16 October 2017

By Maynard Paton

Update on Bioventix (BVXP).

Event: Preliminary results for the year to 30 June 2017 published 16 October 2017

Summary: The antibody specialist delivered another outstanding set of results, as astonishing margins, robust cash production and magnificent equity returns once again underlined the group’s wonderful economics. However, matters were tempered somewhat by management remarks about the immediate revenue potential of a new product. It could mean progress during 2018 won’t be very impressive, which may leave the current 29x multiple rather exposed. I’m hoping things work out for the best, and continue to hold.

Price: 2,700p

Shares in issue: 5,138,674

Market capitalisation: £139m

Click here to read all my BVXP posts

Results:

My thoughts:

* Record results do not have a “single explanation”

Bumper interim figures followed by an upbeat trading statement had already laid the ground for an outstanding annual performance.

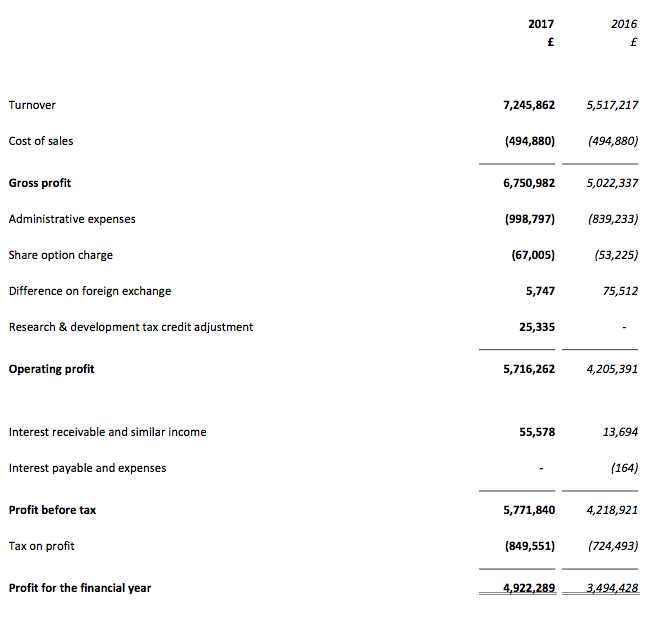

In the event, the results RNS showed revenue up 31% and operating profit (before foreign-exchange gains and tax credits) up 38%. The figures were BVXP’s best ever, and extended the group’s run of substantial annual growth to seven years:

| Year to 30 June | 2013 | 2014 | 2015 | 2016 | 2017 |

| Revenue (£k) | 2,706 | 3,535 | 4,333 | 5,517 | 7,246 |

| Operating profit (£k) | 1,809 | 2,372 | 3,098 | 4,205 | 5,691 |

| Other items (£k) | - | (169) | - | - | 25 |

| Finance income (£k) | 12 | 28 | 8 | 14 | 56 |

| Pre-tax profit (£k) | 1,821 | 2,231 | 3,106 | 4,219 | 5,772 |

| Earnings per share (p) | 30.3 | 36.1 | 50.7 | 69.2 | 96.4 |

| Dividend per share (p) | 14.5 | 24.0 | 32.6 | 42.5 | 51 |

| Special dividend per share (p) | - | - | - | 20.0 | 40.0 |

The full-year dividend also marched higher — up 20% — with the second interim payout up 19% to 31p per share. A bonus was the declaration of a special dividend of 40p per share — equivalent to more than £2m.

As promised within September’s trading update, BVXP did comment on its revenue “in more detail”.

Sales of the firm’s vitamin D antibody gained 24% to £2.75m, while the aggregate turnover of five other antibodies climbed around 30% to £2.1m.

BVXP chief exec Peter Harrison couldn’t really explain the group’s positive performance:

“Our expectation was that, whilst test volumes are increasing globally, price pressure (i.e. $/test prices achieved) would balance the increase in volume leading to a relatively flat total market in US Dollars. This [customer] feedback set our expectations for royalties received after 30 June 2017 (but relating to the reporting period). Actual royalties received were in excess of these expectations.”

…

“This healthy increase in these [five] core antibodies that are sold to a number of customers in many countries does not have a single explanation over and above the 5-10% increase in the global diagnostics industry that is reported by third party analysts.”

