10 July 2024

By Maynard Paton

H1 2024 results summary for City of London Investment (CLIG):

- A subdued performance due to ongoing market “headwinds”, with funds under management (FuM) and revenue up 2%, profit down 5% and the dividend kept at 11p per share for the fourth consecutive H1.

- CLIG blamed further FuM withdrawals of $294m on higher deposit rates and appealing index trackers, although the follow-up Q3 statement reported a bumper $224m inflow as clients reappraised the group’s “compelling” portfolio valuations.

- A “strategy of engagement” with unhappy major shareholder George Karpus has led to welcome cost cuts, yet the staff profit-share continues to edge higher and doubts persist about whether CLIG is run for the benefit of employees instead of shareholders.

- Other questions from this H1 concern the effectiveness of the salesforce, the reduced disclosure on fee rates, the necessity of a main-market listing, the revised testing for goodwill impairment and the failure to meet the group’s sole KPI.

- While CLIG’s own projections point to earnings that just about support the 33p dividend and 9% yield, publishing USD accounts but declaring GBP dividends may confuse the 1.2x payout-cover policy. I recently bought more and continue to hold.

Contents

- News links, share data and disclosure

- Why I own CLIG

- Results summary

- Functional and reporting currency change from GBP to USD

- Revenue, profit and dividend

- Funds under management: inflows and outflows

- Funds under management: capacity and growth plans

- Funds under management: investment performance

- Funds under management: fee rates

- Engagement with George Karpus: board membership

- Engagement with George Karpus: corporate cash management

- Engagement with George Karpus: expenses

- Engagement with George Karpus: corporate governance

- Q3 2024 FuM update

- Financials

- Valuation

News links, share data and disclosure

- Interim results for the six months to 31 December 2023 published 23 February 2024;

- Change of auditor published 08 March 2024;

- H1/Q3 2024 presentation published April 2024;

- Update on 2023 Annual General Meeting Resolution Votes published 16 April 2024, and;

- Q3 2024 FuM update published 22 April 2024.

- Share price: 370p

- Shares count: 50,679,095

- Market capitalisation: £188m

- Disclosure: Maynard owns shares in City of London Investment. This blog post contains SharePad affiliate links.

Why I own CLIG

- Fund manager that employs a “risk-averse” strategy of buying investment trusts at attractive discounts through a team-based approach (point 1).

- Accounts showcase high 37% margin, significant net cash and ability to distribute majority of earnings via dividends.

- Yield of 9% offers meaningful income potential with upside linked to a market rotation into ‘value’, winning extremely elusive new clients and/or activist intervention from unhappy major shareholder George Karpus.

Further reading: My CLIG Buy report | All my CLIG posts | CLIG website

Results summary

Functional and reporting currency change from GBP to USD

- CLIG had already announced the preceding FY results would be the last to be presented using GBP, and these H1 figures would be the first to be presented using USD:

(FY 2023) “As mentioned in the Annual Report for the year ended 30th June 2023, the Board decided to change the Group’s financial reporting currency to US dollars with effect from 1st July 2023. This allows us to present a more transparent statement of comparative financial performance that neutralises currency fluctuations. This is the first time the Group’s results are being reported in US dollars.”

- The preceding FY had included complete USD-denominated income statements, balance sheets and cash flow statements for FYs 2022 and 2023 (point 28).

- For FYs prior to FY 2022, I have translated the original GBP performances into USD using the average GBP:USD rate that prevailed during each FY.

- Although my translations are estimates and will not be entirely accurate, they do underline how CLIG’s GBP progress had benefitted from a stronger USD.

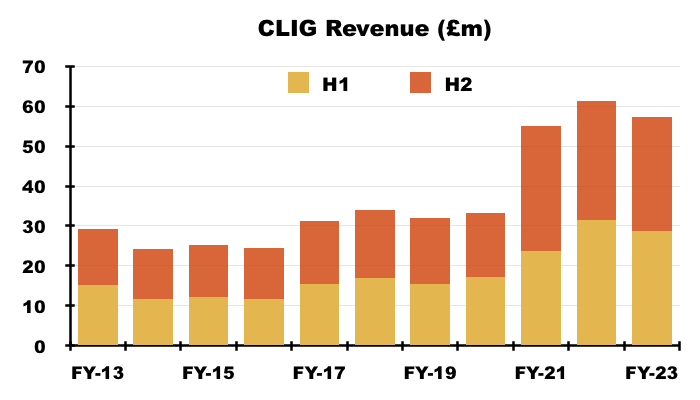

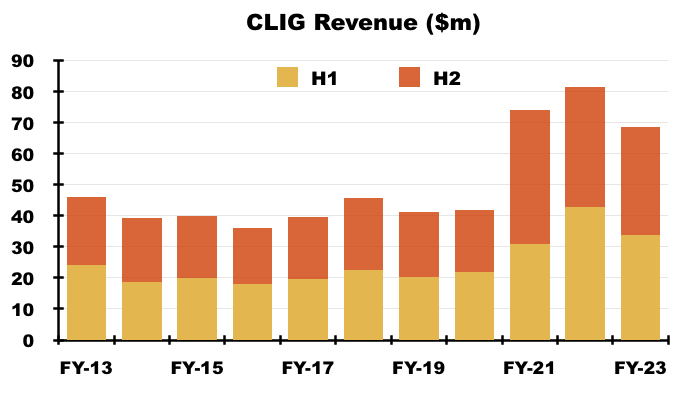

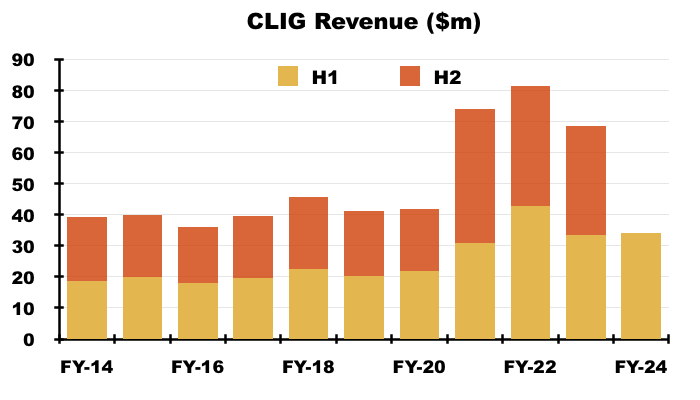

- For example, GBP revenue between FYs 2013 and 2023 advanced 95%…

- …while USD revenue increased 49%:

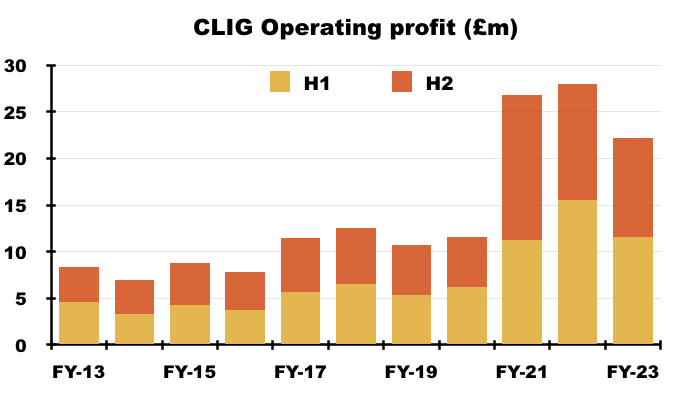

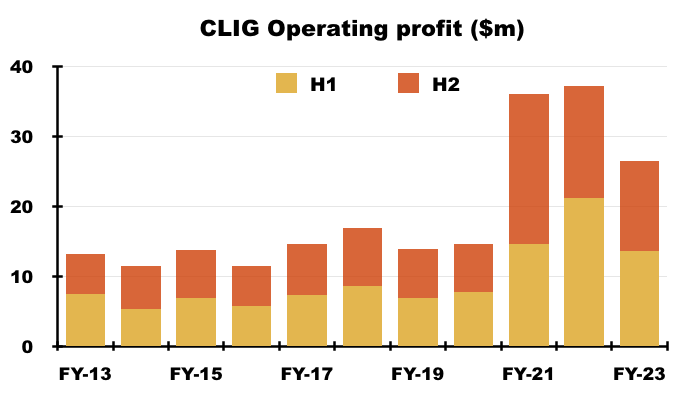

- Furthermore, GBP adjusted operating profit between FYs 2013 and 2023 gained 166%…

- …while USD adjusted operating profit improved 102%:

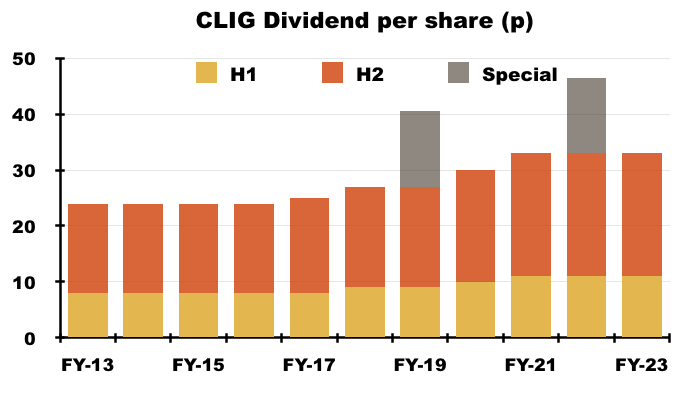

- CLIG’s dividend history gives further perspective to the GBP-USD comparison.

- The GBP payout was 24p per share for FY 2013 and 33p per share for the preceding FY — an increase of 38%:

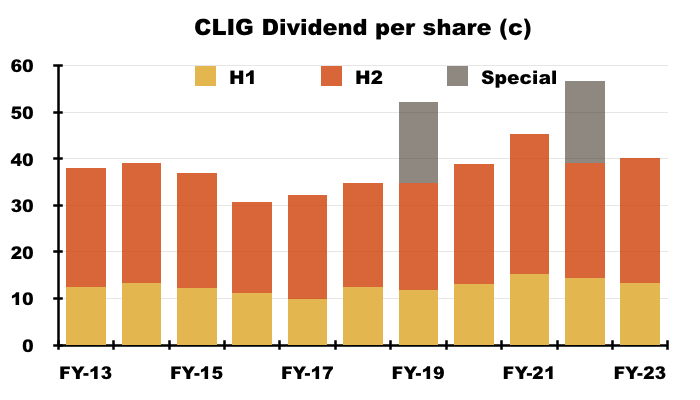

- But a USD-converted payout would have gained only 6% — from 37.9 US cents to 40.1 US cents — during the same period:

- Indeed, while CLIG has held its H1 dividend at 11p per share during H1s 2021, 2022, 2023 and 2024…

- …shareholders converting their 11p per share H1 payout into USD have suffered an 11% income decline (from 15.2 to 14.1 US cents)!

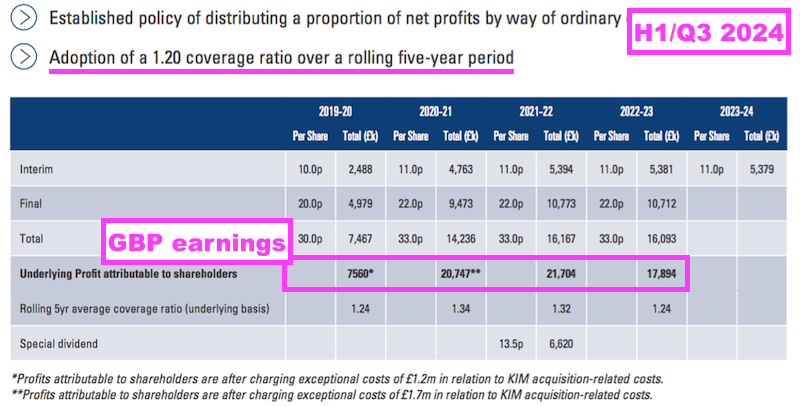

- Despite CLIG adopting USD as the group’s functional and reporting currency, dividends continue to be declared in GBP…

- …and the dividend-cover policy — a minimum 1.2x cover over rolling five-year periods — still seems based on GBP-denominated earnings:

- The preceding FY implied the dividend-cover policy would be reviewed at the forthcoming FY 2024 results:

(FY 2023) “This [dividend-cover] policy was introduced in 2014 and was reviewed in 2019. No changes were proposed. It was designed to incorporate the required flexibility to deal with the potential volatility of CLIG’s income.

…

This is not a long-term policy. Rather, it will be reviewed after five years and every five years thereafter.”

- A dividend-policy review may well reconsider declaring a GBP-denominated payout while reporting USD earnings.

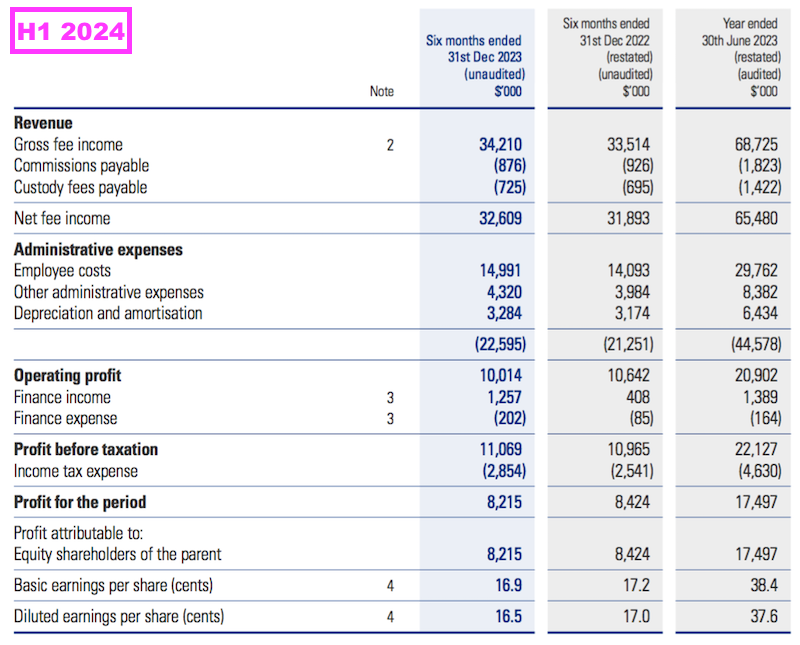

Revenue, profit and dividend

- January’s Q2 trading statement had already outlined how this H1 would show very modest advances to funds under management (FuM) and profit:

(Q2 2024) “The Group estimates the unaudited profit before amortisation and taxation for the six months ended 31 December 2023 to be approximately US$13.9 million (six months ended 31 December 2022: US$13.8 million, restated in USD based on average exchange rate).

