Last updated: 05 January 2019

By Maynard Paton

This blog page expands on How Shares Helped Me Quit The Day Job and is for anyone who wishes to pay off their mortgage and give up the 9-to-5.

I became mortgage-free during 2011 aged 40, and made the leap from conventional employment at the start of 2015 aged 43.

I am convinced anyone with a passion for shares and the determination to retire early can take the same path.

Thousands of bloggers currently write about the so-called Financial Independence Retire Early — or FIRE — movement.

When you read my story below, you will notice important differences to the typical FIRE blog:

- I do not hide behind a pseudonym;

- I actually live mortgage-free and have given up full-time employment, and;

- I provide real-life figures to explain what happened.

Attaining a ‘FIRE’ lifestyle boils down to the following:

- Working hard;

- Saving lots;

- Keeping records;

- Investing well, and;

- Not stopping.

Importantly, I did not:

- Inherit wealth;

- Marry wealth, or;

- Win wealth.

You may be pleased to know that my story does not involve a university degree, a professional qualification or an early high-flying job.

Instead, my story involves mundane matters such as redundancy, renting, commuting into London and supporting a young family.

Maybe luck has played a part. That said, you do make your own luck in life. Read my story below and decide for yourself about any good fortune.

Contents

- Working hard: From £5,271 to £27,000 within 10 years

- Saving lots: Enjoying a 30% savings rate

- Keeping records: Tracking every penny

- Investing well: ISA stock-picks 2004-2007

- Investing well: Selling almost everything for cash 2008-2010

- Investing well: ISA stock-picks 2011-2014

- How much I required to make the leap from full-time work

- Drawbacks to becoming a full-time investor

- Unexpected benefits of becoming a full-time investor

- Earning a side-income from SharePad

- Saving lots: An important lesson about family life

- A few clarifications

- A 10-point summary of my story

- Take your first step right now

Working hard: From £5,271 to £27,000 within 10 years

I left school during 1989 aged 18 and became a Poll Tax clerk for my local authority.

However, computing had been a hobby during my school years and I was keen to start work in IT.

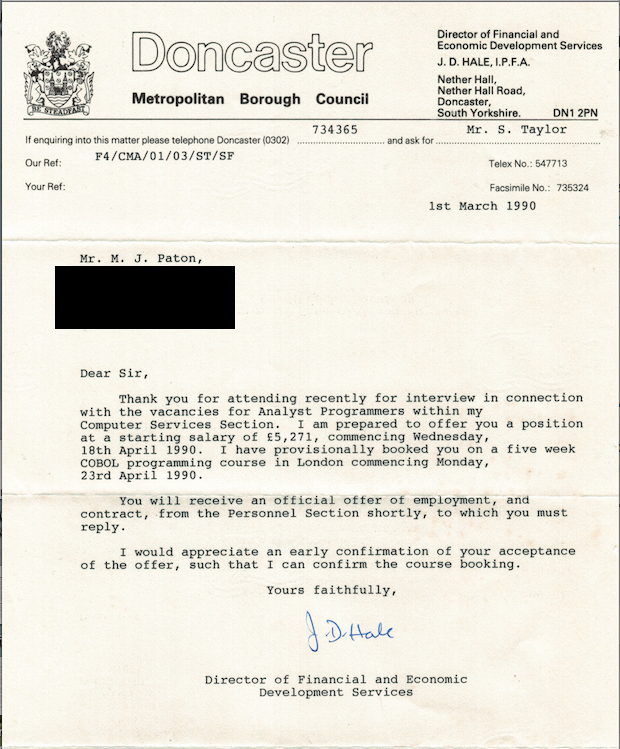

I was therefore very pleased when my career proper started in 1990 as a computer programmer with the same employer.

My starting salary was £5,271:

