and £58m in July 2021. Aspen’s growing reputation and the introduction of new products mean that it is attracting more experienced and expert borrowers, which have seen average gross loan size increase to around £875,000 so far this year, helping both the receivables and revenue growth.

This trend towards higher quality and more seasoned borrowers has seen a slight reduction in blended book yield on last year, although above budget, coupled with excellent repayments and continued good credit quality.

All this gives a very strong and stable base for further progress in what is likely to remain, despite increased costs of borrowing, a strong residential property market.

——————————————————————————————————————

All positive stuff. Aspen’s loan book has grown 55% during the last 12 months and is now 24% of the group’s loan book. Clearly the division could become very significant to SUS if the bridging-loan momentum continues. The £875k average loan compares to £618k for FY 2022, and talk of the “trend towards higher quality and more seasoned borrowers” is welcome.

——————————————————————————————————————

Treasury

S&U’s continued investment in book growth at both Advantage and Aspen, in addition to the payment of our final dividend has seen Group net borrowings rise to £154m in July against £125m in May and £115m in July 2021. Our medium-term facilities are £180m giving us ample headroom for further growth, whilst our low level of gearing, our strong credit quality and cash generation will facilitate additional facilities as required.

Commenting on S&U’s trading outlook, Anthony Coombs, S&U chairman, said:

“I am very pleased and encouraged by S&U’s trading this year. However, like many in the financial services sector, S&U’s performance and its prudently planned prospects for the future, are inadequately reflected in stock market commentary and valuations dominated by uncertainty and pessimism. That pessimism is not shared by S&U. We believe that realistic underwriting, good products, and supportive and sensitive customer relations will enable us to make further significant and sustainable progress in the markets which we serve.”

——————————————————————————————————————

Net borrowings of £154m means net assets are approximately £216m (or c£17.77 per share) given net receivables were earlier said to be £370m.

Net assets were £207m at FY 2022, so this H1 has seen a £216m less £207m improvement = £9m. Add on the cost of the final 57p per share dividend (almost £7m) = earnings of £16m (132p per share) = pre-tax of £20m. So the H1 2023 performance appears to have only just beaten the £20m of H1 2022.

I always worry a little when executives talk about share prices and valuations, although knowing that the current market pessimism “is not shared by S&U is helpful I guess. Markets have always suffered mood swings, and management teams ultimately have to get on with running their businesses and prove to investors their despondency is misplaced. And management teams never complain about valuations being dominated by certainty and optimism!

Maynard

S & U (SUS)

Publication of 2022 annual report

Here are the points of interest beyond those noted in the blog post above:

——–

1) CHAIRMAN’S STATEMENT

Quite a few matters addressed here, including apparent criticism of “woke” regulation and ESG “virtue signalling“:

a) Optimism

The chairman remained optimistic despite various economic difficulties:

“These results show that S&U plc has emerged stronger than ever and primed for a new era of profitable growth.”

“As the world reels from one crisis to another, it is apt to remember the words of Winston Churchill, our greatest war leader: “I’m an optimist – it does not seem too much use to be anything else”.”

“In sum, current trends in both our businesses remain very encouraging with current new loans this financial year already beating budget.”

b) The importance of employees

The chairman reiterated the group’s staff supported two of the three “pillars” for long-term growth:

“S&U’s remarkable ability to produce consistent and long-term growth rests on three pillars.

The first is the tenacity, hard work, imagination and ambition of our remarkable colleagues.”

“Second, they have used the pandemic period to set in place a raft of operational improvements which are making both Advantage and Aspen more competitive than ever.”

The group’s third “pillar” is the health of the economy, which looks “mixed“:

“Third, long experience has proved to us that successful lending businesses do not exist in a vacuum. Both the attraction and affordability of all our products depend not only upon the financial health of our customers but on prevailing economic conditions. In turn, these depend upon health of the British economy and in particular the motor and housing markets which we serve. Currently, to put it mildly, the runes are mixed.

