04 September 2019

By Maynard Paton

Trading update and presentation summary on Tristel (TSTL):

- TSTL’s 2019 open-day presentation and the associated scuttlebutt did not yield any ground-breaking news.

- Unpicking the accompanying trading update suggested second-half UK sales gained an impressive 12%.

- However, the contribution from international operations was distorted by the purchase of Ecomed in November.

- The former Ecomed boss was confident sales in France could one day exceed those in Germany — TSTL’s largest overseas market.

- The purchase of the group’s Italian distributor — which has expanded quickly during recent years — appears very sensible.

Contents

- Event links and share data

- Why I own TSTL

- Open-day presentation

- Trading update

- UK sales

- Overseas sales and Ecomed

- Ecomed scuttlebutt

- United States

- Profit

- Cash

- Italy

- Other overseas markets

- Ambu

- Three-year guidance

- MobileODT

- Valuation

Event links and share data

Event: Trading update published 22 July 2019 and open-day presentation hosted 23 July 2019

Price: 270p

Shares in issue: 44,574,823

Market capitalisation: £120m

Why I own TSTL

- Develops medical-instrument disinfectants that are repeat-purchase and face limited direct competition due to multiple patents, scientific testimonies, secret ingredients and regulatory hurdles

- Enjoys a sizeable and resilient UK market position alongside significant expansion opportunities abroad

- Boasts financials that showcase high margins, decent cash flow, no debt and conservative profit recognition

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Open-day presentation

- During July I attended TSTL’s fourth open-day presentation at the group’s headquarters near an obscure Cambridgeshire village.

- Similar to the previous three events (2016, 2017 and 2018), the 2019 open day consisted of a management presentation/Q&A, a large sandwich buffet, the opportunity to tour the factory and a chance to inspect various products.

- Once again the main presentation took place in a white marquee out in the car park on a blisteringly hot day.

- TSTL must be applauded for arranging these open days. They remain popular with investors — the photo above suggests approximately 40 people attended this year’s gig — and more quoted companies ought to host similar events.

Trading update

- The trading update said:

“The Company confirms that results will be in line with market expectations and it expects to report turnover of £26m (2018: £22.2m), with pre-tax profit (before share-based payments) of at least £5.5m (2018: £4.7m).

Revenue from overseas markets increased by 26% and contributed 55% of total revenues — a record level (2018: 51%). Revenue in the UK rose by 9%.”

- The performance was bolstered by the acquisition of Ecomed during November. Ecomed sells TSTL products in Benelux and France.

- The table below shows my best guess of TSTL’s second-half revenue progress:

| Revenue | H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019* | FY 2019* | |

| UK (£k) | 5,354 | 5,481 | 10,835 | 5,610 | 6,145 | 11,755 | |

| Overseas (£k) | 5,373 | 6,012 | 11,385 | 6,408 | 7,880 | 14,288 | |

| Total (£k) | 10,727 | 11,493 | 22,220 | 12,018 | 14,025 | 26,043 |

(*estimated)

UK sales

- UK sales during the second half may have gained an impressive 12%.

- Management told the open-day attendees that a new three-year NHS pricing agreement — a one-off 8% price increase — had become effective from December.

- The price lift was said to have generated extra revenue of £400k during the second half — suggesting H2 underlying UK sales growth was a still-respectable 5%.

- Not every product sold in the UK had its price raised.

- My notes from February said the NHS price lift was between 10% and 15%.

- TSTL’s ‘non-core’ products are sold mostly in the UK and the trading update admitted such sales declined during the year (my bold):

“Sales of products using the Company’s core chlorine dioxide technology grew by 22% compared to non-core products which decreased by 5%.”

- As such, perhaps ‘core’ UK sales performed a little better than my calculations suggest.

