29 September 2017

By Maynard Paton

Happy Friday! I hope you continue to enjoy my Blog… and that your shares have fared well during the summer.

After experiencing positive first and second quarters, my portfolio has maintained its gains and its performance has improved to 14.0% for the year so far.

Furthermore, following an inactive second quarter, I have since dusted off my share-dealing account and executed a few buys and sells.

I have top-sliced one holding and added to two existing holdings. More on those trades a bit later.

Sadly, I have to admit that — once again! — a lot of my time of late has been absorbed by matters outside of investing.

While I’ve managed to keep on top of the news from my own portfolio, I’ve still not had the chance to study other companies and publish fresh watch-list reviews.

This is how my portfolio has changed since the start of the year

I publish updates every quarter to round-up what’s been happening within my portfolio, and this Blog post outlines my July/August/September activity. You can read all of my previous round-ups here.

The table below shows how my portfolio has changed since the start of the year:

| Holding | Weighting 31 Dec 2016 (%) | Weighting 31 Mar 2017 (%) | Weighting 30 Jun 2017 (%) | Weighting 30 Sep 2017 (%) |

| Andrews Sykes | 3.4 | 3.3 | 4.2 | 4.2 |

| Bioventix | 5.3 | 6.6 | 6.9 | 9.5 |

| Castings | 6.7 | 7.1 | 6.7 | 6.5 |

| City of London Inv | 6.5 | 6.7 | 7.1 | 7.0 |

| Daejan | 7.1 | 7.0 | 6.6 | 5.9 |

| Electronic Data Proc | 2.8 | - | - | - |

| Getech | 3.8 | 3.4 | 2.9 | 2.4 |

| Mincon | 3.3 | 3.8 | 4.0 | 4.2 |

| Mountview Estates | 8.9 | 8.3 | 8.5 | 8.2 |

| Record | 5.7 | 6.9 | 6.4 | 6.9 |

| S & U | - | 4.3 | 4.1 | 3.9 |

| System1 | 2.6 | 3.5 | 3.6 | 2.1 |

| Tasty | 7.6 | 3.7 | 2.6 | 6.3 |

| FW Thorpe | 9.1 | 8.8 | 10.2 | 8.9 |

| Tristel | 8.0 | 9.9 | 8.9 | 9.1 |

| M Winkworth | 5.6 | 5.4 | 5.7 | 5.7 |

| World Careers Network | 4.4 | 4.1 | 4.1 | 3.9 |

| Cash | 9.2 | 7.2 | 7.5 | 5.3 |

| TOTAL | 100.0 | 100.0 | 100.0 | 100.0 |

I should add that I injected some cash into my portfolio at the start of August. The sum represented almost 2% of my portfolio’s end-2016 value, and the aforementioned 14.0% return has been calculated based on a part-year contribution from that additional money.

A busy quarter with news from 13 of my 16 shares

As usual I have kept watch on all of my existing holdings. Here is a summary of the Q3 news:

* Satisfactory statements from Andrews Sykes, Bioventix, Daejan, Mincon, S & U and FW Thorpe;

* An informative open day at Tristel;

* Acceptable progress at City of London Investment and M Winkworth;

* Lacklustre statements from Getech and Record;

* Underwhelming news from Tasty;

* A profit warning from System1, and;

* Nothing of major significance from Castings, Mountview Estates and World Careers Network.

Adding to Tasty and Winkworth, and selling some Tristel

Amid all the Q3 results and updates, I topped-up two investments and top-sliced another.

I increased my holding in restaurant chain Tasty by 286%, paying an average 47.1p including all costs.

With the share price now around 36p, I was clearly too early with my purchases.

As I mentioned within my latest Tasty update, I continue to have faith in the two members of the Kaye family that sit on the board.

The Kayes have already built and sold multi-bagger restaurant groups ASK Central for £223m (in 2004) and Prezzo for £304m (in 2015)…

…and I’m trusting the Kaye directors will — eventually! — sell Tasty for a lot more than its current £22m market cap.

Meanwhile, I have upped my holding in estate-agency franchisor M Winkworth by 11%. I paid 103.5p including all costs.

I felt the firm’s recent results were quite acceptable in the circumstances.

