01 January 2023

By Maynard Paton

Happy 2023! I hope you survived last year’s tough market and continue to find my blog useful.

A summary of my portfolio’s 2022:

- Total return of -23.3% (Q4: +0.2%)*;

- 2 holdings recorded a gain while 9 holdings recorded a loss;

- Returns ranged from up 23%, for Bioventix, to down 67%, for System1;

- One share was topped-up: City of London Investment, and;

- No new shares were purchased and no shares were sold.

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

I publish a portfolio review after every quarter (Q1, Q2 and Q3), and this post recaps my October/November/December activity as well as my 2022 performance.

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, Tasty, FW Thorpe, Tristel and M Winkworth.

Q4 share trades

I increased my City of London Investment position by 50% at 353p including all costs.

The fund manager experienced a rough 2022, with funds under management (FuM) falling 17% between January and June and sliding a further 8% by September. But CLIG’s full-year results delivered a maintained 33p per share dividend that, despite the lower FuM, should still be covered by near-term earnings.

My purchase should provide a 9% yield, and I trust a wider market rebound will eventually deliver healthy double-digit returns assuming the shares can recover to their 550p high of 2021. Net cash and investments at £30m should meanwhile limit any operational trouble. This podcast has more.

Q4 portfolio news

As usual I have kept watch on all of my holdings. The main Q4 developments are summarised below:

- The seventh consecutive annual special dividend from Bioventix.

- My AGM visit to City of London Investment.

- Underlying annual profit up 20% at FW Thorpe.

- 2022 profit running ahead of forecasts alongside mixed comments for 2023 at M Winkworth.

- A welcome H1 special dividend from Mountview Estates.

- A promising trading update from Mincon.

- A reassuring trading update from S & U.

- Unimpressive interim results plus an underwhelming conclusion to a strategic review from System1.

- Complicated full-year progress reported by Tristel.

- Nothing from Andrews Sykes and Tasty.

I have written a full review of all the shares I held during 2022 — simply click here for the complete run-down.

Full-year review

I always study my portfolio’s performance at the start of every year.

I am keen to discover where my gains and losses occurred during the previous twelve months, and check whether my portfolio decisions have become consistently good, bad or indifferent.

2022 performance

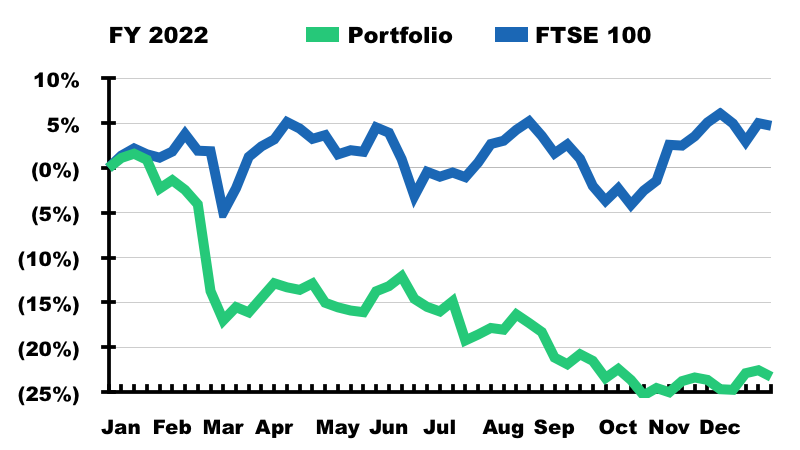

The chart below compares my portfolio’s weekly 2022 progress to that of the FTSE 100 total return index:

I finished down 23.3% versus a 4.7% gain for the UK benchmark. Last year’s performance was my worst annual result for at least 20 years and was due to:

- My largest holding performing badly: System1 started the year representing 26% of my portfolio and subsequently dived 67%, and;

- Substantial exposure to smaller UK companies: My portfolio could not sidestep the wider market sell-off caused by higher base rates, rising costs and heightened recession worries (the FTSE SmallCap index fell 16% during 2022).