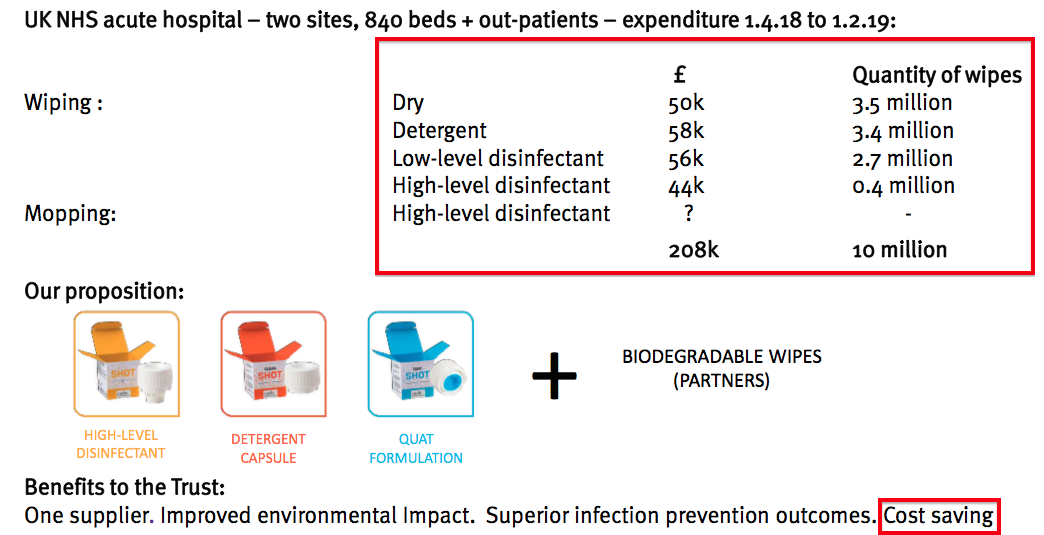

- Management claimed Shot — a new product for cleaning mattresses, bedside tables and other items that hospital patients come into contact with — was now being used in 25 UK hospitals.

- February’s results presentation showed a Midlands hospital paying £208k every ten months for an alternative to Shot:

- Could TSTL one day earn £208k-plus from 25 hospitals (i.e. £5m) every year through sales of Shot?

- The open-day vibes suggested current Shot revenue was growing quickly albeit from a very small base.

Overseas sales and Ecomed

- Management told me that Ecomed had generated revenue of £2.5m — and additional revenue to TSTL of £1.7m — since its purchase during November.

- Those figures suggest Ecomed was selling TSTL products for 3x their wholesale price.

- During the first half, Ecomed generated revenue of £400k and additional revenue to TSTL of £250k.

- As such, the second half perhaps saw Ecomed produce revenue of £2.1m (£2.5m less £400k) and additional revenue to TSTL of perhaps £1.45m (£1.7m less £250k).

- The table above indicates H2 overseas revenue gained almost £1.9m — suggesting H2 overseas sales excluding Ecomed advanced by £450k (£1.9m less £1.45m), or 7.5%.

- Overseas sales growth (excluding Ecomed) of 7.5% is at the lower end of my expectations. During H1, overseas sales (excluding Ecomed) gained 16%.

- I am not convinced these sums are entirely accurate. To balance the numbers, Ecomed must have performed particularly well.

- During the six months to June 2018, Ecomed earned revenue of €1.66m — equivalent to £1.45m — which suggests the new subsidiary produced extra revenue of £650k (£2.1m less £1.45m), up 45%(!!), during the comparable period of 2019.

- Perhaps TSTL’s rejig of its Chinese subsidiary — sales there fell by £200k to £100k during the first half — has skewed these overseas calculations.

- October’s full-year results will no doubt clarify Ecomed’s actual revenue contribution and I will revisit my sums then.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Ecomed scuttlebutt

- The open day provided the opportunity to speak to Bart Leemans, the former owner of Ecomed and now a TSTL executive director.

- Why sell Ecomed to TSTL? “Focus”. Mr Leemans explained he could now concentrate on selling TSTL’s disinfectants and not have to worry about distributing products from other companies.

- The decision to sell may have been also prompted by Ecomed’s dependence on TSTL.

- Mr Leemans admitted TSTL’s disinfectants had represented 80% of Ecomed’s revenue during the two years prior to purchase, and 70% before that.