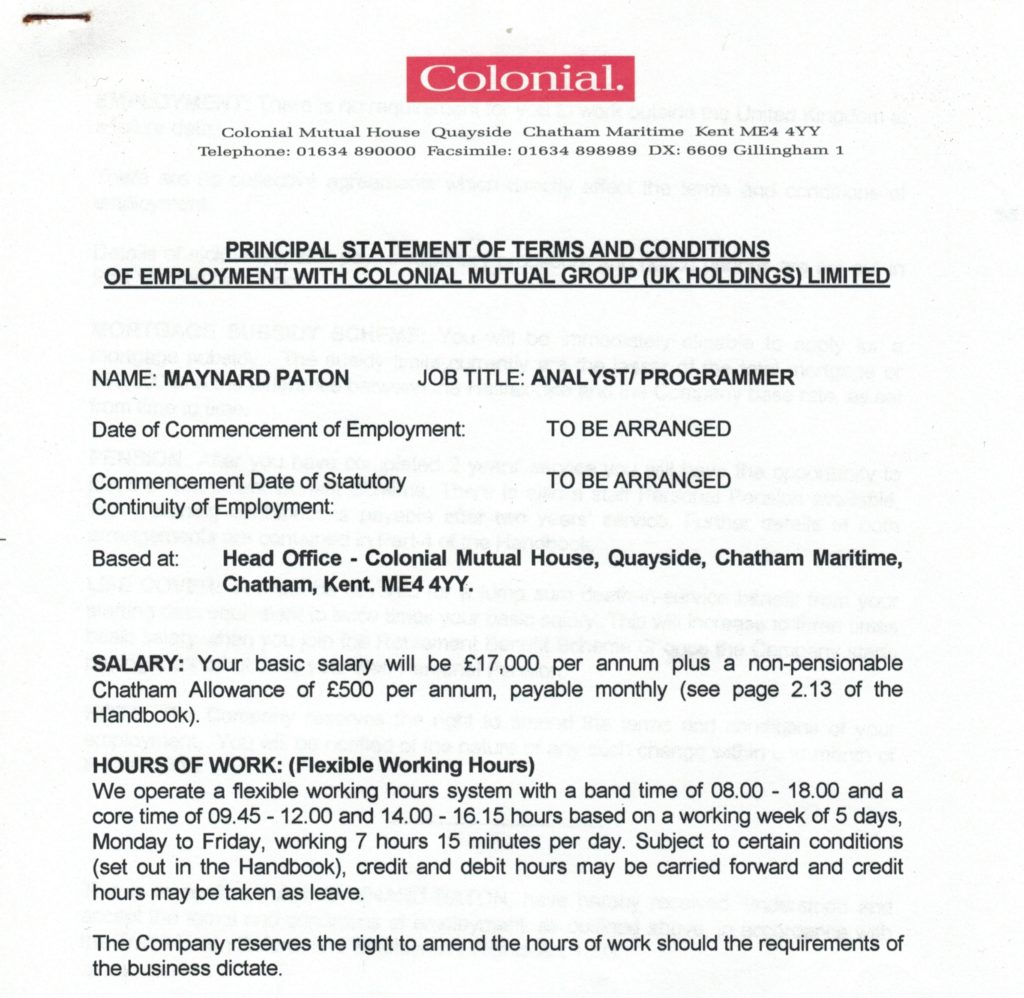

By 1996 I thought my IT prospects were better ‘down south’, and I decided to move on. I started my next job earning £17,500:

I soon realised this new IT role was not working out. I therefore decided to concentrate more time on my stock-picking hobby.

I had started dabbling with shares during 1993 and my plan now was to move from IT into an investing career.

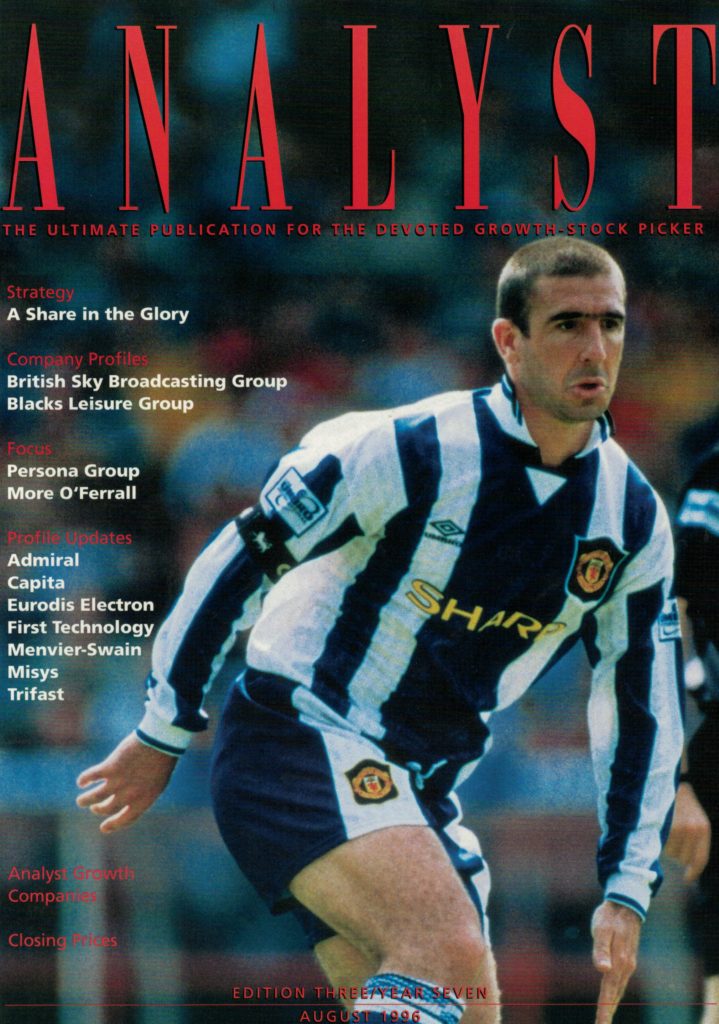

I learnt all I could about investing. I taught myself about accounting and read a high-brow publication called Analyst:

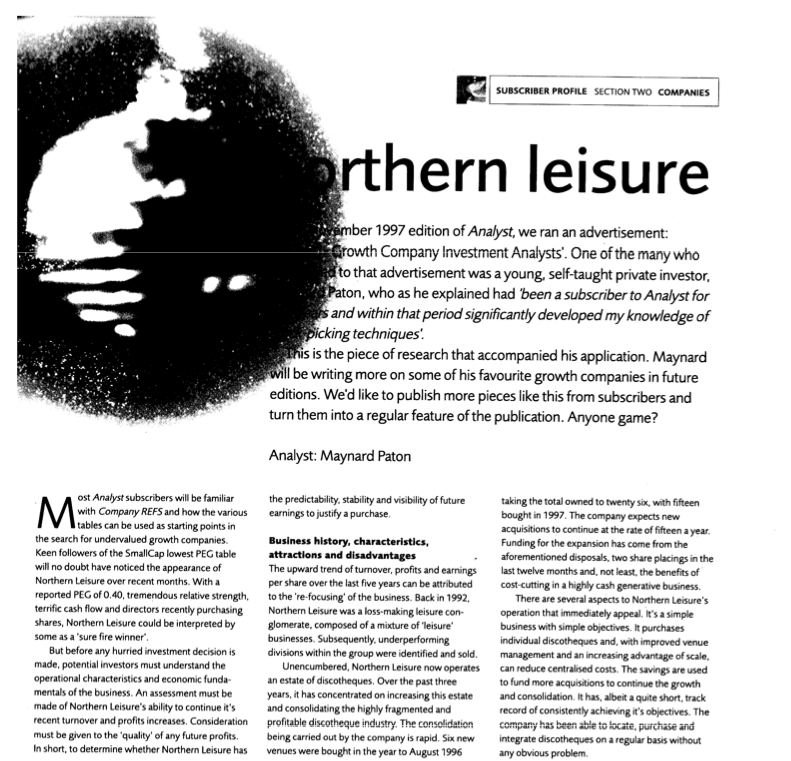

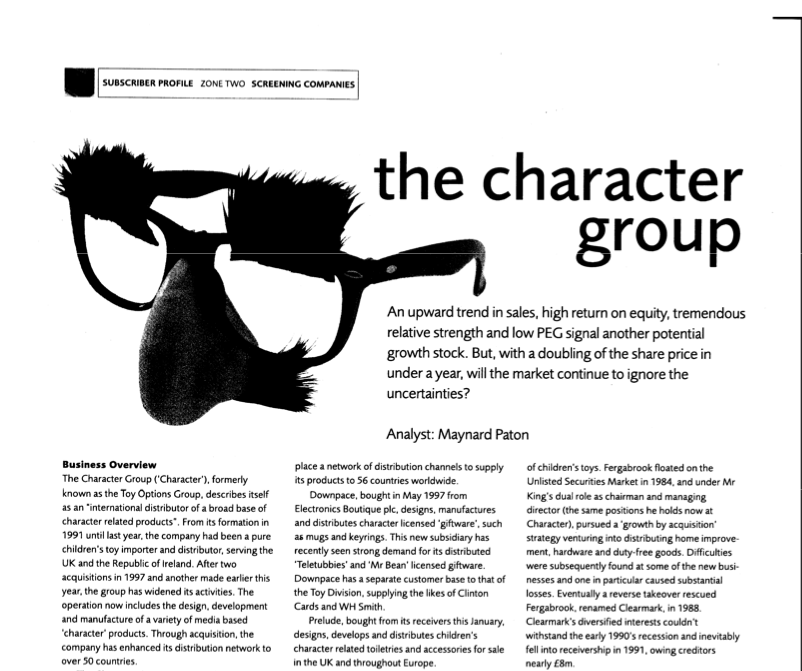

I got nowhere applying for mainstream investing jobs, but I did manage to write three articles for Analyst during 1998:

My Analyst articles on Northern Leisure, Character Group and Moss Bros can be downloaded here.

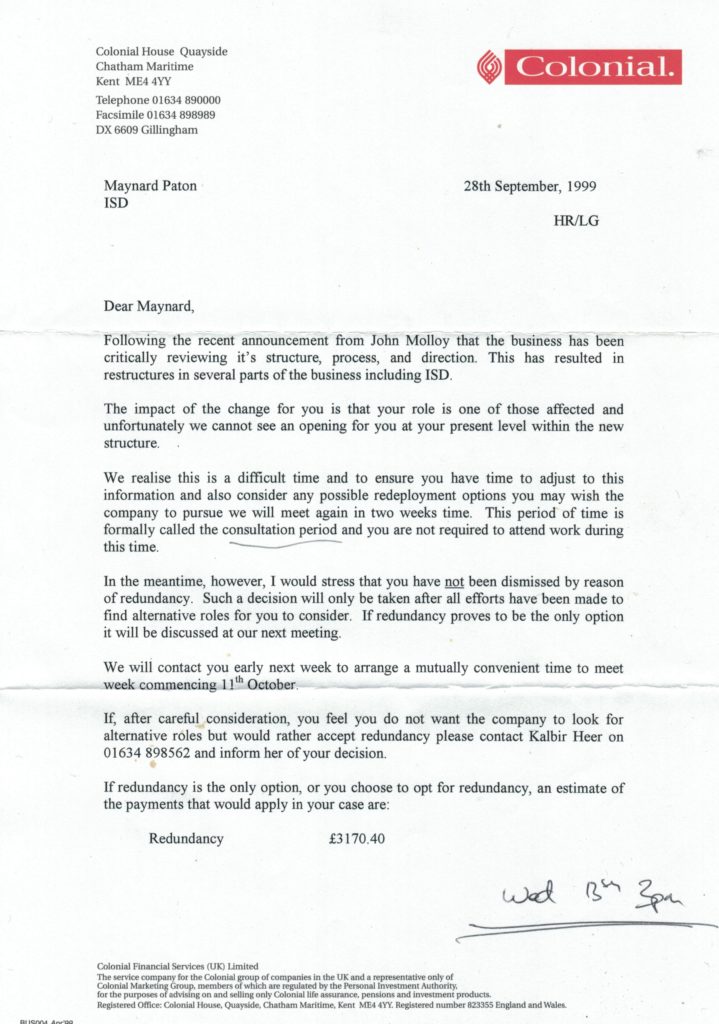

Bad news came in 1999. I was made redundant from my IT job:

However, I had already found my new investing career.