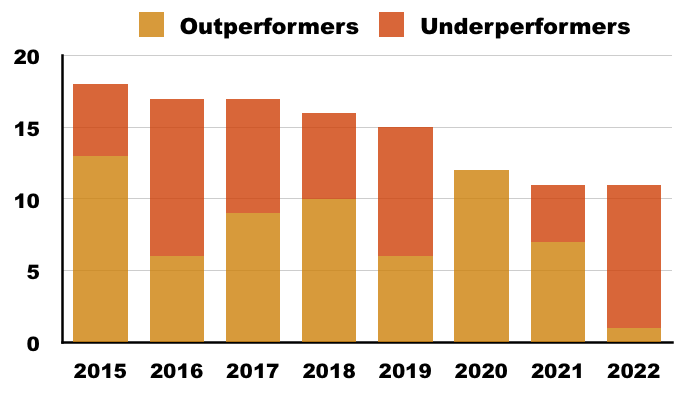

2015-2022 performance

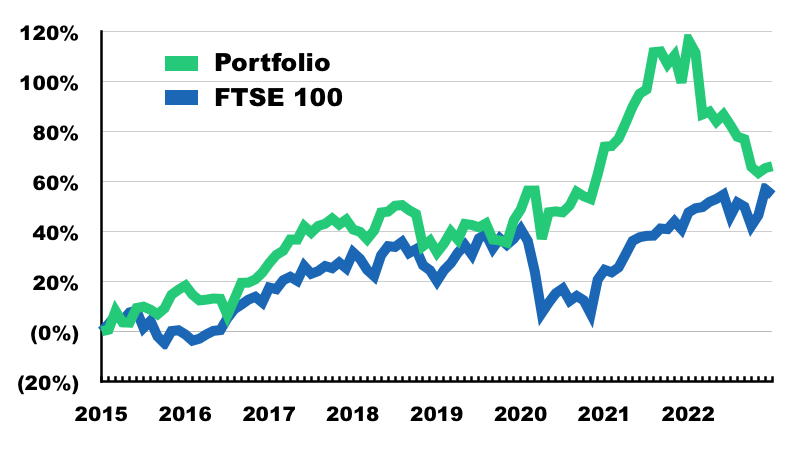

The next chart compares my portfolio’s monthly progress to that of the FTSE 100 total return index. The chart commences at 2015, which coincides with me becoming a full-time-ish investor:

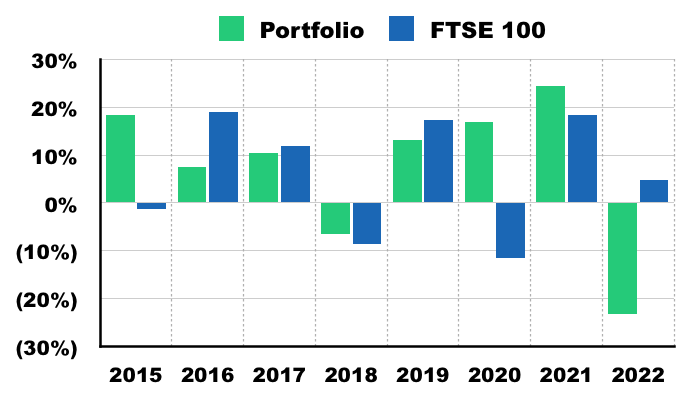

I am just about ahead of the FTSE 100 on this eight-year view — up 66% versus up 54%. But I have underperformed the UK benchmark during four of those eight years (2016, 2017, 2019 and 2022):

My poor 2022 was perhaps a follow-on from a bumper 2021, during which my portfolio gained 24.5% after my (then) largest holding (System1) surged 104%.

Investment returns and attribution analysis

Just to confirm, during 2022:

- I did not buy any new holdings;

- I topped up one holding (City of London Investment (Q4));

- I did not top-slice or sell any holdings, and;

- I left ten holdings untouched (Andrews Sykes, Bioventix, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tasty, Tristel and M Winkworth).