- I understand TSTL is able to cancel/revise agreements — and set up in-house operations to compete directly — with overseas distributors.

- Maybe that is why the distributors in Australia and Italy sold out to TSTL at low-ish prices. Maybe that is why Mr Leemans thought selling out was best, too.

- Mr Leemans said he had been in contact with TSTL about a sale for between three and four years. My notes from February said a “lengthy courtship” had commenced “this time last year”.

- Mr Leemans said the ability to develop or supply new products for his Benelux and French markets was a benefit of working within TSTL. For example, he can now ask for a ‘side product’ to help sell a main product — something that was harder and slower to achieve as a local distributor.

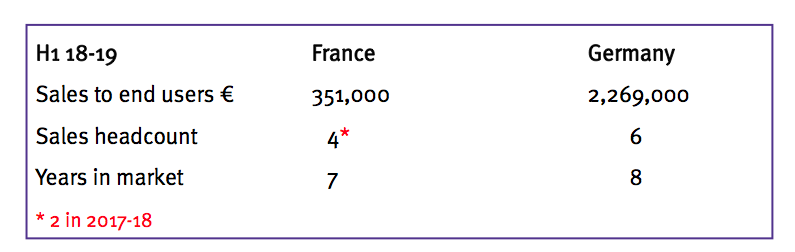

- Management’s presentation during February had indicated France could be a Germany-size opportunity:

- Mr Leemans claimed France could actually become a larger market than Germany for TSTL.

- He said France now offered a favourable regulatory environment. The country endorses wipe-based disinfectants (TSTL’s best seller is the Trio wipe system) and French hospitals must now clean medical devices using a high-level disinfectant.

- Mr Leemans also claimed the price and efficiency of TSTL’s products should not be an issue to French hospitals. According to Mr Leemans, the only reason a French hospital may overlook TSTL was because the staff had a “religion” towards disinfection machines.

- Mr Leemans added that he had taken charge of TSTL’s e-commerce operations. His experience within France taught him that dedicated sales teams were too expensive to serve small hospitals — the alternative for such customers being a low-cost online system.

United States

- The marquee attendees were not presented with any revelations about TSTL’s US regulatory project. (My February write-up summarises the protracted regulatory efforts).

- Management did say the US project had to date cost £1.5m and that the rest of the project “would not cost as much”.

- Some £1.3m was spent during 2016, 2017 and 2018, with a further £100k spent during H1 2019. That leaves another £100k spent during H2 2019.

- I understand the US regulatory delays were due in part to the ‘pathway’ for FDA approvals changing during recent years. New leadership at the US regulator has apparently widened the scope for the more demanding ‘de novo’ application.

- I also understand that the FDA had apparently told TSTL during an early meeting that the speedier ‘predicate’ application would be suitable.

- Management said Parker Laboratories — the group’s US manufacturing partner-in-waiting — was “used to” the FDA process and “knows how it works”.

- A TSTL staff member claimed Parker Labs was “ready to go” and that the first US sales could be recorded “weeks” after the FDA approval. TSTL has interested US hospitals lined up, too.

- Other marquee attendees told me:

- FDA approval could be less than one year away;

- Doctors participating in TSTL’s tests for the FDA are impressed with the product, and;

- Parker Labs is not a large firm — perhaps of a similar size to TSTL.

Profit

- The trading statement said pre-tax profit before share-based payments would be at least £5.5m for 2019.

- The table below outlines my best guess as to TSTL’s H1 and H2 profit split:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019* | FY 2019* | ||

| Share-based payments (£k) | (164) | (501) | (665) | (196) | (196) | (392) | |

| US costs (£k) | (500) | - | (500) | (100) | (100) | (200) | |

| Ecomed (£k) | - | - | - | (125)** | ? | ? | |

| Profit before tax, SBP and US costs (£k) | 2,513 | 2,658 | 5,171 | 2,627 | 3,198 | 5,700 | |

| Profit before tax and SBP (£k) | 2,013 | 2,658 | 4,671 | 2,402 | 3,098 | 5,500 |

(*estimated **calculated as £230k transaction costs less £105k profit contribution)

- I calculate H2 profit before tax, share-based payments and US costs gained £540k, or 20%, to £3.2m.

