26 September 2017

By Maynard Paton

Update on S & U (SUS)

Event: Interim results for the six months to 31 July 2017 published 26 September 2017.

Summary: These results displayed further “steady and sustainable” growth from the used-car loan firm. Although the seasoned executives remain optimistic about the group’s prospects and the wider economy, margins have dipped once again as the impairment charge representing potential bad loans continues to rise. Still, the 11-12x multiple appears modest given the company’s growth rate and there is a near-5% income, too. I continue to hold.

Price: 2,000p

Shares in issue: 11,978,709

Market capitalisation: £240m

Click here to read all my SUS posts

Results:

My thoughts:

* On course for the 18th consecutive year of record results

A trading update last month had already hinted these first-half figures would be quite respectable.

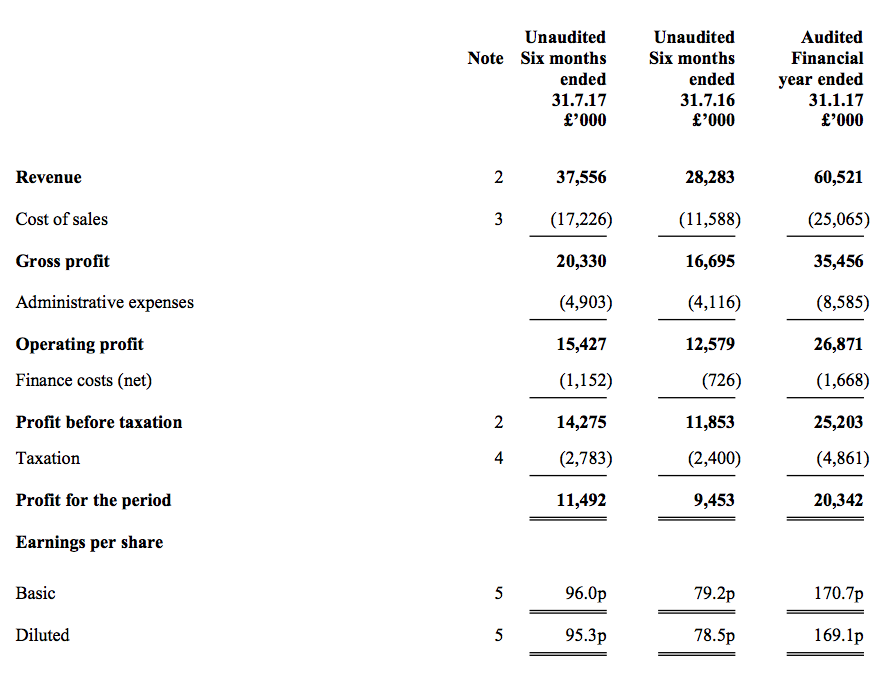

The H1 statement showed revenue up 33% and operating profit up 23%, and trumpeted the fact that SUS had already enjoyed 17 consecutive years of increasing profits from its Advantage motor-finance division. An 18th year of growth now looks very likely.

Long-time boss Anthony Coombs said the overall performance showed “steady and sustainable growth, which investors should recognise as our trademark”.

Mr Coombs also claimed the group’s “excellent and continuously improving standards of speed and customer service” had helped generate a further 12,542 car-loan agreements during the half.

Emphasising that SUS is somewhat picky with its clientele, that 12,542 figure represents only 3% of the total 440,000 applicants.

* The growing prospect of greater bad loans

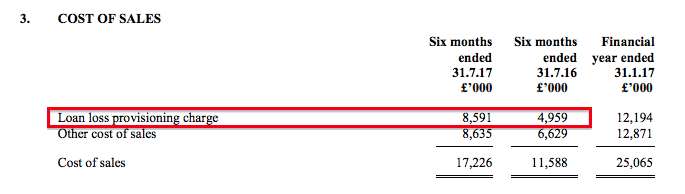

A prominent feature of March’s annual results was the impairment figure leaping 60%.

My verdict at the time was that the favourable lending conditions of the preceding few years may now have turned — and I believe these results underline the growing prospect of greater bad loans.

