01 July 2021

By Maynard Paton

Happy Thursday! I trust your shares are thriving and that you still find my blog useful.

A summary of my portfolio’s progress:

- Q2 change: +7:4%*

- Q2 trades: System1 and M Winkworth

- YTD change: +13.2%*

- YTD winners/losers: 9 winners vs 2 losers

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees and paid dividends)

I am pleased the portfolio gains recorded during Q1 were extended during Q2. Recent RNSs from my portfolio have been mostly encouraging, and I anticipate boardrooms will remain optimistic as the pandemic subsides and social restrictions ease.

I topped up on two shares during the quarter: System1 and M Winkworth. I talked about both purchases during this Capital Employed podcast. I remain hopeful other buying opportunities will arise and allow my 7% cash position to be put to good use. I am keen to keep my portfolio relatively concentrated, so any new idea may have to replace an existing holding.

I have summarised below what happened within my portfolio during April, May and June. (Please click here to read all of my previous quarterly round-ups). I will then explain what I have learned from holding five shares for ten years.

Contents

- Disclosure

- Q2 share trades

- Q2 portfolio news

- Q2 portfolio returns

- 5 lessons from owning 5 shares for 10 years

Disclosure

Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S&U, System1, Tasty, FW Thorpe, Tristel and M Winkworth. This blog post contains SharePad affiliate links.

Q2 share trades

System1

I increased my System1 holding by 40% at 242p including all costs.

The advert-testing specialist issued an encouraging trading statement during April that confirmed the group’s remarkable H1 profit recovery had continued throughout H2. Of particular note was the group’s data products representing 15% of Q4 sales compared to just 1% during H1. The business finally appears to be transitioning from bespoke consultancy work to a more reliable data-sales operation. My sums suggested a potential P/E of 8 with net cash representing 20% of the market cap. Read more.

M Winkworth

I increased my M Winkworth holding by 10% at 178p including all costs.

The estate-agency franchisor unveiled promising 2020 figures during April, which were underpinned by a record quarterly dividend for the first quarter of 2021. Winkworth’s AGM statement then reiterated bumper current trading due to the stamp-duty holiday, with income from property sales “almost doubling on Q1 2020“. Winkworth continues to outperform London rival Foxtons and future market-share gains could support growth even if property activity quietens. The P/E looks to be approximately 11-14x. Read more.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Q2 portfolio news

The main Q2 developments at my shares are listed below:

- Second-half profit down a disappointing 37% at Andrews Sykes;

- Stable funds under management at City of London Investment;

- Promising results, a record quarterly dividend and a very encouraging AGM statement at M Winkworth;

- A promising update and AGM questions commendably answered at Mincon;

- Full-year net asset value up 4% and the dividend up 6% at Mountview Estates;

- Notable board changes and profit running “ahead of group projections” at S&U;

- A remarkable profit turnaround continuing at System1;

- Predictably awful figures but talk of “robust” summer trading at Tasty;

- Sales of medical-device disinfectants falling short at Tristel, and;

- Nothing from Bioventix and FW Thorpe.

Q2 portfolio returns

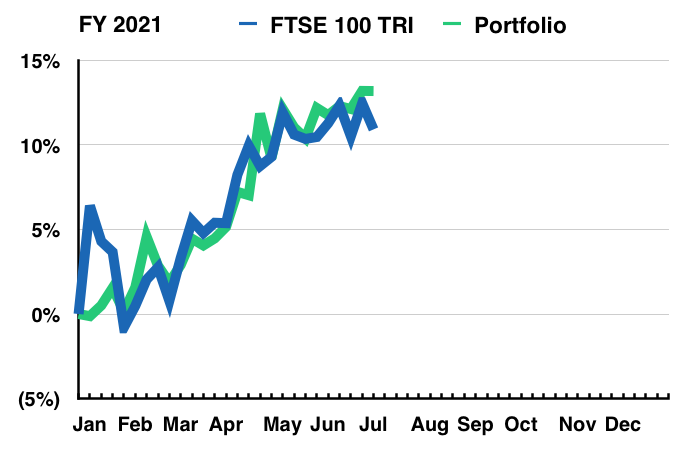

The chart below compares my portfolio’s weekly 2021 progress (in green) to that of the FTSE 100 total return index (in blue):