However, one source that did help the group was currency movements:

“Our revenues continue to be dominated by US dollars and Euros. We have commented in recent reports on the effect of post Brexit referendum exchange rates on our revenues in the absence of any hedging mechanisms.”

I calculate BVXP’s GBP-denominated revenue may have benefitted by between 15% and 20% during the year. So perhaps the company’s underlying growth rate was between 10% and 15%.

(EDIT 18 Oct: I have revised my sums and now reckon the underlying growth rate was about 20%. Details in the Comment below.)

I should add that BVXP’s second-half performance showcased very satisfactory growth:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Revenue (£k) | 2,371 | 3,146 | 5,517 | 3,125 | 4,121 | 7,246 | |

| Operating profit (£k) | 1,666 | 2,538 | 4,205 | 2,461 | 3,230 | 5,691 |

* Introducing the “education period” for troponin

Today’s RNS introduced some caution about the recent launch of BVXP’s tropronin antibody.

To recap, this particular product is supplied to Siemens and BVXP has said in the past that the antibody has the potential for “significant revenue”. Indeed, broker notes have suggested annual product sales could eventually reach £2m or more.

Anyway, Mr Harrison now admits the new troponin product will experience an “education period” before sales can really take off (my bold):

“The rate at which this new test will be adopted by Siemens customers in hospitals in the EU, Asia and elsewhere outside the US is unfortunately not something of which we have detailed knowledge.

Whilst it is clear that a quicker test will be of benefit to patients, clinicians and hospital budget holders, it is also clear that there is likely to be an education period during which clinicians become comfortable with a significant change in diagnostic practices that can result in non MI (i.e. patients not having a heart attack) being released from A&E much earlier.”

We will develop a better understanding of this matter during 2018.

While the mooted delay does not sound too worrying, there is another factor at play here.

You see, revenue from the troponin product has been expected to offset the disappearing revenue from another antibody….

* 2018 revenue gap rises to £1m

Today’s results heralded a change of tone with regard to the replacement of revenue from a product named NT proBNP:

Mr Harrison stated (my bold):

“The revenues resulting from the success of the Siemens troponin project will be important in replacing approximately £1 million of NT proBNP sales that will be lost from the 2017/18 accounts due to the termination of a specific technology license.”

The term “will be important’ does not sound as confident as past statements:

Back in March BVXP declared (my bold):

“Significant troponin revenues during the financial year 2017/2018 are expected to offset the loss of revenues of around £800,000 from another product due to the expiry of the relevant agreement.”

And this time last year BVXP said (my bold):

“Troponin remains an important product for Bioventix’s future performance as we expect to commence significant sales during the financial year 2017/2018 and we anticipate that this revenue will offset revenues of £0.7 million – £0.8 million from another product which will terminate during this period.”

What with the aforementioned “education period” for troponin and the revenue gap to fill rising from £0.8m to £1m, I get the impression 2018 may actually see revenue reverse, with perhaps a notable effect on profit.

Still, all is not lost just yet. Income from the company’s other antibodies continues to grow, while further progress is being made with deliveries to the group’s fledgling Chinese market.

* No more than £5m needed in the bank

BVXP’s financials remain extraordinary.

In particular, the group’s operating margin has risen further into the stratosphere, while the exemplary return on average equity ratios continue to suggest the business runs on thin air:

| Year to 30 June | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating margin (%) | 66.9 | 67.1 | 71.5 | 76.2 | 78.5 |

| Return on average equity* (%) | 109.5 | 103.6 | 117.9 | 132.4 | 144.7 |

(*adjusted for net cash)

I have no concerns with BVXP’s cash flow:

| Year to 30 June | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating profit (£k) | 1,809 | 2,372 | 3,098 | 4,205 | 5,691 |

| Depreciation (£k) | 24 | 21 | 46 | 42 | 39 |

| Cash capital expenditure (£k) | (21) | (2) | (114) | (21) | (22) |

| Working-capital movement (£k) | (513) | (546) | (279) | (581) | (570) |

| Net cash (£k) | 2,586 | 3,351 | 4,131 | 5,380 | 6,167 |

I calculate total capital expenditure has represented a microscopic 1.2% of BVXP’s aggregate operating profit during the last five years — and the £22k spent during 2017 was ludicrously tiny.