The day after my redundancy, the following letter arrived in my inbox:

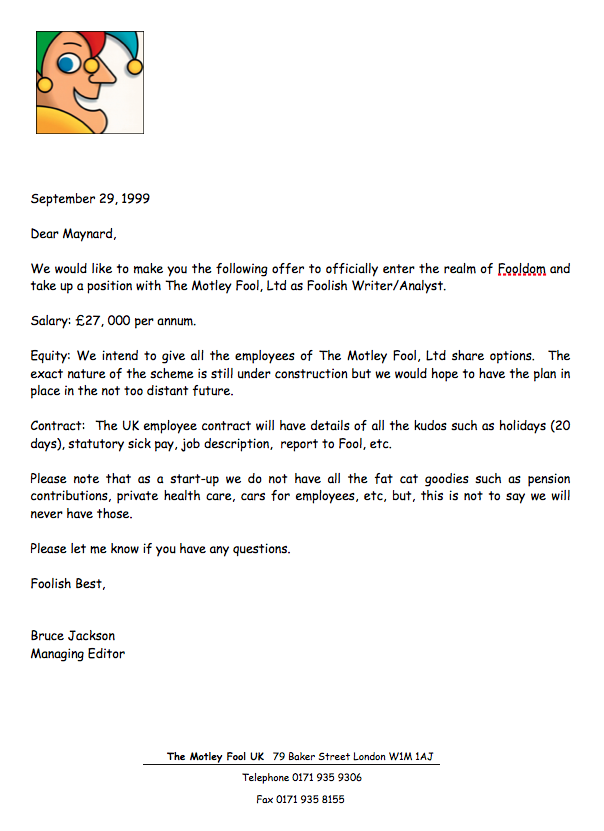

Those Analyst articles helped me secure a job at The Motley Fool UK, a financial website based in central London. I was 28 and my salary was now £27,000.

Saving lots: Enjoying a 30% savings rate

You can see I did not enjoy a vast salary during my 20s.

And yet this period was perhaps the most important for my FIRE journey — although I did not know that at the time.

I invested £21,000 into ISAs and PEPs between 1995 and 1999. Those contributions equated to approximately 20% of my total gross pay during those five years.

I bought my first house during this period, too.

I purchased a £71,500 two-bed semi with a 10% deposit during 1998. Include saving for that deposit, and my estimated savings-to-gross-pay ratio approached 30%.

The house was hardly a mansion. But I was fortunate to buy when property was relatively cheap.

I married in 1999, and 2000, 2001 and 2002 saw me inject £39,000* into my (and my wife’s) ISA.

These three years were another important period for my FIRE journey — I estimate those ISA contributions represented at least 30%** of my aggregate gross salary.

(*includes redundancy money **excludes redundancy money)

I even survived two rounds of redundancies at Motley Fool during the 2001-2002 dotcom crash.

So far then, so good.

But a significant change now occurred.

I became a father during 2003 and the two-bed house was suddenly too small. At the start of 2004, we sold up:

The house sale provided a £78,000 cash profit. We decided to move into rented accommodation after the chain further up fell apart.

Keeping records: Tracking every penny

I started proper income and expenditure record-keeping at the start of 2004.

You see, my wife had stopped work to look after our young son — and the monthly rent was more than double my old mortgage payment. Bills such as council tax increased substantially as well.

I had to ensure we were not spending more than I was earning, and so I tracked every penny using MS Money.

For some perspective, at the start of 2004:

- My Motley Fool salary, commissions and bonuses that year would come to £50k;

- My ISA shares and cash savings (including the house-sale proceeds) were £183k, and;

- My debt was zero.

Not a bad financial position for someone just about to turn 33.

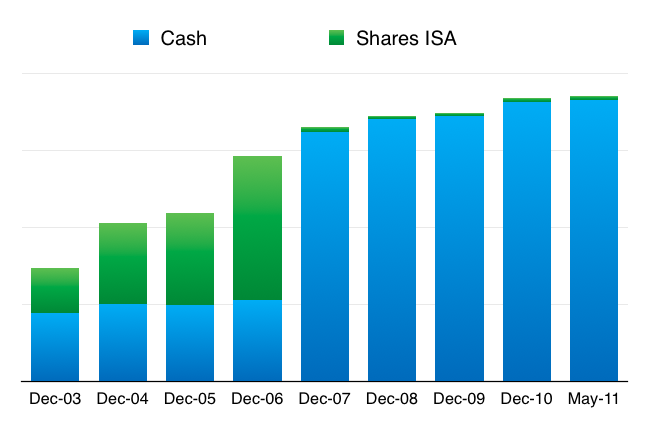

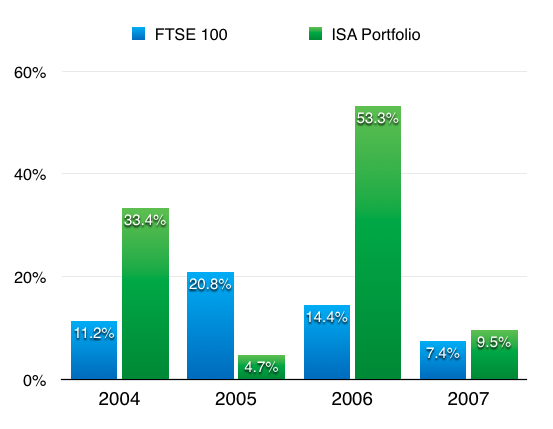

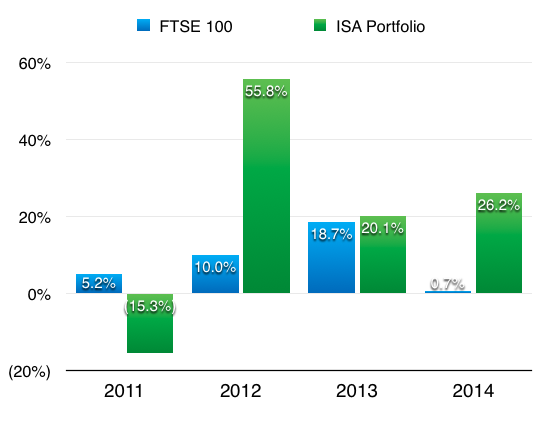

The following chart shows how my ISA shares and cash savings advanced until I bought another house (this time outright) during mid-2011:

Two important points:

- My shares did really well between 2004 and 2006, and;

- I sold almost all my ISA shares during 2007.

