28 September 2017

By Maynard Paton

Update on Andrews Sykes (ASY).

Event: Interim results for the six months to 30 June 2017 published 28 September 2017

Summary: I was very satisfied with ASY’s first-half progress. The specialist hire group reported positive performances both within the UK and overseas and could now be on course to deliver its best-ever annual results. A 20%-plus operating margin and substantial net cash remain key bookkeeping features, while management hints of an encouraging second half have kept the share price buoyant. I continue to hold.

Price: 610p

Shares in issue: 42,262,082

Market capitalisation: £258m

Click here for all my ASY posts.

Results:

My thoughts:

* ASY could be heading for its most profitable year ever

When I studied ASY’s annual results in May, I wrote:

“I hope the momentum from the buoyant H2 will extend throughout 2017.”

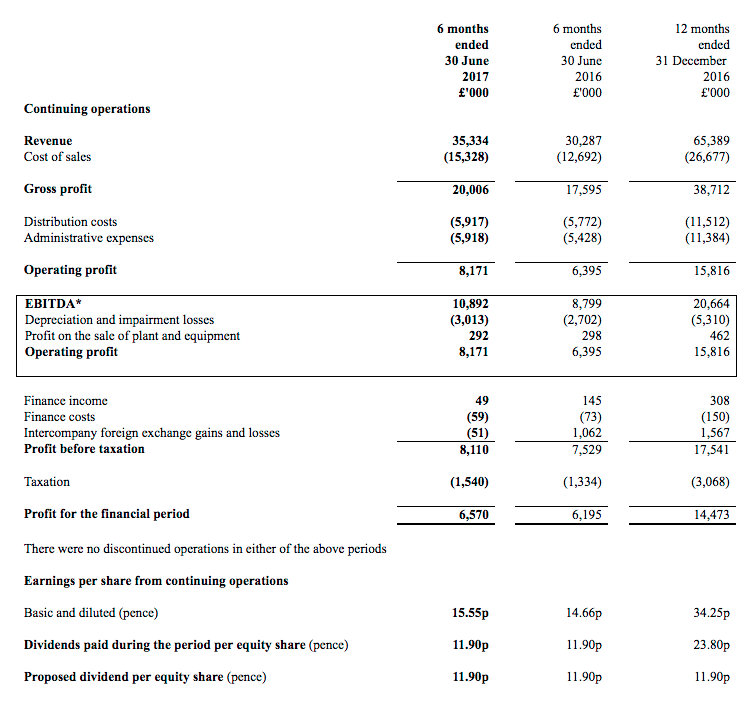

I’m very pleased that has been the case, with this first-half statement revealing revenue up 17% to £35.3m and operating profit up 28% to £8.2m.

While these H1 figures were not a clear record for the hire firm — profit during H1 2008 was £8.8m — the general performance seemed very encouraging.

In fact, a repeat of last year’s H2 effort could mean 2017 becomes the group’s most profitable year ever.

What’s notable about ASY’s progress is that it has not been helped by acquisitions (my bold):

“We have continued our policy of pursuing organic growth within our market sectors and start up costs of the new businesses discussed in previous Strategic Reports continue to be expensed as incurred.”

The mention about expensing start-up costs is interesting.

I remarked in my review of ASY’s 2016 annual report (see point 1) that the fledgling operations in Europe were now mostly profitable.

Revenue within Europe surged 48% during H1 and I assume the overseas progress — with start-up costs now being covered — helped to underpin the 28% profit leap.

Sales from Europe now represent 20% of ASY’s top line.

However, I note there was no mention of the effect of the weaker GBP on ASY’s international performance.

Meanwhile, revenue from the UK gained a useful 12%.

Apparently, “the winter months created some good opportunities for our heating and boiler hire products” while “demand for our air conditioning products… increased mainly due to a warmer-than-expected start to the summer in the month of June.”

It also appears the wetter UK weather during July and August may not have hurt ASY’s business too much:

“Trading in the third quarter to date has continued to be positive.”

* A pension surplus that absorbs an extra £1m a year

These interim figures confirmed ASY remains a high-margin business. I am impressed 23% of first-half revenue was converted into profit — the best H1 conversion since 2010.

Elsewhere in the accounts, net funds ended the six months a few £000k lighter at £17.4m.