- This H1 confirmed H1 FuM was indeed $9,576m and H1 profit before amortisation and tax was indeed $13.9m.

- Note that January’s statement claimed cash was $28.8m and investments were $2.4m:

(Q2 2024) “Inclusive of our regulatory and statutory capital requirements, cash and cash equivalents stood at US$28.8 million at the end of the calendar year (US$28.6 million as at 30 June 2023, restated in USD based on closing exchange rate), in addition to the seed investments of US$2.4 million.“

- However, H1 cash was in fact $25.9m and H1 investments were in fact $5.4m. Cash of c$3m was therefore reclassified as investments between January’s statement and this H1 (see Financials).

- This H1 reeled off a list of now-familiar operational “headwinds”:

“Investors have been wrestling with a series of shocks over the past four years including the Covid-19 outbreak, the ensuing pandemic, post-Covid inflation, the Russia-Ukraine war and now a new conflict in the Middle East. In combination with the ongoing Russia-Ukraine conflict, the Israel-Hamas war has put further pressures on energy prices and exacerbated global supply chain difficulties.“

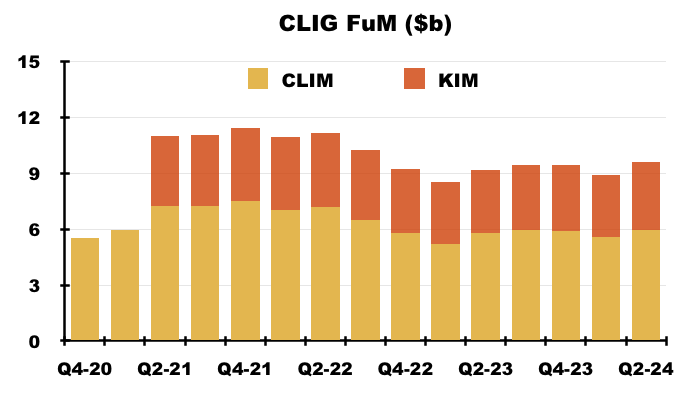

- FuM averaged $9.2b during this H1 versus $9.1b during the comparable H1 and $9.4b during the preceding H2:

- The slightly higher average FuM during this H1 helped H1 revenue improve 2% to $34.2m:

- This H1’s higher revenue was achieved despite a lower fee rate charged against FuM.

- This H1 oddly did not confirm the 70 basis-point weighted-average fee rate cited within January’s statement (see Funds under management: fee rates).

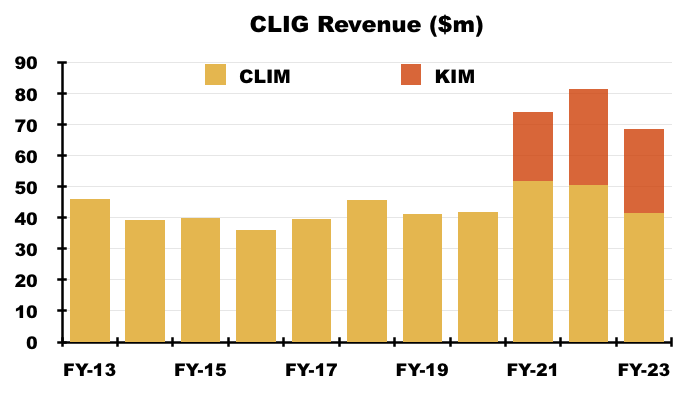

- CLIG does not distinguish between revenue from its original City of London Investment Management (CLIM) division and revenue from its £102m merger partner Karpus Investment Management (KIM).

- But Companies House reveals CLIM reported FY 2023 revenue of £34.5m, which translated to approximately $41.5m and supported 60% of the preceding FY’s top line:

- Excluding amortisation associated with the KIM merger, H1 operating profit was $12.8m or 5% less than the comparable H1 ($13.4m):

- The H1 profit shortfall reflected costs increasing by $1.2m while revenue increased by $0.7m (see Engagement with George Karpus: expenses).

- The 11p per share H1 dividend was declared within January’s Q2 trading update and matched the payout declared for H1s 2021, 2022 and 2023:

- This H1 referred to the dividend-cover policy when deciding the 11p per share H1 payout:

“The Board continues to believe that the use of a dividend-cover policy based on rolling five-year periods provides a prudent template that serves to protect shareholders from the market volatility that can affect profits of asset management companies.”

- I wonder if the aforementioned dividend-policy review will reconsider the 1.2x target for rolling cover over five years.

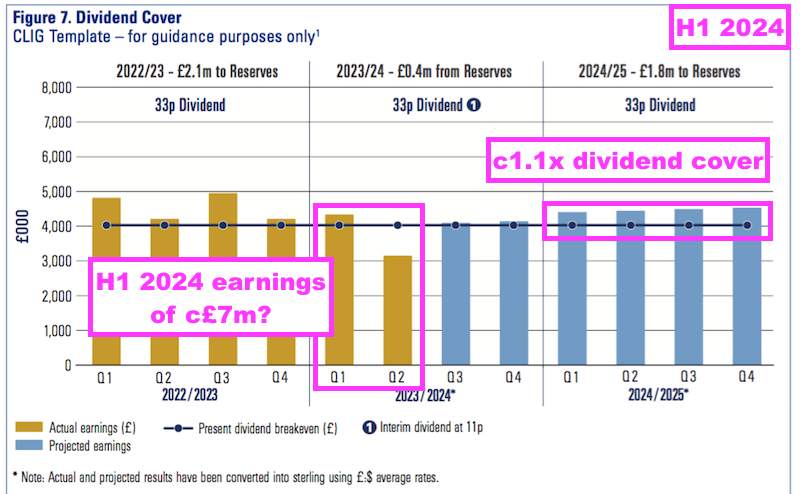

- CLIG’s own projections indicate very thin dividend cover for FY 2025:

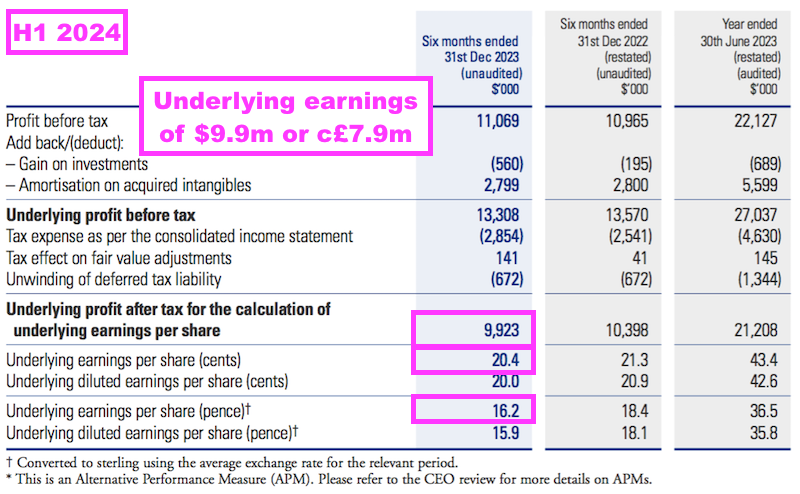

- The Q2 earnings drop within CLIG’s chart above looks very peculiar and suggests earnings for this H1 were approximately £7m.

- However, this H1’s reported adjusted earnings seemed closer to £8m based on my calculations using CLIG’s official USD and GBP versions of earnings per share (i.e. $9.9m*16.2/20.4):

Funds under management: inflows and outflows

- CLIM’s FuM can be divided into two main categories:

- Emerging Markets (EM), and;

- Other strategies, which cover:

- Developed (or “International“) markets outside the United States;

- “Opportunistic Value”;

- “Frontier” markets, and;

- Seeded funds (REITs and “Global”).

- Both categories apply a long-standing value approach of buying UK- and US-listed investment trusts at attractive discounts and often take an activist stance. CLIM customers are primarily US-based institutions, although an EM fund-of-funds is offered to UK retail investors through intermediaries.

- KIM meanwhile manages fixed-income portfolios while also applying a value/discount approach to US investment trusts. KIM clients are almost entirely high-net worth individuals residing in the US.

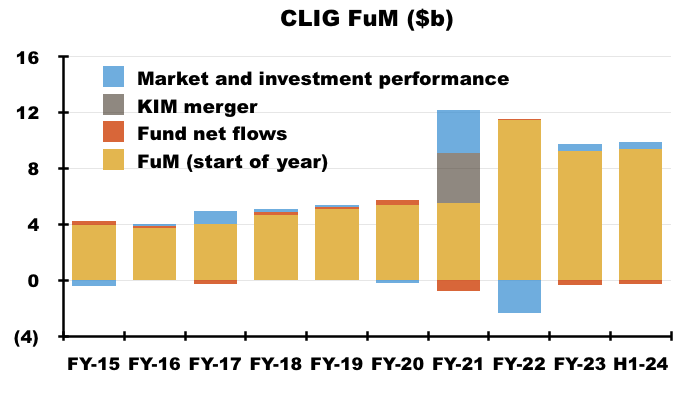

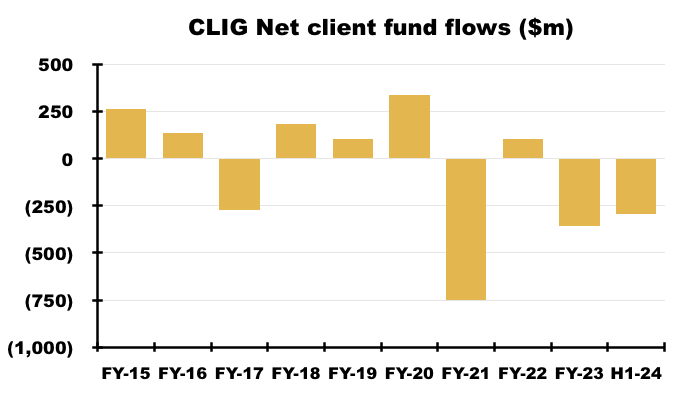

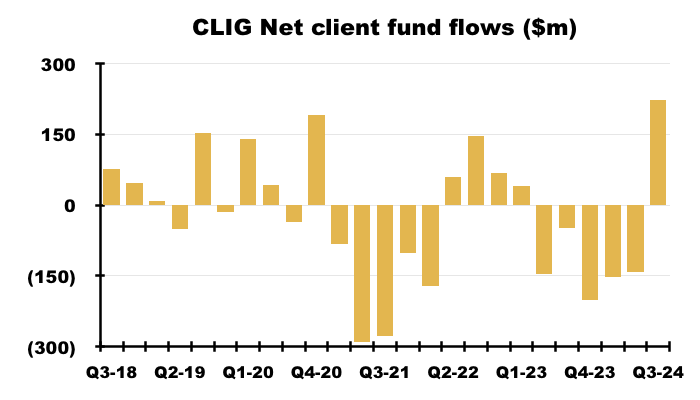

- For years CLIG has struggled to attract significant new client money.

- The (very thin) red bars on the chart below show new client money has been minimal since FY 2015:

- Indeed, this H1 witnessed net withdrawals of $294m…

- …which left aggregate net outflows since FY 2015 at $544m:

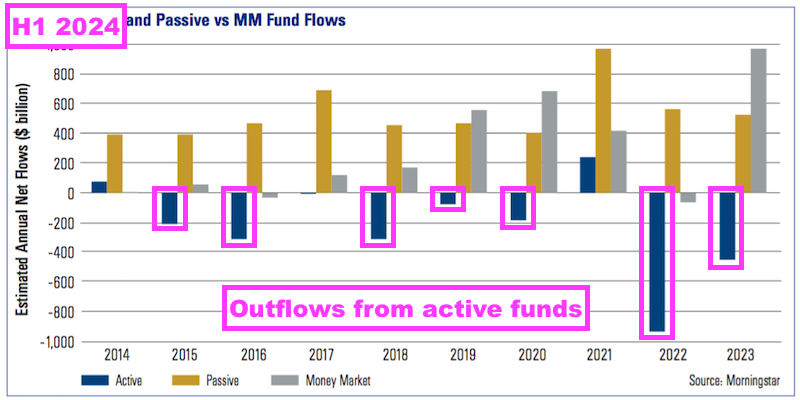

- This H1 appeared to blame the persistent lack of new CLIM money on the wider shift from active funds to index trackers and, increasingly, to money-market funds:

“The ongoing trend of outflows from active managers into passive managers continued in 2023, but with an additional twist, as flows into money market vehicles reached an all-time high for net inflows during calendar year 2023…“

- KIM withdrawals continue to be blamed on higher interest rates tempting clients to invest elsewhere:

“Some individual clients, particularly those concerned about their retirement assets, reduced their portfolio’s market exposure locking in losses during recent market downturns; instead choosing the safety of bank deposits and money market vehicles paying high rates of interest…

Broadly speaking, the psychology of US individual investors has been negatively impacted by rising interest rates and broad market losses in fixed income assets in 2022 and continuing into part of 2023. This is compounded by the aforementioned safety provided in bank deposits and money market funds, at a higher interest rate than at any time over the last twenty years. Finally, the ongoing drumbeat of geopolitical issues and risks add to the negative mindset of investors.”