A bit more on the importance of staff:

“These collections represented an average 93.21% of due (2021: 83.26%) and the year finished on a remarkable 98.25% of due in January. They were made possible by Advantage’s close and harmonious customer relations, responsible lending, the success of a new customer payment portal introduced last summer and, last but not least, by the professionalism and empathy of our customer facing teams.”

c) Affinity partnerships

Despite the lack of reference within the presentation slides, perhaps potential affinity partnerships with mainstream loan providers may still bubble away in the background:

“For the longer term, a number of marketing and branding initiatives have been introduced. They will broaden the funnel of our new business, develop new affinity and consolidated partnerships and open direct channels to future customers.”

d) Electric vehicles

EVs will become important to SUS one day (also see point 2d below):

“Again, with an eye to the future, Advantage has this year increased its financing of electric cars. Although electric vehicles currently only comprise about 3.5% of the UK car parc, the market is growing strongly. Indeed 28% of new vehicles sold this year were either electric or plug in self-charge hybrids. A working group has been set up to track the development of this market and we expect to be able to introduce more of our customers to it over the next few years.”

“As evidence of intent, many of the Board of Advantage now either possess or have ordered an electric vehicle.”

e) Aspen

Encouraging commentary on Aspen’s progress, with a higher limit of loans now available:

“Defaults are at their lowest ever and no actual realised losses have been incurred this year on the loan book.”

“As the business develops, new products have been introduced. Loans now range up to £5m per deal as, in the absence of flexible mainstream bank support, the refurbishment and small development market expands.”

f) Buffett mention

Always good to name-check Mr Buffett:

“Together with Warren Buffett, the legendary American investor, we believe that shareholders’ rewards should reflect the long-term view of the cash thrown off by the profits of the businesses they own.”

g) Regulation

SUS is not keen on ever-greater regulation and government intervention:

“ Whilst technological change has been at the forefront, the most profound change has been philosophical, and one which could threaten the flexibility, development and success of the industry. Previously widely accepted notions regarding the success of the free enterprise system in harnessing the energy, motivation and multiple decisions of millions of consumers and producers for the benefit of all, are no longer widely held.

As Milton Friedman, and even the great Adam Smith, lauded the ability of markets, flexibly regulated to benefit the common good and improve standards of living generally, current trends are increasingly more interventionalist, judgemental and even “woke”… ”

“All this has resulted in a tsunami of regulation, sometimes ill- coordinated and even contradictory, apparently designed to remove all risk for consumers irrespective of circumstances. This has two serious consequences.

First, it restricts innovation, robust competition and therefore economic growth…

Second, waves of new regulation, often without any parliamentary or even ministerial scrutiny or oversight, have led to complication and uncertainty…”

h) ESG

Not quite sure why the chairman had to mention “virtue signalling” when remarking upon ESG matters:

“More widely, S&U’s habitual responsibilities for the world around it are itemised in its Environmental, Social and Governance Responsibilities (“ESG”). How we fulfil these, are detailed, without any virtue signalling, in later sections on S&U’s Corporate and Social Responsibility and in our Section 172 Statement.”

Interestingly enough, the chairman cites a “a majority female shortlist” for a new board director…

“Our pragmatic approach means that the last year has seen recruitment at Aspen fully reflect the ethnic diversity of its West Midlands base; a selection process for a new main Board Director which involved a majority female shortlist;…”

…but then confirms the new board directors were in fact both male:

“Finally, it gives me great pleasure to welcome to our Board this year two new members. The first is my cousin Jack who replaces Fiann Coombs, whom I warmly thank for the wise contribution he has made to our proceedings over the past decade…

The second, and latest appointee to the Board is Jeremy Maxwell, whom we were delighted to appoint earlier this year after an exhaustive and very thorough process, and who brings considerable talent, wisdom and experience in marketing, particularly in the Business to Consumer field, at Wolseley UK, Carpetright, B&Q, Screwfix and Mothercare. ”