Let me explain what happened.

Investing well: ISA stock-picks 2004-2007

The 2004-2007 period overlapped with me managing/writing a ‘Quality Portfolio’ series of articles for Motley Fool.

This ‘Qualiport’ portfolio was run on Warren Buffett-type principles and sought to invest in great companies at reasonable prices that could be held for the long term.

My own ISA investments were selected on very similar lines. The table below shows the shares I owned and their associated weightings:

| Holding | Weighting 31 Dec 2003 (%) | Weighting 31 Dec 2004 (%) | Weighting 31 Dec 2005 (%) | Weighting 31 Dec 2006 (%) | Weighting 31 Dec 2007 (%) |

| Assoc British Ports | - | 10.1 | 10.7 | - | - |

| Carpetright | 17.8 | - | - | - | |

| DFS | 9.7 | - | - | - | |

| Games Workshop | 18.3 | 14.7 | 5.4 | 3.7 | - |

| Halma | 6.4 | 4.7 | 4.9 | 3.8 | - |

| Johnston Press | 20.8 | 15.8 | 12.0 | 6.4 | 7.4 |

| London Stock Exchange | 23.4 | 39.5 | 38.8 | 28.2 | - |

| Instore | - | - | - | - | 31.1 |

| iShares FTSE 100 | 2.5 | 1.8 | 14.5 | 49.3 | 49.9 |

| Nokia | - | 11.2 | 13.5 | 8.4 | 7.5 |

| Cash | 1.1 | 2.2 | - | 0.2 | 4.1 |

| TOTAL | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

I ran a very concentrated portfolio.

Here are my returns (in green):

The big gains came almost entirely from the London Stock Exchange. I bought LSE shares during 2004 and sold during 2006 and 2007 for an overall 297% profit.

Other winners bought and sold during the same period were Associated British Ports, up 117%, and Nokia, up 146%.

I bought iShares FTSE 100 during this period as well.

My position as a Motley Fool share tipster meant my personal share dealings became restricted due to various regulatory reasons. I therefore decided to invest any new money in an index tracker.

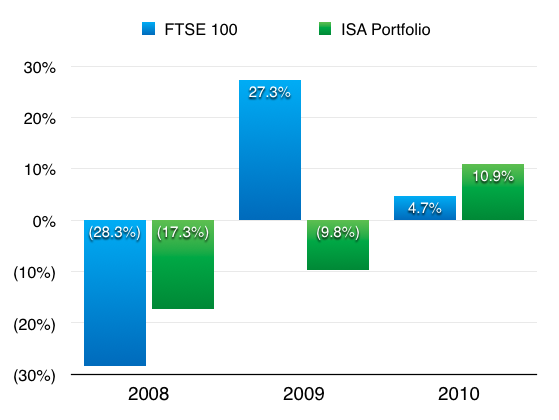

Investing well: Selling almost everything for cash 2008-2010

During 2005 and 2006, I felt house prices had become too expensive. I therefore actively decided to continue renting while awaiting a property downturn.

Then came the run on Northern Rock, which told me the banking sector was in trouble and the effects on the housing market could be substantial (or at least I hoped they could be substantial).

To ensure I was ready to purchase a great home at a cheap price, I sold almost all my shares during the autumn of 2007.

The proceeds then left my ISAs for various high-yield savings accounts.

At the start of 2008, just about every penny I owned was in cash. My ISAs were left with a few tiny holdings that I had overlooked during my selling spree.

My portfolio record-keeping (but not my income and expenditure record-keeping) now became very lax. I often went months without recording share prices and I am sure my ISA details below are inaccurate:

| Holding | Weighting 31 Dec 2008 | Weighting 31 Dec 2009 (%) | Weighting 31 Dec 2010 (%) |

| Instore | 14.4 | - | - |

| iShares FTSE 100 | 55.9 | 52.5 | 46.0 |

| Nokia | 6.0 | 6.5 | - |

| Record | - | - | 25.3 |

| Cash | 23.7 | 41.0 | 28.7 |

| TOTAL | 100.0 | 100.0 | 100.0 |

I must confess to being tempted to reinvest some of my 2007 share-sale proceeds back into the market during late 2008.

However, I decided not to be too clever and instead sat on the cash for the right housing purchase.

In retrospect, I was a little lucky selling my shares when I did. I never thought the stock market would collapse to the level it did during 2008/09 (down c40%).

I finally purchased a house (outright) during 2011. I slowly realised rock-bottom interest rates were never going to create the property bargains I had previously imagined.

I still had to work, but at least I owned a house without a mortgage. I was 40 years old.

Investing well: ISA stock-picks 2011-2014

Around the same time as buying the new house, I gave up on my Motley Fool share-tipster duties.

Both events allowed me to once again invest freely.

I should add that my stock-picking approach changed between 2007 and 2011.

This time around, I concentrated on smaller companies where owner-management, cash-rich balance sheets and lowly valuations appeared to offer decent upside with lower risk.

During my years as a share tipster, I discovered many companies that exhibited such traits went on to perform quite well for my subscribers.

In addition, there were many more of these small-cap opportunities to study than Buffett-type stocks such as the London Stock Exchange.