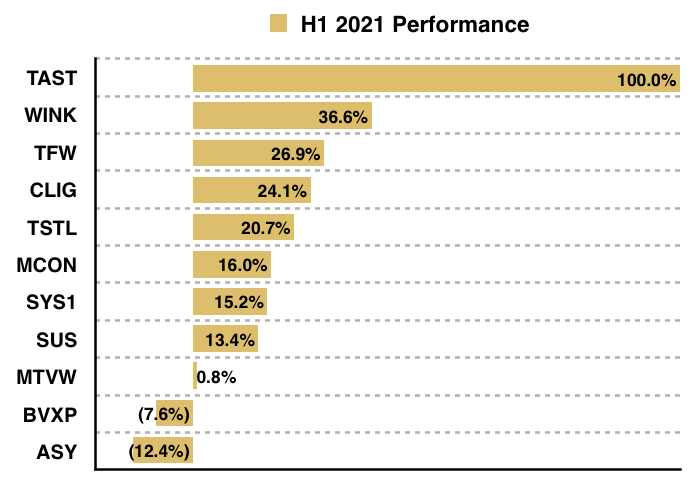

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me year to date:

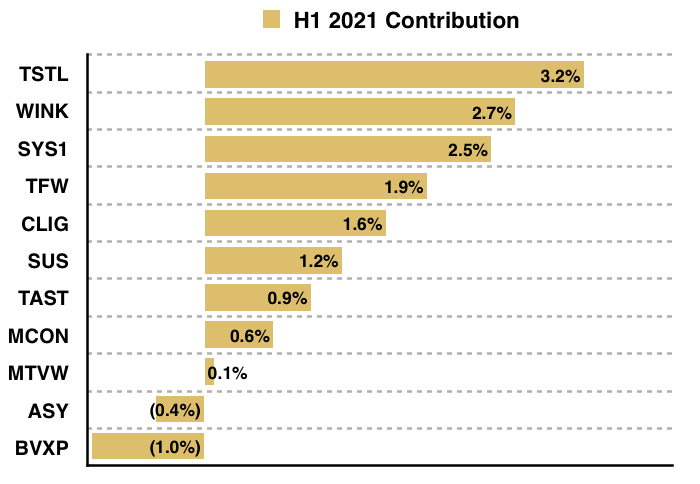

This chart shows each holding’s contribution towards my overall 13.2% gain:

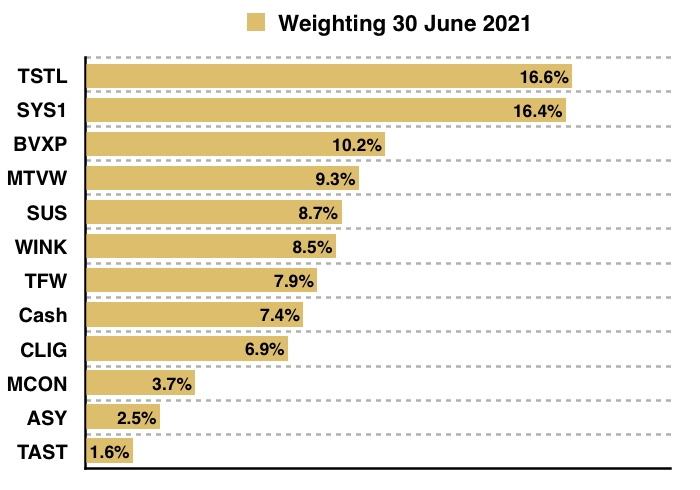

And this chart shows my portfolio’s holdings and their weightings at the end of Q2:

5 Lessons From Owning 5 Shares For 10 Years

This summer marks ten years since I resumed buying individual shares following a stint holding mostly cash (a story explained here). Five of the shares I bought around that time remain in my portfolio today, and the table below lists those five companies, when I first invested and the initial price I paid:

| Holding | First bought | Initial price paid (p) |

| City of London Inv (CLIG) | August 2011 | 355 |

| Mountview Estates (MTVW) | November 2011 | 4,164 |

| Tasty (TAST) | December 2011 | 49 |

| FW Thorpe (TFW) | October 2010 | 68 |

| M Winkworth (WINK) | June 2011 | 89 |

(Click on the company name to read an archive of my company posts. Click on the date of my first purchase to read my initial buy report.)