The board consists of nine men and no women (see point 8b)

2) STRATEGIC REVIEW

Included a variety of useful reminders about SUS’s business alongside snippets of new text describing recent progress:

a) Typical car-loan customers

A reminder of the typical car-loan customer:

“This long experience has enabled Advantage to gain a significant understanding of the kind of simple hire purchase motor finance suitable for customers in lower- and middle- income groups. Although decent, hardworking and well intentioned, some of these customers may have impaired credit records, which have seen them in the past unable to access rigid and inflexible “mainstream” finance products. Advantage provides transparency, simplicity, clarity and suitability to both service and product, which these customers require.”

b) Car-loan applications

Nearly 1.5 million last year:

“As a result, Advantage currently now receives nearly 1.5m unique applications a year and has written over 210,000 customer loans since starting trading in 1999. The loans have an average original term of just over 4 years and this medium-term loan cycle means that motor finance profits are normally earned over a much longer period than just the year of origination.”

Applications were “over” 1.5 million for 2021, so a slight reduction during 2022 presumably due to car supply shortages. Applications were 1.3 million for 2020 and 1.0 million for 2019, so the general trend is rising. While there is no shortage of would-be car buyers approaching SUS, applications of course have to be filtered for buyers that are likely to repay their loans.

c) Car market

All new text for 2022 about the car market:

“The year also saw a further decline in the public’s appetite for new diesel engines. Sales have fallen from 50% of all new passenger cars in 2014 to less than 15% now. On the other hand, sales of petrol new vehicles rose to 58% of the total market last year. Electric and hybrid vehicles sold a record 440,000 cars in 2021 up 75% on a year earlier and now comprise a quarter of new registrations.”

“The first and fundamental factor in Advantage’s success is the relative buoyancy and resilience of the used car market in which it operates. Thus, although the UK’s new car market at just 1.65m registrations last year is down about 30% on the levels pre-pandemic, the used car market in which Advantage operates has been more buoyant. Thus, in 2021 it saw 7.53m used car sales up 11.5% on the previous year.”

d) Electric vehicles

This text is repeated from 2021 about electric vehicles:

“Advantage’s current estimates predict that by 2030 new registrations of petrol vehicles will constitute about 20% of the market, diesel will be negligible whilst hybrid and electric sales will take 80% of the market, 30% of which will be EV. However, these trends will have a less effect on the make-up of the UK’s car parc over the next decade. This is estimated to reach about 50m vehicles of which 30% will be EV. Although at present the older and higher income profile of EV buyers does not match that of the Advantage customer, as EVs enter the used car market over the next five years, Advantage sees significant opportunities in electric vehicle finance.”

But new text for 2022… finance now being provided for EVs:

“Indeed, Advantage is developing products for this market and has already financed some used electric vehicles.”

e) Customer service portal

New text for 2022 highlighting the success of a new-ish website allowing customers to pay online:

“A new customer service portal was launched in 2021 this is proved very successful in improving communications between Advantage and its customers and also enabling them to make on-line payments.“

f) Housing market

New text for 2022 about a favourable housing market for Aspen:

“After a very strong mid- year when new mortgage advances rose to £159.8bn nationally (FCA), as buyers chose to take advantage of the Government’s stamp duty holiday, the residential lending market has cooled slightly, although overall total lending is back to pre-pandemic levels. The long-term confidence in the UK housing market which Aspen serves is further evidenced by a 11% house price increase in the UK during 2021. These trends are reflected in Aspen’s volume of loans written which nearly trebled to £130m throughout the year – and also in the quality of the loan book.”