Here are my 2011-to-2014 ISA weightings and returns:

| Holding | Weighting 31 Dec 2011 (%) | Weighting 31 Dec 2012 (%) | Weighting 31 Dec 2013 (%) | Weighting 31 Dec 2014 (%) |

| Abbey Protection | 21.2 | 14.8 | 8.9 | - |

| City of London Inv | 14.1 | 15.3 | 18.2 | 19.2 |

| Elec Data Processing | - | 5.7 | 8.0 | 5.9 |

| French Connection | 10.2 | 19.3 | 18.0 | 16.7 |

| Getech | - | - | - | 4.2 |

| M Winkworth | 10.3 | 5.4 | 4.0 | 1.4 |

| Pennant International | - | - | 1.4 | 1.1 |

| Record | 19.5 | 14.6 | 12.4 | 8.3 |

| Robert Wiseman Dairies | 4.8 | - | - | - |

| SeaEnergy | - | - | 11.0 | 7.8 |

| Soco International | - | 18.4 | 15.8 | - |

| Tasty | 3.4 | |||

| Tristel | - | - | 2.1 | 14.1 |

| Cash | 19.9 | 6.5 | 0.2 | 17.9 |

| TOTAL | 100.0 | 100.0 | 100.0 | 100.0 |

After a rocky investing comeback during 2011 (when all of my shares lost money!), a fabulous 129% total return from Record carried my portfolio during 2012.

I then enjoyed a broad spread of winners during 2013, while City of London Investment, French Connection and Tristel ensured a very satisfactory 2014.

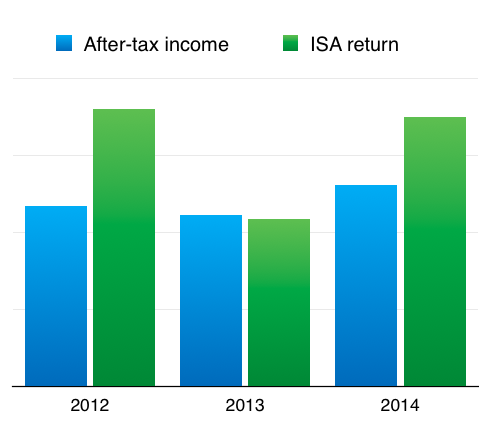

How much I required to make the leap from full-time work

How did I know when my investments could allow me to quit the day job?

Comparing my after-tax employment income to my ISA returns suggested the time was right at the end of 2014:

I needed ‘only’ a 6.8% annual ISA return to pay my (then) living expenses.

In light of my 2012-to-2014 ISA performance, I made the FIRE leap and gave up the 9-to-5 at the start of 2015. I was 43 years old.

I made a last-minute decision to sell 17% of my ISA shares to ensure I had three years’ worth of living expenses on hand in cash.

That way, I thought I could ride out any market downturn and not have to sell at low points to fund my expenses.

The decision meant I now had to earn 8.2% a year from my capital.

My formula for quitting the day job was therefore:

Required capital = ( Expenses / 8.2% ) + ( 3 * Expenses )

I said to my wife that I would re-assess my early-retirement plan after three years. If my ISA returns were not sufficient, I would ditch this blog and seek employment at the local Tesco.

(For context, Warren Buffett is quoted in the book The Snowball: “I had about $174,000 and I was going to retire. I rented a house… for $175 a month. We’d live on $12,000 a year. My capital would grow.” He was 26 and required a 6.9% annual return).

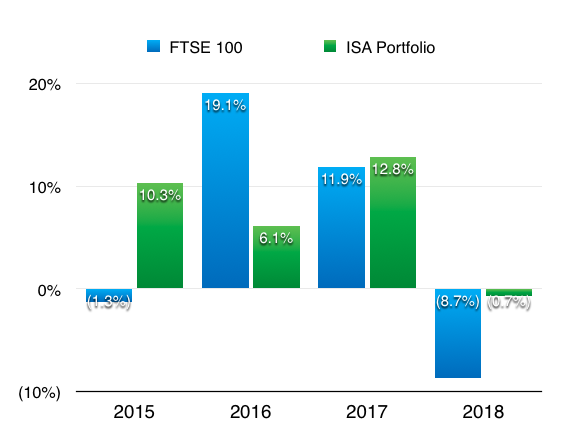

Drawbacks to becoming a full-time investor

So far at least, my ISA returns (in green) have been sufficient:

Between 2015 and 2018, my ISA’s compound average growth rate has been 9.4%.

But the returns as a full-time investor have not been as great as I had expected.

I have since realised that my gains have been curbed by the following two drawbacks:

- Not having a regular salary to easily average down, and;

- Thinking too much about locking-in profits to fund my living expenses.

Unexpected benefits of becoming a full-time investor

On the other hand, I have made surprisingly good progress on my living expenses:

Just so you know, my expenses cover all the basics:

- Supermarket expenditure (food, toiletries, and so on);

- Monthly bills (council tax, electricity, gas, water, broadband, and so on);

- Motor expenditure (fuel, servicing, and so on);

- Insurance (life, house and car), and;

- Investment (websites, travel, subscriptions, and so on).

Plus every so often, I am faced with an unexpected large cost (for example, a new boiler).

Still, something I did not expect when I quit the 9-to-5 was having the time to learn some (much-needed) practical skills. Courtesy of Youtube, my new talents include:

- Clearing blocked drains;

- Fitting a loft-tank ballcock valve;

- Fitting a toilet flusher washer;

- Fitting an oven element;

- Fitting car headlight bulbs (fiddlier than it sounds);

- Re-hanging a fridge door, and;

- Re-jigging electrical socket wiring.

I have also enjoyed more time to think about cutting my wider expenditure.

For instance, my supermarket spending has reduced by £1,000 a year since giving up full-time work. No more expensive packaged meals for a time-pressed father, and much more fresh food and my cooking for the family.

All told, my living expenses have reduced by between 10% and 15% after leaving full-time employment.