Ten years is a long time to hold any investment and I thought I would share what I have learnt:

1) Holding for 10 years does not guarantee spectacular returns

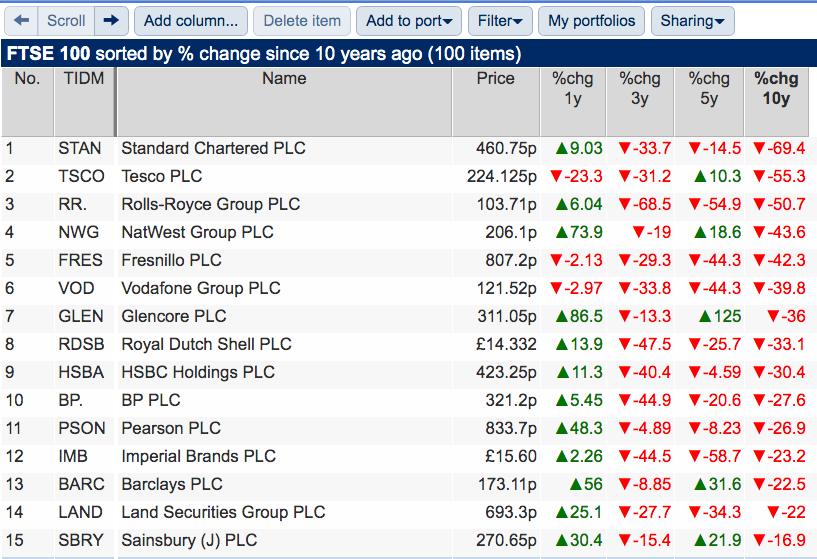

Just ask anyone who bought into Shell, Vodafone, HSBC or Tesco a decade ago. Those household names have seen their share prices drop by 30% or more since June 2011…

…and if such ‘safe’ blue chips can lose money over ten years, then what chance did I have investing in smaller companies?

The aggregate returns from my five shares (based on my initial purchases) have thankfully outperformed the likes of Shell, but the overall performance could have been better.

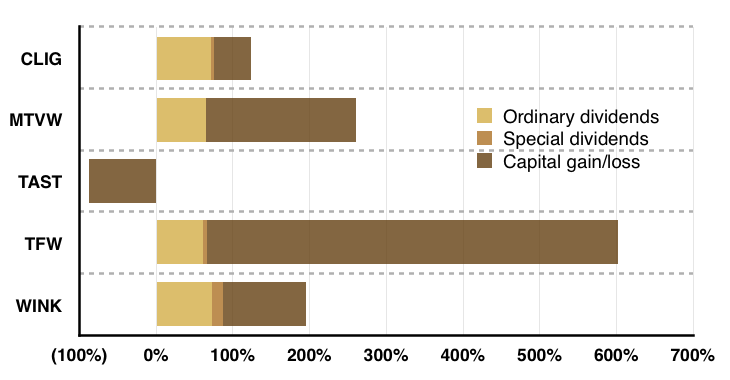

Individual returns ranged from +602% to -88% with an average of +219% that equates to an annualised 12.3%:

If you exclude my Tasty disaster, the 10-year compound rate improves to 14.7%.

I am ideally seeking 15% annualised returns, which over ten years equates to a four-bagger — and only FW Thorpe of the five shares has achieved four-bagger status. Dividends helped the cause, especially with City of London Investment, but capital gains were generally a little lacking.

For perspective, the FTSE 100 total return index (i.e. with dividends reinvested) has climbed 73% during the ten years. I recognise funds such as Fundsmith, up 455%, and a Nasdaq ETF, up 677%, have trounced the FTSE (and my portfolio) since 2011.

Quality UK investment discussion at Quidisq. Visit forum.

2) Share prices do not go up in a straight line

You may think big ten-year winners would show nice smooth journeys to fantastic returns as all the share-price ups and downs even out. Not so.