Indeed, the impairment charge for this H1 surged 73%:

Published originally in my March write-up, the following table shows how the impairment charge (loan provision) for 2017 compares to the previous four years:

| Year to 31 January | 2013* | 2014* | 2015* | 2016* | 2017** |

| Loan provision (£k) | 5,291 | 5,087 | 5,863 | 7,611 | 12,194 |

| Revenue (£k) | 20,801 | 26,147 | 36,102 | 45,182 | 60,521 |

| Average net customer receivables (£k) | 47,377 | 62,734 | 89,678 | 125,764 | 169,335 |

| Loan provision/Revenue (%) | 25.4 | 19.5 | 16.2 | 16.8 | 20.1 |

| Loan provision/Average net customer receivables (%) | 11.2 | 8.1 | 6.5 | 6.1 | 7.2 |

This next table shows how the loan provision as a proportion of revenue and as a proportion of net receivables (customer loans) increased notably during H2 of 2017, and again during this H1 2018:

| FY 2016 | H1 2017 | H2 2017 | H1 2018 | |||

| Revenue (£k) | 45,182 | 28,283 | 32,238 | 37,556 | ||

| Operating profit (£k) | 21,251 | 12,579 | 14,292 | 15,427 | ||

| Loan provision (£k) | 7,611 | 4,959 | 7,235 | 8,591 | ||

| Average net customer receivables (£k) | 125,764 | 159,528 | 183,722 | 210,168 | ||

| Loan provision/Revenue (%) | 16.8 | 17.5 | 22.4 | 22.9 | ||

| Loan provision/Average net customer receivables (%) | 6.1 | 6.2 | 7.9 | 8.2 |

The trend does not look too encouraging, but the veteran chairman appears quite relaxed. Mr Coombs declared (my bold):

“Doubtless, this [first-half progress] also reflects the robust state of the labour market, with unemployment at 4.4% the lowest for 42 years. In addition, according to the Recruitment and Employment Confederation, job vacancies are at a two year high, which appears to be exerting a gradual and beneficial influence on recent real wage trends. We therefore remain confident of future demand in our sector.”

[…]

“Although a return, for competition reasons, to Advantage’s traditional customer mix has seen an increase in impairment to revenue, risk adjusted yield has been protected by good interest rates.

Indeed, current levels of impairment are significantly below those experienced just five years ago following the financial crisis, when the business continued to increase profits and maintained very good returns on capital employed.

The rigour and accuracy of our under-writing has always been at the heart of Advantage’s success.”

Impairments ran beyond 30% of revenue during 2012 and the preceding years, so there is still some way to go before those levels are reached.

(I should add that my reading of SUS’s 2017 annual report (point 4 here) indicated the firm could be acting very conservatively with its recent bad-loan calculations.)

* Addressing concerns about the PCP ‘bubble’

This H1 statement made further references to personal contract plans (PCPs) used within the motor trade.

Articles such as this have suggested PCPs are fuelling a credit ‘bubble’ in the car market.

SUS reiterated it has never sold such plans:

“Our relations with the regulatory authorities continue to be good.

Whilst the Financial Conduct Authority expects to scope its report on the motor finance market by next year, we expect this to concentrate upon the recent significant expansion in the personal contract plan (PCP) market, in which Advantage has never been involved.

We also concur with the recent conclusion by the Guardian newspaper which said: “Figures suggesting the used car market is cooling could alleviate concerns over [any] credit bubble in motor finance.” – The Guardian 16 August 2017.”

Last month the group claimed it would escape any fall-out from a PCP downturn:

“Advantage is not involved in the PCP market which has recently come under public scrutiny. Advantage’s average loan size is just £6,200 so should changes in the PCP market have a knock-on effect upon car residual values generally, this would have only a marginal effect upon S&U’s business.”

* Margin, return on equity and debt

There has been no major change to the general shape of SUS’s accounts.

The higher impairment charge meant SUS’s operating margin dropped to 41% from 44% during 2017.

Although a 41% margin remains very high compared to that of most other businesses, a high level of profit is required to generate an acceptable return on the equity that supports the business.

For this H1 2018 and the preceding H2 2017, I reckon SUS earned a reasonable 16% (£22m) return on the average £137m of equity employed throughout the twelve months. (I calculated 15% back in March)

However, the 16% return was assisted by the use of significant debt — net borrowings increased from £49m to £81m during the six months — and adjusting my sums for the loans and associated interest reduces the result to a modest 12%.

Valuation

Net customer receivables (customer loans) now stand at £227m, from which I estimate SUS can produce near-term revenue of £81m.