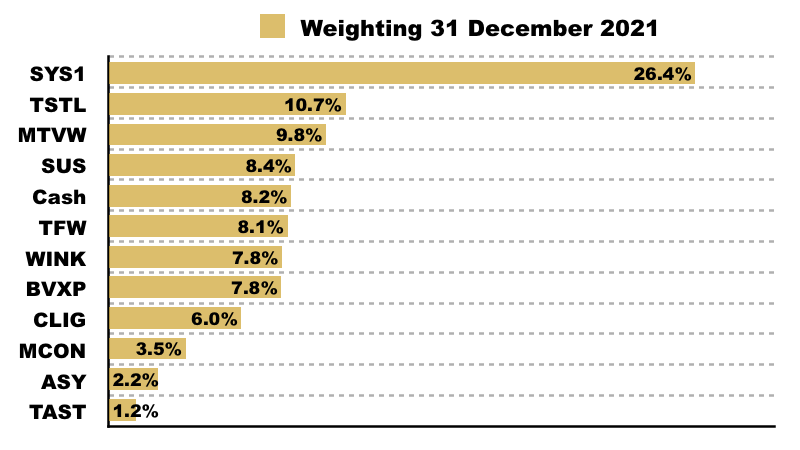

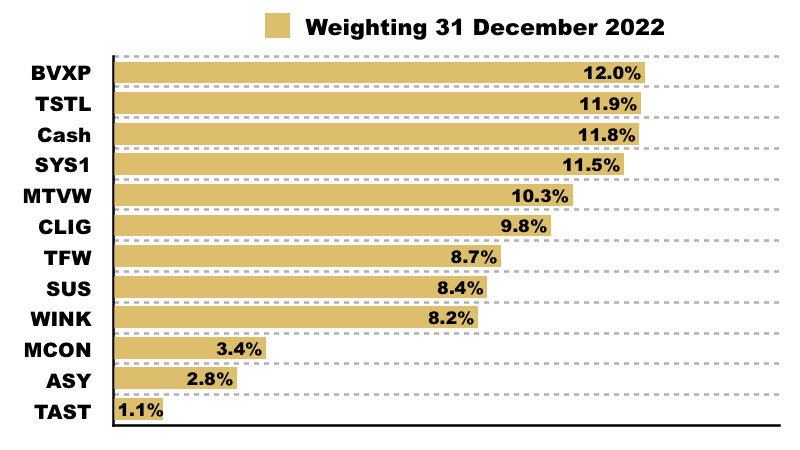

My portfolio started 2022 like this…

…and finished 2022 like this:

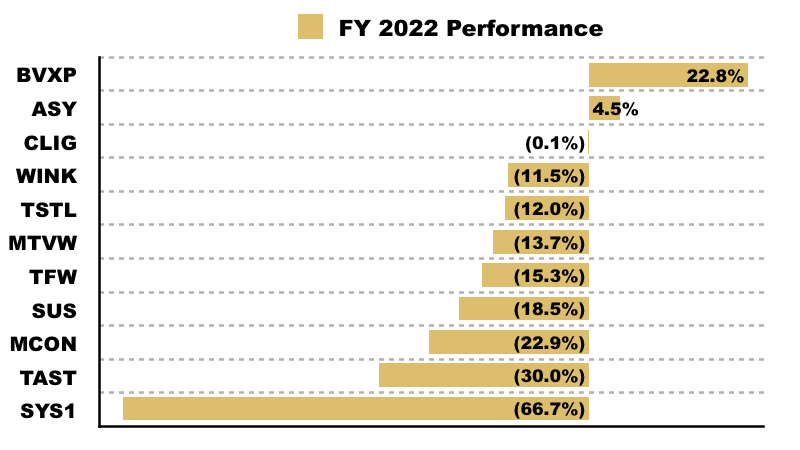

This next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding produced for me during the year:

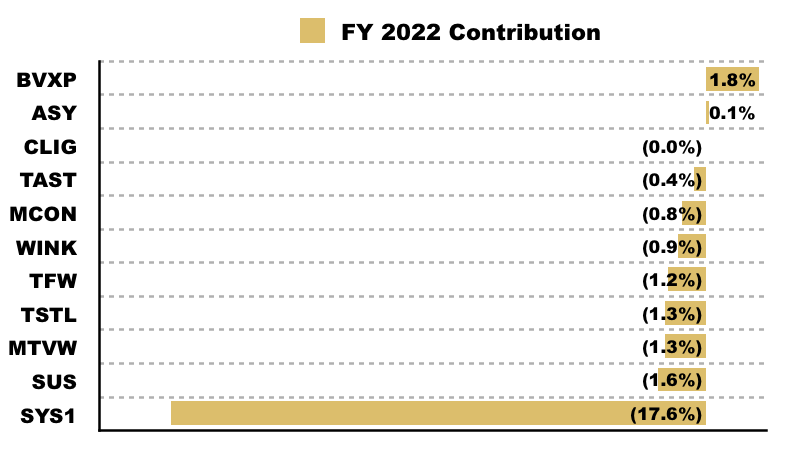

And this chart shows each holding’s contribution towards my overall 23.3% loss:

System1 crashing lower had an enormous influence on my performance. My portfolio would have lost ‘only’ 6% had I sold out of the share at the start of the year and kept the proceeds in cash.