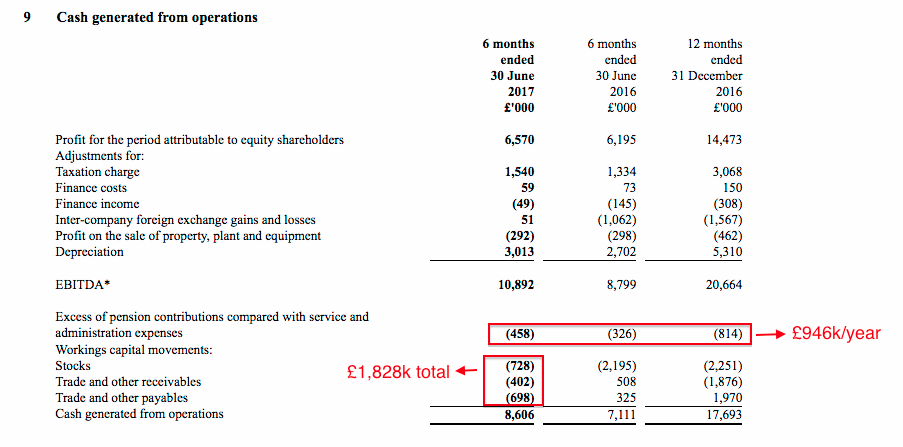

A sizeable £1.8m of the group’s £8m operating profit was absorbed into working-capital movements. I trust the trend of previous years will be followed and much smaller movements will occur during the second half:

One item the cash-flow statement revealed was an extra £458k contribution to the group’s defined-benefit pension fund.

This type of contribution is not charged to the income statement and, in ASY’s case, is not insignificant when the cost now runs at almost £1m a year.

The irony here is that ASY’s balance sheet shows a pension-scheme surplus of £2.6m. I’ve looked at the pension situation in a bit more detail in this Comment below.

Almost all of the left-over cash flow was distributed as an 11.9p per share/£5m dividend. These results promised an identical payout during the second half.

Valuation

ASY’s operating profit presently runs at £17.6m a year and translates into earnings of £14.3m, or 33.7p per share, using the 19% tax charge applied in these results.

Subtract the £17.4m net cash position from the £258m market cap (at 610p) and the enterprise value comes to about £241m or 569p per share. Then divide that 569p by my 33.7p per share earnings guess and I arrive at an underlying P/E of approximately 17.

Clearly the stock market believes ASY’s growth can now continue at a decent pace and that the ‘lost’ decade of 2006 to 2015 — when revenue and profit remained broadly stagnant — will gradually fade into a distant memory.

With hindsight, the time to have bought more of these shares was exactly twelve months ago, when the signs of improved trading were becoming clear and the underlying P/E was only 11. The price has since climbed 75%.

Meanwhile, the trailing yield is 3.9% and my 33.7p per share earnings calculation covers the trailing 23.8p per share payout 1.4 times.

Maynard Paton

Disclosure: Maynard owns shares in Andrews Sykes.

Andrews Sykes (ASY)

Pension surplus and extra contributions

A follow-up to point 6 of my review of ASY’s 2016 annual report.

This extract of the first-half results details the movements of the pension scheme’s assets:

At present, the scheme’s assets of £44,403k are required to pay annual member benefits of £1,624k, which is equivalent to a 3.7% required return. That return is quite high relative to other schemes (with major deficits) I’ve looked at.

If you adjust for the contributions of £1,080k less scheme admin costs of £134k, the required return is (£1,624k – (£1,080k – £134k))/£44,403k) = 1.5%. That is a much more comfortable required return and in line with other pension schemes.

So it seems the extra contributions are required to ensure the benefits can be paid if the value of the assets are hit in any downturn, which would leave the required rate of return from the assets to pay the yearly benefits far more demanding.

So…why does the balance sheet show a pension surplus? Well, the scheme’s stated liabilities come to £41.8m. I guess the key point is how those liabilities are calculated — but all that involves actuarial complex sums that are not shown in the accounts, and beyond the likes of me

These days I tend to ignore the started pension liability calculation and just compare the assets in the plan with the benefits that need to be paid and the contributions being made. Essentially, can the scheme’s assets pay the benefits with a very modest yearly return?

Maynard