09 April 2023

By Maynard Paton

Happy Easter! I trust your shares have enjoyed a positive start to the year following the rough conditions of 2022.

A summary of my portfolio’s first quarter:

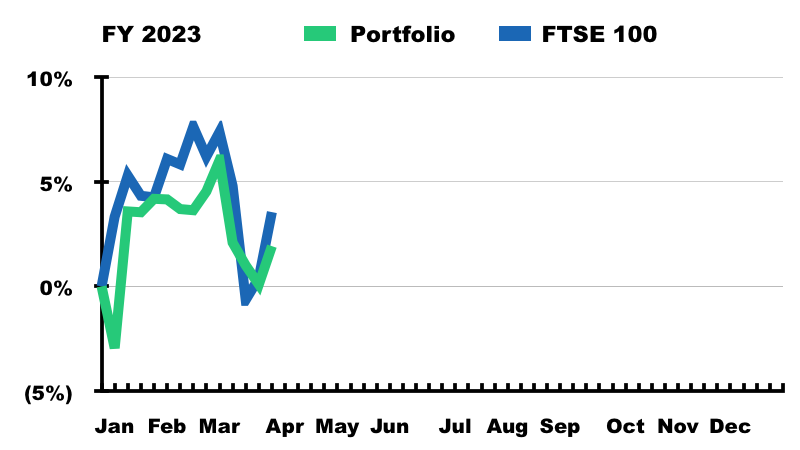

- Q1 return: +1.9% gain* (FTSE 100: +3.6% gain).

- Q1 trades: None.

- Q1 winners/losers: 6 winners vs 4 losers (1 unchanged).

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

I will gladly take a 1.9% gain for this Q1 after the 23% mauling I suffered last year. My portfolio now requires ‘only’ a further 28% advance to revisit its all-time high from December 2021.

Company RNSs were generally very acceptable during the quarter. Dividends were held or raised and thankfully no profit warnings emerged. As always I am hopeful a mix of respectable competitive positions, capable managers and asset-rich balance sheets will steer my portfolio through whatever the markets may bring.

Q2 could witness greater portfolio action. Shareholders of System1 could appoint a new executive chairman who has very ambitious plans for a trade-sale exit, while Tristel will announce whether one of its disinfectants has (finally!) gained regulatory approval within the United States. Both events could lead to favourable longer-term progress at those two holdings.

I have summarised below what happened within my portfolio during January, February and March. (Please click here to read all of my previous quarterly round-ups). I will then outline the ten lessons I learned (or re-learned!) after attending three small-cap AGMs.

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, Tasty, FW Thorpe, Tristel and M Winkworth.

Q1 share trades

None.

Q1 portfolio news

As usual I have kept watch on all of my holdings. The Q1 developments are summarised below:

- A 19% H1 dividend lift and upbeat R&D remarks from Bioventix.

- Unchanged half-year funds under management and a standstill payout at City of London Investment.

- FY 2022 profit up 9% and talk of “strong” order books at Mincon.

- Net asset value up 9% and commentary supporting the country’s “free enterprise system” at S & U.

- A notice of a requisitioned general meeting at System1.

- Final results that exposed inherent cost flaws at Tasty (NOTE: formal blog coverage now ceased).

- Acquisition-boosted adjusted six-month profit up 34% and high energy costs “stimulating” H2 activity at FW Thorpe.

- Adjusted first-half profit rebounding 41% and confirmation of an FDA regulatory verdict by June from Tristel.

- News of full-year profit being “modestly” ahead of expectations at M Winkworth.

- Nothing of significance from Andrews Sykes and Mountview Estates.

Q1 portfolio returns

The chart below compares my portfolio’s weekly 2023 progress to that of the FTSE 100 total return index:

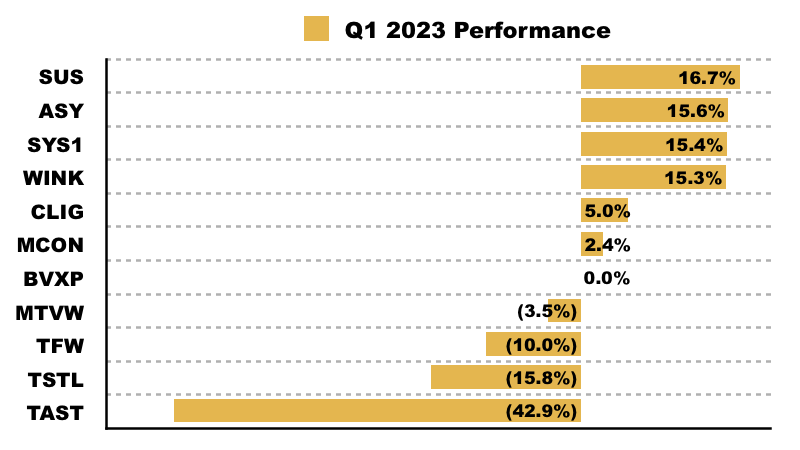

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me year to date:

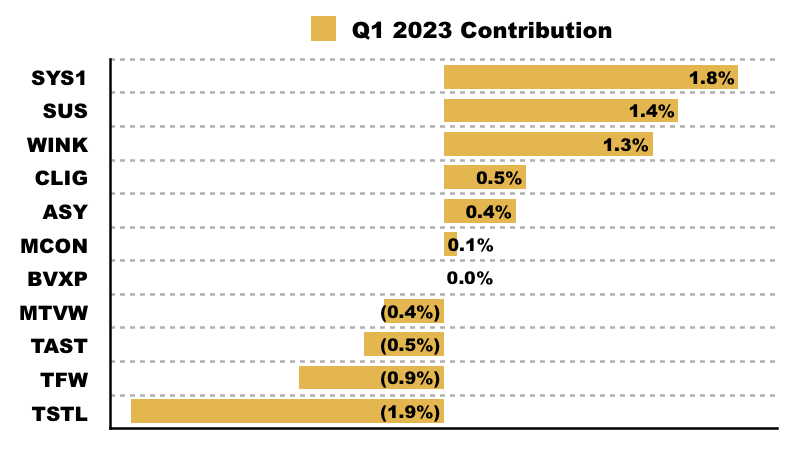

This chart shows each holding’s contribution towards my overall 1.9% gain:

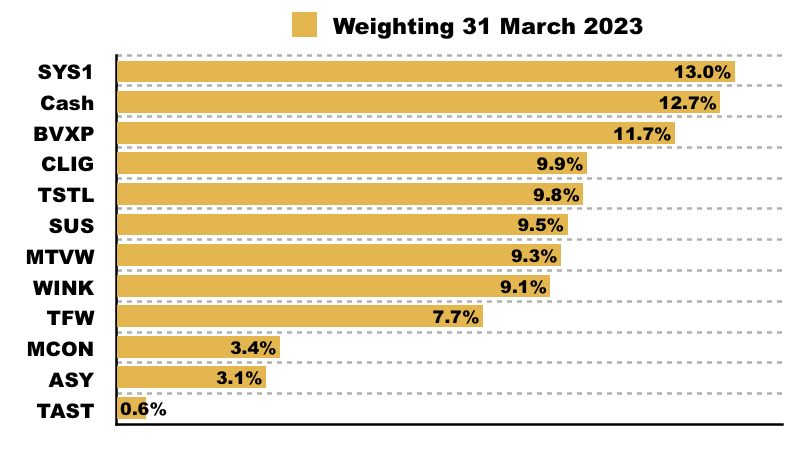

And this chart shows my portfolio’s holdings and their weightings at the end of Q1:

10 lessons from 3 small-cap AGMs

Last year I attended the AGMs of three of my holdings: Bioventix, City of London Investment and System1. I asked a variety of questions at each meeting and then discussed the answers during these podcasts:

- Bioventix: AGM podcast (and AGM notes)

- City of London Investment: AGM podcast (and AGM notes)

- System1: AGM podcast (and AGM video)

Attending those three AGMs reinforced my view that such meetings can be very valuable to private investors. I therefore distilled what I learned (or re-learned!) into the ten lessons below, which I trust can help you get the most from any AGMs you attend.

1) Companies can conduct AGMs how they like

I am pretty sure AGMs have no strict rules. Just so long as an AGM is convened with sufficient notice and the required quorum turns up, quoted companies can then manage the meeting anyway they like.

For example, System1 started its AGM by announcing the voting results of each resolution and then followed up with a Q&A.

City of London Investment in contrast led with the Q&A and then asked attendees to complete their voting cards. The resolutions were not formally put to the meeting and the voting results were not mentioned.

Bioventix meanwhile led with the voting results that commendably included inviting questions on each resolution. Then followed a ten-minute statement from the chief executive that then made way for the Q&A.

I attended one AGM during which the chairman started by reading out all of the voting resolutions… and then promptly stood up and left the room. The formal business of that meeting therefore finished, leaving shareholders no opportunity to direct questions to the whole board.