A reminder of why customers choose Aspen:

““Mainstream” banks, including the newer “challengers”, continue to lack the speed, flexibility and appetite to furnish the smaller, short-term loans in which Aspen specialises. Recent consolidation in the challenger banking sector is evidence of this and again shows that, technology, speed and a quality bespoke service – as well as price – are what give smaller entrants like Aspen their competitive edge.”

g) 80-plus years of success

A reminder of why SUS’s style of family management has succeeded for more than 80 years:

“Our over-arching factor in the success of our business over 80 years and through three family generations of management is our business philosophy. The identity of interest between management and shareholders has fused our ambition for growth with a conservative approach to both credit quality and funding.”

h) Payment holidays

A few snippets on how car-loan customers restarted their payments after FCA allowed customers a payment “holiday” (I get the impression SUS remains unimpressed with the FCA’s decision allowing payment holidays, given previous webinar commentary suggested many customers taking the holiday could have still made their repayments):

“This result benefitted from a collections performance which justified a write back of loan loss provisions made during the Covid lock down last year. This recovery has been startling. Of the 21,221 customers taking Covid related payment “holidays” last year just 1709 have so far been classified as “bad debt”, representing just 1.3% of Advantage’s overall book. In total there are 13218 post payment holiday customers still on our live book at the end of January 2022 and these customers paid a remarkable 97.01% of due in January.”

i) Improved productivity

Seems like SUS has found a good balance of office/home working:

“Hybrid working for those who wish it, at two to three office days per week has seen productivity increase still further. No redundancies or short-time working have been necessary and the Company, as well as S&U plc generally, is pleased not to have taken a penny in Government subsidy.”

j) Bridge to Let

Brief confirmation of a “Bridge to Let” option for property developers:

“Aspen widened its range of increasingly supportive and loyal brokers, reshaped its range of loan products and introduced a new Bridge to Let product, designed for the builder refurbisher with a mind to later transition to investment.”

k) Property visits

I do wonder how SUS will ensure property visits are always undertaken as the number of loans increase:

“In order to achieve and further bolster this progress, Aspen recruited experienced business development managers, tightened its processes to ensure even stronger more robust underwriting and still insists that every property upon which Aspen lends for security is personally visited by a member of the team.”

Increasing the loan limit to £5m (see point 1e) may help with the ‘scalability’ of Aspen, but it seems to me the number of staff (and their associated costs) will have increase with loan volumes. But property visits do improve the underwriting, and have to continue.

3) PRINCIPAL RISKS AND UNCERTAINTIES

No change to the four main risks:

* Consumer and economic risks

* Funding and liquidity risk

* Legal, regulatory and conduct risk

* Operational risk

a) Consumer and economic risks

SUS remains circumspect about having to employ macro-economic forecasts…

“Whilst Corporate Governance guidelines, and the provisioning insisted upon by the Financial Reporting Council require macro- economic forecasts, both Covid, the recovery from it, current inflationary trends and now a war in Europe make this a virtually impossible task. For instance, last year the Office for Budget Responsibility expected the British economy to grow by over 7% in 2022. Current projections for growth this year are now just 4.8%.”

…which may explain why its inflation projection was rather inaccurate:

“Current trends in interest rates, although upward, are in our view unlikely to be very significant particularly since inflation is unlikely to persist at more than 4% throughout the year.”

b) Chief risk officer

Reassuring to know Advantage’s chief risk office also chairs the industry’s risk committee:

“Alan Tuplin, formerly Head of Credit, is Chief Risk Officer of Advantage and plays a key role in managing and mitigating legal, regulatory and conduct risk within Advantage. Alan has over 20 years of experience in non-prime motor finance and chairs the Risk Committee at the Finance and Leasing Association, the industry’s trade body.”

c) Advantage operational improvements

Snippets of new text for 2022 covering ongoing operational developments at Advantage:

“ The Group is very proud of its excellent underwriting and fraud deterrence processes which it continues to develop. Advantage’s underwriting capability, already state of the art in the motor finance industry, is being further refined through work with open-banking providers which will give an even more comprehensive overview of customer circumstances, affordability and their income and expenditure.”