Following my portfolio gains and lower expenditure, at the start of 2019 I required a 5.6% annual ISA return to cover my living costs.

Earning a side-income from SharePad

Helping to cover my expenses from September 2018 has been my side-income from SharePad.

Writing this blog provided me with an unexpected benefit — you never know who is reading and what the Contact form may deliver:

“Hi Maynard, as you may have heard Phil Oakley is leaving us and I am looking for intelligent investors who might be interested to write for us on whatever frequency suits them. Both Phil and Richard Beddard rate you highly. I note the comment on your Contact page about guest blog posts but would it be worth a conversation?”

— an e-mail from SharePad (July 2018)

My decision to become a SharePad contributor was not difficult.

I had used the investment software since 2015 and considered it to be an exceptional service for private investors. I also rated the educational and analytical articles that SharePad had published.

I thought the SharePad income could assist my investment returns. For one thing, I would not have to think as much about withdrawing capital to fund my living expenses.

Up until writing for SharePad, I had received no freelance or employment income since leaving Motley Fool.

Factor in SharePad, and at the start of 2019 I required an approximate 3% annual ISA return to cover my living expenses — and my projected ISA dividend income for the year was 3.4%.

I therefore currently live off my ISA dividends combined with my SharePad income, with enough cash on hand outside of my ISA to fund my living expenses for 2019, 2020 and 2021.

I must admit, this position feels more comfortable than my original 2015 plan.

Saving lots: An important lesson about family life

Let me track back to the start of 2004.

I was renting a more expensive house, my wife had stopped work and we now had a six-month old son. Needless to say, my savings rate plummeted.

Between 2004 and 2014 my aggregate gross salary and other employment income was spent as follows:

- 28% on tax and national insurance;

- 21% on general credit-card expenditure;

- 17% on rent;

- 6% on company pension contributions;

- 6% on train season tickets (which seems low in hindsight);

- 5% on monthly bills (which also seems low);

- 5% on other expenditure, and;

- 12% transferred to ISA/cash savings

As I have mentioned, I had been socking away 30% into ISAs prior to 2004.

And note: the above 2004-2014 stats involve natural frugality that included (among other things) taking a packed lunch into work every day.

The lesson is obvious: anyone thinking about retiring early really has to save lots and invest well before starting a family.

Once you become a parent, move to a larger house and your parter (perhaps) gives up work… the savings become much harder to make.

A few clarifications

Before I conclude, a few clarifications:

- My investments were held within ISAs and no capital gains tax has ever been paid;

- My SIPP has not been relevant to obtaining a FIRE lifestyle, and has therefore been excluded from the above analysis;

- Differences between the information within the above analysis and on my Portfolio page are due to the exclusion of my SIPP, and;

- My wife is not rich. Between 2003 and late 2018, she either did not work or worked part-time on a wage that rarely troubled HMRC. She pays for holidays and miscellaneous family items.

A 10-point summary of my story

Could you repeat my savings rate and investment returns, and make the FIRE leap for yourself?

One thing is for certain. If you never try, you will never find out.

Looking back, my story can be summarised in ten points.

I had to:

- Start at the bottom and work my way to a higher salary;

- Have a keen interest in shares;

- Secure another job just before being made redundant;

- Live relatively frugally to be able to invest up to 30% of my gross salary;

- Employ ISAs to avoid paying capital gains tax;

- Avoid all debt except for a mortgage;

- Continually find attractive shares (admittedly easier to do when writing full-time about investing, as I was at Motley Fool);

- Concentrate my portfolio on my very best ideas;

- Enjoy a mini housing boom, and;

- Make a very bold move to sell (almost) everything based on a property judgement.

On the downside, I spent several years as a share tipster during which time I held mostly cash or a tracker. Neither are conducive to exceptional long-term returns.

And while I escaped the 2008 stock-market carnage, I also missed re-investing during the 2009 lows.

Take your first step right now

I hope you found my story informative. Maybe you can join me one day, and spend your 9-to-5 reading and writing about shares as well.

Recording your exact income and expenditure must be your first step. I use an ancient copy of MS Money.

You will almost certainly under-estimate your total expenditure. And you will be shocked at the amount you spend each year on certain items or within certain shops.

Use that information to cut out all unnecessary expenses. Then assess how much you need to live on and then how large your ISA pot must become.

Becoming mortgage-free and retiring early does not involve any great secret.

You just have to:

- Work hard;

- Save lots;

- Keep records;

- Invest well, and;

- Don’t stop.

Oh, and one more point:

- START NOW

Please let me know how you get on in the Comment box below or on the dedicated Quidisq FIRE discussion board.

Good luck.

Maynard Paton

Disclosure: Maynard owns shares in City of London Investment, Getech, M Winkworth, Tasty and Tristel.

Hi Maynard

Thank you for an interesting and motivating blog. I became mortgage free about the same age as you but did not retire until I was about 55. The reason is straightforward: although I was working hard and saving lots, I didn’t know how to invest. I have been following Motley Fool for about 15 years and now your blog too, and, despite starting so much later, am able to enjoy the FI if not the RE of FIRE.

Thank you again for being so open and educational in your blog.

Deb

Hello Deb,

Thanks for the comment. I am glad you find my blog useful. I am super-impressed you became mortgage free without knowing how to invest! Well done.

Maynard

Maynard

Great story…. let us know when you feel it’s time to turn investments to cash again, that was a great move to avoid the 2008 crash.

I’m 58 this year and will hang up my boots by age 60. I have so many investment elements with various pensions etc tied up in the stock market it’s scary but over time it always seems to work out

David

Hello David

I will let you know when the time has come to consider cashing up. I have to admit, such extreme times do not come around that often, they can be very stressful, and repeating the trick may not be easy. I am quite happy having made such a call just the once.