- The H2 performance was flattered by the Ecomed acquisition, the profit contribution from which is difficult to judge accurately.

- Back in February I guessed Ecomed could contribute an £800k profit for a full year — and perhaps therefore £400k for H2.

- The additional £540k profit for H2 2019 over H2 2018 less my £400k Ecomed contribution guess leaves just £140k extra profit from the existing business — equivalent to only 5% growth.

- Similar to my overseas sales-growth sums above, I am not convinced my profit calculations are completely accurate.

- That said, I am alert to the possibility that growth during the second half — excluding Ecomed — may have been somewhat pedestrian.

- October’s full-year results will no doubt clarify Ecomed’s actual profit contribution and I will revisit my sums then.

Cash

- The trading update said:

“Tristel has continued to generate significant levels of cash and at 30 June 2019 cash balances were £4.2m (30 June 2018: £6.7m). During the year the Company spent £4.9m to satisfy the cash element of the acquisition of its three distributors in Western Europe which demonstrates the cash generative nature of Tristel’s core business.”

- TSTL would have also spent approximately £2.2m as dividends during the year.

- Free cash generation for the year was therefore £4.2m plus £4.9m (Ecomed purchase) plus £2.2m (dividends) less £6.7m = £4.6m.

- Cash generation of £4.6m represents 83% of the £5.5m profit achieved before tax and share-based payments. The 17% difference appears to be a viable tax rate and underlines TSTL’s ability to convert earnings into cash.

- Year-end cash of £4.2m equates to 9.4p per share.

Italy

- The trading update announced the purchase of the group’s Italian distributor:

“The Company has acquired 80% of the share capital of Tristel Italia srl (“TI”) from Michael Donaldson. Tristel has previously owned 20% of TI since 2007 when it supported Donaldson to introduce Tristel’s medical device disinfectants into Italy. Donaldson has single-handedly built the business since. Turnover in the year ended 30 June 2019 was €700,000, exclusively of Tristel products, and EBITDA was €255,000.

The consideration paid on completion is €661,000, and an additional cash consideration of €150,000 may be paid over the next two years if sales reach €926,000 in the year ending 30 June 2021.

In Tristel’s hands TI will now build a sales force to accelerate growth in this well-established market. Tristel expects the acquisition to have a neutral impact on earnings in the current financial year ending 30 June 2020 and to be earnings enhancing in future years.”

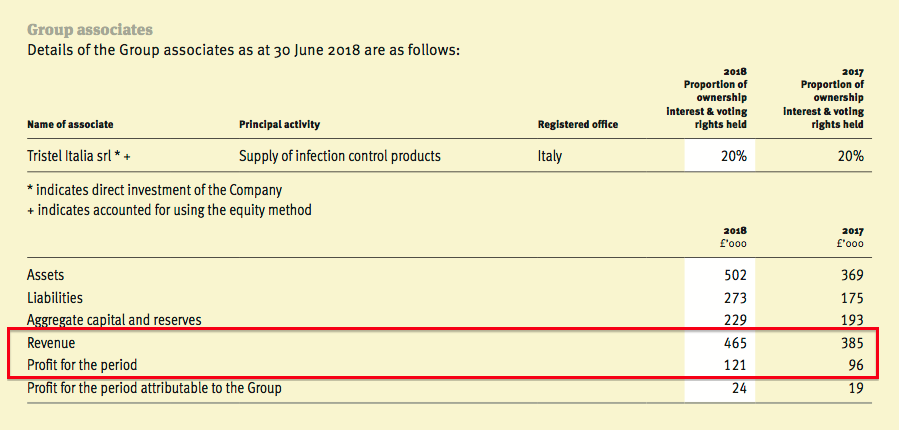

- The Italian business has grown quickly during recent years:

| Year to 30 June | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 207 | 238 | 285 | 385 | 465 |

| Profit (£k) | 40 | 38 | 66 | 96 | 121 |

- Italian revenue and earnings climbed 21% and 26% respectively during 2018:

- Indicated Italian turnover of €700k for 2019 equates to approximately £620k — 33% greater than the £465k registered for 2018.