Meanwhile, BVXP’s working-capital movements are somewhat larger — although absorbing a total £2.5m during the last five years does not ring alarm bells for me when operating profit has jumped from £1.8m to £5.7m throughout the same period.

Most of BVXP’s surplus cash flow was distributed as dividends — £3.4m or 66p per share — during the year. The £0.8m left over lifted the bank balance to £6.2m or 120p per share.

Mr Harrison said the business does not require more than £5m in the bank:

“Our current view is that a cash balance of approximately £5 million is sufficient to facilitate operational and strategic agility with respect to possible corporate or technological opportunities that could arise in the foreseeable future.”

With few demands on cash flow, I dare say this year’s £2m/40p per share special dividend will not be the company’s last.

The balance sheet continues to carry no debt and no pension obligations.

Valuation

Looking ahead, Mr Harrison said (my bold):

“For the financial year 2017/18, our challenge will be to make up for the approximately £1 million of lost sales mentioned above with revenues from the newly launched Siemens troponin project and modest growth from additional vitamin D antibody sales and royalties.”

He does like to use the word “modest”.

This time last year, Mr Harrison said (my bold):

“Furthermore, we remain optimistic that further modest growth next year will come from additional vitamin D antibody sales and royalties.”

And the year before that he said (my bold):

“Furthermore, we remain optimistic that further modest growth in the next two years will come from additional vitamin D antibody sales and royalties.”

Both times, the “modest” growth turned into 20%-plus revenue and profit advances.

I just hope he is trying to under-promise and over-deliver once again.

Anyway, BVXP’s operating profit before foreign-exchange differences and tax credits was £5,685k for 2017, which after standard 19% tax gives earnings of about £4.6m or approximately 90p per share.

Then subtracting the 120p per share cash position from the 2,700p share price, my underlying trailing P/E comes to 2,580p/90p = 29.

That multiple certainly looks racy, especially given the apparent caution expressed about the replacement of the disappearing NT proBNP income.

But the wonderful economics of this business — additional revenue all seems to fall to the bottom line while only 13 people are needed to run the operation — do make BVXP a very special company.

For now at least, I still have my fingers crossed that BVXP can continue to extract further growth from its vitamin D product and those five other antibodies… and that the recent Siemens troponin launch does not remain in an “education period” for too long.

Maynard Paton

Disclosure: Maynard owns shares in Bioventix.

A good review. Thanks Maynard

Bioventix (BVXP)

Further thoughts on currency movements

Prompted by a reader, I have had some further thoughts on the effect of currency movements on BVXP’s 2017 progress.

This is what the company said in its FY 2016 results (my bold):

“Approximately three quarters of Bioventix sales are generated from customer royalties. These are based on our customers’ global sales which are then factored by a royalty percentage and then sent to Bioventix around 2 months after the end of each half year. In the first half of 2016, this mechanism resulted in $ based and Euro based royalties being converted into sterling around August at post Brexit exchange rates of approximately 1.3$/£ and 1.2Euro/£. As no hedging mechanisms are employed, this provided an additional uplift in reported sterling revenues compared to previous periods.”

This is important, as it means BVXP’s second-half performance may not have been influenced significantly by currency movements.

Therefore the underlying progress seen during H2 (and the year as a whole) was much better than I had suggested in my Blog post above.

Let’s look at some figures.

According to x-rates.com:

Average GBP:USD Aug 16 was 1.31

Average GBP:USD Aug 17 was 1.30

Average GBP:EUR Aug 16 was 1.17

Average GBP:EUR Aug 17 was 1.10

For FY 2016, 32% of revenue was from Europe (EUR) and 63% was from the rest of the world (which I assume all pay in USD).

So a little bit of maths makes me think currency movements gave BVXP a currency boost of somewhere between 0% and 5% for H2. For H1, BVXP cited (my bold):

“As mentioned in our last report in October 2016, Bioventix revenues arriving in global currencies converted at post-Brexit referendum exchange rates give an uplift in reported sterling revenues of 15-20% as no hedging mechanisms are employed.”

So I reckon FY 2017 saw currency movements gave a c10% revenue benefit, and left 20% delivered on an underlying basis. That is somewhat better than my 10-15% guess in the Blog post above.