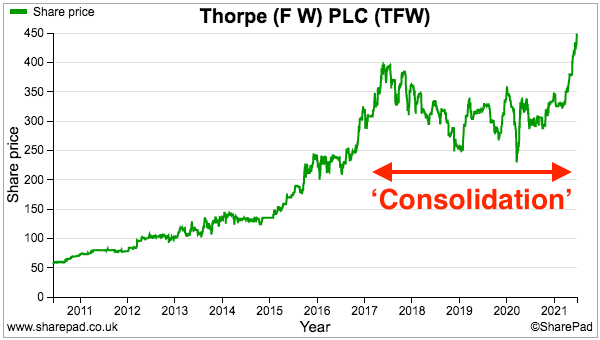

Take FW Thorpe. Its share price rallied well between 2011 and 2017, only then to ‘consolidate’ between 2017 and 2021:

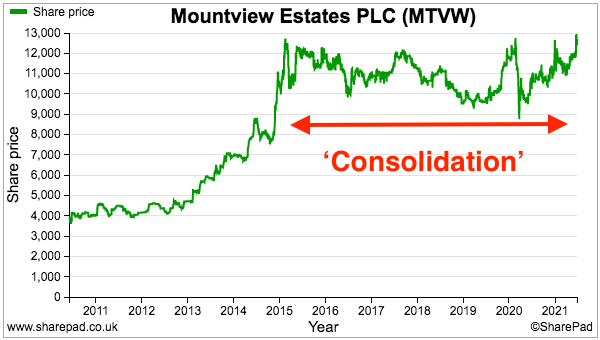

A similar consolidation story happened at Mountview Estates:

Quite often a share price runs ahead of the company’s performance and then stagnates as the company catches up. Trouble is you never know when the consolidation period will start and when it will end. Investing for ten years undoubtedly involves watching prices tread water for long periods.

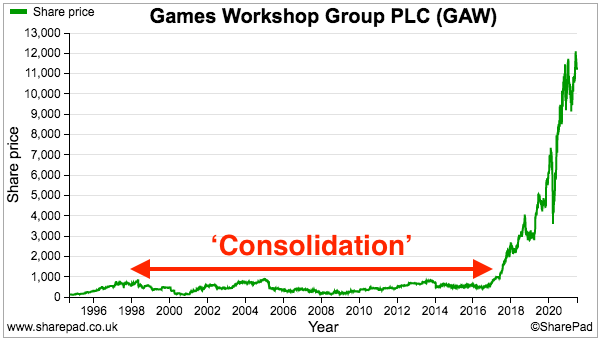

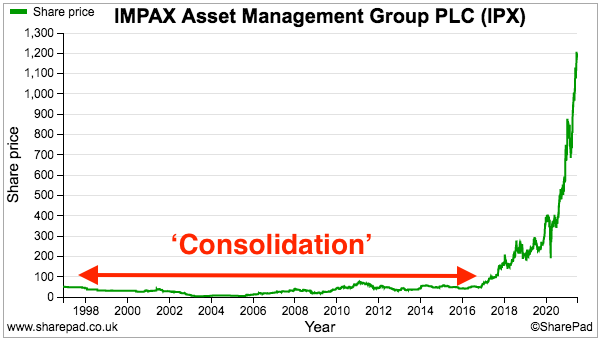

Note how wonder-stocks such as Games Workshop and Impax Asset Management effectively went nowhere for years before going vertical:

Hold a promising business for long enough, and it too may undergo a Games Workshop-type take off. At least that is what I hope happens with my shares during the next ten years!

3) Some companies may be unsuitable to own for 10 years

You can’t just sit back and hope time will allow a poor business to succeed. Certain companies simply lack the appropriate competitive ‘moat’ or a large enough marketplace to outperform over a decade. Just look at Tasty’s chart below:

Steadily up then straight down. Had I sold my entire Tasty holding at close to 200p I would have captured my ten-year target four-bagger after just four years.

Instead I held on to most of my Tasty shares while thinking about the long term…

…rather than acknowledging greater competition and rising costs had shattered the group’s growth story and made many of its restaurants unviable.

Determining which companies can avoid such disruption is not easy.