“As part of Advantage’s IT governance framework, a real time monitoring suite for quality assurance is being evolved. This will both provide absolute assurance in line with IT’s second line risk enterprise and offer still greater regulatory transparency.”

4) CASE STUDIES

No sign of staff member Natalie being mentioned this year. She was name-checked during 2017, 2018, 2020 and 2021.

Helen name-checked for 2022 adds to her case-study appearances from 2016, 2017 and 2020.

5) CORPORATE SOCIAL RESPONSIBLITY

The 2022 report contained new text on diversity and climate change:

a) Diversity

“Although we recognise that current thinking means that diversity reporting should be based around a statistical analysis of our staff’s racial origin, given our above long- standing policies, we consider that this can too often itself be divisive and potentially discriminatory. By recruiting the best people for the job, we both enhance their self-esteem, irrespective of their background, racial or socio economic, and at the same time create an esprit de corps unmarked by tokenism.”

b) Climate change

Lots of new text for climate change, including the formation of a new committee, a strategy and risk management. Snippets below

“Like any group of people who cherish our environment both for our own sakes and for those of succeeding generations, S&U supports the Government’s Green Finance Strategy and is taking measures to reduce our carbon footprint and minimise and then eliminate carbon emissions so far as we are able directly to control them. This means that, particularly so far as Advantage Finance, our motor business and Head Office in Solihull are concerned, we need to monitor and reduce those areas of emissions which we can most directly control in order to achieve net zero status by 2030. ”

“A climate change committee chaired by the Chairman Anthony Coombs and consisting of senior executives and the Chairman of the audit committee meets on a quarterly basis to review the identification, assessment and management of climate change risks within the Group.”

“In addition in order to off-set those Scope one and two emissions, which we are not at present able to reduce to zero, we propose a range of measures including tree planting.”

“The Group identifies climate change risks through the climate change committee and the wider executive teams including the risk management teams of both our operating businesses, Advantage Finance Limited and Aspen Bridging Limited.”

I note SUS’s greenhouse gas emissions data show company cars generating 51 tonnes of CO2 during 2022 versus 49 for (pandemic blighted) 2021 and 115 for (pre-pandemic) 2020 — suggesting less travel and/or greater usage of electric vehicles (see point 1d) post pandemic.

Not quite sure why SUS’s air conditioning usage was listed within the 2021 report but dropped for 2022, and why other restatements left 2021 emissions at 117 tonnes of CO2 versus 146 reported originally.

6) BOARD OF DIRECTORS

The new director appointments (see point 1h) prompt some extra text.

Jack Coombs has swum the channel:

“Jack is also an avid supporter of charity and swam the Channel from England to France in 2011 in 13 hrs and 46 mins to raise funds for Alzheimer’s Research & Mondo Challenge ”

Jeremy Maxwell may have been recruited for his digital skills:

Jeremy brings broad expertise in digital innovation, marketing, commercial development and customer experience from over 25 years in the retail and B2B distribution industries. In addition to other NED and advisory roles, he has held senior customer-facing executive positions at Carpetright, Wolseley UK, Mothercare, Screwfix and B&Q. ”

Aside from Mr Maxwell, the three other non-execs have a variety of financial backgrounds.

7) DIRECTORS REMUNERATION REPORT

Nothing too untoward here.

Basic pay for the executives was unchanged for 2022:

Executive bonuses hit their maximums of £30k-£50k, which seem very fair given the group’s 2022 performance. Pension contributions meanwhile are a very generous 10%-plus for three of the executives, which I suspect is not the rate for ordinary staff.

Anthony and Graham Coombs enjoy hefty salaries and allowances, given the day-to-day operations are managed by Graham Wheeler (Advantage) and Ed Ahrens (Aspen). But quibbling over pay would be somewhat churlish given SUS’s long track record of dividend increases (pandemic aside) since the time the Coombs brothers took charge. Jack Coombs was paid a (pro-rata) £100k salary for 2022 and collected a £10k bonus, which seems very good value.