City of London Investment delivered a neutral result for me after I bought more shares during Q4. The holding would have otherwise endured a 6% loss last year.

All my other holdings suffered during the wider small-cap sell-off, although dividends did help Andrews Sykes scrape a positive total return.

My performance was helped by the 11% average cash position held throughout the twelve months.

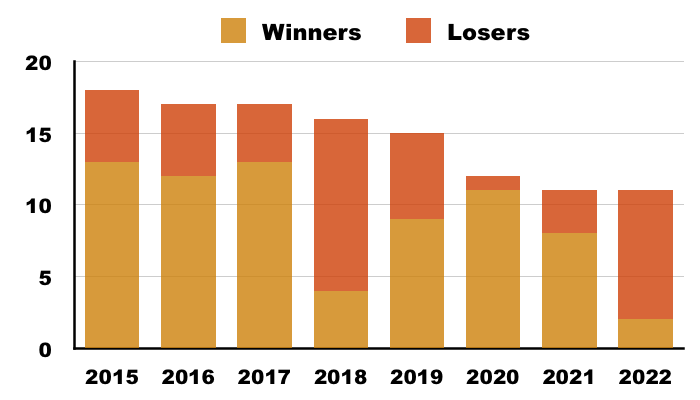

The rough year left 9 my 11 holdings recording negative total returns:

A positive year for the FTSE 100 meant 10 of my 11 shares lagged the index:

Dividends, turnover and costs

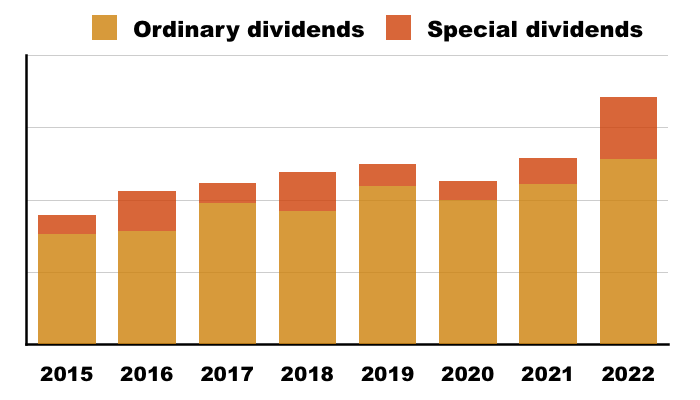

The clear highlight of my year was dividend income. Total payouts jumped a super 33% during 2022 and the income collectively added 2.3% to my performance:

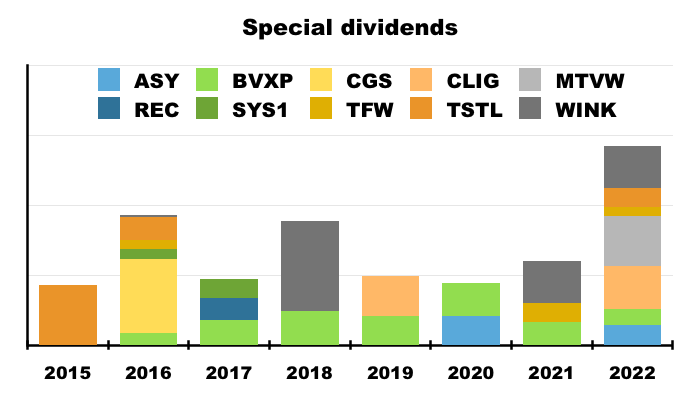

I received no less than seven special payouts — take a bow Andrews Sykes, Bioventix, City of London Investment, Mountview Estates, FW Thorpe, Tristel and M Winkworth — which last year enhanced my ordinary dividends by 33%. Specials have in fact bolstered my ordinaries by 21% since 2015:

My ordinary dividends meanwhile gained 16% last year, which I trust means the portfolio as a whole remains in good shape despite its reduced value.

Portfolio turnover remained low. I bought shares equivalent to 2.1% of my portfolio’s year-start value, and did not sell any shares.

Trading costs were kept modest. Dealing commissions, stamp duty, foreign-exchange costs and account-management fees net of interest received represented an aggregate 0.04% of my portfolio’s year-start value.