To date City of London Investment (fund management), Mountview Estates (property trading), FW Thorpe (commercial lighting) and M Winkworth (estate agency) have been able to sidestep major trouble in part due to stable and sensible management that have kept on top of sector developments.

New LED lighting systems and the impressive SmartScan product have in particular ensured FW Thorpe remains competitive. But I am mindful Tasty boasted very experienced directors who could not prevent it from being pushed to the brink.

4) Spotting better buying opportunities may become easier

You may be able to make better investment decisions with a share you have held for long periods. After all you are more likely to monitor newsflow at a portfolio holding — and then develop a greater knowledge of the business — than anyone completely fresh to the company.

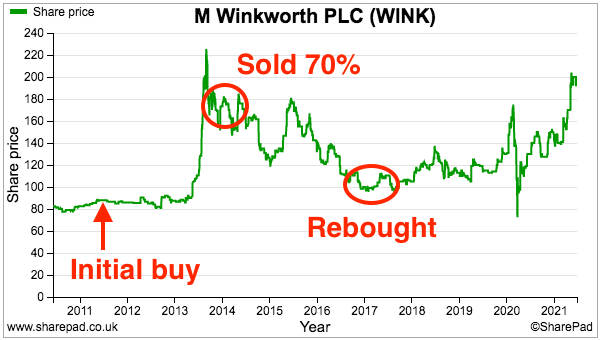

M Winkworth provides a good example. I first bought during 2011 at 89p but, following a sudden share-price surge, sold 70% of my holding during 2013/14 at prices as high as 193p:

But keeping some Winkworth shares ensured I still monitored the company and, sure enough, I bought a lot more shares throughout 2016/17 at prices between 100p to 133p. I am not sure I would have noticed the opportunity had I sold out completely. The price recently touched 200p.

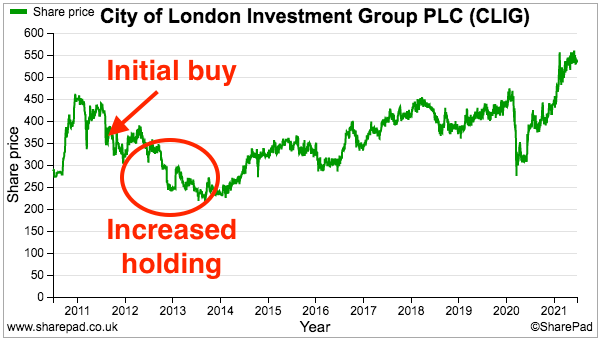

City of London Investment is another example where I developed greater conviction. My 355p initial buy stated in the earlier table is actually the highest I paid for this share. During 2012 and 2013 I averaged down, buying as low was 219p, as I learnt more about the business. The price trades currently at 524p:

Which is best for stock-screening: Stockopedia or SharePad? See my verdict.

5) There will always be opportunities to enjoy great winners

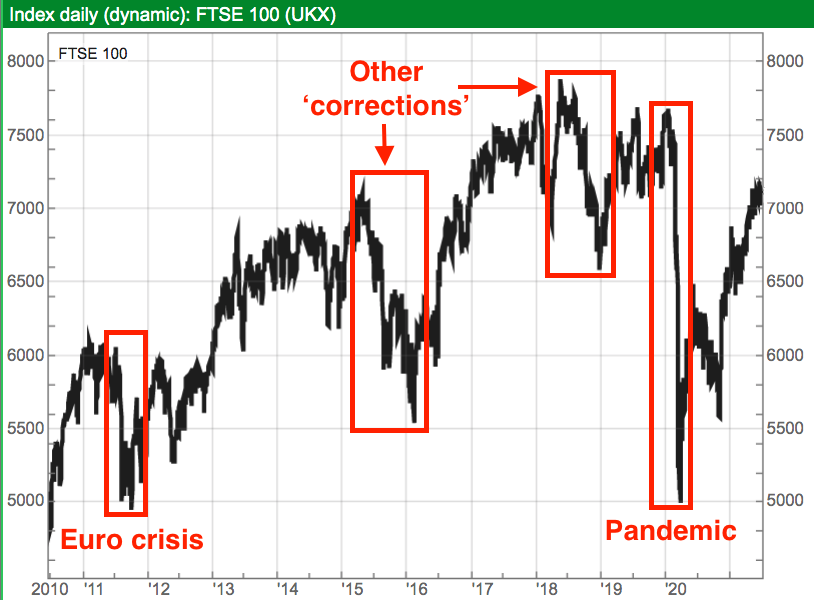

Owning a share for ten years gives you a greater perspective on current market worries.