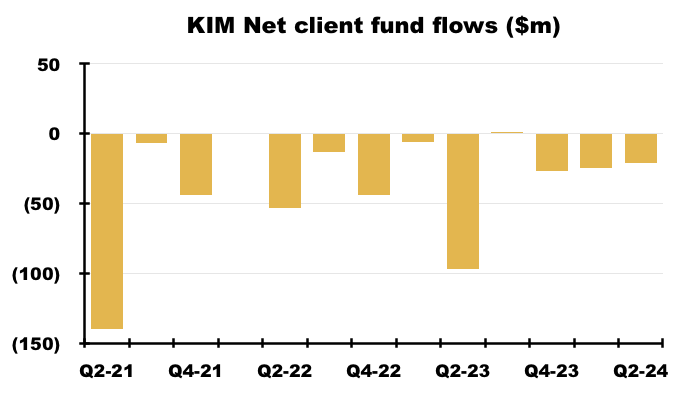

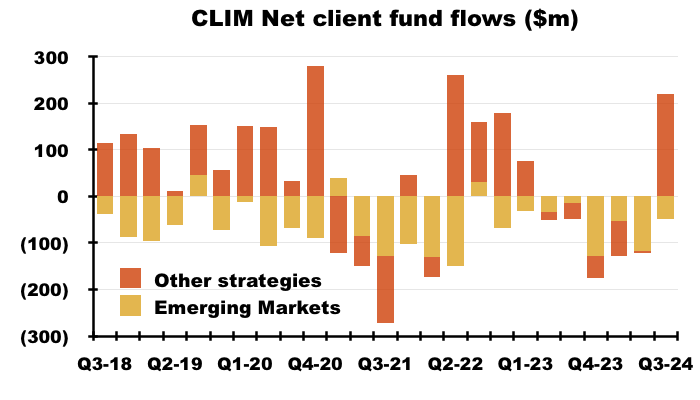

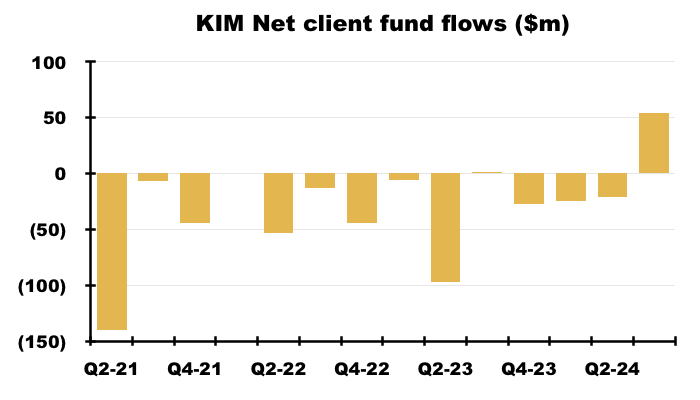

- KIM’s clients withdrew a net $46m during this H1 to take total net KIM withdrawals since the merger to $476m:

- Management during the 2022 AGM claimed KIM suffers “natural” outflows of $100m a year through clients withdrawing capital and income for retirement.

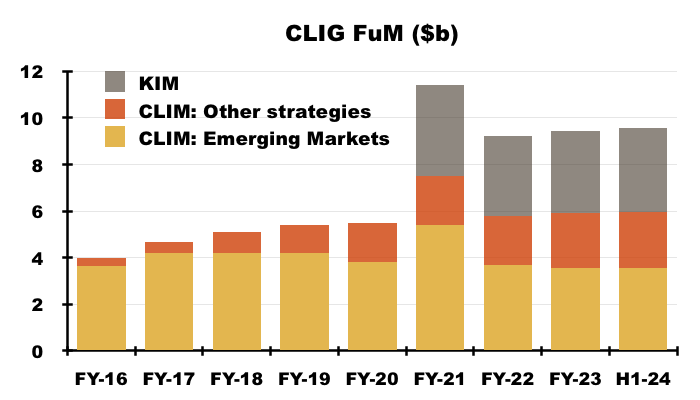

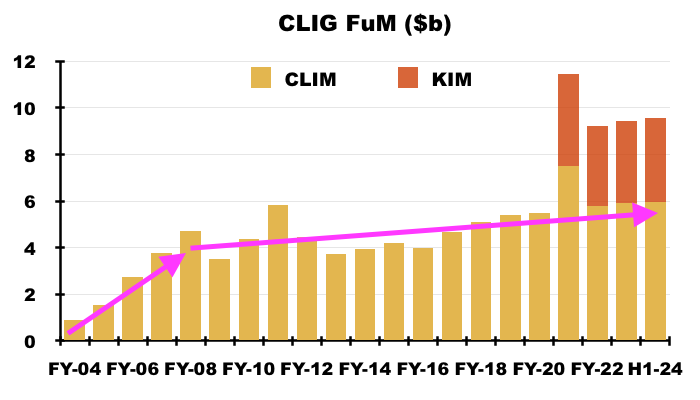

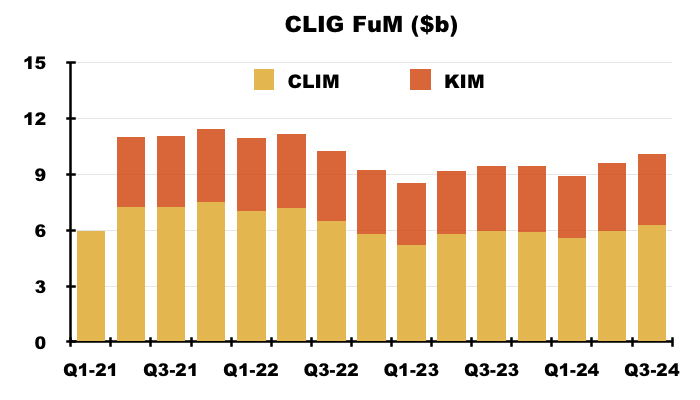

- H1 KIM FuM was $3,618m — only $40m greater than the $3,578m held at the time of the October 2020 merger.

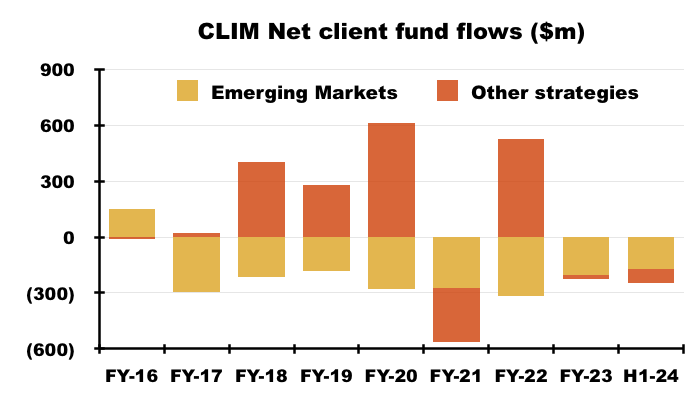

- Alongside the $476m leaving KIM, CLIM clients have withdrawn a net $341m since FY 2016:

- Extra CLIM money received since FY 2017 has been directed entirely towards Other strategies. CLIM’s EM funds have in contrast suffered consistent yearly net outflows.

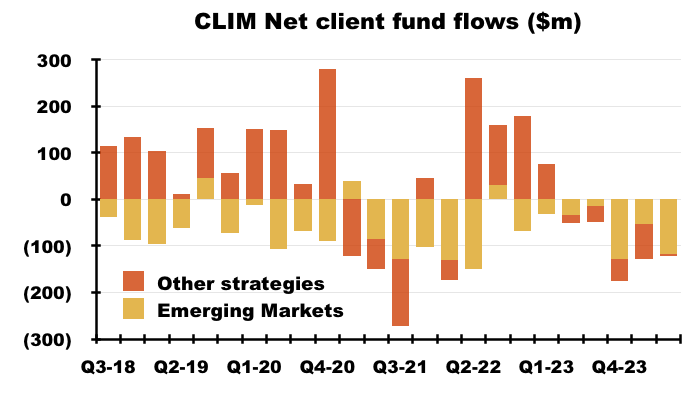

- In fact, this H1 witnessed outflows of EM money extending to 21 of the last 24 quarters:

- Mind you, after enjoying net inflows of client money of more than $1.5b between FYs 2017 and 2022, Other strategies have since experienced net outflows of $99m during the preceding FY and this H1.

- This H1’s inflows and outflows had little effect on how FuM is split, with 37% (previously 38%) in EM, 38% (previously 37%) in KIM and 25% still in Other strategies:

- 37% is the lowest proportion of EM FuM in CLIG’s history.

- EM funds represented 90% of client money during FY 2017, since when CLIG has countered “EM fatigue” by deliberately diversifying its FuM through developing the Other CLIM strategies and undertaking the KIM merger.

- This H1 claimed “good” client retention:

“Client asset retention was good throughout the turbulence of the past six months relative to competitors and what industry statistics suggest.”

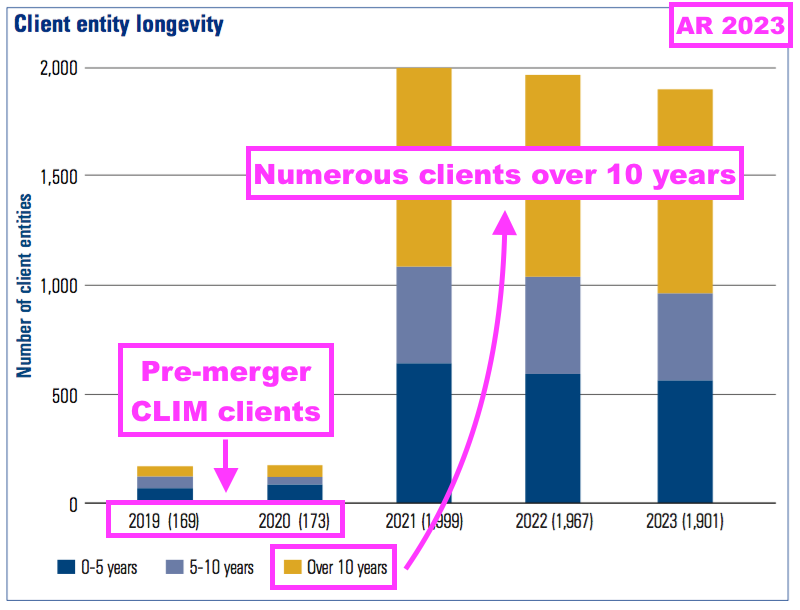

- Many CLIG clients are encouragingly loyal to the group. The 2023 annual report disclosed numerous clients had employed CLIM or KIM for more than ten years:

- Emphasising the lack of new client money, the 173 CLIM clients served immediately before the KIM merger compares to 161 for FY 2014.

Funds under management: capacity and growth plans

- This H1 claimed CLIG could accept “ample” extra client money:

“We remain focused on our [closed-end fund] strategies, which have good long-term performance and ample capacity.”

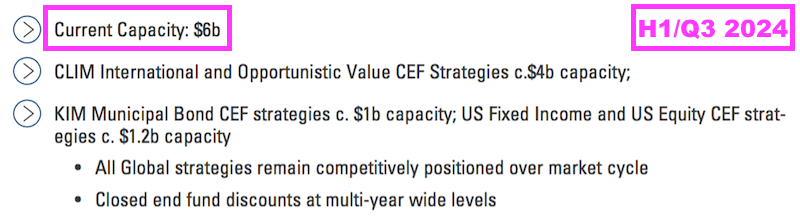

- The H1/Q3 presentation subsequently confirmed CLIG could handle extra client money of $6b:

- The preceding FY suggested extra capacity was $4.5b:

- An extra $6b would increase H1 FuM of $9.6b by more than 60%.

- CLIG said marketing efforts “picked up significantly” after this H1:

“Marketing and sales activity picked up significantly in January 2024 as clients and prospects review their investment allocations. The Group is focused on new mandates in a number of CLIG’s asset classes with very good long-term performance as [closed-end fund] discounts are at compelling levels. Our business development team is actively reaching out to clients and prospects to discuss the current opportunity-rich environment“.

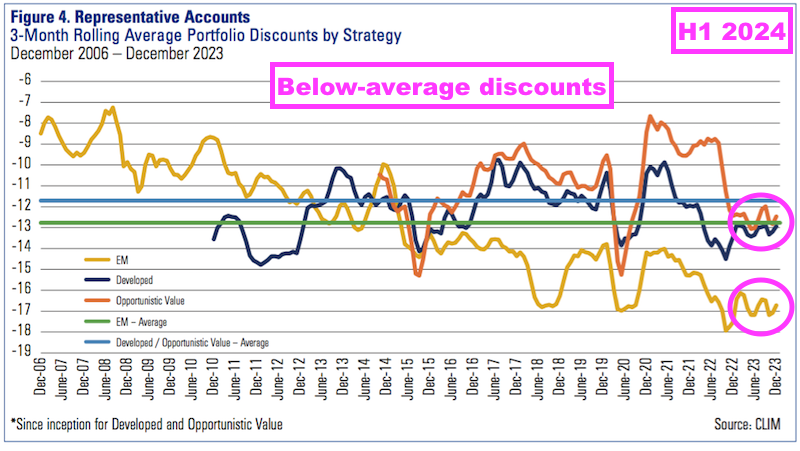

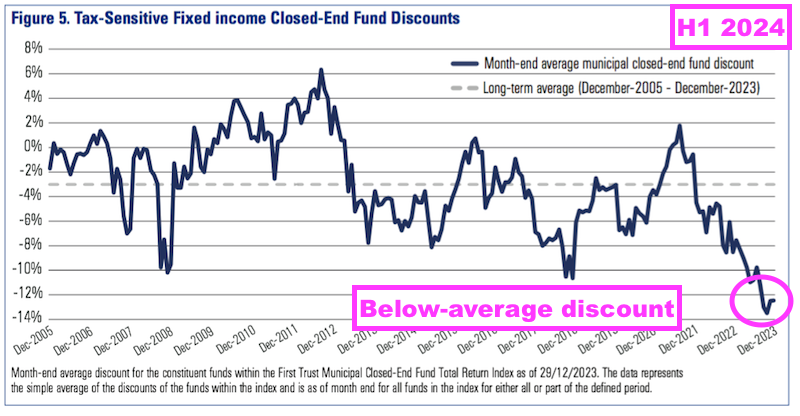

- The “compelling” valuations were emphasised by discounts to NAVs among investee trusts falling to “historically wide” levels:

- April’s Q3 2024 statement published after this H1 confirmed the increased marketing efforts had garnered extra net client money of $224m (see Q3 2024 FuM update).