Summary

So here we go into 2023, with my current investments confirmed below:

My top eight holdings each represent at least 8% of my portfolio, and therefore all stand a good chance of influencing my 2023 result. And this year I do not start with an oversized position that could adversely dominate proceedings!

As usual I have no idea how the market will behave during the next twelve months. But I remain convinced that pinpointing smaller businesses that offer decent accounts, capable managers, respectable prospects and modest valuations remains a sensible long-term approach.

That said, this year’s portfolio review may one day prompt some strategic tweaking. I can’t ignore the encouraging income progress for example, and perhaps I may have more success tilting my stock-picking towards dividends. The companies I hold purely for capital gains — in particular System1, Tasty and Tristel — do seem more prone to suffer frustrating setbacks than others in my portfolio.

For now at least, I will gladly take any capital gains (and dividends!) to support a portfolio rebound during 2023!

Please click here to read a full review of all the shares I held during 2022.

Until next time, I wish you safe and healthy investing.

Maynard Paton

Hi Maynard

Thanks for the detailed writeup, it’s always interesting to see what you’re up to.

I don’t have any specific comments on your holdings because I don’t know any of them in detail, except S&U, which I gladly hold. I did notice in your Q4 review a brief mention of a potential tilt towards more dividend-paying stocks, which of course I think is a very good idea!

Happy new year

Hi John

Thanks for the message and happy new year! Yes, last year’s batch of special payouts and generally resilient dividend performance suggests I may find more portfolio dependability with a greater bias towards income.

Maynard

Thanks for these blogs however is a 66% gain in 8 years (only just beating the FTSE 100 which is a poor index itself) really enough to continue picking stocks?

If you just bought the S&P or the Nasdaq index you would have been up more.

Comparing to the FTSE 100 is also pretty meh because the FTSE 100 is full of old legacy companies with terrible management and poor ROIC for shareholders so it will never outperform the American indexes which have far better shareholder incentives. This year will have been an outlier for the FTSE 100 I will imagine.

Also, US tech stocks are down 60%-90% for really great companies. I find it strange that you aren’t looking at US software companies given tech’s historical dominance and current valuations.

And finally, on dividends, why do you care so much about dividends? This just means companies have poor growth prospects in the UK so they return money to shareholders and you pay a large tax on this to HMRC.

Smaller companies should be reinvesting their money in themselves to fuel growth, paying out dividends means they probably have poor growth or poor management capital allocation.

Thanks

Hi Martin

Thanks for the comment and apologies for my spam filter blocking your message!

Agreed, my portfolio returns have been mediocre since I started this blog in 2015 and I have occasionally questioned whether the effort (stocking-picking and blogging) is really worth it. I would like to get to 10 years for the blog, and after that I may just disappear with a tracker. We’ll see. Not sure I would fare any better in US tech shares to be honest.

Dividends help with total return, and some smaller companies do boast illustrious payout records principally because they have enjoyed — and continue to enjoy — good growth and good management capital-allocation decisions. Hold shares within an ISA, and there is no additional tax to pay HMRC.

Maynard

Stick at it Maynard! 8 years in the longest lowest interest environment ever and a stock bubble is not the best backdrop against which to judge a value investing strategy.

Thanks Jerry!

Hi Maynard, as ever many thanks for taking the time to share your work which I find really informative.

I wondered if the losses incurred by System 1 have given you reason to think about maximum portfolio positions? I certainly couldn’t sleep at night with that much of my portfolio in one stock which would lead to me top slicing following growth. Of course the downside can be missing out on further growth but reduces the risk of potential catastrophe!

My personal share trading portfolio includes about 20 stocks so my natural position size would be about 5%. This naturally fluctuates between 2.5% and 7.5% depending on conviction, building into positions gradually etc. but certainly once above 10% a position would get extra attention due to the potential risk of over-concentration. One thing I need to get better at is considering my exposure to individual shares where I hold within my share account and they will also feature heavily in trackers, ITs etc. A good example here is BAE following its good run last year.

Best wishes for 2023 both personally and financially!

Hi Mike

Thanks for the message. Not sure SYS1 has given me reason to think about position size, more a case of thinking more about possible business risks. The transition from consultancy to data has revealed problems with the old consultancy side, which may explain why the transition was started in the first place, and I should have considered this possible setback more. At no point did I ever think I should be top slicing. My top-slicing of LSE, TSTL and a few others — and not letting those big winners run — provide some experience of losing out when I do top slice. Top-slice decisions are never easy!

Maynard