Winkworth is dependent mostly on London’s struggling property market, and yet appears to be out-performing its largest rival quite well. I also like how the subdued trading conditions seem to be persuading more potential franchisees to consider joining the group.

I paid a multiple of about 9 times earnings and I should collect a yield of 7%. The rating seems modest for a business that boasts net cash, high margins and moderate growth prospects.

My top-slice was Tristel, where I cut my holding by 21% at 288.9p including all costs.

I sold mainly because the rating of the disinfectant specialist had become somewhat extended.

Based on my earlier sums, I calculated the near-term P/E to be close to 30 and the medium-term P/E — using somewhat confident growth projections — to be about 25.

True, I was quite impressed by Tristel’s open-day presentation and the potential for the group’s projects in the United States. But the company has yet to receive any regulatory approval in the States and I thought better medium-term opportunities lay elsewhere in my portfolio.

Today I look at management capability and track records.

Three months ago I started to evaluate my shares on the theme of management.

As I have stated in How I Invest (my bold):

“I want my investments to be led by loyal and capable bosses that have served in the top job for several years. I want to see improvements to profits and the dividend throughout their leadership. Better still is the founder/entrepreneur boss, who set up the firm in the first place, has led it ever since and has therefore shown even more commitment to building the business.”

WithIn my previous quarterly round-up, I evaluated loyalty and commitment. In this post I look at management capability and track records.

Profit growth? Return on capital? Dividends?

Let me start by saying this analysis was not at all straightforward.

I mean, exactly how do you assess management capability and track records… and arrive at a fair and proper judgement?

Do you concentrate on profit growth? What about return on capital? Is dividend consistency considered? Or does share-price performance outweigh everything?

To be honest, I wan’t entirely sure how to accurately measure the leadership talent at my 16 shares.

In the end, I chose to judge the bosses on length of tenure mixed in with overall operating profit growth, dividend consistency and the frequency of ‘setback’ years — times when profit fell significantly (more than 20%) and/or when the payout was cut.

I have assessed each leader since they took on the top job (limited to the last 20 years), or since their company floated, whichever is the shorter period.

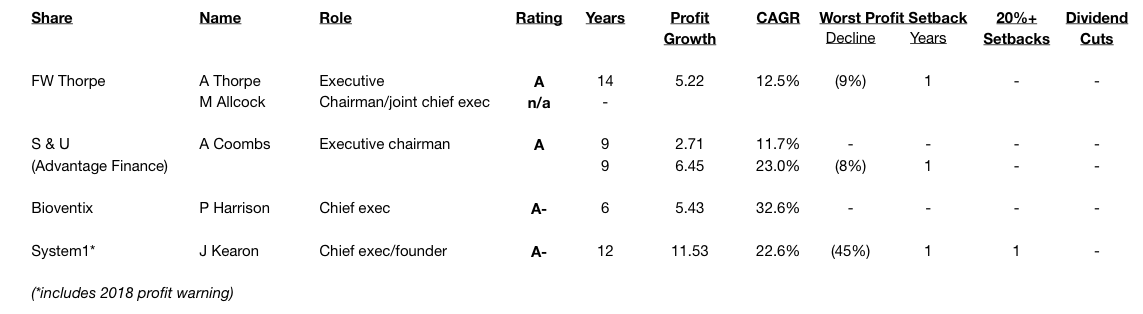

The A-rated all-stars

Let’s begin with the two A+ all-stars of the study.

Being property companies, Daejan and Mountview were assessed on their asset growth rather than profit growth:

(Click image to enlarge)

Benzion Freshwater and Duncan Sinclair have been in charge of their respective companies for 25-plus years.

During the last 20 years, they’ve advanced their NAVs by more than 6-fold, which equates to compound annual growth rates of about 9%. Such long-time progress without any major setbacks gave these two bosses top marks.

Next up are another four directors who I rate very highly:

(Click image to enlarge)

For FW Thorpe, I’ve assessed long-time leader Andrew Thorpe, as he remains an executive (albeit part-time). I’m hoping some of Mr Thorpe’s ‘A’ rating will rub off on Mike Allcock, who is Mr Thorpe’s newly appointed successor and has been a prominent director since 2003.