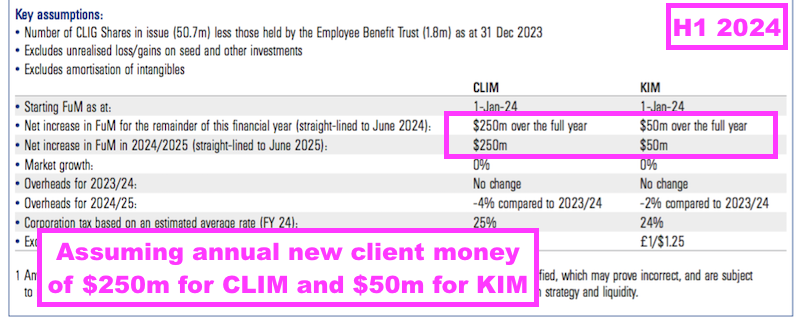

- This H1 reiterated new client money of $300m could be attracted during FY 2024, and claimed a further $300m could be attracted during FY 2025:

- An extra $300m is equivalent to only 3.1% of total H1 FuM of $9.6b.

- Expecting new client money of $250m a year at CLIM is still not completely outrageous; CLIM attracted net inflows of $338m during FY 2020 and $265m during FY 2015.

- Expecting any new client money at KIM had felt very optimistic, given the division suffered net withdrawals of $476m following the October 2020 merger up to this H1.

- But perhaps KIM’s fortunes are now improving, as KIM received new money of $54m after this H1 (see Q3 2024 FuM update).

- The preceding FY had said a new appointment was tasked with lifting group FuM:

(FY 2023) “The integration of KIM is now complete. What remains is to leverage the strengths of the Group in order to raise new FuM across the Group. In this regard, we created a new position – Head of Corporate Partnerships – to deepen our existing client relationships, particularly as baby boomers transfer wealth to the next generation, and build new partnerships with professional organisations. This individual, who has over twenty years of experience in the field, is also responsible for branding opportunities, unique client experiences, and increasing the profile for the Group.“

- But the 2023 annual report (point 16) revealed the business development/marketing department employed two fewer people during the preceding FY:

- Although much remains to be done to promote the “compelling” valuations to potential new CLIM and KIM clients, CLIG’s growth strategy appears stuck in the ‘discussion’ phase.

- For example, small-print with the 2023 annual report (point 9) revealed a “strategy for growth” board discussion:

(AR 2023) “In January 2023 the Board received and considered a paper from the Executive Director which gave a high level overview of the strategy for growth. A strategy discussion was held in April 2023.”

- This H1 then disclosed the merged group’s first ever “Strategy Meeting“:

“This past September, the Board and the teams from CLIM and KIM hadtheir first Group Strategy Meeting since the merger. The meetings were very important in building camaraderie and gave everyone the opportunity to discuss CLIG’s strategic priorities.”

- The outcome of the growth-strategy discussions was not made clear within this H1.

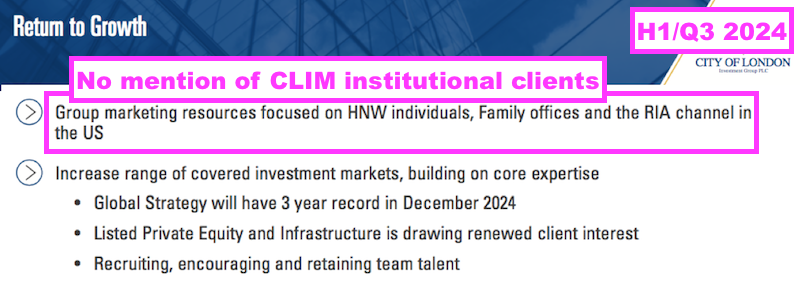

- The H1/Q3 presentation implied marketing efforts behind CLIM’s funds may now be directed entirely towards KIM’s customer base:

- The presentation also mentioned increasing the range of investment markets.

- I speculate CLIM’s long-term lack of new client money is due in part to employing ineffective salespeople. Maybe CLIG should return to outsourcing its promotional efforts to a more capable marketing organisation.

- After all:

- Buying investment trusts is not the most glamorous of equity strategies;

- CLIM’s heritage area of expertise — emerging markets — has underperformed long term, and;

- The group’s “team approach” (point 12b) does not lend itself to the inherent promotional advantages of employing a super-star investor.

- CLIG previously employed North Bridge Capital to help promote its funds, until marketing was brought in-house during FY 2009:

(FY 2009) “Towards the end of 2008 a marketing manager was appointed to implement our decision to bring our US marketing in-house, and ultimately therefore to avoid the commissions which we have historically paid to North Bridge Capital who have served us well since we started the US marketing activity. He will be responsible for developing direct relationships with the consultant industry which advises institutional investors.”

- Assisted by North Bridge, CLIM FuM between FYs 2004 and 2008 went from less than $1b to almost $5b…

- …yet during the next 15.5 years (without North Bridge) CLIM FuM has climbed to only $6b.

Funds under management: investment performance

- CLIG described a mixed (relative) investment performance for this H1:

“Relative investment performance at CLIM was positive for the Opportunistic Value strategy, neutral for the International strategy and slightly negative for the EM strategy, whereas relative investment performance at KIM was positive for the Taxable Fixed Income strategy and Tax-sensitive Fixed Income strategy, while negative for US Equity and Conservative Balanced mandates over the six months ended December 2023.“

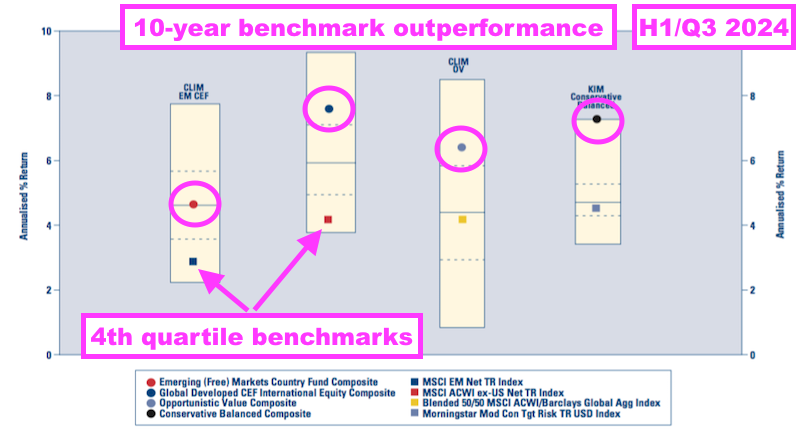

- The H1/Q3 presentation showed CLIG’s major strategies all outperforming their associated benchmarks over ten years:

- The EM and International performances reveal an unusual phenomenon: the associated benchmarks are fourth-quartile performers over ten years.

- Benchmarks languishing in the fourth quartile may also explain why CLIM has struggled to attract new client money — lots of rival funds within the same sector can also claim benchmark-beating returns.

- CLIM’s website underlines a deteriorating investment performance.

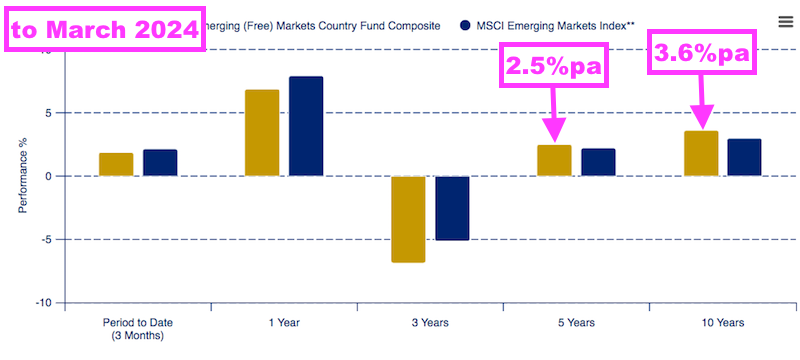

- The EM strategy has returned a 2.5% compound average over five years versus 3.6% over ten:

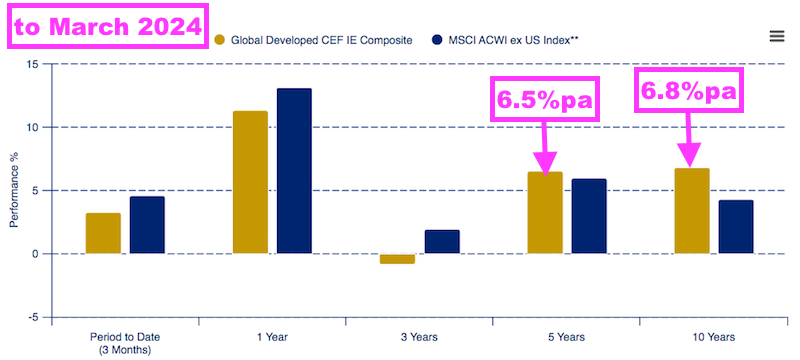

- The International strategy has returned a 6.5% compound average over five years versus 6.8% over ten:

- The Opportunistic Value strategy has returned a 4.2% compound average over five years versus 5.6% since its 2014 inception:

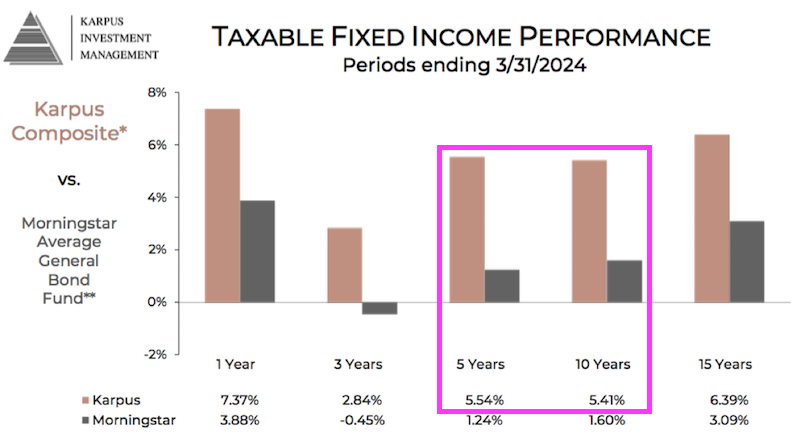

- KIM’s returns have been greater and more consistent than those of CLIM.

- KIM’s Fixed Income for example has returned a 5.5% compound average over five years versus 5.4% over ten:

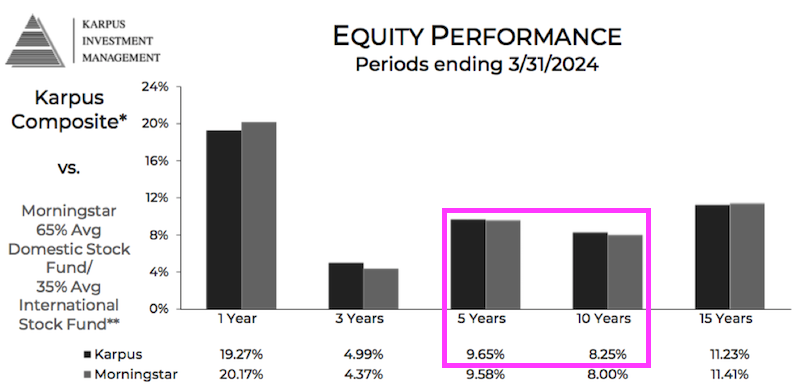

- Equity Management has meanwhile returned a 9.7% compound average over five years versus 8.3% over ten:

- And Conservative Balanced (a mix of fixed income and equities) has returned a 6.6% compound average over five years versus 6.3% over ten:

- This H1 acknowledged CLIG’s funds had lagged the S&P 500 index…

“It is notable that emerging and international markets have substantially lagged the US market since the merger. Indeed, the S&P index has delivered a cumulative return of 49% in the 39-month period versus just 2% for EM and 23% for international markets.”

- …but claimed “relative valuations” were in CLIG’s favour:

“Relative valuations are much lower in the markets where the Group has the majority of its assets under management and discounts in our CEF portfolios are at compelling levels. Our teams are energised and we remain constructive on the outlook for performance at CLIG.”

- I dare say “relative valuations” versus the S&P 500 have been in CLIG’s favour for some years.

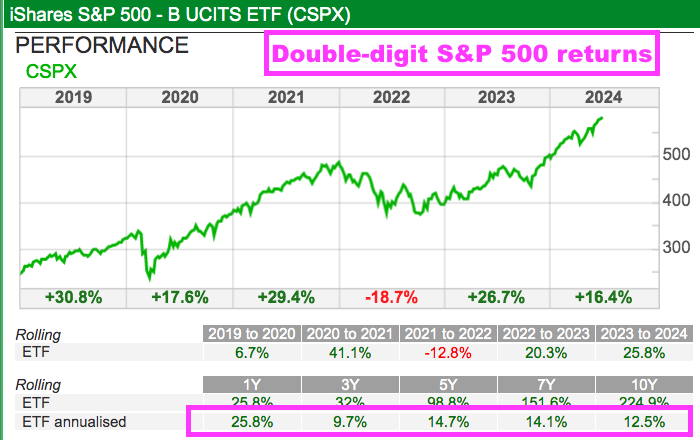

- The S&P 500 — as measured by the iShares S&P 500 ETF (CSPX) — has delivered double-digit annualised (USD) gains during the last decade:

- The CSPX applies a 0.07% annual charge versus an average 0.7% by CLIG’s funds (see Funds under management: fee rates).

- I remain convinced prospective clients have compared CLIG’s funds to the S&P 500 rather than its chosen benchmarks, which would explain the minimal new client money won during recent years…

- …and the aforementioned reference to passive funds within this H1.

- Although NAV (and ultimately share price) progress at investment trusts is dictated by the underlying holdings, I am not clear whether CLIG investigates the underlying holdings to ensure they are appropriate investments.