The Coombs brothers and the finance director receive pay rises matching those of the wider workforce for 2023:

Graham Wheeler deserves a 20% pay rise given his efforts over the pandemic, and which brings his wages closer to those of the Coombs brothers. Jack Coombs looks a genuine ‘thin cat’, with a 10% wage hike to £110k.

Bonuses were based partly on profit before tax surpassing £22.9m:

£22.9m compares to the actual £47.0m reported and the prior-year (and pandemic-disrupted) £18.1m. Will be fascinating to see what the PBT target is for 2023, as the £47m was bolstered by writing back some provisions.

Next year bonuses will be limited to £50k for all the executives bar Jack Coombs, who will receive a maximum £25k.

Ongoing use of “shadow“‘ LTIP options remains unusual:

Performance targets are “commercially sensitive“, and the options seems like a three-year bonus scheme. Options are nil-cost, and the executives simply ‘exercise’ the options for their cash bonus (assuming the secret targets are met). 6,000 options at the recent £22/share = a useful £132k, granted every year!

Only members of the Coombs family have material shareholdings:

Since his appointment in 2004, the finance director has managed only to garner 12,000 shares. The holdings (or lack of) among the non-execs is very sad — and would be quite alarming if it weren’t for the group’s illustrious track record. Why the non-execs have not wanted to share in the group’s success remains a mystery.

Shareholders were mostly happy with the 2021 pay arrangements:

8) GOVERNANCE

a) Audit committee report

No major changes to the text versus 2021. Met three times and “significant matters” considered by the committee remain impairment of receivables and revenue recognition, both within the Advantage car-loan division.

One day the committee may have to study Aspen:

“ As our Property Bridging Finance business is currently less material there were no issues and areas of judgement considered significant by the Committee in relation to Aspen Bridging.”

Unlike many smaller companies, SUS has an internal auditor (RSM). External auditor is now Mazars, following its appointment in 2021 after 20 years of employing Deloitte.

b) Corporate Governance

No major changes to the text versus 2021.

A nice reiteration of a “streamlined, non-bureaucratic, management structure“:

“Family investment and management has over the past 84 years been reflected in ambition for growth and for new markets buttressed by a conservative approach to risk, to treasury activities and to return on capital employed. The same culture is seen in “work force engagements” through employment stability, good communications and a streamlined, non-bureaucratic, management structure, as a staple of S&U well before the Governance Code even existed.”

SUS once again asks investors to consider its corporate governance “thoughtfully“:

“This has inevitably meant some departure from the detailed Provisions of the Code which primarily focusses on larger companies, a more formal approach to employee relations, a shorter history to establish a proven responsible culture, and a divorce between equity and management. We have carefully explained the reasons for any departures and will hopefully, as the revised code requires, now see these considered by investors and their representatives “thoughtfully” and not evaluated in “a mechanistic way”.”

Chairman Anthony Coombs contravenes best practice as chairman on three counts: i) he is an executive, ii) he is also chief executive, and iii) he was appointed to the role more than nine years ago (2008).

Confirmation non-exec Jeremy Maxwell was appointed for his digital skills:

“It is noteworthy that the appointment of Jeremy Maxwell was conducted in a professional and robust manner with the engagement of a recruitment company searching extensively a range of potential applicants for the newly created role to oversee the Group’s digital marketing initiatives.”

More on the “majority female shortlist” (see point 1h):

“This exercise resulted in a final selection of five potential candidates: three females and two males. One female and one male candidate were invited to an orientation visit to the operations of Advantage Finance in Grimsby and Jeremy Maxwell was ultimately considered the most engaged and appropriate candidate for appointment. Through the robust nature of this recruitment process it is demonstrable that the S&U Group is fully committed to ensuring that gender balance on the Board is achieved wherever possible while adhering to the core business principles of appointing the right person for the role.”