S&U is not the easiest firm to evaluate, given it sold one of its two divisions the other year. I’ve therefore assessed Anthony Coombs mostly on the performance of the remaining Advantage Finance operation, which has grown very quickly since he became executive chairman during 2008.

For Peter Harrison at Bioventix, I think a few more years of good progress without setbacks and he will join the ‘A+’ club.

Even though System1 has recently issued a 2018 profit warning, the group will still have advanced operating profit at 20% per annum since John Kearon floated the firm during 2006. I think that longer-term achievement deserves an ‘A-’ grade.

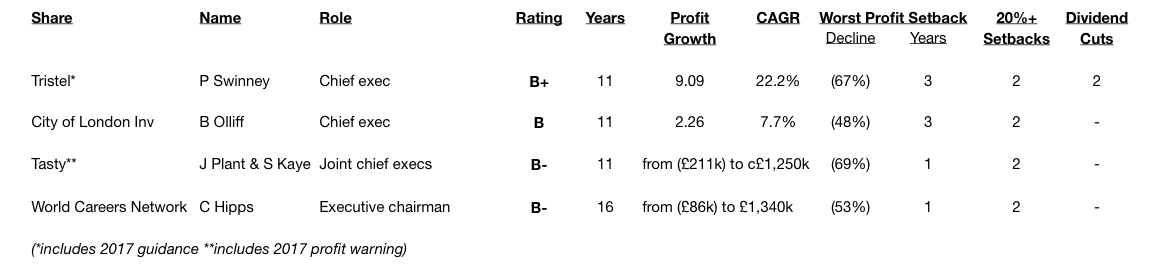

The B-rated bosses

This next group consists of four bosses that, for one reason or another, just did not make the top tier:

(Click image to enlarge)

I could not award an ‘A’ grade to Paul Swinney of Tristel because three years of his tenure witnessed a 67% profit slump and two dividend cuts. However, that grade may well become an ‘A’ if Mr Swinney extends the overall 20% growth rate he has already overseen.

I must admit Barry Olliff at City of London Investment was not the easiest to assess. Long-time profit growth of 8% a year has been acceptable, but progress has been far from smooth. Still, I think Mr Olliff’s 11-year stewardship deserves some merit.

My ‘B’ verdicts for Jonny Plant and Sam Kaye at Tasty, and Charles Hipps at World Careers Network, were influenced by both companies having transformed from loss-makers into profit-makers.

I also considered the fact that both of the groups’ earnings have been far higher in the past.

Indeed, I think these company leaders could have managed ‘A’ grades had I performed this review two years ago and before various setback occurred.

‘Could do better’ and a ‘see me’

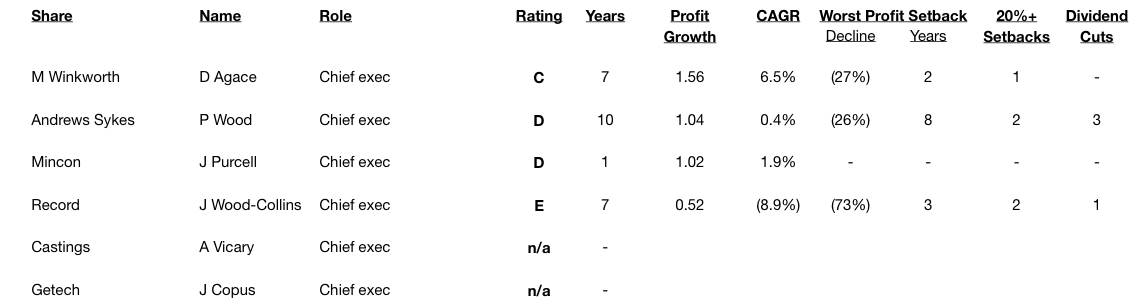

This fourth group contains the remaining six bosses:

(Click image to enlarge)

In retrospect, I may have been a little harsh on Dominic Agace of Winkworth. I gave him a ‘C’ because his tenure at the top is not as long as some of the others, while profit at his firm remains quite low at £1.3m. I reckon he will enjoy a rating upgrade should earnings advance in due course.

I feel a bit sorry for Paul Woods of Andrews Sykes. He took charge of the hire group during 2006 and had to suffer a few lean years after the banking crash. Furthermore, the company’s 87% owner — and his haphazard demand for dividends — has not helped matters.