- CLIM’s website for example summarises the following “key drivers in [the division’s] stock selection process“:

- The historical, net performance of the closed-end fund in NAV terms, versus its benchmark.

- The current discount to NAV of the fund compared to its historical average and its peer group.

- Pre-determined fund liquidation date, if any.

- The potential for the fund’s discount to NAV to narrow due to unitization (conversion to open-ended status), a share buy back program or some other form of corporate activity.

- A wide discount and share buybacks will not result in a good outcome if the investment trust holds a collection of duff shares.

- CLIG’s shareholders still await market conditions that allow CLIM/KIM to record positive returns and outperform the major global indices, which in turn should attract more clients.

- This H1 referred to employee training:

“All employees have attended our ongoing training programme directed towards diversity, equity and inclusion. To reinforce awareness of their role in protecting our network infrastructure, all employees receive monthly training on the critical issue of cybersecurity.“

- I get the impression CLIG’s employees may have been too busy learning about diversity and cybersecurity to think about improving returns for clients.

- A glimmer of hope comes from the retirement of CLIM’s veteran chief investment officer, whose successor might herald enhanced returns for EM clients:

(RNS 2023) “Mark Dwyer, CLIM CIO, has announced his intention to retire from the firm on 30th June 2024. Mark has been with the firm for over 20 years having served as the Head of EM CEF Strategy. We wish him the very best in his retirement.

Oliver Marschner, senior CLIM Portfolio Manager, will assume responsibility for the EM CEF Strategy from 1st January 2024.“

- CLIG’s relative returns have not improved following this H1.

- During CLIG’s Q3 2024 (January to March 2024), CLIM’s strategies returned an estimated 2.5%, KIM’s portfolios returned an estimated 4.3% while the S&P 500 (CSPX) returned 10.1% (see Q3 2024 FuM update).

Funds under management: fee rates

- The comparable H1 said group fee rates had dropped a basis point to 73 basis points:

(H1 2023) “Net fee income currently accrues at a weighted average rate of approximately 73 basis points (31st December 2021: 74 basis points) of FuM.”

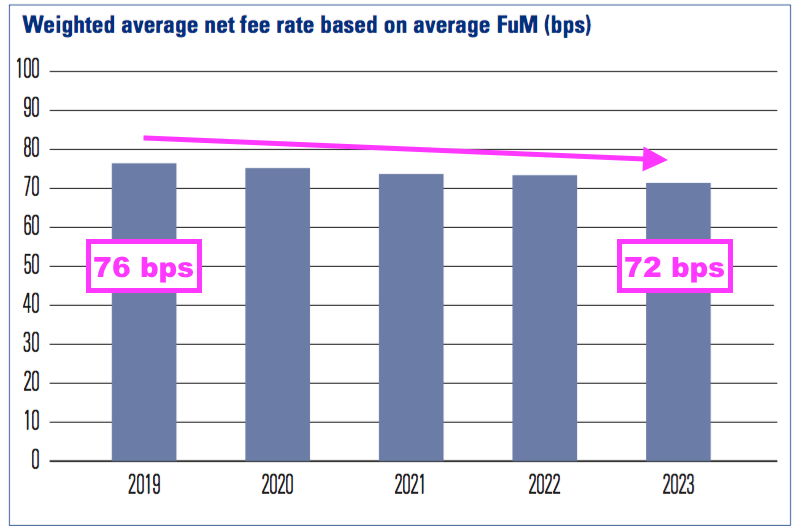

- The preceding FY then said group fee rates had dropped a further basis point to 72 basis points:

(FY 2023) “The Group’s average net fee margin for the year was 72bps (2022: 73bps).

- However, both this H1 and the subsequent Q3 update (see Q3 2024 FuM update) did not confirm a fee rate.

- CLIG’s most recent fee-rate commentary occurred within October’s Q1 2024 FuM update and January’s Q2 2024 FuM update, both of which acknowledged fees accruing at an average 70 basis points:

(Q1 2024) “The Group’s income currently accrues at a weighted average rate of approximately 70 basis points, net of third party commissions.”

(Q2 2024) “The Group’s income currently accrues at a weighted average rate of approximately 70 basis points, net of third party commissions.“

- The sudden lack of fee-rate disclosure feels ominous. Shareholders can only assume the average fee rate after this H1 has fallen below the last-reported 70 basis points.

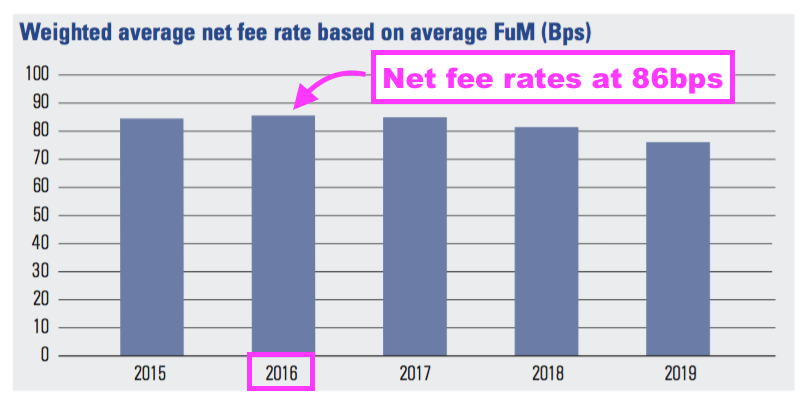

- CLIG’s fee rate has been declining for some time:

- The fee rate was 86 basis points during FY 2016:

- I had previously believed the introduction of lower-fee strategies such as International had influenced the overall group fee rate.

- But with CLIG’s FuM remaining broadly 37% EM, 38% KIM and 25% Other strategies during this H1, different FuM proportions would not influence the overall group fee rate this time.

- Markets generally suffered a rough calendar 2022, which I speculate prompted clients to demand lower fees throughout the preceding FY and this H1.

- I believe fee rates will not stabilise until CLIM’s investment performance in particular improves.

- After all, if typical CLIM clients have indeed earned net annual returns of c4% (i.e. 400 basis points) during the last five years, then fees at 70 basis points a year have captured c15% of their gains.

- In contrast, holders of that S&P 500 ETF delivering double-digit returns would have given away less than 1% of their gains through fees of seven basis points.

Engagement with George Karpus: board membership

- This H1 referred to “a strategy of engagement” with CLIG’s largest shareholder, George Karpus:

“Since our Annual General Meeting on 23rd October 2023, we have pursued a strategy of engagement with our largest shareholder and have had a series of constructive meetings. Discussions on strategy for CLIG’s businesses have been ongoing. We are making progress on a series of shared priorities, including an enhanced focus on the management of our cash balances as well as maintaining our commitment to expense management. We have also been engaging with our other shareholders and, as always, plan to maintain transparency in our ongoing dialogue.”

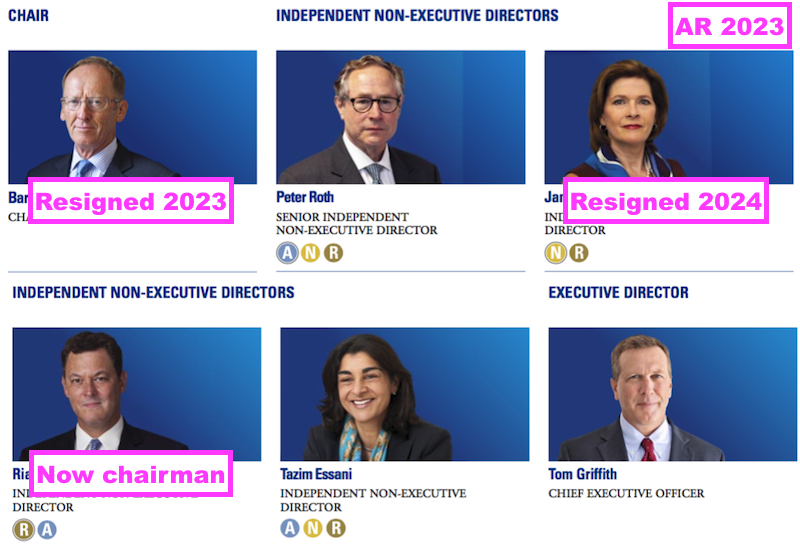

- Mr Karpus founded KIM, became a CLIG non-exec following the CLIM/KIM merger, left CLIG’s board last year and retains a 31.5% personal CLIG shareholding:

- Mr Karpus demanded the board be replaced at the 2023 AGM:

(George Karpus 2023) “I believe the future board should consist of individuals with different skill sets that believe in the great future of CLIG… They should have a combination of experience and skills, so they do not have to rely on outside consultants and advisors…

This board should be replaced with a seasoned group of directors that understand the enormous potential of CLIG and that can guide the management in profitably growing the company.”

- This H1 appeared to respond to Mr Karpus by announcing a replacement non-executive:

“I am pleased to announce that Sarah Ing will be joining CLIG’s Board as a Non- Executive Director as of 1st March 2024. Sarah is a highly effective and seasoned professional in the financial services industry and brings significant Board experience. Sarah’s appointment follows a request by Jane Stabile to resign from the Board with effect from 29th February 2024 due to increasing commitments in her own business.“

- The incoming non-exec is a qualified accountant, ran her own investment business and was a “top-rated equity research analyst“… which seems more relevant to CLIG than the outgoing non-exec’s ‘fintech’ consultancy role.

- I guess only time will tell whether the other three non-execs — and even the new fourth non-exec — will eventually find themselves in the crosshairs of Mr Karpus:

- The H1 small-print emphasised a fundamental difference between how the board and how Mr Karpus utilise CLIG’s services.

- A board member paid CLIG fees of only $211 to manage his or her money:

“Key management personnel are defined as Directors (both Executive and Non-Executive) of City of London Investment Group PLC.

One of the Group’s subsidiaries manages funds for one of its key management personnel, for which it receives a fee. All transactions between key management and their close family members and the Group’s subsidiary are on terms that are available to all employees of that Company. The amount received in fees during the period was $211. There were no fees outstanding as at the period end.”

- Mr Karpus meanwhile paid fees of $39k:

“Person with significant influence

One of the Group’s subsidiaries manages funds for a person with significant influence based on his shareholding in the Group. The amount received in fees during the period was $39k.”

- Paying fees of only $211 suggests the board has very little money invested in CLIG’s funds — which is hardly an endorsement of the group’s strategies to outside clients.

- No wonder Mr Karpus bemoaned at the AGM how most of the board did not “understand the business” nor “appreciate [CLIG’s] excellent money management”:

(George Karpus 2023) “I have found that most of the board members do not understand the business and do not appreciate the excellent money management that has taken place over the years at CLIG. The board members should trust the investment experience [at CLIG] with their own monies as well as their friends’ monies.”

Engagement with George Karpus: corporate cash management

- Mr Karpus said at the 2023 AGM:

(George Karpus 2023) “[The board has] been slow to embrace changes to our reserves (cash management) that would improve returns and reduce risk.”

- Mr Karpus then told me CLIG should:

- Employ the cash-management skills of KIM to enhance the returns on the group’s own cash position, and;

- Promote a corporate cash-management service to clients.

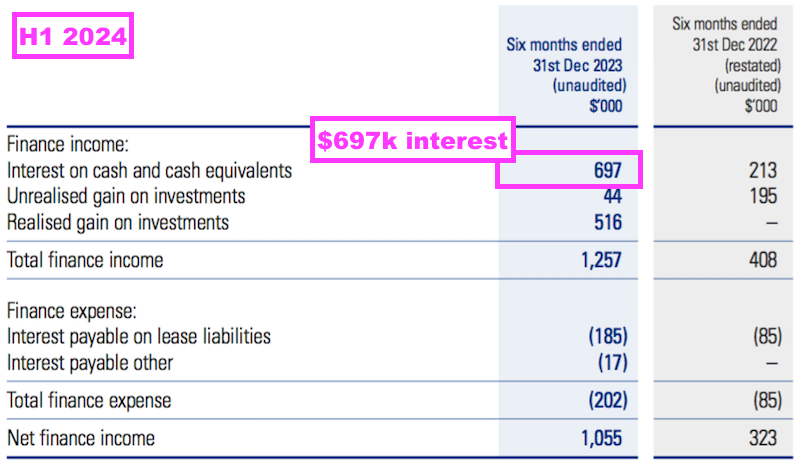

- This H1 revealed significant finance income:

- Collecting interest of $697k on an average cash balance of $27.2m gives an annualised interest rate of 5.1% — well ahead of the levels of interest other companies within my portfolio enjoy.

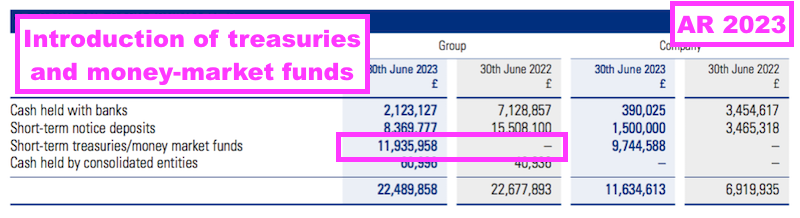

- The 2023 annual report disclosed cash now being held in short-term treasuries and money-market funds (point 23):

- Mr Karpus has clearly had some success persuading CLIG to actively manage its own cash. I am now keen to see CLIG start actively managing cash for its clients.

Engagement with George Karpus: expenses

- Mr Karpus told me last year that CLIG needed to reduce costs to sustain the dividend:

(George Karpus 2023) “Right now I think they must cut costs, and I said in my last board meeting about cutting costs. You have got to look at the areas that are not profitable and get rid of them. The dividend is probably reasonably protected in this current year, but after that it is questionable.”