Assuming the impairment provision stays at 23% of revenue, and other costs remain at about 35%, I arrive at a potential £34m operating profit. Taxed at SUS’s expected 19.5% tax rate, I calculate possible operating earnings to be almost £28m or 230p per share.

Adding net debt of £81m to the £240m market cap (at 2,000p per share) gives an enterprise value (EV) of £321m, or 2,673p per share.

The possible P/E based on my EV and earnings guess is therefore 2,673p/230 = 11.6.

That rating seems quite modest given SUS’s recent growth rate. I can only assume the stock market is worried about a combination of higher impairments, PCPs and wider economic issues.

Meanwhile, the interim dividend was raised 4p to 28p per share, and the rolling 95p per share payout presently delivers a useful 4.8% income.

Maynard Paton

Disclosure: Maynard owns shares in S & U.

S & U (SUS)

Trading Statement

This did not read too badly. Here is the full text:

—————————————————————————————————————————-

S&U plc, the specialist hire purchase motor finance and property bridging lender, announces its trading update for the period from 1st August to 6th December 2017 and is pleased to continue trading in line with expectations.

Motor Finance

Advantage Finance, our specialist motor finance provider based in Grimsby continues its excellent progress. Despite recent downgraded forecasts for the UK economy, Advantage applications for finance have been very good. This has enabled Advantage both to maintain this year’s rate of transactions growth and to revise, refine and further strengthen its under-writing model.

As a result, live customer numbers have grown to 53,000 from 49,000 at the half year; this means that net customer receivables now stand at over £240m for the first time, compared to nearly £227m in July.

Monthly collections and overall credit quality remain good. Whilst rolling 12 months impairment to revenue has increased slightly to 23.4%, this continues to be primarily due to overall portfolio product mix.

Whilst the above underwriting refinements have seen a slight reduction in loan approvals, appropriate in a more uncertain economic climate, the introduction of Advantage’s new e-signature Dealfo system has been well received by both customers and brokers and has led to an improvement in the approval-transaction rate.

Property Bridging Finance

Our pilot bridging operation, Aspen Finance, has made significant progress and increased its loan book to £9m from £2m in July. Margins and LTV are within budget and very early repayment experience is good.

Aspen’s growing reputation for efficient, consistent and prompt service to the broking community, augers well for a successful trial period concluding in H2 2018.

Funding

Having obtained further funding of £20m during the period, the Group now has total available committed facilities of £115m, sufficient to accommodate current growth at both Advantage and Aspen. Further facilities will be arranged as required.

Commenting on the Group’s performance and outlook, Anthony Coombs, S&U Chairman, said:

“Whatever the current political uncertainty, particularly over Brexit, and despite a forecast slowing economy, demand for S&U’s products remains very robust. Our selective lending and continuous refinement of our under-writing underpin our debt quality and produce steady sustainable growth.

“I am pleased to see this seemingly becoming more widely recognised within the investing community; we will continue our high standards of responsible lending and the excellent performance which results from this.”

——————————————————————————————————————————–

There’s not enough information here to rework my valuations sums, but I do see the bad-debt provision is now 23.4%. My Blog post above noted the figure for H2 2017 was 22.4% and for H1 2018 was 22.9%. So the ratio is still creeping higher, although the business is taking on more customers so total profit ought to be moving higher as well.

Maynard

S & U (SUS)

Year-End Trading Statement

Another S & U statement that does not read too badly. Here is the full text:

—————————————————————————————————————-

S&U plc, the motor finance and property bridging lender, today issues a trading update for the period from its trading statement of 7 December 2017 to the Group’s year-end on 31 January 2018.

Group trading remains strong and in line with expectations; demand for Advantage’s motor finance has seen a record 24,500 transactions in the year, defying recent reports of a slowing car market. Aspen Bridging has lent over £10m and early repayments are in line with expectations. S&U’s final results will be announced on 27 March 2018.

Advantage Finance

Our record-breaking motor finance business continues to do precisely that. Customer numbers have reached 54,000 against 43,000 a year ago and new transactions exceeded last year by 22% at 24,500, reflecting strong demand for our products. We continue to further refine our underwriting, underpinning future debt quality and resulting in even tighter approval rates.