A decade ago the global economy was recovering from the 2008 banking crash and investors were then concerned about the ‘whatever it takes’ policies of central banks. The eurozone crisis was in full swing and all the talk was of debt ceilings, fiscal cliffs, vanishing triple-A ratings and Greece going bust.

The FTSE 100 actually plunged from 6,000 to 5,000 — or 17% — during July and August of 2011, and would have given stock-pickers every excuse not to invest until ‘greater certainty emerged’:

In fact, had you known back in 2011 that the next ten years would witness:

- The UK leaving the EU;

- Donald Trump becoming US president, and;

- A pandemic causing the UK economy to shrink by up to 20%…

…you may well have ditched all your shares and headed straight for the bunker.

And yet through all the shocks and upheavals of the last decade, lots of companies continued to prosper and many shares went on to multi-bag. This perhaps is the most important lesson of holding shares for the last ten years: no matter what market conditions are like, there will always be opportunities to enjoy great winners.

Fingers crossed my portfolio contains some great winners between now and 2031!

Until next time, I wish you safe and healthy investing.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Thank you for the interesting and honest write particularly on the stocks you have held for 10 years.

I have read much recently on “coffee can investing” and while I consider myself a long term investor I looked into what happens if you hold for 20 years and for me the results are not encouraging. Using Sharepad to screen, there are only 12 companies that have delivered 20% per annum over 20 years, 44 greater than 15% and 157 companies greater than 10%. (As of today)

The screen would tend to indicate that one is better trying to find companies that are going to out perform over 5 years or so and then sell and move on. As the odds are against the company continuing to deliver a 20% pa return or that is my take on it anyway.

You can see more on my post today on my web site.

Kind regards

Michael

Hi Michael

Thanks for the comment. I think you are probably right with the 20-year stats and conclusion of aiming for 5-year outperformance. The fact that my biggest 10-year winner TFW ‘consolidated’ for 4 of the 10 years underlines your point. Mind you, it is psychologically hard to sell out completely of a good company and move on (at least for me). I sold some of my TFW at 238p thinking I was clever, but the shares have powered on since!

The general consensus from the feedback after I wrote about 10-baggers last year was pretty much the same (i.e. wonderful returns are very rare):

https://maynardpaton.com/2020/06/30/q2-2020-10-lessons-from-a-10-bagger/#10-lessons-from-10-bagger

Sorry to read about your recent portfolio woes:

https://investing4value.wordpress.com/2021/07/01/quarterly-review-q2-2021/

Looking at your history of returns, with notable falls in 2008, 2011, 2014 and 2018 all interspersed with hefty gains, I would say the last 18 months should not worry you (as long as you have applied a consistent investment approach over that time!) You just can’t outperform all of the time, unless you are Terry Smith or an anonymous FinTwit guru!

Maynard

Hi Maynard

Thanks for the five lessons. I’ve definitely noticed that holding companies over years allows you to build up a much more nuanced understanding of how they work.

It’s also a good way to appreciate the pace at which meaningful things happen, which typically takes years rather than a quarter or two.

John

Hi John

Thanks for the comment. Yes, I have concluded that I am more likely to find good, reliable buying opportunities within a small group of monitored/familiar shares, than I am by always looking at new companies (although you do have to refresh the familiar shares every so often with new faces.) Existing holders should have acquired a company ‘knowledge’ advantage over new buyers I feel.

Maynard

Your head can read about over optimistic predictions and how things are obvious in hindsight but until you live it, you don’t really understand it.

This post is as close a lesson in understanding that as you are likely to get without living it. Thanks for sharing.

I would promote the benefits of number 4 further from a personal perspective. Something changes subconsciously when you own a stock rather than have it on a watch list or research it. The info I see and thread together seems to go up 10 fold.

Great Post. Thanks.