- This H1 said expenses had been reduced:

“With reduced FuM we have made some reductions in expenses which will benefit the P&L, largely in FY2025 rather than FY2024. We will continue to reduce our costs by taking more aggressive action in the event that FuM falls as we move closer to the current financial year end.“

- January’s Q2 FuM update had previously said the savings would amount to $2.5m a year:

(Q2 2024) “The Group has proactively undertaken cost reductions as part of normal operations reflecting the current market environment. Based on actions initiated to date, savings of c. US$2.5 million of costs per annum will be fully realised in the next financial year.“

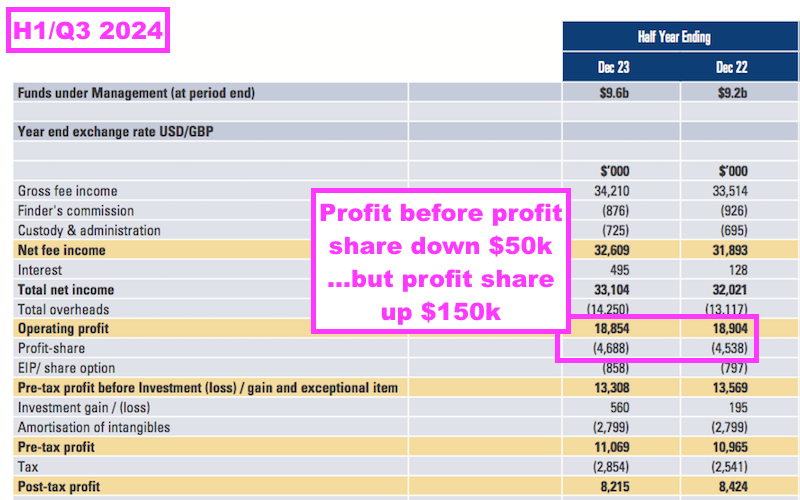

- One cost not reduced during this H1 was the employee profit share, which increased 3%:

- Note that profit before the profit share for this H1 stayed at $18.9m.

- Lifting the profit-share payment just seems wrong when the profit that actually funds the profit share remains unchanged.

- This H1 defended the profit-share payout by claiming “variable pay can be adjusted in line with profitability, and aligns employees with shareholders.“:

“As stated in the Remuneration report contained within our FY2023 Annual Report, rather than making large numbers of employees redundant during market downturns and negatively impacting the business, the variable component of compensation can take the brunt of reduced revenues. Maintaining a high ratio of variable pay for all employees underscores the message that we are a team and rewards should be reduced when the Group underperforms. Variable pay can be adjusted in line with profitability, and aligns employees with shareholders.“

- The variable pay for this H1 was indeed adjusted… just not in line with profitability!

- This H1 included a chart showing a 5% reduction to total employee compensation since FY 2022:

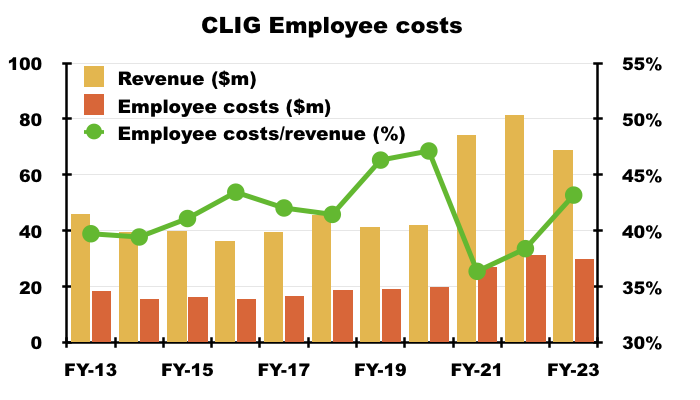

- What CLIG failed to mention was FY 2022 revenue was $81.5m and FY 2024 revenue — based on a doubling of this H1 revenue — could be $68.4m.

- While total employee compensation may have reduced by 5% since FY 2022, revenue may have dived 16% — with obvious implications for profit and margins (see Financials).

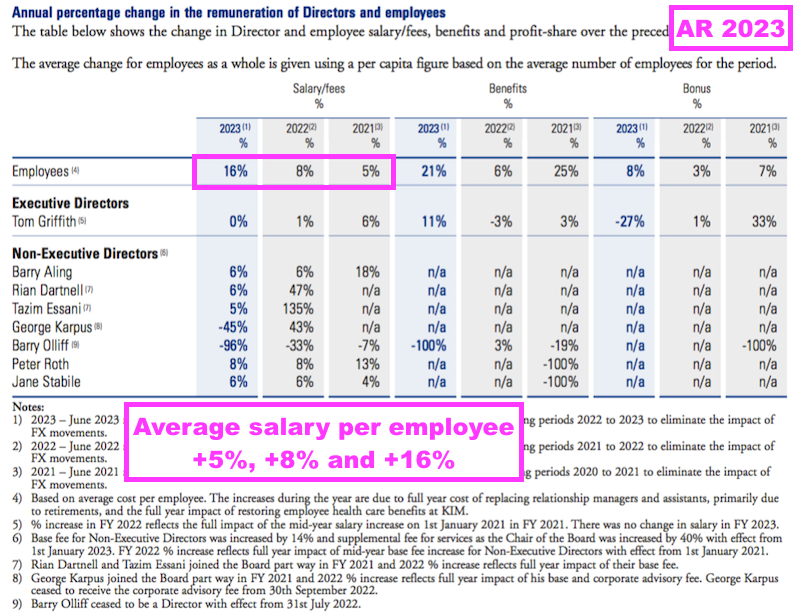

- This H1 cited a “tight labour market” for “modest” salary increases:

“Total compensation for Group employees is comprised of salaries plus related benefits and profit sharing. Salary levels are moderate relative to our competitors as a result of the volatility of markets causing variability in our results. The modest increase in salary and benefit costs over the FY2024 interim period is a product of a tight labour market and continued inflationary pressures. The group has responded to these pressures focusing salary increases on key personnel and areas where the shortage of talent is most acute.”

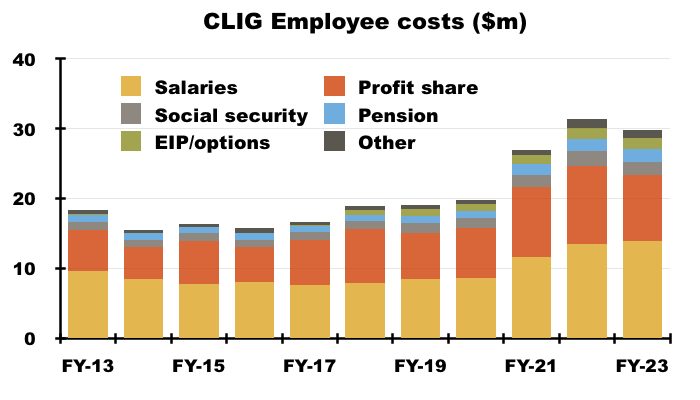

- A “tight labour market” may have prompted the 5%, 8% and 16% lifts to average employee salaries during FYs 2021, 2022 and 2023 (point 12d):

- The same FYs saw shareholders collect a standstill 33p per share dividend.

- No wonder Mr Karpus told me last year the directors “veer too much on the side of employees“:

(George Karpus 2023) “They must take better care of the clients, and focus more on the shareholders. I think they veer too much on the side of the employees, particularly in the last few years. And that has to change.”

- I remain unconvinced CLIG’s salary structure, profit-share pool, option scheme, 12.5% pension contributions and other perks have actually incentivised the workforce to deliver greater returns for shareholders through additional FuM, revenue and profit:

- I note, prior to the Karpus merger, total employee expenses had increased from 40% to 47% of revenue…

- …and following the Karpus merger have rebounded from 37% to 44%:

- I am hopeful:

- The aforementioned cost savings of $2.5m reflect reduced employee expenses;

- Further employee savings can be made that would not harm client returns, service levels or marketing, and;

- The board (through further “engagement” with Mr Karpus) starts to run the group for shareholders rather than to support comfortable lifestyles for non-essential/non-performing staff (note: the total cost per employee during FY 2023 was £213k).

Engagement with George Karpus: corporate governance

- After speaking to Mr Karpus last year, I pondered whether CLIG could switch its listing from the main market back to AIM:

- “I do wonder whether CLIG changing its stock-market listing to AIM could help Mr Karpus revamp the board to his liking.

- CLIG initially floated on AIM during 2006, and re-joining the lighter-regulated junior market from the main market could ease some of the corporate-governance requirements (and costs!) that appear to frustrate Mr Karpus.“

- This H1 dismissed rejoining AIM on corporate-governance grounds:

“In Barry Aling’s final statement as Chair, he stated that CLIG is committed to meeting the standards of our UK listing although it has created a meaningful burden in terms of human and financial resources. To put this statement into historical perspective, CLIG moved from AIM to the main market listing of the LSE in October 2010, in order to meet the requirements of increased transparency on corporate governance initiatives from UK institutional investors.

This successful transition to the main market was critical in broadening the pool of potential investors and increasing demand for Group shares. The stringent demands on the Group from the UK Corporate Governance Code help us in our role of acting as a steward of our shareholders’ trust and remaining on the main market is important to the future of the Group in retaining a larger existing and prospective shareholder base. Recent announcements from the FCA that it will be reducing the regulatory burden on UK listed companies are a welcome development, and begin to address some of the concerns raised in Barry Aling’s final statement as Chair.”

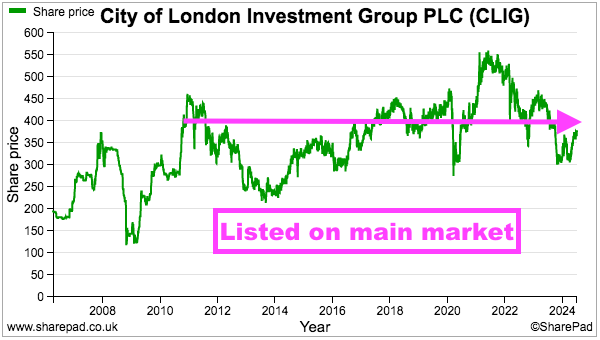

- CLIG’s shares switched from AIM to the main market on 29 October 2010, at which point they opened at 394p versus the recent 370p:

- Almost 14 years without a capital gain is not exactly resounding evidence of “stringent” corporate governance leading to better shareholder outcomes.

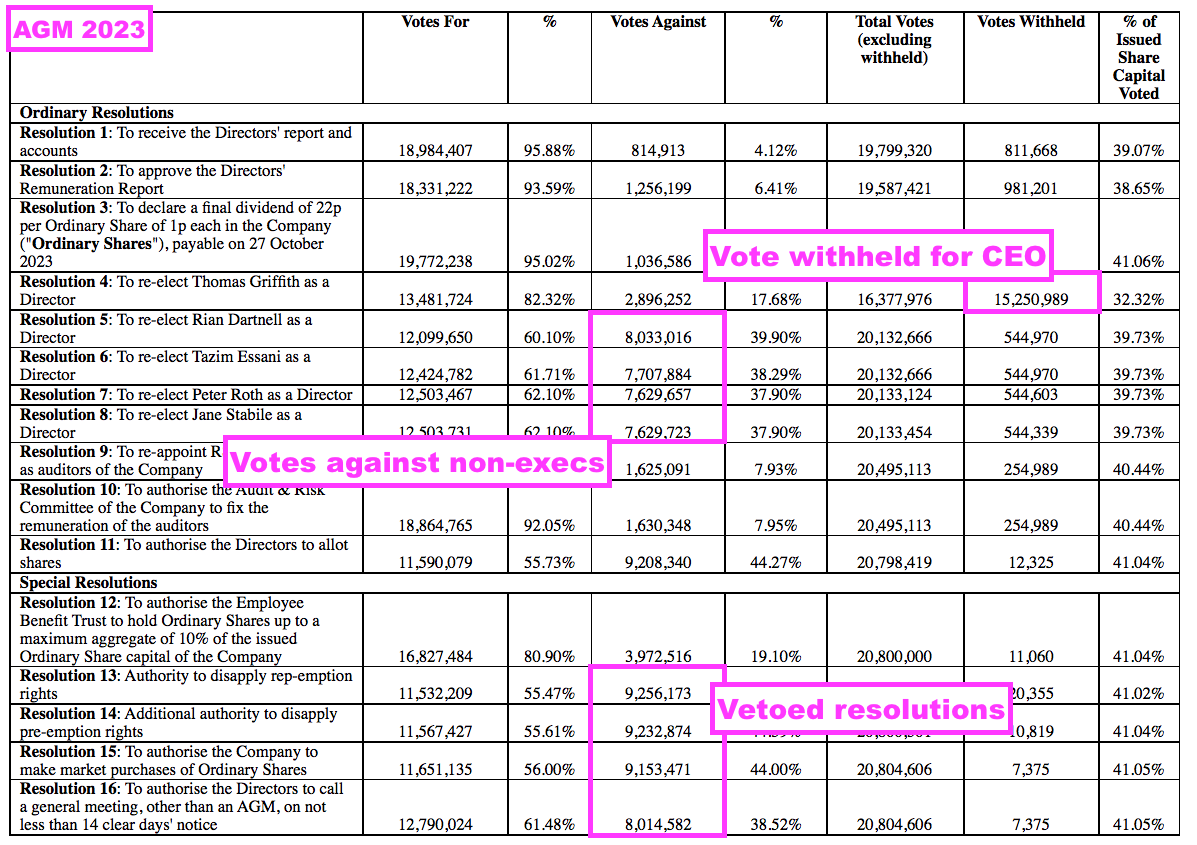

- Mr Karpus accompanied his AGM statement by voting against the re-election of the non-execs:

- The Corporate Code that CLIG adheres to so much asks companies that receive significant protest votes to publish “an update on the views received from shareholders and actions taken” within six months:

(FRC 2018) “When 20 per cent or more of votes have been cast against the board recommendation for a resolution, the company should explain, when announcing voting results, what actions it intends to take to consult shareholders in order to understand the reasons behind the result. An update on the views received from shareholders and actions taken should be published no later than six months after the shareholder meeting“

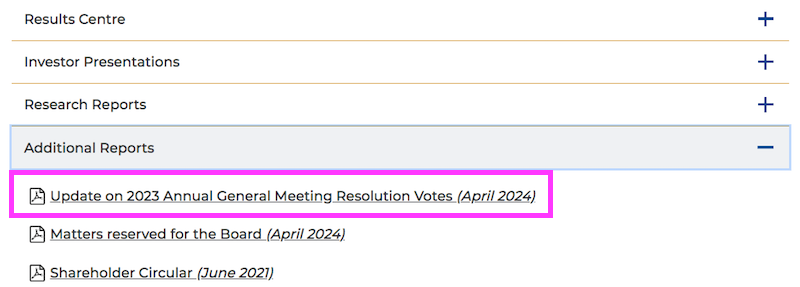

- CLIG quietly published its six-month update on its website during April:

- I had assumed CLIG’s commitment to tip-top corporate governance would see the six-month update published through the RNS.