Whilst this has led to improvements in initial customer quality scores, Advantage’s new industry leading Dealflo system, fully rolled out in the period, has led to a significant improvement in transaction-to-approval rates. We expect this in turn to lead to further growth in high quality business, margin improvement and a gradual reversal in the recent, and historically small, uptick in impairment-to-revenue.

Furthermore, early signs are that the recent fall in new car sales is likely to buttress used car values, whilst the economic advantages of diesel vehicles remain widely appreciated in Advantage’s non-prime sector of the market.

Aspen Bridging

Aspen, our Solihull based, property bridging pilot continues to justify its launch last year. Over £10m of loans have now been issued, many into the buoyant residential refurbishment market for starter family housing. Costs have been controlled and lending margins and LTVs maintained to budget. We have already seen a number of repayments come through and we are increasingly confident in the long-term viability and prospects for this business.

IFRS9

From 1 February 2018 and for our accounts for the forthcoming year ending 31 January 2019, IFRS9 “Financial Instruments” replaces IAS 39 for the way we value and measure our financial assets. In particular, IFRS9 requires the impairment of our customer receivables to be recognised through an expected loss model rather than IAS 39’s emphasis on historical impairment triggers. Good progress has been made on the new methodology and its effect on our accounting policies and receivable values. For illustration, the estimated impact of IFRS9 would have been a reduction of reported receivables by between 0.5% and 2.5% as at January 2017. As this is an accounting adjustment, there is no impact on either the Group’s cash flows or on the underlying profitability of its loans.

Treasury

A healthy market and our confidence in lending quality has seen combined investment in Advantage and Aspen this year reach a record £53m. As a result, Group borrowings are now at £105m and, although this rate of investment is expected to slow next year, we expect further funding facilities to be concluded shortly which will bring total committed facilities to £135m. This will provide sensible headroom for growth whilst maintaining gearing at S&U’s historically conservative levels.

Dividend

The Group’s profit performance and prospects have led the Board to approve a second interim dividend this year of 32p per ordinary share (2016: 28p). This will be payable on 16 March 2018 to shareholders on the share register on 23 February 2018. This means that our first two dividends this year, including the 28p per share paid in November, will total 60p against 52p a year ago, 43p in 2016 and 36p three years ago. These measures are consistent with our aim of returning to twice covered dividends in the near future.

Commenting on the Group trading and outlook, Anthony Coombs, Chairman of S&U said:

“Whilst the political and economic uncertainties inherent in both the Brexit negotiations and a slowing economy remain, S&U continues to demonstrate its historic ability to produce excellent results and strong, sustainable growth. We are confident that will continue.”

Our preliminary results for the year ended 31 January 2018 will be announced on 27 March 2018.

—————————————————————————————————————-

Customer and transaction numbers gained 20%-plus during the year.

My sums indicate:

* the c11,000 new customers were split c6,000/c5,000, and;

* the 24,500 new agreements were split c12,500/c12,000…

…during H1/H2.

The slightly stronger H1 was also reflected during the previous 2017 financial year, so I don’t feel there’s any H2 deterioration to worry about.

Debt was £49m at the start of the financial year, and advanced £32m during H1 and £24m during H2 to £105m. Although additional borrowings are necessary to fund the loans to new customers, I am pleased H2 did not demand as much extra debt as H1.

Regarding extra debt, I am not sure whether the phrase “this rate of investment is expected to slow next year” alludes to customer growth slowing, or simply the business not needing as much extra debt to maintain the present rate of additional customers.

This paragraph is encouraging:

“Whilst this has led to improvements in initial customer quality scores, Advantage’s new industry leading Dealflo system, fully rolled out in the period, has led to a significant improvement in transaction-to-approval rates. We expect this in turn to lead to further growth in high quality business, margin improvement and a gradual reversal in the recent, and historically small, uptick in impairment-to-revenue.”

During 2017, S & U received c750,000 applications of which c240,000 were provisionally approved and c20,000 transacted. So I think I am right in saying the transaction-to-approval rate was 20/240 = 8.3%.

Anyway, I am pleased the new system will apparently lead to a “gradual reversal” of the unfavourable impairment trend seen of late (see my Blog post above).

The dividend news now means the trailing payout is running at 99p per share, up 16% on the 85p per share seen this time last year.

I will update my valuation figures when the full-year results are published in March.

Maynard