Over time I have learned companies can conduct AGMs as they see fit, especially to reduce interference from awkward shareholders. Pot luck may decide whether you are told about the voting results, enjoy a Q&A and hear a statement from the boss.

For the record, section 319A of the Companies Act states:

“At a general meeting of a traded company, the company must cause to be answered any question relating to the business being dealt with at the meeting put by a member attending the meeting.”

No such answer need be given:

(a) if to do so would:

(i) interfere unduly with the preparation for the meeting, or

(ii) involve the disclosure of confidential information;

(b) if the answer has already been given on a website in the form of an answer to a question; or

(c) if it is undesirable in the interests of the company or the good order of the meeting that the question be answered.

2) Listen to the resolutions and voting results!

I was caught out during System1‘s AGM and the group’s voting results. I was too busy preparing my questions and did not instantly clock the major protest votes being announced against certain non-execs.

System1 had not suffered major protest votes before, so I had not really anticipated a revolt.

My first question ought to have asked why the protest votes had occurred, as certain larger shareholders were clearly unhappy about something. I now pay greater attention to the voting results at every AGM.

Often protest votes concern director remuneration, so asking about the high proportion of ‘against’ votes on pay could be an elegant way to start probing what is always a tricky AGM subject for many boardrooms.

3) You may learn about protest votes that other investors do not

Bioventix suffered protest votes at its AGM, but the voting results were not published and therefore only meeting attendees were informed of the polling.

At least Bioventix‘s chief executive explained during his ten-minute statement why the protest votes were lodged (a lack of board ‘diversity’ was cited).

Similar to conducting an AGM, companies appear free to do what they wish with their AGM voting results. Either publish them through the RNS, just pop them on the website or in Bioventix’s case, not bother with either.

If your company holds an AGM but the polling results are not made public, I would enquire why. Maybe embarrassing protest votes are being kept under wraps.

4) Every meeting presents an opportunity to discover new information

The primary reason I attend AGMs is to discover information beyond the annual report. Useful snippets can always be picked up — especially during the informal chats with directors before and after the meeting.

For example, I learnt before the Bioventix meeting started that the company’s industrial-pollution urine test was “not worth putting on my spreadsheet” (eating a barbecued sausage will apparently trigger a ‘false-positive’ reading). That remark allowed me to skip the subject in the Q&A and focus on more pressing matters.

At the City of London Investment meeting, I speculatively asked 36% shareholder and non-exec George Karpus what his future plans were given the annual report said the following:

“George Karpus will continue to serve on the Board for the 2022-2023 financial year and we will provide an update prior to next year’s AGM regarding his future plans.“

I expected a ‘wait and see’ response, but was surprised he confirmed what would actually happen — he will leave the board before the next AGM. Now I do not have to wait for the official announcement to start thinking about how the group will perform without its largest investor on the board.

I should add that some of the snippets I learn from AGMs are not published on my blog nor mentioned in my podcasts.

5) Ask your important questions first

Few shareholders turn up at AGMs, and I suspect many boards assume nobody will attend and so pencil in only ten minutes at most for the meeting. My advice is to therefore ask your questions sooner rather than later before the board makes its excuses.

Alternatively, if the AGM is busy and suffering a lengthy Q&A, the board may call time before you have the chance to speak. The Bioventix Q&A lasted 45 minutes and while the directors were happy to answer every question, the meeting did overrun the allocated time at the venue.

Bear in mind the board may curtail the formal Q&A if the lines of enquiry become too probing. The Q&A at System1‘s AGM was curtailed by the chairman (watch here) after just a handful of questions.

Boards should in theory be ready to answer all shareholder topics. But given companies can conduct AGMs however they want, best in my view to get the burning issues raised at the start.

6) Be prepared with questions because you cannot rely on somebody else

Even if other shareholders do turn up at the AGM, you have no guarantee they will ask suitable questions or even say anything at all. Therefore make sure you do some homework first and bring with you a list of subjects to discuss.

I was one of two private investors that attended the City of London Investment AGM. The Q&A lasted 30 minutes and I asked all the questions and the other investor said nothing.

I am not sure what the other private investor would have done if I had not attended. Nor am I sure what would have happened if I had not prepared any questions; probably a short awkward silence followed by a sudden — and disappointing — conclusion to the meeting.

To be frank, I can’t imagine ever going to an AGM and then not bothering to ask a question.

7) Pay attention to other shareholders’ questions

I often think only about my questions during an AGM and do not pay enough attention to what other shareholders are asking.

The Bioventix AGM was attended by two very informed shareholders (not me!), both of whom asked their questions towards the end of the meeting.