- The six-month update simply repeated the text previously published within this H1:

(Update 2024) “As reported in our Half Year Report for the six-months ended 31 December 2023, since our Annual General Meeting on 23 October 2023, we have pursued a strategy of engagement with the controlling shareholder group which arose following the Company’s merger with Karpus Management, Inc on 1 October 2020 and have had a series of constructive meetings. Discussions on strategy for the Company’s affiliated businesses have been ongoing. We are making progress on a series of shared priorities, including an enhanced focus on the management of our cash balances as well as maintaining our commitment to expense management. We have also been engaging with our other shareholders and, as always, plan to maintain transparency in our ongoing dialogue.

A further update on this matter will be provided in the 2024 Annual Report & Accounts.”

- I am not convinced summarising a “series of constructive meetings” into one paragraph published quietly on the website is maintaining “transparency” about the “ongoing dialogue“.

- I trust/expect the forthcoming 2024 annual report will provide much greater insight into CLIG’s “strategy of engagement” with Mr Karpus.

Financials

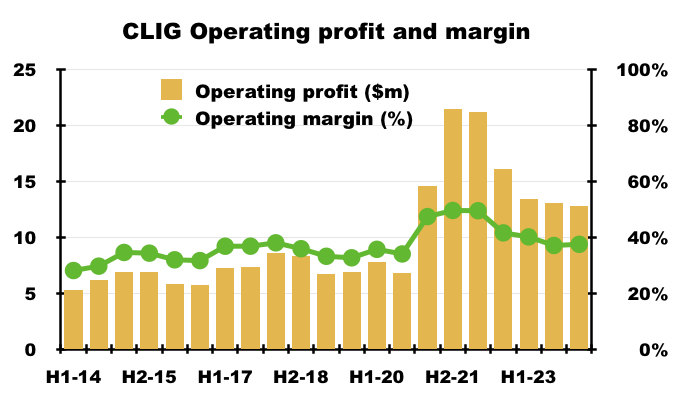

- CLIG remains a high-margin business, although not as high as it once was.

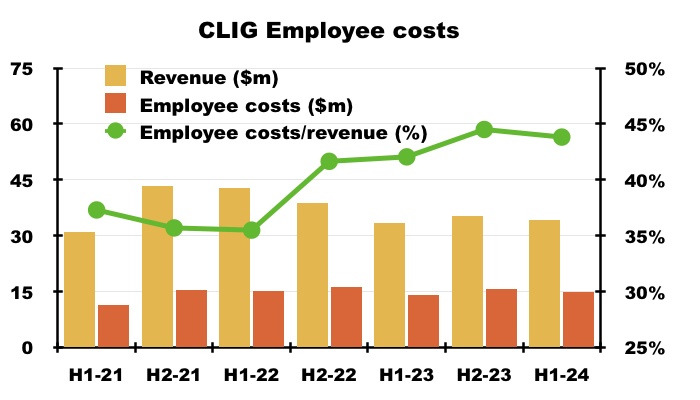

- A healthy 37% of revenue converted into operating profit before amortisation during this H1. That said, the margin was 49% during FY 2021, 46% during FY 2022 and 39% for FY 2023:

- Lower fee rates without commensurate FuM advances and/or without reduced overheads will inevitably squeeze CLIG’s margin further.

- The balance sheet showed cash at $25.9m, investments at $5.4m and conventional bank debt at zero.

- Cash conversion for this H1 was very acceptable.

- Adjusted earnings of $9.9m translated into free cash of $8.8m, with the $1.1m divergence due mostly to greater cash taxation payments. Assisting cash generation was minor expenditure on tangible assets ($0.5m) and a small working-capital investment ($0.6m).

- Overall cash was left $2.7m lighter after $13.0m was spent on dividends, a net $1.0m was spent on shares for the employee benefit trust (EBT) and $2.5m was raised from the sale of investments.

- CLIG’s share-incentive accounting charge became more realistic during this H1.

- In the past, the actual cash cost of the employee share scheme has substantially exceeded the associated accounting expense.

- Between FYs 2019 and 2023 for example, the EBT spent a net $11.4m buying shares to satisfy exercised options while the accounting charge during that same period was $5.4m.

- But during this H1, the share-incentive accounting charge increased to $1.1m and in fact slightly surpassed the net amount spent on shares for the EBT.

- The $2.5m proceeds from the disposal of investments was notable. Mr Karpus told me last year he wanted CLIG to close its sub-scale funds:

(George Karpus 2023) “I suspect they spend £0.5m a year on these [REIT] strategies and they have not produced a dollar of revenue for five years. I asked, ‘when are you going to pull the plug on them?‘”

- All of CLIG’s investments were seeded funds as per the 2023 annual report (point 27), and therefore the $2.5m proceeds imply CLIG has listened to Mr Karpus and closed a sub-scale fund. The H1 commentary did not mention the $2.5m sale.

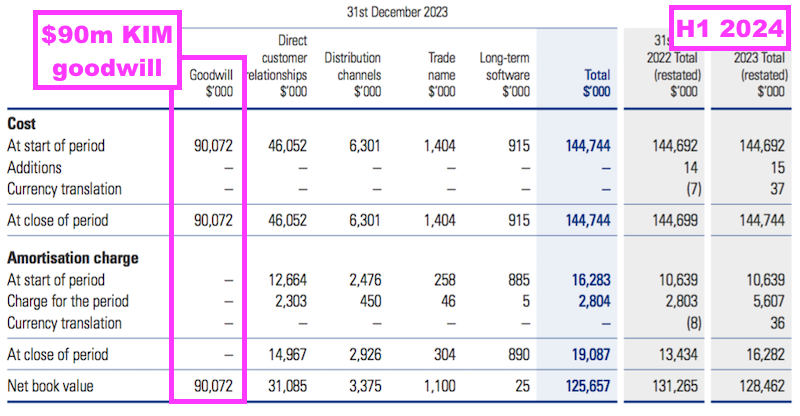

- This H1 showed goodwill relating to the KIM merger at $90m:

- The 2023 annual report (point 20) disclosed rather awkward text about changing the way the KIM goodwill is tested for impairments:

(AR 2023) “The Group had assessed the recoverable amount of the CGU by its value in use, as in the prior period, and found that it was less than the carrying value owing to a higher discount rate and reduced growth forecasts due to changes in market conditions. The Group thus reassessed the recoverable amount by its fair value (Fair Value) less cost of disposal (FVLCOD), which exceeds the carrying value.”

- From what I can tell, CLIG changed the goodwill-testing method because the original method would have led to an impairment.

- Impairing the KIM goodwill would essentially admit the value applied to KIM at the time of the merger was too high.

- Re-jigging KIM’s goodwill testing is perhaps not surprising when other small-print within the 2023 annual report projected KIM’s costs growing at 3% a year but KIM’s revenue growing at only 1.5% a year:

(AR 2023) “The key assumptions underlying the budgets are based on the most recent trading activity with built in organic growth, revenue and cost margins. The annual growth rate used for extrapolating revenue forecasts was 1.5% and for direct costs was 3.0% based on the Group’s expectation of future growth of the business.”

- CLIG announced a new auditor during March:

(RNS 2024) “City of London (LSE: CLIG), a leading specialist asset management group offering a range of institutional and retail products investing primarily in closed-end funds (“CEFs”), is pleased to announce that it has completed a tender process, overseen by CLIG’s Audit and Risk Committee, for its Group audit. This has resulted in a recommendation from the Audit and Risk Committee, which has now been endorsed by the Board, that Grant Thornton UK LLP be appointed as the Group’s auditor with immediate effect. Grant Thornton UK LLP will, therefore, undertake the Group audit for the financial year ending 30th June 2024.”

- Whether the new auditor was recruited to take a more lenient or rigorous approach to goodwill-impairment testing remains to be seen.

- CLIG’s accounts remain free of defined-benefit pension obligations.

Q3 2024 FuM update

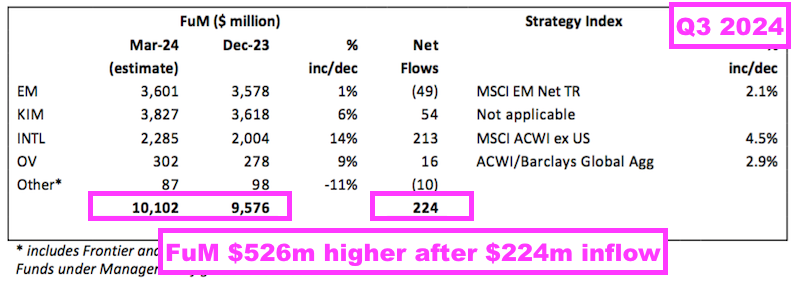

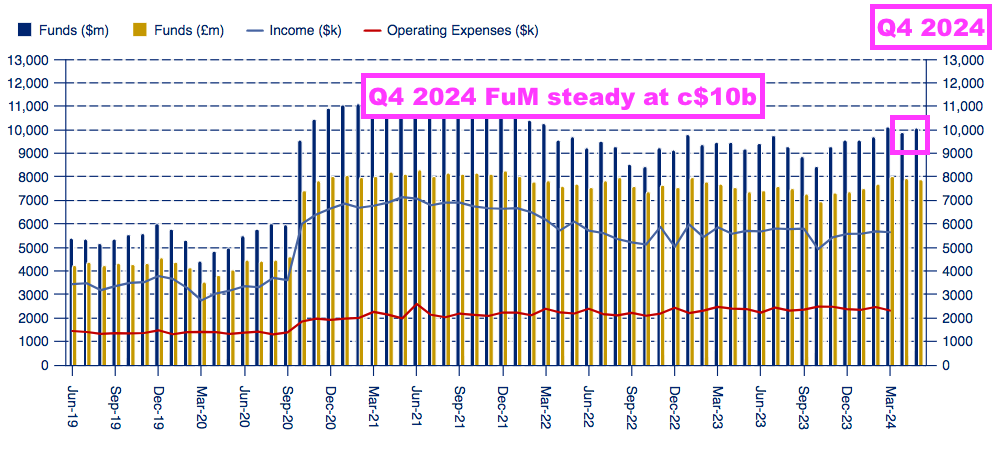

- Following this H1, April’s Q3 2024 FuM update revealed FuM surpassing $10b for the first time since Q3 2022:

- April’s update also revealed new client money of $224m, which was the:

- First quarterly inflow since Q1 2023, and;

- Largest quarterly inflow since CLIG commenced publishing quarterly updates during FY 2018:

- Of the $224m received, $170m went into CLIM funds — the largest quarterly inflow for CLIM for at least five years:

- The remaining $54m of the $224m received was given to KIM and registered the division’s first meaningful inflow following the October 2020 merger:

- CLIG’s previous quarterly statements always included references to fee rates and profit run-rates. January’s Q2 FuM update for example reported the following:

(Q2 2024) “The Group’s income currently accrues at a weighted average rate of approximately 70 basis points, net of third party commissions. “Fixed” costs are c. US$2.3 million per month, and accordingly the current run-rate for operating profit before profit-share is approximately US$3.2 million per month based upon current FuM.“

- But this Q3 update did not include references to fee rates nor profit run-rates.

- The absence of information previously supplied on a regular basis seems very ominous.

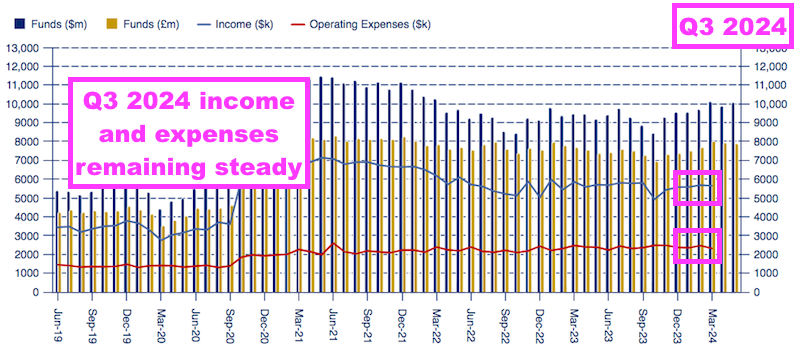

- That said, CLIG’s website provides some reassurance Q3 income and profit have not collapsed:

- Q3 FuM increasing by $526m of which $224m was net new client money meant market movements generated extra FuM of $302m through an approximate 3.2% return.

- The same website chart shows FuM for April and May 2024 remaining around the $10b mark:

Valuation

- This H1 gave a vague outlook:

“Our teams are energised and we remain constructive on the outlook for performance at CLIG.”

“Despite a headwind versus a tailwind, the Group is positioned to go further together, with thanks and appreciation to our colleagues for navigating the rough seas.”

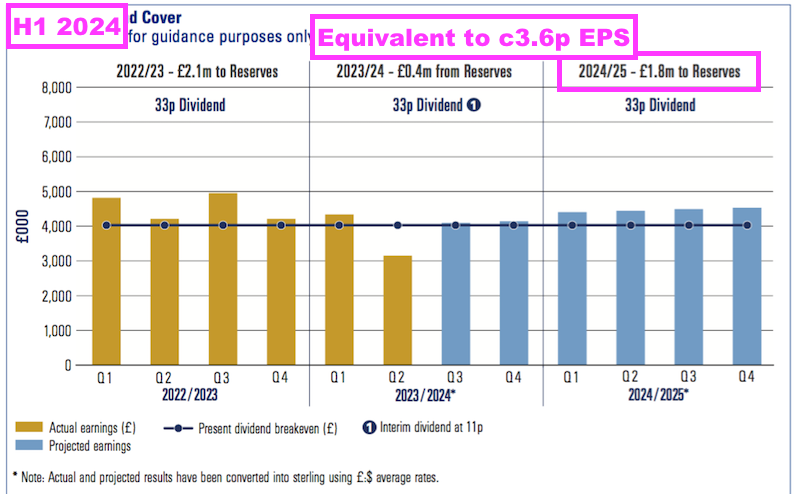

- The aforementioned dividend-cover chart was unchanged from the one published within January’s Q2 2024 FuM update that projected retained earnings of £1.8m for FY 2025:

- Retained earnings of £1.8m are equivalent to 3.6p per share and, when added to the 33p per share dividend, implies FY 2025 earnings might now be 36.6p per share.