Still, running a business for 10 years and watching profit fall by a quarter over 8 years deserves a ‘D’. Recent results, however, do show Andrews Sykes making good progress.

Meanwhile, I awarded Joseph Purcell of Mincon only a ‘D’ because of his short tenure in the top job.

However, it was not difficult to mark James Wood-Collins with an ‘E’. He’s the only boss in my review to have stewarded an overall profit downturn during his leadership.

Similar to Andrews Sykes, a bit of bad timing could be involved here. Mr Wood-Collins joined the currency manager in the midst of a client exodus following the banking crash.

Nevertheless, operating profit being reduced by almost 50% over seven years is hardly an executive achievement to boast about.

I sadly could not assess Adam Vicary of Castings and Jonathan Copus of Getech as neither executive has had their first year of leadership captured within any accounts.

Will any of this make a difference to my future returns?

As I mentioned earlier, this was not a straightforward exercise.

I think my A-grades for the top six bosses are reasonably justified, but plenty of judgement was certainly needed at the ten other shares.

In particular, some ratings were influenced by previous, protracted setbacks that were caused by events outside of management’s control. Other grades were influenced by current setbacks that may only cast a temporary shadow.

No doubt some of you will disagree with a few my verdicts. In fact, you could also ask why I am holding companies with D-, E- or even N/A-grade management.

Well, I suppose it could be a combination of:

* the shares were bought originally when the management ratings were higher;

* there’s evidence of the boss demonstrating talent before taking up the top job;

* perhaps the investment has other attractions that offset the lack of an A-rated boss, and/or;

* the company has already suffered difficulties and there’s now every chance a new leader can turn things around.

Anyway, the only conclusion I can really make from this study is that my portfolio is not full of proven executive all-stars. I will just have to wait and see whether any of this makes a difference to my future returns.

Within a future Blog post, I will endeavour to rank the accounts (see point 1) of my 16 holdings. I trust that exercise will be somewhat easier!

Until next time, I wish you happy and profitable investing!

Maynard Paton

(Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, Castings, City of London Investment, Daejan, Getech, Mincon, Mountview Estates, Record, S&U, System1, Tasty, FW Thorpe, Tristel, M Winkworth and World Careers Network.

Thanks for posting. I don’t own any of the shares you mention but enjoy your blog. A couple of your holdings are on my watch list and another couple I need to read up on

Thanks Christian.

Maynard,

I continue to enjoy your Blog, great update and well done on your 14% return so far this year.

I see you have made a significant top up in Tasty, that’s brave!

I’m intrigued by your comment re a lot of your time is absorbed outside of investing? I thought you had given up your day job, am I correct?

regards

David

Hello David

Thanks for the message. Yes, the TAST top-up may seem bold, but I’m hopeful of decent upside from a turnaround. Although the turning may take some time of course!

Don’t worry, I have still given up on the day job to concentrate on investing — the matters distracting me concerned a family bereavement in Q2 and an illness in Q3. I am ok now though.

Maynard

Sorry to hear that Maynard and glad you’re ok! I lost my Mother unexpectedly recently so know how bereavement feels.

Your track record with investing has produced fantastic results looking at your past 6 years stats….very well done. I’m doing ok but certainly can’t give up the day job which would be nice!

Lets hope Tasty has its turnaround soon

David

what was your compound annual growth rate when at the motley fool ?

And what sort of return do you hope to make long term on this portfolio.

cheers

jon

Hello jon

Thanks for the comment.

Difficult to say for the Motley Fool, assuming you are referring to the performance of the paid-for share-tipping services I wrote for (and even the free Qualiport portfolio I managed before). All the data has sadly been lost in time — or perhaps ranks very low on a Google search.

For my personal portfolio, again difficult to give an accurate figure during that 15 years. My Sipp has achieved an 18% CAGR since I opened it in 2001, but that performance should be put into context — the early sums were relatively small and for a lot of the time the SIPP held only one or two stocks. With my ISAs, difficult to give a figure due to various withdrawals and additions… but I have done ok over time and have been able to become a full-time investor.

For my current portfolio, I just hope to beat the FTSE 100 over time. If I can earn double-digit returns, that would be welcome.

Maynard