Jack Coombs was appointed (understandably) because of his family connections:

“The appointment of Jack Coombs, as an Executive Director, was considered appropriate given both his significant family shareholding and the additional business and accounting skills – he is a chartered accountant-that he brings to the Board.”

Pleasing to see all board/committee meetings were attended, and more audit meetings than remuneration meetings:

9) INDEPEDENT AUDITOR’S REPORT

The switch from Deloitte to Mazars meant this year’s auditor text was constructed differently, although the gist of the text was very similar.

For 2021, the ‘Conclusions relating to going concern’ had six bullet points…

“* obtaining and reading management’s going concern assessment, which included specific consideration of the impacts of the Covid-19 pandemic and the group’s operational resilience, in order to understand, challenge and evidence the key judgements made by management;

* assessing financing facilities in place including the nature of such facilities and their repayment terms, as well as understanding associated covenant conditions and re-performing covenant calculations to evaluate whether they had been complied with;

* challenging key assumptions used in the forecasts such as growth rates based on historic trends and future outlook, including assessing the amount of headroom and the impact of sensitivity analysis;

* testing the clerical accuracy of those forecasts, assessing the historical accuracy of forecasts prepared by management, comparing post balance sheet actual results against forecasts and assessing consistency with forecasts used for other business purposes;

* reviewing correspondence with regulators to understand the capital and liquidity requirements imposed by the group’s regulators; and

* assessing the appropriateness of related disclosures in the financial statements.”

…while the same section for 2022 had eleven bullet points:

“* Undertaking an initial assessment at the planning stage of the audit to identify events or conditions that may cast significant doubt on the group’s and the parent company’s ability to continue as a going concern;

* Obtaining an understanding of the relevant controls relating to the directors’ going concern assessment;

* Making enquiries of the directors to understand the period of assessment considered by them, the assumptions they considered and the implication of those when assessing the group’s and the parent company’s future financial performance;

* Challenging the appropriateness of the directors’ key assumptions in their cash flow forecasts, as described on page 17, by reviewing supporting and contradictory evidence in relation to these key assumptions and assessing the directors’ consideration of severe but plausible scenarios. This included assessing the viability of mitigating actions within the directors’ control;

* Testing the accuracy and functionality of the model used to prepare the directors’ forecasts; Assessing the historical accuracy of forecasts prepared by the directors;

* Engaging in regular discussions with the directors regarding the status of negotiations in respect of new financing options;

* Reviewing regulatory correspondence, minutes of meetings of the Audit Committee and the Board of Directors, and post balance sheet events to identify events of conditions that may impact the group’s and the parent company’s ability to continue as a going concern;

* Assessing and challenging key assumptions and mitigating actions put in place in response to the impact of the Covid-19 pandemic;

* Considering the consistency of the directors’ forecasts with other areas of the financial statements and our audit; and

Evaluating the appropriateness of the directors’ disclosures in the financial statements on going concern. ”

On the other hand, the key audit matter for ‘impairment of amounts receivable from customers’ was addressed by seven bullet points for 2022…

…while the 2021 text devoted a full page to addressing that particular key audit matter.

Whether the increased/decreased volume of text from one year to the next indicates the auditor spending more/less time on a particular aspect of the audit is not easy to say. At least the auditor’s report maintained the other key audit matter — revenue recognition — and did not raise any alarming warnings throughout the entire text.

Materiality returned to the standard 5% of pre-tax profit for 2022 while scope was 100% of revenue, profit and net assets.

10) ACCOUNTING POLICIES

a) Revenue recognition

Includes the following snippets of new text for 2022, which clarify a variety of matters:

“Revenue starts to be recognised from the date of completion of the loan – after completion, hire purchase customers have a 14 day cooling off period during which they can cancel their loan.

…

This results in more of our net receivables being in stage 3 and the associated stage 3 loan loss provisions being higher than if we adopted a more prime customer receivables approach of 3 months or more in arrears. Our approach of 1 month or more in contractual arrears is based on our historic observation of subsequent loan performance after our customers fall 1 month or more in contractual arrears within our non-prime motor finance customer receivables book.