- The full €811k consideration will be paid if Italian sales can compound at a 15% average during 2020 and 2021.

- Assuming the division’s profit can advance at the same pace as revenue, TSTL could enjoy a £200k contribution from its Italian subsidiary by 2021.

- A £200k annual profit from the full €811k consideration would deliver a healthy return.

- Mind you, the trading update did state TSTL would “build a sales force to accelerate growth” in Italy. The associated cost could hinder profit in the short term.

- The Italian deal appears sensible and follows distributor acquisitions in Australia and Hong Kong, as well as Benelux and France via Ecomed.

Other overseas markets

- The marquee attendees were told that France and China offered the most overseas potential alongside the US.

- Management claimed medical probes in China are not disinfected, and that condoms were used on the probes to prevent infection.

- Management also claimed China offered TSTL“huge potential”. TSTL’s Duo foam disinfectant received Chinese regulatory approval earlier this year.

- TSTL also gained regulatory approval in South Korea this year (I am not sure how South Korea has become TSTL’s second-largest distributor without selling any of the group’s ‘core’ chlorine-dioxide disinfectants).

- I understand further purchases of overseas distributors are unlikely because TSTL products represent relatively low proportions of their sales.

Ambu

- Management is aware of Ambu, a quoted Danish business that manufacturers single-use medical devices.

- The advantage of single-use endoscopes and the like to hospitals is the absence of any disinfection requirements.

- Management said the uptake of Ambu’s instruments had been “pretty slow” and that the “vision quality” of the devices was “poor”.

- Ambu’s latest results (Q3 2019) reported sales of single-use endoscopes climbing 33% to 194k units.

- TSTL’s executives added that the benefits of disposable devices were based on claims that used “older, less efficient disinfectants”. TSTL’s disinfectants “should make Ambu’s proposition less appealing”.

- Management also noted the environmental issues concerning the manufacture of single-use instruments.

Three-year guidance

- The trading update essentially confirmed TSTL had achieved the three-year guidance set during 2016.

- The directors previously indicated they would present new three-year guidance at the open day:

- However, the board has deferred publishing new targets due to an ongoing debate about the prospects of the group’s legacy products.

- Management was open to the suggestion of providing guidance relating to only the ‘core’ chlorine-dioxide business.

MobileODT

- A staff member claimed the MobileODT colposcopes were disinfected by CaviWipes in the US. CaviWipes are “no good” and “do not kill spores and HPV”.

- FDA regulatory approval would allow TSTL’s Duo foam to disinfect MobileODT’s colposcopes in the US.

- The staff member said MobileODT sells colposcopes for £4,500 in the UK with a one-year warranty. 3,000 units have been sold in the US and 5,000 have been sold elsewhere. The device is particularly popular in Poland.

- TSTL owns 3% of MobileODT.

Valuation

- My February write-up pointed to possible earnings of 10.8p per share.

- Given my doubts concerning the exact profit contribution of Ecomed and other calculations, I will await October’s full-year figures before fine-tuning my valuation sums.

- For now at least, a 270p share price divided by my 10.8p earnings per share guess gives a P/E of 26.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Tristel.

Tristel (TSTL)

Open-day presentation slide

This was an interesting slide from the open day:

Management said the “manufacturers compatibility” hurdle was perhaps the “hardest to breach“. I suppose even if a rival developed an alternative disinfectant that was cheaper to buy and more effective to use, approval from the medical-instrument manufacturer — as well as the relevant regulator — would have to be sought before customers could make a purchase.

Maynard

Thanks Maynard, it sounds like it was a useful day. Richard

Thanks Maynard,

A really thorough and useful analysis. I had always understood that France was a “non-target” for Tristel because of the strong position “religion” of a national supplier. Looks like Tristel have been cracking the market and that progress will be accelerated by the aquisition.

I still feel that they may get an offer once the US product/market is licensed. Maybe from a Diversey or an Ecolab.

Hopefully I will finally get to go to an open day – if I do, I will say hello.