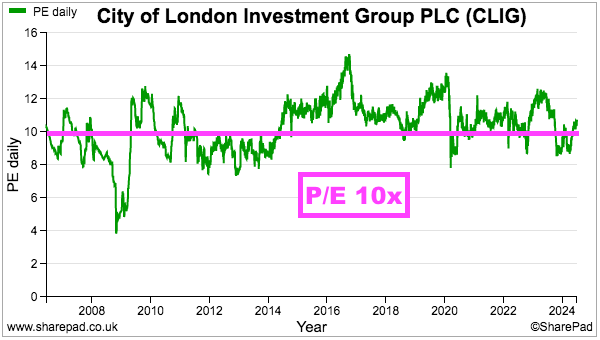

- Possible earnings of 36.6p per share and the trailing 33p per share dividend put the 370p shares on a P/E of approximately 10x and yield of 9%.

- Although CLIG has always traded around a 10x rating…

- …the present yield has been witnessed only on a handful of occasions during the last 15 years:

- Future returns can be judged through CLIG’s (commendably public) total-return ambition, which is said to “stretch the management team”:

(FY 2023) “The goal of this KPI is for the total return (share price plus dividends) to compound annually in a range of 7.5% to 12.5% over a five-year period. This KPI is meant to stretch the management team, without incentivising managers to take undue levels of risk.”

- The minimum 7.5% compound annual total return during the next five years appears very achievable, assuming of course the 33p per share dividend is sustained to support that 9% income.

- The preceding FY had confirmed the KPI was achieved for the five years ending FY 2023:

(FY 2023) “Over the past five years, the average annualised return to shareholders is 8.0%, within the 7.5%-12.5% target range.“

- But my calculations indicate the KPI was not achieved for the five years ending FY 2024:

- The starting share price on 01 July 2019 was 406p;

- Dividends of 171.5p per share were then collected;

- The price finished the five years down 36p to 370p on 30 June 2024, and;

- The total return was 33% or approximately 6% per annum.

- What the repercussions are for the board after the KPI failed to meet the 7.5%-12.5% target remain to be seen.

- The KPI could be achieved for the five years ending FY 2025:

- The starting share price on 01 July 2020 was 383p;

- Dividends of 143.5p per share have so far been collected;

- The price is currently 13p lower at 370p, and;

- The total return to date is 34% or approximately 7.5% per annum with still one year to go.

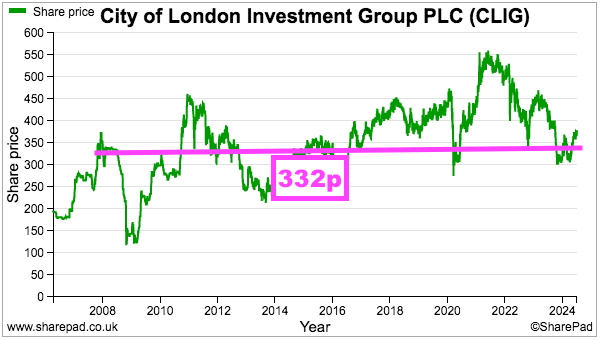

- Earlier this year I bought more CLIG at 332p, a price first witnessed during October 2007…

- …and the lack of capital appreciation over nearly 17 years does suggest CLIG’s operating economics, business strategy and/or employee talent are not quite what they should be.

- I am hopeful:

- Glamour stocks powering the S&P 500 will not remain glamorous forever;

- Markets could then one day rotate into CLIG funds offering “compelling” value;

- The Q3 2024 FuM inflows are evidence of improved CLIG marketing, and;

- Costs can be controlled to help earnings steadily improve and fully secure the 9% yield.

- But this H1 has reiterated the danger of the handsome payout eventually becoming untenable as:

- Major new clients remain very elusive;

- Client returns remain modest;

- Client fees keep reducing, and;

- Employee costs keep advancing.

- The saving grace with CLIG is 31.5% shareholder Mr Karpus, who has thankfully engaged with the board to improve progress and protect the dividend.

- My definite impression from speaking to Mr Karpus last year was he would not entertain CLIG’s modest performance forever.

- CLIG now has its Q4 FuM update (due 25 July), FY 2024 results (due 17 September) and Q1 2025 FuM update (due 21 October) to impress Mr Karpus before the AGM on 28 October…

- …at which point Mr Karpus may issue another scathing statement about the board and take firm action to oust the directors.

Maynard Paton

Excellent review, as ever, Maynard. As you know, I do not think that the disclosures to date that CLIG has made in relation to the concerns raised by George Karpus at the 2023 AGM are adequate or close. If things do not change, I intend to raise that issue at the 2024 AGM. I wonder if we can expect another statement at the 2024 AGM from Mr Karpus’ representatives, as happened in 2023? The changes that have been made to date are quite limited, but I am inclined to favour evolution rather than revolution. But further change is required.

Thanks Andrew. I hope to be there at the AGM as well. Something I did not mention in the blog post is CLIG’s shareholder register listing Hargreaves Lansdown, Interactive Investor, AJ Bell and Halifax Share Dealing as major investors — which I presume reflects significant ownership by private investors. And yet CLIG does not conduct webinars for PI questions, which would help us learn more about the discussions with Mr Karpus. CLIG now has a few months to persuade Mr Karpus against another protest vote!

Maynard

Maynard,

I hold through HL, Interactive Investors and a couple of other platforms. I think that CLIG should engage via InvestorMeetCompany or similar, in addition to face to face meetings. As you know, many other companies do that.

Andrew

City of London Investment (CLIG)

Pre-Close Trading Update for the year to 30 June 2024 published 25 July 2024

A statement that raised more questions about what was not said than what was said. Here is the full text interspersed with my comments:

——————————————————————————————————————

City of London (LSE: CLIG), a leading specialist asset management group offering a range of institutional and retail products investing primarily in closed‐end funds (“CEFs”), provides a pre‐close trading update for its financial year ended 30 June 2024. The numbers that follow are unaudited.

Funds under Management (FuM) were $10.2 billion at 30 June 2024, an increase of 8.7% as compared to $9.4 billion at 30 June 2023. A breakdown by strategy follows:

IM Performance

Investment performance was ahead of the benchmark for the majority of the Group’s strategies during the financial year. CLIM’s International Equity, Opportunistic Value and Frontier Markets outperformed, while Emerging Markets (EM) equity lagged its index over the period. KIM’s fixed income strategies, international equity, conservative balanced and SPAC strategies outperformed their market indices over the period, while the US equity strategy lagged its benchmark.

Flows

Net investment outflows reduced significantly to $26 million in the second half of the financial year, from $294 million in the first six months ending December 2023. Net investment outflows totalled $320 million for the Group over the twelve‐month financial year as clients reduced exposure to EM due to ongoing geopolitical volatility. International equity strategies attracted more than $150 million in net new inflows over the period. Attractive discounts in the strategies continue to be the focus of marketing efforts across the Group’s asset classes. ”

——————————————————————————————————————

The figures in the table above reflect FuM movements over the twelve months, but we can deduce Q4 witnessed:

* EM FuM outflows of $204m;

* International FuM inflows of $30m;

* OV FuM outflows of $64m;

* Other FuM inflows of zero, and;

* KIM FuM outflows of $12m.

The total Q4 FuM outflow was therefore $250m, meaning the Q3 inflow of $224m referred to in the blog post above was sadly not sustained. CLIG has now experienced outflows during 11 of the last 16 quarters that combine to a net $1,327m.

At least investment performance/market movements were positive, and FuM at $10,241m is the highest since Q3/March 2022 ($10,265m). Investment movements during this FY were -$391m during Q1, but +$837m, +$302m and +$389m during Qs 2,3 and 4 respectively.

EM FuM continues to shrink as a proportion of total FuM, down to 35% at the end of this Q4 — the lowest percentage ever. International FuM meanwhile stands at its highest ever level — $2,394m, or 23% of total FuM.

——————————————————————————————————————

Dividend

The Board expects the final dividend for the year ended 30 June 2024 to be in line with the previous year. Following the completion of the year‐end audit, the Board will announce the final dividend and results alongside publication of its Accounts for the year ended 30 June 2024 on 17 September 2024.

The Group’s Annual General Meeting will be held on 28 October 2024 and the Group expects the dividend payment date to be in November 2024 similar to last year’s timing.

——————————————————————————————————————

This Q4 statement was not as clear as last year’s Q4 statement.

Last year CLIG declared a 22p per share final dividend, published the payment timetable and even explained how shareholders could elect to receive their payment in USD. CLIG also accompanied the announcement with this refreshed dividend-cover template:

No such dividend information this year. We are simply told the dividend should be “in line” with last year — i.e. 22p per share — but the lack of specifics does make me wonder.

In particular, the change of functional currency during this FY from GBP to USD could mean the final dividend is in fact held at last year’s 26.8 US cents per share. 26.8 US cents translated at the recent GBP:USD of 1.28 gives 20.9p per share — so a slight reduction on the supposed 22p.

As I noted in the blog post above, the 1.2x dividend-cover policy is under review this year and the board may well reconsider whether declaring a GBP-denominated payout is sensible when reporting USD earnings. The lack of specific dividend information within this year’s Q4 update suggests to me the final payout may not be 22p per share.

Interesting that CLIG uses the phrase “Following the completion of the year‐end audit“. The year-end audit did not interfere with the 22p final dividend being declared within last year’s Q4 statement!

I wonder if CLIGs new auditor — Grant Thornton (of PatVal fame!) — is looking at the accounts in a bit more depth than its predecessor RSM.

I note the 2023 annual report (points 11a and 20) revealed the goodwill impairment methodology was changed to avoid a write-down of the KIM goodwill — which was not a good look for either CLIG or RSM.

Also missing from this update was text outlining fee rates and expected profits, which was contained within last year’s Q4 update:

[RNS July 2023] “The Group’s income currently accrues at a weighted average rate of approximately 71 basis points of FuM, net of third party commissions.

The Group’s overheads for the year to 30 June 2023 are expected to be £22.5 million (2022: £19.7 million), primarily as a result of weaker sterling against USD as well as higher employee retention and retirement costs during the year. “Fixed” costs are c.£1.9 million per month, and accordingly the run-rate for operating profit, before profit-share and amortisation of intangibles is approximately £2.6 million per month based upon current FuM and a US$/£ exchange rate of US$1.2703 to £1 as at 30 June 2023.

For the year to 30 June 2023, the Group estimates that the unaudited profit before amortisation of intangibles and taxation to be approximately £23.4 million (2022: £27.2 million profit before amortisation of intangibles).

Profits after an anticipated tax charge of £3.9 million (representing 21% of profits before taxation) will be approximately £14.8 million (2022: profits of £18.1 million after a tax charge of £5.0 million, representing 22% of profits before taxation). Basic and fully diluted earnings per share are expected to be 30.4p and 29.8p respectively (2022: 36.9p and 36.4p).”

CLIG does seem to be reducing the amount of information disclosed to shareholders. The blog post above bemoans the reduced disclosure on fee rates (“The sudden lack of fee-rate disclosure feels ominous“).

The silver lining I suppose is that if CLIG’s FY 2024 results do contain bad news, largest shareholder George Karpus is likely to cause ructions at October’s AGM. Last year’s AGM witnessed Mr Karpus demand all of the board be replaced.

Maynard

City of London Investment (CLIG)

Full-Year Results release date published 13 September 2024

The auditors require more time to assess the books and the publication of the FY 2024 results has been delayed by a week.

Pre-pandemic, such a delay would ring loud alarm bells, although post-pandemic, audit delays have become more commonplace and less worrisome.

For CLIG, an audit delay does not look good. Here is the full text:

——————————————————————————————————————

The Company is announcing a short delay in the release for our Full Year Results.

The Group’s auditor, Grant Thornton UK LLP (GT), has requested additional time to complete their standard procedures as part of the audit finalisation process. Results were due to be released on 17 September 2024, as set out in our pre-close trading update on 25 July 2024. As a result, the Board will now announce the final dividend and results alongside publication of its Accounts for the year ended 30 June 2024 on 24 September 2024.”

——————————————————————————————————————

As per my comment above, I wonder if CLIGs new auditor — Grant Thornton (of PatVal fame!) — has looked at the accounts in a bit more depth than its predecessor RSM.

I note the 2023 annual report (points 11a and 20) revealed the goodwill impairment methodology was changed to avoid a write-down of the KIM goodwill — which was not a good look for either CLIG or RSM.

I am willing to stick my neck out and predict the FY 2024 results have been delayed a week because — following discussions between the board and Grant Thornton — they will contain a write-down to the KIM goodwill.

Also, the preceding Q4 trading update — unlike the Q4 update of 2023 — did not declare the final dividend. As per my comment above, the lack of specific dividend information within this year’s Q4 update suggests the final payout may not be maintained at 22p per share.

Let’s see if my guesswork is correct! I am happy to be proven wrong on both counts.

EDIT: 24 September 2024

FY 2024 results now published and I am happy to be proven wrong on both counts!

Although the small-print does say “The Group had assessed the recoverable amount of the CGU by its value in use and found that it was less than the carrying value owing to a higher discount rate and reduced growth forecasts due to changes in market conditions. The Group thus reassessed the recoverable amount by its fair value (Fair Value) less cost of disposal (FVLCOD), which exceeds the carrying value.”

So the lack of goodwill impairment still seems a borderline decision.

Maynard