What is notable now is that the 31% revenue gain during H2 was mostly underlying, with little currency benefit. So clearly there is some momentum within the business.

And what with the regular nature of blood tests (read the PS at the end of this Comment), I feel a tad more optimistic about the upcoming revenue ‘gap’ with the loss of NT proBNP.

For instance…

If the vitamin D product can grow at 10% for 2018 (vs 24% for 2017), that is extra revenue of £275k, and if the other five core antibodies can grow at 20% for 2018 (vs 31% for 2018), that is extra revenue of £420k.

So that comes to £695k, which leaves £305k to be found to make up the £1m revenue shortfall from the disappearance of NT proBNP.

Could early Troponin sales plus any revenue advances from the R&D contract side of the business make up that £305k? Quite possibly.

Maynard

Bioventix (BVXP)

Publication of 2017 annual report

A simple text-only report. Just the type I like.

As before, these accounts are unusual as they are presented in the ye olde UK GAAP format, which does not provide as much disclosure as the usual IFRS standard.

AIM Rule 19 allows UK companies without subsidiaries (such as BVXP) to present their accounts using UK GAAP. UK businesses that are formed of a parent company plus one or more subsidiary operations have to present group accounts using IFRS.

Here are the points of interest:

1) Turnover segments and geography

A few minor features here:

First, ‘royalty and licence income’ gained 29% while ‘product revenue and R&D income’ gained 39%. The different growth rates are not that worrying, although product/R&D income is based on direct sales/contract work and is perhaps less predictable than the royalty/licence income.

The 2017 results RNS disclosed the Vitamin D antibody enjoyed royalty revenue of £2.75m, the five other core antibodies enjoyed £2.1m and the NT pro BNP product enjoyed £1m. That left £1.4m for ‘other income’.

Sadly I can not exactly match these product revenue figures with the royalty/licence/direct sales/R&D revenue numbers disclosed in the annual report. I may be wrong on this, but perhaps some antibodies earn revenue from both royalties and direct sales.

I see UK revenue dropped 3%, while ‘rest of EU’ and ‘rest of World’ revenue gained 36% and 32% respectively. The UK is clearly a small market to BVXP, and I am pleased there was good consistent growth outside of the domestic market.

2) Employee costs

BVXP’s employee-related ratios remain strong:

The workforce now numbers 16, and each bears a total cost of £50.3k to the group — last year the figure was £47.3k.

Each employee on average generated a superb £453k of revenue for 2017, up from £394k last year and £165k in 2009. Total employee costs represented just 11% of revenue, down from 12% last year and 14%-plus from the years before.

I suppose BVXP’s already stratospheric operating margin could increase even higher should the company be able to grow its revenue further and keep its employee team so small.

3) Director pay

I have previously described BVXP’s lead executive as a ‘thin cat’, so I have no qualms with his total annual payment moving from £130k to £201k:

It is not clear whether the higher pay is due to a pay rise or a notable bonus, but either way, the payment seems great value given the group’s operating profit has advanced from £1.5m to £5.7m during the last five years.

It seems the three non-execs are on about £15k each.

4) Debtors

This is an interesting note:

For most companies, trade debtors is usually the largest figure within the debtors (or receivables) note. But for BVXP, prepayments and accrued income is the largest.

As I understand matters, BVXP carries a lot of accrued income — which reflects revenue earned during the period but where the customer had not yet been invoiced at the balance-sheet date.

(Trade debtors reflect revenue earned during the period where the customer has been invoiced).

This accrued income is related to the company’s collection of royalties. From this extract of the 2016 results narrative:

“Approximately three quarters of Bioventix sales are generated from customer royalties. These are based on our customers’ global sales which are then factored by a royalty percentage and then sent to Bioventix around 2 months after the end of each half year.”

I believe I am right in saying that BVXP’s customers inform BVXP of their global sales after the period end, and BVXP then invoices the customers for the appropriate royalty sum. As such, the revenue to be collected is deemed to be accrued income — i.e. the revenue had not been invoiced at the balance-sheet date.

Anyway, the year-end prepayment and accrued income figure for 2017 is equivalent to 53% of royalty revenue, which compares to 54% for 2016, 54% for 2015 and 52% for 2014. I am pleased the backlog of customer payments is not growing faster than royalty revenue.

Maynard