…

However, if a customer’s payment holiday finished more than 12 months ago and they are unimpaired 12 months later then an account will not be in stage 2 as the customer’s post payment holiday record now indicates low risk at the reporting date. This is why the volume of customers in stage 2 reduced at 31 January 2022.

…

The macroeconomic overlay assessments for 31 January 2022 reflect that further to considering such external macroeconomic forecast data, management have judged that there is currently a more heightened risk of an adverse economic environment for our customers and the value of our motor finance security. To factor in such uncertainties, management has included an overlay for certain groups of assets to reflect this macroeconomic outlook, based on estimated unemployment, inflation and used vehicle price levels in future periods.

…

Assets in both our secured loan businesses are written off once the asset has been repossessed and sold and there is no prospect of further legal or other debt recovery action. Where enforcement action is still taking place, loans are not written off. In motor finance where the asset is no longer present then another indicator used to determine whether the loan should be written off is the lack of any receipt for 12 months from that customer.”

b) Critical accounting judgements

A new macro-economic table was introduced for 2022:

The extra text was noted in my blog post above. Seems to me as if SUS expects unemployment to rise from 3.8% to 5.65% by 2025, and inflation to fall from 5.7% to 1.81% by 2025. Could be extreme wishful thinking on the latter, given headline inflation is c10% at present.

A £402k impairment loss for every 0.5% advance to the inflation rate could mean going from 5% inflation to 10% inflation will lead to an extra £4.02m impairment.

11) ACCOUNTING NOTES

a) Employees

Nothing obviously amiss here:

200 workers collecting wages of £9.1m gives an average wage of £46k, higher than the pandemic-impacted £40k for 2021 but actually lower than the £48-49k for 2016 and 2017. Revenue per employee was £439k and just about matched the £441k for 2021, but was the lowest since 2015 (£407k). This measure reached £540k during 2018.

Perhaps impressively, the 173 staff members at Advantage each look after gross customer loans of almost £2m, which matches the figure witnessed during the previous four years. The 17 staff members at Aspen meanwhile each look after gross customer loans of £2.9m, up from £2.1m the previous year and £1.3m for 2018.

b) Operating costs

SUS’s costs are a little mysterious. Admin costs of £3m are not disclosed out of a £14m total:

Presumably the £3m consists of listing costs etc. I note the new auditor did not arrive with lower fees.

c) Borrowings

The vast majority of SUS’s debt facilities are not up for renewal until at least 2024:

The small-print says the company borrows at 4% and lends out at 25%:

“The average effective interest rate on financial assets of the Group at 31 January 2022 was estimated to be 25% (2021: 27%). The average effective interest rate of financial liabilities of the Group at 31 January 2022 was estimated to be 4% (2021: 4%)..

The 25% was 27% for 2021, and 28% or more between 2008-2020. So borrowers are paying less, which could mean higher quality borrowers or greater competition squeezing rates. The figures were lending out at 22% and borrowing at 6% during 2007!

A 1% higher interest rate would knock profit by £0.9m:

“If interest rates had been 1% higher/lower and all other variables were held constant, the Group’s…profit for the year ended 31 January 2022 would decrease/increase by £0.9million (2021: decrease/increase by £0.8million). This is mainly attributable to the Group’s exposure on its variable rate borrowings.”

That 1% increase could not be passed onto existing customers, as the contract repayment terms are fixed at the time of inception (I believe).

d) Working capital

Very small numbers here:

e) Options

Just 5,500 options left to exercise (versus a share count of 12.1 million):

No further option grants are planned (just ‘shadow’ options, see point 7).

f) Defined-benefit pension scheme

A tiny pension scheme, which is likely to self-fund itself with assets of £1.1m having to generate a yearly benefit payment of £41k:

Maynard