Only when I studied my notes after the AGM did I realise how perceptive their topics were. One question for example concerned a forthcoming article in a medical journal, which did not seem too important at the time — but did prompt me to look at the article after its publication.

The article confirmed very promising progress with Bioventix‘s R&D for its Alzheimer’s blood-test antibody and (in retrospect!) gave attendees four months’ head start on the encouraging commentary published within the company’s H1 statement.

I now think back to the Bioventix meeting and wished I had asked fewer questions and encouraged the very informed shareholders to ask more.

8) Management may read your blog

Not a problem for most private investors, but writing an investment blog gives advantages and disadvantages to your AGM attendance.

The City of London Investment AGM provides a good example. Half-way through the meeting I gradually realised the directors had all read my blog about the group’s annual results. The board therefore knew the questions I was going to ask, which on reflection probably explains the eloquent answers and readiness to undertake a 30-minute Q&A.

The aforementioned Mr Karpus even complimented my write-up: “You made some good points in your thesis. You were spot on about a couple of things.” (I am not sure that feeling was shared with every director in the room!)

Mind you, knowing you have a website may cause some directors to not talk as openly as they otherwise would — although I can never be sure if that has ever been the case for me. Light-hearted board comments at the Bioventix AGM included something along the lines of “We must be careful of what we say, as it may appear on a blog“.

9) You can pick up clues from the board’s body language

Company bosses undertake many presentations and ought to be very comfortable handling City analyst questions.

But nothing is ever certain at an AGM. The meeting occurs only once a year, includes all the board members plus random shareholders turning up with their obscure/unseemly/awkward topics.

You can therefore obtain a good sense of the directors’ attitude to investors — and with each other! — just by observing what happens, how the meeting is handled and the signs of discomfort from those on the other side of the table.

The System1 AGM provided a good example. The formal Q&A was cut short by the chairman… and the (then) chief executive closed the meeting by revealing the board had arranged a post-AGM farewell lunch for the chairman.

As the only outside shareholder present among several senior employees — who seemed to have attended the AGM just for the lunch — I did feel I was interrupting a works social event…

…which gave the impression shareholders and the AGM were not the board’s priority that day.

Sometimes the body-language clues are obvious.

I attended one AGM where the company was led by two co-chief executives, and one co-chief physically moved the other co-chief aside to talk to me (“You’re that blogger!“). The episode told me which of the two co-chiefs was in charge.

Another AGM involved a barrage of questions to the board, during which the chief executive just sat with his arms folded looking down at the table and not saying a word.

And there was also that aforementioned chairman who just stood up and left the meeting once he had read out the resolutions.

10) Do go to AGMs!

I recognise getting to AGMs is difficult for many private investors. The meetings are often held in central London during a weekday morning, and the effort-to-reward ratio of attending is never clear until after the event.

But I can’t say I have ever regretted attending an AGM — and certainly the meetings held by Bioventix, City of London Investment and System1 were each enlightening for very different reasons.

The upside for shareholders is discovering more about the business, and how much you learn correlates to your pre-meeting homework and the questions you then ask. The downside is the possibility of a long journey to visit an uncooperative board, but even that will still tell you more about the directors than any set of accounts.

A real danger to investors is conventional AGMs disappearing. As I have mentioned, AGM rules do seem very makeshift and a few companies have tried it on with virtual AGMs. My podcast about Telecom Plus noted the group failing to gain shareholder approval for Zoom-only meetings.

Downsides to online-only AGMs include management ‘overlooking’ difficult questions in the Q&A inbox and body-language clues being hard to spot on the broadcast.

If shareholders don’t bother turning up at AGMs, quoted companies may eventually call to scrap the physical meetings… and all of us may then have one less option to garner useful information to get ahead of the market!

Until next time, I wish you safe and healthy investing.

Maynard Paton

Good points. I have been considering attending my first AGM – Serco – at month end. It is not far from where I live but I don’t want to waste half a day by listening to a chairman rubber stamp resolutions. I asked for further info on the format from their IR company, who turned to Infiniti, who don’t know – but I shall give it a bash.

I might try and go to Bioventix next time as presumably they hold their AGM somewhere near Farnham in Surrey?

Hi Stephen

Thanks for the comment. To a certain extent an AGM is what you make it. Go armed with a few relevant questions and you may hear some useful answers. I would like to think a reasonable-sized company such as Serco would host a ‘proper’ meeting and not indulge in some of the unwelcome practices that a few AIM small-caps adopt. The Bioventix AGM was held at Farnham Castle on the outskirts of the town.

Maynard