Maynard

Thank you Maynard, interesting to read your story and appreciate your blog.

Like you I hold CLIG and M WINK. I have a high yield income strategy as I feel it is more easier to cover its expenses with a dividend cash-flow rather than selling shares. After I will reach FIRE I will consolidate my financial fortress with blue-chip companies, the yield becoming less important.

Thanks Eric. I think I may be turning into a higher-income investor. Good luck with your FIRE portfolio.

Maynard

Hi Maynard,

Thanks for sharing your story, which was interesting to read about.

Perhaps it reflects your risk tolerance, but in a low interest rate environment such as currently, do you think it makes sense to not have a mortgage? I.e. if you can borrow a decent amount at say 2% interest rate, and expect to earn significantly more than that from investing, why not?

I am somewhat younger, and currently have a significant mortgage set up as interest only, along with a decent investment portfolio. If interest rates stay where they are, I’m not inclined to try to reduce the mortgage outstanding any time soon. Provided investment returns are good, then this approach should lead to a much better result long term, than if all the investments were sold to pay down mortgage debt. Obviously if the investing goes badly, I will still have to deal with the mortgage.

Hello Alan,

Your strategy would seem sensible assuming you are in full-time work, have the prospect of greater career earnings ahead and are a reasonable investor. Indeed, the mortgage I had (for 5-6 years) was interest-only and my returns beat the payable rate. But at the time I was in full-time work and had the prospect of greater career earnings ahead, so if my portfolio went wrong I could earn back what I lost.

Paying off the mortgage gives you lifestyle flexibility over ‘geared’ financial returns. In time you may find you do not want to work full-time. At least that’s what happened to me.

Regards

Maynard

Well done, Maynard; and it worked because you had a plan rather than luck.

My journey is somewhat similar: married with 3 children by age 28, so I had higher outgoings and less to save.

I worked full time to age 50 and then 10 years part time.

The secret was committing to regular monthly pension savings. Discipline, action, and a long term perspective.

For those starting today it is harder due to (1) ridiculous housing costs (2) the prospect of secular stagnation with lower returns; but I suspect with your skills you will do better.

Thanks Lawman. The secret as you say is committing to regular investing. Not many people want to do that.

Maynard

Great article and thank you for sharing.

I’m not sure if you’ve shared this elsewhere on the blog but what investment platform do you use?

thanks

David

Hi David

Glad you liked the article. I use these stockbrokers.

Maynard

Hi Maynard,

Hope your surviving these scary times

Looks like I spoke to soon about Portfolio performance

Unprecedented times in the market, must be some bargains including a FTSE100 Tracker coming up for the brave!

Keep smiling and all the best to you and your loved ones

David

Hi David,

Thanks for the message. I am surviving. Portfolio had escaped the worst of the carnage up until this week, then the carnage spread to my shares. Unprecedented times indeed. What is shocking is the number of pre-declared dividends being scrapped, even from one or two ‘quality’ names. Cannot recall that happening on a wide scale during the banking crash. Companies clearly desperate to hoard cash. Just got to grin and bear it and believe ‘this too will pass’.

Maynard

Hi Maynard

I found this article very interesting. I did not escape the rat race until 60 but had built up a reasonable share portfolio which I manage myself.

I am a subscriber to SharePad and have found your articles on choosing investments very informative and how you go about analysing different shares.

We are certainly in unusual times, I guess just hang on in there until everything returns to some degree of normality.

Best regards

Peter

Hello Peter,

Thanks for the comment. Glad you find my SharePad articles of use. I hope your portfolio has managed to survive these unusual times so far. I am hanging on in there!

Maynard

Great story, well told…good to see you well, happy and successful.

Phil Birkin — now that’s a name I have not heard in a long time! Thanks for the message, and I trust all is well with you.

Maynard

Hi Maynard,

Although I am too far down the line in career and age to retire in my 40s your article is really interesting and helpful.

After investing in funds via a major retailer for about 10 years and not taking too much notice until last January I have now taken responsibility myself.

Spent 10 months educating myself before transferring everything into a SIPP through October/ December. Currently working on a plan to be mortgage free over the next 3 to 4 years which will make me early 60s.

Reading this article has given me quite a few ideas so it’s much appreciated.

Thanks,

Murray

.

Hi Murray,

Glad you found the article was helpful. Main advice I can give is to earn/save as much you can. On the investment side, nothing is guaranteed and best not to be too ambitious — often the less ambitious you are the less mistakes you make and the better your overall portfolio performs.

Maynard

Hi Maynard,

Thanks for that and it makes a lot of sense. Took me at least a couple of months to choose my funds! Still ended up with a Trust Net rating of 90!

I would like to invest in single companies but am struggling to find the time as f/t working in healthcare currently.

After taking a good look at my finances in January I have pushed my monthly savings through the 20% barrier.

My internal mantra is now invest to retire!!

Cheers,

Murray

Hi Murray,

Ok, sounds a good plan. With individual companies, to become really good you do need a fair bit of time. But studying/backing perhaps one or two interesting companies as ‘side bets’ alongside a core group of funds would ease you into the ups and downs of stock picking!

Maynard

I’ve never really believed in FIRE as it seems to me you are avoiding paying tax, and therefore living off other people that do pay tax. But I don’t really know enough about it to know if this is true?

Hi PaulG, most people on the FIRE path will be paying the normal payroll taxes (PAYE, NI, etc) and making use of tax-efficient saving products available to everyone. But they won’t be spending as much and so won’t be contributing as much to VAT and the wider economy.

Maynard